3

PASSION BUDGETING: HOW IT WILL CHANGE

YOUR LIFE FOR THE BETTER

The bestway to predict your future is to create it.

—Peter Drucker1

In a cartoon published by The New Yorker, two sharks are swimming together in the open ocean. One shark looks over at the other and says, “I start every diet with the best intentions, but it goes to hell as soon as I sense blood in the water.”

Before you try to skip the chapter on budgeting, stop! This is not going to be about cutting out all of the things you love in life. Instead, you are going to learn how to create a budget that keeps everything important to you and eliminates everything else. Yes, you will learn how to be more economical with your purchases and leverage your existing expenses. Yes, you will analyze your incomes and learn how to increase and optimize their power. Yes, you will learn rules of the road and set achievable goals. Yes, you will learn passion budgeting.

Rich people don't focus on the small things; they spend their energy applying the appropriate amount of pressure to the right areas in order to produce maximum results. Rich people do not get distracted.

Who Actually Budgets?

Although the budgeting process may appear dull, embracing the core concepts is the key to getting where you want to go. It can even be cathartic. Before your money makeover, you might have thought that you didn't need to create a budget. After all, you probably have a good understanding of the underlying equation: income minus expenses.

The physical process of sitting down and writing out all of your cash inflows and outflows can be an incredibly powerful and motivating event. That is why the wealthy use it to their advantage. In a recent study, more than 54 percent of affluent investors create a budget and more than 84 percent stick to it.2 This type of proactive planning is used to build and maintain their rich lives.

Some of your favorite companies, such as Apple, Nike, Amazon, Target, and Coca-Cola, also develop operating budgets every year. During the budgeting process, key stakeholders determine their goals, strategies, and objectives for the coming year. Then they prioritize what expenses will help them reach their goals. Budgeting is an iterative process, but highly successful companies understand it, and so should you. Here are some examples of entities that budget:

- Startups

- Hospitals

- Universities

- Large corporations

- Not-for-profits

Chances are that you have been to one of these places recently, maybe a hospital. I bet the hospital's budgeting process never crossed your mind. I'm guessing you didn't stop to think, “This hospital's operating budget must be huge. Look at all the doctors, nurses, and administrators required to keep this place running.”

Instead, you probably walked in, sat down in the waiting room, filled out an ungodly amount of paperwork, and then saw your doctor. But behind the scenes, the engines were humming.

To keep the business of “you” operating like a well-oiled machine, you must have a robust understanding of your cash flow. Gone are the days when you never analyze your income. Gone are the days when you don't think about how much money you spend. Gone are the days of claiming ignorance. Though you don't have to memorize every expense or transaction in your life, you do have to have a holistic understanding of them.

A money makeover is completed in incremental steps. It takes time, patience, and practice, but it produces disproportionate results. Those who take the time to budget win big. That is exactly what you will do here.

Think Big, Win Big

The human brain is an incredibly powerful tool. Our brain allows us to do extraordinary things like remember the past and predict the future. Our capacity for forethought, contemplating the future, and premeditation are uniquely human. Success, it turns out, is deeply rooted in our ability to see the future.

In psychology, there are countless pages of research dedicated to the study of goals and goal-setting. This information provides researchers a glimpse into how humans create the future. In this research, a concept known as goal self-perpetuation explains the reason for mounting success. The idea is that if people set real reachable goals, they will further their success by producing an environment in which winning is attainable. That is precisely what budgeting achieves: the process of setting up small wins that eventually compound into success.

Budgeting also sets up financial bumpers to keep you in line. For some reason, people tend to cringe at the idea of these boundaries. The highly personal nature of budgets produces this visceral reaction. If you boil a budget down to its component parts, a budget encompasses all of the underlying benchmarks by which society judges people: how much money you make, how much you spend, and how much wealth you have accumulated.

You were not taught how to budget properly in school. As a result, you have fear about how to set up a budget correctly. Getting a grip on your finances and budget is the fastest way to gain confidence and correct the areas of uneasiness: income, spending, and savings. The good news is that I am going to teach you how to create a budget. You will be able to use this method for the rest of your life and tailor your budget to meet both your short-term and long-term goals. Once you grasp this concept, you will be able to dominate your finances.

The beautiful thing about budgets is that they give you total autonomy. The independence and freedom to dictate your future are remarkably empowering. You hold your future in your hands. Budgeting for today, this month, or this year will set you up to win big in the future.

The Pareto Principle

Efficiency is something that we all crave. Every business, nonprofit, and household wants to yield more output with fewer inputs. This impulse to operate efficiently is rooted in our desire to spend more time doing the things we love. In budgeting, this can be accomplished by harnessing the power for the Pareto principle.

The Pareto principle states that roughly 80 percent of effects come from 20 percent of the causes.3 This principle highlights the observation, that a majority of results actually come from a minority of inputs. Management consultant guru Joseph Juran popularized the principle as the “80/20 rule” among Silicon Valley startups.

Throughout the last several decades, this 80/20 rule has been applied to a variety of business sectors, such as manufacturing, real estate, and venture-backed startups. The core thesis is that by only concentrating on “what matters” and ignoring everything else, businesses can produce more, increase their bottom lines, and make their customers happier.

Anyone who craves producing more with less has flocked to this idea.

The principle is also applicable to our daily lives and routines. The theory can be used in unexpected places, from your closet, to time spent with clients, to output at work, or even your finances.

