4

THE MAGIC OF WINNING BIG: HOW TO

OPTIMIZE LARGE-TICKET PURCHASES

Life is too short to be little.

—Disraeli

Richmond, Virginia, is a cozy city nestled along the I-95 corridor. Formerly one of the prizes of the South, the city has not hosted anything big these days. But at the University of Richmond, there is a group of professors who live for big things, especially large numbers.

Intrigued by recent public discourse happening in neighboring Washington, DC, professors David Landy, Noah Silber, and Aleah Goldin set out on a journey to understand the psychology of large numbers. They noticed that politicians and business leaders routinely discuss numbers such as millions, billions, and trillions in the public forum. But, the professors wondered, how well does the public synthesize these numbers? Do people treat these numbers equally? Do people have a healthy appreciation for numbers of this magnitude? Do people have the capacity to compare large numbers?

The researchers conducted a study entitled Estimating Large Numbers. The results of their study were enlightening. An excerpt from the study discussed participants estimating numbers on a number line and revealed that “35% of participants in the study reported here . . . seem to evaluate large numbers on the assumption that the number labels pick out roughly equally spaced magnitudes as the numbers increased.”1

This means that people had an extraordinarily difficult time estimating the right spacing between large numbers, say between one hundred million and four trillion. The size and scale of large numbers seemed lost on participants, especially as the numbers increased in size.

For life's large-ticket purchases, such as buying a car, purchasing an engagement ring, paying for a wedding, or acquiring your first house, people tend to get lost in the numbers. And it's not their fault. Large numbers have a very clever way of manipulating our brains. The abstract nature of their magnitude distorts their size.

If you are like most people, it is difficult to comprehend the value of $500,000 or $1,000,000. This is simply because you do not have very many immediate experiences with transactions of this scale, which leaves you with no point for relative comparison.

We continuously experience small numbers throughout the day. It is quite less frequent that we meet large numbers, and as a result they are harder for us to conceptualize. According to Daniel Ansari, a researcher at the Numerical Cognition Laboratory at Western University in Canada, “Our cognitive systems are very much tied to our perceptions.”2 And as we all know, our perceptions become our reality. The difficulty lies when we start thinking about numbers outside of our daily familiarity. “The main obstacle is that we're dealing with numbers that are too large for us to have experienced perceptually.”3 Large numbers are incredibly hard for our brains to grasp.

Our brains understand this deficiency and have adapted to deal with small numbers very well. For large numbers, we fall into the trap of rounding and estimating. The problem is that the scale of the rounding and estimating increases drastically as the numbers increase, furthering the distortion.

This is when most people make massive mistakes. In this chapter, you are going to learn how to avoid the costly mistakes of making purchases that are too large. You will learn to fight your brain's willingness to convert the non-linear to the linear.

To combat this problem, the professors at the University of Richmond suggest a strategy that translates the unfamiliar to the familiar: Convert large numbers into familiar units. For example, if you are used to dealing in hundred-dollar increments, then convert everything into the hundreds unit. That means $1,700 becomes 17 hundreds. Or $10,000 becomes 100 hundreds.

Use this technique when you are about to make a large purchase. And to make this even more powerful, set your baseline metric at your current savings or investments total. Therefore, if you have $5,000 in your savings account, purchasing a new car for $45,000 is nine times the value of your savings account. This allows for proportionate comparison.

Before you make your purchase, ask yourself: How long did it take to save $5,000? Is paying nine times your savings worth it for this car? These questions reset your mental frame of comparison and allow you to convert the abstract into the reality of known numbers.

This is a secret tool of the rich. And it is instrumental in leading the rich life.

This method is not taught in school nor does is come innately. Instead, it is acquired over time. Some people learn it from observing successful people, others through the drudgery of self-experience.

Learning how to optimize large-ticket purchases is a learned skill set, which will be the difference between long-term financial success and failure. The decisions you make about how much to spend on a new car, an engagement ring, your wedding, or your first house can drastically alter your financial health.

Hang on, because this might be the most crucial chapter yet.

Large-Ticket Purchase 1: Buying a Car

On a brisk September day in 2015, I rushed out of my apartment. The night before I had spent hours scouring the Internet for the best local car deals and had dialed in on my new ride. The new car smell was already in my mind.

As I headed to the dealership, the mounting intoxication of the purchase started to pulse through my body. As I sauntered into the showroom, a salesman (whom we will call “Jeff” for purposes of this book), instantly greeted me. Jeff was smiling wide, adopting the classic car salesman's tool of mimicry because, as we greeted, I caught myself grinning from ear to ear.

As we shook hands, my high started to fade. Reality seized me, and I understood that I was in enemy territory. Car salesmen, I reminded myself, are notoriously slick. They are to be watched with caution. I didn't want this schmoozer trying to sell me something I didn't need.

With my research complete, all I needed Jeff to do was facilitate the test drive. As Jeff and I were approaching the car, he threw me the keys. It was like a scene out of a movie, and I was playing the part.

Compared to my fourteen-year-old Suburban, the new car was like a spaceship, decked out with the platinum package: rearview cameras, GPS, automatic steering, heated seats, smooth leather, and gadgets galore. I was falling in love.

As we headed back to the dealership, I launched into a barrage of questions about the car's capabilities. Jeff answered each one in meticulous detail, furthering the appeal. But pulling back into the dealership, I noticed a curious sensation. A little voice was starting to chirp in my ear, “Ask him how much it is already!” I obliged. Jeff reported, “$40,000.”

