ENCYCLOPEDIA TOPIC D

Property Ownership Entity

C Corporation: This type of commercial property ownership is subject to double taxation

Very large commercial real estate holding companies often prefer to own commercial property in C corporations because profits are taxed at much lower rates. This makes sense if the company's main goal is to buy more property with the profits. Another advantage applies to owners who own 10 or more properties in the corporation. When they are applying for a loan personally, they do not have to submit balance sheets, profit and loss statements, and K-1s for each property. This is because they receive all property income from the corporation as an employee, and that income is summarized on one W-2 wage statement. Another benefit for large real estate companies is that there is no limit to the number of shareholder investors (S corporations are limited to 100). A further benefit is that the personal liability of shareholders is limited to their percentage of investment in a property.

Owning commercial investment properties in a C corp makes absolutely no sense for a smaller investor who owns less than 10 properties. The main downside to C corporations—double taxation—will hit them hard. Corporate earnings are taxed first and then when earnings are distributed to individual owners, are taxed again on their personal returns. Another negative is that corporate losses cannot be passed on to personal returns. They can only be passed on to the corporation the following year. To avoid double taxation, make sure all corporate profits are paid out as salaries to owners and show the corporation as not making a profit.

Delaware LLC: Why do so many commercial property owners choose to vest their property in a Delaware LLC?

There are many perks to owning your commercial property in a Delaware LLC. You do not need to live in Delaware and the property does not need to be located there, and an LLC can be set up quickly online for a nominal cost, without an attorney. Why is this so popular? Because doing so provides more benefits than forming an LLC in any other state. Here are the top benefits:

- Remaining Anonymous: Many states require you to disclose the names and addresses of all members of the LLC. That information becomes public record and each partner can be solicited. Worse yet, anyone can identify the extent of your real estate wealth. In Delaware, members' contact information is not required to be listed on the certificate of registration. Only the IRS will know the identity of the members.

- Better Safeguard of Your Personal Liability: Although all LLCs provide some personal asset protection from creditors or lawsuits, the Delaware LLC Act provides more protection than any other state by strongly protecting the LLC against its members' creditors.

- Strong Enforcement of the Operating Agreement: Let's say that your operating agreement states that certain members have to perform specific duties and that all members have to contribute cash if certain events occur. With a Delaware LLC, this becomes legally enforceable.

- A Delaware LLC Can Operate in Any State: Your property can be located in any state and you only pay state tax and file in the state in which the property is located.

- Protection from Lawsuits by Minority Investors: As long as the manager is not self-dealing (making decisions that only benefit the manager), they are protected from lawsuits from minority investors. This gives the managing partner the ability to take risks that they deem to be safe.

- A Separate Court for Dispute Resolution: Delaware has a separate court, called the Court of Chancery, to efficiently resolve disputes involving the LLC. Cases are resolved quickly. There are no jury trials and judges are highly experienced in real estate and business cases.

Delaware Statutory Trust (DST): This can be a godsend for 1031 exchange investors who are running out of time to find the right replacement property

If you are a deal sponsor: If you are trying to raise investors to purchase a large high-quality commercial property, owning the property in a Delaware Statutory Trust may be the way to go. Some benefits are that you can use 100 or more investors and that the property does not need to be located in Delaware and the names and contact information of the sponsor and all investors is kept secret. The top advantage is being able to attract 1031 exchange investors who have just sold or are about to sell a property. They can invest the deferred proceeds tax free into owning a pro rata portion of your property as a replacement property. The IRS has given their blessing for DSTs to do just this. Usually investors have to put in a minimum of $100,000, but this is not set in stone. Investors will not own their share as a partner but as an individual owner within the trust. As the sponsor, you become the master tenant and call all the shots. The investors are passive. Another benefit to attracting 1031 exchange investors is that if they are required by the IRS to replace debt, they can meet this requirement as long as the property they are investing in has debt. A plus for these investors is that they do not have to qualify for financing. As the sponsor, you can recoup expenses for the formation of the DST and marketing as well as charge fees for administrating the DST.

For the 1031 Exchange Investor: If you have not been able to identify the right property for your 1031 exchange funds and are running out of time, choosing a high-quality property being offered in a DST could be a blessing and save you a big capital gains tax bill. Also if you have leftover 1031 exchange funds that are taxable after finding a replacement property, consider using them to invest in a DST.

As a Passive Investor: If you do not have 1031 exchange funds to invest, you could also benefit by owning a small piece of a lower-risk large Class A or B institutional-quality commercial property that is being offered in a DST. Annual returns average 5–7%. You will share in the income from operations and appreciation, and also have a share of the depreciation as a tax shelter. Once the property is sold, your annual internal rate of return could be 10% or more, as it includes appreciation.

As an investor in a DST, watch out for sponsors who are offering a share of the property to you by raising the acquisition price higher than the amount they are paying for the property. This is done legally, but is not disclosed. Be sure to ask sponsors for a copy of the original purchase and sales contract. If they will not provide this, they have almost certainly marked up the original price.