By learning how to concentrate only on the essential tasks, you can free up space to do more of the things you love. From a financial perspective, you make hundreds of transitions every month. When you pause to analyze them through the lens of the Pareto principle, you start to see that not all expenses are created equal.

There are categories in which you spend a disproportionate amount of money and may not align with your passions. By honing in on these areas and eliminating them, you can stop spending on things that don't maximize your happiness. By aligning your monthly spending with your passions you capture the full power of the Pareto principle.

Passion Budgeting

If you enjoy things that bring you pleasure, then this section is for you.

This is probably the most pleasurable budgeting process on the planet. It begins with examining things in your life that bring you joy and ends with removing everything else. The passion budget focuses on optimizing your financial decisions so that you can pay off debt faster, save more, and get to the rich life. The passion budget helps you clean out the clutter in your financial life and frees up your decision-making to accelerate your path to budgeting bliss.

“Americans spend $1.2 trillion annually on non-essential

goods—in other words, items they do not need.”

—Joshua Becker4

Bestselling author and tidiness guru Marie Kondo has become an international sensation after building a massive movement centered around removing “clutter” from people's lives. In The Life-Changing Magic of Tidying, Kondo urges clients and readers who live clutter-filled lives to adopt a new outlook on the things that they own. She advocates that the items you possess should be judged through the lens of passion. The quantity of material possessions is not Kondo's focus, only the quality of passion the items elicit. In her philosophy, the test for passion is binary: Either the object sparks passion, or it does not. Kondo argues, “If the object sparks joy in your life, then keep it.”5

Build a budget that sparks passion in your heart.

Passion budgeting uses the Pareto principle in a new way, because passion budgeting advocates that you should spend your money in areas that make you happy. Why hassle over pennies on purchases when you could strike directly at the core of your spending problems and absolve yourself of guilt when you do spend? However, in the areas that don't spark passion, you should cut your expenses ruthlessly. This is vital to long-term success.

This passion-centric approach to budgeting yields lasting results by examining the things that bring joy into your life. Follow these four steps to decipher what you need to focus on in your budget.

1. Investigate Your Expenses

The first step to passion budgeting is to assume that you are eliminating all of your expenses. Start with a clean slate. Then gradually add items back into your budget, but only those that spark joy or passion.

Don't get me wrong, everyone needs the essential elements of their budget (housing, food, transportation, and so on). The difference is that passion budgeting urges you to spend your money in proportion to your wants. In other words, focus your spending on the categories that matter the most to you. By assigning a weight and importance to each type of expense, you will be able to focus on what drives meaning in your life.

So, where do you begin?

The best predictor of future behavior is past behavior. Take a look at your bank and credit card statements from the last three months. With all of these statements in hand, grab a highlighter and mark the best purchases that you made throughout the last three months. This time frame gives you a clear view of your purchasing behaviors. The criterion for highlighting these purchases is simply whether those purchases sparked joy in your life. If so, then the purchase gets highlighted.

For example, if you love going out to eat, highlight all of the times you went out to dinner. Or if you enjoy working out, highlight your gym membership and any purchase associated with health. Once you are done highlighting, grab a black marker and circle every purchase that was not highlighted.

The chances are that you have a much larger part of your bank statement or credit card statement circled in black rather than highlighted items that spark joy. This is typical. People usually spend the most money on things that do not even matter to them.

2. Analyze Your Passion Categories

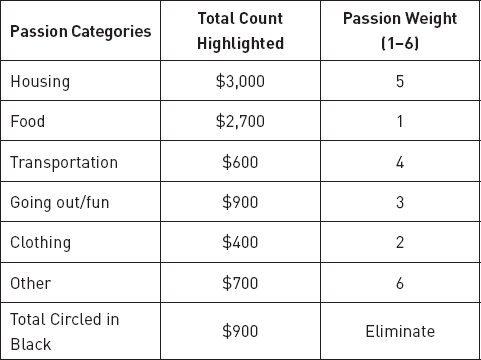

Now that you have a starting point for your new budget, it is time to take it one step further. Look at all of the items that you highlighted in Step 1 and group them into categories. Then assign a weight to each category (1 being the best and 6 being your least favorite). In the following chart there are six major expense categories for you to tally up all of your highlighted purchases. Additionally, it is important to summarize all of the expenses that you circled in black too. Go to MillennialMoneyMakeover.com to download your own passion categories spreadsheet.

After you have analyzed your expenses and summarized them by passion category, the next step is to select the top three areas in which you want to continue spending. These are most likely the top three weighted areas in your passion categories (in the example above—Food, Clothing, and Going out/fun). You should keep spending in these areas (although you might need to regulate total dollars spent) and reduce your spending in the bottom three weighted categories.

Next, take a look at the total amount that you circled in black. This is probably your most significant area for improvement. Investigating the consistency of these expenses will help you determine what to focus on. Sit down and analyze your spending behavior. It is essential to determine how much spending to eliminate in the areas that do not spark passion.

Once you choose an amount to cut, say $200, eliminate that sum from your monthly spending. Instead of spending that money on things that you don't care about, you can now put that $2,400 in annualized savings toward paying off a credit card, eliminating a student loan, building up your retirement nest egg, or investing.

3. Prioritize for Budgeting

You can't manage what you don't measure. Now that you have a clear view of your spending behavior, you need to incorporate this knowledge into building a budget and track your progress.

