SOLUTIONS

Chapter 1

Knowledge check solutions

-

- Correct. The Securities Act of 1933 requires an issuer offering securities to the public in interstate commerce or through the mail, unless specifically exempted, to file a registration statement with the SEC containing financial and other information about the issuer and the offering.

- Incorrect. The Securities Exchange Act of 1934 requires companies to file annual and other periodic reports to keep current the information contained in the original registration filing.

- Incorrect. The Securities Exchange Act of 1934 is primarily concerned with the trading and ongoing reporting related to registered securities.

- Incorrect. The purpose of the Securities Act of 1933 is not to limit the liability of entities offering securities for sale to the public, but instead requires an issuer offering securities to the public in interstate commerce or through the mail, unless specifically exempted, to file a registration statement with the SEC containing financial and other information about the issuer and the offering.

-

- Correct. The Securities Act prohibits fraudulent practices in the sale of securities and requires the dissemination of financial and other information to prospective investors.

- Incorrect. Registration under the 1934 Act is required for companies that become subject to the reporting requirements of the SEC other than by an initial sale of securities to the public.

- Incorrect. The Private Securities Litigation Reform Act governs private lawsuits filed under the federal securities laws and prevents abusive practices by class action lawsuit plaintiffs.

- Incorrect. The Securities Act, not the FAST Act, prohibits fraudulent practices in the sale of securities and requires the dissemination of financial and other information to prospective investors.

-

- Correct. Under Section 406 of the Public Company Accounting Reform Act of 2002, the SEC is required to issue rules requiring public companies to disclose whether or not, and if not, why not, the company has adopted a code of ethics for its senior financial officers.

- Incorrect. Under the Public Company Accounting Reform Act of 2002, public accounting firms that audit public companies must register with the PCAOB, not the securities exchanges.

- Incorrect. The Public Company Accounting Reform Act of 2002 requires that a company’s audit committee to the board of directors be responsible for appointing, compensating, and evaluating the performance of independent auditors.

- Incorrect. Private companies are not required to register with the PCAOB. Under Section 406 of the Public Company Accounting Reform Act of 2002, the SEC is required to issue rules requiring public companies to disclose whether or not, and if not, why not, the company has adopted a code of ethics for its senior financial officers.

-

- Correct. The JOBS Act created a new category of filers called emerging growth companies, which are entitled to certain reporting relief.

- Incorrect. The Dodd‐Frank Act immediately instituted credit rating agency consent requirements by repealing Securities Act Rule 436(g).

- Incorrect. The Dodd‐Frank Act requires the SEC to adopt pay‐for‐performance and pay ratio disclosures.

- Incorrect. The JOBS Act does not require participation in crowdfunding. The JOBS Act created a new category of filers called emerging growth companies, which are entitled to certain reporting relief.

-

- Correct. Section 13 of the Exchange Act requires every issuer of a security registered pursuant to Section 12 of the Exchange Act to file periodic reports with the SEC.

- Incorrect. The Accounting Reform Act of 2002 requires public accounting firms that audit public companies to register with the PCAOB.

- Incorrect. The AICPA is an organization of the public accounting profession, and issuers are not required to register with the AICPA.

- Incorrect. IFAC is an international accounting organization.

-

- Incorrect. The Office of Administrative Law Judges hears cases presented by the Division of Enforcement and other divisions.

- Correct. The Office of the Chief Accountant has the final authority, subject to appeal to the SEC, on accounting issues in registrant filings and may be consulted directly on significant or controversial accounting issues.

- Incorrect. Such an office does not exist at the SEC. Instead, there is an Office of Investor Education and Assistance, which serves individual investors, not auditors, and management teams of registrants.

- Incorrect. The Division of Trading and Markets regulates securities exchanges, national securities associations, and broker‐dealers. It administers the statistical functions.

-

- Incorrect. The Division of Enforcement supervises enforcement activities under the statutes administered by the SEC.

- Correct. The Division of Corporation Finance’s principal responsibility is to ensure that financial information included in SEC filings is in compliance with the rules and regulations of the SEC.

- Incorrect. The Division of Risk, Strategy and Financial Innovation assists the SEC with long‐term strategic analysis and identifying trends and innovations in financial markets.

- Incorrect. The Division of Investment Management administered the Investment Company Act of 1940, and the Investment Advisers Act of 1940. It investigates and inspects broker‐dealers and deals with problems of the distribution methods, services, and reporting standards of investment firms.

-

- Incorrect. Regulation S‐X governs financial statement presentation and disclosure requirements.

- Incorrect. Regulation S‐K governs the nonfinancial information in filings with the SEC.

- Correct. Regulation S‐T governs the preparation and submission of electronic filings using the SEC’s Electronic Data Gathering and Retrieval (EDGAR) system.

- Incorrect. Regulation S‐Z does not exist.

-

- Correct. The PCAOB adopted existing AICPA auditing, attestation, quality control, ethics, and independence standards as interim professional auditing standards, which apply until the PCAOB revises the interim standards or issues new standards on the related topic.

- Incorrect. The SEC continues to recognize FASB pronouncements as being generally accepted for purposes of filings with the SEC.

- Incorrect. The SEC accepts financial statements in accordance with IFRS as issued by the IASB if an entity qualifies as a foreign private issuer. However, the SEC does not have oversight of the IASB.

- Incorrect. The PCAOB did not adopt nonattest standards from the AICPA. It adopted the existing AICPA auditing, attestation, quality control, ethics, and independence standards as interim professional auditing standards, which will apply until the PCAOB revises the interim standards or issues new standards on the related topic.

-

- Incorrect. Section 8 of the Exchange Act provides for audit requirements with respect to the financial statements of an issuer.

- Correct. Under Section 18 of the Exchange Act, a person who makes false and misleading statements in documents filed under the act is liable to any person who, relying on such statements, purchased or sold a security to his detriment.

- Incorrect. Section 903 is a section of SOX that extends potential jail sentences for mail and wire fraud to 20 years.

- Incorrect. Section 104 relates to the Accounting Reform Act requiring the PCAOB to conduct annual inspections of registered public accounting firms that regularly provide audit reports for more than 100 issuers, and to conduct triennial inspections for all other registered firms.

-

- Incorrect. The AICPA and peer review process covers audits under GAAS (those audits not covered by PCAOB standards).

- Correct. The PCAOB conducts annual inspections of registered public accounting firms that provide audit reports for more than 100 issuers and conducts triennial inspections for all other registered firms.

- Incorrect. The CAQ guides and supports the public company auditing profession.

- Incorrect. The IASB is the designated accounting standard‐setter for IFRS.

-

- Incorrect. Section 402 of the Accounting Reform Act of 2002 makes it illegal for companies to extend credit to its directors and executive officers.

- Correct. The Foreign Corrupt Practices Act deals with (1) payments to foreign officials and (2) internal accounting control.

- Incorrect. The Foreign Corrupt Practices Act makes it illegal to offer anything of value to any major foreign official, foreign political party, and so on, in order to influence the enactment of a law or public policy decision or to obtain a government contract. Payments to minor employees of foreign governments whose duties are ministerial or clerical in nature are allowed as long as they are not falsely concealed on the corporate books and records.

- Incorrect. The Foreign Corrupts Practices Act does not require that an entity adopt a system of internal control in accordance with COSO. It deals with (1) payments to foreign officials, and (2) internal accounting control.

-

- Incorrect. Although the 2013 framework broadens the application of internal control by organizations in addressing reporting as well as operational and compliance objectives, it does not provide a robust disclosure framework for issuers’ periodic reports filed with the SEC.

- Incorrect. The 2013 framework was not issued by the PCAOB, nor does it communicate the PCAOB’s desire for all issuers to obtain an audit of internal controls over financial reporting.

