Most revenue transactions are taxable (and therefore increase taxable income) in the current period or in a future period. As well, most expense transactions are deductible for tax purposes (and therefore decrease taxable income) in the current period or in a future period. Under IFRS's temporary difference approach, and ASPE's future income taxes method, interperiod tax allocation is applied when a revenue or expense item is reported on the income statement for financial reporting purposes in one period, but included in taxable income for tax purposes in a different period. Interperiod tax allocation refers to recognition of tax effects in the accounting period when the related transactions or events are recognized for financial reporting purposes, usually resulting in recognition of a deferred (or future income) tax liability and/or a deferred (or future income) tax asset on the statement of financial position. After proper interperiod tax allocation, the income tax consequences of revenues and expenses are reflected on the income statement in the same year that the related revenues and expenses are reported on the income statement, regardless of whether or not those revenues and expenses affect the same year's current income tax payable.

STUDY STEPS

Understanding the Nature of Income Taxes

Accounting income versus taxable income

Income tax payable is calculated based on income as defined by the Income Tax Act, or taxable income. Accounting for income taxes is complicated because income as defined by GAAP (ASPE or IFRS), or accounting income, usually does not equal taxable income. Accounting income is calculated according to ASPE or IFRS accounting principles or standards to provide information that is useful for decision-making, whereas taxable income is calculated according to rules and regulations stated in the Income Tax Act. The Income Tax Act is specific and rules-based regarding the calculation of taxable income. The federal government does this for various reasons, such as to stimulate spending in certain areas by allowing certain expenditures to be deductible immediately, to discourage certain expenditures (such as club dues) by disallowing their deduction in the calculation of taxable income, or to increase government tax revenues.

Because income tax actually paid to the government per the tax return is based on current year taxable income, which often does not include all the tax effects of every revenue or expense amount included in the current year income statement, a deferred or future income tax expense or benefit is often recognized on the income statement to reflect the income tax consequences of revenues and expenses that were not included in current year taxable income. Recognition of a deferred or future income tax expense or benefit (and recognition of a deferred or future income tax liability, or a deferred or future income tax asset) is called the temporary difference approach under IFRS, and the future income taxes method under ASPE. Under ASPE, an entity is not required to apply the future income taxes method; instead, it may choose to apply the simpler taxes payable method. However, under IFRS, an entity is required to apply the temporary difference approach.

Interperiod versus intraperiod tax allocation

Interperiod tax allocation refers to recognition of tax effects in the accounting period when the related transactions or events are recognized for financial reporting purposes, usually resulting in recognition of a deferred or future income tax liability and/or a deferred or future income tax asset on the statement of financial position. In contrast, intraperiod tax allocation refers to allocation of income tax expense or benefit between different areas or lines on the income or other financial statement. On the income statement, this allocation includes such things as presenting income tax expense on income from continuing operations separately, reporting items in discontinued operations on a net-of-tax basis, and reporting items in other comprehensive income on a net-of-tax basis. On the statement of changes in equity or the statement of retained earnings, this allocation includes such things as reporting a prior period adjustment on a net-of-tax basis. This chapter focuses on interperiod tax allocation since it is more complex than intraperiod tax allocation.

Special tax rules relating to loss years

If a company's deductible expenses and losses exceed its taxable revenues and gains in a year, the company reports a loss for income tax purposes, or a tax loss, and does not pay income tax in the year. Furthermore, the company may refile the tax returns of one or more previous years in which it earned taxable income, and deduct the tax loss from those years' taxable income. The company can then recover some or all of the income tax paid in those years (the difference between income tax paid in those years and income tax payable based on revised taxable income as a result of the tax loss carryback). The tax loss may also be carried forward to offset and reduce future taxable income, thereby reducing income tax payable in a future period (or periods).

The company has a benefit to the extent that it can recover income tax paid in a previous year or reduce income tax payable in a future year. According to the Income Tax Act, a company may carry the tax loss back three years (called the loss carryback period) and/or forward 20 years (called the loss carryforward period).

If taxable income was earned in one or more of the three previous years, the tax loss is often carried back in order to recover taxes already paid (and obtain the cash refund sooner). However, the company may choose to carry the tax loss forward (for example, if the tax loss is small, or if future income tax rates are expected to be higher than previous years' income tax rates).

Becoming Proficient in Related Calculations

Accounting for income taxes is theoretically and technically complex. In addition, the terminology can be difficult to grasp.

Therefore, you should devote a significant amount of time to studying the exercises and illustrations in this chapter, which are structured to take you through the learning process gradually. As with most accounting topics, a solid understanding of the fundamental concepts will make it easier to understand the complex concepts.

TIPS ON CHAPTER TOPICS

- The term accounting income (loss) refers to the difference between revenues earned and expenses incurred (other than income tax expense) on an accrual basis income statement in a given year. The term taxable income (loss) refers to the difference between taxable revenues and deductible expenses on a tax return in a given year. Accounting income appears on the income statement with the caption “Income before income taxes.” Accounting income is often referred to as income for book purposes, pre-tax financial income, or income for financial reporting purposes.

- An excess of deductible expenses over taxable revenues on an entity's tax return is called a tax loss. The Income Tax Act provides that a tax loss may be carried back three years or forward 20 years. Although loss carryback is optional, most textbook questions will assume or require full loss carryback to the extent possible.

- Income tax payable for a period is the amount of current income tax expense and is determined by applying the provisions of the Income Tax Act to taxable income (or loss) for the period. If a current year tax loss is carried back, the entity will have an income tax receivable (rather than an income tax payable), which results in a current income tax benefit (or a recovery of income tax) on the income statement.

- Under ASPE, an entity can choose to apply either the taxes payable method (and calculate only current income tax expense) or the future income taxes method (and calculate current income tax expense as well as future income tax expense). The future income taxes method under ASPE is also known as the asset and liability approach and the temporary difference approach. Under IFRS, this method is known as the temporary difference approach, and it is required. Note that it and the future income taxes method under ASPE are almost identical.

- A revenue or expense amount that appears on an income statement for financial reporting purposes or a tax return in one year but never appears on the other report is called a permanent difference. Future income tax expense is never recorded for permanent differences because these differences will never reverse (that is, they will never cause a future taxable amount or a future deductible amount). Examples of permanent differences appear in Illustration 18-1.

- A temporary difference is a difference between the reported amount (book value or carrying amount) of an asset or liability for financial reporting purposes, and the tax base of the asset or liability, which will result in taxable or deductible amounts in future years when the reported amount of the asset or liability is recovered or settled. Temporary differences that will result in taxable amounts when the related assets are recovered are often called taxable temporary differences. Temporary differences that will result in deductible amounts when the related assets or liabilities are settled are often called deductible temporary differences.

- Under IFRS, a taxable temporary difference gives rise to a deferred tax liability, a deductible temporary difference gives rise to a deferred tax asset, and the related expense is referred to as a deferred tax expense (benefit). Under ASPE, a taxable temporary difference gives rise to a future income tax liability, a deductible temporary difference gives rise to a future income tax asset, and the related expense is referred to as a future income tax expense (benefit).

- Most temporary differences are caused by reporting the same revenues or expenses in different periods for financial reporting purposes and for income tax purposes. Examples of temporary differences appear in Illustration 18-2.

- Deferred tax expense (or benefit) for a period results from changes in the deferred tax asset account or deferred tax liability account. A deferred tax expense results from an increase in a deferred tax liability or a decrease in a deferred tax asset. A deferred tax benefit results from an increase in a deferred tax asset or a decrease in a deferred tax liability. This is true because the other half of a journal entry dealing with a deferred tax asset or a deferred tax liability (both statement of financial position accounts) is a deferred tax expense or deferred tax benefit (both income statement accounts). Deferred tax expense increases total income tax expense for the period. Deferred tax benefit reduces total income tax expense for the period.

- Deferred tax benefit is an income statement account to which credits to (or decreases in) deferred tax expense are recorded. Deferred tax benefit is considered a tax income account.

- Total income tax expense (or benefit) is the sum of current income tax expense (or benefit) and deferred tax expense (or benefit). Income tax expense is often referred to as “provision for income tax.” Hence, provision for income tax usually includes both a current portion and a future portion. The meaning of the word “current” used in the context of provision for income taxes bears no relationship to the meaning of the word “current” used in the context of the statement of financial position classification of deferred taxes.

- A reversible (or reversing or timing) difference in the current period that causes an increase in a deferred tax liability, or a decrease in a deferred tax asset, will also cause a debit (charge) to deferred tax expense on the income statement. A reversing difference in the current period that causes a decrease in a deferred tax liability, or an increase in a deferred tax asset, will also cause a credit to a deferred tax benefit on the income statement.