Don't make the same mistakes twice; when you start to create your budget, prioritize what makes you happy. If you are in debt and need to eliminate expenses in your life to allocate toward debt elimination, then cut the areas that you don't care about. If your goal is to save for a wedding or start a retirement account, the same strategy applies.

For now, take some time to prioritize what matters to you. The entire point of creating a budget is to give you an unobstructed view of the future. It is entirely up to you to take advantage of this opportunity.

4. Build a Passionate Income

Now that you have examined your expenses, it is critical to turn your attention to your income. Generating passion in how you make money is just as important as spending on things that make you happy.

Do you love your job? Does it spark passion into your life?

Be honest with yourself here. There should be joy in your work. The daily commute should not be dreaded. Instead, it should be something that cultivates purpose and joy. These are vital elements to a successful and long career. If your job sparks passion and happiness in your daily life, then you are one of the lucky few.

As Millennials, we are the most educated generation in history and we suffer from severe expectation dissonance. For many of us, when we finally made our way into the real world and began adulting, we realized the chasm between what was advertised for our profession and the reality of the daily grind. This is what a lawyer does? This is what an accountant does? This is how you sell insurance? This is how politics work?

We yearn for more. And if you can't find immediate passion in your current job, then focus on building up your resume in something that does spark joy, such as freelancing, a side hustle, or new business. By combining joy, interest, and purpose into your career, you will set yourself up to make more money in the long run.

Now that you understand the importance of incorporating passion into both your income and expenses, it is paramount that you maximize this theory. In the next section, you will work on actually creating your budget.

How to Budget Passionately

As of 2016, Millennials represent the largest generation in the United States workforce.6 This means that the majority of people in their twenties and thirties are employees experiencing the art of business for the first time.

Managing your finances is much like running a business. For the vast majority of people, this means hardwiring a different type of approach to how you handle your money. As a participant in the real world, the time has come to control your life. And that begins with budgeting.

The act of creating a budget has an illuminating effect on your finances. The process can magnify areas for improvement and emphasize areas you are already dominating. As you will see, the basics of budgeting are quite simple, but the remainder is nuanced.

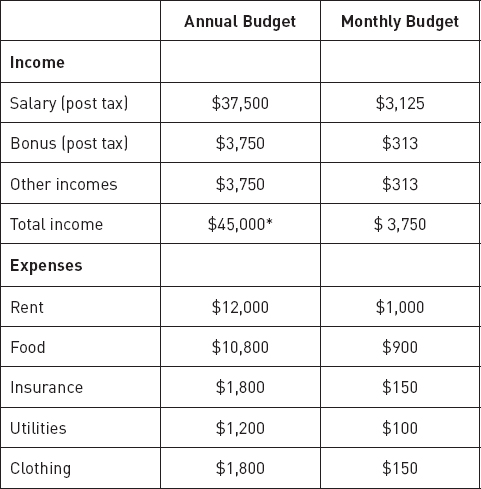

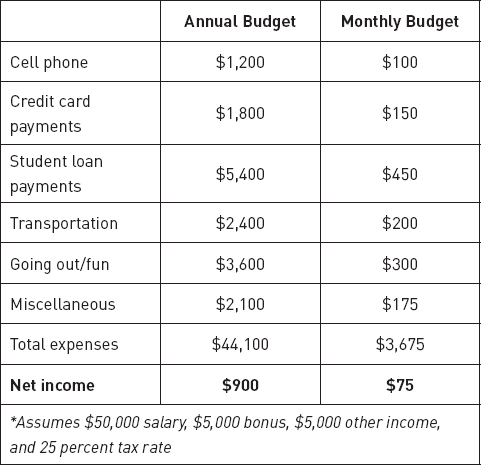

The first step is to list out all of your sources of income. Next, you will list out all of your expenses. You can use your passion expense categories as a reference point. Lastly, you will subtract your total expenses from your total income. You will either be left with a positive number (yes!) or a negative number (no!). Look at the example chart below to get an idea, then download a blank spreadsheet from MillennialMoneyMakeover.com and take a crack at it.

How did you do? If you got a positive number, then you are on the right path. But you will learn how to make this higher. If you had a negative number, don't panic—yet. This is an iterative process, and you will learn what areas to tweak to get to your goal.

Now that you have a holistic view of where you stand, it is time to dive into each component of your budget. Most financial coaches start by focusing on your income. But as you know, most people are pretty much locked into their current earnings, which makes it harder to adjust this number quickly. Although we will cover ways to increase your income, the fastest area of improvement lies in your expenses.

By focusing on restrictive behaviors, like reducing consumption, you can start seeing the results you want immediately. Not all expenses are the same, and it is incredibly important to know which ones to concentrate on.

In the next several sections, we are going to analyze expenses as a whole because focusing on this area of your budget can produce serious benefits, freeing up money to use in other areas. By applying a restrictive strategy to your expenses and maximizing your spend, you will be able to amplify your results.

Variable Vanities and Fixed Costs

There are two main types of costs in life: fixed costs and variable costs. Learning about each type will increase your financial acumen and give you a better understanding of which purchases to control. By learning which types of expenses cause a disproportionate amount of problems in your budget, you ignite the catalyst to your money makeover.

“An important distinction is that rich people buy luxuries last, while

the poor and middle class tend to buy luxuries first.”

—Robert Kiyosaki

Variable Vanities—Get a Grip

The beautiful thing about variable costs is that they are completely controllable. Variable costs are costs that rise and fall in proportion to the goods or services you consume. They vary from month to month and can include food, entertainment, utilities, clothing, and transportation.

