CHAPTER 8

Social Performance Management

I've seen the power of micro‐finance all over the world in the eyes of mothers and fathers. It's unmistakable – joy and deep satisfaction they feel from being able to work hard and provide for their children and their future.

Rich Stearns 1

The microfinance sector distinguishes itself by means of its rapid growth and innovative potential. Profitability is an easily identifiable variable. However, new instruments are continuously being developed for the measurement of social performance and therefore the assessment of the social mission and outreach of MFIs as well as its impact. This is done to ensure that MFIs fulfill their social mission, contribute towards the fight against poverty and promote the financial inclusion of the poor.

Social performance is measured by MFIs and MIVs alike. There is no trade‐off between social performance and profitability. Microfinance institutions do not have to decide on one or the other, as both goals can be met simultaneously. The double bottom line thus becomes even more significant.

8.1 SOCIAL PERFORMANCE

There is no doubt that the sustainable funding of MFIs has been instrumental in their success. Clearly, an MFI that is able to cover its costs, will in turn be able to fund growth and, as a result of that, supply an ever‐increasing client base with loans. Despite the fact that a major part of the growth of the entire microfinance sector is based on sustainable profitability, investors, fund managers and MFIs insist on reaching the destitute and poor of this world, to provide them with useful financial services in order to improve their living conditions. Microfinance focuses on both financial and social aspects to reach these goals. They do not contradict but rather complement each other. In recent years, investors and financial institutions all over the world have been noted to seek ways of transparent assessment of social aspects to complement those of the profitability of investments.

Why does microfinance put so much emphasis on social performance? Microfinance's social aspect is a reservoir of the passion and commitment of all the investors and people involved in this line of business. People who identify with their clients witness and experience on a daily basis how microfinance helps their fellow beings to escape poverty. Governments, financial institutions, foundations, sponsors as well as private investors invest in microfinance from sheer conviction that their money will have a positive impact on societies locally. MFIs therefore must openly declare to their investors both the development of their social mission and how they intend to meet their goals. As a means of monitoring their services, customer satisfaction and the degree of improvement of living standards in their micro entrepreneurs, MFIs regularly publish their business reports.

Social performance is defined as the translation of a social mission into everyday actions of the institution in question. Social performance has to begin right at the core of the internal processes of an MFI, to define social determinants and variables and scale them.2

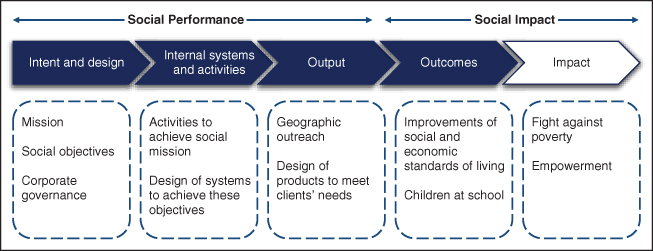

The Social Performance Task Force (SPTF), a global membership organization, has been working on a standard to advance social performance management in microfinance. Figure 8.1 illustrates the difference between social performance and social impact. Social performance denotes the number of poor and financially excluded who are reached by financial services (intent and design). The chart also displays the quality and usefulness of MFI services (internal systems and activities), as well as how borrowers profit from these services (output). Social impact, on the other hand, denotes the improvements on a micro entrepreneur's social and economic standards of living as opposed to someone who has not received a loan (outcomes).3 The changes effectuated by microfinance thus describe the impact on micro entrepreneurs. Microfinance and its idea to “do good” goes above and beyond the concept of any other socially responsible investment, where the main aim is “not to do damage.”

FIGURE 8.1 Social Performance and Social Impact

Data Source: Sinha (2006) and Social Performance Task Force (2014a)

