108 EMPIRICAL RESULTS

0

20

40

60

80

100

NYSE (O) NYSE (N) TSE SP500 MSCI DJIA

Volatility risk (%)

Datasets

Market

BCRP

Anticor

Β

ΝΝ

CORN

PAMR

CWMR

OLMAR

(a)

0

20

40

60

80

100

NYSE (O) NYSE (N) TSE SP500 MSCI DJIA

MDD risk (%)

Datasets

Market

BCRP

Anticor

Β

ΝΝ

CORN

PAMR

CWMR

OLMAR

(b)

0

5

10

NYSE (O) NYSE (N) TSE SP500 MSCI DJIA

Sharpe ratio

Datasets

Market

BCRP

Anticor

Β

ΝΝ

CORN

PAMR

CWMR

OLMAR

(c)

0

5

10

NYSE (O) NYSE (N) TSE SP500 MSCI DJIA

Calmar ratio

Datasets

Market

BCRP

Anticor

Β

ΝΝ

CORN

PAMR

CWMR

OLMAR

(d)

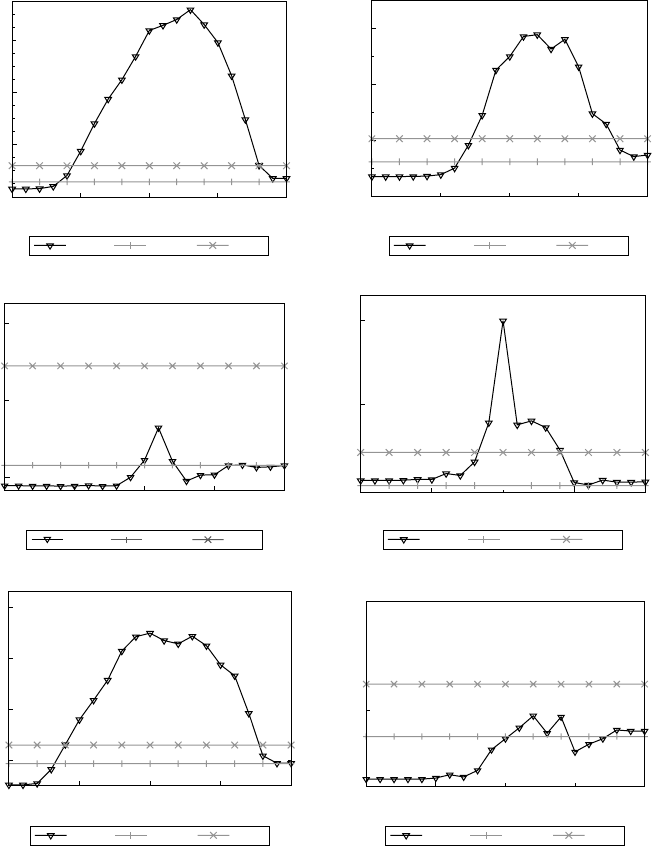

Figure 13.2 Risk and risk-adjusted performance of various strategies on the six datasets.

In each diagram, the rightmost four bars represent the results of our proposed strategies:

(a) volatility risk; (b) drawdown risk; (c) Sharpe ratio; and (d) Calmar ratio.

without high risk.

∗

The volatility risk in Figure 13.2a shows that the proposed four

methods almost achieve the highest risk in terms of volatility risk on most datasets. On

the other hand, the drawdown risk in Figure 13.2b shows that the proposed methods

also achieve high drawdown risk in most datasets. These results validate the notion

that high return is often associated with high risk.

To further evaluate the return and risk, we examine the risk-adjusted return in

terms of an annualized SR and CR. The results in Figure 13.2c and 13.2d clearly

show that CORN, PAMR, and CWMR achieve excellent performance in most cases,

∗

It is true for the long-only portfolio, which is our setting. However, such a statement may be suspect

in regard to long-short portfolios.

T&F Cat #K23731 — K23731_C013 — page 108 — 9/28/2015 — 21:35

EXPERIMENT 3 109

except the DJIAdataset; and OLMAR achieves excellent performance in all datasets.

These encouraging results show that the proposed methods are able to reach a good

trade-off between return and risk, even though we do not explicitly consider risk in

the method formulations.

∗

13.3 Experiment 3: Evaluation of Parameter Sensitivity

In the following four subsections, we evaluate how different choices of parameters

affect the proposed four strategies.

