Organizations Dealing with Money Laundering and Terrorist Financing

Criminals are interested in funding their activities and make profit out of their illegal activities. I Illegal activities might include fraud, drug and arm trafficking, money laundering, and terrorist financing. To prevent illegal activities, money-laundering and terrorist financing, different organizations, and conventions accept and implement international laws and regulations.

Financial Action Task Force (FATF)1

The most recognized organization FATF was established to prevent money-laundering activities.

The FATF was established by the G-7 (Group of 7 countries) Summit that was held in Paris 1989 (Borekci and Erol, 2011).

The FA Task Force is a policy making organization that develops procedures at national and international levels. According to Borekci and Erol, in 1990, the FATF introduced 40 recommendations which provided a comprehensive plan of action needed to fight against money laundering. Those recommendations became international set of standards. The FATF has updated its policies against money laundering and terrorist financing through the years. ‘On 22 October 2004, the FATF has arranged the 40 + 9 recommendations which include additional 9 policies about terrorist financing’ (Koh, 2006). According to the FATF’s website, G-7 was formed in 1976, when Canada joined the group of six countries: France, Germany, Italy, Japan, United Kingdom, and United States.

The 40 Recommendations could be categorized in 4 groups,

• Legal Systems include the scope of the criminal offence of money laundering and provisional measures.

• Measures used by Financial and Non-financial Institutions include

• financing,

• customer care,

• record-keeping,

• Reporting suspicious transactions,

• Measures to be taken with respect to countries that do not or inadequately fulfill the FATF Recommendations, and

• Regulations and supervisions.

• Institutional and Other Measures in Systems include

• Competent authorities, their powers, and resources

• Transparency of legal people and arrangements

• International Cooperation includes mutual legal assistance and transportation and other forms of co-operation.

The FATF organization has 37 members (35 member jusrisdictions and 2 regional organisations) representing most major financial centres in all parts of the globe.

The organization is in close collaboration and cooperation with other international bodies involved in the AML/CTF area, in particular with the International Monetary Fund (IMF) and the World Bank (Borekci, 2011). The IMF and the World Bank are the vital organizations for the assessment and implementation of the FATF standards. The FATF also works with the Basel Committee on banking supervision and Organization for Economic Cooperation and Development (OECD).

Turkey’s Mutual Evaluation Process of the Financial Action Task Force

The 40 Recommendations for AML/CTF (Combat terrorism financing) are applicable to all countries. The mutual evaluation process of the FATF requirements is an element for deciding if countries are in fulfillment with the recommendations of FATF or not.

Based on FATF, four possible ways of fulfillment for each recommendation include:

• Largely compliant (LC): The majority of the essential criteria are fulfilled with some minor shortcomings.

• Partially compliant (PC): Some actions are taken by the country and some of the essential criteria are fulfilled.

• Non-compliant (NC): The majority of the essential criteria are unfulfilled with some major shortcomings.

• Not Applicable (N/A): Because of the structural, legal, or institutional attributions of a country, a requirement or a part of a requirement does not accomplished.

