CHAPTER 2

Fund Management within Shariah-Compliant Investment Guidelines

Is There More Reward?

In contracts, intentions and meanings, not words and structures, shall be taken into consideration.

(Islamic legal maxim)8

INTRODUCTION

“Could the financial crisis have been prevented if the financial world had followed the rules of Islamic—or Shariah—law?” This was the question asked by BaFin President Dr. Elke König in her opening remarks at BaFin’s second Islamic Finance Conference in Frankfurt. Dr. König’s professional career had also led her into the world of insurance. There she had come into contact with a particular branch of Islamic finance—the form of Shariah-compliant insurance known as Takaful. “At that time I found myself faced with a world that at first seemed alien to me, but which on closer inspection wasn’t so very different at all from what I had known up until then,”1 Dr. König said. This demonstrates that when one lifts up the car hood to closely examine the engine of Shariah principles that drive Islamic finance products, one finds that it’s not so different from what we know in the conventional world.

There has been surge in demand for Shariah-compliant asset management from institutional and private clients in the last decade, especially in the Gulf Cooperation Council region. The increasing demand is partly driven by the rapid rise in the region’s wealth and also by the increasing number and breadth of asset classes now available for Islamic investors, spurred by positive outlook of Shariah-compliant instruments. Perhaps another important factor behind the powerful growth of the Shariah-compliant funds industry lies in the simple fact that Muslims represent about a quarter of the world’s population. Therefore, the growth in Shariah-compliant investment funds has created an enormous market demand for asset management, which encompasses both fund management and discretionary portfolios services for institutions and individuals of high net worth.

Accordingly, International Banks such as HSBC, Citigroup, Deutsche Bank, UBS, and Standard Chartered have seized opportunity to adapt their existing asset management services to the needs of investors in Islamic finance industry. They have appointed their own board of Shariah scholars to assure their clients that the services they offer are indeed Shariah compliant. For private banking clients, this might involve the management of trust, established for tax or inheritance reason. Shariah compliance within all of these areas poses interestingly difficult but solution-driven challenges. Fund management is a good starting point for investors to understand how performance and faith investing is derived on more than 700 Shariah-compliant funds available for retail investors globally.2 This includes activities involving treasury/cash management and investment portfolio services, including the holding of the Islamic Sukuk securities, which will be reviewed later, as these are crucial for both retail and institutional clients globally.

The focus of this chapter is on understanding how an Islamic fund manager manages funds aligned with Shariah principles. Shariah-compliant investment is based on five financial Islamic principles, the purpose of which is primarily to promote ethical business practices resulting in positive impact on the economy.

Following are the five core principles that lie at the heart of Islamic finance; prohibited items are shown as (-):

A Shariah supervisory board is appointed to validate whether an investment products, service, or transaction is Shariah compliant. In most cases, this is done through a Shariah board using religious ruling, assisted by a scholarly opinion (fatwa) derived from Islamic law. Prior to their decision for investing in Islamic financial instruments, investors should make sure the investment is Shariah compliant.

For Muslims, the usage of Islamic financial products is a religious requirement. Violating any of the five prohibited Shariah principles is considered a serious offense in Islam. However, this should not be a deterrent for non-Muslims, since religious beliefs and laws are not only about religion but also about daily matters concerning various aspects of life, and the financial aspect is one of them. Shariah is one of the means for promoting basic principles of Islamic finance, which inter alia include transparency, ethics, and fairness, as well as promoting entrepreneurial spirit and risk undertaking and sharing between financiers and customers. Hence, investors need not be Muslim to realize and appreciate the healthy principles of Islamic finance.

Principles in Islamic finance are similar to the values emphasized in ethical and green investment, which steer clear of investment activities associated with wine, weapons, and activities that may be harmful to the environment. Islamic principles of finance strongly emphasize fairness while conducting trade and business by maintaining transparency and truthfulness in any transaction. Misrepresentations of any information, and indulging in excessive debt or leverage, are strongly discouraged. Preservation of environment as God’s bounty to humans and avoiding doing harm to others are principles deeply embedded in its roots. So managers of Islamic funds have a moral, as well as legal, obligation to ensure that investors have clear and reliable information about how their investments are being deployed.

