CHAPTER

TWENTY-EIGHT

AGENCY CMO Z-BONDS

Principal

OffStreet Research LLC

Traditional accrual collateralized mortgage obligation (CMO) bonds in agency deals are long-term bonds structured so that they pay no coupon interest until they begin to pay principal. Instead, the principal balance of an accrual bond is increased by the stated coupon amount on each payment date. Once the earlier classes in the CMO structure have been retired, the accrual bond stops accruing and pays principal and interest as a standard CMO bond. Accrual bonds are commonly called Z-bonds because they are zero-coupon bonds during their accrual phase. Bonds created in this way provide investors with long durations, attractive yields, and protection from reinvestment risk throughout the accrual period. The cash-flow pattern produced is suited to matching long-term liabilities, and, as a result, the bonds are sought after by pension fund managers, life insurance companies, and other investors seeking to lengthen the duration of their portfolios and reduce reinvestment risk.

Z-bonds have been a staple product of the CMO market since its earliest days. The bulk of the Z-bonds currently outstanding are from traditional, sequential-pay CMOs, but the generic structure has adapted well to the PAC-based CMOs favored by the market since the late 1980s, and the inclusion of an accrual bond as the last class continues to be a common practice. At the same time, the Z-bond was the focus of innovation in the CMO market, as issuers created a significant amount of intermediate average life Z-bonds, a growing number of bonds of various average lives that accrue and pay according to a PAC schedule, and bonds that use various conditions or events to turn the accrual mechanism on or off. These innovations expanded the traditional market for Z buyers by improving the stability of Z-bonds’ cash flows, issuing Z-bonds in a wider range of average lives, or by creating bonds that perform well in rallies and preserve their high yields better in declines.

The chapter discusses this important sector of the agency CMO market. We begin with an examination of the mechanics of the traditional Z-bond as well as Z-bonds issued with PACs, and focus on the behavior of these structures in different prepayment scenarios. We also consider the effect Z-bonds have on the other bonds in a CMO, and the relationship between the basic characteristics of the Z-bond and its market properties and economic performance. A discussion then follows of the characteristics of more complex Z-bond structures, such as serial Z-bonds, PAC Zs, and Jump Zs.

An earlier version of this chapter was coauthored with Bruce Mahood.