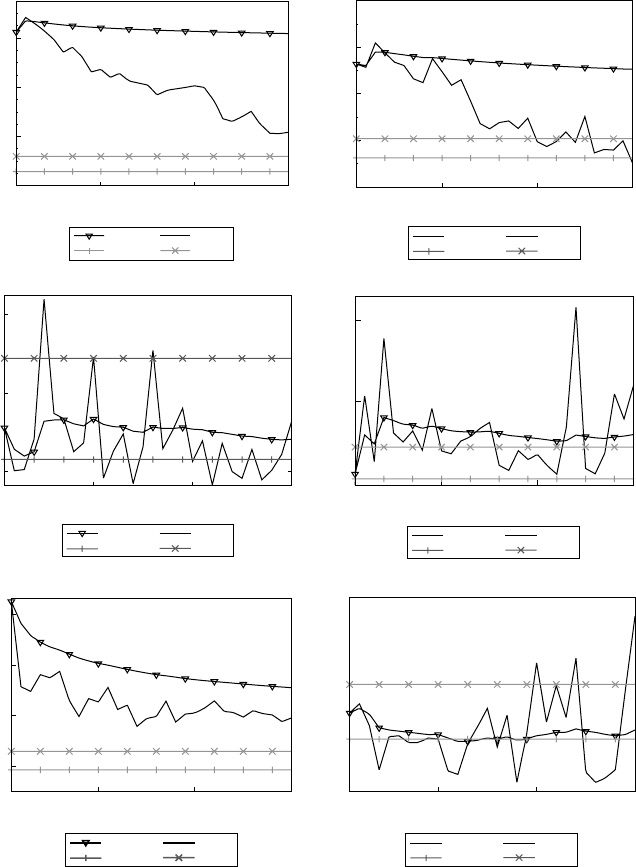

13.3.1 CORN’s Parameter Sensitivity

The proposed CORN has two parameters, that is, the correlation coefficient thres-

hold ρ and the window size for the experts w (or W ).

First, let us see the effects of ρ with fixed W , in Figure 13.3. Clearly, the figures

validate the preliminary analysis in Section 8.4. In general, CORN achieves the best

performance when ρ is around 0, as the figures often peak around 0 or some small

positive values; and, when ρ approaches −1 or 1, CORN’s performance degrades.

Although CORN does not perform well on the TSE and DJIA datasets, on which the

cumulative wealth is often less than the BCRP strategy, it significantly outperforms

the two benchmarks on other datasets. Based on the above observation, choosing a

satisfying ρ for CORN is straightforward, as some small positive values often give

good performance on all datasets.

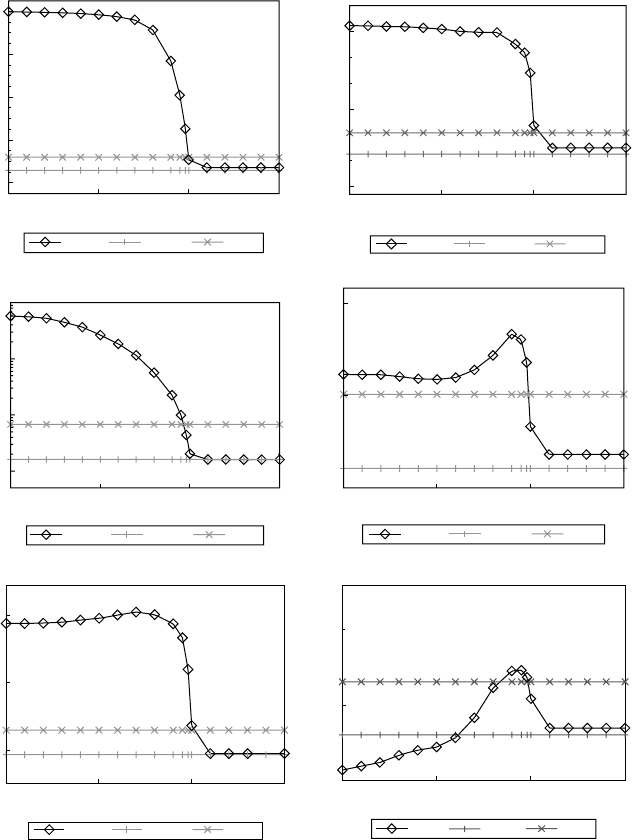

We also examine the effects of W with fixed ρ in Figure 13.4. Note that here CORN

denotes the CORN experts with a specified w and CORN-U denotes the uniform com-

bination of CORN experts with w from 1 to W . Although the cumulative wealth

achieved by CORN experts fluctuates with different w’s, CORN-U’s cumulative

wealth is much more robust with respect to W . Such an observation validates the

effectiveness of the proposed CORN-U and eases the selection of a satisfying W.

13.3.2 PAMR’s Parameter Sensitivity

In this section, we examine PAMR’s parameters, that is, the mean reversion threshold

for the three algorithms and the aggressiveness parameter C for the two variants.

First, we examine the effect of on PAMR’s cumulative wealth. As is greater

than 1, PAMR degrades to uniform constant rebalanced portfolios (CRP) strategy, and

the wealth stabilizes at a constant value achieved by uniform CRP. Thus, we show the

effect of in the range of [0, 1.5]. Figure 13.5 shows the cumulative wealth achieved

by PAMR with varying and two benchmarks, that is, Market and BCRP. Results on

most datasets, except the DJIA dataset, show that the cumulative wealth achieved by

PAMR consistently grows as approaches 0. That is, the smaller the threshold, the

higher the cumulative wealth is, which validates that the motivating mean reversion

does exist on most stock markets. Moreover, in most cases, the cumulative wealth

tends to stabilize as crosses certain dataset-dependent thresholds. As stated before,

∗

We will study it in future.