- Correct. The 2013 framework clarifies the requirements for determining what constitutes effective internal control over financial reporting.

- Incorrect. The 2013 framework did not supersede Enterprise Risk Management– Integrated Framework.

Chapter 2

Review question solutions

-

- d.

- c.

- b.

- a.

- In a final prospectus filed with the SEC under Rule 424(b), generally within two business days of the determination of that price.

- For established companies, usually one day. For relatively unknown or for early‐stage companies, sometimes as long as nine months.

- Examples include the following:

Amazon.com, Inc.

Apple Inc.

eBay, Inc.

Google

Intel Corporation

Microsoft Corporation

Knowledge check solutions

-

- Correct. A privately held company may first offer its securities to the public through an IPO.

- Incorrect. A primary offering refers to offerings of additional securities by publicly held companies.

- Incorrect. A secondary offering refers to the sale of additional securities by selling stockholders of previously issued but unregistered securities by publicly held companies.

- Incorrect. A reverse merger refers to the issuance of stock by an existing public company (generally a public shell company) to acquire a private operating company. The former stockholders of the private operating company own a controlling interest in the public company after the transaction.

-

- Incorrect. The filing of annual reports, quarterly reports, and other reports with the SEC represents a considerable burden in terms of time and effort and also makes available to the public information that company management might prefer to be kept private.

- Correct. Going public increases an owner’s liquidity (subject to the SEC’s limitations on insider sales).

- Incorrect. The filing requirements of a public company make information available to the public, including competitors, which company management may prefer to be kept private.

- Incorrect. The Sarbanes‐Oxley Act established increased corporate governance and disclosure requirements and severe penalties for companies and their directors and officers for noncompliance with the securities laws. An owner of a company that goes public usually continues as an officer or member of the board of directors of the company after it goes public and is exposed to increased responsibility and scrutiny (and corresponding liability).

-

- Correct. The underwriting agreement includes all matters relevant to the issue of the securities and sets forth the responsibilities of each party.

- Incorrect. The comfort letter, prepared by the company’s auditors, gives the underwriters assurance with respect to the financial data contained in the registration statement that are not covered by the accountant’s report.

- Incorrect. The registration statement includes up to three years of audited financial statements of the company. The financial statements reflect the historical operations and financial position of the company.

- Incorrect. The registration statement is a disclosure document filed with the SEC, which contains required information about the securities being offered and the issuing company’s business and management.

-

- Incorrect. In an all‐or‐none arrangement, if the underwriters do not completely sell all shares, the shares are canceled and the funds returned to subscribers.

- Incorrect. In a best efforts offering, the underwriters agree to use their “best efforts” to sell the securities of the company. As a result, part of the issue may not be sold.

- Incorrect. In a minimum or maximum offering, if a minimum number of shares is not sold before the offering period expires, the offering is canceled and funds are returned to the potential investors.

- Correct. In a firm commitment, the underwriter agrees to buy the entire block of securities and resells it to the public at the underwriters’ own risk. If the underwriters cannot sell part of the securities, they must hold the remaining shares for their own account.

-

- Incorrect. Form S‐4 is the form to be used for securities to be issued in certain business combinations.

- Incorrect. Form S‐11 is the form to be used by a real estate company to register securities.

- Correct. Form S‐1 is used to register securities when no other form is specifically prescribed.

- Incorrect. Form F‐1 may be used by a foreign private issuer.

-

- Incorrect. Rule 134 allows the publication of a statement to generate interest for the offering after the filing of the registration statement. This statement may include strictly defined limited information.

- Incorrect. A “tombstone” ad is an ad to sell securities. Rule 134 strictly regulates its display and contents.

- Correct. A “red herring” is a preliminary prospectus. The term arises because the legend identifying the prospectus as preliminary was originally required to be printed in red ink on the cover.

- Incorrect. A summary prospectus is a shortened version of a prospectus usually published in a newspaper, magazine, or other publication.

Chapter 3

Review question solutions

Discussion topics

- Smaller reporting companies can elect to comply with all, some, or none of the scaled financial and nonfinancial disclosures in Regulations S‐K and S‐X on a quarterly basis in their periodic reports and registration statements. The nonfinancial disclosure rules for smaller reporting companies are contained within Regulation S‐K; a chart in Regulation S‐K Item 10(f) outlines the S‐K Items that have scaled disclosure options for smaller reporting companies. The scaled financial statement disclosures available to smaller reporting companies are found in Regulation S‐X Article 8.

To the extent that the smaller reporting company scaled item requirement is more rigorous than the same larger company item requirement, smaller reporting companies must comply with the smaller reporting company item requirement. Currently, Item 404 of Regulation S‐K (transactions with related persons) presents the only instance where the scaled requirements could be more rigorous than the larger company standard.

In determining how much disclosure to provide, companies should consider the following:

- The benefit to investors of providing full S‐K and S‐X disclosure may outweigh the cost savings of providing scaled disclosure.

- If, in subsequent years, a company no longer qualifies as a smaller reporting company, it will have to provide the full disclosures, including prior year comparisons. For this reason, the data needed to comply with the full disclosure rules should continue to be collected and kept on file.

- Because the rules do not permit “cherry‐picking” (that is, providing more disclosure only in periods when expanded disclosure is favorable), companies need to consider whether foregoing a particular disclosure in one year will raise questions if the disclosure is then provided in a subsequent year.

- As reflected in SEC comment letters, registrant restatements, and enforcement actions, revenue recognition has consistently been a focus of the SEC staff. The staff’s rules and views on revenue recognition are included in Regulations S‐X and S‐K, the codification of Financial Reporting Releases, and Staff Accounting Bulletins. The SEC has consistently encouraged registrants to provide clear and robust disclosures that provide investors with an understanding of the type, nature, and terms of significant revenue transactions and how the accounting literature is applied to those transactions. The following is an overview of some of the more significant SEC rules, regulations, and staff guidance related to revenue recognition:

Rule 5‐03 of Regulation S‐X requires registrants to state separately on the face of its income statement (a) net sales of tangible products, (b) operating revenues of public utilities, (c) income from rentals, (d) revenues from services, and (e) other revenues. Revenues of any class that are less than 10% of total revenue may be combined with other classes. Cost of sales should be separated in a similar manner.

SAB No. 13, Revenue Recognition, does not amend any of the existing issued accounting guidance but instead provides the staff’s interpretations on the application of those revenue recognition rules, including the general premise that revenue should not be recognized until realized or realizable and earned. The SAB requires that registrants disclose its revenue recognition policy, noting that if a registrant has different policies for different types of revenue transactions, the policy for each material type of transaction should be disclosed. The staff expects registrants to discuss the significant provisions of revenue transactions such as discounts, return policies, continuing obligations, and warranties and how they affect revenue recognition. In its 2003 Fortune 500 report, in which the staff reviewed all of the annual reports filed by Fortune 500 companies, the SEC noted that revenue recognition policy disclosure was an area in which improvement was needed. The report noted trends in certain industries in which revenue recognition policies were not adequate explained, such as the following:

- Software. Expanded disclosures for software and multiple element arrangements.

- Capital goods. Improved disclosures for deferred revenue, return and price protection features, requirements for installation of equipment.

- Energy. Improved disclosures for material terms of contracts.

- Retail. Improved disclosures for product returns, discounts, and rebates.

Item 303 of Regulation S‐K provides the requirements for management’s discussion and analysis (MD&A), which includes the discussion on the liquidity, capital resources, results of operations, and other information necessary to understand the registrant’s financial condition, change in financial condition, and results of operations. The evaluation of the companies’ operations and changes in revenues is critical to this analysis. Financial Reporting Release 36 (FRR 36) provides further insight into the staff’s expectations of MD&A, noting that the content should “give investors an opportunity to look at the registrant through the eyes of management by providing a historical and prospective analysis of the registrant’s financial condition and results of operations with a particular emphasis on the registrant’s prospects for the future.” Management should not simply recite the information provided on the financial statements, but should provide meaningful analysis of why the results of operations changed and expected future trends.