General Partnership (GP): Smart sponsors have their general partnerships owned by a corporation

When passive investors own their share of the property in a limited partnership, the sponsor will own their share of the property with other managing partners in a general partnership agreement. Because there is unlimited liability for general partners, these days, most sponsors have them owned by a corporation, which protects them from being personally liable.

A general partnership can have two or more partner/managers, each of whom can make decisions on behalf of the partnership. General partners are usually the managing partner and sign purchase contracts and closing documents, and take on the role of being key principals on loans (applying for financing and signing the loan documents).

Individual Ownership/Sole Proprietorship: This is fast and easy, but leaves the property owner personally liable

It is rare these days that investors choose to own commercial property in individual ownership in a sole proprietorship due to having no asset protection. However, there is no faster or easier way to own a property. Income or loss is reported directly on Schedule E of your 1040 federal tax return. But unlike an LLC, LP, or corporation, there is no protection from personal liability in a sole proprietorship. Sole ownership works best for investment property owners that do not have partners and so can call all the shots. A benefit is that in community property states, they can leave the property to anyone they wish in their will.

Joint Venture Agreement: As sponsor, you can often negotiate a better deal with a joint venture partner

If you are the sponsor bringing in just one partner and you are contributing little or nothing toward the down payment, you will likely get a better deal by doing a joint venture agreement with them. The main advantage is that there is a lot less red tape, and it is common for you to end up with a larger share of the pie than in standard partnerships, where it's expected that each partner's ownership percentage is based on the same percentage of equity they contributed.

In a JV, there is an operating member who is the sponsor (see Encyclopedia Topic C, Raising Investor Partners) that created the deal, and a capital member who is contributing money, a building, or undeveloped land toward the down payment. The capital member usually wants very little responsibility or involvement in the deal. Both parties sign a JV agreement, which states how much equity will be contributed by each, what percentage of ownership each will have, how profits will be distributed, how the property will be managed, what duties each member will have, and what the exit plan is. Each JV partner is liable based on the share of capital they contributed. For asset protection the property is usually owned directly by a single-asset LLC or by a limited partnership (LP).

I have made loans to joint ventures where one party contributed a rundown apartment complex as equity and the other used their expertise and time to rehab and reposition it. Another example is where someone owned a valuable infill lot in Portland but did not have the money or experience to develop it. They did a joint venture with an experienced developer. The down payment for our loan was based solely on the land's value.

Limited Liability Company (LLC): You are fully protected against liability with this

The best, easiest, and least expensive way to own a commercial investment property by yourself or with your partners is to form an LLC. An LLC is the most popular commercial property ownership structure in the United States, so I am including the most detail on it. When many partners are involved, it is strongly advised to have a commercial real estate attorney create the LLC document so that all members are protected. An outstanding benefit of an LLC is that individual owners are protected from liability for the property's debts or lawsuits filed against the property. This type of ownership entity is considered a hybrid because it combines the best traits of an S corporation, a partnership, and a sole proprietorship. An LLC can have one owner or many partners. Another advantage of forming an LLC is that income passes through directly to each member's personal taxes, just like a sole proprietorship. Each partner is given a K-1 at tax time, which shows their pro rata share of the property's annual net income

An LLC's operating agreement, or articles of organization, legally identifies the sponsor as the managing partner and the duties of the other members of the LLC, along with their percentage of ownership. It also defines the financial agreement among partners. It is imperative to have an operating agreement that will prevent any misunderstandings among members as to duties and financial agreements. Also, in the event of any litigation between partners, the court will use the operating agreement to uphold the intent of the members.

Essential Items of the LLC Operating Agreement/Articles of Organization

- Organizational Structure: States when the LLC was formed, its term, purpose, who the members are, what the members' duties are, and what percentage of ownership they have.

- Management and Decision Making: States whether the LLC will be managed by one member or by all members, and what each member's duties are. Also states whether decisions will be made by the manager or by consensus of all of the members. Votes can be assigned equally or according to percentage of ownership.

- Contributions of Capital: States how much each member has contributed at the beginning. Also states what the process will be if cash calls (see in Encyclopedia Topic C, Raising Investor Partners) for additional contributions in the future are needed.

- Distributions of Earnings: States how the profits will be distributed among members of the LLC. Also states whether they will be distributed monthly or quarterly, and what happens if there are losses. Also should address how profits will be distributed if the property is refinanced or sold.

- Changes to Membership: States what happens to a member's ownership share if they sell their interest, die, get divorced, or become mentally or physically disabled or financially insolvent due to bankruptcy.

- Dissolution of the LLC: States how and when the LLC can be dissolved when the property is sold.

- Right of First Purchase: States how members can buy each other out, and how the property will be valued.

- Financial Reporting to Members: States when this will be done—usually annually.

- Involuntary Withdrawal of a Member: States that a member can be removed in the case of death or becoming physically or mentally disabled.