8.2 MEASURING SOCIAL PERFORMANCE

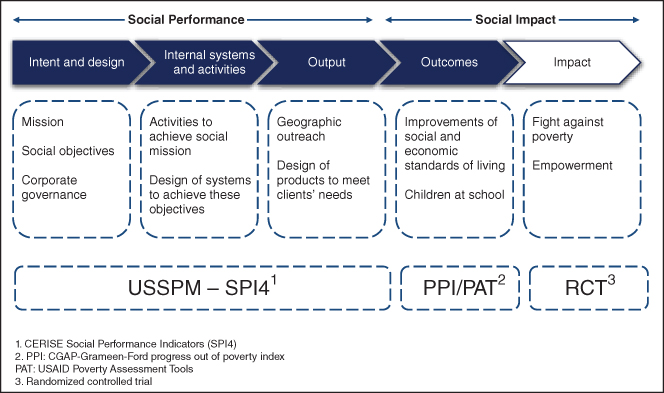

Social performance can be measured by means of different methods. Figure 8.2 displays the different instruments often employed to measure social performance and social impact. The SPTF has devised six dimensions along which social performance can be measured, the so‐called Universal Standards of Social Performance Measurement (USSPM). Today's practice often enough relies on these USSPMs, which include the CERISE Social Performance Indicators (SPI4) commonly used in the industry and designed in collaboration with the USSPM and Smart Campaign, an initiative promoting client protection.

FIGURE 8.2 Measuring Social Performance

Furthermore, the performance is evaluated in the individual regions where microfinance services are offered. CGAP, Grameen and the Ford Foundation have launched the Progress out of Poverty Index (PPI) that measures the results of social performance. The PPI investigates the degree of improvement in a client's social and financial situation, is available in 59 countries and is being applied by over 200 organizations.4 The USAID poverty assessment tool (PAT), an initiative of the US Congress, also measures the level of poverty. All the partners that have assisted USAID in the development of microfinance and who borrow financial means from USAID must apply the PAT – if it is available for their country – and communicate their results. The tool is available in 37 countries and is being applied by 25 to 30 organizations. Both tools, PPI and PAT, are publicly accessible.

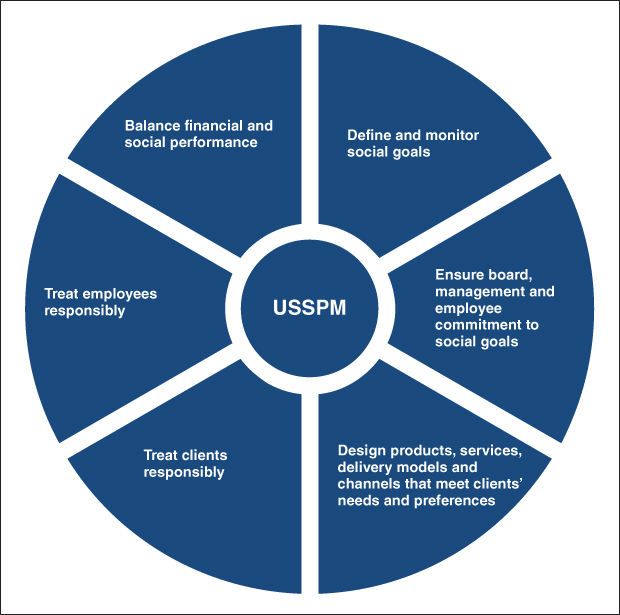

Universal Standards of Social Performance Management (USSPM)

The goal of the USSPM is to further illustrate the concept of social performance management and to standardize proven and tested practices. The USSPM are meant to assist MFIs to implement their social mission. The standards were devised seeing the demand in the sector for guidelines. They now combine the social performance initiatives of stakeholders all over the world in a single document (see Figure 8.3).

FIGURE 8.3 USSPM Overview

Adapted from: Social Performance Task Force (2014b)

In addition to this, guidelines were defined alongside every standard. They will be further illustrated in this chapter by means of applying the SPI4.

Smart Campaign

The Smart Campaign certifies MFIs that commit to client protection. It was launched in 2013 and in April 2016 comprised more than 60 members worldwide (see Figure 8.4). The Smart Campaign's directive is the protection of clients: micro entrepreneurs should not borrow more funds than they will be able to repay, and not use products that they do not ultimately need. There is particular emphasis on a respectful treatment of the client and clients are given the chance to file a complaint, so that microloans can be issued even more effectively. The Smart Campaign has seven client protection principles that help MFIs to internalize an ethical mode of conduct with their clients. The following principles are the so‐called essential practices i.e. basic conduct any client must expect on borrowing from an MFI.5

FIGURE 8.4 Smart Campaign

Adapted from: Smart Campaign (2016)

Appropriate product design and delivery

Providers will take adequate care to design products and delivery channels in such a way that they do not cause clients harm. Products and delivery channels will be designed with client characteristics taken into account.