The last twelve months of dedicated savings started to flash before my eyes. Had all of that effort culminated into this one purchase? Did it make sense to buy a new car? Maybe I only needed a used one?

Suddenly, I didn't feel quite right. I got the immediate sensation that I needed to escape. I realized that every minute I spent in the car was a minute closer to purchasing the damn thing.

I told Jeff he would have my decision by the end of the week. To assuage the look he threw my way, I gave him my email address and told him to send me the specifics of the deal. I reassured him we would be in touch. (Yeah, right.)

Jeff had lost the deal. And he knew it. So, as punishment, he emailed me for months.

Luckily, I escaped the claws of a horrible financial mistake. All of my hard-earned savings would have been gone. And financial insecurity would have strolled right back into my life. Learning to delay immediate gratification is a learned behavior. I was starting to get my practice in that day. It was a small victory on a long journey.

Marshmallows, Pretzels, and Used Cars

In the fall of 1972, on the beautifully manicured campus of Stanford University, a curious thing was happening in a room with a double-sided mirror. A child was sitting at a table, glancing back and forth between a marshmallow and a pretzel. To the child's delight, he could have whichever one he wanted. It was approaching decision time: a marshmallow or a pretzel?

A couple of years earlier, on the same immaculate campus, social psychologists Walter Mischel and Ebbe Ebbesen were working on an experiment that tested the nature of delayed gratification. They were curious as to how people would react when rewards were placed directly in front of them. The researchers theorized that by placing a noticeable reward in front of someone (think Reese's, M&M's, or a Snickers), that person would be very good at waiting patiently to consume their reward. The researchers hypothesized that an increase in delayed gratification would occur because people would engage in “self-persuasion and anticipatory gratification.”4 At the time, that logic made perfect sense. As it turns out, the opposite was true.

In an experiment to test this hypothesis, children were either exposed to a reward or they weren't. The study revealed that the children who were given the option to consume their reward early did so, but the children not exposed to a reward ended up waiting longer to receive one.

This confirmed the “out of sight, out of mind” mentality.

Curiously though, researchers noticed that the children who were trying desperately not to consume their reward, when it was placed directly in front of them, engaged in “covert and overt distracting responses.”5 These kids were trying to distract themselves mentally or physically from consuming their reward, albeit with limited success.

Picking up on this observation, Mischel and Ebbesen conjured up a means to test a new hypothesis: “Overt activities and internal cognition and fantasy which would help the subject to distract himself from the reward would increase the length of time which he would delay gratification.”6

Would they be wrong—again?

With a group of fifty children, the researchers tested their new hypothesis. In this experiment, children were given the choice of a delicious reward: a marshmallow or a pretzel. Then the children were told the researcher was going to leave the room. If the children waited until the researcher returned, the child would be able to eat their preferred reward. If they decided to bring the researchers back into the room, they would have to eat something else.

The children in this experiment were split into three groups. The first group, upon walking into a room and selecting which reward they wanted (marshmallow or pretzel) were cued to play with a slinky. The second group, after choosing their reward, was primed to think of something “fun” as a means of distraction. And finally, the third group was given no activity. They just had to wait.

The results were fascinating. For the group that was provided no means of distraction, the mean wait time was a mere 30 seconds before bringing the researcher back. By contrast, the group with the slinky reached a mean wait time of 8.59 minutes. What was even more surprising was the result of the third group. Those children who were told to think of something fun achieved a mean wait time of 12.12 minutes!7

So what do the results tell us about human behavior? Well, for one, we are terrible at waiting for a prize when we have no means of distraction. However, if we can distract ourselves with activities like going on walks, runs, hiking, or reading, our resistance can be quite impressive. Additionally, if we can mentally distract ourselves from what we want, we can delay consumption even further. The temptation to eat our life's marshmallow ebbs away if we can adequately distract ourselves.

Six Things to Consider When Buying a Car

Adults are essentially large children. It stands to reason that if we want to consume, purchase, or acquire something beyond our financial means, the best way to combat our impulse is to use distraction techniques. But sometimes circumstance requires us to take the plunge.

Whether your current car broke down, an accident left you carless, or you are a first-time car buyer, you might just need to buy a car. The good news is car designers, manufactures, and salesmen don't quite know what to think of Millennial. They know that we value individualism, trust the experience of our peers, are optimistic, and are technology savvy. This puts us in the power seat.

Use this knowledge, as well as the following six rules, to get the best deal possible for your car.

1. Don't Buy New

Transportation is essential. Whether you are in a big city, suburb, or farm town, how you get around can change your financial outlook. For the money makeover expert, keeping transportation costs low is a key component of economic progress, especially for young professionals.

Before we get too far, I want to make one thing clear: A new car is not an investment. It is an expense. Resisting the temptation to purchase a new vehicle is difficult, especially after years of working hard. Naturally, you want something to show for it. Fight this impulse.

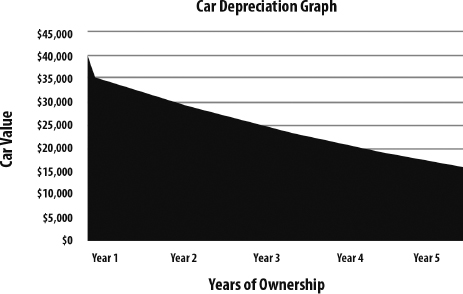

On average, a new car loses about 10 percent of its value the moment you leave the car dealership and another 10 percent by the end of the first year.8 Let this simmer for a moment. If you were to fall to the siren song and purchase a $40,000 BMW, the second the tires leave the dealership, you have lost $4,000 in value.

