Regime Predictive allocation is a technique that has been used by some advanced participants in recent years and is still something that is actively being researched. This studies the performance of different trading strategies as a function of different economic indicators and then builds machine learning predictive models that can predict what kinds of trading strategies and what product groups are most likely to do well given current market conditions. To summarize, this allocation method uses economic indicators as input features to a model that predicts trading strategies' expected performance in the current market regime and then uses those predictions to balance allocations assigned to different trading strategies in the portfolio.

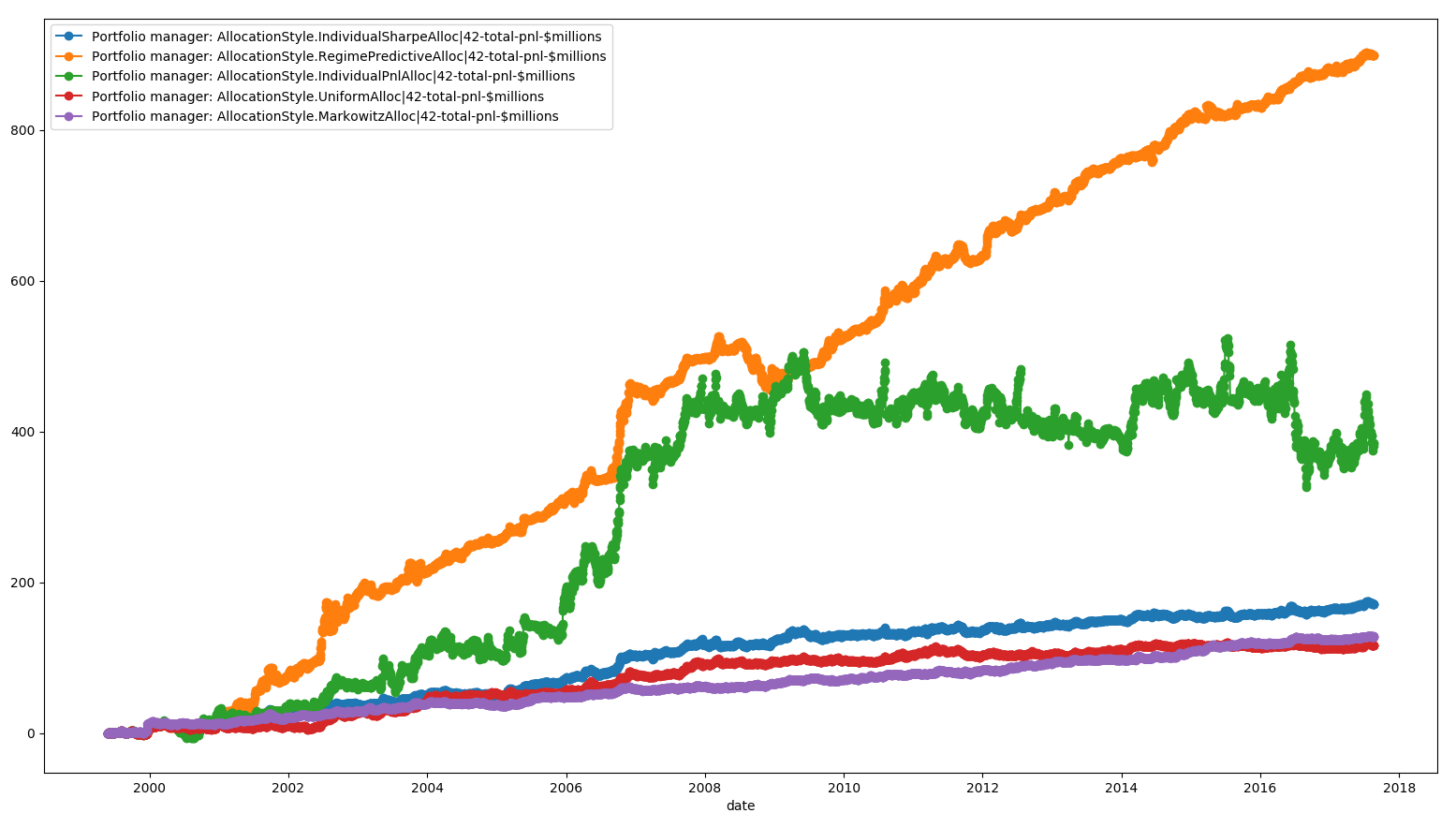

Note that this method is still able to allocate the largest risk to the best-performing strategy and reducing allocation on strategies that are performing poorly. This will make more sense when we compare it to all the different allocation methods covered in the following plot:

When we compare the different allocation methods next to each other, we can make a couple of observations. The first is that the Markowitz allocation method seems to be the one with the least variance and steadily rises up. The Uniform allocation method performs the worst. The Individual PnL-based allocation method actually has very good performance, with a cumulative PnL of around $400,000,000. However, visually we can observe that it has very large variance because the portfolio performance swings around a lot, which we intuitively expected because it doesn't factor for variance/risk in any way. The regime-based allocation method by far outperforms all other allocation methods with a cumulative PnL of around $900,000,000. The regime-based allocation method also seems like it has very low variance, thus achieving very good risk-adjusted performance for the portfolio.

