CHAPTER 11

Real and Financial Economy

The man (real economy) walks down a street. The dog (financial economy) sometimes falls behind and sometimes runs on ahead. However, both man and dog ultimately reach their destination together.

Joseph Schumpeter1

The real economy – the part of the economy that deals with the production of goods and services, unlike the financial markets – is where borrowers are active. It is hardly influenced by the global economic cycle. Borrowers of microfinance institutions hence generate their incomes on local markets, and the local real economy's infrastructure to connect it to the rest of the world is either rudimentary or simply non‐existent.

The financial economy, on the contrary, can influence large microfinance institutions, as they are partly funded by international capital markets. The financial means of microfinance have not faltered despite the global financial crisis.

11.1 MICROFINANCE IS CRISIS‐PROOF

Microfinance's two‐digit growth rates even during the financial crisis amply demonstrate its resilience in the face of changes in the global economic cycle (see Figure 11.1), the reason being that in microfinance, borrowers generate their income in a largely independent, closed economy. They mostly engage in very local markets, which depend more on regional politics, the regional economy and local natural disasters than on the cycles of other economically dominant countries.

FIGURE 11.1 SMX

Data Source: SMX

Microfinance is fundamentally influenced by aspects of the real economy. Its integration in the financial system may result in local markets being affected by global macro‐economic influences. Investors may choose to refrain from further investments in the capital market, which would eventually lead to a drop in the financial means that MFIs can employ for lending. So far, MFIs have been able to collect means from international capital markets even during times of crises. They have remained unaffected by investor withdrawal.

Figure 11.2 displays the balance sheet of an MFI. The assets depend on the real economy and therefore on lending to micro entrepreneurs. The liabilities represent the funding side. To prevent risks presented by the real economy, recent years have seen the introduction of stability mechanisms, such as credit bureaus, micro insurance and enabling MFIs to take deposits.

FIGURE 11.2 Balance Sheet of an MFI

11.2 REAL ECONOMY AND LOCAL INFLUENCING FACTORS

Figure 11.3 compares the trade balances of selected countries that are active in microfinance with those of Germany and Switzerland. These two countries, along with Azerbaijan, Vietnam and Mongolia are the only ones to reveal a trade surplus. All the other countries that are displayed import more than they export.2 Markedly, their volumes of imports and exports are considerably smaller than those of industrialized countries. Germany's export volume is almost five times that of India, despite the fact that the population of India is 15 times that of Germany. A high foreign trade volume indicates that the countries depend on each other. A drop in demand in the regions of destination for Germany's exports will naturally result in a decrease of the German trade surplus and hence lower its GDP. Germany, as an industrial nation, therefore depends on global economic cycles.

The repayment rate of micro entrepreneurs, however, is largely independent of either a global boom or a global recession, as their business model is based on their local economy. Chapter 4 has revealed that about a third of the volume of loans is handed out to borrowers in the local trade, followed by agriculture at 28 per cent and services at 21 per cent. Local purchasing power does react to regional parameters; however, it remains unaffected by interest rate cuts and economic crises in other countries and on other continents. Moreover, microfinance regions lack the infrastructure to make them an integral part of the global network. The repayment rate of micro entrepreneurs therefore depends on aspects of the real economy and the local framework in particular. Micro entrepreneurs operate locally, and this entails a key advantage: diversification is particularly effective. Events such as the catastrophic drought in Andhra Pradesh remain geographically isolated. Any economic activity a mere few kilometers away remains unfazed. A diversified portfolio is therefore the best option to avert losses.

FIGURE 11.3 Trade Balances of Selected Countries

Data Source: World Trade Organization (2015)

11.3 FINANCIAL ECONOMY

Micro entrepreneurs, and MFIs indirectly also, remain virtually unaffected by global developments of the real economy. Global financial integration has increased over the last few decades, and emerging countries have matured into participants of the global capital market. What is the situation of MFIs with respect to the financial economy?

FIGURE 11.4 Foreign Exchange Volume and Outstanding Government Bonds

Data Source: BIS (2013) and BIS (2015)

Influencing Factors

The key factors relating to the financial economy are the liquidity trap, inflation and currency devaluation. The lack of availability of refinancing funds for an MFI may lead to liquidity problems. This can be observed in a decrease in international investment flows or local funding.

