17.2. TECHNICAL INNOVATION AND ECONOMIC DEVELOPMENT

Labor, capital investment, the availability of natural resources and raw materials, technical innovation, and management skills all contribute to high productivity and economic development in a nation. Here the discussion will focus on the role that R&D plays in technological innovation and economic development.

The discussion on the output of science and technology pointed out that R&D productivity to some degree can be measured by output in terms of scientific literature, patents, and the gross domestic product of each employed person. A general relationship or correlation between investment in R&D and these three entities seems to exist. This general correlation can never be high because factors other than R&D (such as capital, quality of the labor force, social, economic, and political factors, among other variables) also play a major role. There is also the phenomenon of economic cycles. Studies conducted by the Systems Dynamic Group at MIT suggest that economies move through long waves of approximately 50 years' duration. In the early part of the cycle, productivity per person increases. This upswing is due to an increase in capital investment per person, but after the accumulation of physical facilities and capital investment, adding more capital does not necessarily add to productivity (Rothwell and Zegwell, 1981, p. 39).

Technological innovation, as discussed previously, combines understanding and invention in the form of socially useful and affordable products and processes. To produce this basic understanding and invention, investment in basic research is required. One could argue that the investment in one country could be in basic research, but that the benefits might accrue to another country that combines the results of basic research with the capacity to produce useful and commercially profitable products and processes. In any case, looking at the world as a complete system, investment in R&D is necessary for innovation.

In examining the role of technology in enhancing productivity for the private, nonagricultural sector of the U.S. economy, we see that from 1909 to 1949 the cumulative percentage change in output per work-hour amounted to 80.9 percent (Rothwell and Zegwell, 1981, p. 24). Of this, 87.5 percent of the total increase in output per work-hour was due to technical change; the rest was due to increased capital per work-hour (Solow, 1957).

When Robert Solow originally published his paper "Technical Change and the Aggregate Production Function" (1957), he determined that the aggregate production function increased at an average of 1.5 percent per year for the years 1909–1949. This means that according to his model, the United States was increasing production in all fields (excluding agriculture) at a given numeric rate. What made his work outstanding was the connection between this increase in productivity and the investment in technical change through research. In fact, Solow attributed seven-eighths of total increase in the production function to technical change. This average upward trend has continued, and in order for it to continue to do so, there must be a consistent commitment to investment in research as well as continued development in methods of technology transfer to appropriate fields. Between 1997 and 2004 the United States increased R&D/GDP spending by 0.91 percent, ahead of most countries but behind Japan and Denmark. This ratio of change in R&D spending to total GDP is a reflection of a country's "investment in knowledge" and is an indicator of how a nation prioritizes increased innovation and technological change (OECD, 2007).

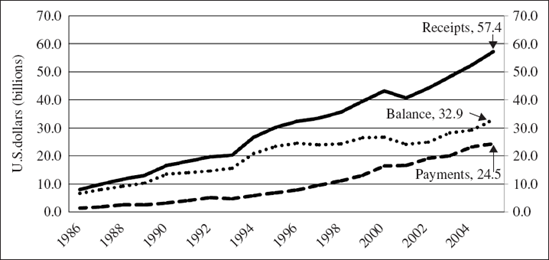

Commenting on the role of technological innovation in economic development, Charpie (1970, p. 3) states that in industrialized economies, all of the studies show that 30–50 percent of long-term economic growth stems from innovation that either improves productivity or leads to new products, processes, or completely new industries. It is further suggested (Charpie, 1970, p. 51) that technology affects international trade in several ways. International payments for technology such as patent royalties, payments for technical know-how, and so on, flow predominantly to the nations that invest heavily in research and development. For example, according to OECD figures as reported by the NAS, the United States receives 2.3 times as much in technological payments from abroad as it makes in such payments to other nations Figure 17.1.

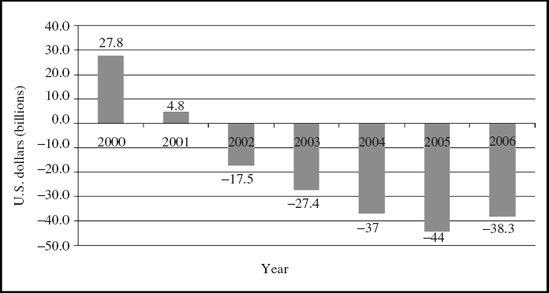

Possession of high-technology capacity has worked to the advantage of innovative industrialized nations in many other ways. When low-technology natural products are produced in low-labor-cost countries, industrialized countries can overcome the labor cost disadvantage by producing high-technology products for export, thus more than replacing the import balance. However, since 2002 the United States has been running a high-technology trade deficit, as can be seen in Figure 17.2, which is a serious matter that requires thoughtful analysis. Industrial and science policy that fosters the effective use of R&D output to produce products and systems —an effective innovation process— that makes us internationally competitive needs to be developed and implemented: clearly a challenging task.

Figure 17.1. U.S. Receipts and Payments of Royalties and Fees for Intellectual Property: 1986–2005: (Source: Bureau of Economic Analysis, U.S. International Services: Cross-Border Trade 1986–2005, and Sales Through Affiliates, 1986–2004, table 4, http://www.bea.gov/international/intlserv.htm, accessed 28 June 2007. Science and Engineering Indicators, 2008.)

Figure 17.2. U.S. Trade Balance in High-Technology Goods: 2000–2006: (Source: Census Bureau, Foreign Trade Division, special tabulations. Science and Engineering Indicators, 2008, p. O-10.)

While in the short run economic progress may be made by applying the existing scientific knowledge base, in the long run this simply is not possible. Freeman and Soete (1997) state:

It is only to assert the fundamental point that for any given technique of production, transport or distribution, there are long-run limitations on the growth of productivity, which are technologically determined. No amount of improvement in education and quality of labor force, no greater efforts by the mass media, no economies of scale or structural changes, no improvements in management or in governmental administration could in themselves ultimately transcend the technical limitations of candlepower as a means of illumination, of wind as a source of energy, or iron as an engineering material, or of horses as a means of transport. Without technological innovation, economic progress would cease in the long run and in this sense we are justified in regarding it as primary.

It is important to note that factors such as the education and training of the labor force, an efficient industrial infrastructure (such as transportation and communication networks), capital investment, intellectual property protection, a culture that encourages risk taking, and management skills all contribute to economic productivity. But without new inventions and the scientific base to produce them, economic growth and productivity simply will not continue to increase.