CHAPTER 9

Project Contracts and Agreements

Critical to Project Finance

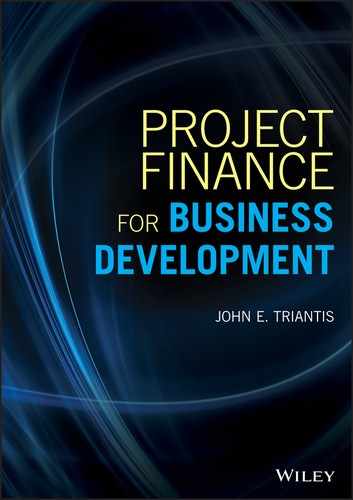

The contracts and agreements part of project finance is a highly specialized field of legal expertise and this chapter aims only to introduce the basics of the types and nature of project documentation created by the sponsor's legal team. The intent of this chapter is to show the multitude and complexity of project contracts necessary to create the framework for project financing. To make the point, Figure 9.1 shows the signatories to and the commonly negotiated project finance contacts.

Figure 9.1 Signatories and Common Project Finance Contracts

Source: Adapted from Merna, Chu, and Al‐Thani (2010).

Having identified project risks and issues, the purpose of project contracts and security packages is to bring some certainty by addressing mitigation of potential future risks to the satisfaction of affected project stakeholders. Hence, familiarity with project contracts and their negotiations is a requirement of PFO and project team members. It is also a prerequisite for striving to obtain competitive advantage through project finance.

An agreement is one's commitment to deliver on an obligation that is accepted by another party. It is like a contract but it is not enforceable by law. A contract is a written and usually registered agreement supported by consideration and enforceable by law. Legally, an agreement binds neither party but a contract does and, hence, the need to document and negotiate agreements and create valid contracts. Contracts are a part of doing business and their importance derives from their use in legal systems to ensure compliance by all parties involved. They state the parties' expectations in terms and conditions, protect the confidentiality of project proposals, provide certainty for the parties involved, and create a basis to address disputes.

In project finance deals, contracts use standardized terms and conditions and deal with a lot of details in order to facilitate the project finance process. The type of contracts and their content vary by project, but in all cases they protect the parties from legal claims and counterclaims and reduce the likelihood of ending up in an international court of law. Because contracts hold all project finance participants accountable to written deliverables, project specifications, and performance expectations they hold the project together, enable project financing, and protect contract signatories from costly changes and surprises.

The structure, prerequisites, and costs of developing and negotiating project contracts are discussed in Section 9.1, and the process ordinarily followed by legal teams is presented in Section 9.2. The common types of project finance contracts that project teams encounter are briefly described in Section 9.3, and the challenges of project finance contract development and negotiation are the topic examined in Section 9.4. The last section, Section 9.5, addresses the factors that successfully complete contracts and projects.

9.1 STRUCTURE, PREREQUISITES, AND COSTS OF CONTRACTS

The role of the legal team is to provide answers to project‐participant questions, organize the process of creating and negotiating project contracts, and provide a fair balance in the structure of the project's costs and benefits to make it sustainable. In the project finance literature, the terms contracts and agreements are used interchangeably, but in this chapter we will only use the term contract. Project finance contracts vary by size, type, and the parties involved but they all have similar structures and prerequisites, yet involve substantially different costs to create. The structure of contracts refers to the specific content used to lay out the participants' rights and obligations while contract prerequisites state what must be in place before contracts are drafted, negotiated, and approved.

The project prerequisites are the basis of contracts once they are satisfied and include the following:

- Harmonized stakeholder interests and managed expectations to reasonable levels

- Proper project screening and sound economic evaluation that validate project viability

- Appropriate project specification and requirements evaluation to ensure technical feasibility

- Comprehensive risk identification, assessment, mitigation, and balanced risk allocation

- Thorough due diligence to verify project viability and stakeholder ability to deliver on obligations

- Adequate sponsor equity, insurance coverage, and security packages

- Sound project financial model structure with validated inputs and output evaluations

- Reasonable and tested assumptions and scenarios used to generate financial forecasts

Project prerequisites also include the project stakeholder qualifications, eligibility, and ability to deliver on their human, physical resource, and financial obligations. A good part of the verification of project prerequisites takes place during the project development stage. International contracts are similar to domestic contracts but have some differences related to the rights of the signatories in different countries, so specifying the language and governing law used in project finance documents that control the transaction's dealings is crucial. Why? Because the enforceability of contracts requires that both the sponsor's and the host country's laws are stated in a common language, usually English, with the ability to enforce obligations.