Examples of revenue recognition disclosures based on the principles of FRR 36 include the following:

- Shipments of product at the end of a reporting period that significantly decrease customer backlog and that reasonably might be expected to result in lower shipments and revenue in the next period

- Granting of extended payment terms that will result in a longer collection period for accounts receivable and slower cash flows from operations

- Changing trends in shipments into, and sales from, a sales channel or separate class of customer that could be expected to have a significant effect on future sales

- An increasing trend toward sales to a different class of customer that might lower gross profit margin

- Seasonal trends or variations in sales

- Accounting and Auditing Enforcement Releases (AAER) provide background on enforcement actions brought by the SEC and illustrate the variety of activities that constitute financial fraud. Very often, revenue recognition manipulation is at the center of fraud. Regulation S‐X is a uniform set of financial statement disclosure requirements that govern the form and content of the financial statements included in SEC filings, including what financial statements must be presented and for what periods. Regulation S‐X, in general, is consistent with GAAP but does contain certain incremental disclosures items that are not required by GAAP. Examples of disclosures that are incremental to GAAP include disclosures related to income taxes, restriction of dividend payments, inventories, and conditionally redeemable preferred stock. The provisions of Regulation S‐X, although prescriptive, are intended to be applied based on the facts and circumstances of the registrant, including consideration of materiality. Regulation S‐X is organized in 12 articles and rules, including Article 8 for smaller reporting companies.

Regulation S‐K contains the disclosure requirements for the textual or nonfinancial statement information included in SEC filings. Items such as the description of business, management’s discussion and analysis of financial condition, and results of operations and market risk disclosures are governed by Regulation S‐K. Regulation S‐K also includes the SEC’s policy on projections, rules on incorporation by reference, and use of non‐GAAP financial measures in SEC filings. Regulation S‐K is organized with subparts and items. In cases where smaller reporting companies are not required to provide disclosures required of larger companies (for example, the disclosure required under Item 305 on quantitative and qualitative disclosures on market risk) a paragraph in the relevant item of Regulation S‐K has been included indicating that smaller reporting companies are not required to respond to the Item.

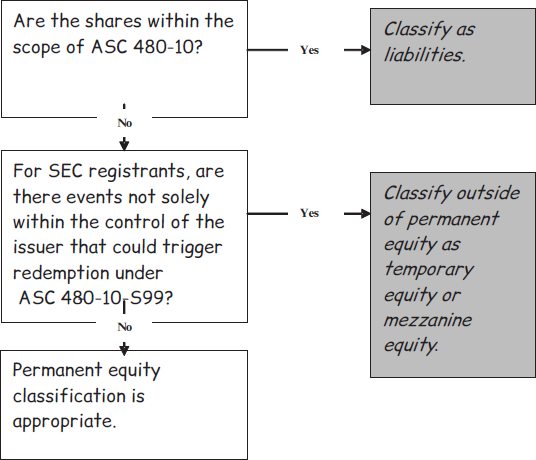

- Under GAAP, instruments that have redemption features must be considered under the guidance of FASB ASC 480‐10. FASB ASC 480‐10 requires that freestanding instruments be accounted for as liabilities if they meet any of the following conditions: (a) mandatorily redeemable, (b) obligate the issuer to buy back some of its shares in exchange for cash or other assets, or (c) obligations that must or may be settled with a variable number of shares the monetary value of which is based solely or predominantly on a fixed monetary amount or a variable such as a market index or a variable inversely related to the value of the issuer’s shares. The SEC’s rules for redeemable securities were written before FASB ASC 480‐10, but if FASB ASC 480‐10 requires the redeemable security to be classified as a liability, that guidance takes precedence over the SEC’s guidance for presentation and disclosure.

For SEC registrants, instruments that fall outside the scope of FASB ASC 480‐10 must be assessed to determine whether they should be classified as permanent or temporary equity. Rule 5‐02.28 of Regulation S‐X defines redeemable preferred stock as any class of stock that the issuer undertakes to redeem at a fixed or determinable price on a fixed or determinable date or dates, (b) is redeemable at the option of the holder, or (c) has conditions for redemption that are not solely within the control of the issuer, such as provisions for redemption out of future earnings (the SEC staff believes that all of the events that could trigger redemption should be evaluated separately and that the possibility that any triggering event that is not solely within the control of the issuer could occur — without regard to probability — would fall into the category of redeemable preferred). Redeemable preferred stock or another type of stock with the same characteristics may be not included under the general heading of “stockholders’ equity” or combined with other stockholders’ equity captions, such as additional paid‐in capital and retained earnings.

The rule also requires registrants to provide a general description of each issue of redeemable preferred stock, including its redemption terms, the combined aggregate amounts of expected redemption requirements each year for the next five years, changes in each issue for each period for which an income statement is required, and other significant features similar to those for long‐term debt.

The following flowchart illustrates the decision process:

Financial statement requirements

- No. Because the registration statement is to be filed before 90 days after its year‐end, the company must look to the criteria in Regulation S‐X Rule 3‐01(c) to determine whether it can include its third quarter 20XC interim financials instead of its 20XD audited financial statements in the filing. Although Company A meets the first and third tests of Rule 3‐01(c), it does not meet the second (“For the most recent fiscal year for which audited financial statements are not yet available the registrant reasonably and in good faith expects to report income after taxes but before extraordinary items and the cumulative effect of accounting changes.”). Had Company A met all of the criteria in S‐X Rule 3‐10(c), it could have filed its registration statement until March 31, 20XE, using audited financial statements for 20XA, 20XB, and 20XC, and unaudited financial statements for the nine months ended September 30, 20XC and 20XD.

- No, the answer would not be the same. If Company A was a large accelerated filer and reasonably and in good faith expected to report income before extraordinary items and the cumulative effect of accounting changes in 20XD, it may file its registration statement within 60 days after its December 31, 20XD, year‐end (that is, until March 1, 20XE), using audited financial statements for 20XA, 20XB, and 20XC, and unaudited financial statements for the nine months ended September 30, 20XC and 20XD.

- Regulation S‐X Rule 3‐12 covers the age of financial statements presented at the effective date of a registration statement.

- Regulation S‐X Article 12 governs the form and content of financial statement schedules.

- For annual filings, Regulation S‐X Rule 3‐01 requires audited balance sheets to be provided as of the end of each of the two most recent fiscal years. Rule 3‐02 requires audited statements of income (and comprehensive income) and cash flows for each of the three fiscal years preceding the date of the most recent audited balance sheet to be provided. Under Rule 3‐04, an analysis of the changes in stockholders’ equity must be presented for each period for which an income statement is required to be filed.

If the issuer is a smaller reporting company, the smaller reporting company rules apply and the number of years required is reduced for audited statements of income (and comprehensive income) and cash flows to two years. Under Rule 3‐04, an analysis of the changes in stockholders’ equity must be presented for each period for which an income statement is required to be filed, and therefore this requirement is also for two years.

For quarterly periodic reports, Regulation S‐X Rule 10‐01 requires an interim balance sheet as of the end of the most recent fiscal quarter and a balance sheet as of the end of the preceding fiscal year to be provided. In addition, interim statements of income for the most recent fiscal quarter for the period between the end of the preceding fiscal year and the end of the most recent fiscal quarter, and for the corresponding periods of the preceding fiscal year must be provided. Interim statements of cash flows for the period between the end of the preceding fiscal year and the end of the most recent fiscal quarter, and for the corresponding period of the preceding fiscal year must also be included. All such financial statements may be unaudited.

