14

Demand for Money: The Keynesian Approach

After studying this topic, you should be able to understand

- The transactions demand for money is the money demanded by the public for carrying on its various current transactions.

- The precautionary demand for money is the demand for cash by the public for contingencies, which may involve unexpected expenditures and opportunities.

- The existence of an uncertainty about the future gives rise to the speculative demand for money.

- In Keynes’ theory, the rate of interest is a monetary phenomenon determined by the equality between the demand for and supply of money.

- Given the demand for money, an increase in the supply of money leads to a decrease in the interest rate and vice versa.

- There can occur a change in the demand for money either due to a change in the transactions demand for money or due to change in the speculative demand for money.

- It can be argued that Keynes’ theory is indeterminate.

INTRODUCTION

In Chapter 13, we had focused on the classical theory of demand for money. According to the classical theory, money is demanded as a medium of exchange or in other words for conducting transactions. But according to J. M. Keynes, who formulated his theory of demand for money in his well known book The General Theory of Employment, Interest and Money in 1936, money is demanded due to three motives which we discuss at length in the present chapter. We go on to determine the rate of interest in this Keynesian model through the supply and demand for money. We also analyse how changes in the supply of money, the income level and the speculative demand for money lead to changes in the rate of interest.

THE KEYNESIAN THEORY OF THE DEMAND FOR MONEY

Unlike the classical economists who recognized only the medium of exchange function of money, Keynes emphasized the store of value function of money also. Thus, he had put forward that money was demanded due to three motives: transactions motive, precautionary motive and speculative motive.

The transactions demand for money is the demand for cash by the public for carrying on its various current transactions.

Transactions Demand

The transactions demand for money is the demand for cash by the public for carrying on its various current transactions. The transactions motive creates transactions demand for money. Everyone needs to hold some amount of money to facilitate their day-to-day transactions in goods and services. Thus money is needed as a medium of exchange, as has also been emphasized by the classical economists.

John Maynard Keynes is largely recognized for having created the shape and terminology of modern macroeconomics. His book, General Theory of Employment, Interest and Money brought about a revolution in the thinking of economists. The book is the foundation of Keynesian thought. It provided a great challenge for the classical school of thought by introducing some new and revolutionary concepts. Keynes is perhaps one of the greatest and most prominent economists of the twentiethth century. He is often known as the father of modern economics.

The reason why this money is held is due to the time gap involved between which the income is received and the payments are made out. In other words, it is required to bridge the gap between the receipts and the regular payments to be made. The closer is this gap the smaller will be the transactions demand for money.

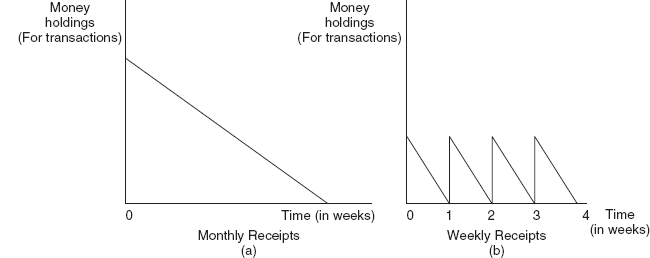

Often, individuals do not find their time patterns for payments identical. Also it is very rare for these payments to be evenly distributed over the entire month. However, for simplicity we assume that these payments are evenly distributed over the entire month. We find that

- A person whose receipts arrive on the first day of the month will be required to hold on an average larger amount of transactions balances as shown in Figure 14.1 (a).

- A person whose receipts arrive at regular intervals in the month will be required to hold on an average smaller amount of transactions balances as shown in Figure 14.1 (b).

(It is important to note that the total amount of receipts is the same in the above two cases and, therefore, a comparison is possible.)

Thus, as the frequency of the receipts increase the average holdings of transactions balances by the individual decreases.

