The Political Macroeconomy

Macroeconomics and National Politics

The relation between national politics and the macroeconomy is always a timely and relevant subject. Public perceptions of the president and the Congress are affected by whether the economy is strong or weak. Citizens reward political incumbents with increased reelection votes if a strong economy occurs. Citizens punish incumbents with reduced votes if a weak economy occurs. Politicians consequently promote policies they think will attain strong economic performance to increase their likelihood of reelection.

This book addresses some concepts, issues, and evidence on the interrelation between American national politics and the U.S. macroeconomy. Electoral, partisan, and other political pressures affect the macroeconomic policy and the state of the economy. The state of the economy, in turn, affects election outcomes, public sentiment, partisan pressures, and other political considerations.

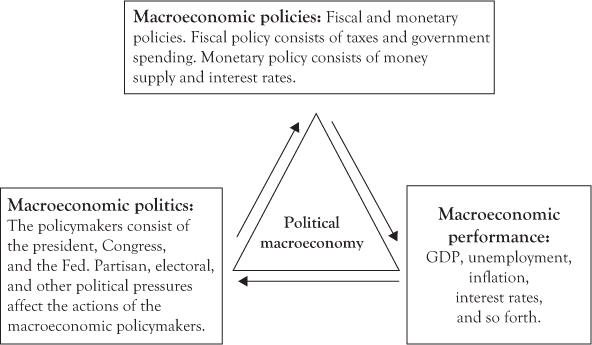

An overview of the main concepts of the political macroeconomy may be expressed using a triangle flow diagram. The Political macroeconomy consists of three elements: (1) macroeconomic politics, (2) macroeconomic policy, and (3) macroeconomic outcomes. Figure 1.1 shows the triangle flow diagram.

Figure 1.1 Triangle flow of the political macroeconomy

Electoral and partisan politics, the policy preferences among policymakers, and the interactions among the macroeconomic policymakers determine macroeconomic policies. The three main macroeconomic policymakers are the president, the Congress, and the central bank (i.e., Federal Reserve or Fed). Macroeconomic policies, in the form of fiscal and monetary measures, affect macroeconomic outcomes such as gross domestic product (GDP), unemployment, inflation, and interest rates. The condition of the economy then impacts public opinion and voter behavior regarding elected politicians.

Macroeconomic Politics Influence Macroeconomic Policies

Macroeconomic politics are national political pressures that influence the macroeconomic policy actions of elected politicians and the central bank. Two main categories of political pressure impact the macroeconomic policy actions of the president and the Congress, and to some degree the central bank.

The two main categories of political pressure are electoral politics and partisan politics. Special interests can also affect macroeconomic policy decisions. The impact of special interests on macroeconomic policy, however, partially overlaps with partisan influence. This occurs because special interest groups tend to be aligned with political parties. Labor interests, for example, tend to align with the political left, while business interests tend to align with the political right.

- •Electoral macroeconomic politics: The public exerts political pressure on the president and the Congress to adopt macroeconomic policies that accomplish the economic interests of voters. Electoral influence occurs through the voting process and public opinion. Some factors that weigh on public opinion and voting behavior are the state of the economy, media activity, and the views of opinion leaders in society. The president and congressional legislators typically seek reelection. Consequently, elected officials consider the macroeconomic preferences of voters in determining the macroeconomic policy to improve reelection prospects.

- •Partisan macroeconomic politics: Political parties exert pressure on member politicians to adhere to partisan economic platforms. To receive political party endorsements, politicians tend to support the preferred macroeconomic policies of their political parties. The partisan influence theory asserts that the political right (Republican party) tends to be relatively inflation averse in its macroeconomic policy preference, while the political left (Democratic party) tends to be relatively unemployment averse.

Electoral and partisan pressures affect the macroeconomic policy actions of the macroeconomic policymakers. Macroeconomic policies consist of fiscal measures and monetary measures. The fiscal policy mainly consists of the influence of taxes and government spending on macroeconomic outcomes. The fiscal policy occurs through the government budgetary process involving the political interaction between the Congress and the president. This interaction occurs in the context of the macroeconomic policy agendas of the conservative and liberal political parties. The president and the Congress consider voter economic attitudes and partisan macroeconomic platforms when implementing fiscal policy.