Financial statement disclosures

- Presentation of separate audited financial statements for the investee is required under Rule 3‐09 of Regulation S‐X. Summarized financial statement information that would normally be required under Rule 4‐08(g) is not required if separate financial statements are provided and they cover the same periods as those for which summarized financial information would be provided. If other equity investees exist (for which separate financial statements were not provided), summarized financial information for all equity investees in the aggregate generally would be required.

Case study solutions—Rule 3‐05, Financial Statement Requirements

Case 3‐1

It would be unusual for a company to sign a letter of intent to make a significant acquisition without first getting approval from the board of directors to proceed with the transaction and without the expectation that the acquisition would be completed. Although the specific facts and circumstances would need to be considered, the acquisition would usually be considered probable.

Case 3‐2

Registrant must provide three years of audited Company T financial statements at the time the registration statement is filed (that is, registrant cannot wait until 75 days after the acquisition was completed, as is permitted when filing acquiree financial statements with the Form 8‐K to report the acquisition) because the significance of Company T exceeds 50% (Rule 3‐05(b)(4)(i)).

In contrast to a Form 8‐K filing, a registration statement involves a transactional filing. In a transactional filing, the age of a target’s financial statements must comply with Rule 3‐01 of Regulation S‐X. The determination of whether a target’s financial statements must be updated on the 46th or the 90th day (75th day if accelerated or 60th day if large accelerated filer) after year‐ end is based on whether the registrant (not the target) meets the conditions in Rule 3‐01(c). If the registrant meets the conditions in Rule 3‐01(c), then financial statements of the same age as what would be required in the Form 8‐K to report the acquisition (December 31, 2016, 2015, and 2014 audited and September 30, 2017, and 2016 unaudited) would be required. If the registrant does not meet the conditions in Rule 3‐01(c) (or it meets those conditions but it amends the registration statement or the registration statement is to be declared effective on or after the 90th day [or 75th or 60th day for accelerated and large accelerated filer, respectively] after December 31, 2017), then the registrant would have to include audited December 31, 2017, Company T financial statements in the registration statement.

Case 3‐3

In general, target financial statements must be updated in a transactional filing if they are over 134 days old at the filing or effective date. The SEC staff permits gaps in reporting, as long as they are less than a complete quarter. If the registrant filed a Form 8‐K at the time of the acquisition that included Company T financial statements for the year ended December 31, 2016 (audited), and the 9 months ended September 30, 2017, and 2016 (unaudited), then the gap in reporting (from September 30, 2017, to the February 22, 2018, acquisition date) would exceed one quarter. Therefore, updating of the Company T financial statements would be required. Further, because the registration statement is being filed more than 45/90 (45/75 for accelerated or 45/60 for large accelerated filer) days after Company T’s year‐end, audited December 31, 2017, Company T financial statements are required.

This example illustrates that financial statements that are sufficient for a current Form 8‐K filing may not be sufficient for a subsequent transactional filing. Therefore, when a company acquires a business shortly after the acquired business’ year‐end and the company plans to file a registration statement in the future, it is often desirable to audit the most recent year for purposes of the Form 8‐K filing (even though not required) to avoid the need to do another audit later.

Case 3‐4

Rule 3‐06 permits a registrant to substitute audited financial statements for 9 months for financial statements for one 12‐month period. Because the significance exceeds 50%, 33 months of audited Company T financial statements must be provided (assuming a 9‐month period is substituted for one of the 3 required 12‐month periods). Although not specified in the rules, in practice the SEC staff accepts that a registrant is in substantial compliance with Rule 3‐05 if (1) the combined pre‐ and post‐acquisition audited periods presented equal the number of months of audited operating results required by Rule 3‐05, and (2) the period audited is continuous (that is, there must be no break in the audit coverage). Therefore, in this fact pattern, Company R could either (1) provide Company T audited financial statements for the years ended December 31, 2014, December 31, 2013, and December 31, 2012, and unaudited financial statements for the three months ended March 31, 2015 and 2014, or (2) provide Company T audited financial statements for the period from January 1, 2015 (or April 1, 2015), to May 15, 2015, and use this period plus the 31½ months of post‐acquisition audit coverage to meet the 33‐month audit requirement.

Knowledge check solutions

-

- Correct. After reviewing the general instructions of the form, the specific Regulation S‐K disclosure requirements applicable to the form should be reviewed.

- Incorrect. The instructions refer to the specific Regulations S‐K and S‐X items that are required for the form and will indicate which items can be incorporated by reference from the annual report to shareholders.

- Incorrect. A “no action” request is usually made by a registrant with respect to a proposal made by an eligible shareholder under Regulation 14a‐8, Shareholder Proposals. A “no action” letter granted by the SEC allows the SEC registrant to exclude the shareholder’s proposal from its proxy statement.

- Incorrect. Although SEC filing fees are required for some SEC filings, the fees are generally based on the aggregate offering amount and would not be the most logical next step after reviewing the form instructions.

-

- Incorrect. Regulation S‐T governs the electronic filing or submission of documents with the SEC.

- Incorrect. Regulation S‐K contains the disclosure requirements for the “textual” (nonfinancial statements) information in filings with the SEC.

- Correct. Regulation S‐X sets forth the form and content of and requirements for financial statements for SEC filings.

- Incorrect. Regulation FD requires that when an issuer discloses material nonpublic information to certain individuals or entities, the issuer must make public disclosure of that information.

-

- Incorrect. Article 7 contains financial statement and schedule instructions for insurance companies.

- Incorrect. Article 6 contains financial statement and schedule instructions for registered investment companies.

- Incorrect. Article 4 of Regulation S‐X outlines the rules regarding general notes to the financial statements.

- Correct. Article 5 contains instructions for commercial and industrial companies on the content and disclosure for the balance sheet and income statement as well as the requirements for financial statement schedules.

-

- Incorrect. Rule 2‐01 of Regulation S‐X contains rules related to the qualifications of accountants.

- Incorrect. Rule 2‐03 of Regulation S‐X provides the requirements on examination of financial statements by foreign government auditors.

- Correct. Rule 2‐02 of Regulation S‐X contains rules on the form and content of accountants’ reports that are to be included in SEC filings.

- Incorrect. Rule 2‐04 of Regulation S‐X provides the requirements on examination of financial statements of persons other than the registrant.

-

- Incorrect. When the other accountant plays a significant role in the audit, the other accountant should be registered with the PCAOB and conduct the audit in accordance with the PCAOB’s auditing standards; however, if the principal auditor does not refer to the other accountant in its report on the consolidated financial statements, a separate report of the other accountant is not required to be included in a filing with the SEC in accordance with Regulation S‐X Rule 2‐05.

- Correct. Regulation S‐X Rule 2‐05 requires that the other accountant’s report be included in the SEC filing when it is referred to in the principal accountant’s report.

- Incorrect. If the other accountant’s report is not referred to in the principal accountant’s report, it does not have to be included in the filing.

- Incorrect. If part of the examination of the financial statements is made by an independent accountant other than the principal accountant and the principal accountant elects to place reliance on the work of the other accountant and makes reference to that effect in his or her report, the separate report of the other accountant shall be filed (Regulation S‐X Rule 2‐05).

-

- Incorrect. The SEC generally will not accept audit opinions that are qualified for audit scope.

- Incorrect. Because GAAP requires assets to be stated not in excess of their net recoverable amount, such an explanatory paragraph would indicate a scope limitation. The SEC generally will not accept opinions that are qualified for scope or fairness of presentation, and would consider the filing incomplete.

- Incorrect. The SEC generally will not accept opinions that are qualified for fairness of presentation and would consider the filing incomplete.

- Correct. The SEC will accept a standard “going concern” explanatory paragraph if prepared in conformity with AS 2415, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern.

