Chapter Fourteen

Economic Considerations

Chapter Outline

- Introduction

- Introductory Case Study: China National Trunk Highway System

- The Relationship Between Infrastructure and the Economy

- Sources of Funds

- Consideration of Project Economics

- Outro

Learning Objectives

After reading this chapter, you should be able to:

- Explain the relationship between infrastructure and the economy.

- List common funding sources for public infrastructure projects.

- Explain economic equivalence.

- Determine the net present value of simplified infrastructure projects.

Introduction

Consider the fact that you can buy fresh produce during the winter in the northeastern United States at prices that are often not noticeably different from what you would pay in the summer for local produce. One of the reasons that these low prices occur is that very low transportation costs are possible because of the investment that federal, state, and local governments have made in infrastructure. If the condition of the infrastructure that helps move the produce (e.g., the interstate highway system and rail system) was less effective than it currently is, produce would take much longer to reach its destination and the price per pound would escalate. Even worse, if the infrastructure was in very poor condition or nonexistent, you wouldn't even be able to buy fresh produce during the winter.

Alternatively, imagine a hypothetical city with an aging wastewater treatment facility that does not have any spare capacity to accept additional wastewater. A company desires to build a factory in the city, but given the city's aging infrastructure, the factory will have to add its own wastewater pretreatment facility, thus increasing the construction cost to the owners of the factory. The extra cost of adding pretreatment may be large enough that the company decides to build in another city, one which has the infrastructure in place to accept the factory's waste without requiring the factory to pretreat its waste. This scenario also illustrates the relationship between economic activity and the quality of infrastructure.

Introductory Case Study: China National Trunk Highway System

The rapid growth of China's economy has been accompanied by tremendous investment in their infrastructure, and future economic growth can only be possible with continued investment. Since the 1990s, rapid expansion of railways, inland waterways, and roads has occurred. Indeed, China is spending a reported 5 percent (or 9 percent, depending on the source) of their gross domestic product (GDP) on transportation, as compared to approximately 2 percent for most other industrialized countries such as the United States.

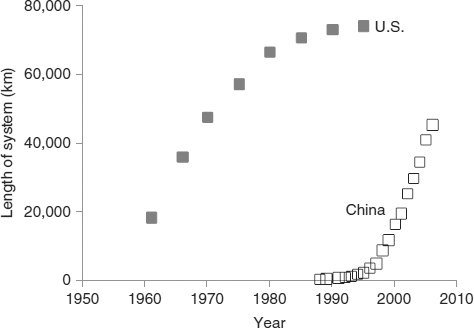

The centerpiece of this transportation expansion in China is their expressway system, known as the National Trunk Highway System (Figure 14.1). The purpose of the system is to link “major cities” with each other and with ports. Major cities include provincial capitals and cities with populations greater than 200,000. This highway system is rapidly expanding (Figure 14.2) and is expected to be 110,000 miles long by 2050. By comparison, the U.S. interstate highway system is 47,000 miles long and as seen from Figure 14.2, was not built as quickly as its Chinese counterpart. At its peak construction period (1955-1970), the United States was constructing 2,000 miles per year; between 2003 and 2008, China constructed 6,000 miles per year.

Figure 14.1 Portions of the National Trunk Highway System in Shanghai, China.

Copyright · Prill Mediendesign & Fotografie/iStockphoto.

Figure 14.2 Comparison Between the Growth of China's National Trunk Highway System and the U.S. Interstate System.

Data source: Chinese National Bureau of Statistics; Federal Highway Administration.

The Relationship Between Infrastructure and the Economy

The relationship between infrastructure and economic well-being is evident at the local, regional, national, and international scale. In fact, we could argue that without infrastructure, we wouldn't have an economy at all. And without infrastructure, a developing country has limited ability to grow its economy, as its economy is tied directly to its ability to move coal from mine to user, agricultural goods from rural farms to metropolitan markets, and light industrial products from factory to consumer. As a result, more international aid to developing countries is being directed to improvements in transportation infrastructure.

PBS Interview with Pennsylvania Governor Highlighting Economic Importance of Infrastructure

PBS Interview with Pennsylvania Governor Highlighting Economic Importance of Infrastructure

Of all infrastructure sectors, the transportation sector may have the largest impact on economic growth. Wayne Klotz, past president of the American Society of Civil Engineers (ASCE), stated “If we don't have the ability to transport people and goods, we don't have an economy.” Consider the economic benefits of a properly functioning transportation system as compared to an undersized or otherwise ineffective system:

- The cost to produce goods decreases, due to the decreased cost in obtaining raw materials.

- A properly functioning transportation system results in less congestion, which in turn results in fewer delays and lower fuel consumption.

- The cost of distribution of goods decreases.

- More households have access to more high-paying jobs. This in turn means that more tax revenue is being generated for the various levels of government. This is just one of the many ways in which infrastructure should be looked at as an investment by government. Some studies suggest a payback period to governments of less than 4 years for money spent on improving the transportation infrastructure.

Payback period is the ratio of project costs to annual savings. For example, if you pay $3,000 for a new furnace and it saves you $300 per year in heating cost, your payback period is 10 years.

- Potential homeowners have more freedom in housing choices, and greater choice and better access to health services.