THE APPLICATION OF ISLAMIC ETHICS TO ASSET MANAGEMENT

Islamic ethics do not just apply to Muslims’ personal lives but equally to all other aspects, including the way they conduct business. The high level principles, such as stewardship of humanity on Earth, integrity, sincerity, piety, justness in exchange, and righteousness and perfection at work, provide the basis for a framework of business ethics.3 These are reflected in a set of behavioral norms and values, such as honesty and fair trade; disclosure and transparency; and avoiding misrepresentation, selling over and above the sale of another, forbidden items, hoarding, sale of goods and assets in the open market, or taking advantage of a seller’s helplessness.4

Islamic fund management is grounded by Islamic finance principles, which express explicit intention to meet the financial needs of participants with integrity and in a manner that is tangible, fair, trustworthy, and honest, while ensuring a more equitable wealth distribution. All Shariah-compliant assets embrace the following key principles:

- Materiality and validity of transactions

- Mutuality of risk sharing

- Investment based on social and moral values

Materiality and Validity of Transactions

Islamic finance encourages investing in business activities that are founded on real, productive, or trade-related activity and that generate fair and legitimate profit. There must be a close link between the financial and productive flows that underpin Islamic finance. This ensures the funds are being invested into real assets and companies rather than exotic investments, such as conventional derivatives, that are not directly linked to the underlying assets. This has had the effect of insulating the Islamic financial system from risks associated with excessive financial leverage and speculative activities in recent years.

A central feature of the Islamic financial system is the prohibition of the payment and receipt of riba, or interest. Riba refers to an increase or excess that accrues to the owner in an exchange or sale of a commodity, or by virtue of a loan arrangement, without providing any equivalent value to the other party. Money in Islam is not a commodity. The prohibition of interest arises from the fact money is perceived only as a medium of exchange, a store of value and unit of measurement. It possesses no intrinsic value.

As such, Islamic bonds, or Sukuk, do not pay interest like conventional bonds, but pay coupons in a different manner such as rent or profit. Sukuk are trust certificates or participation securities that grant investors a share of an asset along with the cash flow or profit and risks commensurate with such ownership. This differs from conventional bonds, which are based on the exchange of paper for money with interest imposed to measure returns and liabilities. This is also the essence of the principle of no profit sharing without risk sharing (alghunm bi-’l-ghurm). That is to say, the earning of profit is legitimized only by engaging in an economic venture that contributes to the economy.

Mutuality of Risk Sharing

The principle of fairness is also reflected in the risk- and profit-sharing characteristics of Islamic financial transactions. This requirement must be clearly defined at the onset and serves as an additional built-in mechanism that promotes the adoption of sound risk management practices by financial institutions engaged in Islamic finance.

The exercise of appropriate due diligence and higher standards of disclosure and transparency must be observed by financial institutions, which, in turn, enforces market discipline and minimizes informational asymmetries.

In Islamic finance, all forms of contracts and transactions must be free from gharar (uncertainty). Terms and conditions should clearly specify the following:

- The roles of the parties

- Date of payments to be made

- Quantity and quality of goods to be exchanged

All this must be honestly and clearly laid out. Ambiguity or uncertainty in contracts is prohibited because it could lead to interpretational differences that may provide an advantage to one party over another. To avoid potential conflicts in Islamic financial transactions, any element of uncertainty is to be strictly avoided.

Investment Based on Social and Moral Values

Although the principles of Islamic finance are explicitly defined in Islamic law, the net effect is ethical business activities and practices. Similar to socially responsible investing, Shariah-compliant investment filters out businesses engaging in activities deemed unacceptable, such as alcohol, tobacco, pornography, gambling, armaments, and so on. Islamic asset management is a social and moral values-based investment alternative that is for the most part compatible to a conventional values-based investment approach that mandates social values and good governance.