Transactions demand for money as a function of income

It is believed that there exists a stable and direct relationship between income and transactions money balances. This relationship can expressed as

| where, | Mt = | amount of money balances demanded for transactions |

| k = | fraction of money income, which the public likes to hold as money balances for transactions |

|

| P = | price level | |

| Y = | income level |

Figure 14.1 Individual’s Money Holdings for Transactions

Figure 14.2 Transactions Demand for Money as a Function of the Income Level

Equation (1) specifies the existence of a direct relationship between the transactions balances and the income level. The equation, which is in nominal terms, can be expressed in real terms by dividing throughout by P to get

Mt / P = k(Y)

or

where,

mt = amount of real balances demanded for transactions

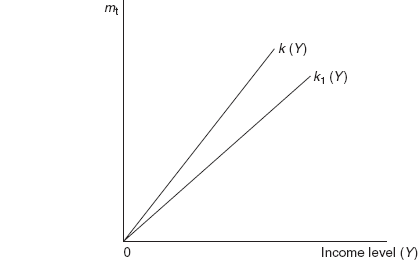

The relationship between transactions demand for money and income can be depicted through Figure 14.2. The line k(Y) shows the amount of transactions balances, mt for different levels of income, Y with k at say 1/4. Thus if Y were Rs. 4000, mt would be 1000. If k were 1/5 we would have the line k1 (Y) in the figure. Hence with Y at Rs. 4000, mt would be 800.

The size of k will be a function of the institutional and the structural conditions in the economy. This includes the time gap between receipts and payments for each individual, speed for movement of money, etc. However for simplicity sake k is assumed to be stable, at least in the short run.

Transactions Demand for Money as a Function of the Rate of Interest

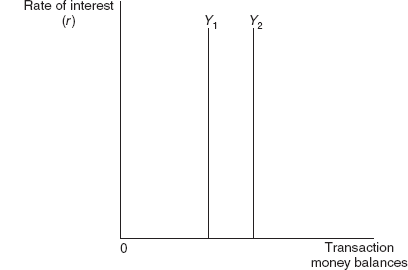

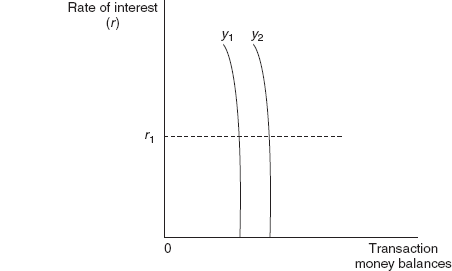

According to Keynes, the transactions demand for money is perfectly interest inelastic as shown in Figure 14.3. A change in income will lead to a shift of the curve from Y1 to Y2, but the curve remains inelastic throughout.

Figure 14.3 Transactions Demand for Money as Interest Inelastic

Figure 14.4 Transactions Demand for Money as Interest Elastic

However, some economists are of the opinion that in practice there may exist some rate of interest r1 at which the transaction demand for money curve may slope backwards as in Figure 14.4. The curve indicates that at low rates of interest, the transactions demand for money may be interest inelastic. But at higher rates of interest, the opportunity cost in terms of holding transactions balances, rather than some interest earning assets, may be too high.

Precautionary Demand

The precautionary demand for money is the demand for cash by the public for contingencies, which may involve unexpected expenditures and opportunities. Thus, precautionary demand for money exists due to uncertainties. It is for those payments, which are neither regular nor planned. Hence, it enables individuals to meet unexpected increases in expenditure or unexpected delays in receipts.

The precautionary demand for money varies with the income level. At higher levels of income, individuals certainly need more money and are in a position and have the means to keep aside more money for emergencies and contingencies. The other factor, which influences precautionary demand for money, is the rate of interest. At high rates of interest, one may feel tempted to hold smaller precautionary balances rather than forego the high interests which could be earned by putting these balances in interest-earning assets.

The precautionary demand for money is the demand for cash by the public for contingencies, which may involve unexpected expenditures and opportunities.

For the sake of convenience and following the conventional procedure, transactions and precautionary balances are often put together as a function primarily of the income level and as being interest inelastic.

Speculative Demand

While the transactions demand and precautionary demand for money do not in any way conflict with the views of the classical theory, the speculative demand for money (also called asset demand for money) represents a complete break from the classical theory. It is one of the most important contributions made by Keynes to the theory of demand for money. It is the speculative motive, which gives rise to the speculative demand for money.

Speculative demand for money arises due to the existence of an uncertainty about the future.