- Rural areas can generate wealth by being connected to urban economies, leading to an overall increase in economic activity.

- Safer roads lead to fewer accidents, and accidents are costly to society. The cost to society due to accidents is more than $160 billion, more than twice that of the cost due to traffic congestion (AAA, 2008). Costs associated with accidents are estimated by assessing the costs of medical care, emergency and police services, property damage, and lost productivity and quality of life.

- Building roads creates jobs for construction workers and engineers, as well as other ancillary jobs (e.g., accounting, human resources, planning).

- Tourism is enhanced due to improvements in accessibility and connectivity.

Norway's Freight Rail System

Norway has identified a major infrastructure deficiency that has a significant impact on ) its economic growth: its freight rail system is not effectively linked to its ports. Shipped freight must be loaded on trucks for transfer to rail. However, once loaded on trucks, it is typically cheaper to continue by truck rather than rail to the final destination. Neighboring nations have better integrated their shipping and rail infrastructure and thus can potentially out-compete Norway for international business. Another drawback associated with ineffective freight rail is that the highway system experiences increased congestion from the truck traffic, as one train is equivalent to between 200 and 500 trucks. Additional advantages of rail include fuel efficiency (235 miles/gallon/ton of freight, approximately three times the efficiency of trucks), air pollutant emissions (approximately 10 percent of that from trucks on a ton of freight per mile basis), and safety (National Atlas, 2009).

These benefits were part of the rationale for the passing of the nearly $800 billion U.S. Recovery and Reinvestment Act (a.k.a. the “stimulus bill”) of 2009. It was apparent to the majority of legislators and the President that in the short term, spending money on infrastructure creates many jobs for transportation and construction workers (who were hit very hard by recession) as well as invests in an infrastructure that will create a more robust economy in the long term. A similar federal program, the Civilian Conservation Corps was instituted in 1933 as part of President Franklin D. Roosevelt's New Deal to provide employment opportunities during the Great Depression. National and state parks, roads, dams, and drainage canals were among the many projects completed by an estimated 3 million enrollees from 1933 to 1941.

Sources of Funds

Infrastructure components (e.g., roads, drinking water distribution systems) are most often owned by the federal, state, or local government rather than private corporations. The government may fund these projects using a variety of sources. At the most basic level, though, the taxpayer eventually pays the bill for any government-funded project.

President Roosevelt's Message to Congress, March 21,1933

“I propose to create a Civilian Conservation Corps to be used in simple work, not interfering with normal employment, and confining itself to forestry, the prevention of soil erosion, flood control and similar projects. I call your attention to the fact that this type of work is of definite, practical value, not only through the prevention of great present financial loss, but also as a means of creating future national wealth.”

FUNDING LOCAL PROJECTS

One method of funding municipal projects is through property tax revenues. For municipalities, these revenues are typically generated by property taxes levied on local properties. Property owners pay taxes based on assessed value. The rate of taxation is termed the “mill rate” and is often expressed as tax $/$1,000, or “tax dollars per thousand dollars of assessed value.” Therefore, a property with an assessed value of $100,000 in a municipality with a mill rate of $20/$1,000 would pay $2,000 in taxes annually.

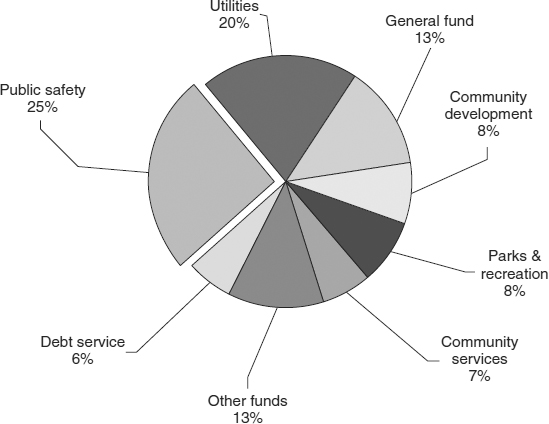

Property tax revenues are generated locally and must be divided among various departments in the municipality (including fire, police, water and sewer, streets, libraries, parks, recreation, museums, and a host of other services as well as administration) and pay for regional services such as schools, county services, and community colleges. School districts are typically the largest “consumer” of property tax revenues, accounting for approximately one-half of distributed funds. An example of operating expenses for a municipality can be viewed in Figure 14.3. Operating expenses do not include capital improvements such as building new roads or upgrading wastewater treatment facilities.

Figure 14.3 Distribution of Operating Expenses for a City. “Utilities” include streets, water, wastewater, and stormwater. “Community development” includes engineering, planning, and building.

Source: City of Lake Oswego, Oregon.

Services and projects can also be funded by user fees rather than by tax revenues. A toll on a toll road and state park entrance passes are examples of user fees. Many municipalities fund the operation and maintenance of water and wastewater treatment facilities and distribution systems via user fees paid to a water and sewer utility. Users pay a fee based on the number of gallons of wastewater generated or water used. This fee is normally set so that the income from users equals the expenses for operations and maintenance.

A utility is an organization that operates and maintains a portion of the infrastructure. The utility is either part of a municipal government, or may be a private business subject to governmental oversight. Examples include water, sewer, electric distribution, natural gas, and telephone.