BENEFITS OF SHARIAH VIS-À-VIS CONVENTIONAL INVESTING

The Shariah-compliant investment industry is still developing, but it is growing at a very rapid pace. In fact, it is one of the fastest-growing sectors within the worldwide financial system. It is estimated that there are globally USD60 billion to USD65 billion5 Shariah-compliant assets under management. Shariah-compliant investing is not just for investors of the Islamic faith. Investors of all stripes are drawn to such values-based investing. Likewise, investments are not limited to Islamic companies, but any company that engages in acceptable activities. Besides the socially responsible motivation, reasons for non-Islamic investors to invest according to Shariah principles include the following.

Comparable Returns to Conventional Investments over Longer Periods6

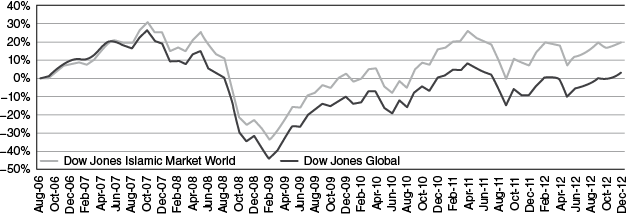

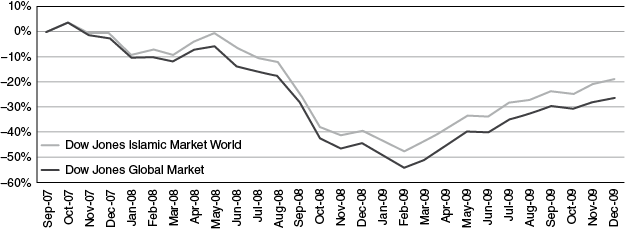

Although Islamic investments may outperform or underperform conventional investments over shorter periods, as can be seen in Figure 2.1 (and Table 2.1) and Figure 2.2, over longer periods their returns are comparable with those of conventional investments. In fact, over the last five years the Dow Jones Islamic Market World Index (DJIM World) outperformed the Dow Jones World Index (DJ World) by 9.91 percent, returning 3.83 percent compared with –6.08 percent. The same can be said for the period between October 2007 and March 2009, the worst bear market in decades, when the DJIM World reported –43.21 percent compared to –50.48 percent for the DJ World (Table 2.2).

Figure 2.1 Dow Jones Global versus Dow Jones Islamic World

Table 2.1 Dow Jones Global versus Dow Jones Islamic World

Table 2.2 Eighteen Months Bear Market

Apart from the core principles, Islamic finance related transactions edges out of conventional because of the following factors:

- Greater stability of returns. Shariah-compliant equities are less volatile than their conventional counterparts, both in times of crisis as well as in times of stability. One reason for this is because excessive financial leverage is prohibited.

- Embedded risk management. To be considered Shariah-compliant, equities must pass a rigorous screening process, which ascertains, among other things, whether the underlying companies are sufficiently capitalized to weather difficult times and liquid enough to meet short-term obligations. This process sets strict limits for various financial ratios, such as debt to total market capitalization or debt to total assets to limit leverage, and cash to market capitalization or cash to total assets to ensure sufficient liquidity and productive use of cash. Because of such rigorous screening, the underlying companies were better capitalized and more liquid than many of their conventional peers. Therefore, they were less exposed to the deleveraging, extreme solvency, liquidity concerns, and the consequent sharp price declines experienced by these peers during the global financial crisis.

- Bonds backed by real assets. Sukuk (Islamic bonds) are asset-based or asset-backed: There is an asset (or pool of assets) underlying every transaction, and the ownership of that asset or pool is transferred to investors. Thus, investors enjoy all rights and obligations that accompany ownership. In asset-backed structures, Sukuk holders have recourse to the underlying assets.

- Greater transparency. Since transactions and contracts must be free of uncertainty, terms and conditions clearly defined at the outset, Shariah-compliant investments may produce more predictable results.