The classical economists had put forward the view that an individual would not hold money in excess of what he requires for transactions and precautionary purposes. For in doing so, he would be losing the interest which he could have earned by putting that amount of money in a bond. Even if the interest rate is extremely low, it would still be advantageous for him to earn whatever interest he can earn on it.

Keynes, however, had different opinions. First of all, to present his views he assumed that individuals hold only two kinds of financial assets in their asset portfolio, namely money and perpetual (or irredeemable) bonds. A bond is an asset that carries a promise to pay to its owner a fixed amount of income per annum. This income entitles the owner of the bond to a future income stream.

A bond is an asset that carries a promise to pay to its owner a fixed amount of income per annum. This income entitles the owner of the bond to a future income stream.

The market price of the bond will depend to a large extent on the rate of interest fixed in terms of money. Keynes had pointed out that an individual who is purchasing bonds does so because he expects that in the near future there will not occur an increase in the interest rates. In case he expects an increase in the interest rates, he should not be purchasing bonds and instead would be holding money. Thus, the existence of an uncertainty about the future gives rise to what is called the speculative demand for money.

Interest Rates and Bond Prices

For an understanding of the speculative demand for money, it is fruitful to understand the relationship between the rate of interest and the price of a bond. We assume on one hand that the bond is totally risk free, or in other words it does not involve any kind of risk, but it does yield an interest income; on the other hand, the holders of money do not earn any interest but the capital value of money remains unchanged.

The price of a perpetual bond is equal to the reciprocal of the market rate of interest multiplied with the coupon rate of interest, where the coupon rate of interest is the interest payable on a bond. For example, suppose the coupon rate of interest is Rs. 1 per annum (1 per cent on the Rs. 100 face value bond) and the market rate of interest is 5 per cent per annum, then the market price of the bond will be Rs. 1/0.05 × 1 = 20. If there is an increase in the market rate of interest to 6 per cent per annum, then the market price of the bond will be Rs. 1/0.06 × 1 = 16.67. Thus, a rise in the market rate of interest implies a decrease in the price of a bond and vice versa. Thus, there exists an inverse relationship between the market rate of interest and the price of a bond.

In addition, the price of a bond is subject to capital gain and losses. Hence, the return from a bond will be the sum of the rate of interest and the capital gains and losses per annum. At the time of the purchase of the bond the market rate of interest is given, but the future rate of interest and hence the price of the bond will keep fluctuating leading to an element of uncertainty and thus a speculation in the money and bond markets.

Speculation in the Money Market and Bond Market

The speculators can be grouped into two categories:

- Bulls are those who expect that the price of bonds will rise in the future. Hence, they move out of money into bonds by investing all their idle cash in bonds.

- Bears are those who expect that the price of bonds will fall in the future. Hence, they move out of bonds into money if they expect capital losses on bonds. Hence, they attempt to minimize on their losses. It is from these bears that the speculative demand for money arises. The bears build up on their cash balances to purchase bonds whenever they expect an increase in the price of bonds in the future.

Bulls are those who expect that the price of bonds will rise in the future.

Bears are those who expect that the price of bonds will fall in the future.

From the above analysis it is obvious that as far as the asset holders are concerned, they either hold only bonds (and are thus bulls) or they hold only money (and are thus bears). Hence, they do not have a diversified portfolio.

Keynes was of the opinion that the depressions could be thought of in terms of recessions, which had fallen into a liquidity trap. In a liquidity trap since the public prefers to hoard money, the government can do just the opposite, that is, spend to restore the circular flow of money. It is a different matter that Keynes’ advice on how to end the Great Depression was not put into practice. In fact, it was the World War II that was to some extent responsible in curing the Great Depression. This was because of the huge amounts of public spending on defense. Could this be the reason for the views that wars are good for the economy and are an economic boon?