Limited Partnership (LP): If you are a passive investor, this is how you will own your share of the property

A limited partnership has one or more general partners and one or more limited partners. When the sponsor and managing partners own their share of a commercial investment property in a GP, the passive partners, whose only role is to invest money, will own their share as a limited partner. The most attractive benefit of being a limited partner is being free from liability. This does not mean that they cannot lose their original investment should the property fail. It is common for LP agreements to have cash calls where the partners have to provide additional capital under defined circumstances, such as if the property is in need of major repairs. Limited partners are given a rate of return or a preferred rate of return on their investment during the term agreed upon in the LP. Usually the property has to be sold by the general partner when the term expires to return the original investment to the limited partners. At this time, appreciation from the sale of the property is distributed to the limited partners. Income to limited partners is passed through to their individual taxes through K-1s issued by the sponsor or their accountant.

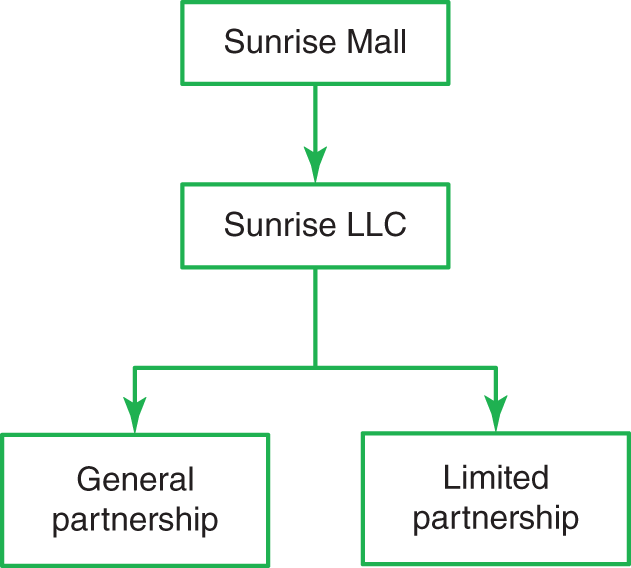

Multiple or Layered Ownership Structure: Most commercial real estate investment properties that have partnerships owned in layered ownership structures

In more complex commercial real estate ownership structures, the property can have two or more layers of ownership entities. For example, a shopping mall could be owned directly by an LLC, which is owned jointly by a GP and an LP, as shown below.

S Corporation: The corporation is not taxed separately. Income is passed directly to the owners' taxes

If you own your commercial property in an S corporation you will not be subject to double taxation. S Corps are not taxed at the corporate level. Income or loss is passed on to the owners' personal taxes. Owners are also protected from personal liability, and earnings are not subject to self-employment taxes if they are taken as owner capital draws instead of W-2 wages. An S corporation is a much more complicated ownership structure for owning commercial real estate. S Corps have shareholders and stockholder meetings for which you're required to take minutes. Owning the property in an LLC is much simpler and gives you the same protection against personal liability.

Often developers that specialize in ground-up construction and plan on selling the property upon completion prefer owning the property in an S corporation. This is also the case for someone whose business is fixing and flipping commercial properties. In both of these cases the income is subject to a self-employment tax, which can be eliminated with an S corporation. Rental income is not subject to a self-employment tax.

Single Asset Ownership Entity: Be sure that your commercial investment property is owned in a single-asset ownership entity

Smart owners of commercial properties practice asset protection. They know to own each of their investment properties in a separate, single-asset ownership entity. This means that that entity owns nothing but the subject property. Smart owners know to never own a property in their name personally, with the exception of their personal residence. This protects them in the event of a lawsuit. If a tenant breaks their hip by tripping on a crack on a walkway at your apartment complex that is owned by a single-asset LLC, they cannot go after you personally or any of your other properties. They can only go after the subject property.

Tenants in Common (TIC): If you have many partners and own your share in a TIC, you can easily sell your share

If you plan on owning commercial property with partners and you want the easiest way to sell your share or pass it on to your heirs, consider owning your share of the property in a tenants-in-common structure. What is unique about a TIC is that each partner can sell their interest without the consent of the other partners. In a TIC, the IRS limits the number of partners to 35. Each one owns a percentage of the property and are entitled to the same percentage of the profits. The partners become cotenants in their ownership. A TIC agreement is drawn up to represent the partners. If a tenant wants to sell their percentage of the property in the future, their partners have the first right to buy it.

On the negative side, if there is a need for a cash injection to pay for expensive repairs it is up to each tenant to decide if they want to participate. If they choose not to, the partners that did contribute will be reimbursed upon a refinance or sale of the property from the shares of the partners who did not participate. Another negative is that all tenants are personally liable for the property and for the loan based on their percentage of ownership. Be sure that your TIC partners have good credit and are financially strong enough to be key principals on the loan. Recourse lenders will require all of the partners to sign the loan documents and the personal guarantees. In the case of a default, if one partner is not on the loan, the lender would not be able to foreclose on their share. Many recourse lenders often do not favor TICs. This is because if there is a default, the lender has to go after each partner individually according to their percentage of ownership.