Chapter 4

Everything Credit: Scores and Reports

IN THIS CHAPTER

![]() Understanding and obtaining your credit reports and credit scores

Understanding and obtaining your credit reports and credit scores

![]() Improving your credit score

Improving your credit score

![]() Protecting yourself from identity theft

Protecting yourself from identity theft

You may not have given much thought to your credit report and may not know what your current credit score is. If you find yourself in that boat, I want you to pay special attention to this chapter. You should care about your credit report and credit score because lenders universally use credit scores to predict the likelihood that you’ll repay a loan, and they’ll generally only offer you a loan after they’ve reviewed your credit details. And you will only qualify for the best loan terms (lowest rates) if you have a high credit score.

Building good credit and a high credit score takes some time and effort. And even if you’re happy renting an apartment and have no plans to apply for a business loan, you should pay attention to building good credit, which I detail how to do in this chapter. There’s no way you can know now what loans or credit lines you may want or need 5, 10, or 20+ years down the road!

If you already have a good grasp of your credit report and credit score, congratulations. You’re on the right track, but I hope to show you some additional steps you can take to help your situation.

In this chapter, I explain the difference between your credit report and credit score and how to improve them both. I also detail how lenders and others use your credit information. Finally, I explain how to keep from falling victim to identity theft, which can damage your credit reports and scores and cost you time and money.

A Primer on Credit Reports and Credit Scores

Your credit report and credit score play a vital role in your financial well-being, impacting the rates and terms when you borrow money and affecting other things like your auto insurance premiums, whether or not you’re approved to rent housing, and sometimes whether or not you’re hired for a job. Therefore, you want to use your credit report and score to your advantage.

The following sections define credit reports and scores, explain how credit bureaus come up with them, point out how lenders use this information, and discuss how you can get the most from your credit during your young-adult years.

Differentiating between credit reports and credit scores

Credit reports and credit scores are different from each other, and you should understand upfront what they are and aren’t. The following sections spell out their characteristics in greater detail.

Credit reports

Your personal credit reports are a compilation and history (assembled by the three major credit bureaus: Equifax, Experian, and TransUnion) of your various credit accounts.

Your credit report details when each of your debt and loan accounts was opened, the latest balance (amount you still owe), your payment history, and so on. It specifies your track record of making payments in a timely or late fashion and whether you’ve failed to pay off previous debts.

Lenders and other creditors who have thrown in the towel on money you owe them may report a charge-off on your credit report and your report also details if you’ve ever declared bankruptcy in order to stop creditors from collecting on debts you owed. Finally, your credit report also shows who has made inquiries on your report when you’ve applied for credit. Numerous recent credit requests may indicate you’re having problems meeting your debt payments and expenses and/or having problems getting approved for a new loan.

Credit scores

Your credit score is a three-digit score based on information in your personal credit report. Because each of the big three credit bureaus (Equifax, Experian, and TransUnion) issues its own report, you actually have three different (although typically similar) credit scores.

FICO is the leading credit score in the industry and was developed by the FICO Company (formerly Fair, Isaac and Company). FICO scores range from a low of 300 to a high of 850. Most scores fall in the 600s and 700s, with the median around 720. As with college entrance examinations such as the SAT, higher scores are better. (In recent years, the major credit bureaus have developed their own credit-scoring systems, but most lenders still predominantly use FICO.) You generally qualify for the best lending rates if your credit score is in the mid-700s or higher.

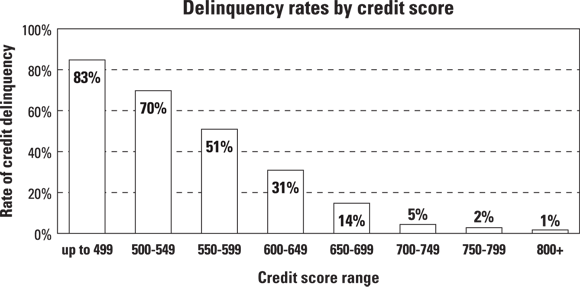

The higher your credit score, the lower your predicted likelihood of defaulting on a loan (see Figure 4-1). Conversely, consumers with low credit scores have dramatically higher historic rates of falling behind on their loans. Thus, people with low credit scores are considered much riskier borrowers, and fewer lenders are willing to offer them a given loan; those who do so charge relatively high interest rates on those loans.