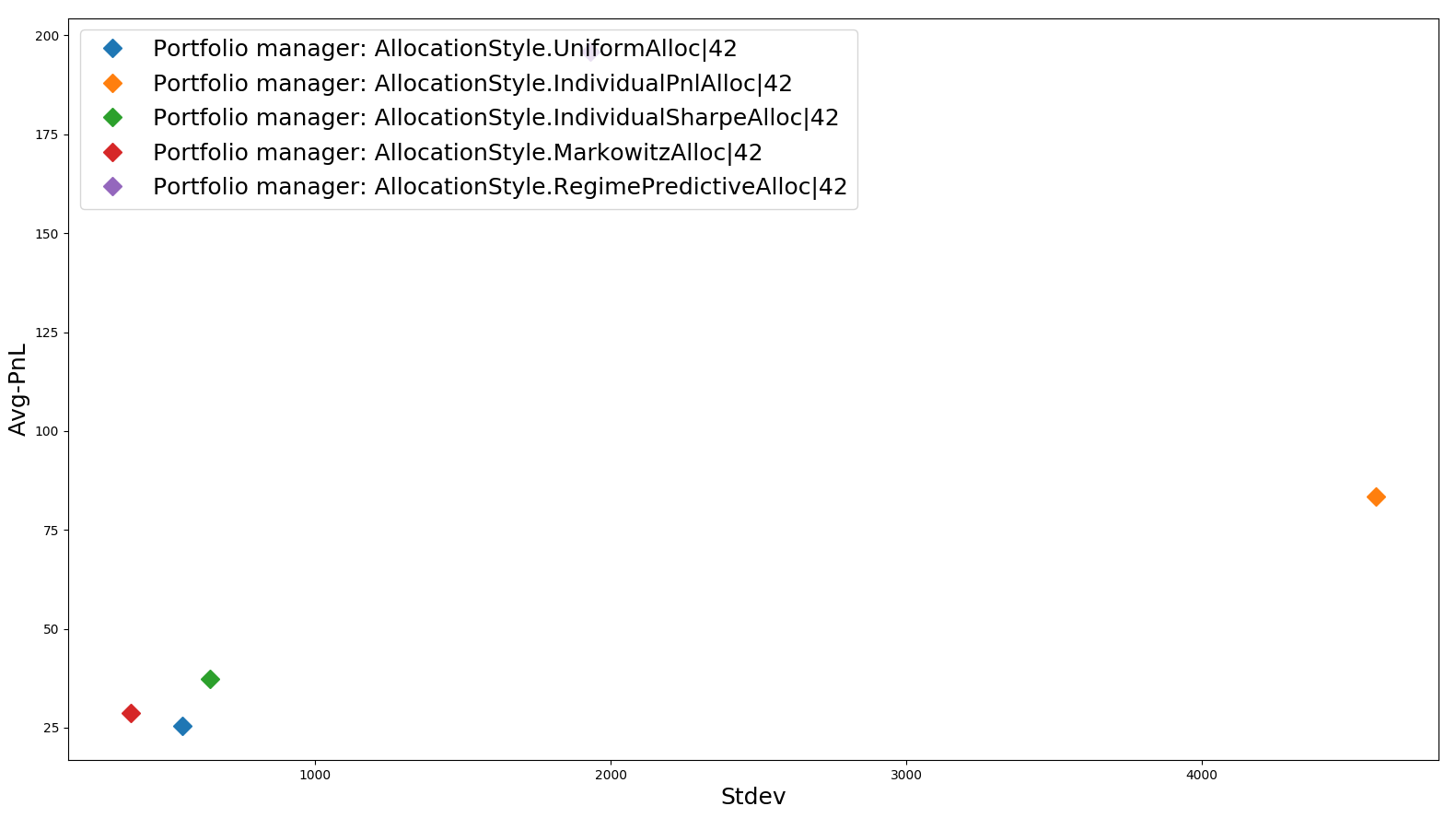

Let's look at the different allocation methods portfolio performance by comparing daily average portfolio performance with daily standard deviation of portfolio performance in the plot. We do this to see where each strategy-allocation method lies on the risk versus reward curve, which we could also extend to find the efficient frontier, as shown here:

We can make the following observations from the preceding plot:

- The avg-daily-PnLs and daily-risk are in $1,000 units.

- We immediately see that Markowitz allocation has the minimum possible portfolio risk/variance with an avg-PnL of $25,000 and risk of $300,000.

- The Uniform risk allocation method has lowest portfolio avg-PnL of roughly $20,000 but higher risk of $500,000.

- The individual PnL allocation has a very large avg-PnL of $80,000 but with much higher risk of $4,700,000, which would likely make it unusable in practice.

- The Regime predictive allocation method has a very high avg-PnL of $180,000 and relatively low risk of $1,800,000, making it the best-available allocation method in practice, thus also validating why it's an active research area right now.