- Pay close attention to terminology in this chapter and be careful not to confuse the many terms introduced. When describing deferred taxes from a statement of financial position perspective, the reference is to deferred tax asset and/or deferred tax liability. When discussing the effects of deferred taxes on the income statement, the reference is to deferred tax expense and/or deferred tax benefit. There is a correlation, however, because changes in a deferred tax asset and/or a deferred tax liability on the statement of financial position result in changes in deferred tax expense and/or deferred tax benefit on the income statement.

- To be recognized as assets and liabilities, a deferred tax asset and a deferred tax liability must meet the definition of an asset and a liability, respectively, as set out in the conceptual framework. A deferred tax asset should only be recognized if it is an economic resource that is capable of producing cash flows. A deferred tax asset is only capable of producing future cash inflows or reducing future cash outflows to the extent that the entity will earn enough taxable income in the future against which the related temporary difference can be applied.

- Under ASPE, a future tax asset may be recognized for the future tax effects of all deductible temporary differences, unused tax losses, and income tax reductions, and then be offset by a valuation allowance to bring the future tax asset to an amount that is more likely than not to be realized in future. However, under IFRS, a valuation allowance is not used; rather, the deferred tax asset is only recognized at an amount at which realization of the deferred tax asset will be probable.

- Under ASPE, future tax asset and future tax liability amounts are broken down between current and non-current assets and liabilities according to the classification of the asset or liability that gave rise to each future tax asset or future tax liability. (If no particular asset or liability gave rise to the future tax asset or future tax liability, classification is based on when the temporary difference is expected to reverse.) One net current and one net non-current amount are then determined. The current portion of the net future tax asset or net future tax liability is reported as current, and the non-current portion of the net future tax asset or net future tax liability is reported as non-current. However, under IFRS, all deferred tax asset and deferred tax liability amounts are classified as non-current.

- A corporation often pays estimated tax payments (instalments) during the year and may charge the payments to an account called Income Tax Receivable. The balance of this account is used to offset the balance of Income Tax Payable for financial reporting purposes. The net amount is classified as a current asset if the receivable account has the larger balance. The net amount is classified as a current liability if the payable account has the larger balance.

- The effective tax rate for a period is calculated by dividing total income tax expense on the income statement by income before income taxes on the income statement. The effective tax rate for a period may differ from the statutory tax rate (the rate set by government legislation) for the same period because of (a) permanent differences, and/or (b) changes in deferred tax assets and/or deferred tax liabilities as a result of differences between the current statutory tax rate and future statutory tax rates.

- The deferred tax asset and deferred tax liability are not discounted amounts.

- Future deductible amounts are often called future tax deductible amounts.

Examples of Permanent Differences

- Revenues or gains that are recognized for financial reporting purposes but are never included in taxable income:

- dividends received from other taxable Canadian corporations

- proceeds from life insurance policies carried by the company on key officers or employees

- Expenses or losses that are recognized for financial reporting purposes but are never deductible for tax purposes:

- golf and social club dues

- premiums paid on life insurance policies carried by the company on key officers or employees (where the company is the beneficiary)

- certain fines and penalties

- Revenues or gains that are included in taxable income but are never recognized for financial reporting purposes:

- no examples exist at the current time

- Expenses or losses or other deductions that are deductible for tax purposes but are never recognized for financial reporting purposes:

- depletion allowance of natural resources in excess of their cost

Examples of Reversing (or Timing) Differences

- Revenues or gains that are included in taxable income in a period after they are included in accounting income (or recognized for financial reporting purposes).

- An example is use of the accrual method in accounting for instalment sales for financial reporting purposes, and use of the cash instalment method in calculating taxable income for tax purposes. (Note also that this situation causes the reported amount of the account receivable asset on the statement of financial position to be higher than its tax basis, which will result in taxable amounts in future year(s) when the asset is recovered—in the years when cash is collected.)

- Other examples include:

- Use of the percentage-of-completion method in accounting for revenue recognition of long-term contracts for financial reporting purposes, and use of the zero-profit method (under IFRS) or the completed-contract method (under ASPE) in calculating taxable income for tax purposes

- Accrual of revenues in the period earned for financial reporting purposes, and inclusion of revenues in taxable income as cash is collected

- Recognition of unrealized holding gains for financial reporting purposes, and inclusion of gains in taxable income in the year they are realized

- Expenses or losses that are deductible for tax purposes in a period after they are included in accounting income (or recognized for financial reporting purposes).

- An example is accrual of an expense or loss (such as litigation accrual) for financial reporting purposes, which is only deductible for tax purposes when it is settled. (Note also that this situation causes the reported amount of the liability on the statement of financial position to exceed its tax basis of zero. This will result in deductible amounts in future year(s) when the litigation liability is settled.)

- Other examples include:

- product warranty expenses and liabilities

- estimated losses and liabilities related to discontinued operations or restructurings

- accrued pension expenses and the pension liability

- holding or impairment losses on investments or other assets and the carrying amount of such assets

- Revenues or gains that are included in taxable income in a period before they are included in accounting income (or recognized for financial reporting purposes).

- An example is revenue received in advance for rent or subscriptions. For tax purposes, the revenue may have to be included in taxable income in the period when the cash is received; however, the revenue is not included in accounting income until it is earned. (Note also that this situation causes the reported amount of the liability, such as unearned revenue, to exceed its tax basis of zero. This will result in deductible amounts in future year(s) when the liability is settled.)

- Other examples include:

- sale and leaseback gains, including a deferral of profit for financial reporting purposes that would be reported as realized for tax purposes

- royalties received in advance

- Expenses or losses that are deductible for tax purposes in a period before they are included in accounting income (or recognized for financial reporting purposes).

- An example is depreciating an asset faster for tax purposes (according to the capital cost allowance, or CCA rules) than for accounting purposes. (Note also that this causes the PP&E asset's reported value on the statement of financial position to exceed its tax basis or UCC. This will result in taxable amounts in future years when depreciation expense exceeds the CCA or when the asset is sold.)

- Other examples include:

- property and depletable resources that are depreciated/depleted faster for tax purposes than for financial reporting purposes

- deductible pension funding that exceeds the pension expense that is recognized

- prepaid expenses that are deducted in calculating taxable income in the period when they are paid, but are expensed in the income statement when the benefits are received

Reconciliation of Accounting Income to Taxable Income

Accounting Income

+/− Permanent Differences:

− Revenues recognized in accounting income this period, but never included in taxable income

+ Expenses recognized in accounting income this period, but never deductible for tax purposes

+ Revenues included in taxable income this period, but never recognized in accounting income

− Expenses deducted for tax purposes this period, but never recognized in accounting income

+/− Originating Reversible (Timing) Differences:

− Revenues recognized in accounting income this period, but to be included in taxable income in a later period

+ Expenses recognized in accounting income this period, but to be deducted for tax purposes in a later period

+ Revenues included in taxable income this period, but to be recognized in accounting income in a later period

− Expenses deducted for tax purposes this period, but to be deducted from accounting income in a later period

+/− Reversing Reversible (Timing) Differences:

− Revenues recognized in accounting income this period, but included in taxable income in an earlier period

+ Expenses recognized in accounting income this period, but deducted for tax purposes in an earlier period

+ Revenues included in taxable income this period, but recognized in accounting income in an earlier period

− Expenses deducted for tax purposes this period, but recognized as an expense in accounting income in an earlier period

= Taxable Income

- No deferred tax expense or deferred tax benefit is recognized for permanent differences because they will not have any future tax consequences.

- Timing differences that originate in the current period and give rise to future taxable amounts are deducted from accounting income in the reconciliation of accounting income to taxable income. These differences will also cause a deferred tax liability account to be recognized on the statement of financial position in the current period, representing the deferred tax expense on those future taxable amounts.

- Timing differences that originate in the current period and give rise to future deductible amounts are added to accounting income in the reconciliation of accounting income to taxable income. These differences will also cause a deferred tax asset account to be recognized on the statement of financial position in the current period, representing the deferred tax benefit of those future deductible amounts.

- Refer to Illustration 18-1 for examples of permanent differences; refer to Illustration 18-2 for examples of reversible or timing differences. The four types of examples addressed in Illustration 18-1 and Illustration 18-2 appear in the same order as they are referenced in this illustration. Thus, the first type of permanent difference listed in Illustration 18-3 corresponds to the first type of permanent difference described in Illustration 18-1. Also, the first type of reversible/timing difference listed in Illustration 18-3 corresponds to the first type of reversible/timing difference described in Illustration 18-2.

- This reconciliation will help you in solving some homework assignments and exam questions, but it is not relevant in all situations. The timing differences included in this reconciliation are only the ones that originated in or are reversed in the current year. This reconciliation can be used to solve for taxable income, accounting income, and changes in the related temporary differences on the statement of financial position in the current year. This reconciliation does not identify the temporary differences that exist at year end.

