CLOSED-END FUNDS

Good intelligence is nine-tenths of any battle.

—NAPOLEON

Chapter 10 discussed mutual funds and the appeal of index funds. Some mutual funds may be even more attractive than index funds. To see this, we need to make an important distinction between open-end and closed-end funds.

Open-end funds increase or reduce the number of shares outstanding as more money is invested in the fund or withdrawn from the fund. Suppose that a mutual fund with the optimistic name BeatTheMarket has 10 million shares outstanding and owns a portfolio of stocks worth $100 million. Its net asset value (NAV) per share is calculated by dividing the market value of its portfolio by the number of shares the fund has issued.

If BeatTheMarket is an open-end fund, it will issue new shares or redeem existing shares at a price equal to the fund’s net asset value of $10 a share. If investors buy a million shares at $10 apiece, the number of shares will go up to 11 million and the fund’s assets will increase to $110 million, leaving its NAV at $10/share:

If, instead, investors were to redeem a million shares at $10 apiece, the number of shares would go down to 9 million and the fund’s assets would fall to $90 million, again leaving its NAV at $10/share:

![]()

Fair’s fair. Investors deal directly with the fund and their decisions to come or go are at a fair price, with no effect on the other shareholders.

CLOSED-END FUNDS

If BeatTheMarket is a closed-end fund, instead of an open-end fund, it issues a fixed number of shares—say, 10 million shares when it is created—and, once established, does not issue new shares or redeem old ones. Investors cannot buy new shares from the fund or sell their shares back to the fund. Instead, closed-end shares are traded on stock exchanges, where investors buy shares from existing shareholders or sell their shares to someone else—the same way that they buy or sell shares of GE and IBM.

IBM’s stock price need not equal its book value; in fact, it is seldom, if ever, equal to its book value. IBM’s stock price is whatever is needed to maintain a balance between people wanting to buy IBM stock and people wanting to sell. It is the same with closed-end funds. The market price of a closed-end fund need not be, and seldom is, equal to its net asset value.

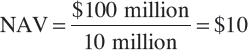

Closed-end funds typically trade at a discount from net asset value, though some trade at premiums. The discounts ebb and flow, increasing when small investors leave the stock market and shrinking when they return. Before the Great Crash of 1929, the naive enthusiasm and greed of small investors gave the average closed-end fund a 50 percent premium. One closed-end fund, the Goldman Sachs Trading Corporation, sold for a 100 percent premium. (After the crash, its price dropped 98 percent.)

Figure 14-1 shows that discounts of 20 to 30 percent were common in the 1970s, but then declined, perhaps because investors became more aware of the existence of closed-end fund discounts and the advantages of buying funds at a discount.

A DISCOUNT IS AN ADVANTAGE

A critic of closed-end funds wrote that “frequently, closed-end shares representing $25 in assets will be selling for $20. Such profits may be largely illusory, however, because when the time comes to sell, the discount may persist.” The closed-end advantage does not depend on the disappearance of the discount. Even if the discount never narrows, closed-end funds can be financially advantageous simply because investors earn dividends and capital gains on more stock than they paid for.

Suppose that BeatTheMarket is a closed-end fund with a NAV of $10 and a market price of $8, a 20 percent discount. Each share of BeatTheMarket implicitly owns stocks that would cost $10 if purchased directly. If BeatTheMarket can be bought for $8, investors pay $8 and receive dividends and capital gains on $10 worth of stock. If the annual dividends and capital gains are 10 percent of $10, investors receive $1 in dividends and capital gains on an $8 investment—a 12.5 percent return. Why pay $10 for stock that you can buy for $8?

Closed-end funds do have expenses, typically around one percent a year, a figure that is roughly consistent with a 10 percent discount. But these expenses do not explain why funds sell for 20 percent or 30 percent discounts. Nor do they explain why so many people invest in load funds, paying a premium over net asset value, when they could buy shares in a closed-end fund at a discount from net asset value. Closed-end funds may not beat the market, but they certainly beat open-end funds, especially those with load fees. Compared to open-end funds, closed-end funds are $100 bills on the sidewalk.

The explanation that most observers have settled on is that mutual funds are not bought, but sold, in the sense that people do not buy funds based on their own independent research but are instead sold funds by people who benefit from the sale, much like people are sold products by infomercials. Closed-end funds have no salespeople because they do not issue new shares. Large investors prefer to manage their own portfolios while small investors, the natural audience for mutual funds, are persuaded to buy open-end funds with load charges by salespeople who profit from the load.

I always have an eye out for closed-end funds selling for large discounts.

THE JAPAN FUND

If a closed-end fund sells at a discount from its net asset value, it is worth more dead than alive, in that its shareholders would benefit if the fund sold its portfolio and distributed the proceeds to its shareholders, either directly or by repurchasing the fund’s stock.

