Syntax. LOGNORM.DIST(x,mean,standard_dev,cumulative)

Definition. This function returns the values of the distribution function of a lognormal distributed random variable where ln(x) is normally distributed with the parameters mean and standard_dev. Use this function to analyze data that has been logarithmically transformed.

Arguments

x (required). The value at which to evaluate the function

mean (required). The mean of the lognormal distribution

standard_dev (required). The standard deviation of the lognormal distribution

cumulative (required). The logical value that represents the type of the function

Note

If one of the arguments isn’t a numeric expression, the LOGNORM.DIST() function returns the #VALUE! error.

If x is less than or equal to 0, or standard_dev is greater than or equal to 0, the LOGNORM.DIST() function returns the #NUM! error.

Background. The LOGNORM.DIST() function returns the probabilities of a logarithmically normal distributed random variable. Use this function to evaluate probability distributions where the natural logarithm instead of the random variable is normal distributed.

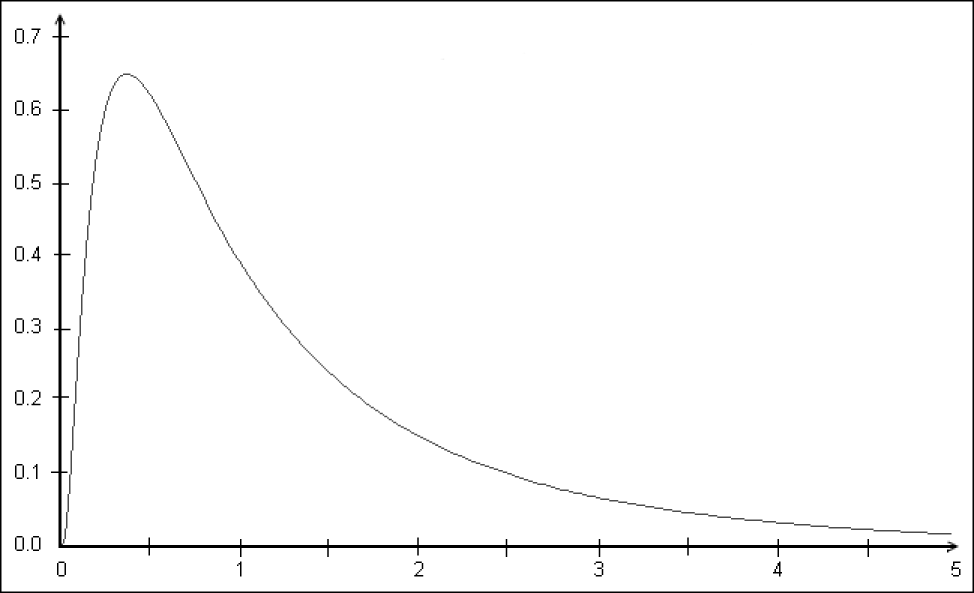

The lognormal distribution is similar to the normal distribution but has a logarithm in the exponent. The lognormal distribution is right skewed (see Figure 12-91 later in this section). If a random variable is lognormal distributed, its logarithm is also normal distributed. For example, incomes are often lognormal distributed. The reason for this is the usual percentage increase. Large incomes increase a lot, and smaller incomes increase only a little. Over time, the small incomes remain small, and the large incomes become bigger. Therefore, the distribution is right skewed. The logarithmic function transforms the multiplicative structure into an additive structure. Then the logarithmized values are normal distributed.

Another reason for the lognormal distributed income structure is the lack of high-salaried jobs. The salary for the majority of jobs is small, but extremely low incomes are less common. Most lognormal distributions are based on this fact.

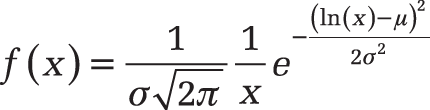

The lognormal distribution with the μ and σ2 parameters for positive real numbers is defined by the following probability density:

Figure 12-91 shows the probability density of the lognormal distribution.

The equation for the distribution function of a lognormal distribution is:

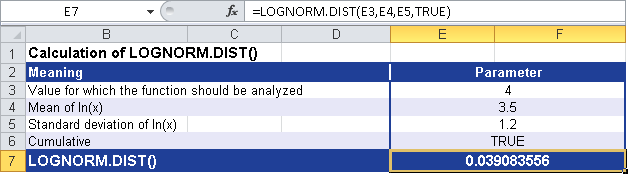

Example. Use the following values to calculate LOGNORM.DIST():

4 = the value at which to evaluate the function (x)

3.5 = the mean of ln(x) (mean)

1.2 = the standard deviation of ln(x) (standard_dev)

TRUE = the logical value that represents the type of the function

Figure 12-92 shows the calculation of LOGNORM.DIST().

The LOGNORM.DIST() function returns the cumulative lognormal distribution of 0.039084 based on the parameters shown in Figure 12-72.