A car is a depreciating asset, which means it declines in value over time. During the first five years of ownership, a new car value depreciates between 15 and 25 percent every year. Therefore, buying new is a terrible idea because the value of your purchase drops significantly during the first part of its useful life. Check out the rapid decline in value on the BMW purchase in the following chart.

If you are going to buy a car, then buy used. The sweet spot for purchasing used cars is when depreciation plateaus, around year 4 or 5. If you buy in this time frame, the car will have all of the latest features, but you can escape the wrath of the early depreciation curve.

Not all cars depreciate at the same rate. Some brands hold their value much longer than others, so do your research and check out websites like Edmunds.com or ConsumerReports.org to compare depreciation rates on cars you are considering.

2. Don't Lease

At first glance, leasing a new car can seem like an enticing idea. You get to drive the newest cars, forgo the capital expenditure of purchasing, and often receive the option to buy the car at the end of the lease.

Don't fall for it.

According to ConsumerReports.org, “The financial workings of leasing are so confusing that people don't realize that leasing invariably costs more than an equivalent loan. And even if they did, the extra cost is difficult to calculate.”9

There are often hidden fees that dramatically increase the cost of leasing: finance charges, mileage overage charges, or high down payments. The probability of getting a great deal on leasing a car is extremely low. Leasing a car almost always benefits the car dealership. Leasing allows the dealership to move inventory and make money on financing.

Don't confuse short-term affordability with sound financial management. Listen to the professionals who have already run the numbers and are telling you to avoid the leasing trap. Avoid locking yourself into fixed monthly payments because it is financially stifling. While you are in the money makeover, your goal is to free up as much of your monthly cash flow as possible.

3. Think Long Term

Buying a car is one of the largest purchases that you will make as a young professional, so it is important to do it right. Be strategic and think about the long-term nature of your purchase.

Although flashy cars are alluring, buy something that is realistic. The sexy brands typically lack utility and practicality—two of the most important factors when car shopping. The rich have made this a rule for themselves.

Research conducted by Experian Automotive showed that 61 percent of people who earned more than $250,000 per year do not buy luxury brand cars (think Mercedes, Lexus, BMW). It turns out that the rich buy Fords, Toyotas, and Hondas.10 They aim for dependability, longevity, and affordability. You should too.

4. Calculate the Total Cost of Ownership (TCO)

The sticker price is simply the beginning of the cost calculation. Unfortunately, most people (not you) only consider the purchase price when determining affordability.

The problem with this approach is that there are tons of hidden, related, and invisible costs that purchasers fail to take into account. If you don't consider these costs when calculating affordability, they can weigh you down later.

Here is a list of variables to consider when calculating the TCO:

- Initial purchase price

- Tax and tag fees

- Car insurance

- Gas or electricity

- Repair and maintenance fees

- Warranties

- Resale value

- Length of ownership

Calculating the TCO will give you the most accurate comparison when deciding between cars. Once you have factored in all of the variables, don't let emotions get the better of you. Choose wisely.

5. Pay With Cash

You might have picked up on a theme throughout the money makeover: You should eliminate debt. This applies to all forms of debt, including consumer debt. If you have found the car that you want to buy, then save up the cash to purchase it.

This is an old-school approach to a new-school problem.

Millennials are highly leveraged. To shift from the affordability mindset to the ownership mindset, you must view things as how much they are going to cost you in cold hard cash. By making your purchases this way, you are ratcheting up the full pain of the transaction. Otherwise, by financing your car purchase, the pain is very small up front, but evenly deferred to each car payment. Why opt for death by a thousand cuts?

Paying for your car in cash will help you in three ways: It reduces your ability to purchase beyond your means; it keeps you out of debt; and it allows you to negotiate the best deal possible.

6. Negotiate

When you have found the car you want and have saved up the necessary cash, it is time to start negotiating. Let the dance begin.

Some of the best deals are won through the art of negotiation. This dance between buyer and seller involves both parties trying to discern what the other party truly wants. Here are some questions to ask yourself during this process:

- Why is the owner selling the car?

- Are you the first person to see the car?

- How long has the car been on the market?

- Are you prepared to walk away from the deal?

Because you have cash in hand, you hold the ace card. Your cash ceiling allows you to work with the seller and provides you a stopping criterion.

Above all, when you are looking to buy your first car be diligent in your research and check your emotions. Determine the car you want, pay with cash, and negotiate the best deal possible. You will learn countless lessons along the way.

Large-Ticket Purchase 2: Love and Money

Millennials want more out of life.

This generational craving has led to a focus on the self and the decision to delay life's major milestones, such as engagement, marriage, and family. Throughout the past three decades, the average age of marriage has skyrocketed to twenty-seven years old for women and twenty-nine years old for men.11 But looking at the numbers tells only half the story.

The postponement of life's milestones also happens to coincide with Millennials' lack of earning power and financial health. Now more than ever it is important for Millennials to be cautious when mixing love and money.

This means your relationship health is dependent upon having difficult conversations with your partner about love, money, debt, your future, and family planning. You need to have what I call the “define the financial relationship” (DTFR) talk. This conversation might feel a little awkward, but discussing your financial reality early on will help you work out kinks in your relationship and determine whether the relationship is a good match.

How you have this conversation is just as important as having the conversation. I suggest getting a bottle of wine, dedicating some time on the calendar, and sitting down to have this intimate financial discussion. Both of you will be nervous. Have faith that it will go well.