Prevention of over‐indebtedness

Providers will take adequate care in all phases of their credit process to determine that clients have the capacity to repay without becoming over‐indebted. In addition, providers will implement and monitor internal systems that support prevention of over‐indebtedness and will foster efforts to improve market‐level credit risk management (such as credit information sharing).

Transparency

Providers will communicate clear, sufficient and timely information in a manner and language that clients can understand so that clients can make informed decisions. The need for transparent information on pricing, terms and conditions of products is highlighted.

Responsible pricing

Pricing, terms and conditions will be set in a way that is affordable to clients while allowing for financial institutions to be sustainable. Providers will strive to deliver positive real returns on deposits.

Fair and respectful treatment of clients

Financial service providers and their agents will treat their clients fairly and respectfully. They will not discriminate. Providers will ensure adequate safeguards to detect and correct corruption as well as aggressive or abusive treatment by their staff and agents, particularly during the loan sales and debt collection processes.

Privacy of client data

The privacy of individual client data will be respected in accordance with the laws and regulations of individual jurisdictions. Such data will only be used for the purposes specified at the time the information is collected or as permitted by law, unless otherwise agreed with the client.

Mechanisms for complaint resolution

Providers will have in place timely and responsive mechanisms for complaints and problem resolution for their clients, and will use these mechanisms both to resolve individual problems and to improve their products and services.

Smart Campaign certifies MFIs that have implemented adequate processes for client protection, ultimately not just for the profit of the client, but for the entire industry.

MFTransparency

Micro Finance Transparency (MFTransparency) is an NGO founded in 2008. It promotes pricing transparency in the microfinance industry.6 MFTransparency allows for a transparent exchange of information concerning the prices of microfinance products among market participants. Information concerning loan products and their prices, for instance the effective annual interest rate, are presented in a clear and consistent manner so that they are comparable. The NGO collaborates with other institutions such as the SPTF, The Microfinance Index Exchange MIX and the Smart Campaign. By using MFTransparency, an array of market participants can contribute towards the development of transparency standards.7

Social Performance Indicators (SPI4)

CERISE is a research enterprise in the microfinance sector that has developed the SPI4 rating tool in collaboration with the Smart Campaign and the SPTF. The SPI4 measures social performance along the USSPM and targets and identifies the strengths and weaknesses of the MFI under scrutiny (see Figure 8.5). An evaluation of the internal systems and activities of an MFI on the basis of a questionnaire will establish whether the MFI has reached its social goals. The questionnaire examines to what extent low‐income parts of the population and the financially excluded are being reached, whether products and services have been adapted to this target group, whether MFIs grant their clients not only social but also political capital, and whether they embrace the responsibilities of their organization altogether.8 The SPI4 is publicly accessible and may be used for one's own assessment or for advisory services. The following examples will demonstrate the application of the SPI4 and illustrate the goals of the USSPM.

FIGURE 8.5 Measuring Social Performance by Means of USSPM

Data Source: Social Performance Task Force (2014b)

- Define and Monitor Social Goals

In a first step, both the mission of an MFI and its suitability for the target market are assessed. The focus thereby is on how the MFI measures those goals and achieves them, and how much attention it pays to monitoring its clients' performance as well as to client supervision during the entire lending process.

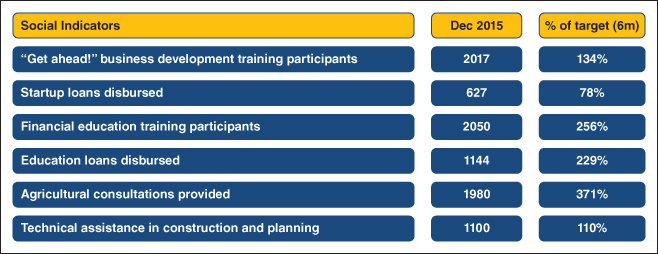

Imon International, for example, is an MFI in Tajikistan that clearly stipulates its mission and means to achieve these goals, monitors them on a regular basis and measures their progress. Imon International manages to reach 82,000 people by mostly lending to the rural population and providing them with training and other non‐financial services. They obtained their license to accept deposits in 2013 to broaden their range of services. In August 2014, Microfinanza Rating awarded Imon International an impressive A+ rating. The MFI's mission is “to promote sustainable economic development and improve quality of life in Tajikistan by ensuring reliable access to financial services for the economically active members of the population.” Figure 8.6 displays the development of the social indicators that measure Imon International's social performance over the period of January to June 2014. It reveals that 10 of the 11 indicators are on target for their half‐yearly goal and even exceeded it by up to 128 per cent.