-

- Incorrect. Regulation S‐X Rule 4‐01 sets forth the rules for the general form and content of the financial statements.

- Correct. The additional requirements are set forth in Regulation S‐X Rules 4‐08(a) through (n). If the amounts involved are not material, disclosures may be omitted.

- Incorrect. Regulation S‐X Rule 3‐09 requires that registrants present separate financial statements for 50%‐or‐less owned equity method investees that are significant.

- Incorrect. Regulation S‐X Rule 3‐11 contains the financial statement requirements of inactive registrants.

-

- Incorrect. Regulation S‐X Rule 4‐08(g) requires summarized financial statement footnote information for equity method investees when any one of the significant subsidiary tests of Rule 1‐02(w) is met on an individual or aggregate basis for any fiscal year presented by the registrant.

- Correct. Summarized financial statement footnote information as to assets, liabilities, and results of operations for all of the registrant’s equity method investees (except those for that separate financial statements are provided pursuant to Rule 3‐09 of Regulation S‐X) is required when any one of the significant subsidiary tests of Rule 1‐02(w) is met on an individual or aggregate basis for all fiscal years presented by the registrant.

- Incorrect. Summarized financial statement footnote information is required when any one of the significant subsidiary tests of Rule 1‐02(w) is met on an individual or aggregate basis for any fiscal year presented by the registrant for all fiscal years presented by the registrant.

- Incorrect. Summarized financial statement footnote information for all of the registrant’s equity method investees (except those for which separate financial statements are provided pursuant to Rule 3‐09 of Regulation S‐X) is required when any one of the significant subsidiary tests of Rule 1‐02(w) is met on an individual or aggregate basis for all fiscal years presented by the registrant, and not for the investee that meets the significance threshold only.

-

- Incorrect. Rule 3‐10 of Regulation S‐X generally requires a guarantor of a registered security to file full financial statements or modified financial information, depending on the circumstances. Summarized financial information is not an alternative.

- Correct. If the conditions described in the question are met, Rule 3‐10 permits the parent company to include in its periodic reports a footnote to its financial statements that provides condensed consolidating financial information for the parent company, guarantor subsidiary, and all other subsidiaries combined.

- Incorrect. If the guarantor is 100% owned by the parent and the guarantee is full and unconditional, the parent company (registrant) is allowed to file in a footnote disclosure condensed consolidating financial information for the parent, subsidiary guarantor, and all other subsidiaries in accordance with Rule 3‐10. Separate financial statements of the guarantor subsidiary would be required only if they were not wholly owned and did not meet the “full and unconditional” criteria.

- Incorrect. Rule 3‐10 of Regulation S‐X generally requires a guarantor of a registered security to file full financial statements or modified financial information, depending on the circumstances. Summarized financial information is not an alternative.

-

- Correct. Schedule II must be filed in support of valuation and qualifying accounts included in each balance sheet, but not included in Schedule VI.

- Incorrect. Certain real estate companies file schedule IV in support of investments in mortgage loans on real estate.

- Incorrect. Condensed financial information of the registrant is filed on Schedule I.

- Incorrect. The Summary Compensation table is required by Item 402(c) of Regulation S‐ K and may be included under Item 11 of Part III of Form 10‐K or incorporated by reference from the definitive proxy or information statement (if filed no later than 120 days after the end of the fiscal year covered by Form 10‐K).

-

- Correct. Item 303 of Regulation S‐K sets forth the requirements for MD&A.

- Incorrect. Regulation S‐X sets forth the form and content of and requirements for financial statements for SEC filings.

- Incorrect. Regulation S‐B, which contained the financial and nonfinancial rules for small business issuers, was phased out and eliminated effective March 15, 2009. The rules for the new category of smaller reporting companies are now included within Regulations S‐K and S‐X.

- Incorrect. Regulation M‐A contains the disclosure requirements for merger and acquisition transactions and other extraordinary transactions.

-

- Incorrect. Regulation S‐X schedules are required in Form 10‐K.

- Correct. Although schedules are not required to be presented in Form S‐3, they are part of filings on that form because that form requires the Form 10‐K to be incorporated by reference.

- Incorrect. Regulation S‐X schedules are required in Form S‐4.

- Incorrect. Regulation S‐X schedules are required in Form S‐1.

-

- Correct. FRRs, or Financial Reporting Releases, are published to communicate significant amendments to Regulations S‐X and S‐K. They frequently provide guidelines and interpretations on the rules and related amendments.

- Incorrect. AAERs, or Accounting and Auditing Enforcement Releases, are issued to communicate enforcement actions brought by the SEC against companies and people who have violated the securities laws.

- Incorrect. SLBs, or Staff Legal Bulletins, reflect the views of the staff on SEC legal issues.

- Incorrect. SABs, or Staff Accounting Bulletins, reflect the SEC staff’s views on matters related to accounting and disclosure practices.

-

- Incorrect. The SEC staff’s views related to accounting and disclosure regarding discontinued operations are expressed in SAB Topic 5‐Z.

- Incorrect. The SEC staff’s views regarding disclosure of potential impact of accounting standards that have been issued but not yet adopted are expressed in SAB Topic 11M.

- Incorrect. The SEC staff’s views regarding accounting for revenue recognition are expressed in SAB Topic 13.

- Correct. SAB Topic 5DD expresses the SEC staff’s view that expected cash flows related to servicing a loan commitment should be included in the measurement of all written loan commitments that are accounted for at fair value.

-

- Correct. The staff believes that registrants should use a combination of two approaches, the “rollover” approach and the “iron curtain” approach for quantifying misstatements to evaluate materiality. The SEC refers to this combined approach as the “dual approach.”

- Incorrect. The rollover approach focuses only on the income statement and quantifies an error as the amount by which the current year income statement is misstated. The staff believes that in addition to this approach, registrants also need to apply the “iron curtain” method in evaluating misstatements for materiality, which focuses on the magnitude of the misstatement to the current balance sheet.

- Incorrect. The iron curtain approach focuses on the magnitude of the misstatement in the current balance sheet. The staff believes that in addition to this approach, registrants also need to apply the “rollover” approach in evaluating misstatements for materiality, which focuses on the magnitude of misstatement to the income statement.

- Incorrect. The staff believes that registrants should use a combination of two approaches, the “rollover” approach and the “iron curtain” approach for quantifying misstatements to evaluate materiality. The SEC refers to this combined approach as the “dual approach.”

Chapter 4

Review question solutions

- It is to minimize duplication of effort by facilitating the incorporation by reference of certain information from the annual report to shareholders and the proxy statement for the election of directors.

- Five years, as called for by Item 6, under Part II of Form 10‐K, concerning selected financial data. See Regulation S‐K, Item 301. (Certain schedules may require longer than five years, but they are not required for most companies.)

- D. All of the above. The general instructions to Form 10‐K permit the information required by Part I and II of 10‐K to be incorporated from the annual report to shareholders. Information required by Part III, such as Item 11. Executive compensation usually may be incorporated by reference from the registrant’s proxy statement so long as it is filed within 120 days of the fiscal year‐end.

- Generally, a major customer is one that represents 10% or more of revenues. The name of a major customer must be disclosed if the loss of the customer would have a material adverse effect on the registrant.

- A company must reissue a 302 certification if the amended filing contains financial statements.

- D. Cash dividends declared per share. Item 301 of Regulation S‐K requires registrants to include the following:

- Net sales or revenues

- Income (loss) from continuing operations and related earnings per share

- Total assets

- Long‐term obligations

- Cash dividends declared per share

Item 301 permits registrants to include other items that they believe would enhance an understanding of and would highlight other trends in their financial condition and results of operations.