Let’s look again at BeatTheMarket, a closed-end fund with 10 million shares outstanding and holding stocks with an aggregate market value of $100 million, giving a net asset value of $10 a share. If the fund can repurchase one million of its shares in the open market for $8 a share (a 20 percent discount from NAV), this will cost $8 million, reducing its assets from $100 million to $92 million and reducing the number of outstanding shares from 10 million to 9 million. The net asset value increases from $10 to $10.22:

![]()

If the fund continues to sell at a 20 percent discount, the market price rises to $8.17.

The repurchase of shares at a discount always increases the net asset value of the remaining shares. Shareholders who sell do so voluntarily; those who stay enjoy an increase in the net asset value of their shares. Win-win. If a fund’s repurchase plan narrows the discount, so much the better.

An even more shareholder-friendly plan would be for BeatThe-Market to liquidate its $100 million stock portfolio and give its shareholders $10 a share, 25 percent more than the market price of their BeatTheMarket stock.

Why don’t closed-end funds routinely repurchase shares whenever a discount appears? The most convincing reason is that management fees depend on the size of a fund; so, while repurchases are good for shareholders, they are not good for management. A liquidation would be even worse for fund managers as it would cost them their jobs.

Sometimes this understandable reluctance is overcome by aggressive investors who gain control of the fund and liquidate its assets. In the 1930s, Claude Odell made millions of dollars by liquidating closed-end funds.

A more recent case involved T. Boone Pickens III, the youngest son of the famous corporate raider. In 1987 he announced that he and several partners had acquired a 5.5 percent stake in the Japan Fund, which was then selling at a 20 percent discount from net asset value. With $700 million in assets, this 20 percent discount implied a $140 million gap between the market value of the Japan Fund’s shares and the liquidation value of its assets.

Fearful that Pickens would force a liquidation, the fund’s managers recommended that shareholders approve a resolution converting the company into an open-end fund. This move would eliminate the discount, thereby increasing the value of the fund’s shares and satisfying Pickens and other shareholders while preserving the managers’ jobs. The resolution was overwhelmingly supported by those shareholders who voted, but not enough voted to give it the necessary approval by 51 percent of all outstanding shares. The fund’s managers quickly resubmitted the resolution and lobbied even harder for shareholder approval. The second time around, it did pass, and Pickens and his partners had a $10 million profit for their efforts on behalf of all shareholders.

It is interesting that, even after the conversion resolution passed in May 1987, the fund’s discount did not immediately go to zero but hovered around 5 percent. The open-end conversion would not happen until July and investors were evidently worried that the inflated Japanese stock market might crash. Either that, or $100 bills were lying on the sidewalk.

I was tempted to go for a 5 percent profit on a two-month investment, but I decided to pass. A friend of mine, a Stanford professor of economics, invested heavily in the Japan Fund, even taking out a home equity loan to buy shares. He figured that a 5 percent return over two months was a briefcase full of $100 bills. It would have been more prudent to hedge his position by selling Nikkei futures. If the Japanese stock market crashed, the profits on his futures would offset the drop in the fund’s net asset value. Instead, he took an unhedged position.

There were some scary ups and downs over the next two months, but the Japan Fund’s NAV when it went open-end was about the same as when he bought shares, and he made his 5 percent profit.

There was a very different situation in 1986. The Korea Fund, a closed-end fund that invests in Korean stocks, had 5 million shares outstanding with a net asset value of $18 and a market price of $32, a 78 percent premium over net asset value. At the time, it was difficult for Americans to invest directly in Korean stocks, and the Korea Fund was the only U.S. fund that the Korean government allowed to buy Korean stocks. Americans were willing to pay a 78 percent premium to do so through the Korea Fund. The idea that Korean companies were prospering was compelling. The idea that Korean investors did not know this and had wildly underestimated the value of Korean stocks was preposterous.

The Japan Fund, which sold at a discount, could help its shareholders by repurchasing shares. The Korea Fund, which sold at a premium, could help its shareholders by issuing new shares. It did. The Korea Fund sold 1.2 million new shares at $32, raising $38.4 million. This increased the fund’s net asset value from $18 to $20.71. Existing shareholders happily saw the net asset value of their shares increase 15 percent because new shareholders happily overpaid.

On December 31, 2015, Korea Fund shares sold for $31.85—a 10.2 percent discount from net asset value. A $10,000 investment in the Korea Fund in 1986 would have grown to $63,000 compared to $171,000 for a dollar investment in the S&P 500. The Korean miracle was real, but buying Korea Fund stock at an unrealistic premium was a distinctly poor investment.