For example, if you examine how much money you spent on clothing throughout the last six months, chances are you did not pay the exact same amount per month. Instead, you may have purchased new shoes one month, a bathing suit the next, and four shirts the following month.

Here is where dealing with variable costs gets fun. The costs that rise and fall the quickest are often the most unnecessary. Sure, you may want new shoes, but do you really need them?

Overall, cutting variable costs is a crucial element to success when you are trying to improve other areas of your financial life, such as making higher debt payments, building a savings fund, or purchasing investments.

Eliminating life down to the studs is not a successful approach to create sound financial habits. Small pleasures make up our day. For example, I love coffee. There is no way I would ever eliminate my morning espresso consumption. Although my monthly Nespresso bill is directly correlated with my espresso consumption, it is a cost I will never remove because I would not be happy in my money makeover. Marrying the things you enjoy in life with your budget is critical for long-term success. That is where passion budgeting comes in; cut the costs that you don't care about.

Fixed Costs—Keep Them Low

Fixed costs are the exact opposite of variable costs. By definition, fixed costs are expenses that are not dependent on the consumption level of a certain set of goods or services. They tend to be longer-term and have a set contracted amount. They can include your rent or mortgage, a monthly gym membership, student loans, or car notes.

Although variable costs offer the opportunity to pick the low-hanging fruit from your budget, fixed costs are where the high expenses reside. If you can adjust these to acceptable levels, you will disproportionately affect your budget.

Let me give you a real-world example. When I moved from New York City to Austin, I was able to cut my rent by more than 45 percent, while at the same time keeping everything else in my finances constant—income and variable costs. This simple adjustment alone freed up more than $500 per month in my budget. Imagine what you could do with $500 extra dollars a month for one year: save six times as much as the average American, pay off 20 percent of the average student loan, or eliminate the average Millennial credit card debt.

If you aim to accrue financial intelligence and change the behaviors that genuinely matter, then you need to focus your efforts. Hone in on the major players in your life: fixed costs. Worrying about eliminating small expenses, which erode your happiness, is not an effective strategy. This may not be the traditional approach, but it is essential to determine what truly impacts your money.

Happy Spending

Now that you have learned how to build a budget and determine the types of costs to keep, it is essential to examine how to maximize your spending. In this section, we will examine how to best spend money. It turns out what we spend our money on can make us feel richer and more fulfilled. This is the fun part.

In their groundbreaking book Happy Money—The Science of Happier Spending, psychologist Elizabeth Dunn and Harvard Business School professor Michael Norton examined a curious question: Does the way in which we spend our money affect our happiness? The answer is: absolutely.

Dunn and Norton found that spending your money in the five following ways can increase your financial outlook.7

- Buying experiences: This principle is driven by the premise that buying experiences over material purchases is better in the long run. The novelty of new purchases tends to wear off over time, while experiences such as a vacation with family or a concert with friends can be mentally revisited over and over, thus allowing the consumer to extract more pleasure from the purchase.

- Making it a treat: Do you love dining out and trying new restaurants? Instead of eating out every week, make it a treat and reward yourself only after a major accomplishment. Once you receive that promotion, hit that goal, or earn that annual bonus, then and only then, splurge on going to that swanky new restaurant. This strategy will make the happiness of the purchase last longer and ties a positive memory to the reward.

- Buying time: Let's face it. We are all a little selfish. Buying time allows us to do what we want when we want. If you love reading but your house is a complete disaster, then hiring a maid to clean while you enjoy your book is a fantastic use of capital. This decision creates the needed time for you to read and simultaneously completes a household chore. This concept is life-changing.

- Paying first and consuming later: Credit cards have turned the traditional payment sequence upside down. Today, the mantra is to consume first and pay later. But prepaying draws on the idea that paying early, and with cash, increases the pain of the transaction and places the pain before consumption. By prepaying, we bask in anticipation of the purchase longer, thereby drawing a longer mental value from the purchase.

- Investing in others: Helping those in need is a core value of the American way of life. We are taught at an early age that sharing, giving gifts, and making charitable contributions is the responsible thing to do. It turns out following this advice can make our wallets feel heavier. The act of giving makes us feel more affluent and increases our overall well-being.

We all have to spend money. So, we might as well do it intelligently. By focusing on the five ways to increase our happiness through spending, you can leverage your budget to your advantage. Remember these principles as you progress throughout the budgeting process and the rewards will be twofold: financial health and increased happiness.

Financial Rules of Thumb: Myth vs. Reality

To determine whether you are in line with good financial practices or incredibly off base, the finance industry has provided rules of thumb. These rules are distributed in an attempt to give you a baseline of comparison and keep your costs under control. The problem is that these rules are wildly generic and offer terrible advice. There are three of them that I'd like to tackle head-on.

Debt Myth: Your debt payments should not exceed 20 percent of your take-home pay. The implicit assumption in this rule is that it is acceptable to finance your lifestyle. That drives me crazy. This rule allows you to allocate a substantial portion of your take-home pay to finance credit card debt, student loans, or consumer debt. The issue is that the average college graduate will have $37,172 in student loans and some credit card debt sprinkled on top of this as well.8 Based on the average graduating salary, the average debt payments are already approaching, if not exceeding, 20 percent of take-home pay, which is a financial disaster.