PURPOSE: This case provides practice in distinguishing between reversible or timing differences and permanent differences. It also provides practice in distinguishing between differences that will be taxable or deductible in the future.

In reviewing a client's records, you find the items listed below pertaining to the current year.

Instructions

Indicate whether each item involves:

(a) a reversing difference that will result in future deductible amounts.

(b) a reversing difference that will result in future taxable amounts.

(c) a permanent difference.

Solution to Case 18-1

- (b)

- (a)

- (b) Use of the accrual method for accounting purposes causes the entire profit from the instalment sale to be reflected in the income statement in the period of sale. Use of the instalment (cash) method for tax purposes causes the profit to be allocated or taxed over the collection period (as cash is collected). The amount of profit taxed in a period is proportionate to the amount of revenue collected in the period.

- (c) Dividends between taxable Canadian corporations flow tax-free.

- (a)

- (c)

- (c)

- (b)

- (c)

- (a)

- (b) When an asset is amortized or depreciated faster for tax purposes than it is amortized or depreciated for accounting purposes, more amortization or CCA is deducted in determining taxable income in the current period. This means that the excess CCA, for example, deducted in the current year will have to be added to taxable incomes in the future. That is, this results in net future taxable amounts.

- (a) This unrealized holding loss is not deductible for tax purposes until it is realized (in the future period in which the securities are sold).

- (b)

- (a) This loss is not deductible for tax purposes until it is realized.

- (b)

- (a) The royalty receipts are included in taxable income in the period they are received.

- (a) The gain is generally deferred for accounting purposes but included in current taxable income for tax purposes. (Under IFRS, the gain is recognized over the lease term. Under ASPE, the gain is amortized on the same basis as the depreciation of the leased asset.)

- (a)

- (a) Subscriptions collected in advance are included in taxable income in the period received. The related revenue is deferred for accounting purposes until it is earned.

- (a)

- (a)

- (b)

Journal Entry to Record Income Taxes

To record income taxes, the best approach is to perform the following steps in order.

- Calculate income tax payable for the current period. This is always based on the amount of taxable income and the tax rate in the current year. This amount is recorded with a debit to current income tax expense and a credit to income tax payable. If there is a tax loss in the current year, the benefit of a loss carryback is recorded with a debit to income tax receivable and a credit to current income tax benefit.

- Calculate the change required in the deferred tax asset and/or deferred tax liability. The balance of the deferred tax asset and/or deferred tax liability account at the statement of financial position date must be determined. This may require the preparation of a schedule. The appropriate balance of the deferred tax asset and/or deferred tax liability represents the future tax consequences of the (cumulative) temporary differences and tax loss carryforwards existing at the statement of financial position date. The difference between the correct ending balance at year end and the unadjusted beginning balance of a deferred tax account is the deferred tax expense or benefit, depending on whether a debit or a credit is required. The adjustment brings the deferred tax asset or liability account to the correct balance, with the same amount recognized as the deferred tax expense or benefit.

- Record income tax expense. Total income tax expense is the total of the current income tax expense (or benefit) and the deferred tax expense (or benefit). The current expense (benefit) is offset by a credit (debit) to income tax payable (receivable).

- A temporary difference is equal to the cumulative amount of timing differences that still exist at year end between an asset or liability's carrying amount in the accounts and its tax value or tax base.

- In calculating deferred taxes at a statement of financial position date, the amount of temporary differences must be determined. Information on when each temporary difference originated is not required; some or all of the differences could have originated in years prior to the current period. Information about the individual future years when each temporary difference is expected to reverse is generally not needed if the statutory tax rate is the same flat rate year after year going forward. However, if the future statutory tax rates have been enacted and will differ from the current rate, information about the individual future years when each temporary difference is expected to reverse is needed. Thus, if a single statutory tax rate applies to all future years, an aggregate calculation of the deferred tax asset/liability is appropriate. However, if different statutory tax rates apply to individual future years, a schedule of when the temporary differences will become taxable or deductible amounts is required, including a separate calculation for each future year affected.

- In determining the future income tax consequences of temporary differences (Step 2), a phased-in change in statutory tax rates requires a schedule to be prepared showing each future year in which existing temporary differences will reverse, resulting in taxable or deductible amounts. In determining the applicable statutory tax rate, you must make assumptions about whether the entity will report taxable income or a tax loss in each future year affected by the reversal of existing temporary differences. When calculating income tax payable or receivable in the future due to existing temporary differences, the provisions of the tax law and enacted statutory tax rates for the relevant future years must be applied. The following guidelines are used to determine the applicable statutory tax rate:

- If taxable income is expected in a year when a future taxable or deductible amount is scheduled to reverse, use the enacted statutory tax rate for the future year to calculate the related deferred tax liability or deferred tax asset.

- If a tax loss is expected in a year when a future taxable or deductible amount is scheduled to reverse, use the enacted statutory tax rate of the prior year to which the tax loss would be carried back or the enacted statutory tax rate of a future year to which the tax loss carryforward would be applied, whichever is appropriate, in order to calculate the related deferred tax liability or deferred tax asset.

- It is more straightforward to prepare separate journal entries to record current income taxes and deferred income taxes. With separate journal entries, you could perform Step 1 above and record the results with either a credit to income tax payable (if there is taxable income in the current period) or a debit to income tax receivable (if there is a tax loss in the current period and a loss carryback is applied). The other half of this first journal entry would be a debit or credit (whichever is needed to make the entry balance) to current income tax expense or current income tax benefit. A second journal entry would be recorded for the results of Step 2 above. In this journal entry, a debit or credit would be recorded to the deferred tax asset or deferred tax liability account to bring it to its correct year-end balance on the statement of financial position. The other half of this second journal entry would be either a debit or credit to deferred tax expense or deferred tax benefit, as appropriate, to make the entry balance. Step 2 can be repeated (and another journal entry recorded) if there is more than one reason for having temporary differences and separate entries are preferred. Thus, if the entity has three types of temporary differences, Step 2 might be performed three times, making a total of four single journal entries to record income taxes for the period. This approach to recording separate entries for income taxes is illustrated in parts (a) and (b) of the Solution to Exercise 18-1.

CASE 18-2

PURPOSE: This case examines the temporary difference approach and the steps in the calculation of the deferred tax assets and deferred tax liabilities at the reporting date.

The objectives of accounting for income taxes are to recognize (a) the amount of income tax payable or receivable for the current year, and (b) the amount of deferred tax liabilities and/or deferred tax assets that arise due to the future tax consequences of transactions and events that have been recognized in an entity's financial statements and tax returns.

Instructions

(a) If a revenue item is reported on the income statement in 2014, but is included on the tax return in 2015, explain whether the related income tax effect should be reflected on the income statement in 2014 or 2015, and explain why.

(b) Explain whether the temporary difference approach to accounting for deferred taxes focuses on proper valuation of assets and liabilities (and therefore the statement of financial position) or on income determination (and therefore the income statement).

(c) List the steps required in the calculation of deferred tax liabilities and deferred tax assets.

Solution to Case 18-2

(a) The income tax consequences of a transaction or event are recognized in the same period that the transaction or event is recognized in the financial statements. This is the essence of the temporary difference approach. Thus, the income tax effect of revenue recognized in 2014 should also be recognized on the income statement in 2014, even if payment of the related income tax is deferred to a later year.

(b) At any reporting date, the correct balance of the deferred tax account is calculated by multiplying the future taxable and deductible amounts stemming from temporary differences existing at the statement of financial position date by the applicable statutory tax rate(s). As such, a deferred tax liability (or a deferred tax asset) is recognized representing the likely income tax effect of existing temporary differences in future years. The amount of deferred tax expense (or benefit) recognized on the income statement is determined by the change in the deferred tax liability and/or deferred tax asset balance from the previous statement of financial position date to the current reporting date. Therefore, deferred tax expense (or benefit) is a residual figure, often called a “plug” figure. Under IFRS, a deferred tax asset is recognized only to the extent that it is probable that the tax benefit will be realized in the future. Under ASPE, if a future income tax asset is recognized, it may be offset by a valuation allowance to bring the future income tax asset to an amount that is more likely than not to be realized in the future. Therefore, both the temporary difference approach and the future income taxes method focus on proper valuation of assets and liabilities (and therefore the statement of financial position).

(c) The steps required in the calculation of deferred tax liabilities and deferred tax assets are as follows:

- Identify (a) the types and amounts of existing temporary differences, and (b) the nature and amount of any tax loss available for carryforward and the remaining length of the carryforward period.

- Measure the total deferred tax liability resulting from taxable temporary differences, using the applicable statutory tax rates.

- Measure the total deferred tax asset resulting from deductible temporary differences and tax loss carryforwards, using the applicable statutory tax rates.