FIRST FINANCIAL FUND

There was a time when banking was a boring profession—basically assessing the credit worthiness of local loan applicants (many of whom the bankers knew personally) and keeping accurate records. It was said to be as easy as 1, 2, 3. Pay your depositors one percent, loan the money out at 2 percent, and be on the golf course by 3 p.m.

In the 1960s and early 1970s, savings and loan associations (S&Ls) paid their depositors 2 to 5 percent interest and loaned the money out in mortgages at 4 to 8 percent, enough to pay depositors, cover expenses, and make a profit, too.

Mortgage rates topped 8 percent in 1971 and hit an unprecedented 10 percent in 1978. Most observers thought that interest rates would soon fall to more normal levels. They were wrong. Interest rates went higher still, to 18 percent plus in 1981. Homeowners who had mortgages with single-digit interest rates were lucky. The S&Ls they had borrowed from were not so lucky.

S&Ls had to raise deposit rates to double-digit levels to hold on to their depositors, but were earning single-digit interest rates on mortgages written in the 1960s and 1970s. The net worth of S&Ls nationwide fell from $23 billion at the end of 1977 to a frightening–$44 billion at the end of 1981. Yes, that is a negative sign in front of the dollar sign. The S&L industry was bankrupt. Nearly a quarter of the S&Ls operating in the 1970s collapsed or merged in the early 1980s.

So widespread and severe was the damage that Edward Yardeni, a Yale classmate and chief economist at Prudential-Bache, a major brokerage firm, defied the conventional wisdom and predicted a drop in interest rates. His outside-the-box reasoning was that the Federal Reserve would lower interest rates to bail out banks and S&Ls. In February 1985, he wrote, “The Fed must lower interest rates to offset the erosion of the financial system’s net worth. . . . Otherwise the financial system will collapse.”

He was right. Interest rates tumbled downward.

Unfortunately, Congress intervened in a clumsy way by deregulating the industry, allowing S&Ls to move away from their traditional emphasis on home mortgages and make more business loans. Some states, including California and Texas, allowed state-chartered S&Ls to invest in almost anything, including restaurants, health clubs, and wind farms.

S&Ls that were bleeding money and technically bankrupt had a choice—moan and groan through their death pangs or throw the dice and hope for a lucky roll. Bankrupt S&Ls could gamble with taxpayer money. Their net worth was already negative and the top executives would soon be unemployed; nothing worse could happen to them. If they took a huge gamble and lost, it would just be more money that the government had to pay their insured depositors. But if the gamble paid off, it might save the bank, and their jobs. These technically bankrupt S&Ls were zombie banks—dead, but walking about because of the magic of government intervention. No surprise that many zombie banks rolled the dice.

Others took advantage of the newfound freedom. Instead of applying for a loan that might be rejected, real estate developers took over S&Ls and loaned themselves money. It was cheaper for developers to pay deposit interest rates than to pay loan rates, and easier to get your loan approved if you owned the bank. They sometimes even paid themselves large fees for finding such attractive borrowers—themselves! One developer acquired an $11 million savings bank in California and increased its assets to $1 billion in less than three years, using half the deposits to finance the developer’s real estate deals. He was unapologetic: “Who would you rather lend to, yourself or a stranger?”

Interest rates fell after 1982, but losses in the banking industry continued. The problem was no longer an interest rate squeeze, but mounting loan defaults—caused too often by excessive risk-taking or outright fraud: depositor money squandered on desert land and lavish bonuses. By 1990, the S&L industry had a negative net worth of at least $200 billion. The government finally realized its mistake. It began supervising S&Ls more closely and moving quickly to chop off the heads of zombie banks.

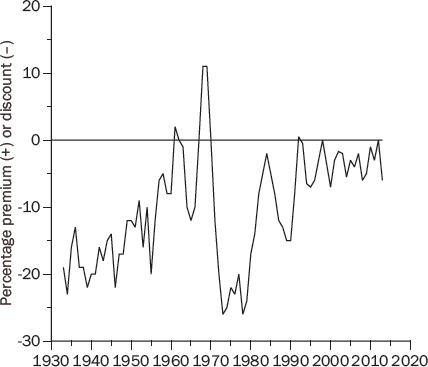

First Financial Fund (FF) was launched in May 1986, in the midst of the S&L crisis, with the objective of investing in midsize banks and S&Ls. What a terrible idea! First Financial’s stock price quickly fell to a 20 percent discount from NAV. I saw this evidently dumb idea as an opportunity. If most investors think the banking industry is going under, bank stocks are probably cheap. Remember Warren Buffett’s advice: “Be fearful when others are greedy and greedy when others are fearful.”