The higher your credit score, the lower your predicted likelihood of defaulting on a loan (see Figure 4-1). Conversely, consumers with low credit scores have dramatically higher historic rates of falling behind on their loans. Thus, people with low credit scores are considered much riskier borrowers, and fewer lenders are willing to offer them a given loan; those who do so charge relatively high interest rates on those loans.

Source: FICO Corporation

FIGURE 4-1: Credit scores show the probability of defaulting on a loan.

Understanding how credit scores are determined

You have many credit scores, not just one. The reason you have multiple scores is because each of the three major credit bureau reports has somewhat different information about you and generates a unique score. But most consumers find, not surprisingly, that their three FICO scores from the big-three credit bureaus are fairly similar.

Credit scores change over time as your credit reports change. If you have a low score, the potential for change is good news because you can improve your score, perhaps significantly, in the weeks, months, and years ahead. The bureaus weigh current behavior more heavily than past behavior, though increasing your score is harder to do than decreasing it.

To have a credit score, you need to use credit. The FICO scoring system requires you to have at least one account open for a minimum of six months on your credit report and one account that has been updated in the most recent six months (it can be the same account).

The factors that determine your credit score include the following:

-

Your payment history: Your record of paying bills determines about 35 percent of your credit score.

Your score decreases with a recent negative mark (a late payment, for example), with a high frequency of negative marks, and with the severity of the negative mark (for instance, a 60-day late payment is worse than a 30-day late payment).

Your score decreases with a recent negative mark (a late payment, for example), with a high frequency of negative marks, and with the severity of the negative mark (for instance, a 60-day late payment is worse than a 30-day late payment). - How much you owe: This factor, which accounts for 30 percent of your score, examines the total amount you owe, as well as the amount by type of loan. The more you owe relative to your credit limits, the more adverse the effect on your credit score (most Americans use less than 30 percent of their available credit). With revolving debt (credit cards, credit lines), the greater the gap between your balances and your credit limits, the better. Also, paying down installment loans (for example, mortgages, auto loans) relative to the amount you originally borrowed will boost your credit score.

- How long you’ve had credit: Generally speaking, the longer you’ve had credit, the better for your credit score. This factor, which comprises 15 percent of your score, considers the average age of your accounts as well as the age of your oldest account.

- Your last application for credit: Applying for and opening new accounts, especially multiple new accounts, can reduce your credit score. This factor accounts for 10 percent of your FICO score.

- The types of credit you use: The FICO score rewards you for having a “healthy mix” of different types of credit (such as a mortgage, credit cards, and so on), although FICO is vague about what the best mix is. This factor accounts for 10 percent of your credit score.

Valuing of a good credit score

Generally, the higher your credit score, the better the loan terms (especially the interest rate) you receive and the more likely your loan applications are approved.

Over the course of your adult life, having a high credit score can save you tens (and perhaps hundreds) of thousands of dollars. Additionally, you can earn more money by being able to borrow money to make investments, such as in real estate or a small business.

Lenders aren’t the only ones that use credit scores. The following individuals and organizations/companies also use credit scores:

- Landlords: A high credit score can lead to the approval of your apartment rental application.

- Insurance agents: A high credit score can help you qualify for lower rates on certain types of insurance such as auto insurance.

- Prospective employers: Significant problems on your credit report can cause some employers to turn you down for a job.

Jump-starting your credit score as a young adult

If you’re just starting out financially, you may not have a credit score yet, simply because you don’t have enough information on your credit report. Don’t despair. To obtain a credit score if you don’t yet have credit, the following actions help:

- Establish a checking and savings account (and even a debit card). Doing so demonstrates financial responsibility and stability.

- Get added to someone’s credit card as a joint or authorized user. The logical person to ask would be a parent. Make sure this person is very responsible and shares your goal of keeping a terrific credit report and score. And, be sure that you are fully responsible for making your payments in a timely fashion.

- Have someone with good credit cosign a loan with you. I would only advise doing this with a relative, and only if the two of you have a long discussion about what could go wrong and have an agreement in writing to minimize the potential for misunderstandings.

-

Apply for a credit card after turning 21 years old and when you have a job, because approval is relatively easy.

Just be sure to get a card with a low annual rate and no or a low annual fee. Consider a rewards card if the benefits you can earn are something you value and will use. And be careful not to rack up balances you can’t immediately pay off every month. Most important, don’t use credit cards if having them causes you to spend more than you otherwise would.