Erin Lowry, author of Broke Millennial, says getting financially naked is a fundamental relationship step to have with your partner. Getting financially naked involves defining how much debt you have, going over your credit reports and scores, and how you are currently handling your debt. Lowry adds, “This doesn't mean you have to pull up all your bank statements, credit card bills, student loan payments, and investments during the first talk, but it's imperative that you both disclose approximate numbers, positive or negative, when the time is right.”12

Mixing love and money can be potent to your pocketbook. It is crucial to make your expectations clear, be honest, and create an open rapport with your partner. After all, this is only the beginning.

Five Questions to Ask Your Significant Other

Divorce rates are high, and one of the leading contributors to divorce is a money problem.13 However, money problems can be solved early. Just like conversations about careers, children, or where you want to live, being open about money will help you determine if your partner is the right fit and whether you both want the same things out of life.

Having the DTFR conversation early in your relationship will only strengthen it. If you are thinking about getting engaged, married, or moving in together, consider asking your significant other these five questions:

1. How Much Do You Have in Savings?

Savings is paramount to financial health. According to a 2015 Google Consumer Survey, 62 percent of Americans have less than $1,000 in their savings account.14 Are you one of these people? Is your partner one? Do either of you have a savings plan?

The chances are that one of you will have more saved than the other. “It's almost impossible to be hooked up to somebody who has the same balance of spender and saver as you, or expansiveness versus conservativeness or financial circumstances,” says psychologist Gregory A. Kuhlman.15

It is important to find out which one of you is the spender and which one is the saver. So which one are you? Are you both financial mavens with thousands stored away? Or are you both broke? Either way, knowing your savings cushion gives true insight into your current financial outlook and can set the tone for the rest of the conversation. Beginning your financial conversation with savings can provide tremendous insights into your partner's financial health.

2. Do You Have a Plan for Getting Out of Debt?

Statistically speaking, both of you are in debt. But the kind of debt-student loans, credit card, or consumer debt-matters. Each of these debts carries with it a different story. Knowing the good, the bad, and the ugly will give you a glimpse into the future.

As you learned earlier, the average college graduate will have thousands of dollars in student loans. If you both fall into this category, then knowing that your partner is also dealing with this stress can be both a liberating and bonding experience.

Maybe you both had to pay for college or graduate school. Perhaps one of you got lucky and your parents paid for your education. Whatever the case, discussing your financial reality can provide needed insights into financial behaviors.

A typical red flag will be your partner's credit card debt. This can be a sign of poor financial planning, shopping gone wild, trying to keep up with the Joneses, or a more systemic spending issue. Let's face it: We all have our weaknesses, such as a spa day, a new suit, eating out, or happy hours. Sometimes it is just hard to say no. Discussing credit cards provides a peek into each other's outlook on consumerism.

3. Have You Started Saving for Retirement?

If you are serious about your partner, then you probably want to be with him or her for a long time. And if you plan on getting engaged or married, then your commitment to each other is forever. So, why not start planning now?

Forming an idea of what you want your life to look like together thirty years from now will help fortify your relationship, while at the same time establish clear expectations for the future. Saving for retirement is one of those things, which if done early enough, can be a nonissue later in life. If you find that you are both slightly behind on saving for retirement, don't worry. We will discuss more of this in Chapter 5.

4. What Is Your Ideal Income?

In the movie Wall Street: Money Never Sleeps, the main character, Jacob Moore, asks the banking titan Bretton James, “What is your number?” Cool, calm, and with a wry smile, James answers, “More.”16

How much money do you want to make? How much does your partner want to make? Does that comingle with your discussion on career and family?

If your fiancée wants to be a partner at a law firm because she worked her butt off in law school, are you okay with that lifestyle? Will one of you work and the other care for children? Does one of you value making partner while the other is content not chasing after the corner office?

If you have an ideal income to attain, chasing after your goal can give you the necessary motivation to fuel your path to success. The question forces you both, as a couple, to start thinking about where you are in life and where you want to go.

5. Can You Be Poor With Me?

Fortunes are gained and lost every day. Relying on money to fuel a relationship is an uphill battle. Money is simply a means of providing texture to your life story. Your story will contain twists and turns, and being prepared for these changes will be just as important as navigating them together. Making sure you are both comfortable with little money is a testament to the strength of your relationship. Even if only for a short time, it is worth conducting an experiment and living on the “cheapest fare.” The results will be eye-opening.

“Set aside a certain number of days, during

which you shall be content with the scantiest and

cheapest fare, with coarse and rough dress, saying to

yourself all the white: Is this the condition that I feared?”

—Seneca17

Open and honest conversations about personal finances can help resolve significant issues early that would otherwise cause problems later down the road. Remove the financial facade and get financially naked. Have the DTFR talk now and save yourself time, energy, and money.

On Buying the Ring

Okay, so you had the DTFR talk. If your relationship survives that conversation, you can now enter into a world of continued open and honest financial rapport. Knowing how much each of you has saved, if you are in debt, your retirement goals, your ideal incomes, and your willingness to get through the tough times is a priceless relationship asset, albeit intangible.

If you are still head over heels, then congratulations. But it's time to get real and not let the love goggles cloud your financial intelligence. The next step is finding and saving for a ring. Are you ready? No, are you really ready?

Buying an engagement ring is usually where the financial train derails. Common sense goes out the door, emotions are at an all-time high, and egos are at stake.