- Diversification. While they are highly correlated, Shariah-compliant investments limit the downside slightly better than conventional investments do. As shown in Figure 2.2, during the recent bear market, Islamic funds fared better period than conventional portfolios did, declining less, experiencing lower volatility and recovering nearly as much ground lost as the markets have recovered.

Figure 2.2 Performance during the bear market period

Source: CIMB-Principal Islamic Asset Management (Case for Islamic Asset Management as of July 31, 2012)

Holistic Islamic Fund Management

The popular definition of Islamic asset management deems that an investment manager is mandated to invest only in Shariah-compliant investment instruments. CIMB-Principal Islamic Asset Management (a prominent Islamic asset manager in Malaysia) advocates for a much broader definition of Shariah-compliant investing, going beyond the investment screening process to ensure that all aspects of the investment management operations are Shariah-compliant.

The organizational structure identifies a variety of roles and responsibilities that are designed and structured in such a way as to ensure segregation of duties, generally divided into investments, operations, and compliance and risk management, with appropriate corporate governance in place to avoid conflicts of interest.

Identical to a conventional asset manager, an investment team is headed by a chief investment officer and supported by portfolio manager(s) and analyst(s) who understand the concept of Islamic asset management. Conventional asset management investment mandates are usually transparent with respect to investment objectives, general constraints on risk parameters, investment style, and adherence to benchmark performance, investment universe, investment restrictions, counterparty restrictions, delegation to third-party fund managers, and reporting. In addition, the general constraints for a Shariah-compliant investment mandates will have a reference to the fact that all investments and assets must be Shariah-compliant.

The asset management company needs to work with a variety of partners to ensure that operations and processing work efficiently and effectively, with sufficient controls in place. The investment team will work with a selection of brokers and counterparties on executing investment decisions. The company’s operations and accounting team will work externally with a custodian on subscription, redemption, payment, and reporting processes. All partners and their processes will need to be Shariah-compliant.7

Shariah compliance of the asset management company is part and parcel of a holistic compliance culture. In the interest of investors’ protection, reporting and disclosure follow global best practices. Identical to conventional asset management companies, Shariah-compliant compliance and risk management requirements will naturally include the know-your-client (KYC) practices, as well as controls to prevent insider trading and financial crime (e.g., money laundering, tax evasion, and fraud).

Like conventional asset management, Islamic asset management still incurs liquidity, credit, settlement, leverage, operations and business risks. However, these companies can and do successfully operate based on current international financial regulations, while still remaining Shariah compliant.

Employing Islamic Ethics for Permissible Investment

Islamic equities are screened at the operational level to ensure that business qualifies as Shariah compliant. Broadly, screening is based on industry type, financial ratios, and tolerable benchmarks. Islamic bonds (Sukuk) are determined to be Shariah compliant predominantly based on their financing structure. As mentioned earlier, Sukuk grant investors a share of the underlying asset, along with the associated profit and risks, rather than paying interest like conventional bonds. Additionally, proceeds from Islamic bonds (Sukuk) issuance must be used in Shariah-compliant activities, which reflect their usage for productive real economic activities.

In situations where adverse market changes, mergers and acquisitions, or change in principal business activity occurs, Islamic equities can become noncompliant. When this happens, the asset management house will have to divest or sell the stocks. Divestment is typically allowed to occur over a period of time to ensure that investors are not unnecessarily disadvantaged. If the stock price is currently below the cost of investment, it is encouraged that the divestment be done when the affected stock(s) reaches breakeven of the total cost. However, if there are profits derived from the divestment of these nonpermissible investment, this profit will need to be purified via charitable contributions.

Sukuk are Shariah-compliant contracts by definition, as all the monies raised with the issuance of Sukuk are primarily used to purchase permissible assets outright for regular rental income. Therefore, a Sukuk is unable to become nonpermissible during its tenure.