Just be sure to get a card with a low annual rate and no or a low annual fee. Consider a rewards card if the benefits you can earn are something you value and will use. And be careful not to rack up balances you can’t immediately pay off every month. Most important, don’t use credit cards if having them causes you to spend more than you otherwise would. - If you can’t get a regular credit card, apply for a department store or gas charge card. Doing so is generally easier, but watch out for high interest rates and other fees if you can’t pay your bill in full each month. Alternatively, find out why you don’t qualify for a regular card; then work at addressing that shortcoming and reapply when your credit report and credit score have improved.

- Apply for a secured credit card. This type of card requires that you keep money on deposit in the bank that issues the card.

For what it’s worth, I am not a big fan of college students having credit cards. The reason is that most cards allow charging of substantial amounts and may lead to overspending. In the worst cases, some college students end up with large balances at high interest rates upon graduation in addition to all of their student loans. Having one credit card with a low credit limit that you can pay in full each month is worth considering because it can help build your credit rating and score.

Having a debit card is a better choice, in my opinion, for most college students because a debit card is attached to an account with a balance and thus prevents you from spending more than that amount.

Getting Your Hands on Your Credit Reports and Scores

Given the importance of your personal credit report, you may be pleased to know that each year you’re entitled to receive a free copy of your credit report from each of the three credit bureaus (Equifax, Experian, and TransUnion).

If you visit www.annualcreditreport.com, you can view and print copies of your credit-report information from each of the three credit agencies (alternatively, call 877-322-8228 and have your reports mailed to you). After entering some personal data at the website, check the box indicating that you want to obtain all three credit reports, as each report may have slightly different information. You’ll then be directed to one of the three bureaus, and after you finish verifying that you are who you claim to be at that site, you can easily navigate back to www.annualcreditreport.com so you can continue to the next agency’s site.

Your credit reports don’t include your credit score because credit bureaus aren’t required to include it by the federal law mandating that the three credit agencies provide a free credit report annually to each U.S. citizen who requests a copy. Thus, if you want to obtain your credit score, you generally need to pay for it. (An exception: You’re entitled to the credit score used by a lender who denies your loan application. For more exceptions, see the following section.)

A recent small perk from some credit-card issuers is that your credit score is listed on your billing statement. Examples are American Express, Capital One, and Walmart. While not always a FICO score, they are a close estimate.

Recommended websites for free credit scores

A few websites provide you with a free credit score without forcing you to sign up for something and/or provide your credit-card information. Here are some reliable sites:

- After verifying your identity on their website, Discover Financial Services offers your free Experian credit score with no strings attached or credit-card registration required. Visit their website at

www.creditscorecard.com/registration. (Discover does have its own credit card, and it will pitch you that online.) - The credit bureau Experian is behind the website

FreeCreditScore.com, through which you can get your free credit score. - Another free option to try is the FICO score simulator at

www.myfico.com/free-credit-score-range-estimator, which provides an estimate of your FICO score based on your answers to a series of questions about your credit usage and credit history.

Websites to avoid

Many websites, including the major credit bureaus, purport to offer you your credit score for free, but more often than not, to obtain this supposedly free score, you end up having to sign up for an ongoing and decidedly not free credit monitoring service! You may not realize that you’re agreeing to some sort of ongoing credit monitoring service for, say, $50 to $100+ per year. I don’t recommend spending money on those services. Instead, for free, request your credit report from one of the three agencies every four months to make sure your credit information is accurate (I talk about reviewing your credit report in the upcoming section) and get your credit score from one of the websites that I recommend earlier in this section.

A number of web-based entities such as Credit Karma and WalletHub claim to provide you with your credit score for “free.” These sites don’t give you the FICO credit score that lenders most often use. Instead, the sites, which do a poor job of disclosure, give you one of the credit scores developed by the credit reporting bureaus, such as the TransUnion VantageScore. As with Discover, you will be pitched a credit-card offer after obtaining your credit score. That’s how they keep these sites “free” for consumers seeking their score without paying for it.

In addition to getting a somewhat useless credit score at such sites, remember that you’re sharing with them an enormous amount of confidential information about yourself. How some of these sites make money isn’t completely obvious, but I can guarantee you that it involves finding ways (legal, hopefully) of tapping into all that information you give them. That would certainly include things like pushing auto loans, credit cards, and home mortgage loans to people in the marketplace for real estate.