- Ensure Board, Management, and Employee Commitment to Social Performance

Social goals can only be reached if an entire organization supports them wholeheartedly and commits to them on a daily basis.

Ever since its foundation as an NGO in 1985, Banco Fie in Bolivia has subscribed itself to social performance (see Figure 8.7). Their efforts were awarded with a banking license in 2010. Banco Fie promotes the implementation of social performance throughout their company and therefore ensures that the supervisory board, management and all employees also contribute towards the success of this mission. The bank thereby reaches almost 25,000 borrowers and 800,000 depositors in their regional subsidiaries all over Bolivia.

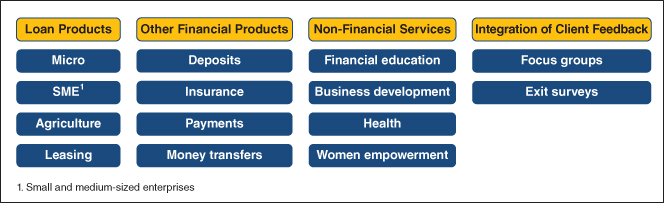

- Design Products, Services, Delivery Models and Channels that Respond to Clients' Needs and Preferences

Product design is the be‐all and end‐all of microfinance. This indicator therefore investigates the range of financial and non‐financial products as well as how well these services manage to reach their targeted clients (see Figure 8.8).

- Treat Clients Responsibly

The SPI4 promotes socially responsible lending. It engages MFIs in a transparent, sustainable and socially responsible mode of conduct. MFIs are to implement the Smart Campaign standards of client care or disclose their data with MFTransparency. Moreover, it investigates how MFIs can avoid over‐indebtedness in their clients, protect their data and explain the mechanisms for complaint resolution. The example of Crezcamos in Columbia (see below) illustrates how an MFI can take responsibility for their clients by specifically enhancing their range of products.

- Treat Employees Responsibly

An MFI's interaction with its employees speaks volumes about its social responsibility. MFIs are role models for local enterprises and should therefore provide attractive employment opportunities. Among other things, staff turnover, staff assessment, compensation and opportunities for further training are all part of an MFI's assessment. The following box illustrates an MFI's responsibilities and how to assume them with respect to staff.

- Balance Social and Financial Performance

Successful MFIs all over the world demonstrate that profitability and social performance can exist side by side and may in many cases be increased simultaneously. A financially stable MFI can operate sustainably and extend its range of services to serve more clients. Thoughtful client care and client satisfaction prove its mindful conduct when it comes to society (see the example in the following box). This combination of profitability and social performance attracts investors' funds. The balance of profitability and social performance can be investigated with the following questions:

- Does the MFI pass on any proceeds generated from bundled efficiency on to its clients?

- Is the management adequately and reasonably rewarded for their efforts?

- Does the MFI work in the interest of the community?

- Promote Environmental Protection (not yet a USSPM)

Other measuring tools such as the Social Performance Impact Reporting and Intelligence Tool (SPIRIT), which is based on the USSPM, also witness a proactive change in MFIs towards the development of the protection of the environment. SPIRIT investigates whether an MFI has included a comprehensive environmental policy into their standards and guidelines, and whether they also grant “green loans” to save energy and support environmentally friendly products. The Promotion of energy‐saving models not only protects the environment, but also is cost‐efficient and has a positive impact on the health of the local population. For example, the MFI HKL notably encompasses environmental protection by providing specific funding products for renewable energies as well as water and sanitary installations.