T&F Cat #K23731 — K23731_C013 — page 109 — 9/28/2015 — 21:35

110 EMPIRICAL RESULTS

10

0

10

4

10

8

10

12

–1 –0.5 0 0.5 1

Total wealth achieved

ρ

(a)

CORN

Market

BCRP

10

0

10

2

10

4

10

6

–1 –0.5 0 0.5 1

Total wealth achieved

ρ

(b)

CORN

Market

BCRP

1

5

9

–1 –0.5 0

(c)

0.5 1

Total wealth achieved

ρ

CORN

Market

BCRP

1

8

15

–1 –0.5 0 0.5 1

Total wealth achieved

ρ

(d)

CORN

Market

BCRP

1

4

16

64

–1 –0.5 0 0.5 1

Total wealth achieved

ρ

(e)

CORN Market

BCRP

1

2

–1 –0.5

(f)

0.501

Total wealth achieved

ρ

CORN

Market

BCRP

Figure 13.3 Parameter sensitivity of CORN-U with respect to ρ with fixed W (W = 5):

(a) NYSE (O); (b) NYSE (N); (c) TSE; (d) SP500; (e) MSCI; and (f) DJIA.

we choose = 0.5 in the experiments, with which the cumulative wealth stabilizes

in most cases. Contrarily, on the DJIA dataset, as approaches 0, the cumulative

wealth achieved by PAMR drops. Such phenomena can be interpreted to mean that

the motivating (single-period) mean reversion does not exist on the dataset, at least in

T&F Cat #K23731 — K23731_C013 — page 110 — 9/28/2015 — 21:35

EXPERIMENT 3 111

10

0

10

4

10

8

10

12

1

10

(a)

20 30

Total wealth achieved

W

CORN-U CORN

Market

BCRP

10

0

10

2

10

4

10

6

1 10 20 30

Total wealth achieved

W

(b)

CORNCORN-U

Market

BCRP

1

5

9

1

10 20 30

Total wealth achieved

W

(c)

CORNCORN-U

Market

BCRP

1

8

15

110 20 30

Total wealth achieved

W

(d)

CORNCORN-U

Market

BCRP

1

4

16

64

110 20 30

Total wealth achieved

W

(e)

CORNCORN-U

Market

BCRP

1

2

110 20 30

Total wealth achieved

W

(f)

CORNCORN-U

Market

BCRP

Figure 13.4 Parameter sensitivity of CORN-U with respect to w (W) with fixed ρ (ρ = 0.1):

(a) NYSE (O); (b) NYSE (N); (c) TSE; (d) SP500; (e) MSCI; and (f) DJIA.

the sense of our motivation. We also note that, on some datasets, PAMR with = 0

achieves the best. Though = 0 means moving more weights to underperforming

stocks, it may not mean moving everything to the worst stock. On the one hand, the

objectives in the formulations would prevent the next portfolio from being far from the

T&F Cat #K23731 — K23731_C013 — page 111 — 9/28/2015 — 21:35

112 EMPIRICAL RESULTS

10

0

10

4

10

8

10

12

10

16

0

ε

(a)

0.5 1 1.5

Total wealth achieved

PAMR

Market BCRP

10

0

10

3

10

6

0

(b)

0.5 1 1.5

Total wealth achieved

ε

PAMR

Market BCRP

10

0

10

1

10

2

10

3

0

(c)

0.5 1 1.5

Total wealth achieved

ε

PAMR Market

BCRP

1

4

16

0

(d)

0.5 1 1.5

Total wealth achieved

ε

PAMR

Market

BCRP

1

4

16

0 0.5

(e)

ε

1 1.5

Total wealth achieved

PAMR

Market BCRP

1

3

00.5

(f)

1 1.5

Total wealth achieved

ε

PAMR

BCRP

Market

Figure 13.5 Parameter sensitivity of PAMR with respect to : (a) NYSE (O); (b) NYSE (N);

(c) TSE; (d) SP500; (e) MSCI; and (f) DJIA.

last portfolio. On the other hand, PAMR-1 and PAMR-2 are designed to alleviate the

huge changes. In summary, the experimental results indicate that the proposed PAMR

is robust with respect to the mean reversion sensitivity parameter, in most cases.

Second, we evaluate the other important parameter for both PAMR-1 and

PAMR-2, that is, the aggressiveness parameter C. Figure 13.6 shows the effects on the

T&F Cat #K23731 — K23731_C013 — page 112 — 9/28/2015 — 21:35

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.