CHAPTER 9

Beyond the Reach of Microfinance?

Humanity's greatest advances are not in its discoveries, but in how those discoveries are applied to reduce inequity.

Bill Gates1

Prejudices and reservations, such as that the term “borrower” is synonymous with repayment difficulties and that extortionate interest rates exacerbate poverty rather than alleviate it, are deep‐rooted.

Microfinance is a relatively young asset class, and detailed knowledge and research on it are yet to be made publicly accessible on a larger scale. It is therefore subject to widespread criticism that the microfinance industry has to account for.

9.1 PREJUDICES AND RESERVATIONS

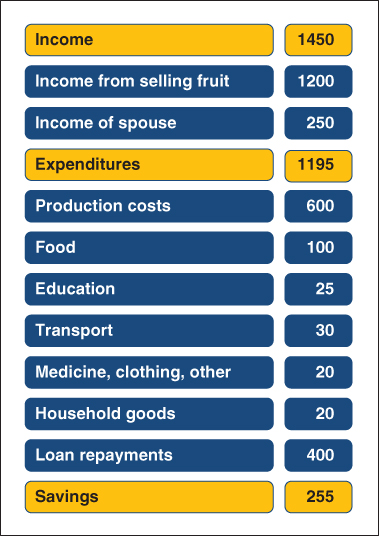

Prejudices about the poor and how they handle money are deep‐set. The consensus seems to be that low‐income parts of the population should not borrow money, as they will fail to repay it anyway. Or that the poor, even on the verge of starvation, would rather squander the funds given to them to indulge themselves instead of investing them in a sustainable business activity. Practice, however, has shown a different picture altogether. As a rule, for the poor, long‐term economic advancement clearly takes priority. Borrowers are fully aware of their unique investment opportunity, and there are loan officers who will ensure that a loan is used as specified. They will step in to monitor the situation more closely should it prove necessary. A partial use of a loan for food may in fact even be beneficial, as the example in Figure 9.1 reveals. A group of ceramicists in Siguatepeque in Honduras, for instance, used part of their loan for the purchase of food. It allowed them to store their finished pots and wait for prices to rise instead of being forced to part with them less profitably.2

FIGURE 9.1 Exemplary Budget of a Female Borrower (in $)

Data Source: BlueOrchard Research

It is equally remarkable perhaps to note that the savings rate of micro borrowers is comparatively high. Deposits of the year 2014 accounted for an average of 30 per cent of the MFI loan portfolio.3 To maintain that the poor do not save money is therefore utterly unfounded. What is true, however, is that they use their initial loan to generate their own income and then save a part of it.4

Why Are Microloan Interest Rates Seen as Excessive?

In microfinance, the share of the operating costs of the entire credit costs – i.e. the determinants of the interest rate – averages at 60 per cent. Chapter 7 has illustrated that this figure is largely the result of high resource intensity, the fact that micro entrepreneurs live in remote areas and the rather low amounts for which loans are issued, as shown in the example in Figure 9.2. Financial services for micro entrepreneurs are costly, hence the reluctance of commercial banks and financial service providers to supply them with loans. As a consequence, the operating costs that are incurred with a microloan are comparatively high.

FIGURE 9.2 Receivables from Loans Provided Per Employee (in $)

Data: Deutsche Kreditbank (2015); Prasac (2015); Raiffeisen Group (2015)

Local rates of inflation, often two‐digit, are another factor that distorts absolute interest rates. Figure 9.3 illustrates this phenomenon using Ghana as an example.

FIGURE 9.3 Inflation in Ghana

Data: World Bank (2016)

Transparency is a must, and costs are to be disclosed so that interest rates can be understood and corruption kept at bay. The ultimate proof that this model is successful in practice as well as in theory, however, lies with the fact that, except for a few, micro entrepreneurs manage to redeem their loans and interest on time.

What Are the Reasons for the Financial Crisis in India, the Suicides and Over‐Indebtedness?

It is unclear how microloans may have been involved in some suicides in Andhra Pradesh in 2010 (see Chapter 11.2). The fact is that the country was savaged by a prolonged period of drought with devastating consequences for those working in agriculture. Loans were either only partly or not at all redeemed as crops had been lost. Borrowers were more than aware of the impending termination of all business activities of MFIs as a result of the weak political and legal framework, which in any case would have made any further loans virtually impossible.