Increasingly, municipalities are instituting stormwater utilities, whereby residents pay a stormwater user fee. Rather than pay a fee for gallons of stormwater produced (which cannot readily be metered), one method is to have property owners pay based on the amount of imperviousness (e.g., area of rooftop and pavement), since the amount of imperviousness is directly related to the amount of runoff produced. A stormwater utility removes stormwater management expenses from the general tax revenue pool and creates a separate “account.” This decreases the likelihood of cuts to stormwater infrastructure projects, as the expenditures are not directly competing with other needs funded by general tax revenue.

Special Assessments

Some infrastructure components may be funded through special assessments. For example, if water and sewer services must be extended to a new industrial park, a special assessment (sometimes termed a development impact fee) may be added to the cost of building permits to pay for the infrastructure.

Congestion Pricing

One innovative user fee is congestion pricing, in which automobile drivers must pay a surcharge when using certain roads during times of peak use. The rationale is that the surcharge will discourage some drivers from driving during peak times, thereby reducing congestion. Thus, the solution is to reduce the demand for extra roadway lanes rather than increase the supply. As such, it is a non-physical (non-structural) solution to the congestion problem. And it has the benefit of making users more aware of the actual costs they are incurring in using the roadway system. Congestion pricing is used in Europe but has not been implemented in North America for several reasons. For example, congestion pricing amounts to a tax, and few politicians are willing to champion such a policy. Nonetheless, several large U.S. cities are exploring this option.

Often the general tax revenues or user fees are not sufficient to fund infrastructure projects, and municipalities must resort to borrowing to fund their projects. Most often, they borrow by selling bonds. The advantage to borrowing is that a municipality can tap into a large amount of money to fund infrastructure projects that cannot be funded based on tax revenues in a given year. The drawback is that just like any borrowing (e.g., a home mortgage), interest is charged and must be paid back. For example, a $10 million infrastructure project may be too large for a municipality to fund in a single year. By borrowing that money at say a 5 percent interest rate and paying it back over 20 years, the municipality will only need to pay back $800,000 each year. However, that means that over 20 years, the municipality will be paying a total of $16 million for the $10 million project. The term debt service applies to payments made by municipalities on borrowed funds; this often accounts for a significant portion (6 percent in Figure 14.3) of annual budgets.

A bond is similar to a loan, and is a certificate of debt that is issued in order to raise money; the issuer is required to pay back funds over time.

Bond Ratings

Municipal bonds are sold to investors. Bonds are rated by credit agencies based on the likelihood of default, or inability to repay, as summarized in Table 14.1.

Municipalities and states desire high ratings, as higher ratings provide lower interest rates. When a state or municipality gets into financial trouble, its bond ratings drop and interest rates increase. The increasing rate may correspond to millions of dollars of additional interest payments.

The “grades,” or ratings, are deceiving when compared to letter grades that you are accustomed to as a student. The rating of “A” is far from excellent. In March of 2010, only two states, California and Illinois, had A ratings (all others were AA or AAA). Detroit, Michigan, and New Orleans, Louisiana, had ratings as low as BB, which is considered “junk” status. International headlines were made in August 2011 when the U.S. federal credit rating was downgraded from AAA to AA+.

Table 14.1 Bond Ratings as Defined by Standard & Poor's

| Likelihood of Default | Rating |

| Highest quality | AAA |

| High quality | AA |

| Upper medium quality | A |

| Medium grade | B |

| Somewhat speculative | BB |

| Low grade, speculative | B |

| Low grade, default possible | CCC |

| Low grade, partial recovery possible | CC |

| Default, recovery unlikely | C |

Municipalities also apply for grants (funds without obligation to repay) from the state and federal government. For example, the state may help fund a city's cleanup of a brownfield (contaminated) site for redevelopment, or installation of a bike path. Grants often require matching funds, whereby the city is required to provide a portion of the funding for a project. In terms of the infrastructure, federal or state governments also provide low interest loans to municipalities for some infrastructure projects.

Asset Management

The Federal Highway Administration defines asset management as a “systematic process of maintaining, upgrading, and operating physical assets cost effectively.” More and more infrastructure owners (including all levels of government) are undertaking infrastructure asset management projects to better guide their decision-making process concerning how to most effectively invest in the infrastructure. Asset management is carried out by public works officials, lawyers, accountants, and planners as well as by engineers. Asset management should address these six questions:

- What assets do you have and where are they?

- What is the remaining service life of your assets?

- What are they worth?

- What needs to be done to preserve your assets (repair, renewal, or replacement)?

- When do you need to do it and how much will it cost?

- How will you equitably distribute the cost burden among users?

Source: CDM.

One funding mechanism that is becoming increasingly popular is Tax Incremental Financing (TIF). TIF is best explained with an example. Consider a piece of property that is not developed. Undeveloped property generates limited revenue for the city, since the taxes generated are based on property value. However, if that land is developed, it will have a much higher property value and will thus generate much more tax revenue. The difference between current (undeveloped) tax and proposed (developed) tax revenues is the “increment” (the “I” in TIF). Of course, to transform the property from undeveloped land to developed land often requires an investment in infrastructure. The purpose of TIF is to borrow money in order to pay for the new infrastructure, and then repay the loan using the incremental tax revenue generated by the improved property.