Monetary policy occurs through the actions of the Fed. The Fed chairman and the Federal Open Market Committee of the Fed are the main monetary policymakers. Monetary policy is the influence of money supply and interest rates on the macroeconomy. A simplifying assumption often made in political macroeconomic analysis is that monetary policy tends to coincide with the macroeconomic preference of the president. The realism of this assumption is addressed in Chapter 9.

Two important political influences affect monetary policy as administered by the central bank. They are the presidential appointment of the Fed chairperson and periodic congressional hearings that involve testimony by the Fed chairperson. Additionally, the monetary policy decisions by the Fed are susceptible to political pressure from financial special interests, the media, opinion leaders, and public opinion.

Macroeconomic Policies Impact Macroeconomic Performance

Chapter 2 discusses the main macroeconomic indicators, including GDP, inflation, unemployment, interest rates, and the business cycle. Understanding the main macroeconomic measurements establishes a foundation for consideration of politico-macroeconomic effects.

The business cycle is the up-and-down pattern of macroeconomic performance over time. An economic expansion or boom denotes a growing economy as measured by rising real GDP (RGDP) and declining unemployment. A recession in the business cycle denotes a declining economy as measured by decreasing RGDP and worsening unemployment. The performance of inflation during the up-phase versus the down-phase of the business cycle depends on the underlying macroeconomic supply and demand factors.

Chapter 3 examines the macroeconomic supply and demand forces that determine inflation, unemployment, and real economic growth in the short run and in the long run. The framework we will use is the expectations-augmented Phillips curve model. This model explains the interconnection between inflation and unemployment. The empirical relation of Okun’s law is also examined. Okun’s law expresses the empirical connection between GDP and unemployment. The three indicators of GDP, unemployment, and inflation are important considerations for political macroeconomic analysis because these variables affect voter opinions as well as presidential and congressional election outcomes. These three economic indicators are also important factors for the preferred macroeconomic agendas of the left and right political parties.

Through legislation such as the Employment Act of 1946 and the Full Employment and Balanced Growth Act, the federal government has the responsibility to promote strong macroeconomic performance. Three major measures of a strong economy are high RGDP growth, low unemployment, and low stable inflation.

Chapter 4 examines macroeconomic policy, also called stabilization policy. The macroeconomic policy affects macroeconomic outcomes, such as inflation, unemployment, economic growth, and the pattern of the business cycle. The macroeconomic policy may be expansionary or contractionary. An expansionary policy seeks to attain high RGDP and low unemployment. These two macroeconomic objectives generally coincide with each other. High economic growth tends to occur alongside low or declining unemployment as employers hire more workers to produce more goods and services.

A short-run macroeconomic trade-off, however, sometimes occurs regarding inflation. In some circumstances, the goals of high economic growth and low unemployment conflict with the other objective of low inflation. The simultaneous attainment of low inflation along with high economic growth and low unemployment is not always possible. The two goals of low unemployment and high economic growth may come at the long-run economic cost of greater inflation. For example, during the Kennedy–Johnson presidencies of the 1960s, an expansionary macroeconomic policy led to a decrease in unemployment from 6.7 to 3.6 percent, while inflation rose from 1.1 to 4.2 percent.

In contrast to an expansionary policy, the main goal of a contractionary policy is to reduce inflation. This objective, however, may occur at the short-run cost of declining real economic growth and worsening unemployment, possibly even a recession. Policymakers do not generally seek higher unemployment. In some instances, however, higher unemployment is unavoidable to bring down inflation. For example, in the early 1980s, during the first term of Ronald Reagan, the Fed sought to curb high inflation that was inherited from the oil shocks of the 1970s. Through a contractionary macroeconomic policy, inflation fell from around 10 percent in 1981 to about 3 percent in 1983. This, however, came at the cost of a severe recession and a rise in unemployment from approximately 7½ percent to more than 9½ percent.