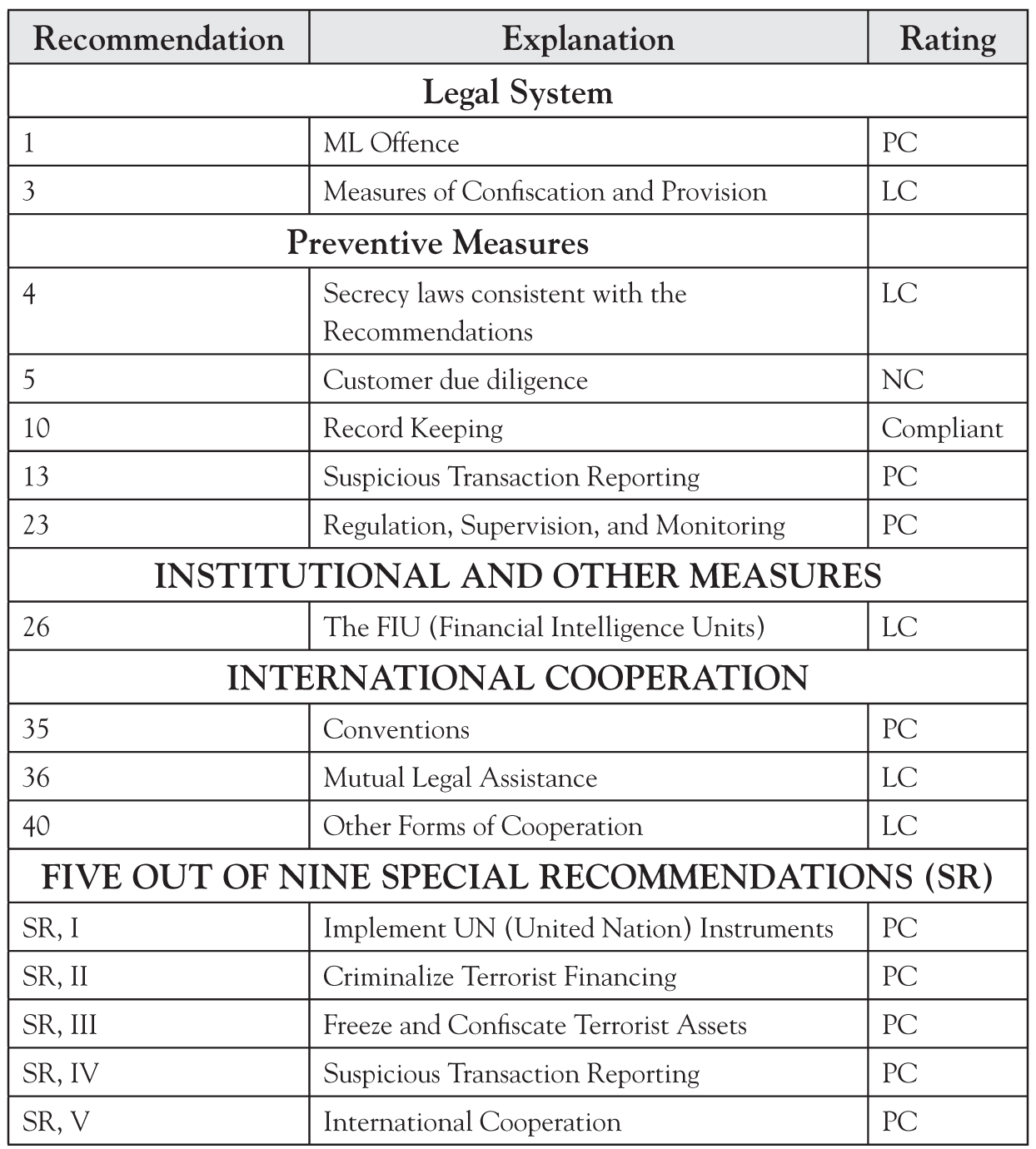

The FATF Recommendations have core and key measures. Since 1991, Turkey has been a member of FATF. The final Mutual Evaluation Report (MER) has been estimated in 2007. According to the report including the core and key recommendations of FATF, Turkey’s mutual evaluation is shown below (See the following Tables 6.1 and 6.2):

Table 6.1 FATF core and key recommendations

Source: ICRG, Report by the Europe/Eurasia Regional Review Group Co-Chairs, FATF/ICRG (2009)19, 30 September 2009, p: 96.

The explanation of the core and key recommendations is as follows:

Table 6.2 Explanations of Recommendations

Source: ICRG, Report by the Europe/Eurasia Regional Review Group Co-Chairs, FATF/ICRG (2009)19, 30 September 2009

Shortages in those recommendations show the need of the need of serious measures in a country’s AML/CTF system to reflect a stronger international financial system. According to the table above, for Turkey, the evaluation includes 9 PC and 1 NC out of 16 core and key recommendations.