FIGURE 8.6 Measuring Social Performance with Imon International

Data Source: BlueOrchard (2014)

FIGURE 8.7 Banco Fie's Commitment to Social Performance

Data Source: BlueOrchard (2016)

FIGURE 8.8 Products and Services of MFIs

Data Source: BlueOrchard (2014)

8.3 MEASURING THE OUTCOME OF MICROFINANCE

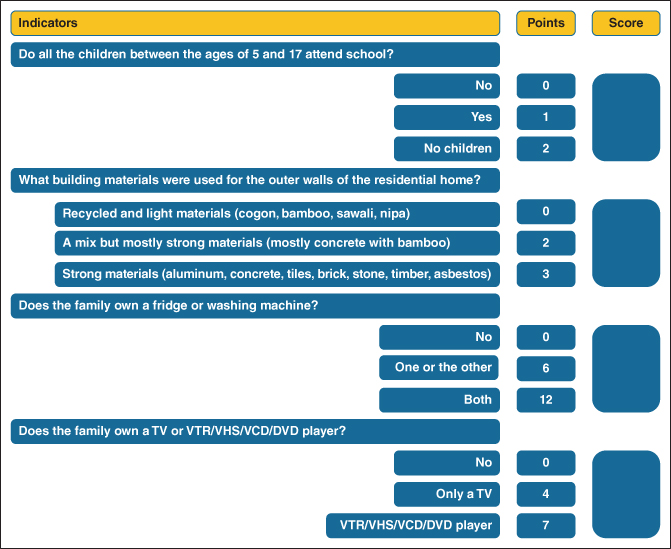

The PPI measures the economic development of MFI clients and the improvement of their living standards and makes them comparable on a global scale, leaving causality aside. A poverty scorecard was developed for this purpose (a points system in the fight against poverty) that relies on analyses of living standards measurement questionnaires in specific countries.9 The indicators are simple, cost‐efficient for detection, transparent and intuitive. The survey is based on ten easy questions, the answers to which indicate precisely whether borrowers live above or below the poverty line. Trials have revealed that these questionnaires yield precise results on both the rural and urban population of a country.

Figure 8.9 is an extract from the poverty scorecard of the Philippines. The points awarded for the answers were determined via econometric analysis based on a living standard measurement of the population of the Philippines. An MFI employee will question people locally and note down their answers. The subsequent evaluation will calculate the average answer and compare it with the data on a chart that displays the different stages of the likelihood of poverty. This determines the share of the population living below the poverty line. The scorecards of other countries rely on the same pattern, are equally simple and their aim is the same; the questions, however, are different.10

FIGURE 8.9 Poverty Scorecard of the Philippines (Extract)

Data Source: Grameen Foundation (2015)11

The USAID poverty assessment tool (PAT) works in a similar way and likewise collects household data.

8.4 SOCIAL RATING AGENCIES

Social rating predominantly aims to compare the social performance of all the MFIs in one sector. The rating report highlights the strengths of an institution and indicates the remaining potential in a poignant way.

The difference between a rating and a social performance assessment (which is mostly performed by asset managers and MFIs themselves) is mainly that reports of the institutions are not necessarily disclosed or published and are not compulsorily subject to a uniform process. Social performance can be measured in various ways.

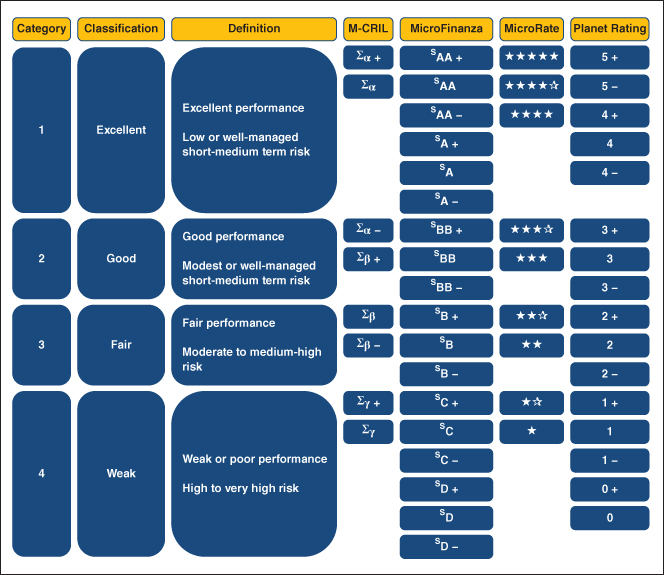

In addition to their financial credit rating, rating agencies that are specialized in microfinance have introduced a social performance rating. These external ratings are based on USSPM, the Client Protection Principles (CPP) of the Smart Campaign, and the poverty assessment tools such as CGAP's PPI. The main aim of these ratings is client protection and to ensure that MFIs take care of their clients and their needs throughout the entire lending process. The four well‐known rating agencies – M‐CRIL, MicroFinanza, MicroRate and Planet Rating – generally distinguish between the standard methodology based on information from MFIs, and the comprehensive approach based on focus groups and client feedback.12