For example, consider a 20-acre farm field on the edge of a municipality that has a mill rate of $20/$1,000. The farm field is valued at $200,000 and thus generates $4,000 per year in property taxes. A developer proposes to build a “big box” store on this property but cannot afford to pay $500,000 to build the needed infrastructure such as water mains and widening of the road. However, this store will be assessed at $10 million and thus will generate $100,000 in tax revenue annually, or an increment of $96,000 ($100,000 – $4,000) per year. To encourage this development, the city agrees to finance the necessary infrastructure through a TIF, rather than requiring the developer to incur the costs. The infrastructure investment can be readily paid off since the incremental amount of $96,000 can be used directly to pay off the loan needed for the $500,000 investment in infrastructure.

In addition to the creation of new jobs and an enhancement to the local economy, an advantage to the municipality is that all of the incremental taxes (new tax revenue generated) can be used by the municipality to repay the loan. Without a TIF, only a portion of the incremental tax revenue would go to the municipality. The remainder would go to support schools and perhaps other regional needs. Once the loan is repaid, the TIF is “closed,” and the future taxes will be apportioned to the other agencies. This highlights a drawback to the TIF, in that schools and governmental offices do not get a portion of the incremental tax revenues until after the TIF loan is repaid, yet may need to provide increased services due to the new development.

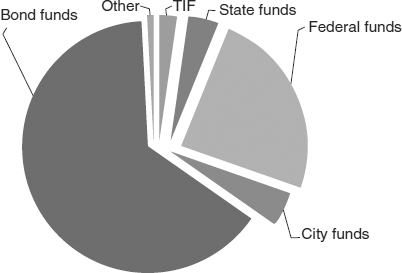

Thus, local governments have a variety of funding mechanisms to rely upon. This can be seen by re-examining the Capital Improvement Program (CIP) for Chicago that was introduced in Chapter 11, Planning Considerations. The funding sources for projects in the CIP are shown in Figure 14.4. As is typically the case, Chicago is relying very heavily on bonds to fund their infrastructure projects, with approximately 75 percent of the funds generated by bonds. The second greatest contribution is from federal funds.

Given that a community's revenues are based on the value of property in their community, it is tempting for communities to attract growth. However, a community should carefully consider the additional expenses incurred by the growth. For example, a successful industrial park will generate significant property tax revenue. But it may also require upgrades to wastewater treatment facilities, sewer lines, water treatment facilities, water mains, increased road capacity in the vicinity, additional police presence, expanded firefighting capability, etc. Also, it is possible that a new residential subdivision may cost more to support itself than it generates in tax revenue. Cost of community service studies seek to quantify the cost that various land uses generate as a means of helping communities plan future growth.

Figure 14.4 Funding Sources for Chicago's Capital Improvement Program (CIP) for 2010-2014.

Data source: City of Chicago, 2010.

Many consulting engineers spend a significant portion of their time helping clients procure funding for their projects. This may entail helping the client set up a TIF, or it may entail writing grant proposals to federal and/or state agencies. Engineers within each sub-discipline of civil and environmental engineering must be familiar with the current funding mechanisms available to their clients. They also must be proficient in writing clearly and persuasively. The stereotypical engineer seeks out a career in engineering because of strength in mathematics and science and a weakness in written and spoken communication. However, engineers seeking to rise to positions with more responsibility (and higher pay) find that it is essential to be excellent communicators in addition to having excellent technical skills.

FUNDING STATE AND FEDERAL PROJECTS

The discussion of the generation of funds and payment of projects has focused on municipalities to this point, but also applies to state and federal governments. State and federal governments also borrow and debt service comprises 8.5 percent of the 2009 U.S. federal budget. Sales taxes, gasoline taxes, income taxes, vehicle registration fees, “tourist” taxes (e.g., hotels) and alcoholic beverage taxes are among the many types of taxes upon which state and federal governments rely.

Federal and state budgets often contain a “transportation fund,” used to fund the various subsectors and components of the transportation infrastructure sector. This transportation fund is funded by gasoline taxes that are factored into the cost of gasoline at the pump. The federal gasoline tax is $0.18/gallon, and states add on their own gasoline tax (ranging from approximately $0.10 to $0.40/gallon). The federal gas tax has not been adjusted for inflation in 20 years; by adjusting for inflation, the $0.18/gallon in 1990 should be $0.30 today.

Unfortunately, transportation funds are sometimes “raided” by legislators during budget shortfalls and used to pay for other services. Thus, tax revenues that were collected for road replacement, safety upgrades, and new road construction is diverted to non-infrastructure projects.

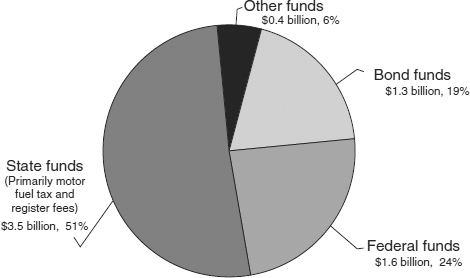

The source of funds for the Wisconsin DOT (Department of Transportation) is depicted in Figure 14.5. Wisconsin's gas tax ($0.33/gallons) is the largest funding source for transportation projects. Transfers of federal money to the state DOT is also a sizeable portion.