Speculative Demand Curve for Money

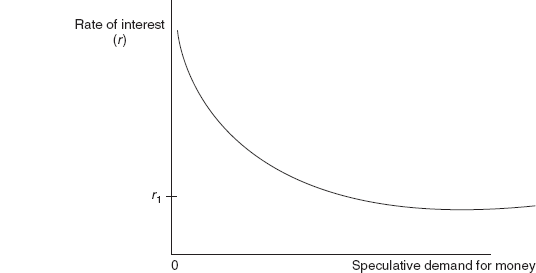

Keynes had assumed that there are many asset holders, each with a different expectation regarding the interest rate. At some very high rate of interest (low price of bonds), all may expect an increase in the price of bonds and hence they may all be bulls. Here, the speculative demand for money will be zero. At a slightly lower rate of interest, expectations may change with some bulls now becoming bears and with there appearing a positive demand for speculative money balances. At a still lower interest rate, some more of the bulls may become bears with a higher speculative demand for money. Hence, Keynes arrived at a downward sloping speculative demand curve for money as shown in Figure 14.5.

The speculative demand curve for money depicts the inverse relationship between the interest rate and the speculative demand for money. A very significant contribution of Keynes is what he called the liquidity trap. The liquidity trap is a situation when at some very low rate of interest all asset holders become bears. The demand for money becomes what can be called to be perfectly elastic. In such a situation, any amount of expansion of money supply cannot lower the interest rate any further. At this interest rate, the public is willing to hold only money. We often say that the extra liquidity gets sucked in the asset portfolio of the public in the form of money and no additions to the money supply can succeed in lowering the interest rates any further. Thus, r1 in Figure 14.5 is the minimum interest rate and cannot fall any further.

A very important feature here without which a discussion on Keynes’ theory of speculative demand will be incomplete is the normal rate of interest. Keynes had emphasized that at any point in time there will exist a certain r which can be said to be that rate of interest which will prevail under normal circumstances. For the asset holders, this ‘normal’ r is the benchmark or yardstick with which they compare any actual r in making their decisions. Thus if at any point of time the interest rate were above the normal level, people would expect it to fall and thus expect capital gains and interest income from holding bonds and will continue to hold bonds. If it were below this normal rate, people would expect it to rise and expect capital losses on holding bonds.

Figure 14.5 Speculative Demand Curve for Money

In the case of an individual with given expectations about the future rate of interest, the speculative demand for money is a discontinuous curve. However for the aggregate economy, different individuals have different expectations regarding the rate of change of the actual rate of interest. Hence, the aggregate speculative demand for money curve becomes a smooth downward sloping curve showing an inverse relationship between the speculative demand for money and the current rate of interest.

Speculative Demand for Money as a Function of the Rate of Interest

Unlike the direct relationship between income and transactions money balances, there exists an inverse relationship between the speculative balances and the rate of interest. This relationship can be expressed as

| where, | Msp = | amount of money balances demanded for speculative purposes |

| P = | price level |

Equation (3) specifies the existence of an indirect relationship between the speculative balances and the rate of interest. The equation, which is in nominal terms, can be expressed in real terms by dividing throughout by P to get

Msp/P = g(r)

or

where msp = amount of real balances demanded for speculative purposes.

The Total Demand for Money

The total demand for money can be expressed as follows:

| md = | total demand for money | |

| where | mt = | transactions demand for money |

| msp = | speculative demand for money | |

| But from Eq. (2), | mt = | k(Y) |

| and from Eq. (4), | msp = | g(Y) |

Thus, combining these equations we can write

Given any price level from k we can deduce as to what will be mt for each income level. In a similar manner, given any price level from g we can deduce as to what will be msp for each level of the rate of interest. Thus, from k and g we can find out the total demand for money for each and every possible combination of Y and r.

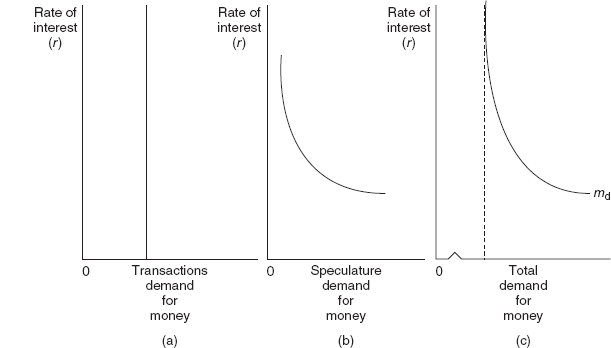

Figure 14.6 The Total Demand for Money

Figure 14.6 attempts at determining the total demand for money. It has been divided into three parts: part (a) shows the transactions demand for money as vertical (since it is interest inelastic); part (b) shows the speculative demand for money as a downward sloping curve (since it is inversely related to the interest rate); part (c) shows the total demand for money as the sum of mt and msp. Thus, md is the Keynesian demand curve for money and is downward sloping.