- No, they may not. The SEC believes accountants have an obligation to withhold their report on the financial statements if a significant amount of nonpublic information is missing, and we have already determined that the loss of more than 10% of sales is deemed significant.

- Audited balance sheets as of the end of the most recent two fiscal years (20XC and 20XB), and audited statements of income, stockholders’ equity, and cash flows for the most recent three fiscal years (20XC, XB, and XA).

- It means management’s search for an auditor willing to support an accounting treatment intended to accomplish a registrant’s reporting objectives, even though that treatment might conflict with reliable reporting.

- For the principal executive officer, the principal financial officer, and the three other most highly compensated executive officers, total compensation must be disclosed in the Summary Compensation Table. The disclosures cover salary, bonus, stock options, restricted stock, pension benefits, deferred compensation, and all other compensation including perks. Grants of plan‐based awards are disclosed in the Grants of Plan‐Based Awards Table. Compensation policy and decisions are covered in the new principles‐based analysis: Compensation Disclosure and analysis. Details of the named executive officer compensation are included in the Outstanding Equity Awards at Fiscal Year‐End Table, Option Exercises and Stock Vested Table, Pension Benefits Table, Nonqualified Deferred Compensation Table, and narrative on potential payments upon termination or change in control.

- Item 401 of Regulation S‐X requires identification of certain significant employees if such individuals make or are expected to make significant contributions to the company’s business. Such individuals could include research scientists. Therefore, the professor should probably be included in Item 10, “Directors and Executive Officers of the Registrant.”

- The critical accounting policy disclosure should communicate uncertainties and how they might affect the financial statements. The discussion should provide insight into how the estimate was arrived at, including the assumptions that factored into the initial estimate, and how susceptible the estimate is to variability. It should include a discussion of how assumptions changed from the prior period, the reason for the change and resulting impact on the estimate, and factors that could cause the estimate to change in the future, including the potential magnitude of future changes.

- The SEC staff advised that the registrant should disclose the following in MD&A for a reporting unit with a material amount of goodwill that is at risk of failing step 1 of the impairment test in FASB ASC 350‐20‐35:

- The percentage by which fair value exceeded the carrying amount

- The amount of goodwill allocated to the reporting unit

- Key assumptions that drive fair value (for example, cost of capital)

- Any uncertainty or potential events that could have a negative effect should also be disclosed

Due to the interplay between assumptions, the SEC staff now believes that a sensitivity analysis focused on the impact of a change in only one assumption does not provide the most meaningful information.

If an issuer does not have any reporting units that are at risk of future material goodwill impairment, the staff recommends that it disclose that fact in MD&A.

Knowledge check solutions

-

- Correct. A large accelerated filer must have a public float of $700 million or more as of the end of its second fiscal quarter and meet the other tests included in the definition of accelerated filer.

- Incorrect. The public debt test is one of the tests for determining whether or not an issuer is a well‐known seasoned issuer (WKSI).

- Incorrect. The float is measured at the end of its most recently completed second fiscal quarter.

- Incorrect. The $1 billion float is not part of the measurement to determine large accelerated filer status.

-

- Correct. Large accelerated filers must file their Form 10‐Ks within 60 days.

- Incorrect. The SEC eliminated the final 60‐day phase‐in date for regular accelerated filers.

- Incorrect. Non‐accelerated filers have 90 days.

- Incorrect. 60 days is the deadline for large accelerated filers.

-

- Incorrect. The public float test performed within 60 days of the determination date applies to the determination of an issuer’s status as a WKSI.

- Correct. The test for determining accelerated filer and large accelerated filer status is performed at year‐end using an issuer’s public float as of the end of its second fiscal quarter.

- Incorrect. The public float test is measured at the most recently completed second fiscal quarter.

- Incorrect. The determination of accelerated filer status for the annual report to be filed is done at the end of the issuer’s fiscal year with the public float test measured as of the end of the second fiscal quarter.

-

- Correct. A large accelerated filer may begin filing as accelerated filer beginning with the annual report due in the same year in which the issuer’s public float dropped below $500 million as of the end of its second fiscal quarter.

- Incorrect. A drop in public float to below $50 million allows an issuer to move to non‐accelerated filer status.

- Incorrect. The public float measurement is performed as of the issuer’s second fiscal quarter.

- Incorrect. The determination is made at the end of a fiscal year that the issuer’s public float was less than $500 million as of the last business day of the its most recently completed second fiscal quarter.

-

- Correct. Each nonfinancial disclosure item is located in Regulation S‐K, and the scaled disclosure, if available, is noted in the S‐K item.

- Incorrect. Regulation S‐M does not exist. Regulation S‐K includes the scaled disclosure requirements for smaller reporting companies.

- Incorrect. Regulation S‐B no longer exists. The smaller reporting company nonfinancial disclosure requirements are included in Regulation S‐K.

- Incorrect. Regulation S‐X covers the form and content of and requirements for financial statements.

-

- Correct. If consolidated revenue does not exceed $50 million in any of the years, the materiality factor is 15% instead of 10%.

- Incorrect. Liquidity and capital resource disclosures are required under Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operation.

- Incorrect. The materiality threshold increases to 15% when revenues are below $50 million.

- Incorrect. Market for common equity is disclosed in Item 5, Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

-

- Incorrect. The Securities Offering Reform rules were adopted by the SEC and do not contain any provisions related to disclosure of tax shelter penalties.

- Correct. In Rev. Proc. 2005‐51, the IRS requires public companies to disclose in Form 10‐K any requirement to pay a monetary penalty for the failure to include on any tax return any information required to be disclosed with respect to certain “reportable” transactions.

- Incorrect. FASB ASC 740, Income Taxes, is a GAAP accounting standard. The Item 3 disclosures are required by the IRS.

- Incorrect. Regulation S‐X covers the form and content of and requirements for financial statements.

-

- Correct. The liquidity section of MD&A should include an analysis of material increases and decreases in working capital items to explain whether changes are due to growth or contraction, or changes in turnover.

- Incorrect. The results of operations section of MD&A generally includes a discussion of the reasons for material year‐to‐year changes in the amount of income statement line items or the historical relationship between income statement line items.

- Incorrect. Contractual obligations are typically disclosures about long‐term obligations.

- Incorrect. Critical accounting policies disclosures should communicate uncertainties and how they might affect the financial statements, not just repeat the accounting policies footnotes. The discussion should be about those estimates that are most critical and known uncertainties that are reasonably likely to materially affect future operating results.

-

- Correct. Item 7a of Form 10‐K (Quantitative and Qualitative Disclosures about Market Risk) requires a company to furnish the information required by Item 305 of Regulation S‐K, which includes the market risks for financial instruments entered into for trading purposes and for purposes other than trading.

- Incorrect. These disclosures are required by Regulation S‐K Item 503 and would generally be provided in a registration statement under “Risk Factors.”

- Incorrect. Registrants are encouraged, not required, to provide market risk disclosures regarding market risk sensitive instruments and transactions other than those specifically required by Item 305.

- Incorrect. Item 305 disclosures are not required in the financial statements. Also, the safe harbor from liability in private lawsuits for certain forward‐looking statements does not apply to financial statements, so there is a disincentive for including the Item 305 disclosures in the financial statements.

-

- Incorrect. Item 15 of Form 10‐K requires exhibits and financial statement schedules.

- Correct. Item 8 of Form 10‐K requires financial statements and the supplementary financial data required by Item 302 of Regulation S‐K.

- Incorrect. Item 10 of Form 10‐K requires information about directors, executives, and corporate governance.

- Incorrect. Item 9B of Form 10‐K requires information to be disclosed in a report on Form 8‐K during the fourth quarter of the year covered by the Form 10‐K, but not reported.

-

- Correct. The disclosures required by Item 9 (Changes in and Disagreements with Accountants on Accounting and Financial Disclosure) would alert the SEC to possible opinion shopping by a company.