In January 2010, MASAK, the Turkish Financial Crimes Investigation Board stated the need for the implementation of the AML/CTF system according to its 40 FATF recommendations and prepared an action plan. The Turkish government submitted a plan including standards and criteria of

• Criminalizing the financing of terrorism and associated money laundering (SR II), and

• Freezing and confiscating terrorist assets (SR III).

According to the ICRG (International Country Risk Guide) report, this action plan has been adopted and lead by the delegate prime minister and several authorities, including the Ministries of Justice, Interior, Foreign Affairs as well as MASAK.

European Union (EU) Money-Laundering Combat Directives

The EU has introduced a total of three directives to combat money laundering:

• A Council Directive in 1991,

• A Directive in 2001 of the European Parliament and Council, and

• A Directive in 2005 of the European Parliament and Council.

The directives deal with:

• The definition of AML,

• Specification of Categories of Financial Intermediaries,

• Obligations of these intermediaries,

• Explanation of these obligations,

• Identification of the Responsibilities of Public Authorities, and

• Control purposes.

The directives are vital for establishing the control for environment against money laundering and terrorist financing. The directives include four major criteria:

• Customer Identification (Know Your Customer)

• Record Keeping

• Suspicious Transactions, and

• Reporting.

The third AML directive, adopted in 2005, is the most important one among the others with international approaches of preventing money-laundering activities, terrorist financing activities, and suspicious transaction reporting.

Turkey is a European Union candidate country. For that reason, the country will not be involved in this section. However, the organization has 28 countries as of July 20132, as follows:

• Austria,

• Belgium, Bulgaria,

• Cyprus, Czech Republic, Croatia

• Denmark,

• Estonia,

• Finland, France,

• Germany, Greece,

• Hungary,

• Ireland, Italy,

• Latvia, Lithuania, Luxemburg

• Malta,

• The Netherlands,

• Poland, Portugal,

• Romania,

• Slovakia, Slovenia, Spain, Sweden, and

• United Kingdom. [Brexit pending – 2016]3

Figure 6.1 describes the European Financial Institutions: distribution by Country Reported figures above differ according to the countries’ financial markets. The main reason for that variation emanates from the different counting rules and concepts within EU. The transaction processes are as follows:

Figure 6.1 European Financial Institutions

Source: Eurostat

• Financial Intelligence Units (FIUs) process transactions received in Suspicious Transaction Reports (STRs) as cases.

• The related cases are sent to the Law Enforcement Authorities.

• Some FIUs record and combine all related STRs as one case, when some FIUs count the STRs as the first case-opening.

For some EU members, the activities which might not be related to any monetary transaction, such as opening a bank account, could be interpreted as a Suspicious Activity Report (SAR). On the other hand, some EU members could send Unusual Transaction Reports (UTR) to the law enforcement authorities if those activities are found to be suspicious.

European Union’s (EU) Action Plan to Fight Against Terrorist Funding

The European Union has adopted its fourth directive on May 20th, 2015. Its main goal is to prevent the EU financial system from being used for money laundering and terrorist financing purposes. 4

The Plan has two main objectives:

1. PREVENT THE MOVEMENT OF FUNDS AND IDENTIFY TERRORIST FUNDING:

Key actions:

• Ensure virtual currency exchange platforms are covered by the AntiMoney Laundering Directive;

• Tackle terrorist financing through anonymous pre-paid instruments such as pre-paid cards;

• Improve access to information and cooperation between EU Financial Intelligence Units;

• Ensure a high level of safeguards for financial flows from high risk third countries;

• Give EU Financial Intelligence Units access to centralised bank and payment account registers and central data retrieval systems.

2. DISRUPT SOURCES OF REVENUE FOR TERRORIST ORGANISATIONS:

Key actions:

• Tackle terrorist financing sources such as the illicit trade in goods, cultural goods and wildlife.