Criticism of Keynes’s Theory of Demand for Money

- As pointed out by Tobin, in reality, individuals do not hold either just money or only bonds. They, in fact, hold a diversified asset portfolio with a blend of both bonds and money and other financial assets.

- It has also been pointed out that Keynes’ theory treats all non-money financial assets as bonds while in reality there exists a variety of assets, which have characteristics which are far removed from those of bonds.

- As Keynes himself had also accepted like the other economists, the possibilities of the occurrence of a liquidity trap are quite far-flung. However, it seems that what is occurring in the world today may be something akin to a liquidity trap.

- Keynes’ division of money into transaction, precautionary and speculative demands is not realistic. The same unit of money can be used to serve all the three motives.

- Many economists like Baumol and Tobin had emphasized that the transactions demand for money is interest elastic.

RECAP

- As the frequency of the receipts increase, the average holding of transactions balances by the individual decreases.

- There exists a stable and direct relationship between income and transactions money balances.

Figure 14.7 Determination of the Rate of Interest: The Keynesian Theory

- According to Keynes, the transactions demand for money is perfectly interest inelastic.

- There exists an inverse relationship between market rate of interest and the price of a bond.

- The liquidity trap is a situation when at some very low rate of interest all asset holders become bears.

THE KEYNESIAN THEORY OF INTEREST

In the classical theory, the rate of interest is a real phenomenon determined by the equality between savings and investment in the commodity market. In contrast in Keynes theory, the rate of interest is a monetary phenomenon determined by the equality between the demand for and supply of money. It is in fact a compensation for parting with liquidity.

The liquidity trap is a situation when at some very low rate of interest all asset holders become bears.

As far as the total demand for money is concerned from Eq. (6), we have

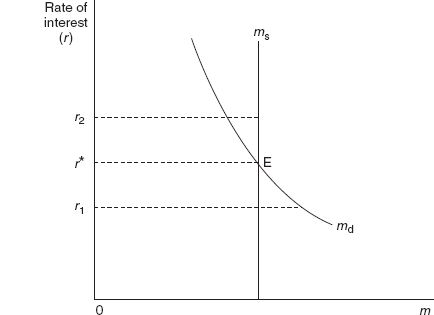

Regarding the supply of money, Keynes assumed that the supply of money is exogenously determined by the monetary authorities. Hence in Figure 14.7, it is shown by a vertical line parallel to the vertical axis and is interest inelastic.

The money market will be in equilibrium when the demand for money is equal to the supply of money.

In nominal terms,

Md = Ms

In real terms,

md = ms

or

k(Y) + g(r) = ms

At a higher rate of interest rate r2, the demand for money will be less than the supply of money. In other words, there is an excess supply of money in the money market. This implies an excess demand for bonds in the bond market. Thus, there will be an increase in the price of bonds and a decrease in the rate of interest till r* is achieved.

According to Keynes, r* represents a stable equilibrium value of r which is determined by the monetary forces of demand and supply of money. Variations in r alone act as the adjustment mechanism for bringing about equilibrium in the money market whenever disequilibrium occurs. Variations in r will occur due to changes in the supply of money and the demand for money.

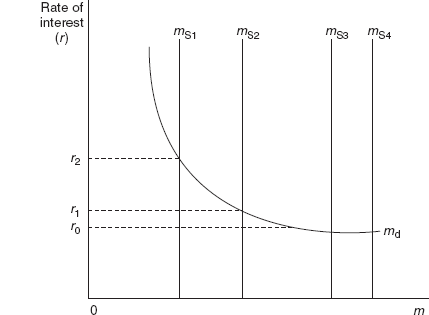

Figure 14.8 Effect of Changes in the Money Supply on the Interest Rate

RECAP

- Variations in the rate of interest alone act as the adjustment mechanism for bringing about equilibrium in the money market whenever disequilibrium occurs.