Figure 14.5 State of Wisconsin Funding Sources for Transportation Projects. The total budget is $6.8 billion for 2009-2011.

Data source: Wisconsin Department of Transportation.

Unlike the initial funding of the U.S. Interstate System, China is financing their National Trunk Highway System primarily through bonds to be paid back by tolls. This is seen by some as “risky,” as those provinces with less traffic (and therefore less tolls) may not be able to pay back the bonds.

Public works can also be managed and financed by the private sector. Many aspects of the infrastructure are privatized, including water and wastewater utilities and transportation components. The umbrella term for such privatization enterprises is public-private partnerships (PPP). PPP can come in many forms, but two common methods for financing infrastructure projects are operations and maintenance concessions and long-term leases.

With an operations and maintenance concession, a private company operates a public work. Such a partnership may be as simple as a municipality contracting roadside mowing rather than conducting this work using public employees, or as complex as contracting with a private water company to operate a municipality's drinking water treatment facility.

Long-term leases are becoming increasingly common. Two recent high-profile long-term leases are the Chicago Skyway toll road and the Indiana Tollway. The former is an 8-mile, highly traveled (50,000 vehicles per day) toll road, the lease for which was sold for $1.8 billion, whereas the latter is a 157-mile toll road that traverses the state of Indiana and was sold for $3.8 billion. As part of the lease agreement, the private companies can collect tolls in exchange for maintaining and operating the road. These two leases are long-term (99 and 75 years respectively). These leases were also noteworthy (and controversial) due to the fact that the leasers were foreign-based investment companies. However, these sources of funds are very attractive to states and cities that are struggling with budget shortfalls, as leasing the roadway provides a significant upfront payment that can be used for other infrastructure projects.

There is considerable debate currently over PPPs. One advantage of a PPP is that private firms can operate systems more cost-effectively and often have more technical and managerial expertise than may be available at the local government level. For example, a private company may operate several water treatment facilities, and hire one or two “experts” that can manage several facilities cost-effectively. Such on-staff experts, who would not otherwise be affordable to the municipality, are more able to respond to ever-changing regulations. On the other hand, the private sector is a profit-driven sector, which may lead to conflict with the not-for-profit perspective of a municipal government.

Overview Article on Privatization of Water Utilities

Design-Build as a Form of PPP

The vast majority of local infrastructure projects are delivered by the traditional design-bid-build method. In this method, the design is completed by an engineer and then the construction is awarded through a competitive bid process to a contractor, who then builds the project. An alternative project delivery method is design-build. Rather than an owner contracting out for design work of an infrastructure component separately from the construction (build) phase, these two are combined in design-build. Thus, the project owner (e.g., a county or city) can partner with a private firm, the latter which designs and builds the infrastructure component. This method can provide cost savings and other efficiencies in that the design-build provider can better design the component, knowing that they will also be in charge of building it.

Design-build has been expanded to design-build-operate, in which the private sector will also operate and maintain the component for a contracted period of time, perhaps 20 to 30 years after construction. Design-build and design-build-operate methods account for approximately 10 percent of infrastructure project delivery in the United States (ACEC, 2008).

Consideration of Project Economics

Engineering design nearly always requires the engineer and client to choose between several alternative designs. The scale of the decision may be between “simple” options such as choosing between light-emitting diode (LED) and mercury vapor street lights, or may be between complex treatment processes for a wastewater treatment facility. One criterion that is used to select the final design option in nearly every situation is cost. Given that sources of funding are typically limited and that competition for these funds can be quite intense, cost is often the most important criterion.

However, as we discussed in Chapter 10, Design Fundamentals, and will repeat in future chapters, economics is not the only criterion to consider; in other words, the lowest cost alternative is not necessarily the most appropriate choice. A client might select an option that is significantly more costly than the lowest cost option based on past experience, public acceptance (real or perceived), aesthetics, or sustainability.

When comparing multiple options, engineers have to make sure they are comparing the entire costs over the life of each project, not only the upfront costs. Upfront costs include the costs involved in initial purchasing of equipment and buildings as well as the cost to design, construct, and/or install the option. Other costs that must be considered are costs associated with operations, maintenance, rehabilitation, and replacement. In many cases, these costs can equal many times the upfront costs. Consequently, to compare among alternatives, a thorough accounting of all of the costs over the project's life span must be conducted, termed life-cycle cost. In many cases, the life span of the competing options will vary.

Consider choosing between a concrete road and an asphalt road. The concrete road will be much more expensive initially, perhaps twice the upfront cost of asphalt. However, the perspective changes when operations and maintenance costs are considered. For a time frame of 40 years for example, the asphalt road may need to be resurfaced twice while the concrete road requires minimal maintenance.

Environmental Life-Cycle Analysis (LCA)

The life-cycle cost analysis described in this chapter evaluates the quantifiable monetary costs associated with a project. An environmental life-cycle analysis (LCA) seeks to evaluate all of the environmental impacts associated with a product or process. This analysis is applied to the product or process from its “birth” (e.g., raw material extraction) to its ultimate disposal. Thus, it has a much longer viewpoint as compared to life-cycle cost assessment, which only includes capital costs, operations and maintenance costs, and abandonment.