Macroeconomic Performance Impacts Macroeconomic Politics

The condition of the economy affects various measures of public opinion and voter behavior:

- •Presidential election outcomes

- •Congressional election outcomes

- •Presidential job approval

- •Voter participation rates

- •Macropartisanship

- •Societal happiness index

- •Consumer sentiment

These indicators of voter sentiment and behavior are discussed in Chapter 10. For example, the public holds the president accountable for the condition of the economy through the democratic process of voting and opinion polls. The conventional theory (responsibility hypothesis) asserts that a strong economy tends to boost presidential approval, which improves the likelihood that the incumbent or the candidate from the incumbent political party will win reelection to the presidency. The incumbent political party, or the in-party, is the party that controls the White House prior to a presidential election. The opposition political party, or the out-party, is the party that is not in control of the White House. If a Democratic president is in the White House preceding an election, then the Democratic Party is the in-party. If a Republican is in the White House prior to an election, then the Republican Party is the in-party.

The responsibility hypothesis asserts that a weak economy lessens the prospect that the in-party will gain reelection to the White House. Citizens are inclined to penalize the in-party with low reelection votes if a sluggish economy occurs. The in-party consequently has a strong incentive to establish policies that achieve strong economic performance to improve reelection chances.

Intersection between Macroeconomic Performance and Macroeconomic Politics

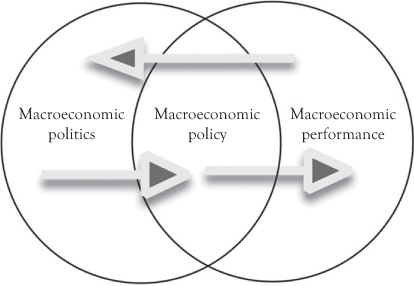

The main characteristics of the political macroeconomy may be shown using a Venn diagram. Figure 1.2 shows the union and intersection of the political and economic spheres of the political macroeconomy.

Figure 1.2 Intersection and union of the two spheres of the political macroeconomy

Macroeconomic policy occurs at the intersection between the political and macroeconomic spheres of the political macroeconomy. Macroeconomic politics—in the form of electoral and partisan pressures—impact the macroeconomic policy decisions of the president, the Congress, and the Fed. Macroeconomic policies subsequently affect macroeconomic events such as GDP, unemployment, and inflation, and the pattern of the business cycle.

The macroeconomic policy may be expansionary or contractionary, based on whether the main goal of the policymakers (as influenced by partisan and electoral pressures) is to reduce unemployment or fight inflation. The level of macroeconomic performance then impacts voter attitudes, election results, and partisan economic priorities, which affects the next round of macroeconomic policy decisions by the policymakers.

Political Macroeconomy of Peace and Prosperity versus Conflict and Poverty

Another type of politico-macroeconomic effect is the relation between the economic conditions of a nation-state and its political stability. Although not an absolute generalization for all circumstances, the greater the economic prosperity of a country, the stronger the probability of political stability. Moreover, international economic prosperity among nations increases the likelihood for peaceful relations among those countries.

For example, the economic development and international trade and financial flows among western industrialized countries in the post–World War II era played a major role in the relatively peaceful relations among those nations. Countries that conduct substantial international commerce with one another are less prone to go to war against one another. This is because the destructiveness of war disrupts the profitable flow of economic activity among nations.

Besides the link between economic prosperity and political peace and stability, a reverse causation also occurs. Economic crises, severe income inequity, and poverty tend to worsen political discontentment and strife. Economic plight is also a contributing factor to terrorism and war. A classic example was the economic collapse and hyperinflation of Germany in the aftermath of World War I. In consequence of the 1919 Treaty of Versailles and the 1921 London Ultimatum, Germany was economically penalized for starting World War I. War reparations and other stringent measures were placed on Germany as a retribution.