As for the fundamentals, the First Financial’s 2 percent dividend yield was okay, the price-earnings ratio of 6 was seductive, and the fact that the managers were repurchasing the fund’s stock at a 20 percent discount showed me that they cared about shareholders. Still, it was mostly a contrarian strategy based on my suspicion that the stock market had probably overreacted to the banking crisis, making banks and S&L stocks bargains and making First Financial’s 20 percent discount on these bargain prices a double bargain. I invested a large amount in First Financial in 1986 and 1987, at a 20 percent discount to NAV, and held on for the ride.

First Financial’s annual return was 19.4 percent during its first twenty years, compared to 11.6 percent for the S&P 500. An investment of $10,000 in First Financial at its inception was worth $345,000 twenty years later, compared to $90,000 for a similar investment in the S&P 500. It was a good twenty years for the overall stock market, but it was a great twenty years for First Financial.

Unfortunately, First Financial’s success attracted the interest of an outside group that gained control of First Financial in 2006. The outside group changed the fund’s name to First Opportunity Fund in 2008, and the fund was delisted from the New York Stock Exchange in 2010 when its focus changed from investing in banks and S&Ls to investing in hedge funds. Figure 14-2 shows First Financial’s cumulative return compared to the S&P 500 from its inception in 1986 until its delisting in 2010.

If bought at the beginning and held the entire time First Financial was in existence, a $10,000 investment in FF would have grown to $191,000 compared to $87,000 from an investment in the S&P 500. An investor prescient enough to get out in 2006, when outside investors gained control of First Financial, would have done even better.

I got out in 2004, too early, but it is foolish to think that one can buy at the bottom and sell at the top, except by accident. My simple logic for selling was my concern about the outside group’s intentions. If it ain’t broke, don’t fix it. I could see the possible upside from an outside group taking over a company that was doing badly and shaking things up. But where was the upside from shaking things up at a company that was doing wonderfully?

The intended lesson from this example is that value investors should be alert for contrarian opportunities. Just as the dot-com bubble was a time to sell, panics and crises are times to buy.

DUAL-PURPOSE FUNDS

Dual-purpose funds are closed-end funds with two shareholder classes: income and capital. The income shareholders receive all the dividends from the stocks in the fund’s portfolio; the capital shareholders receive all the capital gains on the fund’s termination date, typically ten to twenty years after the fund’s inception.

On the termination date, the income-shareholders receive a specified redemption price (usually their initial investment), or the value of the fund’s assets if this is less than the redemption price. The capital-shareholders get any excess of the fund’s assets over this redemption price.

Consider a fund that starts by selling one million income shares for $10 and one million capital shares for $10, with a fifteen-year termination at a $10 redemption price for the income-shareholders. Each income share receives dividends on $20 worth of stock, plus $10 back in fifteen years. If the fund’s stocks have a 5 percent dividend yield, the income-shareholders get a 10 percent dividend since they invested $10 and get dividends on $20.

The capital shares, meanwhile, have 2-to-1 leverage. If the value of the portfolio increases by 50 percent, from $20 to $30, the value of the capital shares increases by 100 percent, from $10 to $20. If the portfolio goes up 100 percent, the capital shares go up 200 percent.

Dual-purpose funds were created to meet the differing needs of investors, particularly when dividends and capital gains are taxed at different rates. Individuals and institutions in low tax brackets have a natural affinity for the generous dividends paid to the income shares. The capital shares hold special appeal to investors who pay lower taxes on capital gains than on dividends, and to investors who seek leverage.

No one can be made worse off by splitting the fund’s shares into two classes, because investors can, if they want, buy equal amounts of both. If you own one percent of the income shares and one percent of the capital shares, you get one percent of the profits, no matter how they are divided, just as if the company were an ordinary closed-end fund. But there are two big differences. First, a dual-purpose fund gives investors flexibility in varying the proportion of dividend income to capital gains. Second, a dual-purpose fund’s discount must go to zero on the termination date.

Figure 14-3 shows the seventeen-year history of the Gemini Fund, a very successful dual-purpose fund that was started in 1967 and terminated on December 31, 1984. In 1974 the capital shares sold at close to a 40 percent discount and the combined income and capital shares were at a 15 percent discount. For anyone who wanted to invest in stocks over the next ten years, this was an appealing way to do so. The capital shares had tremendous leverage with a huge discount that was guaranteed to vanish.

At the time, I was a low-paid assistant professor at Yale with not much money to invest. As it turned out, a $10,000 investment in the S&P 500 in January 1974 would have grown to $18,000 by 1985, a 5.6 percent annual rate of return. My $10,000 invested in Gemini Capital shares grew to $110,000, a 24.4 percent annual rate of return. Move over Warren Buffett!