• Work with third countries to ensure a global response to tackling terrorist financing sources

The EU and national governments decided to bring extra precautions against terrorism financing activities after the events in Paris, France (European Commission Factsheet, Feb 2016). These precautions combined formed EU Action Plan.

The EU’s Action Plan has 2 purposes:

1. To identify and prevent the transfer of Terrorist Funding by

• Guaranteeing that the AML directive is applied on cyber currency exchange platforms

• Investigating on anonymous pre-paid instruments

• Expanding the information access between EU Financial Intelligence Units

• Applying more precautions for high risk third countries’ financial transfers

• Expanding the authority of EU Financial Intelligence Units to access central bank’s data and payment account registers.

2. To dislocate Income Sources for Terrorist Financing Groups by

• Confronting the sources of the illegal activity (trade in wildlife, cultural goods)

• Collaborating with third countries to have a worldwide response to reveal the sources of terrorist funding.

In Feb 2016, European Commission published a factsheet about an action plan to fight terrorism funding. The action plan indicates things to do in 2016 and 2017 to combat financing terrorism. 5

EU Action Plan

The action plan is designed to gather EU countries working together to prevent funding criminal activities.

“The recent terrorist attacks on Europe’s people and values were coordinated across borders, showing that we must work together to resist these threats” (European Commission President Jean-Claude Juncker).

According to the action plan for 2016 and 2017, some steps are needed to be taken immediately as a criminal action preventative strategy.

• Accelerate the UN’s application with improved exchange of information and fast implementation on freezing procedures by the EU.

• Provide technical support to third countries for them to keep up with UN procedures such as asset freezing, authorizations and permissions.

In addition to the immediate actions, EU commission also divides 2016 into two parts. In the first half of 2016, the commission aims to apply and update existing laws to prevent terrorist financing and transferring the illegal funds.

First Half of 2016’s Actions

• Create a list to spot high-risk third countries that have shortages to fight terrorist financing and money laundering.

• Create a plan to stop wildlife trafficking.

• Include the issues below within the EU Anti-money Laundering Directive:

• Design improved measures for high-risk third countries.

• Avoid the risks of cyber currency exchange boards and pre-paid transactions.

• Offer electronic data recovery systems or payment account records and a central bank.

• Improve Financial Intelligence Unit’s access to information

• Improve the exchange of information between units (the Commission, the member states, and economic hands) on how to apply the preventive measures.

The Second half of 2016’s Actions

The second half of 2016 action plan is designed by EU commission to imply new initiatives to strengthen the existing legal outline. In addition to that, the commission wanted to help third world countries to prevent and fight terrorist financing.

• Help high-risk regions like North Africa, South East Asia and Middle East to display and prevent terrorist financing activities.

• Provide technical support to high-risk regions to fight cultural goods trafficking using terrorist linkages.

• Accelerate the application date for the Fourth AML Directive.

• Offer new EU legislation to tone the illegal money-laundering agreements.

• Offer new EU legislation to prevent illegal fund transfers and assets transportation across borders.

• Evaluate the necessity for a new EU legislation on freezing the assets of terrorists within the borders of EU.

• Contribute all EU Member States on recognition of freezing and confiscating terrorists’ assets.

• Introduce new measures to EU-US Terrorist Finance Tracking Programme.

In 2017, the goal is to identify terrorist financing activities and target the sources of criminal activities.

1. 2017 Actions

• Writing a money laundering and terrorism financing report including recommendations.

• Publishing the report to Member States to guide and warn them on illegal activities.

• Strengthening the power of authorities to fight the illegal trade of terrorists by offering a new legislation.

Cash Movement Controls

The Regulation accepted in 2005 and applied in 2007 controls the cash movements into and out of the European Union. According to that Regulation:

• Travelers need to make a declaration to customs authorities when entering or leaving the EU and carrying EUR 10,000 (or its equivalent in other currencies or easily convertible assets as checks drawn on third party) or more (Tavares, 2010).