At the same time, 82 per cent of all households in Andhra Pradesh had also taken out loans with informal money lenders, who would not only issue overpriced loans, but at the same time grant volumes that exceeded their borrowers' repayment capabilities. This illustrates the risks and size of the market of informal money lenders. A mere 11 per cent of the Andhra Pradesh households had borrowed from an MFI, and only 3 per cent of those borrowers were in debt with more than one MFI.6

To counteract similar situations, MFIs today also provide weather risk insurance. In collaboration with credit bureaus (see Chapter 5.5) an information system was devised that makes loan data and information accessible to MFIs and clients in an attempt to avoid over‐indebtedness.7

With hindsight, it can now be safely established that the lack of regulation of informal money lenders was largely responsible for the destabilization of the entire microfinance industry in 2010. It is more than frustrating that not only borrowers from informal money lenders had to bear the brunt of it, but along with them millions of people who were consequently deprived of any chance of a loan.

Can Social Performance Be Measured at All?

Social performance measures to what degree MFIs implement their social mission and ensure that both management and employees contribute towards the same goal. It investigates whether an MFI tailors its products and services to its clients' needs, treats its clients and staff respectfully, and whether it manages to strike a balance between profitability and social performance.

The Social Performance Task Force, for instance, has devised global standards to measure social performance (see Chapter 8.2). The SPI4 is a tool that measures social performance by means of a points system.8 The indicator also includes global standards of the Smart Campaign – an initiative devoted to client protection.

Rating agencies that assess an MFI as an institution (Microfinanza Rating) are joined by rating agencies that focus on social performance (M‐CRIL, Microfinanza Rating, MicroRate, Planet Rating). Their aim is to disclose the results of their social performance ratings in order to achieve a uniform rating system for all MFIs.

In simple terms, social performance denotes to what degree MFIs assume their social responsibilities. Overall it is easily measurable, and there are various tools available to do so.

MFIs go to great lengths to implement their social mission, but how can their social endeavors be measured? Aforementioned tools such as the PPI and the PAT are easily applicable and reliable instruments. Research also uses sophisticated methods such as randomized controlled trials; however, they are less suitable in practice.9

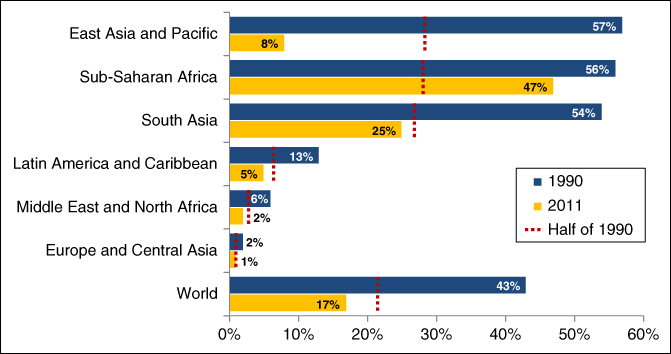

On a macro level there is ample proof that poverty worldwide is decreasing (see Figure 9.4). Admittedly, not all the credit perhaps belongs to microfinance, but some undoubtedly does.

FIGURE 9.4 Comparison of Poverty Levels10

Data: World Bank (2016), database 2012

The countless success stories of micro entrepreneurs are the irrefutable proof of the efficacy and effectiveness of microfinance. Take Judith Martinez's story, for example. A microloan nine years ago allowed her to set up her own flower stall. With the proceeds she has been able to expand her business to meet the increasing demand for flower bouquets and pot plants. Today, she is renovating her house, can support her family financially and can increase the living standard of her entire family. Her second loan steeply increased to five times the amount of her first.

Does Microfinance Breed Corruption?

Many MFIs respond to a feeble legal system, and are amidst daily political conflicts and corruption. Corruption often takes the shape of bribery, fraud and blackmail.

In all honesty, it would be presumptuous to conclude that corruption is non‐existent in MFIs, which are as a rule personnel‐intensive. There are viable options, however, to keep corruption to a minimum. The most effective steps in the fight against corruption are an utmost degree of transparency in connection with the cash and interest rate flows of all the protagonists involved. But alongside transparency, supervision is key. Conventional and non‐conventional control mechanisms can identify and fight systematic corruption and deceptive practices. In cases of fraudulent practices with a criminal energy, there are limits to what these control mechanisms can do, reminiscent of similar incidents in established financial institutions of the Western hemisphere. In microfinance, self‐monitoring plays a much more important role than in Western institutions. There is considerable emphasis on social norms and honor, but most importantly, there is an awareness that human lives are at stake – fellow countrymen, neighbors, friends and family. To further counteract fraudulent practices, loan officers are usually well‐paid, which makes them less prone to corruption.