Debt Reality: Once you become debt free, you should remain debt free. After paying off all of your debt you should stay in the black, plain and simple. The controllable debt in your life should be eliminated. The only true exception here is a mortgage, which we will discuss in Chapter 4. Because your primary goal should be to alleviate yourself from debt completely, there is no turning back to debt after you have completed your money makeover.

![]()

Housing Myth: Your housing payments should not exceed 30 percent of your take-home pay. The problem with any standard is that human behavior migrates to the mean. People will get too close to this standard, if not exceed it. Setting the standard housing payment—rent or mortgage—at 30 percent of your take-home pay is ludicrous. The problem is that housing will be your highest fixed cost and it is a long-term commitment. Your goal should be to keep this as low as comfortably possible.

Housing Reality: Your housing payments should not exceed 20 percent of your take-home pay. Keeping your housing cost at or below 20 percent will free up the necessary cash in your budget to construct a healthy ecosystem—paying off debt, building up a savings cushion, investing to grow your wealth, and stashing away cash for retirement. You cannot complete all of these necessary things at the appropriate rate by spending more than 20 percent of your take-home pay on rent.

Now, before we move on, I want to address everyone in the peanut gallery: What about New York, Los Angeles, Chicago, and Boston? It is impossible to spend just 20 percent of your take-home income on rent!

This is a makeover, and if you want to expedite your path to financial freedom, then you need to consider moving to a city where you can afford to live. If you live in a city that eats up more than 20 percent of your discretionary income solely on rent, it is time to make some hard choices. This is not a book on how to stay in the rat race. This is a book about jumping off the wheel and finding the richness of life.

There is good news though. Once you have built up enough savings, you can move back to these cities. Geographic arbitrage is very real and tangible. Take advantage of this.

![]()

Savings Myth: Your savings should be at least 15 percent of your take-home pay. This rule is not as bad as the rest because at least it advocates saving. But 15 percent will not get you where you want to go. If you have read this far, I know that you are “all in” on the money makeover. Although 15 percent will get your savings headed in the right direction, you will need to crank this up as soon as possible.

Savings Reality: Your savings should be at least 30 percent of your take-home pay. The fact that you are saving means that you are ahead of your peers. By saving at least 30 percent of your take-home pay (once you are done paying off your debt), you will be speeding down the highway to riches. As that 30 percent begins to accumulate you will find that the worries you had before suddenly begin to disappear.

Saving, and then investing, is the quickest way to cross the money makeover finish line. Ratchet this number up as high as you can and automate this decision (more on this in Chapter 6).

When you are setting up your passion budget, it will be important to allocate where you are spending your money correctly. If you are leveraging the Happy Money principles and looking for places to optimize your spending, this can be a painless and fun process. There will be areas where you can cut and others where you can splurge. The important point is to focus on getting the biggest bang for your buck.

![]()

The rules of thumb are exactly that—standard. Your money makeover is anything but standard. The process of financially redefining yourself requires a change in perspective. Adopt the money makeover rules of thumb, and they will serve you well.

Socioeconomic Downsizing

Financial success can be engineered. The problem is that the equation runs dangerously juxtaposed to our ingrained social values of consumption and hyper spending. In a world run by Facebook, Instagram, and Snapchat, it is far too easy to be lured into the false assumption that everyone is in the one percent. Social media exacerbates this notion, and as a result, we are always worried about the fear of missing out.

Raised in a world where having the latest phone, car, or clothes is the proverbial choice, it comes as no surprise that savings and delayed gratification are becoming extinct concepts. However, the key to getting ahead financially is to embrace these generationally archaic concepts by socioeconomic downsizing.

“Live like no one else today so you can live like no one else tomorrow.”

—Dave Ramsey

By definition, socioeconomic downsizing is the active choice to live one or two rungs lower on the economic ladder than your current income allows. Let's look at an example.

Jane and Bob, a happily married couple from Dallas, each earn $50,000. With a combined total household income of $100,000, they are in the top 28 percent of household incomes. They have two choices: to live high on the hog or to socioeconomically downsize. They choose the latter. With this choice comes a significant adjustment in lifestyle. Their discretionary spending on rent, food, and fun changes drastically. This choice to downsize completely alters their day-to-day life.

Instead of living in the nicest part of town, paying a monthly rent of $1,100 (or roughly 20 percent of their monthly take-home pay) the couple will pay $550 if they choose to downsize. Instead of spending $600 per month on financing new cars, Jane and Bob will drive cars they own if they choose to downsize. Instead of taking two ski vacations this year, they will embrace a staycation if they choose to downsize.

So, why would anyone choose this masochistic path?

The answer is: This choice allows Bob to save his yearly salary of $50,000. After three short years the couple will accumulate $150,000 in savings, or 1.5 times their household income. As the emergency fund, slush fund, and retirement savings begin to build, Jane and Bob can start the process of shopping for their dream house, purchase new cars, or start saving for their children's college tuition. They have already put in the sacrifice early to accumulate their base savings. The couple can now take enjoyment in watching their investments grow for the rest of their lives. For them, the hard part will already be over.

Now that we have sufficiently covered how to stretch your spending and analyzed strategies for boosting your happiness along the way, it is time to turn your attention to the top line of your budget: income. Increasing your income can alleviate the stress of managing an anemic monthly cash flow. The first step is to determine how you measure against your peers, and then contemplate how to leverage your existing skills and assets to garner more income.

Where Do You Stand?