- Incorrect. Item 11 of Form 10‐K requires disclosures about executive compensation.

- Incorrect. Item 8 of Form 10‐K concerns financial statement requirements and the supplementary quarterly data required by Item 302 of Regulation S‐K.

- Incorrect. Item 14 of Form 10‐K requires disclosures about principal accountant fees and services.

-

- Correct. All accelerated and large accelerated filers, regardless of whether they are domestic or foreign issuers, are required to have an auditor attestation of their ICFR.

- Incorrect. Accelerated filers were first subject to the internal control reporting requirements of Section 404 for fiscal years ending or after November 15, 2004. Non‐accelerated filers are permanently exempted from the auditor attestation on ICFR by the Dodd‐Frank Act and SEC rules.

- Incorrect. All public companies have been required to have management report on ICFR since fiscal years ending on or after December 15, 2007.

- Incorrect. Regardless of whether it is a domestic or foreign private issuer, a filer that qualifies for non‐accelerated filing status does not need to obtain an auditor attestation on its ICFR at the end of every fiscal year based on the permanent exemption provided by the Dodd‐Frank Act and SEC rules.

-

- Incorrect. The financial expert need not be a CPA.

- Incorrect. The financial expert does not have to register with the PCAOB.

- Incorrect. The years of experience the financial expert has is not required.

- Correct. The requirement to disclose information regarding the financial expert and the person’s independence was a result of rulemaking mandated by the Sarbanes‐Oxley Act.

-

- Incorrect. Honest and ethical conduct, including ethical handling of actual or apparent conflicts of interest between personal and professional relationships, is included in the definition.

- Correct. The definition includes compliance with applicable governmental laws, rules and regulations — not GAAP.

- Incorrect. The definition includes full, fair, accurate, timely, and understandable disclosure in reports and documents that a registrant files with, or submits to, the SEC and in other public communications made by the registrant.

- Incorrect. The definition includes the prompt internal reporting to an appropriate person or persons identified in the code of violations of the code.

-

- Incorrect. Financial information systems and design implementation fees are not required

- Correct. Item 14 of Form 10‐K requires disclosure of fees billed to the company by its principal accountant broken out into the categories described here for the two most recent fiscal years.

- Incorrect. Tax fees are required to be disclosed, in addition to audit fees, audit‐related fees, and all other fees. Consulting services cannot be provided to SEC audit clients under Rule 2‐01(c)(4) of Regulation S‐X and, consequently, consulting fees are not required.

- Incorrect. Audit‐related fees are required to be disclosed, in addition to audit fees, tax fees, and all other services fees.

-

- Correct. Rules 14a‐3 and 14c‐3 require disclosure in the described proxy solicitation of the dividend policy, performance group, and market prices (per S‐K Item 201).

- Incorrect. Item 301 of Regulation S‐K requires five years of selected financial data.

- Incorrect. Item 301 of Regulation S‐K requires five years of selected financial data, and this data is not required for smaller reporting companies.

- Incorrect. Selected quarterly financial data for the last five years is not a required disclosure.

-

- Correct. Form 12b‐25 must be filed with the SEC no later than one day after the due date for the Form 10‐K (or other periodic report) in order to receive an extension on the due date. Form 10‐K must then be filed no later than the 15th day following the original due date of the report.

- Incorrect. Form 15 is filed when a company, upon meeting certain conditions, wishes to suspend its reporting requirements under the 1934 Act.

- Incorrect. Registrants are required to file a complete Form 10‐K.

- Incorrect. There is no Form 10‐K/L.

Chapter 5

Review question solutions

- b. To be eligible as a WKSI, an issuer must have either (1) a worldwide market value of outstanding voting and non‐voting common equity held by non‐affiliates of $700 million or more or (2) during the past three years, issued at least $1 billion in aggregate principal amount of non‐equity, non‐convertible securities in primary offerings for cash. Another requirement is that the issuer must be eligible to register a primary offering of its securities on Form S‐3 or Form F‐3.

- The public equity float test for WKSI eligibility determination is made within 60 days of the issuer’s eligibility determination date. The eligibility determination date is the later of the time of filing of the issuer’s most recent shelf registration statement or the time of its most recent Section 10(a)(3) amendment (requiring updates to a prospectus that is used more than nine months after the effective date of the registration statement).

Knowledge check solutions

-

- Incorrect. S‐1 is the general form to be used when no other form is specifically prescribed. This form is generally used for a domestic company’s initial public offering, including an IPO for a smaller reporting company and an emerging growth company.

- Incorrect. S‐3 is generally used by companies that have been reporting to the SEC for 12 or more months and have filed on a timely basis all reports required to be filed during the 12 calendar months preceding the filing.

- Incorrect. S‐4 is generally used for securities to be issued in certain business combinations that involve a public offering.

- Correct. 10‐K is the annual report required to be filed by companies whose securities are registered with the SEC.

-

- Incorrect. Information regarding use of proceeds from a securities offering should include disclosure of use of estimated proceeds for each purpose in order of priority.

- Correct. In addition, other required disclosures include descriptions of businesses or assets to be acquired, terms of debt to be reduced, and the amount and sources of further funds (if any) needed for each specified purpose.

- Incorrect. It would include information about other sources of funds that will be required for each purpose.

- Incorrect. It would include the terms of any indebtedness that will be repaid. If the indebtedness was incurred within one year, issuers should provide a description of the use of proceeds of the debt.

-

- Correct. The net tangible book value per share before and after the distribution is among the information required to be disclosed.

- Incorrect. Ratio of earnings to fixed charges is required when a company is registering debt or preference equity securities.

- Incorrect. The net tangible book value per share is required both before and after the distribution.

- Incorrect. The information regarding dilution does not require a capitalization table.

-

- Incorrect. This criterion applies to an issuer’s status as an accelerated filer.

- Correct. The criteria for WKSI includes having a worldwide public equity float of $700 million or more or having issued during the past three years at least $1 billion aggregate principal amount of non‐equity, non‐convertible securities in primary offerings for cash.

- Incorrect. The criteria for WKSI includes having a worldwide public equity float of $700 million or more or having issued during the past three years at least $1 billion aggregate principal amount of non‐equity, non‐convertible securities in primary offerings for cash.

- Incorrect. The public float requirement is $700 million met within 60 days of the determination date.

-

- Incorrect. The public float test for WKSI status is made within 60 days of the issuer’s eligibility determination date.

- Incorrect. If the WKSI does not meet the public float requirement, it can achieve WKSI status by having issued at least $1 billion aggregate principal amount of non‐equity, non‐ convertible securities in primary offerings for cash over the last three years.

- Incorrect. The WKSI criteria regarding Form S‐3 or Form F‐3 eligibility determination, other than determination of public float, is made at the time of filing of the issuer’s most recent shelf registration statement.

- Correct. The public float test for WKSI status is made within 60 days of the issuer’s eligibility determination date (that is, the date Form S‐3 or F‐3 eligibility is determined).

-

- Incorrect. Public notices permitted in accordance with Rule 134 are commonly known as “tombstone” ads.

- Correct. Rule 405 defines a free writing prospectus as any written communication that constitutes an offer to sell or buy securities relating to a registered offering that is used after the registration statement is filed (or, in the case of a well‐known seasoned issuer, whether or not such registration statement is filed) and is made by means other than a statutory prospectus.

- Incorrect. A free writing prospectus is any written communication that represents an offer to buy or sell securities relating to a registered offering that is used after the registration statement is filed and is made by means other than a statutory prospectus. In the case of WKSIs, it can be used regardless of whether a registration statement is filed.

- Incorrect. Free writing prospectuses are available to WKSIs even before a registration statement is filed and is available to all other issuers only after a statutory prospectus is on file with the SEC.