THE BASIC ACCRUAL STRUCTURE

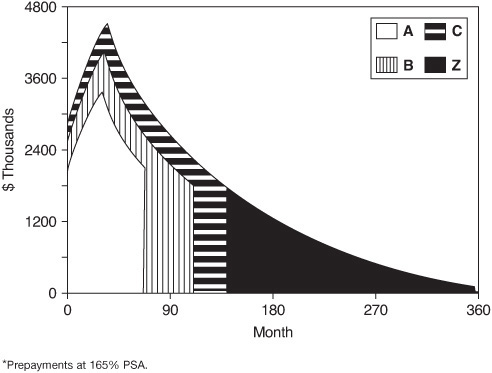

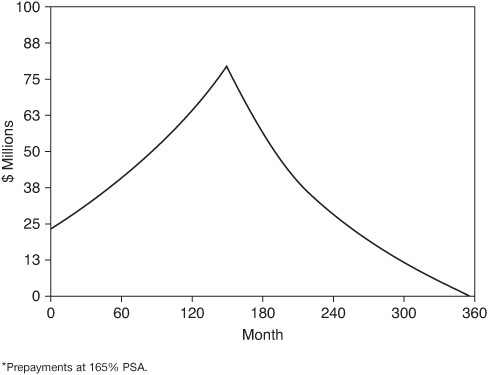

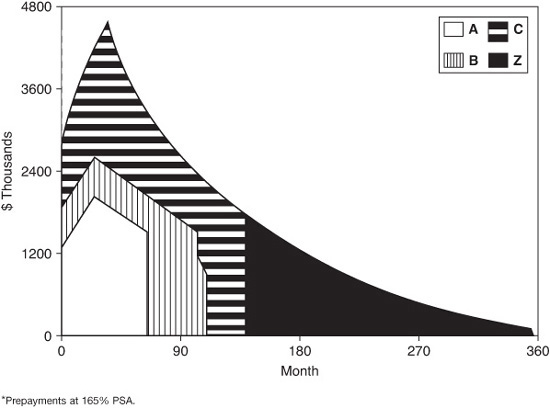

Most Z-bonds have been issued from traditional, sequential pay CMO structures. Typically, they were the last in a four-class bond issue, and had nominal average lives of 20 years. The principal and interest cash flows for a traditional, sequential-pay CMO containing a Z are diagrammed in Exhibit 28–1. As the graph indicates, the first class pays principal and interest until it is retired, at which time the second class begins to paydown. The coupon-paying bonds, Classes A, B, and C, receive payments of interest at their stated coupon rates on their original principal balances. The Z-bond Class Z, however, receives no payments of interest until the preceding classes are fully retired. Instead, its principal balance increases at a compound rate, in effect guaranteeing the bondholder a reinvestment rate equal to the coupon rate during the accrual period, and insulating the investment from reinvestment risk as long as the earlier classes remain outstanding. The principal balance can triple or quadruple in amount over the accrual period projected at issue. This is graphically depicted in Exhibit 28–2, which indicates the growth of the principal balance of the Z-bond in Exhibit 28–1 over its expected life at an assumed constant prepayment speed of 165% PSA. The principal balance of the tranche at issue is $25 million, and grows to a maximum level of $79.5 million by the 150th month. From that point, coinciding with the last payment to the preceding tranche, the balance begins to decline as scheduled amortization and prepayments from the collateral are paid to the bondholders.

EXHIBIT 28–1

Total Principal and Interest Payments of a Traditional Sequential-Pay CMO with a Z-Bond*

EXHIBIT 28–2

Principal Balance of a Z-Bond Over Time—$25 Million Beginning Balance*

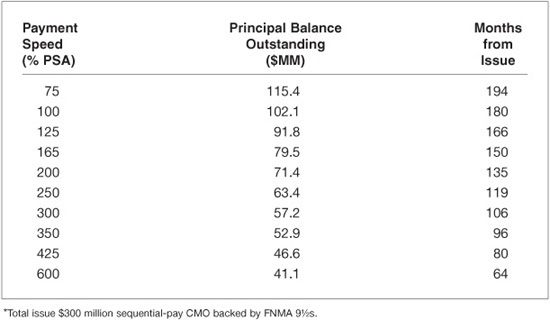

If actual prepayments occur at a faster rate than 165% PSA, the principal balance of class Z at the end of the accrual period will be smaller than the $79.5 million shown in the diagram. Since the earlier tranches pay down sooner, the Z-bond accrues over a shorter period of time, and the total amount of accrued interest is lower. Conversely, slower prepayments allow the Z-bond to accrue for a longer period, resulting in a larger principal balance at the time when the Z-bond begins to generate cash for the bondholders. Principal balances at the end of the accrual period are shown for various constant prepayment speeds in Exhibit 28–3. At the pricing speed of 165% PSA, the balance in this example reaches an amount more than three times the size of the original face amount at issue. At a faster speed of 350% PSA, the original face amount doubles, and at a slower speed, 100% PSA, it quadruples. Likewise, faster prepayments accelerate the receipt of the first payment of principal and interest. In the example, the first payment jumps from halfway into the 12th year at 165% PSA to the beginning of the 9th year at 350% PSA. If prepayments slow to a constant rate of 100% PSA, the first payment to the Z-bond is not made until the beginning of the 16th year after issue.

EXHIBIT 28–3

Effect of Prepayment Speed on the Length for the Accrual Period and the Principal Balance at the end of the Accrual Period of a $25-Million 20-Year Average Life Z-Bond Class*

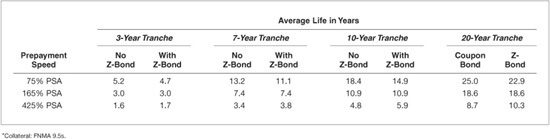

The effect of faster or slower prepayments on the average life and yield of this same example is shown in Exhibit 28–4, under the heading Z-Bond in a Traditional Sequential-Pay CMO. The average life of the Z-bond at the pricing assumption of 165% PSA is about 18.5 years; traditional Zs typically have expected average lives at pricing of 18 to 22 years (and expected accrual periods of 8 to 10 years). If prepayments occur at a constant rate of 100% PSA, the bond lengthens modestly, to an average life of about 22 years. Like other last tranches, the Z has more room to shorten. In this example, the Z shortens to an average life of about 12 years at 350% PSA, and down to about 7.5 years at 600% PSA.1

The yield received on a Z-bond is less sensitive to differences in prepayment speeds the closer to par it is priced. At deeper discounts, Z-bonds, like other discount mortgage-backed securities, will benefit as their average lives shorten, since principal is returned at par earlier than assumed at pricing. The deeper the discount, the sharper the boost in yield at faster prepayment speeds. Conversely, the yield declines as a function of a slowdown in prepayments and the original discount. Traditional 20-year average life Zs have been issued at original prices as low as 30, but prices above 85 currently are more common. In general, issuers can lower the coupon, achieving a more attractive price, by using discount collateral or by stripping interest into another class.