Scrutinizing Your Credit Reports to Improve Them

Because your credit score is based on the information in your credit report, the first step to improving your score is to review each of your three reports (head to www.annualcreditreport.com, where you can access your credit report information from each of the three credit agencies). The following sections point out what you need to look for, what you can do to fix inaccurate information, and how you can improve your reports and credit score.

Identifying errors and getting them fixed

Carefully look through your credit reports for any potential inaccuracies. If you find any errors, you want to get them corrected quickly.

Follow these steps to ensure that you properly vet each report:

Follow these steps to ensure that you properly vet each report:

-

Review the identifying information to be sure that other folks’ information hasn’t gotten mixed up with yours.

Look for the following errors:

- Names that aren’t yours

- Incorrect Social Security numbers

- Incorrect date of birth

- Addresses where you haven’t lived

- Inspect the credit accounts for problems, such as

- Accounts that don’t belong to you

- Negative entries that don’t belong to you (such as late payments and charge-offs, which are amounts you supposedly borrowed that a lender no longer expects to get back from you)

- Negative entries that are more than seven years old

- Debts that your spouse incurred before marriage

- Incorrect entries due to identity theft or a credit bureau snafu that mixed up someone else’s information with yours

- Examine the collection actions and public records section of your report for the following errors:

- Bankruptcies more than ten years old or ones that aren’t listed by a specific bankruptcy code chapter (such as a Chapter 7 bankruptcy)

- Lawsuits, judgments, or paid tax liens more than seven years old

- Paid liens or judgments that are listed as unpaid

- Loans that went into collection that are listed under more than one collection agency

- Any negative information that isn’t yours

If you identify any errors, you can submit corrections by using one of the online forms for disputing incorrect information that accompany your credit reports. All credit bureaus are mandated to investigate and correct errors within 30 days. Your persistence may be required.

Boosting your credit score

After you get your credit report cleaned up, here are some ways that everyone can improve their credit score:

-

Pay your bills on time. The better your credit score, the more a late payment harms your score because such a change in behavior may indicate increasing financial difficulties.

To avoid making late payments, consider putting your bills on an automatic payment system either through your bank’s online bill-pay service or the company’s auto-pay option (if they offer one). Major investment firms like Fidelity and Schwab also generally offer cash management accounts that provide similar banking services. If you’ve never used automatic payments and you’re skittish, try the system first with one company you trust the most. Another option is to put the charges on your credit card. Only do this, however, if you always pay your credit-card bill in full each month. Be cautious charging large bills on your credit card because using a big portion of your available credit can reduce your credit score. Also be sure that the companies you’re paying don’t charge an extra fee for using your credit card for payment. - Pay down your debt. Paying down your debts over time is exactly the kind of responsible credit behavior that lenders want to see in the folks to whom they lend money. The lower the portion your balances are of your credit limits (try to keep them under 30 percent), the better your credit score will be. For this reason, you should avoid both consolidating debts and charging so much on a card in a month that you near the card’s credit limit.

- Avoid closing credit-card and other revolving accounts. Closing accounts makes your remaining balances look that much larger in comparison to your total available credit. Also, closing older accounts lowers the average age of your credit accounts, which reduces your credit score.

- Apply for credit sparingly. Applying for credit more frequently lowers your credit score.

Preventing Identity Theft

A study by Javelin Strategy & Research found that young adults are at significantly greater risk for identity theft than people in other age groups. This is largely a function of young people spending so much time online and due to a general lack of experience with being the victim of such problems and learning from the incident. Therefore, you must be proactive in preventing your personal information and accounts (bank, investment, credit, and debit) from being used by crooks to commit identity theft and fraud.

Victims of identity theft can suffer trashed credit reports, reduced ability to qualify for loans and even jobs (with employers who check credit reports), out-of-pocket costs, and dozens of hours of time to clean up the mess and clean their credit records and name.

According to the aforementioned study, young adults are at greater risk for identity theft because

- Their use of social networking exposes confidential information. Younger people use social networking websites more heavily than others, and these sites promote the sharing of personal information. Those who use social networking sites are twice as likely to suffer identity-theft problems.

- They’re common targets of friendly fraud. Younger people are at far greater risk of friendly fraud, in which the perpetrator (family members, domestic workers, employees who have access to personal information, and so on) is known to the victim.

- They take much longer than older folks to detect fraud. Younger people are less likely to closely monitor accounts and credit reports that could reveal that fraud is taking place.