To manage the heavy war debt, Germany monetized much of its financial obligations. This action of excessive printing of money (monetization) to pay international war debt caused hyperinflation and economic breakdown in Germany in the early 1920s. Additionally, the subsequent worldwide Great Depression of the early 1930s compounded Germany’s economic turmoil.

This economic catastrophe fueled a political climate of fascist extremism in Germany and elsewhere in the world (e.g., Italy, Japan). Hitler was able to seize political and military power in Germany because of this unstable economic and political environment. This series of economic and political crises led to the Nazi war machine and the outbreak of World War II in Europe.

Economic prosperity tends to promote political stability and peace, while poverty and economic collapse often breed social dissatisfaction and even war. Table 1.1 summarizes the interconnection between the state of the economy and political stability.

Table 1.1 Peace and prosperity versus war and poverty

Economic condition |

Political consequence |

Politico-macroeconomic outcome |

Economic prosperity |

Political stability and tranquility |

Peace and prosperity |

Economic breakdown |

Political instability and discontent |

Social conflict and poverty |

The Classical View versus Keynesianism

The classical view versus Keynesianism are the two main perspectives on the role of government versus market forces in the economy. The subsequent chapters examine some implications of these two opposing perspectives regarding political ideology, macroeconomic policy and performance, political party economic preferences, and voter behavior. The two perspectives of classicism versus Keynesianism tend to be loosely aligned with the two political ideologies of the political right versus the political left.

The classical view asserts that market forces are relatively stable, efficient, and flexible. This perspective fears that government intervention in the economy often adversely distorts prices, hinders production, and causes inefficiency. This viewpoint maintains that market forces normally yield win-win or positive-sum results for buyers and sellers, including the labor and business sectors of the economy. Any adverse results from market forces that may arise, according to the classical view, are often mild and short-lived. Flexible prices and business competition in the market system will normally cure economic inefficiencies, such as a recession.

The classical perspective argues that government intervention in the economy is frequently harmful, even if well-intentioned. Government economic activism often creates unforeseen and adverse economic consequences, according to the classical view. This perspective maintains that government is usually not sufficiently well-informed to recognize and implement what is best for economic society. Even if the government possesses altruistic economic motives, the policy actions that take place often create harmful unintended consequences, such as high prices, less economic innovation, and lower economic growth.

The classical view argues that the state is often less effective than decentralized market forces in determining the economic outcomes that are best for society. The flexibility of decentralized market forces is more efficient and beneficial than government controls, regulation, and government production of goods and services.

The concept of government failure refers to the negative consequences of activist government policies on the economy. For example, the state could mistakenly or shortsightedly adopt policies that overstimulate the macroeconomy in an attempt to increase economic growth and reduce unemployment. However, a negative result of higher inflation could occur with no lasting benefit on economic growth. Another example is governmental controls that could end up overregulating, overtaxing, or otherwise over-constraining the economy in various ways, which could hinder economic growth.

The classical view states that the government’s role in the economy should be relatively minor. This perspective prescribes low taxes, low government spending, and minimal government regulation of the business, labor, financial, and consumer sectors. Citizens with a classical laissez-faire economic outlook tend to identify with the political ideology of the conservative right. This outlook generally aligns politically with the Republican Party and other conservative political perspectives, such as libertarianism.

In contrast to the classical view, the other main macroeconomic perspective is Keynesianism. This perspective is named after John Maynard Keynes, the noted 20th century British economist. Keynes advocated an activist fiscal policy to address the Great Depression of the 1930s. The New Deal economic programs to combat the Great Depression in the United States were an example of Keynesian government stimulus. Keynesianism asserts that government intervention in the macroeconomy is sometimes necessary to resolve inefficiencies, imperfections, and rigidities in market forces. The concept of market failure denotes the detrimental side effects of market forces.