Conventional wisdom tells us that if we love our significant other, then the ring needs to be big and expensive, symbolic of our love. This has led to the cultural maxim that you should spend two to three months of salary on an engagement ring.

I call bullshit and here is why.

Economic researchers Andrew Francis and Hugo Mialon of Emory University set out to find the correlation between how much people spent on weddings and divorce rates.18 What they found surprised a lot of people and challenged conventional wisdom. As it turns out, a diamond is not forever.

In a survey of more than 3,000 “ever-married persons in the United States,” Francis and Mialon discovered that divorce rates and the size of the engagement ring were directly correlated. Their findings revealed an inverse relationship between how much people spent on engagement rings and whether that couple stood the test of time. You read that correctly. The more you spend on the engagement ring, the more likely you are to have your marriage end in divorce.

Their findings run counter to cultural standards, and that is by design. If you feel the pressure to buy expensive engagement rings, you can thank Gernold Lauck of the N.W. Ayer advertising agency. In 1938, De Beers, the world-renowned diamond company, turned to Lauck for marketing advice. Lauck commissioned a study to help De Beers market to young professional men—their ideal target customers. He pitched that it was critical to link the diamond to love. The core message needed to be that the larger and finer the diamond, the greater the expression of love.19 De Beers began preaching this as gospel, and the accretive effect has altered the diamond industry.

In an attempt to raise revenues even more, a well-designed marketing campaign by De Beers in the 1980s sought to increase the standard on how much men spent on engagement rings. De Beers created a slogan that was rather catchy: “Isn't two months' salary a small price to pay for something that lasts forever?”20

As time went on, this campaign sunk deeper and deeper into the consumer psyche, and during the economic booms of the 1980s and 1990s, the corporate slogan took a firm hold on consumer behavior.

However, during the economic collapse of 2008, millions of families started to halt their purchases on large-ticket items. For struggling Millennials, buying large engagement rings was simply a nonstarter. Would-be purchasers also realized that a diamond is a terrible investment. Diamonds can depreciate by as much as 50 percent as soon as you walk out of the store.21 From an investment perspective, it doesn't get much worse than that.

When you are in the market for an engagement ring, keep this thought in mind: The size of the diamond does not correlate to your love. Hopefully, after having the DTFR talk, your partner will be on the same page as you.

A word of caution: If you have skipped ahead in this book and still have debt of any kind, you should not, under any circumstances, think that spending thousands of dollars on an engagement ring is justifiable. If you have debt, eliminate it completely and then save up enough cash to purchase the engagement ring. As a newly engaged couple, there will be plenty of expenses coming your way. Be strategic and thoughtful about this process. You will thank yourself later for your discipline today.

How to 10X Your Wedding

A wedding is a big event. Once you know your wedding budget, you will want to optimize every allocated dollar to having the wedding you deserve. The wedding industry is about to welcome you with open arms.

Throughout the last several decades, the wedding industry has experienced unprecedented growth, as there has been a major push to “commodify love and romance.”22 According to TheKnot.com, in 2015 the average wedding cost $32,641.23 I hope you have been saving.

Planning for a wedding means that you are going to have to be a master at juggling seating arrangements, ordering food, coordinating with the band, and organizing flower deliveries, just to name a few. The options about what you want to have in your wedding can seem endless, so it is important to focus on exactly what you want and not get distracted by all of the noise. Don't get caught in the vortex of the paradox of choice.

You can 10X your wedding experience by placing your “must haves” at the top of your priority list. Concentrate on making sure those are done well. Then, as The Beatles say, “Let it be.” Here are three ways to maximize the impact of your wedding budget:

1. Share Your Budget

The wedding industry is ripe with revenue. That means that there are wedding experts to handle all different tiers of weddings, no matter the budget. There are wedding planners who specialize in the $100,000 wedding. And the $50,000 wedding. And the $10,000 wedding. And the $3,000 wedding too.

The first step is for you to determine your budget. Once you know how much you can spend, it is time to start looking for vendors that align with that number. Weddings happen every day. Wedding planners, caters, or virtually anyone accepting a check will see your “special day” as business as usual. So treat it as such.

When you are negotiating with vendors, share your budget with them. Honesty is the best policy. You want to get an excellent bang for your buck, and vendors want to give you the best of what they can offer. Plus, they will be relieved by your transparency.

See how far they are willing to stretch your dollar. If you like them, great. If not, move on to the next vendor. Light a fire in your negotiations by getting counterbids. There is nothing businesses hate more than losing revenue, and losing that revenue to the competition is even worse. See how badly they want your business.

2. Look for Discounts and the Rising Stars

There is an old saying, “If you don't ask, you will never know.” Once you have selected your preferred vendor, ask if they provide discounts.

Put them in the hot seat. Do they offer volume discounts? What about a Sunday wedding? Another tactic is to look for the rising star in your city. The wedding industry is awash with talent. This means newcomers are always trying to make a name for themselves. These rising starts will usually give you better deals and work longer and harder than their more seasoned competition. Find the people who are willing to put in the extra hours to ensure that your special day is everything you want. These are the people you want on your team.

3. Leverage Your Wedding Registry

A wedding is a celebration of two people becoming one. Commercially, this is displayed on your wedding registry. Luckily, technology has made this easier for the couple and the guests with the advent of the online wedding registry.

Use this to your advantage by being thoughtful and strategic with your listing. Here are a couple of points to keep in mind while you are working on your registry.