Member countries must keep the records of the information collected from the declaration. Members also need to make those records available to the authorities to combat terrorist financing and money laundering.

United Nations (UN) Conventions Regarding Financial Institutions

The Vienna Convention:

The Vienna convention signed in 1988 under the protection of United Nations and became effective in 1990, is against Illicit Traffic in Narcotic Drugs and Psychotropic Substances. This agreement was signed by European Union and G-7 countries. Countries signed the agreement agreed to join to combat drug trafficking and laundering the earnings of the activity.

The success of the Convention depended on the mutual assistance and synchronization between the countries as there was variety in languages, and legal environments within the union. UN has developed two models for countries to implement the arrangements against money laundering. These models were:

a. The United Nations Model Agreement on Mutual Assistance in Criminal Matters, and

b. The United Nations Model Agreement on Extradition.

Both of the models were designed to distinguish the differences within the legal systems and the relations between them.

The Palermo Convention6:

The Convention was against Transnational Organized Crime, signed in 2001.

Merida Convention:

The Convention was against Corruption, signed in 2005

UN had defined the topics for fighting against money laundering. As a result of this directive the member states were expected to ensure that:

• money laundering is forbidden,

• customer identifications should be confirmed and records should be kept,

• suspicious transactions should be monitored and checked,

• institutions should co-operate with the authorities by reporting suspicious transactions and relevant information,

• suspects should not know that they are under investigation,

• anyone reporting a suspicious transaction should be protected from the breach of confidence actions,

• Institutions should implement and maintain sufficient systems of internal controls and employee training.

Basel Committee on Banking Regulations

The Basel Committee on Banking Supervision (BCBS) is a committee of banking supervisory authorities that was established by the central bank governors of the Group of 10 countries in 1975 (Bank of International Settlements).

The Committee’s member countries are,

• Argentina, Australia,

• Belgium, Brazil,

• Canada, China,

• European Union

• Hong Kong SAR

• France,

• Germany,

• Hong Kong SAR,

• India, Indonesia, Italy,

• Japan,

• Korea,

• Luxembourg,

• Mexico,

• Netherlands,

• Russia,

• Saudi Arabia, Singapore, South Africa, Spain, Sweden, Switzerland,

• Turkey,

• The United Kingdom and

• The United States.

In December 1988, the Basel Committee on Banking Supervision issued a “statement of principles” which international banks of member states are expected to fulfill. These principles were the basic rules for banking system which will make the authorities to track money laundering activities. The principles were covering the subjects as:

• identifying customers,

• avoiding processing of suspicious transactions, and

• Cooperating with law enforcement agencies.

While issuing these principles, the Committee stated the threat to public confidence in banks, and their stability that can occur if they unintentionally become associated with money laundering.

This document is related to the initial composition of the 1990 Forty Recommendations with its four major principles:

1. Know Your Customer (KYC),

2. Conduct business in compliance with high ethical standards and laws,

3. Cooperate fully with law enforcement authorities, and

4. Have in place policies and procedures to carry out the three principles above (Koh, 2006).

The International Monetary Fund (IMF)7

Money laundering and terrorism financing have effect on economy. Money laundering crime is considered as a profit-making crime involves the activities of:

• Drug and arm-trafficking,

• Corruption,

• Tax elusion, and

• Fraud.

These criminal activities generate a financial flow that affects the economy in a negative way. IMF has been active to prevent the negative effects of money laundering and terrorist financing on financial institutions and systems. According to Min Zhu Deputy Managing Director, IMF, ‘Effective anti-money laundering and combating the financing of terrorism regimes are essential to protect the integrity of markets and of the global financial framework as they help mitigate the factors that facilitate the financial abuse’...

The activities achieved by IMF about Money laundering:

• In 2000, the work in the area of AML is expanded by international community.

• After September 11, 2001 AML activities are more expanded and included combating terrorism financing.