- Ensure the proper valuation of deferred tax assets or future income tax assets. Under IFRS, recognize a deferred tax asset only to the extent that it is probable that the benefits will be realized in the future. Under ASPE, apply the “more likely than not” rule by offsetting the total future income tax asset by a valuation allowance to bring the future income tax asset to an amount that is more likely than not to be realized in the future. ASPE permits a choice between using a valuation allowance and determining only the net amount as under IFRS.

PURPOSE: This exercise illustrates how to record current income tax expense and deferred tax expense when one taxable temporary difference exists. It will also demonstrate the effect of reversal of the same temporary difference on income tax expense.

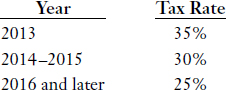

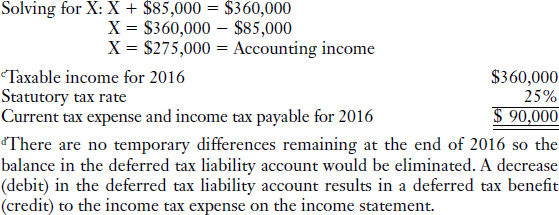

Gary Winarski Inc. has accounting income of $400,000 for 2014. There are no permanent differences in calculating taxable income, and there were no deferred taxes at the beginning of 2014. At the end of 2014, there are temporary differences of $85,000, which are expected to result in taxable amounts in 2016. The statutory tax rates enacted in 2014 are as follows:

Instructions

(a) Calculate taxable income for 2014 and record income tax payable.

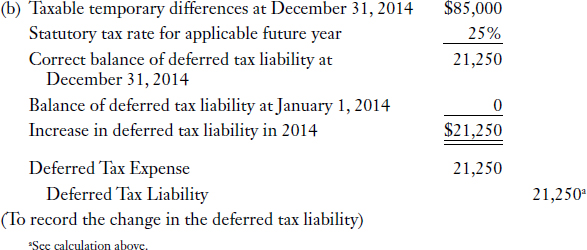

(b) Calculate the deferred tax liability at December 31, 2014, and record the change in the deferred tax liability, assuming that taxable income is expected in all future years.

(c) Draft the income tax expense section of the income statement for 2014 (beginning with “Income before income taxes”).

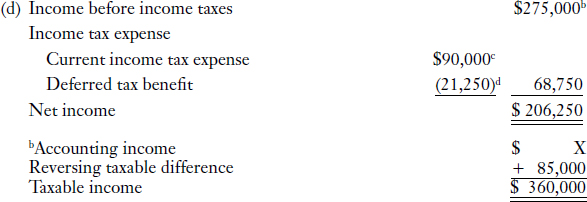

(d) Draft the income tax expense section of the income statement for 2016 assuming taxable income for 2016 is $360,000 (beginning with “Income before income taxes”).

Solution to Exercise 18-1

EXPLANATION: Use the reconciliation format in Illustration 18-3 to calculate taxable income. Since there were no deferred taxes (and, thus, no temporary differences) existing at the beginning of 2014, all $85,000 of temporary differences existing at the end of 2014 must have originated (come about) in 2014. Because these originating reversible or timing differences will result in future taxable amounts, they cause taxable income to be lower than accounting income in 2014.

EXPLANATION: The deferred tax liability at December 31, 2014, is measured using the statutory tax rate of the future year (2016) in which the underlying temporary difference is expected to reverse and result in a taxable amount in that year.

Notice that the effective tax rate for 2014 is 28.938% ($115,750 ÷ $400,000 = 0.28938), which is lower than the 30% statutory tax rate for 2014. This is because $315,000 of the $400,000 is taxed at 30% and $85,000 of the $400,000 is expected to be taxed at 25%.

- Notice that the effective tax rate for 2016 is 25% ($68,750 ÷ $275,000 = 0.25), which equals the statutory tax rate for 2016.

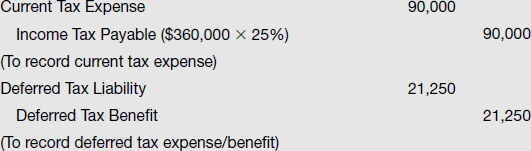

- Think about the journal entry(s) that would be required in 2016 to record income taxes. They would appear as follows:

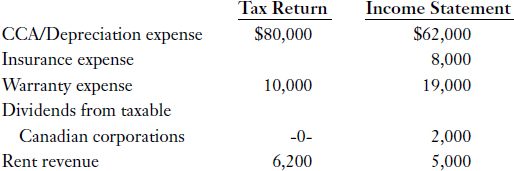

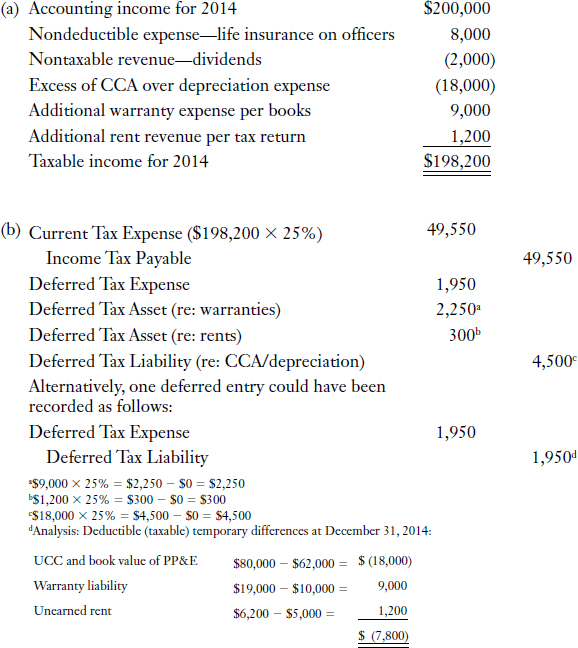

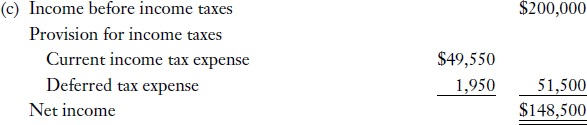

PURPOSE: This exercise illustrates how to account for income taxes when there are both permanent and reversing differences involved and the same statutory tax rate is enacted for all periods affected.

The Monte Corporation has accounting income of $200,000 for 2014 (its first year of operations). The accounts where there were differences between the revenues and expenses reported on the 2014 tax return and the 2014 income statement are as follows:

The insurance expense was for life insurance policies carried by Monte on key officers, for which Monte is the beneficiary.

The tax rate for 2014 is 25%, and no new rate has been enacted for future years.

Instructions

(a) Calculate taxable income for 2014.

(b) Prepare the journal entries to record income taxes for 2014.

(c) Prepare the bottom of the 2014 income statement beginning with the caption “Income before income taxes.”

Solution to Exercise 18-2

While only one deferred tax asset or deferred tax liability account may be used as shown above, the use of separate deferred tax accounts for each type of temporary difference (as illustrated above) may be helpful if deferred tax assets and liabilities are later classified between current and non-current on the balance sheet (as required under ASPE).

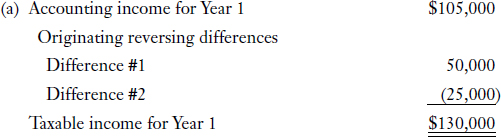

PURPOSE: This exercise illustrates the steps involved in calculating and recording income taxes when two types of temporary differences exist and there is a phased-in change in tax rates.

Benyon Corporation has the following facts available:

- Accounting income for Year 1 is $105,000.

- Year 1 is the first year of operations.

- One temporary difference exists at the end of Year 1 that will result in deductible amounts of:

$20,000 in Year 2.

$30,000 in Year 3.

- Another temporary difference exists at the end of Year 1 that will result in taxable amounts of:

$11,000 in Year 2.

$14,000 in Year 3.

- Statutory tax rates enacted by the end of Year 1 are:

35% for Year 1.

30% for Year 2.

25% for Year 3.

- Taxable income is expected in all future years.

- Benyon Corporation prepares financial statements in accordance with IFRS.

Instructions

(a) Calculate taxable income for Year 1, assuming there are no permanent differences.

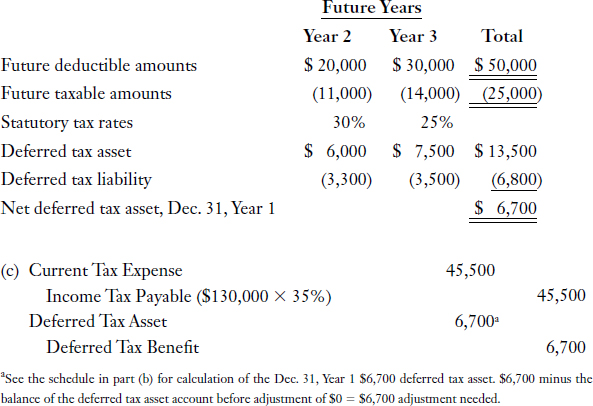

(b) Calculate deferred taxes to be reported on the statement of financial position at the end of Year 1.