VARIATIONS IN THE INTEREST RATE

Changes in the Supply of Money and their Effects on the Interest Rate

We now analyse the effects of a change in the supply of money and its influence on the interest rate. Given the demand for money curve, an increase in the supply of money leads to a decrease in the interest rate and vice versa.

In Figure 14.8 given the demand for money curve md and supply of money as ms1, the money market is in equilibrium at only one rate of interest, r2. Suppose that while the demand for money remains unchanged, the supply of money is increased from ms1 to ms2. The equilibrium value of the rate of interest will fall from r2 to r1.

As the money supply is increased further to ms3, the equilibrium value of the rate of interest will fall from r1 to r0. Any further increases in the supply of money, say to ms4 will not lower the rate of interest any further because at r0 it is caught in what is called the liquidity trap. Thus, r0 is the absolute minimum below which there cannot be a fall in the rate of interest. This is that rate of interest at which, according to the liquidity trap hypothesis, the public is willing to hold only money and no bonds.

Changes in the Demand for Money and their Effects on the Interest Rate

There can occur a change in the demand for money either due to a change in the transactions demand for money or due to change in the speculative demand for money.

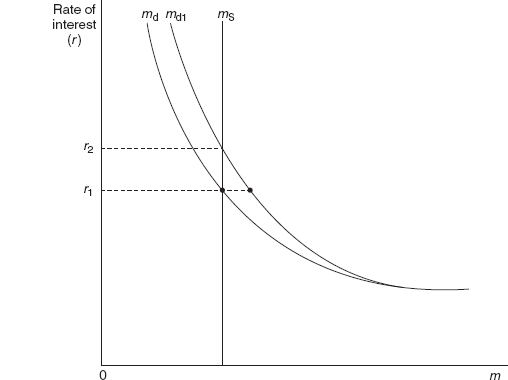

Figure 14.9 Effect of Changes in the Transactions Demand for Money on the Interest Rate

Changes in the Transactions Demand for Money and their Effects on the Interest Rate

Given the money supply and the speculative demand for money, the rate of interest will vary directly with the income level.

An Increase in the Income Level

In Figure 14.9, initial equilibrium in the money market is determined at the intersection of ms and md with the equilibrium rate of interest at r1. Given the value of k (fraction of money income which the public likes to hold as money balances for transactions), an increase in the income will raise the transactions demand for money and hence the total demand for money curve will shift outwards at each rate of interest to give the new demand curve md1. Given the supply of money and an increase in the demand for money, the rate of interest will rise to new equilibrium rate of r2.

The underlying process here involves a diversion of money from speculative balances to transactions balances. With an increase in their incomes, individuals realize that they need more money for transactions. As the supply of money is unchanged, the additional demand for transactions balances can be satisfied only by selling bonds leading to a decrease in the price of bonds and an increase in the rate of interest from r1 to r2.

A Decrease in the Income Level

Initial equilibrium in the money market exists with ms and md1 with the equilibrium rate of interest at r2. Given the value of k, a decrease in the income will reduce the transactions demand for money and hence the total demand curve will shift inwards at each rate of interest to give the new demand curve md. Given the supply of money and a decrease in the demand for money, the rate of interest will fall to new equilibrium rate of r1.

Changes in the Speculative Demand for Money and their Effects on the Interest Rate

We assume that the money supply and the transactions demand for money are given and there is a change in the speculative demand for money.

The question arises how does the speculative demand for money change? This particular demand for money is based on the wealth holder’s expectations regarding the normal rate of interest. The change in the expectations regarding the normal rate of interest occurs if there are expected changes in the domestic and international factors, which have an influence on the business forecasts and also the response expected from the Central Bank to such changes.

Suppose in Figure 14.9, money supply is given as ms while the demand for money is given as md and the normal rate of interest is r1. With no decrease in the supply of money and no increase in the income level, suppose the wealth holders’ views undergo a change and they now regard a higher rate r2 as the normal rate of interest. Thus rates above r2 will be viewed as high while rates below r2 will be viewed as low. This will amount to an outward shift in the demand curve from md to md1.