Comparison offers a proxy for reality. Knowing where your salary stands among your peers gives you the ability to see how on or off track you are trending. In their groundbreaking book The Millionaire Next Door, professors Thomas Stanley and William Danko establish the positive correlation between high incomes and the ability to generate wealth. Intuitively, this makes perfect sense—the higher your income, the more money you can put toward saving and investing. Of course, this only happens if you can avoid the pitfall of amassing high levels of debt because you think your high salary will fuel your spending machine.

“I don't care what anyone says. Being rich is a good thing.”

—Marc Cuban

In the long run, your ability to increase your income can have a significant impact on your ability to pay off debt, generate needed savings, and fuel your desired lifestyle. Knowing where you stand among your peers can give you the relative insight into how well you are performing.

Luckily, with data collected from a 2015 survey, Business Insider can give you that needed glimpse. From the survey data, Business Insider calculated the income levels necessary to be in the top 50 percent and the top 1 percent of Millennial earners. The results might make you seriously reexamine your earnings.

At the young end of the spectrum, the data found that a twenty-five-year-old worker needed an income of $31,000 to be in the top 50 percent of earners, while an income of $116,000 was necessary to reach the top 1 percent.

As you might expect, the income numbers continued to climb in direct correlation with the age of the Millennial worker. In the middle of the data, a thirty-year-old worker needed to generate $40,000 to be in the top 50 percent, while a whopping $173,000 of income was required to reach the top 1 percent. This trend continued with their older counterparts, who at thirty-five-years-old needed an income of $45,000 to remain in the top 50 percent but a staggering income of $291,000 was necessary to earn a spot in the top 1 percent.9

So, where do you stand?

If you feel behind, don't freak out. There are plenty of ways to increase your income, all of which you can start working toward today. This might mean gunning for that promotion at work, starting your own business, or freelancing.

Readers might find themselves in the top income brackets but don't feel rich at all. This is because they are not living the rich life. Proper money management does not increase with financial position. The “just in time” lifestyle is just as dangerous for the janitor as for the judge. If your salary increases and financial literacy remains constant, then your problems will only grow in size.

Wherever you fall on the income chart, it is important to keep in mind that although increasing your income is highly correlated with long-term wealth, it does not guarantee financial success. How you handle your money is just as important as how much you earn.

Increasing your income has tremendous benefits on your ability to pay off debt, accumulate savings, and start investing. Let's examine a few ways to upgrade your lifestyle.

From Side Hustlers to Entrepreneurs

Philip Taylor is a successful entrepreneur, writer, and businessman. Nick Loper is a podcast extraordinaire, TEDx alumni, and Chief Side Hustler at Side Hustle Nation. Nicole Lapin is a television host and bestselling author. They didn't all start this way.

This section is dedicated to showing you real-world success stories of people who have turned their quest for more money in their budget into full-time, and highly profitable, careers.

PT Money

In April 2007, Philip Taylor made a purchase that would alter the course of his life: his blog domain name. Since that day, Taylor—or PT Money, as most of his readership knows him—has become a sensation in the personal finance community.

A certified public accountant by trade, Taylor was working as an internal auditor in a corporate environment and making six figures. But something wasn't quite right.

Like most young professionals, Taylor was working to get his finances in order and was reading vigorously on the topic of money. But at that moment, in the calm of corporate life, Taylor decided to “quit consuming and start creating.”10 He wanted to become part of the financial conversation.

After starting his personal finance blog, PTmoney.com, Taylor's efforts started paying off. Within a couple years, Taylor was making $40,000 from blogging (in addition to his corporate salary), and he was beginning to put his newfound cash to good use.

“I was using that extra money to get my finances in order. I was paying off consumer debt with the extra cash and starting to get operationally lean in my daily expenses,”11 said Taylor. Taylor's success came in the form of a two-pronged approach. Step one was to generate extra cash from his new side business, and step two was to cut expenses simultaneously. The formula worked.

Two years after launching PTmoney.com, Taylor made the leap from corporate life to full-time entrepreneur. Since then, Taylor has developed a strong following among his readers and his website has millions of page views a year.

I asked Taylor what advice he would give to readers who want to turn a side business into a full-time opportunity. “Get your finances in the best shape possible. Be as lean and mobile as you can,” says Taylor. “Business is not about the ‘me versus them’ attitude. Instead, work with your competition as collaborators. Go find the people who have done what you want to do—set goals, set expectations, and move forward.”12

Although Taylor has already found his success, he still thinks the Internet is wide open with opportunity. The only question is: Who will seize the moment?

Nick Loper

In his 2014 TEDx talk, Nick Loper delivered an unorthodox message. Playing to an older crowd, Loper gave the audience a sound bite they wanted to hear: Millennial are entitled. What the crowd didn't expect was Loper's new twist on the subject.

His message was: Yes, Millennial are entitled. They are entitled to the pursuit of their dreams, and our future economy fundamentally depends on Millennials' unprecedented pursuit of entrepreneurship. Loper is speaking from first hand experience.

In 2005, Loper was stuck in a sales job with Ford Motor Company that wasn't sparking passion. Assigned to meeting monthly sales quotas, Loper yearned for a creative outlet. After some experimentation, Loper created his first successful online business, and from that point, his days at Ford were numbered. He has since gone on to develop several successful online companies, his most noteworthy being Side Hustle Nation. As “Chief Side Hustler” at Side Hustle Nation, Loper has dedicated himself to helping others turn their part-time passion projects into full-time employment.