(c) Prepare the journal entries to record income taxes for Year 1.

(d) Draft the income tax expense section of the income statement for Year 1.

Solution to Exercise 18-3

(b) At December 31, Year 1, a net deferred tax asset of $6,700 should be reflected on the statement of financial position and classified as non-current, because under IFRS, all deferred tax assets and deferred tax liabilities are classified as non-current. Deferred taxes are calculated using a schedule as follows:

(d) The relevant section of the income statement for Year 1 would appear as follows:

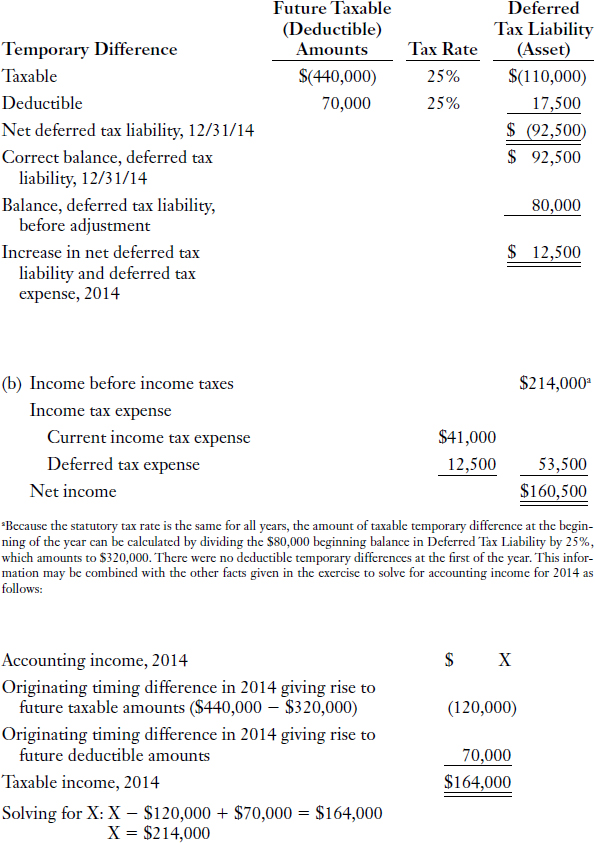

PURPOSE: This exercise reviews a situation that involves both a deferred tax asset and a deferred tax liability at the beginning and at the end of the year. It also reviews a reconciliation of accounting income to taxable income.

The following facts relate to the Tasty Bits Corporation:

- Deferred tax liability, January 1, 2014, $80,000.

- Deferred tax asset, January 1, 2014, $0.

- Taxable income for 2014, $164,000.

- There are no permanent differences in 2014.

- Temporary difference at December 31, 2014, giving rise to future taxable amounts, $440,000.

- Temporary difference at December 31, 2014, giving rise to future deductible amounts, $70,000.

- Tax rate for all years, 25%.

- The company is expected to operate profitably in all future years.

- The company prepares financial statements in accordance with IFRS.

Instructions

(a) Prepare the journal entries to record current and deferred taxes for 2014.

(b) Draft the income tax expense section of the income statement for 2014, beginning with the line “Income before income tax.”

Solution to Exercise 18-4

Supporting calculations:

PURPOSE: This exercise will illustrate the application of guidelines for classification of deferred tax assets and deferred tax liabilities.

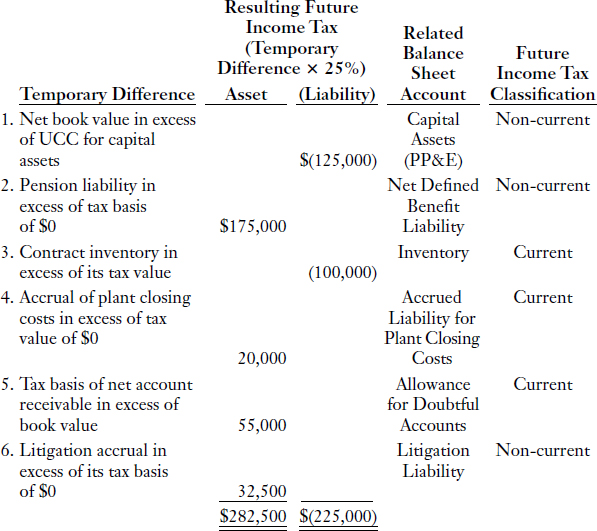

The following information relates to The Chip Corporation, which has several temporary differences existing at December 31, 2014:

- The carrying value of capital assets exceeds the tax basis (the UCC) of those assets by $500,000.

- A long-term pension liability of $700,000 appears on the statement of financial position as a result of accrual of pension costs. Only funds contributed have been deducted from taxable income over the years.

- For tax purposes, $400,000 of gross profit on contracts has been deferred until 2015. This profit is included in the year-end balance of inventory and in 2014 accounting income.

- Disposal of an operating segment is scheduled for 2015; an accrued liability of $80,000 for related plant closing costs is classified as a current liability.

- An allowance for doubtful accounts of $220,000 appears on the statement of financial position. Uncollectible accounts are deductible for tax purposes only when individual accounts are written off. All accounts receivable are classified as current assets.

- An estimated liability for litigation settlements of $130,000 appears in the long-term liability section of the statement of financial position. The liability has a tax basis of zero.

The statutory tax rate is 25% for all years.

The Chip Corporation prepares financial statements in accordance with ASPE.

Instructions

Calculate current and non-current future tax assets and/or future tax liabilities to appear on the statement of financial position at December 31, 2014. Indicate how they are to be classified.

Under ASPE, future income tax assets and future income tax liabilities are reported on the statement of financial position in a net current and a net non-current amount. A future income tax asset or future income tax liability is classified as current or non-current based on the classification of the related asset or liability for financial reporting purposes. A future income tax asset or future income tax liability that is not related to an asset or liability for financial reporting purposes, including a future income tax asset related to loss carryforwards, is classified as current or non-current based on the expected reversal date of the temporary difference.

Solution to Exercise 18-5

SUMMARY: The net current amount to be reported on the balance sheet is a future income tax liability of $25,000 ($100,000 − $20,000 − $55,000 = $25,000). The net non-current amount to be reported on the balance sheet is a future income tax asset of $82,500 ($175,000 + $32,500 − $125,000 = $82,500).

EXPLANATION:

- $500,000 future taxable amount × 25% = $125,000 future income tax liability. The related assets, capital assets (PP&E), are classified as non-current on the balance sheet. Therefore, the resulting future income tax liability is classified as non-current.

- $700,000 future deductible amount × 25% = $175,000 future income tax asset. The related liability, Net Defined Benefit Liability, is a non-current liability on the balance sheet. Therefore, the resulting future income tax asset is classified as non-current.

- $400,000 future taxable amount × 25% = $100,000 future income tax liability. The related asset would likely be an inventory account. Therefore, the future income tax liability is classified as current.

- $80,000 future deductible amount × 25% = $20,000 future income tax asset. The related liability, Accrued Liability for Plant Closing Costs, is classified as current on the balance sheet. Therefore, the resulting future income tax asset is classified as current.

- $220,000 future deductible amount × 25% = $55,000 future income tax asset. The related contra asset account, Allowance for Doubtful Accounts, is classified as current on the balance sheet. Therefore, the resulting future income tax asset is classified as current.

- $130,000 future deductible amount × 25% = $32,500 future income tax asset. The related accrued liability account, Litigation Liability, is classified as non-current on the balance sheet. Therefore, the resulting future income tax asset is classified as non-current.

- Under ASPE, the term “current” is used in the description of two totally unrelated amounts in accounting for income taxes. These two amounts are current income tax expense on the income statement and future income tax asset or future income tax liability classified as current on the balance sheet. Both current and future income tax expense are presented in the income tax expense section of the income statement. Current income tax expense on the income statement refers to the amount of income tax expense for the current period based on the current period tax return. Having taxable income in the current period results in a current income tax expense reported on the income statement. A tax loss in the current period, if carried back to a prior year, results in a current income tax benefit reported on the income statement. Under ASPE, future income tax assets and liabilities are classified as current or non-current on the balance sheet based on the classification of the underlying asset or liability that resulted in the future income tax asset or future income tax liability. The total change during the period in both current and non-current future income taxes on the balance sheet determines the amount of future income tax expense or benefit on the income statement.

- Under IFRS, all deferred tax assets and deferred tax liabilities are classified as non-current.