On the other hand, with no increase in the money supply and no decrease in the income level, suppose the wealth holders now regard a rate below r1 as the normal rate of interest. Thus, rates above r1 will be viewed as high while rates below r1 will be viewed as low. This will amount to an inward shift in the demand curve.

RECAP

- Given the money supply and the speculative demand for money, the rate of interest will vary directly with the income level.

A CRITICISM OF THE KEYNESIAN APPROACH

- The money market equilibrium equation of Keynes k(Y) + g(r) = ms, is actually one equation and two unknowns, r and Y. Only if the value of Y is known can k(Y) be taken as known and then the above equation can be used to calculate r. However, the problem is that while Y not only affects r through k(Y) but that itself is affected by r through investment, I. Thus, r and Y are interdependent variables. Hence, it can be argued that Keynes theory is indeterminate.

- Keynes had denied the influence of the real factors, saving and investment, in the determination of the rate of interest. This is perhaps a view which is too extreme as the influence of these real factors cannot be ignored.

RECAP

- Keynes had denied the influence of the real factors in the determination of the rate of interest, a view which is too extreme as the influence of these real factors cannot be ignored.

SUMMARY

INTRODUCTION

The chapter discusses the three motives for holding money and the determination of the rate of interest in the Keynesian model through the supply and demand for money.

THE KEYNESIAN THEORY OF THE DEMAND FOR MONEY

- Unlike the classical economists who recognized only the medium of exchange function of money, Keynes emphasized the store of value function of money also.

- According to Keynes, money was demanded due to three motives: transactions motive, precautionary motive and speculative motive.

TRANSACTIONS DEMAND

- The transactions demand for money is the demand for cash by the public for carrying on its various current transactions.

- The reason why this money is held is due to the time gap involved between which the income is received and the payments are made out.

- As the frequency of the receipts increase, the average holding of transactions balances by the individual decreases.

- There exists a stable and direct relationship between income and transactions money balances.

- Keynes had argued that the transactions demand for money is perfectly interest inelastic.

PRECAUTIONARY DEMAND

- The precautionary demand for money is the demand for cash by the public for contingencies, which may involve unexpected expenditures and opportunities.

- The precautionary demand for money varies directly with the income level.

- The other factor which influences precautionary demand for money is the rate of interest. At high rates of interest, one may feel tempted to hold smaller precautionary balances.

- For the sake of convenience and following the conventional procedure, transactions and precautionary balances are often put together as a function primarily of the income level and as being interest inelastic.

SPECULATIVE DEMAND

- The speculative demand for money represents a complete break from the classical theory and it is one of the most important contributions made by Keynes.

- Keynes assumed that individuals hold only two kinds of financial assets in their asset portfolio, namely money and perpetual (or irredeemable) bonds.

- The existence of an uncertainty about the future gives rise to what is called the speculative demand for money.

- There exists an inverse relationship between market rate of interest and the price of a bond. In addition, the price of a bond is subject to capital gain and losses.

- The speculators can be grouped into two categories: bulls who expect that the price of bonds will rise in the future and bears who expect that the price of bonds will fall in the future.

- It is from the bears that the speculative demand for money arises.

- The asset holders either hold only bonds or they hold only money. They do not have a diversified portfolio.

- A very significant contribution of Keynes is the liquidity trap, which is a situation when at some very low rate of interest all asset holders become bears. No additions to the money supply can succeed in lowering the interest rates any further.

- Keynes had emphasized that at any point in time there will exist a certain r which can be said to be that rate of interest which will prevail under normal circumstances and which is the benchmark or yardstick with which any actual r is compared in making decisions.

- The aggregate speculative demand for money curve is a smooth downward sloping curve showing an inverse relationship between the speculative demand for money and the current rate of interest.

THE TOTAL DEMAND FOR MONEY

The total demand for money can be written as md = mt + msp or md = k(Y) + g(r). It represents the Keynesian demand curve for money and is downward sloping.

CRITICISM OF KEYNES’ THEORY OF DEMAND FOR MONEY

- In reality, individuals do not hold either just money or only bonds and in fact hold a diversified asset portfolio.

