Let's implement a moving average convergence divergence signal with a fast EMA period of 10 days, a slow EMA period of 40 days, and with default smoothing factors of 2/11 and 2/41, respectively:

num_periods_fast = 10 # fast EMA time period

K_fast = 2 / (num_periods_fast + 1) # fast EMA smoothing factor

ema_fast = 0

num_periods_slow = 40 # slow EMA time period

K_slow = 2 / (num_periods_slow + 1) # slow EMA smoothing factor

ema_slow = 0

num_periods_macd = 20 # MACD EMA time period

K_macd = 2 / (num_periods_macd + 1) # MACD EMA smoothing factor

ema_macd = 0

ema_fast_values = [] # track fast EMA values for visualization purposes

ema_slow_values = [] # track slow EMA values for visualization purposes

macd_values = [] # track MACD values for visualization purposes

macd_signal_values = [] # MACD EMA values tracker

macd_histogram_values = [] # MACD - MACD-EMA

for close_price in close:

if (ema_fast == 0): # first observation

ema_fast = close_price

ema_slow = close_price

else:

ema_fast = (close_price - ema_fast) * K_fast + ema_fast

ema_slow = (close_price - ema_slow) * K_slow + ema_slow

ema_fast_values.append(ema_fast)

ema_slow_values.append(ema_slow)

macd = ema_fast - ema_slow # MACD is fast_MA - slow_EMA

if ema_macd == 0:

ema_macd = macd

else:

ema_macd = (macd - ema_macd) * K_slow + ema_macd # signal is EMA of MACD values

macd_values.append(macd)

macd_signal_values.append(ema_macd)

macd_histogram_values.append(macd - ema_macd)

In the preceding code, the following applies:

- The

time period used a period of 20 days and a default smoothing factor of 2/21.

time period used a period of 20 days and a default smoothing factor of 2/21. - We also computed a

value (

value ( -

-  ).

).

Let's look at the code to plot and visualize the different signals and see what we can understand from it:

goog_data = goog_data.assign(ClosePrice=pd.Series(close, index=goog_data.index))

goog_data = goog_data.assign(FastExponential10DayMovingAverage=pd.Series(ema_fast_values, index=goog_data.index))

goog_data = goog_data.assign(SlowExponential40DayMovingAverage=pd.Series(ema_slow_values, index=goog_data.index))

goog_data = goog_data.assign(MovingAverageConvergenceDivergence=pd.Series(macd_values, index=goog_data.index))

goog_data = goog_data.assign(Exponential20DayMovingAverageOfMACD=pd.Series(macd_signal_values, index=goog_data.index))

goog_data = goog_data.assign(MACDHistorgram=pd.Series(macd_historgram_values, index=goog_data.index))

close_price = goog_data['ClosePrice']

ema_f = goog_data['FastExponential10DayMovingAverage']

ema_s = goog_data['SlowExponential40DayMovingAverage']

macd = goog_data['MovingAverageConvergenceDivergence']

ema_macd = goog_data['Exponential20DayMovingAverageOfMACD']

macd_histogram = goog_data['MACDHistorgram']

import matplotlib.pyplot as plt

fig = plt.figure()

ax1 = fig.add_subplot(311, ylabel='Google price in $')

close_price.plot(ax=ax1, color='g', lw=2., legend=True)

ema_f.plot(ax=ax1, color='b', lw=2., legend=True)

ema_s.plot(ax=ax1, color='r', lw=2., legend=True)

ax2 = fig.add_subplot(312, ylabel='MACD')

macd.plot(ax=ax2, color='black', lw=2., legend=True)

ema_macd.plot(ax=ax2, color='g', lw=2., legend=True)s

ax3 = fig.add_subplot(313, ylabel='MACD')

macd_histogram.plot(ax=ax3, color='r', kind='bar', legend=True, use_index=False)

plt.show()