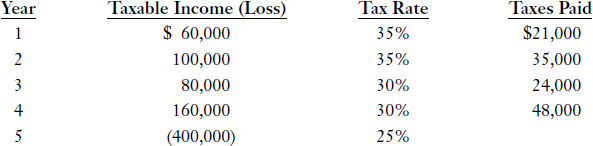

PURPOSE: This exercise reviews the accounting procedures for a tax loss (or loss for income tax purposes).

The Evans Corporation has had no permanent or reversible differences since it began operations. Information regarding taxable income and taxes paid is as follows:

The statutory tax rate for Year 6 and subsequent years is 20%.

The Evans Corporation prepares financial statements in accordance with IFRS.

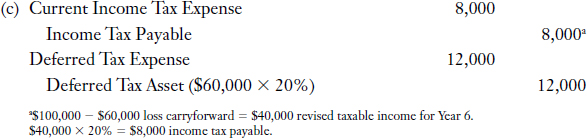

Instructions

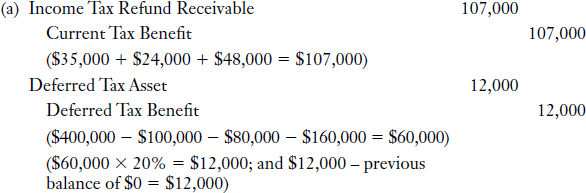

(a) Assuming the tax loss in Year 5 is carried back to the extent possible, prepare the journal entries to record the loss carryback and to record the expected benefits of any related loss carryforward. Assume it is probable that the benefits of any loss carryforward will be fully realized.

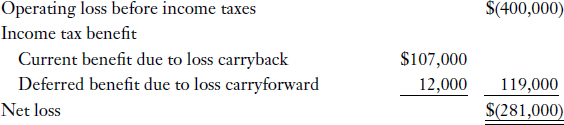

(b) Explain how all of the accounts in the journal entries from part (a) are to be reported in the financial statements for Year 5. Draft the income tax expense section of the income statement for Year 5, beginning with the line “Operating loss before income taxes.”

(c) Assuming taxable income is $100,000 (before considering the loss carryforward) in Year 6, prepare the journal entries to record income taxes. Also, draft the income tax expense section of the income statement for Year 6, beginning with the line “Income before income taxes.”

Solution to Exercise 18-6

- The benefit of a tax loss carryforward is recognized in the year of the loss that gives rise to the loss carryforward if it is probable that the benefit will be realized. The statutory tax rate for the future year in which the benefits are expected to be realized is used to calculate the related deferred tax asset.

- Current Tax Benefit and Deferred Tax Benefit are both negative components of income tax expense; therefore, they are credits to the income statement.

- In this exercise, we are asked to assume that it is probable that the benefits of any loss carryforward will be fully realized. However, if realization of the full $12,000 deferred tax asset was not probable, under IFRS, the above journal entry would be for an amount less than $12,000 (an amount at which realization in future would be probable).

- If the Evans Corporation prepared financial statements in accordance with ASPE, the $12,000 future income tax asset could be set up, and be offset by a valuation allowance if the full $12,000 was not more likely than not to be realized in the future. A valuation allowance would be established with a debit to Future Income Tax Expense and a credit to Allowance to Reduce Future Income Tax Asset to Expected Realizable Value. For example, in this exercise, if one half of the benefit of the loss carryforward was not expected to be realized within the loss carryforward period, an adjusting entry for $6,000 would be recorded with a debit to Future Income Tax Expense (re: Loss Carryforward) and a credit to Allowance to Reduce Future Income Tax Asset to Expected Realizable Value. For simplicity, Evans might choose not to set up the future income tax asset only to effectively draw it down again. If the future income tax asset is not set up and the benefit is realized in a later year, the benefit of the reduction in future taxes would be accounted for in that future year.

(b) Income Taxes Receivable would be classified as a current asset on the statement of financial position, and Deferred Tax Asset would be classified as a non-current asset on the statement of financial position.

The other two accounts are negative components of income tax expense. The income tax expense section of the income statement would appear as follows:

Under IFRS, all deferred tax assets and deferred tax liabilities are classified as non-current. However, if the Evans Corporation prepared financial statements in accordance with ASPE, the future income tax asset would be classified as a current asset if the benefit of the loss carryforward was expected to be realized in the year that immediately followed the balance sheet date.

PURPOSE: This comprehensive exercise illustrates how interperiod allocation of income taxes affects financial statements.

The following facts pertain to the Hess Corporation:

- There were no future income taxes on the December 31, 2013 balance sheet.

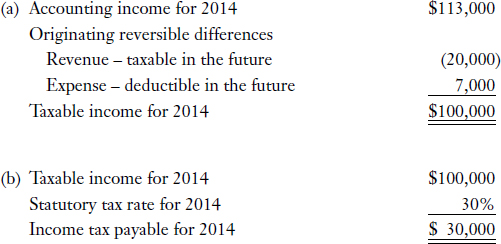

- Accounting income for 2014 is $113,000.

- $20,000 of revenue reported on the 2014 income statement will be included on the 2015 income tax return.

- $7,000 of expense reported on the 2014 income statement will be reported on the 2016 income tax return.

- There are no differences between accounting income and taxable income for 2014, other than the two items mentioned above.

- Statutory tax rates as at December 31, 2014, are as follows:

- Taxable income is expected in all future years.

- The Hess Corporation prepares financial statements in accordance with ASPE.

Instructions

(a) Calculate taxable income for the year ending December 31, 2014.

(b) Calculate income tax payable for the year ending December 31, 2014.

(c) Describe how each of the two reversible differences will affect future income tax returns.

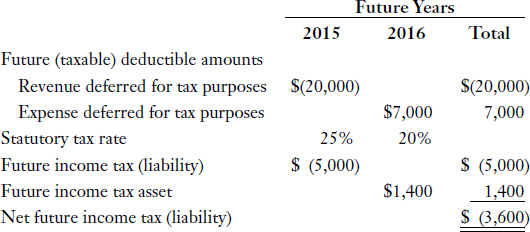

(d) Calculate the future income taxes to be reported on the balance sheet at December 31, 2014. Describe how they will affect the income statement for the year ending December 31, 2014.

(e) Prepare the journal entries to record income taxes for 2014.

(f) Describe how the future income tax account(s) will be reported on the balance sheet at December 31, 2014.

(g) Prepare the income tax expense section of the income statement for 2014, beginning with “Income before income taxes.”

Solution to Exercise 18-7

(c) The $20,000 of revenue that will be included on the 2015 tax return will result in a taxable amount (an amount that increases taxable income) on the 2015 income tax return. The $7,000 of expense that will be included on the 2016 tax return will result in a tax deductible amount (an amount that reduces taxable income) on the 2016 income tax return.

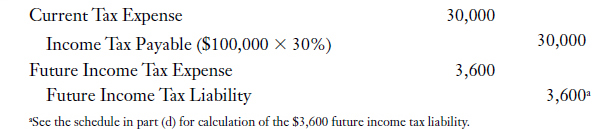

(d)

There were no future income taxes on the December 31, 2013 balance sheet. Therefore, the journal entry to record income taxes for 2014 will include an increase in Future Income Tax Liability (credit) of $3,600. This will cause a corresponding increase in Future Income Tax Expense (debit) of $3,600.

- Notice that the $5,000 increase in future income taxes, as a result of the deferral of the $20,000 of revenue, is recognized on the income statement in 2014 (which is the year in which the revenue appears on the income statement). Also, notice that the $1,400 decrease in future income taxes as a result of the deferral of the $7,000 of expense, is recognized on the income statement in 2014 (which is the year in which the expense appears on the income statement).

- Analyze the definitions of “taxable temporary difference,” “future income tax liability,” and “future income tax expense,” and how they apply to this situation. The definitions and analysis are as follows:

Taxable temporary difference: Definition—a temporary difference that will result in taxable amounts in a future year(s) when the related asset or liability is recovered or settled, respectively. Analysis—$20,000 of revenue is being recognized for accounting purposes in 2014, but deferred for tax purposes to 2015. The revenue may be an accrued revenue that results in recording of an account receivable or accrued receivable for accounting purposes in 2014. In 2015, this asset (receivable) is expected to be recovered (collected), which will result in reporting of the $20,000 of revenue on the 2015 tax return. That is, a taxable amount of $20,000 will appear on the 2015 tax return. Thus, at December 31, 2014, there is a $20,000 taxable temporary difference, which will be taxable in 2015.

Future income tax liability: Definition—the future tax consequence of a taxable temporary difference. Analysis—the $20,000 taxable temporary difference existing at December 31, 2014, will cause an increase of $5,000 in income tax payable in the future when the $20,000 amount is included in taxable income on the 2015 tax return.