His Side Hustle Show podcast, which has been running weekly since 2013, boasts a burgeoning collection of notable guests. A typical show might include a quest to find out how other people bring their business from $0 to $50,000 a month, like Michelle Schroeder-Gardner of Making Sense of Cents, or how successful founders of multi-million-dollar businesses get their start, like Noah Kagan, the founder of Sumo. Loper's audience loves hearing about real-world people creating, growth hacking, and building their way to profitable businesses. The numbers speak for themselves.

The Side Hustle Show has more than five million downloads. What started as a passion project for Loper has morphed into a successful business. In an interview with Loper, I asked what advice he would give to those trying to make more money with their side project. Loper reminded me that everyone starts at the same point: zero. Loper emphasized, “The best opportunities aren't visible until you are in motion. The practice of getting started leads to new opportunities.”13

The only direction, it seems, is up.

Nicole Lapin

Among the offices of CNN and CNBC, Nicole Lapin is the youngest anchor ever at both networks.14 Lapin cut her teeth early, and that experience has paid dividends for her career.

Lapin leveraged her early start covering business news and is already starring as the host of the business show Hatched on the CW, a show dedicated to connecting emerging brands with successful mentors.

When Lapin isn't helping entrepreneurs turn their businesses into success stories, she is working on her other side projects. And those projects have been tremendously successful.

Lapin is the author of two bestselling books, Rich Bitch and Boss Bitch. Her breakout book Rich Bitch, a personal finance guide for women, made the New York Times Best Sellers list.15 So, she doubled down on the momentum and started writing a syndicated personal finance column for Redbook Magazine.

After the initial success of her debut book, Lapin did the unexpected and churned out another bestseller, Boss Bitch. This book focuses on taking charge of your life and offers advice for women in their careers and personal lives.16

![]()

All three of these entrepreneurs embody the rewarding principles of the money makeover on their journey toward financial and career success. The workman-like approach to chasing their dreams, while simultaneously increasing their income, should serve as inspiration. You can always find ways to push the boundaries of your career, life, and budget.

If you need extra cash to help expedite paying off your credit cards, student loans, or building up your savings accounts, then I have good news. We live in an age of online businesses, the sharing economy, and many other accessible opportunities. The process of making more money has never been easier.

How to Ask for a Raise

If you feel like you aren't making enough money, you are in good company. According to a 2016 analysis of Federal Reserve data, Millennial are earning a whopping 20 percent less than their parents at the same stage in life.17 With systemic economic problems diffusing into the daily lives of millions of Millennials, young professionals feel behind.

If you feel overworked and undercompensated, there might be more money lurking right under your nose. Asking for a raise might be a great way for you to earn more money and simultaneously establish career momentum. But just asking for a raise could be damaging to your relationships in the workplace. Instead, you need to develop a winning strategy. Asking for a raise can feel intimidating, so build up your confidence by taking four concrete steps to solidify your raise.

1. Determine Exactly What You Want

The art of negotiating a raise begins with some self-reflection. If you are building up your confidence to ask for a raise, then you must have a reason. Are you feeling overworked? Do you think you deserve a promotion? Are you getting equal pay for equal work?

At the core of your desire to ask for a raise, something is troubling you. You need to use this opportunity to identify the issue. If you think you deserve a promotion, then you need to demonstrate your case in a clear and concise manner. If you want a 10 percent increase in salary, then you need to articulate how you go above and beyond your current job description.

It is critical to be as specific as you can when developing your goal. Pinpointing your “ask” will allow you to construct a roadmap to achieving your goal.

2. Develop Your Plan

With your goal now formalized you have something to aim toward. The problem is always “How do I get from A to B?” First, you should take a deep breath and realize that whatever you are trying to accomplish has already been done before.

If you are gunning for a promotion, then examine the job description of the position you are pursuing. What are the baseline criteria? Have you achieved them all already? If you have, then you need to do it again, but this time with your boss noticing. If you have not met this baseline, then you need to figure out how to incorporate those new skills into your daily work. Give yourself time to strive toward your goal. Write down three things that you can improve upon over the next three months.

Let's say you are an account manager. Your first month's goal could be to get a handle on all of your existing accounts. The second month could be replicating the first month's efficiencies plus landing a new client. The third month may be doing everything in the first and second months and additionally mentoring junior account associates. In three short months, you will have developed great rapport with your accounts, gained new business, and demonstrated your management ability.

3. Set an Ask Date

Asking for a raise without coming to the table with tangible results is a terrible idea. So if you need more than three months, then you should take the time to meet your objectives. However, once you are ready, showing up to a meeting with a list of accomplishments will speak volumes about your skill set and what you have to offer.

While working on establishing your list of accomplishments, map out a timeline of when you want to ask for your raise or promotion. I suggest doing this well before your company's typical mid-year and year-end review periods.

The reason you don't want to have this critical conversation during your regular compensation meeting is that the decision about your future has already been made. The executive suite has already determined who will get raises and promotions. Showing enthusiasm and drive before these meetings will allow your superiors to advocate on your behalf during performance evaluation meetings.

Understanding the timing of when to present your reasons for advancement is almost as important as the reasons themselves. As they say, timing is everything.

4. Deliver and Get Feedback

Once you have set your ask date, the last thing to do before your meeting is to write down your expected outcome. This will give you a clear means to decide if you received the answer you wanted, especially after the fog of the conversation evaporates. Otherwise, there is no way to determine whether you were successful or not.