- Be selective. Aiming for quality over quantity is a great way to make sure your registry stands the test of time. Resist the urge to be extravagant. Be fair to your guests when you are selecting items to put on your registry.

- View it as a money saver. The wedding registry process is a chance to eliminate your basic needs. Decorating a living room, bedroom, or kitchen requires more effort than meets the eye. Take this opportunity to get the basics out of the way.

- Register at a few places only. The paradox of choice is real. By giving your guests only a few places to shop, being selective, and choosing quality items, the likelihood that you will receive everything you want increases dramatically.

- Set up your registry early. With the average couple enjoying a fifteen-month engagement, there is plenty of time to plan.24 Take an inventory of what you and your future spouse separately own. Be prepared to discuss exactly what additional items you will need to purchase once you consolidate assets. This will alleviate paying for duplicate items, and you can start putting money toward a honeymoon, savings, or investments.

Although your wedding is a personal statement, it is also a moment for reflection, family, and fun. Don't let the commodifying effect of your special day steal your happiness or attention away from what matters. Above all else, enjoying your wedding day with your new spouse is the best way to maximize your wedding.

Large-Ticket Purchase 3: Buying a House

Peter Thiel is one of Silicon Valley's household names. As a cofounder of PayPal, Thiel made a name for himself when he sold his once fledgling business for $11 billion in 2002. The mystique around Thiel and his ragtag group of cofounders, dubbed the “PayPal Mafia,” has only grown with time.

Now an established player in Silicon Valley, Thiel is known for his contrarian views on business. In his bestselling book Zero to One, Thiel makes the argument that competition is bad for business. Instead, as a founder, you want to look for monopolies.25 This is not an everyday American viewpoint.

One of Thiel's most well-known attributes is the unique way he conducts interviews. As the founder of multiple companies, Thiel understands the importance people play in building a successful business and is no stranger to interviewing executives. In fact, his interview questions have only increased his lore. One of his most famous questions is, “Can you tell me something that is true that no one agrees with?”

If Thiel asked me that question, I would have an answer: I believe buying a house is one of the worst financial decisions young professionals can make.

Buying a house is not inherently a bad investment, but buying a house too early in life is often one of the biggest financial mistakes someone can make, and it has years of lasting consequences. The fascination of purchasing the perfect home in a great neighborhood transcends the rational reality of financial wisdom. What follows is a focus on the affordability of mortgage payments in lieu of creating a proper financial base to secure your financial future.

Homeownership is deeply embedded in American culture, but a systemic issue with housing is that people get sucked into the idea that they need to purchase too much house. This leaves them financially riddled with high mortgage payments. In an economy where the average Millennial changes jobs every 3.7 years26 and the typical American moves 11.4 times in their life,27 the utility of buying a house is not what it used to be.

The money makeover has one major rule on housing: Do not buy a house until you have accumulated at least one to two times your annual household income in cash or investments.

Pundits will hate this. Banks will brush this aside. Realtors will laugh in your face. Ignore them all because the traditional view of housing is outdated.

The reality is that this rule gives you the financial momentum to combat the temptation of purchasing a house that will break your budget, cause high anxiety, buyer's remorse, ballooning mortgage payments, and low cash reserves. This rule offers a hedge against your innate inability to process large numbers and tendency to bite off more than you can chew. This rule flips the traditional order of the success sequence and emphasizes securing your financial future first.

With soaring real estate prices, the affordability of housing has plummeted throughout the last several decades. Yet the pressure to purchase still remains high. Millennials are left caught in this paradox. The dream of homeownership needs to be reevaluated because it can quickly morph into a financial nightmare.

Here are the four most common mistakes that young homebuyers make.

1. Buying Too Soon

It pays to be prepared. Buying a house before you are financially secure is the biggest mistake you can make. Many homebuyers are lured into the pressure of homeownership by external factors, such as nagging family and friends or keeping pace with marketed societal norms. Before buying a home, I advise having more important aspects of your financial life fully secured.

2. Having Other Debts

Before buying a home, you should have completed Step 2 of the money makeover. That means you should have no student loans, credit card debt, or consumer debt. Get rid of all your debt before you even think about buying a house.

Practically speaking, all of your expenses will go up once you purchase a house. You will have to furnish the house, pay real estate taxes, buy home insurance, pay broker fees, incur repair and maintenance costs and countless other unforeseen expenses. All of these hidden costs of homeownership are not included in the sticker price, only furthering the total cost of purchase.

3. Not Saving One to Two Times Their Household Income

This can be in investments, retirement savings, or cold hard cash, but first-time homeowners often forego securing a healthy financial base before buying a home. This financial foundation will provide you the support you need to establish a healthy ecosystem. The momentum of this savings base will carry you to a rich future. As you saw earlier, humans' ability to conceptualize large numbers is pretty poor. Don't let the numbers work against you on such a monumental purchase.

If you are researching buying a home, then you should already have at least one to two times your annual household income saved before taking the plunge into homeowner-ship. This will dampen your desire to purchase beyond your means because this savings base will act as a relative and tangible point of comparison.

4. Not Putting 20 Percent Down

One of the most prohibitive aspects of purchasing a home is the down payment. This is meant to be a gatekeeper. The down payment was designed as a barrier to entry because it prevents purchasers from buying houses they cannot afford.

Millennials are no strangers to the financial difficulty of homeownership, and major tech companies in the housing space are paying attention. “Young workers face a lot of hurdles on the way to homeownership, including saving for a down payment in the first place and deciding where and when to settle down,” said Zillow's chief economist, Stena Gudell.28

Saving for a down payment can take years, but it doesn't have to be painful. Set up a savings account and automate 5 to 10 percent of your income to automatically pile up in this account (see Chapter 6). Then put these savings on cruise control until you are ready to purchase.