Future income tax expense: Definition—the change in the balance sheet future income tax asset or future income tax liability account from the beginning to the end of the accounting period. Analysis—the $5,000 increase in future income tax liability in 2014 combined with the $1,400 increase in future income tax asset in 2014 results in a net future income tax expense of $3,600 on the income statement for 2014.

- Analyze the definitions of “deductible temporary difference” and “future income tax asset” and how they apply to this situation. The definitions and analysis are as follows:

Deductible temporary difference: Definition—a temporary difference that will result in deductible amounts in a future year(s) when the related asset or liability is recovered or settled, respectively. Analysis—$7,000 of expense is being recognized for accounting purposes in 2014, but is deferred for tax purposes to 2016. The expense may be an accrued expense that results in recording of an account payable or accrued payable for accounting purposes in 2014. In 2016, this liability (payable) is expected to be settled (paid), which will result in reporting of the $7,000 of expense on the 2016 tax return. That is, a deductible amount of $7,000 will appear on the 2016 tax return. Thus, at December 31, 2014, there is a $7,000 deductible temporary difference, which will be deductible for tax purposes in 2016.

Future tax asset: Definition—the future tax consequence of a deductible temporary difference or loss carryforward. Analysis—the $7,000 deductible temporary difference existing at December 31, 2014, will cause a decrease of $1,400 in income tax payable in the future when the $7,000 amount is deducted on the 2016 tax return.

(e) The journal entries to record income taxes for 2014 are as follows:

(f) Because Hess prepares financial statements in accordance with ASPE, each temporary difference and related future income tax asset or future income tax liability must be classified as current or non-current based on the classification of the asset or liability underlying each specific temporary difference. Assuming the $20,000 revenue has a related receivable on the books classified as a current asset, the resulting $5,000 future income tax liability is classified as a current liability on the balance sheet. Assuming the $7,000 expense has a related payable on the books classified as a non-current liability, the resulting $1,400 future income tax asset will be classified as a non-current asset on the balance sheet. Under ASPE, future income tax assets and future income tax liabilities are netted for reporting purposes, by netting future income tax asset and future income tax liability amounts that are classified as current (net current) and by netting future income tax asset and future income tax liability amounts that are classified as non-current (net non-current).

- Notice that the effective tax rate for 2014 ($33,600 ÷ $113,000) is not equal to the statutory tax rate for 2014 (30%). This is because the future statutory tax rates of 25% and 20% will apply to the $20,000 revenue and the $7,000 expense, respectively, that are included in 2014's $113,000 income before income taxes.

- Recall the objectives of the future income taxes method of accounting for income taxes and review the solution above to see how these objectives are met. These objectives are:

- to recognize income tax payable (or receivable) for the current year, and

- to recognize future income tax liabilities and/or future income tax assets representing the future tax consequences of transactions and events that have been recognized in the current year's financial statements or tax returns.

- Think about what will happen in 2015 when the $20,000 taxable temporary difference reverses. The $20,000 amount will be included as a revenue item on the tax return but not on the income statement for that year. There will be no remaining future income tax liability on the December 31, 2015 balance sheet related to the $20,000 amount. The reduction in the future income tax liability (debit) in 2015 will result in a future income tax benefit (credit) of $5,000 as part of the total income tax expense on the 2015 income statement.

- Think about what will happen in 2016 when the $7,000 deductible temporary difference reverses. The $7,000 amount will be deducted on the tax return but not on the income statement for that year. There will be no remaining future income tax asset related to the $7,000 amount on the December 31, 2016 balance sheet. The reduction in the future income tax asset (credit) in 2016 will result in a future income tax expense (debit) of $1,400 on the 2016 income statement.

ANALYSIS OF MULTIPLE-CHOICE QUESTIONS

Question

1. A temporary difference arises when a revenue item is reported for tax purposes in a period:

EXPLANATION: Revenue that is taxable in a period after the period when it is recognized in accounting income creates a temporary difference between the tax basis of an asset (zero) and its reported amount on the statement of financial position. This temporary difference will result in a taxable amount in a future period(s) when the asset is recovered (payment is collected). For example, if revenue is earned and accrued in a period in advance of the period in which the related cash is collected and taxed, cash collection is the taxable event, and a receivable is reported on the statement of financial position for accounting purposes until cash collection occurs.

Revenue that is taxable in a period before the period when it is recognized in accounting income creates a temporary difference between the tax basis of a liability (zero) and its reported amount on the statement of financial position. This temporary difference will result in a deductible amount in a future period(s) when the liability is settled (goods or services are delivered). For example, if revenue is collected in a period in advance of the period in which it is earned, cash collection is the taxable event, and an unearned revenue is reported on the statement of financial position for accounting purposes until the revenue is earned. (Solution = a.)

Question

2. Which of the following should be recorded to recognize future tax consequences attributable to temporary differences that will result in deductible amounts in future years?

EXPLANATION: A temporary difference giving rise to future deductible amounts requires recognition of a deferred tax asset for the amount of the future tax consequences related to the temporary difference. A temporary difference giving rise to future taxable amounts requires recognition of a deferred tax liability for the amount of the future tax consequences related to the temporary difference.

(Solution = b.)

Question

3. Assuming a 25% tax rate applies to all years involved, which of the following situations will give rise to a deferred tax liability on the statement of financial position?

- A revenue is deferred for financial reporting purposes but not for tax purposes.

- A revenue is deferred for tax purposes but not for financial reporting purposes.

- An expense is deferred for financial reporting purposes but not for tax purposes.

- An expense is deferred for tax purposes but not for financial reporting purposes.

- item II only

- items I and II only

- items II and III only

- items I and IV only

EXPLANATION: Notice that each situation describes a difference in timing of revenue or expense recognition for financial reporting purposes (accounting purposes or book purposes) and tax purposes (tax reporting purposes). Thus, each situation also results in a temporary difference. For each situation, determine if future taxable or deductible amounts will occur. Since a constant tax rate applies to all periods involved, a temporary difference resulting in net future taxable amounts will give rise to a deferred tax liability, and a temporary difference resulting in net future deductible amounts will give rise to a deferred tax asset. Items II and III will give rise to future taxable amounts; items I and IV will give rise to future deductible amounts. (Solution = c.)

Question

4. At the December 31, 2014 statement of financial position date, Brooks Corporation reports an accrued receivable for financial reporting purposes but not for tax purposes. When this asset is recovered in 2015, a future taxable amount will occur and:

- accounting income will exceed taxable income in 2015.

- Brooks will record a decrease in deferred tax liability in 2015.

- total income tax expense for 2015 will exceed current income tax expense for 2015.

- Brooks will record an increase in deferred tax asset in 2015.

EXPLANATION: The accrued receivable is likely the result of revenue earned but not collected; the revenue has been recorded for accounting purposes but not for tax purposes. When this asset (accrued receivable) is recovered (collected) in 2015, it will result in a taxable revenue amount being included in taxable income on the 2015 income tax return. Thus, in 2015, taxable income will be higher than accounting income because of the reversal of the temporary difference. Also in 2015, Brooks will record a decrease in the deferred tax liability account, resulting in a deferred tax benefit on the 2015 income statement. This will cause total income tax expense to be lower than current tax expense for 2015. (Solution = b.)

Question

5. The Kanak Corporation collects rent revenue in advance from tenants. Collection of $50,000 in 2014 is reported as revenue for tax purposes, but will be reported as revenue for accounting purposes in 2015 when it is earned. This situation will:

- result in future deductible amounts.

- result in a deferred tax liability on the statement of financial position at the end of 2014.

- cause total income tax expense to be less than income tax payable in 2015.

- cause accounting income to exceed taxable income in 2014.

EXPLANATION: Collecting and reporting of revenue for tax purposes in a period before it is earned and recognized for accounting purposes will result in future deductible amounts. A deferred tax asset is recognized to represent the future tax consequences of the revenue already reported for tax purposes. In a later period, the unearned revenue on the statement of financial position (a liability) will be settled by delivery of goods or services to customers, resulting in recognition of revenue, or perhaps by refunding customers' money. In that later period, taxable income will be lower than accounting income. Also in that later period, total income tax expense will exceed current income tax expense by the amount of the decrease in Deferred Tax Asset due to the reversal of the related temporary difference. (Solution = a.)

Question

6. Kaminsky Company reported deferred tax expense of $70,000 on its income statement for the year ended December 31, 2014. This could be the result of an increase in:

EXPLANATION: Think about the journal entry to record deferred tax expense. The journal entry involves a debit to Deferred Tax Expense and a credit to a statement of financial position account for deferred taxes. This credit is therefore either an increase in Deferred Tax Liability or a decrease in Deferred Tax Asset.

(Solution = d.)