EXHIBIT 28–4

Yield and Average Life at Various Prepayment Speeds of Comparable CMO and 20-Year Average Life Bonds in Structures with and without Z-Bonds (Pricing Assumption: 165% PSA)

HOW THE Z INTERACTS WITH OTHER BONDS IN THE STRUCTURE

The interaction of the Z-bond with earlier bonds in the CMO structure is a key determinant both of its own behavior and that of the other bonds. By including an accrual bond in the CMO structure, issuers accomplish two purposes: (1) a higher proportion of the total issue can consist of tranches with earlier final maturities than if there were no Z-bond in the structure, and (2) the earlier classes have more stable cash flows and average lives across a range of prepayment rates than in a comparable structure without a Z-bond. Furthermore, since the timing of cash flows from the Z-bond depends on when the earlier tranches are retired, the Z-bond itself also is more stable.

An accrual bond supports a larger proportion of early classes because the coupon interest that would have been paid on the outstanding balance of the Z-bond is added to the principal payments from the collateral and used to retire the earlier classes. At the same time, the principal amount of Z-bonds is increased by the dollar amount of interest diverted. Although at first glance this may look like sleight of hand, the accrual procedure maintains a simple algebraic relationship in which the sum of the principal balances of the outstanding bonds always equals the outstanding principal balance of the collateral. The simple numerical example in Exhibit 28–5 illustrates this relationship. In the example, the collateral pays a 10% coupon and a $100 principal balance in ten equal payments. Both Class A and Class Z have stated coupons of 10%, so that the sum of the interest paid to Class A and either accrued or paid to Class Z is always equal to the interest paid by the collateral. (In an actual CMO, there can be a differential between interest on the collateral and the interest paid to the bondholders, which is then payable to the residual holders.) Notice that Class A is paid down more quickly than it would be if the Z were a coupon-paying bond.

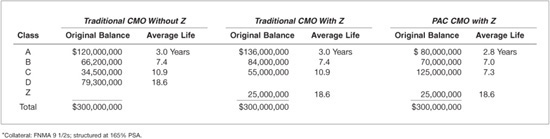

The accrual structure permits issuers to create larger classes with short-and intermediate-term average lives. The effect of an accrual bond on the size of the earlier classes is graphically illustrated in Exhibit 28–6, a diagram of the principal payments only from the CMO in Exhibit 28–1. The discontinuity between the size of principal payments to the Z and those to the earlier tranches reflects the fact that the Z-bond’s pro rata share of coupon interest is treated as principal in order to pay down larger earlier tranches (if the last payment to the fourth would be much smaller). This strategy is attractive to issuers when the CMO arbitrage depends primarily on the shape of the yield-curve, and larger profits can be made the larger the amount of bonds that can be priced off the front end of the yield-curve. In periods when the yield-curve is flat or inverted, this strategy helps issuers minimize the proportion of longer average life bonds in the issue. This works because interest payments from the collateral, which would have been paid to holders of the last tranche, are used to support the first tranche. Just how much of an effect an accrual class can have on the allocation of principal to the earlier classes is shown in Exhibit 28–7. The exhibit compares two four-tranche sequential pay CMOs backed by the same collateral, one with a Z and one without. The four tranches in each issue have the same average lives, roughly 3, 7, 10, and 20 years. (The fourth tranches from these examples, all nominally 20-year bonds, are included as well in Exhibit 28–4.) The two structures differ in the way the collateral’s principal is distributed among the classes. For example, in the Z-bond structure, a $25 million Z-bond class supports a $136 million 3-year first tranche. The structure without a Z-bond has $120 million 3-year bonds in the first class and $79 million 20-year bonds in the fourth tranche.

EXHIBIT 28–5

How a Z-Bond Accrues and Pays: A Simplified Example

EXHIBIT 28–6

Total Principal Payments of a Traditional Sequential-Pay CMO with a Z-Bond*

The accrual mechanism imparts greater stability to all the bonds in a typical structure. This is readily apparent in Exhibit 28–8. Each column compares the average life at different prepayment speeds of the different tranches from the sample structures. In each case, the average lives of the tranches are less variable across all scenarios for the structure containing a Z-bond than in the structure without.