When done correctly, homeownership can be a financial blessing. But it does not make sense for everyone. Evaluate where you are on your money makeover before taking the plunge.

Interest Distorts Your View, Again

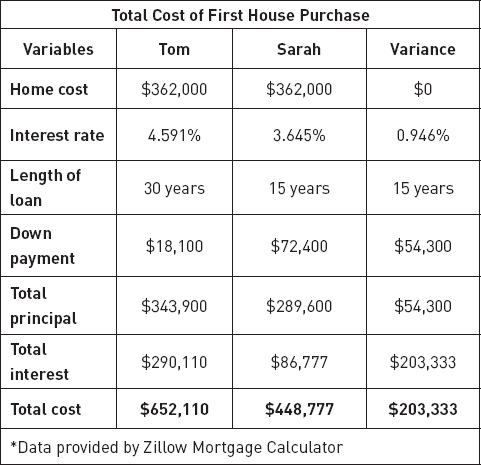

In this section, we will analyze the nature of interest and its inherent ability to increase the total cost of purchase of a mortgage. We will look at two very different home purchasers, Tom and Susan, and the financial repercussions of their choices when purchasing a home. For the sake of this demonstration, we are going to assume the perspective homeowners will pay the average purchase price of a first home in 2016, or $362,000.29

Scenario 1

Tom is an information technology manager. He makes good money working for a startup, where he has been employed for the last two years. The good news is that Tom enjoys his job. However, Tom took out massive student loans to afford his high-tech education. Recently, Tom and his wife started exploring the idea of owning a home. As the parents of a two-year-old, they found out recently that there would soon be another member of the family, turning their manageable apartment for three into close quarters for a family of four.

Tom starts to analyze the pros and cons of buying a house, even though he knows he should pay off his debt first. Going against the money makeover, Tom decides to defer his student loan payments and save for a down payment of 5 percent. He purchases the house with a thirty-year fixed loan with an interest rate of only 4.591 percent. Not bad—he thinks.

Tom's $362,000 house will cost him $652,110 over the life of his loan. This includes the $343,900 of principal payments and the whopping $290,110 of interest payments.

Scenario 2

Sarah is a lawyer. And a damn good one. During her first couple years out of law school, she made a name for herself in her private practice. However, don't let her high income deceive you. Sarah is up to her neck in debt. But Sarah and her husband are adamant about paying it off quickly, even with small children.

Crammed in a two-bedroom apartment, Sarah feels like her income doesn't translate to her lifestyle. Sarah wants to buy a house to give the family more space. Plus, all of Sarah's friends have upgraded to purchasing homes. She feels pressure from her family and friends to make the plunge into homeownership. But Sarah has read Millennial Money Makeover, and she knows that she still has debt to eliminate.

After hunkering down and getting rid of all of their debt, Sarah and her husband then save one times their household income, which took significant delayed gratification. Next, Sarah and her husband concentrate on saving for a down payment. Within eighteen months, they have enough to put down 20 percent on a $362,000 house.

Sarah's finances are in order. Because she is financially secure with no debt and a 20 percent down payment, Sarah decides to opt for a fifteen-year fixed loan with an interest rate of only 3.645 percent. Not bad—she knows.

Sarah's $362,000 house will cost her $448,777 over the life of her loan. This includes the $289,600 of principal payments and $86,777 of interest payments.

The total cost difference over the life of the loans is a whopping $203,333.30

Or roughly four times the average American household income.31

Or more than double the average 401(k) balance in 2016.32

The gaping difference between the cost of the same home, based upon the length of mortgage and size of the down payment, is why we are concentrating on housing now and are not leaving it as an aside in a later chapter. Decisions on housing can financially make or break you.

Five Reasons Millennials Aren't Buying Homeownership

Homeownership is a hallmark of the American dream. With average new home sales now topping $380,000, the dream of homeownership has become daunting for Millennials.33 The idea of becoming a first-time homeowner seems to be more of an illusion than a pillar of the American experience.

Millennials are shifting the tide on the timing of traditional life-stage purchases, and many don't view buying a house as a necessary reality, as once advertised by previous generations.33 The weight of costly student loans, consumer debt, and recent urbanization has transformed the Millennial outlook away from traditional homeownership. Housing trends among Millennials are changing the norm. Here are five reasons Millennials aren't subscribing to the traditional mantra of first-time homeownership.

1. New Housing Isn't for Millennials

Despite the headlines about the surging housing market, people in their twenties and thirties don't feel they can participate in the boom. There is a disconnect between what Millennials read in the news and what they are experiencing in reality. Surveys conducted by the National Home Owners Association show that less than 20 percent of the new home construction over the past several years was dedicated to “entry-level” properties.34 This is down from the pre-recession levels of more than 30 percent. In short, houses are literally not being built for the Millennial market.

Instead, developers have shifted their focus to building larger houses that cater directly to the more established and affluent Baby Boomers. Until there is a shift back to building affordable first-time homes, this trend is likely to continue.35

2. Down Payments Are the Worst

If the average sales price for new homes stands around $380,000, with some quick math, you can see that the average Millennial needs to amass $76,000 for the recommended 20 percent down payment for the average house.36 However, Millennials clearly face major financial burdens that restrict their ability to accumulate the necessary down payment to make purchasing a house a viable option.