The cost of developing project documentation and negotiating contracts is a significant project development cost component incurred over a period of several months or years and includes the following expenditure elements:

- The salaries of legal personnel and wages of support and clerical staff

- Travel‐related expenses for fact‐finding meetings and preparation of agreements

- Acquisition of internal data and information from external providers and reviewers

- Drafting of agreements, printing, distribution, and review

- Updates and changes to contracts to include new information and lender requirements

- Obtaining expert witness studies, reviews, opinion, and independent validation and verification

- Storage and retrieval costs of legal documents and contracts produced for the project

- Management and monitoring of contracts to ensure compliance in the host country

- Expenses incurred to resolve legal issues outside the court system of the host country

Up until the mid‐1990s, the storage of legal documents and contracts for large project financings could take the entire space of a large room, but now contracts and related documents are stored online and accessible by parties who have a need to know. It is commonly understood that because of the necessarily high legal team costs to create and negotiate contracts, projects under $75 million are difficult to prove profitable.

9.2 CONTRACT DEVELOPMENT AND NEGOTIATION PROCESS

The discussion of the project finance contract development and negotiation process herein is from the sponsor PFO's perspective. It is rather sketchy and lacking intermediate activities and steps performed by the legal team. It does, however, show the basic steps taken by the sponsor company's legal department that include:

- Forming the contract development and negotiation team and linkages with the core project team, defining roles and responsibilities, and initiating contact with counterparts in other stakeholder organizations and potential funding sources

- Identifying and assessing stakeholder expectations and contributions, verifying qualifications to enter into contracts and ability to deliver on current and future obligations

- Developing a sponsor partnership agreement and forming the special purpose vehicle such as to maximizing the tax benefits to the sponsor(s)

- Undertaking a host country fact‐finding effort that involves legal and regulatory, environmental, and industry‐structure evaluation; tax, labor, and environmental law review

- Assessing the host government's competitive tender system, reviewing the business and industry environment, and obtaining contracting information and project requirement details

- Reviewing the sponsor company's corporate strategy and risk tolerance, evaluating the feasibility study results, and defining contract needs and legal requirements in accordance with project objectives

- Identifying project‐critical success factors, links and dependencies, and project governance issues and determining key contract development and negotiation process objectives

- Assessing project stakeholder organizations, values, and skills and competencies, and leading the due diligence effort jointly with the lender's legal team

- Evaluating information assembled for decision making and developing a coordinated workflow and measurement and control system consistent with the project team's processes

- Assessing the due diligence report, determining project risks, and evaluating the adequacy of risk mitigation and enhancement requirements

- Creating a repository for management of contracts and their terms and conditions and identifying tools, systems, data, analyses, and evaluations needed

- Assembling and cataloging all contracting information, beginning discussions with the host government's contracting authority and funding sources, and developing plans and schedules of events to take place

- Reviewing financial model indicators and obtaining project‐team inputs on contract needs and terms and conditions, insurance contracts, and other requirements

- Drafting contracts and sharing with appropriate stakeholders and confirming participation of lenders, equity investors, and host government

- Coordinating the development of a negotiation approach, plan, and process and ensuring that a correct financial model evaluation of contract new terms and conditions is performed in real time and results related back to the legal team

- Negotiating contract terms, conditions, and deliverables with milestones on the scope of the project—pricing, budgets, performance specifications, contract language and compliance clauses, financial reporting requirements, construction costs and drawdown schedule, financing documents, approvals, and financial close

- Creating a contract performance monitoring and control plan, overseeing project completion acceptance, incorporating change orders and resolving disputes, and performing compliance audits

9.3 COMMON PROJECT FINANCE CONTRACTS

The nature of project finance necessitates that contractual agreements form the basis of limited‐recourse financing upon which funding for the project is raised. Some of the project contracts are developed or sourced from the sponsor group while others originate from the host government's ceding authority, debt and equity investors, and export credit agencies (ECAs), unilateral, and multilateral agencies. Many contracts are tailor‐made to fit specific project needs and peculiarities, but our interest is on common project finance contracts which are the pillars supporting financing structures and include:

- The shareholder agreement, between the sponsor(s) and the project company, defines the terms of participation and ownership interest in the project, the rights and obligations, and the roles and responsibilities of the signatories. Usually, this contractual agreement is preceded by a separate sponsor partnership agreement specifying their initial and subsequent equity and debt investments in the project company.