-

- Incorrect. The free writing prospectus must contain a prescribed legend, but disclaimers of responsibility or liability that are impermissible in a statutory prospectus are impermissible in the free writing prospectus.

- Correct. The prescribed legend must be included.

- Incorrect. Disclaimers of responsibility or liability that are impermissible in a statutory prospectus are impermissible in the free writing prospectus.

- Incorrect. Inclusion of information in a free writing prospectus that conflicts with information in the registration statement would be considered a prohibited offer.

-

- Correct. For well‐known seasoned issuers, a more flexible version of shelf registration, referred to as automatic shelf registration, has been established.

- Incorrect. The more flexible version of a shelf registration for WKSIs is an automatic shelf registration, not a pay‐as‐you‐go registration.

- Incorrect. The more flexible version of a shelf registration for WKSIs is an automatic shelf registration, not a well‐known seasoned registration.

- Incorrect. Immediate takedowns of securities covered by shelf registration statements are permitted, eliminating the so‐called 48‐hour waiting period for using a shelf registration statement once it becomes effective.

-

- Correct. Prior to the Securities Offering Reform rules, Form S‐1 did not provide for any incorporation by reference. The rules permit issuers to incorporate previously filed Exchange Act reports by reference into Form S‐1, so long as the reports are available on the issuers’ websites and the prospectus identifies all reports and materials incorporated by reference.

- Incorrect. Form S‐3 allowed incorporation by reference before the Securities Offering Reform.

- Incorrect. Form S‐8 allowed incorporation by reference before the Securities Offering Reform.

- Incorrect. Form S‐4 allowed incorporation by reference before the Securities Offering Reform.

-

- Correct. New Rule 430B provides that for Section 11 liability purposes of the issuer and any person that is at that date an underwriter, information omitted from a base prospectus and provided at a later date creates a new effective date for the registration statement.

- Incorrect. The Section 11 liability that applies to a prospectus supplement for issuers and underwriters does not extend to officers, directors, or experts, such as independent auditors.

- Incorrect. The Section 11 liability does not extend to independent auditors.

- Incorrect. The Section 11 liability extends to underwriters and not the experts.

-

- Incorrect. In 2007, the SEC adopted amendments to Form S‐3 and F‐3 to allow smaller reporting companies to use these forms to register primary offerings for securities if they have a class of common equity securities listed and registered on a national securities exchange such as NYSE or NASDAQ and eliminated the $75 million public float requirement.

- Incorrect. As part of the Smaller Reporting Company Regulatory Relief Act, the $75 million public float requirement no longer exists.

- Incorrect. As part of the Smaller Reporting Company Regulatory Relief Act, the $75 million public float requirement no longer exists.

- Correct. In 2007, the SEC adopted amendments to Form S‐3 and F‐3 to allow smaller reporting companies to use these forms to register primary offerings for securities if they have a class of common equity securities listed and registered on a national securities exchange such as NYSE or NASDAQ. To be eligible to use these forms, a registrant must meet the periodic reporting requirements under the Securities Exchange Act of 1934 and must have timely filed all required periodic reports for a period of at least one year immediately preceding the filing of the registration statement. The $75 million public float requirement was eliminated.

Chapter 6

Review question solutions

- Form 10‐K requires an audit by accountants; Form 10‐Q requires only a review.

- Earnings and dividends per share of common stock, the basis of the computation, and the number of shares used in the computation for all periods presented. Also, a reconciliation of basic‐to‐diluted earnings per share, as required under FASB ASC 260, Earnings per Share, must be included in a note.

- b. For all accelerated filers, including large accelerated filers, the third quarter report must be filed by November 9, 20X8 (40 days after the issuer’s third quarter‐end).

- Yes. The tests to determine an issuer’s filing category are made at year‐end based in part on information as of the issuer’s most recent second fiscal quarter. Thus, the first report an accelerated issuer files under a new filing category is always an annual report. In this example, if in 20X8 the issuer’s public equity float drops below $500 million on the last day of its second fiscal quarter, the issuer is still required to file its Form 10‐Qs for the quarters ending June 30 and September 30, 20X8, on an accelerated filer basis within 40 days of quarter‐end, but may file its Form 10‐K for the year ending December 31, 20X8 within 75 days of year‐end rather than the large accelerated filer 60 days.

- The company remains an accelerated filer for purposes of its second and third quarter Form 10‐Qs because its public float has not dropped below $50 million. For reporting purposes, however, the company is a smaller reporting company and has the option of following the scaled disclosure rules. Filing status and reporting status are independent of each other, and a company can be both an accelerated filer and a smaller reporting company.

- PCAOB Auditing Standard (AS) 3315, Reporting on Condensed Financial Statements and Selected Financial Data, and AS 4105, Reviews on Interim Financial Statements, cover condensed financial statements derived from audited financial statements and the requirements for reviews of interim financial statements.

Case study solutions

- Disclosures regarding going concern issues are very facts‐ and circumstances‐oriented and require substantial judgment on the part of management in determining when and what to disclose. In XYZ Company’s case, even though management concluded that it did not need to make going concern disclosures in its year‐end reporting, it should consider such disclosures for its interim reporting. Management needs to revisit going concern issues on a continual basis, especially if there have been negative trends over the past several quarters or there are other indications that the company is struggling financially or may be in the near future.

There are many factors besides operating results that indicate there could be substantial doubt about a company’s ability to continue as a going concern. AS 2415, The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern, lists the following factors to consider:

- Negative trends. For example, recurring operating losses, working capital deficiencies, negative cash flows from operating activities, and adverse key financial ratios.

- Other indications of possible financial difficulties. For example, default on loan or similar agreements, arrearages of dividends, denial of usual trade credit from suppliers, restructuring of debt, noncompliance with statutory capital requirements, and a need to seek new sources or methods of financing or to dispose of substantial assets.

- Internal matters. For example, work stoppages or other labor difficulties, substantial dependence on the success of a particular project, uneconomic long‐term commitments, or need to significantly revise operations.

- External matters that have occurred. For example, legal proceedings, legislation, or similar matters that might jeopardize an entity’s ability to operate; loss of a key franchise, license, or patent; loss of a principal customer or supplier; or uninsured or underinsured catastrophe such as a drought, earthquake, or flood.

Given XYZ’s negative earnings and liquidity trends that began in 20X7, additional disclosures are warranted in both the first and second quarter 10‐Q filings. Management should consider whether, based on its current financial condition, appropriate disclosures regarding operating performance and liquidity issues have been made in both the notes to the financial statements, as well as within MD&A. Expanded disclosures to consider could include

- forward‐looking disclosure regarding future operating results;

- the potential impact to the company as a result of having a downgrade in the company’s credit rating;

- subsequent events that may affect the company’s future operating performance, liquidity, and capital resources;

- early warning disclosures about the possibility of a future impairment, with a discussion of the conditions that would lead to such an impairment;

- sources and availability of financing for current and long‐term liquidity needs; and

- the current and future impact on the company of a lack of previously available funding sources.

In addition, the company may need to provide an explanation of differences between perceived expectations about the company’s financial results and its actual results — such as why there is no goodwill impairment, no other‐than‐temporary impairment, or no valuation allowance despite the negative trends described in MD&A.

Current going concern guidance requires an evaluation of an entity’s ability to continue as a going concern for a “reasonable period of time,” not to exceed one year beyond the date of the financial statements.1 If, as of the end of the first or second quarter, management has identified conditions or events that, in the aggregate, indicate there could be substantial doubt about the company’s ability to continue as a going concern, disclosures should be made in MD&A and the financial statements similar to what would be made in an annual filing, including

- the conditions and events giving rise to the assessment of substantial doubt about the company’s ability to continue as a going concern;

- the possible effects of those conditions and events;