Consider comparing a cloth diaper to a disposable diaper. For the cloth diaper, many environmental impacts exist. A few of these are fertilizer and pesticide use during growth of the cotton; wastewater discharges and air emissions at the facilities involved in the process of turning raw cotton into a diaper; greenhouse gas emissions in transportation; detergent use in laundering. For the disposable diaper, an LCA would inventory similar impacts as for the cloth diaper, with a major difference being that disposable diapers are made of plastics derived from petroleum or natural gas and do not degrade in landfills.

A similar analysis can and should be performed on many aspects of the infrastructure including asphalt versus concrete pavements; LED versus conventional street lights; solid waste incineration versus landfilling; mass transit versus automobile use. LCA is becoming a more common approach to evaluating design options, and in some cases is required by regulation. A senior vice president from a leading multinational engineering consulting firm recently stated, “Perhaps only 10% of our employees use LCA routinely, but all of our employees must understand LCA.”

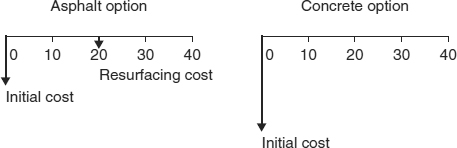

Figure 14.6 Cash Flow Diagrams for Asphalt and Concrete Pavement Options.

The upfront costs and operating costs can be presented in a cash flow diagram. In a cash flow diagram, revenues and expenses are represented as arrows. Expenses include initial investments and maintenance costs and are represented by arrows pointing down. Revenues include tolls, sales, and the salvage value at the end of use and are represented by arrows pointing up. The base of the arrow is placed at the end of the year in which the expense or revenue occurred, and the length of the arrow is proportional to the magnitude of the cost or revenue.

Consider Figure 14.6, in which cash flow diagrams comparing asphalt and concrete paving options are depicted. In year 0, both projects incur a large expense, the design and installation of the pavement. For the concrete project, this arrow is twice as long as the asphalt option. For this simplified example, no other costs are assumed for the concrete option, while the asphalt option incurs an additional cost in year 20, when resurfacing occurs.

Note that in Figure 14.6, all the arrows are pointing down. That is because these options only have expenses associated with them. If this road were a toll road, upward-pointing arrows would be used at each year to represent the annual revenue due to tolls.

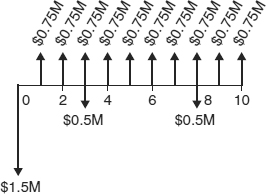

As another example, consider a cash flow diagram, from a developer's perspective, for developing a parcel of land into residential housing lots. The developer purchases the land for $500,000 in year 0. The cost of adding the infrastructure (roads, sewer, etc.) is $2.5 million. The project will be divided into three construction phases: $1 million will be spent on construction in year 0, $0.5 million in year 3, and $0.5 million in year 8. Lots are projected to sell at a steady rate of 15 lots per year for 10 years, at a cost of $50,000 per lot (equal to $750,000 each year). The cash flow diagram for this development scenario is provided in Figure 14.7.

But, how do we compare between the alternatives shown in Figure 14.6? How do we know which pavement type is most cost-effective? Or, how does the developer know how well the scenario shown in Figure 14.7 compares to other development options? It might be tempting to simply add up the arrows in Figure 14.6, but this would ignore an extremely important concept known as the time value of money.

Figure 14.7 Cash Flow Diagram for Residential Land Development Scenario.

To understand the time value of money, consider being given two options: you can receive a gift of $1,000 today or a gift of $1,000 in 10 years. Ignoring any effects of inflation, you would most certainly prefer to be given the $1,000 today. Having that money today allows you to use the money for investment or consumption purposes; this is the concept of the time value of money.

Now, consider being offered $1,000 today or $2,000 dollars in 10 years. If you are rational, you would consider how much interest you could earn in 10 years by investing the $1,000 today, and compare that value to the $2,000 option. If the initial $1,000 gift is predicted to grow to say $2,500, perhaps by investing in a bank certificate of deposit (CD), you will most likely accept the $1,000 today. (The term economic equivalence, or simply equivalence, describes the fact that, for this example, $1,000 today and $2,500 in 10 years are completely the same; in other words, if you were offered $1,000 today or $2,500 in 10 years, you would have to flip a coin to choose, if your only criteria was economic value.) This analysis, in which the value of two options is compared at some future time, is known as a future value analysis. For this example, we would say that the future value of the $1,000 gift is $2,500.

Creative (Desperate) Sources of Funding

Illinois was one of the hardest-hit states by the recent recession. Facing a $13 billion budget deficit in 2010 and a low bond rating, alternative sources of funding were sought. One alternative considered was to sell half of the $300 million that the state receives annually as part of a multi-state settlement with the tobacco industry. By doing so, Illinois would be giving up a fixed long-term revenue source for a lump sum to help solve current financial troubles. The State's Budget Director summarized the proposal by saying (to a hypothetical investor), “Will you trade me $1 billion now for the right to get $150 million a year?”

