This risk measure is an interval-based risk check. An interval-based risk is a counter that resets after a fixed amount of time and the risk check is imposed within such a time slice. So, while there is no final limit, it's important that the limit isn't exceeded within the time interval that is meant to detect and avoid over-trading. The interval-based risk measure we will inspect is maximum executions per period. This measures the maximum number of trades allowed in a given timeframe. Then, at the end of the timeframe, the counter is reset and starts over. This would detect and prevent a runaway strategy that buys and sells at a very fast pace.

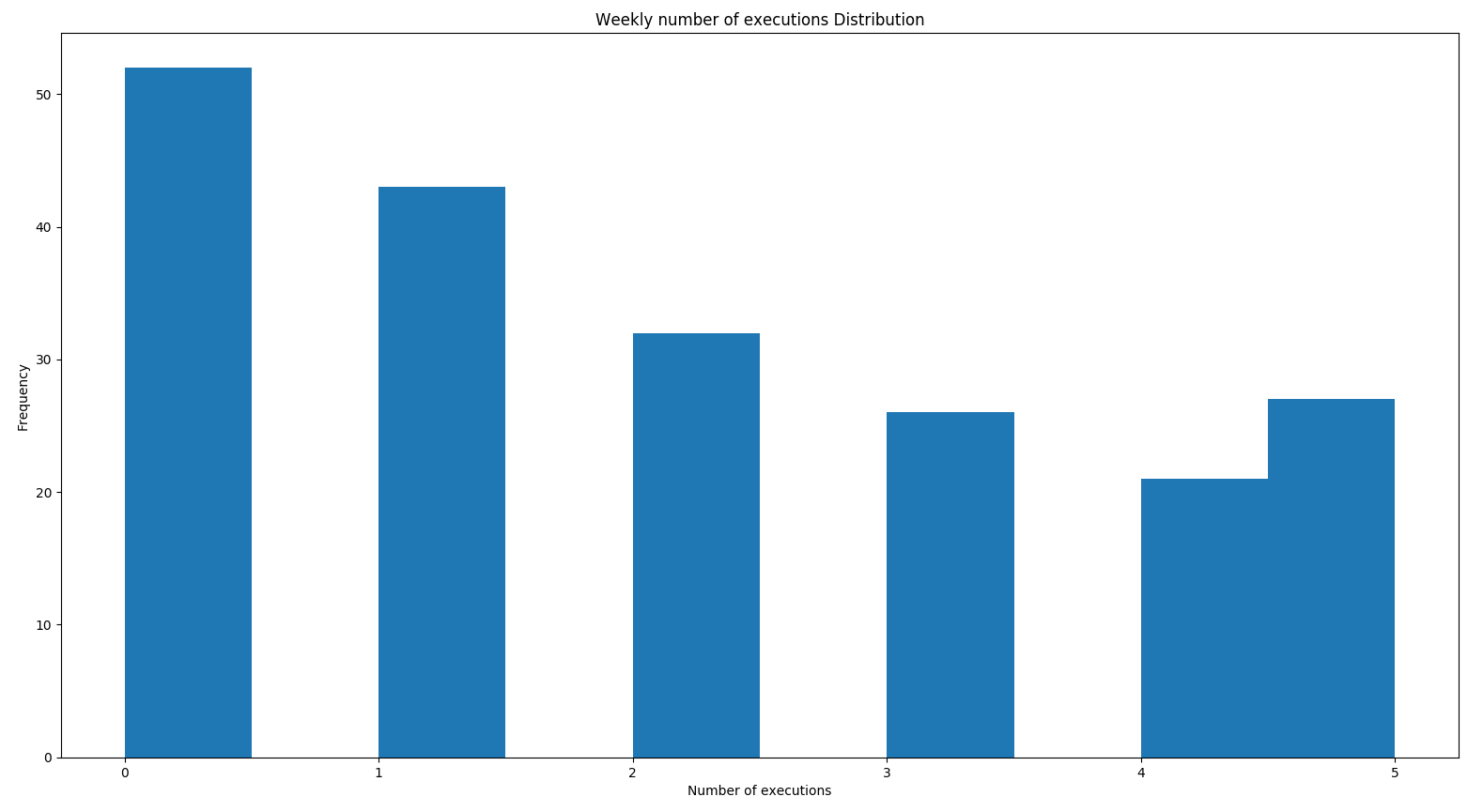

Let's look at the distribution of executions per period for our strategy using a week as our timeframe, as shown here:

executions_this_week = 0

executions_per_week = []

last_week = 0

for i in range(0, num_days):

if results['Trades'].iloc[i] != 0:

executions_this_week += 1

if i - last_week >= 5:

executions_per_week.append(executions_this_week)

executions_this_week = 0

last_week = i

plt.hist(executions_per_week, 10)

plt.gca().set(title='Weekly number of executions Distribution', xlabel='Number of executions', ylabel='Frequency')

plt.show()

The code will return the following output. Let's have a look at the plot:

As we can see, for this trading strategy, it's never traded more than five times a week in the past, which is when it trades every day of the week, which doesn't help us much. Now, let's look at the maximum executions per month:

executions_this_month = 0

executions_per_month = []

last_month = 0

for i in range(0, num_days):

if results['Trades'].iloc[i] != 0:

executions_this_month += 1

if i - last_month >= 20:

executions_per_month.append(executions_this_month)

executions_this_month = 0

last_month = i

plt.hist(executions_per_month, 20)

plt.gca().set(title='Monthly number of executions Distribution', xlabel='Number of executions', ylabel='Frequency')

plt.show()

The preceding code will return the following output. Let's have a look at the plot:

We can observe the following from the preceding plot:

- It is possible for the strategy to trade every day in a month, so this risk measure can't really be used for this strategy.

- However, this is still an important risk measure to understand and calibrate, especially for algorithmic trading strategies that trade frequently, and especially for HFT strategies.