After you have your meeting, it will be important to examine the result. Did you get what you asked for? Was it better or worse than you expected? Did your receive a contingent answer?

Whatever the result, write down exactly what happened. This will serve as an excellent reference for future negotiations. If something did not work, then maybe you need to adjust a variable to make the conversation more successful.

Asking for a raise can be a crucial part of career development. Your bosses may not realize how hard you are working. They might take you for granted. They might happily give you a raise. Either way, the important thing is that you asked. That is a win.

By bolstering your income, you will be well on the way to developing a more sophisticated budget. The next step to building a passion budget is to make sure you are adopting the right processes to win over the long term. These processes and maxims will serve as guiding forces as you scale your success.

Adopting a Savings Process

After optimizing your budget to increase your income and leverage your spending, it will also be crucial to build savings into your routine. Defining how much you want to save ties back into your goal-setting from Chapter 1.

“Don't save what is left after spending; spend what is left after saving.”

—Warren Buffet

For example, if your goal is to buy your first car, then you need to calculate a total savings goal. Knowing this total goal allows you to deconstruct your overall savings goal into yearly, monthly, or weekly components. Meeting these intermittent goals dramatically increases your chances of overall goal achievement.

The following tips can help you improve your odds at accumulating those small wins.

1. Pay Yourself First

If you are like most people, the end of the month leaves you scratching your head, wondering where all of your money went. The typical process goes something like this: Your paycheck comes in, the monthly bills are paid, and you save (if you are lucky) what is left over. This is a poor way to accumulate savings.

The cable bill, rent, utilities, and car payment all come before your savings goals. This haphazard way of managing your finances prioritizes paying expenses above savings and yields low results. My guess is that this method has not worked for you either.

To meet your savings goals, you need to readjust the order of operations and start paying yourself first. When your paycheck comes in, your savings goal should be deducted first. Everyone else who has a claim on your money can wait.

Without the critical decision to prioritize your savings, you will always feel like you are underachieving. Stop the cycle of under accumulating by paying yourself first.

2. Automate Your Savings

Once you start paying yourself first, the next step is to automate the process. By automating how much to save, you increase the probability of meeting your savings goals and simultaneously remove the temptation to spend your savings.

The best way to automate your savings decision is to make the decision once and apply the “set it and forget it” method. Most payroll providers have the ability to directly deposit funds into a separate account before your paycheck hits your primary bank account. If you are not sure if your payroll provider has this function, then consult with your human resources department. The alternative is to set up automatic deductions from your bank account to your savings account. Both methods are highly effective.

Ultimately, the trick is never to see your savings enter your spending account or, at the very least, have it stay there for as little time as possible. By not ever seeing the money in your spending account, you feel no attachment toward the money. As a result, your savings are left alone to accumulate.

3. Save Extra Pay

As you read earlier, our economy has endless ways to make more money. Whether you increase your pay through the traditional path of career progression or find successful side hustles, putting your newfound wealth into savings will expedite your ride to the rich life.

By making the decision to put all extra money into your savings, you alleviate the income trap. The income trap theory is: When you earn more money, you tend to spend more money. This is a philosophy of the financially unhealthy. The issue with the income trap is that as incomes rise, so too do the size of financial mistakes.

The best way to protect yourself from these mistakes is to preemptively allocate your savings by automating the decision. By doing this, you will not feel the temptation to start spending your extra income. Of course, all work and no play is an unhealthy recipe. You should treat yourself occasionally while still keeping your savings momentum going.

4. Track Your Progress

Metrics matter, so it is important to monitor your performance. While you don't need to track your progress daily, it is essential to keep a regular pulse. After all, there is a reason that you are working hard to save your money. A fun and effective way to track your goals is to name your savings accounts. For example:

- Down payment on our first house

- Honeymoon fund to Thailand

- Wedding and bachelorette parties

- Annual ski trip to Vail

Research conducted by Dr. Brad Klontz of Creighton University found that naming your savings accounts could dramatically increase the odds of meeting your savings goals.18 Have some fun during the naming process and make the names memorable. By tracking your progress and assigning purposeful names, your intentions will eventually turn into reality.

Everyone wants more savings. Even affluent people worry about not saving enough. You can mitigate this worry by identifying your savings goals, remembering to pay yourself first, and automating that decision. This series of decisions will catapult you toward success. Finally, don't forget to track your progress and have some fun along the way.

In the following table, find your savings goal amount in the left column and the corresponding savings needed to reach your goal based on the time frame you select in the top row.

![]()

Action Items

An entire chapter on budgeting is a necessary stop on your money makeover. Your financial transformation begins with gaining a holistic view of your financial life. This is often the most resisted, but eye-opening, part of any money makeover. The truth can be an unforgiving teacher.

When creating your budget, remember the following lessons and harness the power of passion budgeting.

- Build a passion budget that works.

- Focus on keeping things in your life that spark passion.

- Understand the expenses that control your budget.

- Make more money; it helps everything.

- Understand that your budget is a living document.

The entire point of creating a budget is to give you insight. The money makeover is about taking that knowledge and applying it purposefully. The information gained from the exercises in this chapter will give you the knowledge, tools, and insights for continuous improvement.

In the next chapter, you will boost your financial mastery even further by learning how to best purchase large-ticket items and position yourself for decades of financial success. I encourage you to put yourself, and your budget, in your stretch zone. That is where the real growth begins.