- The possibilities of the occurrence of a liquidity trap are quite far-flung.

- Keynes’ division of money into transaction, precautionary and speculative demands is not realistic and the same unit of money can be used to serve all the three motives.

THE KEYNESIAN THEORY OF INTEREST

- In Keynes’ theory, the rate of interest is a monetary phenomenon determined by the equality between the demand for and supply of money. Thus, k(Y) + g(r) = ms.

- Variations in r alone act as the adjustment mechanism for bringing about equilibrium in the money market whenever disequilibrium occurs.

VARIATIONS IN THE INTEREST RATE

CHANGES IN THE MONEY SUPPLY AND THEIR EFFECTS ON THE INTEREST RATE

- Given the demand for money curve, an increase in the supply of money leads to a decrease in the interest rate and vice versa.

- However in the liquidity trap, any increases in the supply of money will not lower the rate of interest any further.

CHANGES IN THE DEMAND FOR MONEY AND THEIR EFFECTS ON THE INTEREST RATE

- There can occur a change in the demand for money either due to a change in the transactions demand for money or due to change in the speculative demand for money.

- As far as changes in the transactions demand for money are concerned, given the money supply and the speculative demand for money, the rate of interest will vary directly with the income level.

- As far as changes in the speculative demand for money are concerned, given the money supply and the transactions demand for money a change in the speculative demand for money will lead to a change in the interest rate.

CRITICISM OF THE KEYNESIAN APPROACH

- The money market equilibrium equation of Keynes is actually one equation and two unknowns. Hence, it can be argued that Keynes theory is indeterminate.

- Keynes had denied the influence of the real factors, saving and investment, in the determination of the rate of interest.

REVIEW QUESTIONS

TRUE OR FALSE QUESTIONS

- The precautionary demand for money is the demand for cash by the public for carrying on its various current transactions.

- Keynes had laid emphasis on the store of value function of money.

- The average holdings of transactions balance by the individual increases as the frequency of the receipts increases.

- The speculative demand for money arises due to the existence of an uncertainty about the future.

- The liquidity trap is a situation when at some very low rate of interest all asset holders become bulls.

VERY SHORT-ANSWER QUESTIONS

- Is the transactions demand for money interest elastic? Explain.

- What is the precautionary demand for money?

- Bulls and bears are the two categories of speculators in the market? How do they function? Explain.

- ‘The liquidity trap is a situation when at some very low rate of interest all asset holders become bears.’ Explain.

- The speculative demand for money represents a complete break from the classical theory and it is one of the most important contributions made by Keynes. Comment.

SHORT-ANSWER QUESTIONS

- Analyse the transactions demand for money as a function of the income level.

- What is the precautionary demand for money? What are the factors that influence it? Discuss.

- Derive Keynes’ total demand for money curve.

- (a) What is normal rate of interest in the Keynesian speculative demand for money? Explain.

(b) Give a criticism of Keynes’ theory of demand for money.

- In the Keynesian theory of interest, ‘there can occur a change in the demand for money either due to a change in the transactions demand for money or due to change in the speculative demand for money’. Explain.

LONG-ANSWER QUESTIONS

- What is the transactions demand for money? Explain

- ‘According to Keynes, money is demanded due to three motives: transactions motive, precautionary motive and speculative motive.’ Briefly discuss the three motives.

- What is the speculative demand for money? What are the factors that influence it? Discuss.

- How is the rate of interest determined in the Keynes theory? Is it a real or a monetary phenomenon?

- ‘In Keynes theory, variations in r will occur due to changes in the supply of money and the demand for money.’ Explain.

ANSWERS

TRUE OR FALSE QUESTIONS

- False. The transactions demand for money is the demand for cash by the public for carrying on its various current transactions.

- True. Unlike the classical economists who recognized only the medium of exchange function of money, Keynes emphasized the store of value function of money also.

- False. The average holdings of transactions balance by the individual decreases as the frequency of the receipts increases.

- True. The existence of an uncertainty about the future gives rise to the speculative demand for money.

- False. The liquidity trap is a situation when at some very low rate of interest all asset holders become bears.