Question

7. Mix Corporation reported $50,000 in revenues on its 2014 income statement, of which $22,000 will not be included in taxable income on its tax return until 2015. The statutory tax rate is 30% for 2014 and 25% for 2015. Assuming there are no other temporary differences related to similar situations, what amount should Mix report for the deferred tax liability on its statement of financial position at December 31, 2014?

- $5,500

- $6,600

- $7,000

- $8,400

EXPLANATION: At the statement of financial position date, December 31, 2014, there is a temporary difference of $22,000, which will be taxable in 2015. The income tax payable on that amount will be $5,500 ($22,000 × 25%) in 2015; however, future tax consequences related to transactions and events recorded in 2014 should be reflected on the financial statements for 2014. The journal entry to record these future tax consequences (assuming no balance of deferred taxes at the beginning of the period) would be a credit to Deferred Tax Liability and a debit to Deferred Tax Expense for $5,500. Therefore: (1) revenues of $50,000, and (2) current income tax expense of $8,400 ($28,000 × 30%), and (3) deferred tax expense of $5,500 ($22,000 × 25%) will be reflected on the 2014 income statement. Thus, both the $50,000 in revenues and the current and future tax consequences of the $50,000 in revenues appear on the same income statement in the same year, regardless of when the taxes are paid.

(Solution = a.)

Question

8. Bohémier Inc. uses the accrual method of accounting for financial reporting purposes and uses the cash instalment method of accounting for income tax purposes. Profits of $500,000 recognized for accounting purposes in 2014 will be collected in the following years:

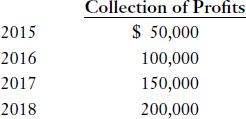

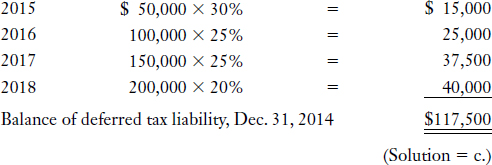

The statutory tax rates are: 35% for 2014, 30% for 2015, 25% for 2016 and 2017, and 20% for 2018. Taxable income is expected in all future years. What amount should be included on the December 31, 2014 statement of financial position for the deferred tax liability related to the above temporary difference?

- $15,000

- $100,000

- $117,500

- $175,000

EXPLANATION: This temporary difference will cause future taxable amounts, taxable at the statutory tax rates enacted for each applicable future period. Calculation of the deferred tax liability is as follows:

Question

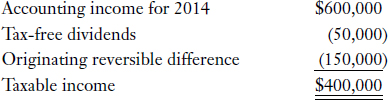

9. CMP Corporation prepared the following reconciliation for its first year of operations:

The originating difference will reverse evenly over the next two years at a statutory tax rate of 25%. The statutory tax rate for 2014 is 30%. What amount should be reported on the 2014 income statement for total income tax expense?

- $37,500

- $120,000

- $157,500

- $180,000

The originating reversible difference causes taxable income to be lower than accounting income in 2014; therefore, it will result in future taxable amounts. An increase in the deferred tax liability causes a deferred tax expense to be reported on the income statement. No deferred taxes are recorded for the tax-free dividends (a permanent difference). (Solution = c.)

Question

10. Refer to the facts of Question 9 above. In CMP's 2014 income statement, what amount should be reported for the deferred portion of its provision for income taxes?

- $157,500 debit

- $120,000 debit

- $37,500 credit

- $37,500 debit

EXPLANATION: The temporary difference existing at December 31, 2014, will result in future taxable amounts, and therefore gives rise to a deferred tax liability of $37,500 ($150,000 temporary difference × 25%) to be reported on the statement of financial position at that date. There was no beginning deferred tax liability since 2014 is CMP's first year of operations. Therefore, the $37,500 increase in deferred tax liability results in a deferred tax expense (debit) of $37,500 on the 2014 income statement. No deferred taxes are recorded for permanent differences, such as tax-free dividends, because they will never reverse. (Solution = d.)

Recall that “provision for income taxes” is another term for “income tax expense.”

Question

11. Refer to the facts of Question 9 above. In CMP's 2014 income statement, what amount should be reported as the current portion of its provision for income taxes?

- $180,000

- $157,500

- $150,000

- $120,000

EXPLANATION: The taxable income of $400,000 multiplied by the statutory tax rate of 30% for 2014 amounts to current tax expense of $120,000. (Solution = d.)

Question

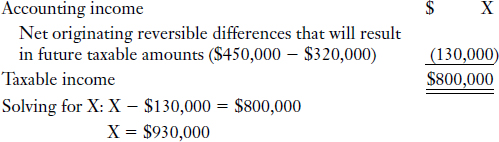

12. The Seong Company has the following taxable temporary differences:

![]()

The statutory tax rate for 2014 is 30%, and the statutory tax rate enacted for future years is 25%. Taxable income for 2014 is $800,000 and there are no permanent differences. Seong's accounting income for 2014 is:

- $350,000.

- $670,000.

- $930,000.

- $1,250,000.

EXPLANATION: Use the format for the reconciliation of accounting income to taxable income (see Illustration 18-3 and its accompanying tips). Enter the data given. Solve for the unknown. (Solution = c.)

The statutory tax rates were not required in this solution.

Question

13. At December 31, 2014, Norman Corporation has a future income tax asset of $50,000, which is based on the recognition of 100% of the potential tax benefits of a tax loss carryforward. The statutory tax rates are as follows: 35% for 2014 to 2016; 30% for 2017; and 25% for 2018 and thereafter. Norman Corporation prepares financial statements in accordance with ASPE. Assuming that management expects that only 50% of the related benefits will actually be realized, a valuation account should be established in the amount of:

- $25,000.

- $8,750.

- $7,500.

- $6,250.

EXPLANATION: Prepare the journal entry to record the necessary valuation account for the future income tax asset. The journal entry is as follows:

Since only 50% of the potential tax benefits are expected to be realized, a contra asset valuation account is required for the 50% of the future income tax asset (50% × $50,000 = $25,000) that is not expected to be realized. The tax rates are not relevant in this question, because applicable future income tax rates were already applied in calculating the $50,000 future income tax asset.

(Solution = a.)

- For simplicity, Norman might choose not to record the full future income tax asset only to effectively reduce it through the allowance. If the full future income tax asset is not recorded and the tax benefit of the total loss carryforward is realized in a later year, the tax benefit of the portion not previously recognized would be recognized in the year it is realized.

- Under IFRS, a valuation account is not used for deferred tax assets. A deferred tax asset is only permitted to be recognized at an amount at which realization in future periods is probable.

Question

14. At December 31, 2013, Malcolm Corporation reported a deferred tax liability of $60,000, which was attributable to a taxable temporary difference of $240,000. The temporary difference is scheduled to reverse in 2016. During 2014, a new tax law increased the corporate tax rate from 25% to 35%. Which of the following entries would correctly account for the effect of this change in future taxes?

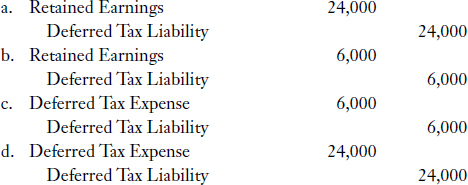

EXPLANATION: When a change in the tax rate is enacted (or substantively enacted) into law, deferred tax liabilities and deferred tax assets are adjusted accordingly in the period of the change. The effect is included in income from continuing operations as a component of deferred tax expense [($240,000 × 35%) − $60,000 = $24,000]. (Solution = d.)

Question

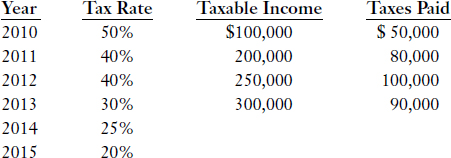

15. Freeman Corporation began operations in 2010. There have been no permanent differences or temporary differences to account for since inception of the business. The following data are available:

In 2014, Freeman has a loss for tax purposes of $510,000. What amount of income tax benefits should be reported on the 2014 income statement as a result of this tax loss?

- $198,000

- $127,500

- $153,000

- $102,000

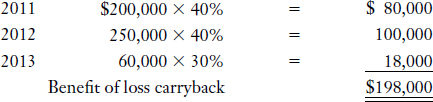

EXPLANATION: A tax loss can be carried back three years and/or forward 20 years. Freeman's tax loss should be carried back three years and applied to the earliest year first as higher tax rates were applied in those years (resulting in higher benefit of the loss carryback). The $510,000 loss should be applied as follows:

The future income tax rate (2015 and beyond) would only be used to calculate the benefit of a tax loss carryforward. A loss carryforward would result if the tax loss was larger than the combined taxable income for the three preceding years in the loss carryback period, or if the company elected to forego the loss carryback and carry the loss forward instead. The income tax rate for the current period (2014) is not used in calculating the benefits of a tax loss carryback or carryforward. (Solution = a.)