M‐CRIL

The rating agency M‐CRIL has played a pioneering global role in developing a systematic methodology for social rating. With its solid and fast approach to defining social performance in processes and investments, and to publishing the reports, M‐CRIL has strengthened its commitment to supporting the microfinance sector.

Social ratings are conducted by means of a comprehensive and a standard methodology. M‐CRIL uses the comprehensive rating to investigate all dimensions of the SPTF in the areas of social performance and impact (intent and design, internal systems and activities, output, outcomes, impact). This type of rating is more extensive than other methodologies. M‐CRIL not only assesses the data of an MFI, but uses the results of a questionnaire to measure the impact the MFI has on a micro business. The standard rating methodology only comprises data on the level of an MFI, and therefore the impact on micro entrepreneurs cannot be measured adequately. Both rating methodologies rate an MFI with the Greek letters alpha, beta, and gamma. They are easily recognizable as they are preceded by a sigma as the following shows: ![]() ,

, ![]() und

und ![]() (see Figure 8.10).13

(see Figure 8.10).13

FIGURE 8.10 Rating Agencies for Social Performance

Data Source: The Rating Initiative (2013)

MicroFinanza Rating

To begin with, MicroFinanza exclusively used the standard methodology that corresponds with a simplified version of M‐CRIL's rating. Nowadays, MicroFinanza and M‐CRIL make use of both methodologies. MicroFinanza ratings are very similar in structure to those of the credit rating agencies Standard & Poor's and Fitch, recognizable by a preceding S, and range from SAA+ (excellent) to SD– (weak).

MicroRate

The rating methodology of MicroRate is similar to that of M‐CRIL. In a first step, clients are questioned locally. Upon evaluation of the MFI in its headquarters and in selected branches, the final report that includes the rating will be written. The entire rating process takes an average of six to eight weeks, and the rating itself is evaluated by means of stars ranging from excellent to weak.14

Planet Rating

Planet Rating is the only one of the four rating agencies to evaluate social performance by means of the standard methodology only. Eventually, only data from the MFI will be taken into consideration when rating the MFI. The agency's rating is based on figures ranging from 5 (excellent) to 0 (weak).15

8.5 TECHNICAL ASSISTANCE

Managers of investment vehicles will base their assessment of an MFI's social performance on the instruments mentioned above. To further strengthen social values locally, to improve underlying processes or even build them, MIV managers also require technical assistance (TA). Besides that, TA promotes the implementation of new knowledge with the help of training and work groups. Standard TA projects provide tailored support services in areas such as strategy and business planning, quality of the lending process, product development, risk management and the reporting or measuring of social performance. TA therefore denotes advisory services that assist MFIs to implement their mission in a sustainable manner, as there is no doubt that only economically sustainable MFIs will receive investor funds.

Increase in MFI Capacity

TA can help to improve internal processes, strengthen IT systems and risk management, or introduce new products. The transformation process of an MFI into an official financial institution also makes part of the TA advisory services. Here is a list of the services that TA can provide:

- SWOT analysis16

- Developing new products, services and training thereof

- Planning of market strategies

- Conducting impact studies and market research

- Devising of business and improvement plans

- Introduction of IT systems

- Devising of social performance management

Strengthening the Financial Sector

To bolster the growth of the financial sector, TA applies not only to MFIs but to other protagonists at the same time: local microfinance networks, banks, governments, central banks and development banks.