Depending on the type of funding, some MFIs may be more strongly affected by capital decrease at times of international tensions than others. Most MFIs in India, for example, fund themselves by means of local capital, i.e. via local banks, whereas MFIs in Nicaragua are mainly funded by capital from international markets.

Inflation, on the other hand, can also influence an MFI's liquidity situation, albeit indirectly. Soaring prices result in rising wages, as the labor market adjusts to inflation. This means that in addition to the rising costs for production materials, micro entrepreneurs will incur higher operating costs with respect to employees and administration. Inflation will, however, also boost turnover, for the simple reason that goods may now be sold at higher prices. The temporal delay in price adjustments between the purchase and distribution of goods and services may affect the liquidity of micro entrepreneurs, which may in turn lead to loan repayment delays.

Local currencies may be devalued because of slow economic growth or rising inflation. Any devaluation changes the exchange rate and may thus have an impact on the profitability and the management of the assets and liabilities of MFIs, should they be funded in foreign currency.

Prevention and Hedging Against Risks from the Financial Economy

Risks posed by the financial economy are particularly relevant with respect to the liquidity management and the asset liability management of a microfinance institution. In order to prevent and hedge risks from the financial economy, regulators and investors have imposed a series of measures.

In most countries regulators define, for example, strict minimum liquidity requirements. In addition to this, the analysis of the liquidity situation of an MFI is an integral part of the rating and investment processes, which explains why MFIs are eager to maintain sufficient liquidity reserves. Today, there are various instruments available even for exotic currencies that will allow a fund manager to hand out loans in local currencies and hedge the currency risk at the same time. Neither MFI nor investor will thus be subjected to currency risks.

The successful development of many emerging economies and the ensuing increased local funding of MFIs additionally reduce the liquidity squeeze and credit crunch risk. Even during the financial crisis of 2008, microfinance managed to attract new funds and was one of the few asset classes to yield a positive return during these arduous times.

11.4 STABILITY MECHANISMS

With the aim of supporting the rising returns and further strengthening an already stable microfinance sector, numerous credit bureaus have been launched and the regulatory framework has been pushed on.

Credit bureaus record data of micro entrepreneurs and the terms of their loans with their responsible MFI in order to monitor multiple loans. Institutions such as the Central Bank regulate MFI business activities and structures. The World Bank has further increased its commitment locally to exert more influence on the local microfinance markets in the short and the long run.

Micro insurance is another financial service that further enhances the stability of the system. It covers both micro entrepreneurs and MFIs against loan default. In many cases, the premium of this mandatory insurance makes part of the loan terms and conditions.

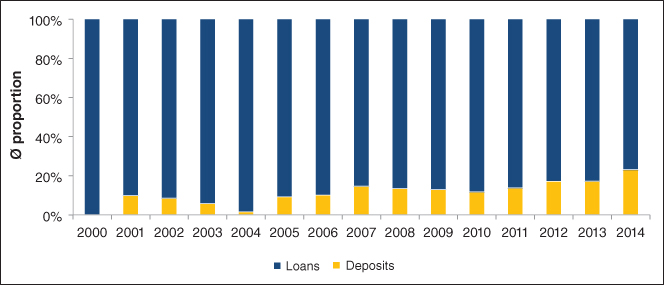

FIGURE 11.5 Deposits Compared to Loans

Data Source: MIX (2016)

Further, regulation enables MFIs to take deposits, much to the benefit of the entire industry. Figure 11.5 reveals that the proportion of deposits in comparison with outstanding loans has been on a steady increase since 2004. This means that MFIs have more financial means at their disposal for lending, and the currency risk can be averted. Most micro entrepreneurs are reliable savers in any case, putting money aside for times of hardship and to support the business they have launched. Saving and borrowing are not by any means a contradiction in terms.

11.5 PRELIMINARY CONCLUSIONS

Microfinance is an overwhelming success story and has unfailingly sustained its two‐digit growth rates all the way through global economic and financial crises, and turbulence in emerging markets.

From a real economy point of view, microfinance most of all benefits from the locally‐bound activities of micro entrepreneurs, which amplify the effects and impact of diversification. From a financial economy perspective, both the intense focus of MFIs on their liquidity situation and appropriate hedging instruments provide a reliable shield against losses.

Credit bureaus and other stability mechanisms have been introduced to prevent crises, and regulation has been tightened. Today, beyond all these measures, specially designed insurance policies additionally protect borrowers and lenders alike.