Conversely, you might consider a present value analysis. In this case, for a given interest rate, you would calculate how much the $2,000 in 10 years is equivalent to today; that is, you would calculate the present value of the future $2,000 gift. This can be accomplished by using Equation 14.1.

where

PV = present value

F = future value

i = interest rate

n = number of time periods

The units on the number of time periods (n) and the interest rate (i) should correspond. That is, if the interest rate used is an annual interest rate, the time period must be in years.

numerical example 14.1 Present Value Calculation

What is the present value of a $2,000 gift that you will receive in 10 years, using an interest rate of 5.00 percent?

solution

![]()

Therefore, $2,000 in 10 years is equivalent to $1,230 today for an interest rate of 5.00 percent.

A present value analysis can be readily applied to a cash flow diagram to compare among life cycle costs. This can be accomplished by computing the net present value, which is the difference between the sum of the present value of the revenues and the sum of the present value of the expenses (Equation 14.2).

where

NPVK = net present value

PVrevenues = present value of the revenues

PVexpenses = present value of the expenses

To use a net present value (NPV) analysis, the present values of all the expenses and revenues must first be calculated individually. When comparing alternatives, the NPV for various options can be computed; the option with the highest NPV is the best option in terms of economics.

numerical example 14.2 Present Value Analysis

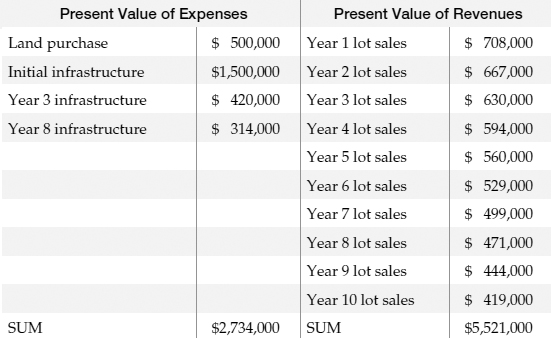

Conduct a present value analysis for the land development scenario presented in Figure 14.7. Use an interest rate of 6.00 percent for the analysis.

solution

The PV of all the expenses and all of the revenues must be individually calculated. A sample calculation is shown here for the present value of the $500,000 infrastructure expense in Year 3.

![]()

The remaining PVs are calculated in a similar manner and are summarized in Table 14.2; you should be able to confirm the values presented using a calculator or spreadsheet.

The sum of the present value of the expenses and the sum of the present value of the revenues is provided in Table 14.2. From this, Equation 14.2 can be used to compute the NPV of this development option.

![]()

So, this project has a positive NPV, which is most likely encouraging to a developer. However, it may not be a large enough NPV for a developer to decide to make the investment when considering the risk of declining property values or other economic uncertainties. For example, the recent housing market “bubble burst” had a tremendous impact on the U.S. economy. Housing demand, and thus demand for new development is cyclical (Figure 14.8) and not readily predictable. Many developers (and engineering companies relying on them for projects) went bankrupt or severely reduced the number of employees during the downturn of the housing market. For developers, there is a substantial financial risk when investing in land and infrastructure necessary for development.

Table 14.2 Present Value of Expenses and Revenues

Figure 14.8 New Housing Starts in the United States.

Data source: U.S. Census Bureau, 2010.

Now, we should reconsider Figure 14.6; neither of the options have any revenue. This is typical of infrastructure projects; projects for the public welfare do not necessarily generate direct revenue. Even though we have shown at the beginning of this chapter that they make a significant impact on the economy, these are difficult to show as “revenues” in a cash flow diagram, even if they could be calculated. For such public works projects, the NPV analysis is still applicable and the analyst would still select the largest NPV; in other words, the project with the least negative NPV would be the chosen alternative, ignoring other selection criteria.

Outro

This chapter has introduced you to two very important questions related to economics: “how will we pay for it?” and “which option is the least costly over the project life cycle?” Keep in mind that often, but not always, cost is not the most important criterion by which alternatives are compared.

Also, please reconsider Figure 14.2, which demonstrated the rapid increase in the extent of the Chinese expressway system. Note that according to this figure, expressway length has doubled in 5 years! There are many implications to this doubling that will affect the environment, society, human health, and welfare in potentially beneficial or adverse ways. These are each subjects of following chapters. For example, vehicle miles traveled will likely mirror this trend, as will associated traffic fatalities, fossil fuel consumption, tailpipe emissions, etc. Positive impacts include economic benefits noted in this chapter, most notably increased mobility and opportunity for Chinese citizens.

chapter Fourteen Homework Problems

- 14.1 Given an annual interest rate of 5.00 percent, how much is $500 today equivalent to in 10 years? In 1 year? In 100 years?

- 14.2 Given an annual interest rate of 7.00 percent, how much is $1,700 today equivalent to in 10 years? In 6 months? In 18 months?

- 14.3 Given an annual interest rate of 5.00 percent, how much is $5,500 in 10 years equivalent to today? What if the interest rate is only 0.5 percent?

- 14.4 Given an annual interest rate of 3.00 percent, how much is $45,000 in 6 months equivalent to today? What if the interest rate is only 0.500 percent?

- 14.5 How much should you place into a 5-year certificate of deposit (CD) bearing 3.00 percent annual interest in order to have the CD worth $6,000 in 5 years?