TA is available with local microfinance networks in order to support regional businesses and establish specific local strategies. This includes the following services:

- Training programs for instructors

- Resource center

- Impact assessment and market research

- IT support

- Credit bureaus

- Development of internet portals

Banks and financial institutions support TA with the following activities:

- Impact assessment and market research

- Support of financial projects

- Training loan officers

- Assistance in the choice of business associates

Governments and central banks may profit by using TA to implement adequate standards and guidelines that will in turn boost growth in microfinance:

- Impact assessment and market research

- Definition of a national microfinance strategy

- Implementation of adequate guidelines and standards

- Improved supervision of MFIs

TA also works as a catalyst for development banks in their assistance of MFIs by means of the following:

- Impact assessment and market research

- Identification of sustainable and social MFIs

- Supervision of microfinance portfolios

- Employee training for successful evaluation of MFIs

TA therefore tackles an array of specific problems in microfinance. Social performance benefits society. The following will demonstrate the impact of social performance on micro entrepreneurs.

Impact on Micro Entrepreneurs

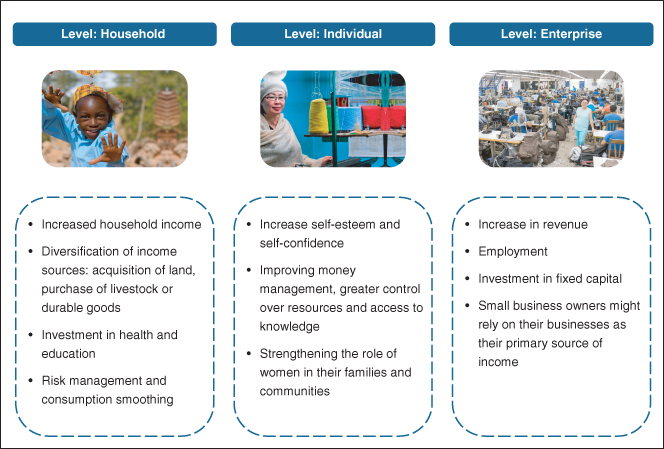

Measuring social performance in microfinance warrants that an investor's commitment always benefits the poor. This empowers the poor, because they are economically active, and achieve a better standard of living to allow them to provide for their families (see Figure 8.11). Successful micro enterprises on the other hand also boost the economy, employment and growth. As a result of the targeted social upswing, the respective region's experience improved and there were increased supplies of food and better health and education.

FIGURE 8.11 Impact of Microfinance

8.6 LINKING SOCIAL PERFORMANCE WITH PROFITABILITY

The double bottom line of the microfinance sector challenges MFIs to reach their social development goals. It is a common misconception that measures that have been implemented in order to achieve the social mission have a detrimental effect on an MFI's profitability. Figure 8.12 illustrates the empirical connection between social performance and profitability of the loans issued to MFIs.17 It has become evident that there is no trade‐off between the two goals. Loans with a high social performance are similarly profitable as loans with a lower social performance, which again supports the double bottom line theory.

FIGURE 8.12 Social Performance and Profitability

Data Source: BlueOrchard, Mangold (2015)

Systematic evaluation and an adequate investment process can boost social performance and profitability at the same time. This conclusion is all the more important as it means that MFIs do not have to choose between social performance and profitability. Both goals can be met simultaneously.

8.7 PRELIMINARY CONCLUSIONS

Measuring social performance ensures that all actions are performed in the interest of the fight against poverty and exclusively serve to meet the needs of the poor segments of the population. The SPTF devised six standards to measure social performance that in turn measure and evaluate the implementation of an MFI's social mission.

Measuring social performance in MFIs at the same time means a thorough investigation of their social impact. There are several issues under scrutiny: Is the client provided with a range of adequate products and services? Do these empower the micro entrepreneur to improve their living standards? Measuring social performance measures the impact on society at large, for instance the fight against poverty and the empowerment of women.

For MFIs, advisory services (TA) are provided that should help MFIs and other protagonists in the microfinance sector to operate successfully and sustainably and fulfill their social mission at the same time. TA on the other hand is also instrumental in introducing new products, as well as implementing efficient and innovative processes. Social performance is measured in addition to a credit rating. There are now a number of independent social rating agencies such as M‐CRIL, MicroFinanza Rating, MicroRate and Planet Rating.

Empirical analysis has revealed that there is no trade‐off between social performance and profitability, and MFIs therefore do not have to decide in favor of one or the other, as both can be met simultaneously. The double bottom line thus becomes even more significant.

Social performance is an integral part of microfinance. Only this way can we be sure that the poverty in this world is targeted so that micro entrepreneurs can create better lives for themselves and their families and thereby boost the economy of their region and their country.