• In 2009, the IMF initiated a trust fund to finance and support the activities in AML/CTF. Canada, France, Japan, Korea, Kuwait, Luxembourg, the Netherlands, Norway, Qatar, Saudi Arabia, Switzerland, and the United Kingdom committed to provide US$25. 3 million over 5 years to the financing of the Topical Trust Funds (TTF). The countries are expected to support the TTF to strengthen the global AML/CTF systems.

• In 2011, IMF reviewed the effectiveness of the Fund’s in AML/CTF program and presented assistance for the future work.

The World Bank8

The purpose of the World Bank is to support client countries to strengthen their reliability in financial sectors with Technical Assistance, Policy Developments, and Assessments. To increase the awareness for preventing money laundering, the World Bank conducts regular trainings like the organizations as FATF and IMF. ‘Lately, the World Bank delivers training for assessed countries for preparation to the assessments both on substance and processes.’ The assessments are meant to identify the flaws in AML activities on country bases. The purpose of the assessments is to improve the country’s framework in fighting against money laundering. Analyzed areas in assessments include:

• Legal and institutional,

• Supervisory and regulatory for the financial sector and other financial services providers, and

• International assistance.

The assessments need to follow certain regulations. ‘All the assessments are conducted with reference to the FATF’S 40 + 9 Recommendations.’

Turkey is a significant money laundering country because of its geographical location.

Reasons for criminals’ use of Turkey to launder money include:

1. Geographical Location (Middle-Eastern Region)

• Continuous conflict and war between Israel and Palestine,

• The ex-war between Iraq and Iran that took more than 7 years,

• The ongoing dispute and warfare between Turkey and illegal Kurdish terrorist organization PKK.

2. Turkey is on the main road for drug trafficking. Drug smugglers need a massive economy to serve, collect, and hide the funds within the financial market. Turkey plays an important role within the global economy with the potential and the infrastructure of the country, the available financial tools in its domestic market, and its role as a player in international markets.

3. The region is preferred for illegal arm trading especially for Islamic Terrorist organizations that trade guns. Several countries use Turkey for arms trafficking.

4. Turkey is in the middle of the OPEC (Organization of Petroleum Exporting Countries) and within this region unofficial oil trading is very common. However, the member countries are not fighting against the illegal oil trading because of economic and social reasons.