- 14.6 If you place $600 from your first paycheck into a Roth IRA earning 4.00 percent annual interest, how much will it be worth when you withdraw it in 40 years?

- 14.7 Repeat the previous problem, except now take $100 from each of your first 12 monthly paychecks and determine what they will collectively be worth in 40 years.

- 14.8 A certain wastewater treatment unit process costs $50,000 to purchase and install, and will cost $500 per year to operate. Given an interest rate of 4.00 percent, what is the net present value of this scenario?

- 14.9 Reconsider Numerical Example 14.2. What would the net present value be if lots took twice as long to sell (i.e., $375,000 in lot sales each year) for 20 years.

- 14.10 Reconsider Numerical Example 14.2. What would the net present value be if lots sold at the same rate but the sales price was $40,000 per lot instead of $50,000 per lot?

- 14.11 Reconsider Numerical Example 14.2. What if the designer did not design the subdivision such that it could readily be constructed in phases? Rather, the construction of the entire subdivision infrastructure must occur in a single phase. How does this affect the NPV?

- 14.12 Why might it not be a good idea for a community to grow?

- 14.13 List five ways that the quality of the transportation infrastructure affects the economy.

- 14.14 List one benefit and one drawback for a municipality to take out a bond to fund a project.

- 14.15 Compare an environmental life-cycle analysis (LCA) to a life-cycle cost analysis.

- 14.16 Explain the concept of equivalence.

- 14.17 What do the upward-pointing arrows on a cash flow diagram represent? The downward-pointing arrows?

- 14.18 Describe the infrastructure in your community that supports bicycle use. If you were to assign this infrastructure a grade, what grade would you give? List the criteria you used to assign this grade. How would improving this infrastructure help the economy?

- 14.19 Describe the infrastructure in your community that supports automobile use. If you were to assign it a grade, what grade would you give? List the criteria you used to assign this grade. How would improving this infrastructure help the economy?

- 14.20 Do you agree with this quote from the chapter? “If we don't have the ability to transport people and goods, we don't have an economy.” Give some reasons why someone might agree with this statement and some reasons why someone might disagree.

- 14.21 Do you think public-private partnerships (PPPs) are a good idea? Give three benefits and three drawbacks to the private acquisition of the Indiana Tollway discussed in this chapter.

- 14.22 As introduced in Chapter 5, stormwater detention ponds are used to store excess runoff and release it in a controlled manner. What are the life-cycle costs associated with a detention pond?

- 14.23 Research the use of permeable pavements. Explain how they work and provide a typical cross-section. What are the life-cycle costs associated with permeable pavement? Limit your response to one page.

- 14.24 How might the environmental impacts of an asphalt pavement compare to the environmental impacts of a concrete pavement? List and describe at least five environmental impacts for each. List your sources.

- 14.25 Use the Internet to determine the current value of the U.S. debt. List your source(s). Express this debt as a $/person.

- 14.26 How does your state fund transportation projects? What are the sources of funds? How much is spent? What other interesting information did you find when researching this topic? Limit your response to one page.

- 14.27 How does your state fund wastewater treatment projects? What are the sources? How much is spent? What other interesting information did you find when researching this topic? Limit your response to one page.

Key Terms

- bonds

- cash flow diagram

- cost of community service

- debt service

- design-bid-build

- design-build

- design-build-operate

- economic equivalence

- equivalence

- future value

- grants

- life-cycle analysis (LCA)

- life-cycle cost

- long-term leases

- matching funds

- net present value

- operations and maintenance concessions

- payback period

- present value

- public-private partnerships (PPP)

- tax incremental financing (TIF)

- time value of money

- user fees

- utility

References

American Automobile Association (AAA). 2008. “Crashes vs. Congestion -What's the Cost to Society?” http://www.aaanewsroom.net/Assets/Files/20083591910.CrashesVsCongestion FullReport2.28.08.pdf, accessed August 29,2011.

American Council of Engineering Companies (ACEC). 2008. Design & Construction Industry Trends Survey, 2008-2009. Washington, DC.

CDM. Infrastructure Asset Management—A Practical Guide for Utility and Public Works Directors. http://www.cdm.com/NR/rdonlyres/163702E9-1399-45CB-AE71-12574E632247/0/APracticalGuidefor UtilityandPublicWorksDirectors.pdf, accessed September 23, 2010. City of Chicago. 2010.

City of Chicago 2010-2014 Capital Improvement Program. http://www.cityofchicago.org/content/dam/city/depts/obm/supp_info/CapitalImprovementProgram2010-2014.pdf, accessed August 29, 2011.

City of Lake Oswego: Finance Web Site. http://www.ci.oswego.or.us/FINANCE/Budget05-07/Message.htm accessed August 29, 2011.

National Atlas of the United States. 2009. Overview of U.S. Freight Railroads. http://www.nationalatlas.gov/articles/transportation/a_freightrr.html, accessed September 23, 2010.

U.S. Census Bureau. 2010. The 2010 Statistical Abstract: Construction & Housing: Authorizations, Starts and Completions. http://www.census.gov/compendia/statab/cats/construction_housing/authorizations_starts_and_completions.html, accessed September 23, 2010.