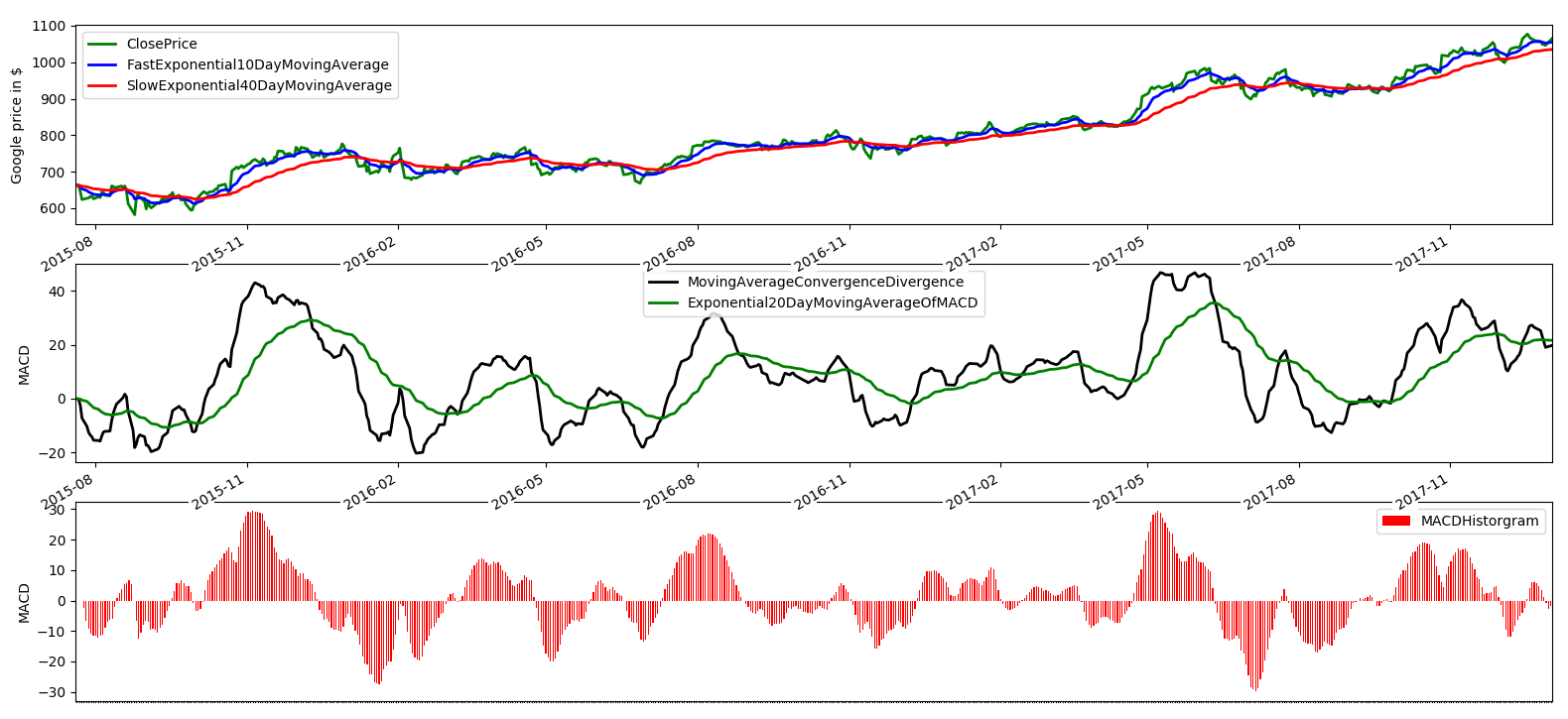

The preceding code will return the following output. Let's have a look at the plot:

The MACD signal is very similar to the APO, as we expected, but now, in addition, the  is an additional smoothing factor on top of raw

is an additional smoothing factor on top of raw  values to capture lasting trending periods by smoothing out the noise of raw

values to capture lasting trending periods by smoothing out the noise of raw  values. Finally, the

values. Finally, the  , which is the difference in the two series, captures (a) the time period when the trend is starting or reversion, and (b) the magnitude of lasting trends when

, which is the difference in the two series, captures (a) the time period when the trend is starting or reversion, and (b) the magnitude of lasting trends when  values stay positive or negative after reversing signs.

values stay positive or negative after reversing signs.