To complicate matters, most Millennials tend to live in large urban areas where housing prices are higher than the national average. Thus, the practicality of buying a house is quickly dismissed.

Some Millennials are taking a nontraditional approach to saving for a down payment and living at home longer. According to Forbes, for the first time in more than 130 years, more Millennials are living with their parents than with a significant other.37 For the few Millennials who are buying houses, their time at home serves as a strategic move to allow them to save enough cash to afford their down payment.

3. Flexibility Is More Valuable

With major cultural shifts occurring, many Millennials don't feel the need to be strapped down by purchasing a first-time home. Not only are Millennials pushing “adulting” to later in life, they honestly don't quite see the need for the mortgage and the white picket fence. Thanks to personal finance advocates, a home mortgage is now viewed as a liability and not the asset it was once considered.

In today's fluid economy, Millennials value flexibility and mobility over security and stability. Therefore, the pressure to find a house and settle down to long-term employment isn't what it used to be. Millennials are privately thankful for that because, honestly, they can't afford it.

4. Rental Options Are Abundant

Although Millennials are not warming up to the new housing market, they are doing quite well in subscribing to the renter's market. Even as rents rise, urban-based Millennials are left with the option of finding an “affordable” place to rent. In fact, the cost of renting is rising faster than inflation. This leaves Millennials paying a larger percentage of their take-home income on housing.38

Although rents remain high, they are not high enough to incentivize saving for a down payment and often impede the progress toward saving for that goal. Additionally, after watching families struggle following the housing collapse of 2008, many believe homeownership is not worth the risk. And if renting an apartment doesn't work, there is always Mom and Dad's house (see Reason 2).

5. It's the Economy, Stupid

As with most generations, Millennial' outlook and consumption patterns are often driven by the economic conditions of their time. Many Millennials graduated from college or were exposed to the job market during the economic collapse of2008 and felt its lasting ramifications. Over the last decade, salaries have been relatively stagnant and economic growth anemic. As a result of this slow growth, Millennial have focused on staying solvent and financially afloat. Until the economy fully turns around, Millennial will be patient, waiting their turn.

The takeaway is that purchasing a home, if done incorrectly, can be a giant mistake. Even in the wake of the housing crisis of the last decade, people are still not abiding by the rational mantra that homeownership has its time and place in life's milestones. Don't let other people's ideas of what your future should look like define yours. Learning to be patient with large purchases, especially housing, can be the quickest path to the rich life.

Thoughts on Financial Leverage

Semantics matter.

When it comes to buying large-ticket items, people often confuse affordability with ownership. The ability to make monthly payments on a new car, boat, or house does not justify the purchase. Affordability is not a synonym for ownership. Although you might be able to make the payments, this does not mean that you should. The ability to meet the minimum monthly payments blinds people to the true questions they should be asking:

- Does this purchase make financial sense?

- Does it align with my goals?

- Will this purchase wreak havoc on my budget?

- Is this a rich decision?

The only major purchase you should finance is your house. All other purchases should be made with cash.

In fitness, the Body Mass Index gives a quick glimpse into physical health. The financial equivalent is called the financial leverage ratio.

| Typical Household Items | |

|---|---|

| Assets | Liabilities |

| Cash | Credit card debt |

| Investments | Student loans |

| Furniture | Car note |

| Jewelry/Electronics | Mortgage |

Financial Leverage = Household Liabilities/Household Assets

This ratio provides a gauge of financial health. The higher your financial leverage ratio, the more debts your household carries relative to its assets. A high financial leverage ratio can foreshadow financial disaster. One missed payment, one emergency, or one layoff could derail everything.

Conversely, a low financial leverage ratio indicates a stronger financial makeup. Ideally, you want this ratio to hover around zero. And once you complete all of the steps in Chapter 2, and are completely debt free, your goal will be to keep this as low as possible. Financing large purchases can skyrocket this ratio, especially for young working professionals. If you graduated from college with the typical debt load, you probably haven't had the time to increase your household assets. Since you have debt and relatively few assets, you are highly leveraged. Due to interest on your loans, your liabilities will continue to grow. This is why in Chapter 2 you worked to eliminate your debts as quickly as possible.

Once you have eliminated your debt, your financial ratio will start looking much healthier, and you can start building up your assets (cash, bonds, stocks, real estate, and so on). Keep tabs on this ratio and don't overexpose yourself to debt. If you follow the money makeover principles to success you will protect yourself from being overexposed.

![]()

Action Items

Applying the lessons learned in this chapter will accelerate your money makeover. They will work like magic. You might not see all of the benefits immediately, but the results will pay for themselves in perpetuity. Your bank account with be healthier, your life will be richer, and you will find happiness in your decisions.

When you are making large milestone purchases, remember the following ideas from this chapter:

- Buying a new car is for suckers; do your research.

- Mixing love and money can be dangerous; proceed with caution.

- Buying a house should only be done when you are financial prepared.

- Remember that education does not end in the classroom.

- Optimize large purchases and expedite your makeover.

Optimizing large purchases will propel you into the rich life. Being smart with your money is not always the easiest path. But this discipline will open your eyes to the reality that life is about more than material possessions. Remaining financially secure and making measured financial choices is a cornerstone of your money makeover.

This decision will allow you the mental space to begin preparing for accumulating investments and saving for the future. The rich life is about forward thinking. In the next chapter, you will learn how to turn your financial diligence into a wealth-generating machine.

Let's start the engine.