- The concession agreement, also known as the implementation agreement, is a contract between the government and the project company that grants it the right to build and operate the project. It states the concession period, project company roles and responsibilities, eventual transfer of ownership, and project performance. Concession agreements include licensing, joint‐venture contracts, production‐sharing agreements, build, operate, and transfer of ownership (BOT) and public–private partnership (PPP) agreements, and offtake agreements. Concession agreements comply with host country laws and regulations and these contractual agreements usually include:

- The objectives, expectations, and support to the project by the host government

- Completion and termination dates

- The obligations of the concessionaire

- Direct lender agreements with the host government

- Security rights in the project company

- Force majeure clauses

- Liquidated damages and dispute resolution

- Changes in law and waiver of sovereign immunity

- The construction agreement—one of the key contracts—spells out the scope of the project, the terms and conditions of a fixed price, date‐certain turnkey engineering, procurement, and construction (EPC) contract, and the responsibilities of the contractor and the other project stakeholders. It covers items such as contractor responsibility for design flaws, extensions, and tests to determine completion of construction, payment procedures, and price changes. It also deals with issues such as contractor performance bond, performance guarantees, force majeure, and liquidated damages in the event of construction delays, security retainers, and dispute resolution measures.

- The intercreditor agreement is a contractual agreement between project lenders that defines their position relative to each other and the project company, and what happens when problems arise, such as bankruptcy or default. It also spells out their lien positions and security interests and the rights and obligations of the parties involved and may include buy out provisions giving a lender the option to buy another lender's debt.

- The sponsor guarantees is a form of credit support normally required by project senior lenders to reduce their risk in the project along with providing additional equity funding and cash infusions to handle cash flow shortfalls, secured interests over the project company's assets, guarantees related to project performance, and insurance against project risks

- The insurance contracts can vary according to individual project risks and have a significant impact on risk mitigation and project negotiations and are covered in more detail in Chapter 10. Insurance contracts may include the following:

- Transportation insurance of materials and equipment to the project site

- Insurance of project assets before, during, and after construction

- Construction and erection of all‐risk insurance that covers project assets and operations during construction

- Third‐party liability insurance that provides third‐party claims' coverage against omissions of the project company, contractors and subcontractors during construction and operation

- Consequential loss insurance for startup delays and business interruption

- Political risk insurance that includes partial risk guarantees, credit guarantees, and ECA or a multilateral agency guarantees

Political risk insurance provides coverage for revocation of permits and licenses, adverse regulatory changes, changes in tax and business laws, expropriation, currency inconvertibility, political violence and war, breach of contract, disruption of access to project company facilities, and asset transfer risks.

- The hedging contracts are financial instrument contracts used in project finance to minimize interest rate and exchange rate risk with swaps when the parties agree to exchange floating rate to fixed rate loans and floating exchange rates to fixed exchange rates.

- The loan agreement is an agreement between the project company and the lenders that provides loans for the project. The main parts of loan agreements include:

- The terms of the loan disbursement and repayment terms

- Conditions precedent

- Positive and negative covenants

- Representations and warrantees

- Remedies in the event of default

Additional project finance documentation involves an agreement on waterfall accounts, such as proceeds accounts, operating accounts, major maintenance reserve account, and debt payment and debt service accounts (Khan and Parra, 2003).

- The equity support agreement, where the lenders shift completion and abandonment risks to the project sponsors by requiring equity commitments in the 20–40% range and in some cases even higher.

- The capital injection agreement deals with a future sponsor's working capital contributions to cover cost overruns.

- The offtake agreement is contract for the entire concession period that specifies the amounts the offtaker will purchase at a specific price adjusted for inflation. There are several types of offtake agreements for specific projects and financing requirements, the common ones being:

- Take or pay contracts where the purchaser pays for the project company's output even if they do not take it

- Take and pay contracts where the purchaser takes the project company's output and pays for it when the project company provides that output

From the project company and the lenders' perspective, the take‐or‐pay offtake contract is more advantageous because the project company's revenue is independent from the production of output. Other offtake agreements include:

- Contracts for differences, when the project output is sold in the open market but the offtaker pays if the price goes below the agreed level and vice versa if the price goes above the agreed level

- Long‐term sales contracts of the project company's output

- Throughput contracts used in pipeline projects where the user commits to carry at least a certain volume of a product and pays a minimum price

- Input processing contracts used in waste incineration projects and sewage plants to agree to certain levels of inputs

- The supplier agreement is a contract for the duration of the concession period between the project company and the supplier of the key production inputs and it is intended to ensure uninterrupted supply of key production inputs to the project company to meet its output requirements. It specifies the duration of the contract, conditions for price changes, and force majeure clauses. The supplier agreements in project finance are of the supply or pay, or put or pay type under which the supplier pays the entire cost of procuring alternative supply.

- The operations and maintenance agreement defines the roles and responsibilities, the length of the agreement, performance expectations, and payments to the O&M company. This contract also includes incentives and penalties for the O&M company for meeting performance expectations.