Here’s how to greatly reduce your chances of falling victim to identity theft:

- Don’t provide personal information over the phone or via text message, unless you initiated the call/exchange, and you know well the company or person on the other end. And don’t fall for incoming calls/texts that your caller ID says are coming from a particular business, because folks have found ways to dupe caller ID systems. Suppose you get a call/text from someone saying he is with Chase Credit Card services and is contacting you about a problem with your credit-card account. If you have an account with Chase, ask the person to provide you with his contact information and name. End the exchange; then get out your credit card, call the phone number listed on the back of your card, and ask the representative you speak with to verify whether the previous contact you received was legitimate or not.

- Ignore emails soliciting personal information or action. Online crooks are clever and can generate a return/sender email address that looks like it comes from a known institution but really does not. This unscrupulous practice is known as phishing, and if you take the bait, visit the site, and provide the requested personal information, your reward is likely to be some sort of future identity-theft problem. Never click on links in emails, and only access your online accounts by typing in your bank’s URL or by using your own created bookmarks.

-

Review your monthly financial statements. Although your bank, mutual fund, and investment company may call, text, or email you if they notice unusual activity on one of your accounts, some people discover problematic account activity by simply reviewing their monthly credit card, checking account, and other statements. Review line items on your statement to be sure that all the transactions are yours.

You can simplify this process by closing unnecessary accounts. The more credit cards and credit lines you have, the more likely you are to have problems with identity theft and to overspend and carry debt balances. Unless you maintain a separate card for your own small business transactions (or carry an extra card or two due to the rewards those cards offer you), you really need only one piece of plastic with a Visa or Mastercard logo. Give preference to a debit card if you have a history of accumulating credit-card debt balances.

- Periodically review your credit reports. Some identity-theft victims have found out about credit accounts opened in their name by reviewing their credit reports. Because you’re entitled to a free credit report from each of the three major credit agencies every year, you could review one agency report every four months to keep a close eye on your reports and still obtain them without cost. Is it necessary to review your credit reports that frequently, and do I personally do this? The answer to both of those questions is no! But you may want to scrutinize your reports that often if you’ve had problems or otherwise have reason to be concerned about the security and integrity of your credit. (See the earlier section “Scrutinizing Your Credit Reports to Improve Them” for more information.)

- Freeze your credit reports. Thanks to a change in federal law in 2018, you may freeze your credit reports for free, which is done through a PIN code at each credit bureau. Doing so puts you in total control of who may access your credit report. To “unfreeze” your reports, you will again use your PIN code at each credit bureau. In addition to contacting the three major credit bureaus, the last listing is a credit bureau used by cell-phone companies and utilities:

- Equifax:

www.equifax.com/personal/credit-report-services/or call 800-349-9960. - Experian:

www.experian.com/freeze/center.htmlor call 888-397-3742. - TransUnion:

www.transunion.com/credit-freeze/place-credit-freezeor call 888-909-8872. - National Consumer Telecommunications & Utilities Exchange:

www.exchangeservicecenter.com/Freeze/jsp/SFF_PersonalIDInfo.jspor call 866-349-5355.

- Equifax:

-

Avoid placing personal information on checks. Information that’s useful to identity thieves and that you shouldn’t put on your checks includes your credit-card number, driver’s license number, Social Security number, and so on. I also encourage you to leave your home address off your preprinted checks when you order them. Otherwise, everyone whose hands your check passes through gets free access to that information.

When writing a check to a merchant, question the need for adding personal information to the check (in fact, in numerous states, it’s against the law to request and place credit-card numbers on checks). Use a debit card instead for such transactions.

- Protect your computer. If you keep personal and financial data on your computer, use up-to-date virus protection software and a firewall, and password-protect access to your programs and files.

- Protect your snail mail. Stealing postal mail from most mailboxes is pretty easy, especially if your mail is delivered to a curbside box. Consider using a locked mailbox or a post-office box to protect your incoming mail from theft. Consider having your investment and other important statements sent to you via email, or simply access them online and eliminate mail delivery of the paper copies. Minimize your outgoing mail and save yourself hassles by signing up for automatic bill payment for as many bills as you can. Drop the rest of your outgoing mail in a secure U.S. postal box, such as those you find at the post office. (If you continue receiving paper statements, consider getting a shredder to shred documents you want to dispose of.)