Keynesianism maintains that market forces sometimes become unstable, inflexible, and inefficient. The Keynesian view states that market forces sometimes generate market failures, especially in the labor and financial markets. Market failures arise from economic rigidities, bottlenecks, uncertainty, speculation, and excessive economic risk aversion to entrepreneurship and innovation. These potential market deficiencies generate harmful macroeconomic consequences, including the episodic occurrence of severe recessions. The Great Depression of the 1930s is the usual example of a major market failure, according to Keynesianism. In contrast to Keynesianism, many classicists (and monetarists) argue that mismanagement of monetary policy by the Fed (rather than market failure) was a major reason for the Great Depression.

Keynesianism asserts that government has a duty to intervene in the economy through macroeconomic policies to resolve recessions that otherwise could end up being long and severe. The Keynesian view prescribes expansionary macroeconomic policies to boost macroeconomic demand, also called aggregate demand. Keynesian macroeconomic stimulus seeks to create jobs and raise GDP through government intervention.

Higher government spending, lower taxes, and lower interest rates are standard Keynesian techniques aimed at alleviating weak economic performance. Individuals with a Keynesian macroeconomic outlook tend to identify with the political left ideology and the Democratic party in the United States.

The conservative and liberal political parties tend to have differing macroeconomic priorities. Chapter 7 discusses this subject and the related topic of liberal and conservative partisan cycles in the macroeconomy. Conservative presidencies, for example, tend to emphasize minimal government involvement in the economy and macroeconomic policies that emphasize low, stable inflation. Liberal presidencies tend to adopt more activist government macroeconomic policies that emphasize low unemployment as the primary objective.

Table 1.2 summarizes the connections among the macroeconomic perspectives, political ideologies, political party preferences, and the roles of government versus market forces.

Table 1.2 Classical view versus Keynesian view

Macroeconomic perspective |

Political ideology |

Political party affiliation |

Impact of market forces |

Government economic activism |

Partisan macroeconomic priority |

Classical view |

American political conservatism (also libertarianism) |

Republican party |

Market forces generally efficient, if unimpeded by government |

Government failure that worsens the economy |

Low inflation emphasis |

Keynesian view |

American political liberalism |

Democratic party |

Periodic market failures, such as recessions |

Government activism can remedy market failures |

Low unemployment emphasis |

Median Voter Model and Political Business Cycle Effects

Chapter 5 looks at the theory of rational voter behavior and the median voter model. This framework addresses the interaction among voters and policymakers. The model asserts that government actions (including macroeconomic policy) tend to align with the median voter’s most preferred political outcome. This occurs through vote-maximizing economic policies adopted by politicians and political parties. We discuss the assumptions and realism of the median voter model.

Chapters 6 and 7 examine political influence on macroeconomic policy and the business cycle. The two main political business cycle (PBC) effects are the electoral cycle and the partisan cycle. The electoral cycle effect occurs from presidential manipulation of macroeconomic policy to create an economic boom in an election year as an attempt to increase reelection votes. The partisan cycle refers to the effects of the differing macroeconomic preferences of the left and right political parties on the business cycle.

Chapter 8 examines inflation and unemployment in the U.S. economy for evidence of the two PBC effects during the period from 1961 to 2016. The results suggest that the partisan cycle tended to occur during Democratic presidencies. Macroeconomic outcomes during most Republican administrations, on the other hand, were more compatible with the electoral cycle.

Chapter 9 considers some additional issues on the American political macroeconomy. For example, one key assumption of the partisan and electoral cycle theories is that the president can manipulate the macroeconomic policy. We consider the realism of this assumption. We likewise discuss the predictability of macroeconomic performance in response to stabilization policy. We also discuss the issue of independence of the Fed.

Chapter 10 surveys the subject of economic influence on voter behavior and some measures of citizen sentiment. We consider macroeconomic influence on the presidential vote, the congressional vote, and presidential approval. We also discuss economic influence on measures of public opinion and behavior such as macropartisanship, the voter participation rate, the social happiness index, and consumer sentiment.

Chapter 11 then examines some international aspects of the political macroeconomy. We consider the political economy of free trade versus protectionism. We also discuss the three international ideological perspectives of economic liberalism, neomercantilism, and structuralism. Finally, Chapter 12 summarizes the main ideas of this book and provides concluding remarks on the American political macroeconomy.