MFIs may either be directly affected by corruption in microfinance by granting fictitious loans, or indirectly, for instance by accepting money from bogus transactions. Microfinance institutions may in fact take deposits from clients who are involved in corrupt affairs.11 This is rather unlikely, however, as MFIs are in close contact with their clients and steadily monitor their business activities. Moreover, bogus transactions are more likely to be undertaken via larger financial institutions due to the fact that deposits or the transfer of larger sums of money usually attract attention in MFIs. Entrepreneurial activities of poor households usually leave little room for corruption.

Does Microfinance Actually Have an Effect on SME Growth?

Microloans mostly support small‐scale activities. It is therefore wrong to maintain that microfinance does not promote the development of SMEs.

On the contrary, the support of activities on a small scale promotes financial and economic thinking right from the start and encourages and builds functioning, economic activity. If micro entrepreneurs are successful, they may turn their business venture into an SME with increasing local relevance. In fact, established SMEs are perhaps better served by banks than by MFIs, as they present collateral along with a successful business model and are able to take out a loan with more flexible maturities in the long run. Although a sound business development is significant for micro entrepreneurs, it is most relevant particularly for economic development on a national level.

Microfinance and Child Labor?

Small enterprises succeed or fail depending on their range of products and the diligence and determination of their founders. For this reason, they are usually supported by an entire family network, which naturally includes children. It would be mistaken, however, to refer to this as child labor. Child labor, according to the Oxford English Dictionary12, refers to the employment of children in an industry or business, especially when illegal or considered exploitative. If children assist in their parents' business it does not primarily serve the purpose of generating financial revenue, but ensures the continuation of the business. Any additional income very often flows into the children's education at any rate. As women often generate an income for the benefit of their families (see Chapter 6.3), this strongly contradicts the assumption that the business aspect is in the foreground. Children's activities in their parents' business rather enhance the living standard of all the family members involved.

Impending Mission Drift?

The term “mission drift” refers to MFIs that stray from their social mission of providing poorer parts of the population with access to capital, but instead switch their attention to another target group, i.e. wealthy clients. In many cases MFIs deal with wealthy clients in a more profitable manner, as their higher collateral allows them to take out more substantial loans, which in turn lowers their risks and costs. Let us remind ourselves that the operating costs are mostly independent of the amount of a loan (see Chapter 7.1).

It is often incorrectly assumed that higher average loans are synonymous with mission drift.13 Higher average loans may have perfectly positive aspects as well. On the one hand, it may well be that former micro entrepreneurs have expanded their business activities rather speedily and that their credit limits therefore have risen substantially over the years. In such cases, severing all ties with a functioning business makes little sense for MFIs. On the other hand, macro‐economic influences may also increase the amount of the loans. A country's increased welfare – undoubtedly also thanks to microfinance – automatically leads to higher loans. The existence of mission drift is widely disputed. Whatever the case may be, measuring social performance is the best way to keep it at bay.

Fund of Funds Diversification?

Although asset managers assess MFIs independently and with the help of different tools, investment into identical MFIs cannot be avoided. The reasons for this are as follows: firstly, the MFI universe in the different regions is limited, and secondly, MFIs are selected according to their financial and social performance. Sufficient diversification can therefore already be achieved by a single asset manager, provided that there are a high number of investments and the avoidance of correlation and country risks. Topical and sector‐specific diversification, however, is a different and more individual issue.

9.2 PRELIMINARY CONCLUSIONS

The largest countries in the world, countless government funds as well as private initiatives and partnerships, increasingly commit themselves to development institutions, as the soaring growth rates of impact investing amply demonstrate.14

All the protagonists along the value chain of impact investing have to answer to the points of criticism that have been and are being raised in an attempt to find solutions to streamline processes for better efficacy and efficiency. In the first place, it is all about the micro entrepreneurs. In the past, over‐indebtedness could be lowered by the launch of credit bureaus and the fact that they collect personal and loan‐specific data on their clients, ultimately the reason for more transparency in the market. The data disclosed can be viewed by MFIs and borrowers alike, which enables the latter to self‐monitor their borrowing over prolonged periods of time.

Impact investing is a relatively young financial sector, and processes are being streamlined on a daily basis. The two decisive factors thereby are digitalization and the implementation of new technologies.