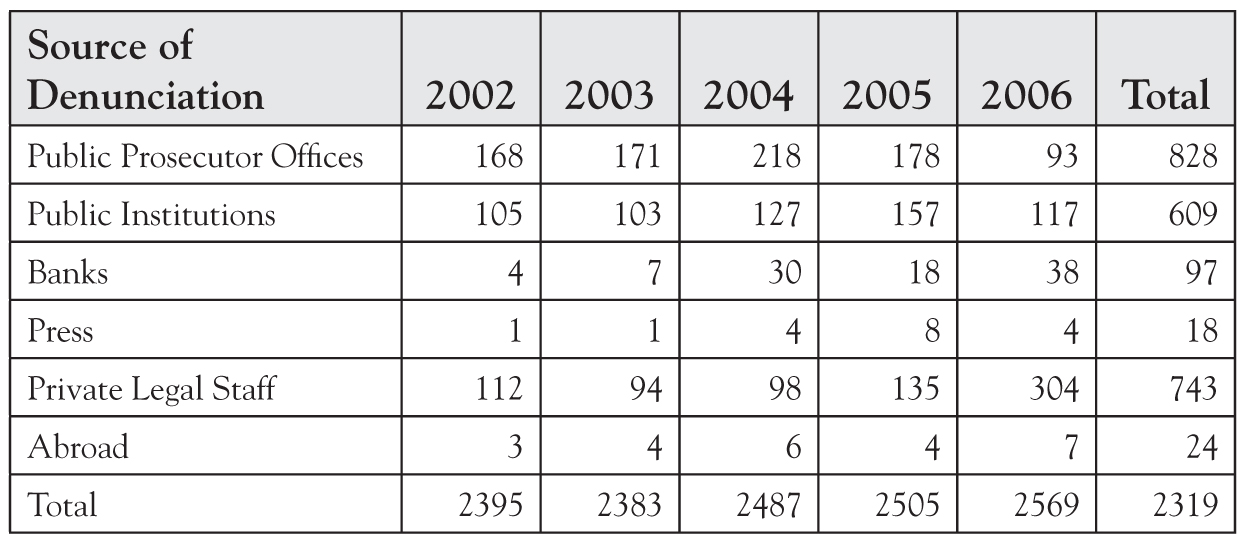

5. Turkey has a traditional habit of doing cash transactions. The habit creates an attractive environment for criminals to launder money via cash transactions. (See Tables 6.3 and 6.4)

According to MASAK’s statistics August 2011, the sources and volumes of denunciation in Turkey between 2002 and 2006 are:

According to the data shown below between 2002 and 2006, banks (financial institutions) are developed in detecting and reporting money laundering cases. Financial sector has some different branches within. The improvement of the banks in tracking and reporting suspicious transactions is greater than the other financial institutions.

Table 6.3 Sources and volumes of money-laundering denunciations in Turkey

Source: MASAK Statistics, August 2011

Table 6.4 Suspicious Transactions Statistics of Financial Sector (Jan 2002-Dec 2006)

Source: MASAK Statistics, August 2011

As we can see from the table, banks reporting suspicious transactions increased by 223% from 2005 to 2006 and.

Turkish government has introduced many measures to fight money -laundering activities targeting both financial and non-financial institutions. The measures cover:

• Incoming and outgoing fund transfers,

• Cross-border Currency Smuggling, and

• Purchasing high value objects such as gold, real estate or luxury cars.

Criminals can also launder money by:

• Weapon smuggling,

• Organ or Tissue smuggling,

• Smuggling of Historical Remaining,

• Fake Invoicing or related crimes,

• Crimes targeting to State’s Identity, and

• Distributing fake money.

To prevent money laundering, knowing customers’ identification becomes significant for financial institutions. Banks should require providing some acceptable documents for real and corporate clients’ identification, like:

• For Persons

• Turkish Citizens

• Official ID

• Driver’s License

• Passport

• Foreigners

• Passport

• Residential Permit

• For Corporations

• Registered in Turkey

• Copy of commercial Entity Registration

• Authorized Signature List of the authorities of the organization

• Non-profit Organizations

• Registration Certificates to the related government bodies.

• Foundations or Other Entities

• Documentation evidencing the activity of the organization.

____________

1The Financial Action Task Force (FATF) is an inter-governmental body established in 1989 by the Ministers of its Member jurisdictions. The objectives of the FATF are to set standards and promote effective implementation of legal, regulatory and operational measures for combating money laundering, terrorist financing and other related threats to the integrity of the international financial system. The FATF is therefore a “policy-making body” which works to generate the necessary political will to bring about national legislative and regulatory reforms in these areas. See: http://www.fatf-gafi.org/

2Source: https://europa.eu/european-union/about-eu/countries/member-countries_en

3Brexit is the forthcoming withdrawal of the United Kingdom (UK) from the European Union (EU). In the June 2016 referendum, 52% voted to leave the EU, leading into a complex separation process implying political and economic changes for the UK and other countries. As of August 2016, neither the timetable nor the terms for withdrawal have been established: in the meantime, the UK remains a full member of the European Union. The term “Brexit” is a portmanteau of the words “British” and “exit” https://en.wikipedia.org/wiki/Brexit

4See: http://ec.europa.eu/justice/criminal/files/aml-factsheet_en.pdf

5See: http://europa.eu/rapid/press-release_IP-16-202_en.htm

6See: https://www.unodc.org/documents/middleeastandnorthafrica/organised-crime/UNITED_NATIONS_CONVENTION_AGAINST_TRANSNATIONAL_ORGANIZED_CRIME_AND_THE_PROTOCOLS_THERETO.pdf