Many of the risks associated with project finance deals are mitigated through the contracts mentioned above. However, the risks the debt investors bear beyond those contracts are mitigated with various project finance agreements, such as:

- Each separate facility agreement, that is every debt and equity agreement entered to

- The accounts agreement

- Each security agreement

- The equity support agreement

- Each direct agreement, i.e., every lender's direct agreement with the host government

- The drawdown request schedule

- Each hedging agreement

In addition to the main project contracts, there are other contractual agreements and project documentation developed as part of the legal team's effort. They include ceding‐authority collateral agreements, project‐company performance bonds, collateral guarantees, bond and private placement financing documentation, and the project prospectus or information memorandum. Notice however, that there are a number of risks that cannot be mitigated through contracts and agreements such as misrepresentations, rigged procurement processes, corruption, and many others.

An important project finance document that is based on the feasibility study and the due diligence reports is the project prospectus or the information memorandum, which is prepared by the project team led by the legal group to market the project to potential debt and equity investors. It is a summary report of the project feasibility analyses and evaluations, the findings of the due diligence, and the project company's business plan to demonstrate the profitable value creation of the project.

9.4 CHALLENGES OF PROJECT FINANCE CONTRACTS

Some challenges of project finance contracts result in contracts that cannot prevent project failures and are caused by the following factors:

- Lack of actual data from reliable sources, incorrect assumptions and methods used in cost and revenue forecasts and project evaluations

- The feasibility study and due diligence reports leave project aspects partly investigated or reported incorrectly

- Lack of skills and competencies in structuring effective project proposals and presenting convincingly analyses and evaluations

- Unclear corporate strategy driving confused project objectives that translate into weak contracts, especially if the legal and financing processes are not properly aligned

- Insufficient resources allocated to provide input and support in drafting project documents and contracts and assessing negotiations feedback

- Time pressures resulting in ineffective contract reviews, merging of all contracts in a single package, and auditing and managing of contracts

- Credit‐impaired project stakeholder contract provisions for the currency governing the project transaction

- Security agreements involving parties in different legal jurisdictions and disagreements among project stakeholders as to which country's courts should have jurisdiction and which country's laws should apply

- Enforceability of force majeure clauses for project nonperformance

Additional project finance contract challenges are presented by the following individual factors and combinations thereof:

- Contractual misunderstandings due to unclear contract provisions for dispute resolution

- Insufficient front‐end research and planning and inadequate contract development process

- Complexity of multiparty, multifaceted contracts and multiparty reviews and approvals

- Coordination issues between the legal team, the project team, and other project stakeholders' processes and deliverables

- Errors related to multiple iterations of drafting, revising, reviewing, revising, and so on

- Lengthy contract negotiations and renegotiations compounded by order changes, and schedule slippages

- Lack of sufficient experience of project stakeholders in project finance contracts and, occasionally, lack of qualifications to enter into contracts

- Language and cultural barriers and approach to negotiations focused on maximizing sponsor or host government benefits from the project at the expense of other stakeholders

- Incomplete and unbalanced agreements, unconfirmed evaluations and unchecked assumptions, and faulty financial assessments entering into defective formal contracts

- Contract enforceability issues in developing countries, contract failures, and inability to get remedies

- Unmitigated risks passed into contracts due to weak third‐party guarantees and insurance coverage

- Reactive risk management and undue reliance on contracts to mitigate risks without proper attention to project economics and stakeholder qualifications, skills, and ability to manage to contractual requirements

- Ethical issues and corrupt behavior that can never be managed effectively through contracts, but which must be dealt with at the early project phases

9.5 PROJECT CONTRACT SUCCESS FACTORS

Successful project financing relies on sound and effective contracts that are characterized by factors such as:

- Clearly stated and reasonable project objectives and customer expectations managed to reasonable levels

- Well‐defined project scope and clarity of what needs to be done and clarity of participant obligations, roles, and responsibilities

- Early participation of the PFO and the project team and all around, unimpeded communication, cooperation, coordination, and collaboration (4Cs) characterizing the contract development process, and sound vision and contract objectives

- The prerequisites of drafting effective project contracts are satisfied

- Early involvement of the PFO in contract preparation, structuring, and ensuring 360‐degree 4Cs

- Comprehensive contract planning, negotiation process, and assessment of negotiation results by the financial model

- Balance of participant interests using unambiguous language and fair, balanced, and cost‐benefit based risk allocation

- Real commitment of the contract parties to project success throughout its lifecycle

- Skilled and highly qualified legal staff and project team managers assigned to support the drafting of legal documents

- Independent and critical review and evaluation of contracts by external legal experts

- Creation of a project contract management system for contract administration, auditing, and control