Shariah Governance for Investment

Governance for Islamic asset management services extends to the Shariah compliance of the asset management company. For instance, the Securities Commission of Malaysia, the world’s first country to have a full-fledged Islamic financial system, operates in parallel to the conventional banking system and has mandated the following requirements:

- Shariah adviser appointed at company level

- Shariah adviser appointed at fund level, if offering retail products

- Dedicated Shariah-compliance officer reporting directly to the Shariah advisor and board

- Fund management organization with adequate knowledge of Islamic fund management

These guidelines may vary from country to country but are viewed as a benchmark within the industry. Finally, the investment manager must have processes in place to handle investment securities that may turn “noncompliant” due to various reasons. This is called the purification process. In Malaysia, there is a clear guideline on the purification process. In some countries, the purification may even be done at dividend level, where the “non-Shariah” portion is purified by divesting it to charity.

Islamic Advisory

One of the key success factors of Islamic asset management is the investment manager’s appointed Shariah adviser. The Shariah adviser must have a robust and institutionalized advisory process in place to enhance the integrity of its Shariah decisions. To ensure its Shariah interpretations are practicable, the concerned person must have traditional capital markets, investment, and product development experience. The adviser must also be familiar with the differences in Shariah interpretation in different jurisdiction. Finally, to promote universal acceptability of its decisions across regions, the Shariah advisory board must ensure its Islamic scholars are of diverse backgrounds ranging across different jurisdictions.

CONCLUSION

Shariah-compliant investing is growing rapidly as an alternative investment class for all investors, both Muslim and non-Muslim, mainly for its foundation in ethical business practices, social responsibility, and fiscal conservatism. Although Islamic clients may be mandated to invest only in a Shariah-compliant manner, other investors do so for the benefits they derive from greater stability of returns, transparency, and diversification.

Islamic finance encourages investing in business activities that generate fair and legitimate profit. The principle of fairness is also reflected in the risk- and profit-sharing characteristics of Islamic financial transactions. Similar to socially responsible investing, Shariah-compliant investment filters out businesses engaging in activities deemed nonpermissible, such as alcohol, tobacco, pornography, gambling, and armaments. Investors (Muslim or not) who choose this socially responsible form of investing will also enjoy comparable returns to conventional investing over longer periods (5 to 10 years). The investment performance of Shariah equity indices has been examined and found to offer diversification and relatively stable returns, with embedded risk management via a screening process.

For investors who value or are mandated to operate within Shariah law, it is important to have a trusted investment management partner experienced in both investment management and Shariah principles. A holistic Islamic asset management company will go beyond the investment screening process to ensure that all aspects of the investment management operations are Shariah-compliant. Shariah governance and compliance of the asset management company is part and parcel of a holistic compliance culture.

NOTES

1. www.bafin.de/SharedDocs/Veroeffentlichungen/EN/Fachartikel/fa_bj_2012-06_islamic_finance_en.html

2. KFH Research Ltd. and the Global Islamic Finance Forum (GIFF). “Global Islamic Finance Forum (GIFF).” Kuala Lumpur, Malaysia: September 18–20, 2012.

3. Natalie Schoon, Islamic Asset Management: An Asset Class on Its Own? University of Edinburgh Press, 2011.

4. Ibid.

5. KFH Research Ltd. and the Global Islamic Finance Forum (GIFF).

6. CIMB-Principal Islamic Asset Management, “Case for Islamic Asset Management,” July 31, 2012.

7. Natalie Schoon.

8. The legal maxim states the importance of substance in business and finance; hence it encourages the Islamic fund manager to manage funds as long as they are aligned with Shariah principles. When the fund is Shariah complaint, there is not much consideration given to the form and structure. The Shariah-compliant contract will have embedded benefits in its features and it will also realize Maqasid al Shariah (Objective of Shariah) by securing returns with less risk through transparency and stability in business.

General Reading

Dar, Humayon, and Mufti Talha Ahmad Azami, Global Islamic Finance Report (GIFR). An Edbiz Consulting Publication, 2011.

Jaffer, Sohail, Forming the Future of Shariah Complaint Investment Strategies. Euromoney Books, 2004.

Rahman, Yahia Abdul, The Art Of Islamic Banking and Finance. Tools and Techniques for Community-Based Banking. Hoboken, NJ: John Wiley and Sons, 2010.