CMOs WITH PACs AND A Z-BOND

The Z-bond has a similar effect on earlier bonds in a typical PAC structure. For a given collateral and pricing assumption, accrual from the Z can be used to support a larger amount of PAC and support bonds in the earlier tranches. The principal and interest payments for a structure containing 3- and 7-year PACs, a 7-year support bond, and a 20-year Z are shown in Exhibit 28–9. The yield and average life at various prepayment levels of the Z-bond from this structure are included in Exhibit 28–4, and the size and average life of the various classes are shown in Exhibit 28–7. (In fact, the average life of the Z-bond is 18.6 years, matching, for the sake of discussion, the average lives of the Z and regular coupon-paying tranches in the other examples.) Funding the earlier classes from the Z-bond’s accrual generally creates a much larger portion of available principal, for a given pricing speed, from which to carve PACs, allowing issuers to increase the size of the PAC classes.

EXHIBIT 28–7

Comparison of Various CMO Structures Created with and without Z-Bonds*

EXHIBIT 28–8

Effect of a Z-bond on the Average Life Variability of the Various Classes in a Traditional Sequential-Pay CMO*

EXHIBIT 28–9

Total Principal and Interest Payments of a CMO with PACs and a Z-Bond*

Since support bonds absorb the prepayment volatility from which the PACs are shielded, the proportion of PACs to support bonds is an important parameter in determining the degree to which the average lives of the support bonds will vary over various prepayment scenarios. The presence of a Z-bond increases the total amount of principal available at the pricing speed to pay both the PACs and the support bonds. This means that, all other factors being equal, more PACs may be issued with less negative effect on the stability of the support bonds. In turn, the length of the accrual period is more stable. Nonetheless, the Z-bonds created to support PAC tranches are necessarily more volatile than Z-bonds in the traditional CMO issues. The truth of this can be seen by comparing the average life at various prepayment speeds of a Z from a PAC structure to those of a Z from a traditional CMO, as was shown in Exhibit 28–4. As is the case with the fourth tranches in the sample traditional deals, this Z also has an average life of 18.6 years at 165% PSA. As the exhibit indicates, the average life of the Z from a PAC structure would extend more significantly as well, since slow prepayment rates will delay the retirement of the support bonds, further extending the accrual period for the Zs. (This effect is obscured by oversimplification of the example.)

If the support bond tranche(s) in front of a Z are targeted amortization class bonds (TACs), the Z may be more volatile than if structured with standard support bonds. When the priorities enforcing the structure require that principal in excess of the TAC (and PAC) payments be paid to the Z, then the Z may begin to receive payments before the support bond TAC is retired. This kind of structure produces a Z that is much more volatile in bull markets than a traditional or support Z-bond. Prepayment speeds fast enough to shorten a traditional 20-year Z to a 10-year can shorten this bond to a 1-year. When they carry a low coupon, these bonds are priced to produce generous returns from accelerating prepayments. Indeed, this is one way to create the bullish Z-bond known as a “Jump Z.” The Jump Z is discussed in greater detail later in this chapter.

PERFORMANCE OF Z-BONDS

The variability in the yield of a Z-bond over a range of prepayment rates gives at best an imperfect indication of the Z’s expected price, and hence, economic performance in different interest rate scenarios. A major drawback of using yield as a measure of a Z-bond’s, or for that matter, any mortgage-backed security’s expected performance is that the calculation of yield-to-maturity presumes that the amount and timing of cash flows are known with certainty and are reinvested over the life of the investment at a rate equal to the yield. In actuality, mortgage-backed securities are more exposed to reinvestment risk than other common fixed income investments. Most CMOs pay both principal and interest monthly. More importantly, prepayments of principal normally accelerate when market rates decline, just as the yields available on reinvestment opportunities are declining. The opposite occurs as market yields rise; prepayments decline, slowing the receipt of principal just as more attractive reinvestment opportunities appear. Z-bonds are protected somewhat from this later source of reinvestment risk, since the reinvestment rate is locked in over the accrual period. They are not fully protected, however. The accrual period is of uncertain length, and when it ends the bonds begin to pay exactly like a coupon-paying CMO bond. For these reasons, yield does not capture the difference in the Z-bond’s performance relative to a security with lower reinvestment risk, such as a Treasury bond that pays only coupons until maturity, or one with a fixed accrual period, such as a Treasury zero.

Prepayment risk also exposes investors to call and extension risk, and these have additional consequences for market value. For mortgage-backed securities purchased at prices above par, the early return of principal at par is a negative event, since less interest is earned over the investment horizon. Reflecting the market’s perception of these risks, the prices of premium coupon CMOs, including Z-bonds, rise more slowly the steeper the decline in interest rates. Investors also are exposed to possible declines in market value when the bond’s average life extends and it shifts outward on a positively sloped yield-curve. When a bond lengthens in an upwardly sloping yield-curve environment, the discount rate applied to the expected cash-flow rises, resulting in a lower market value.

Another characteristic that yield calculations cannot reflect is the call provisions established for CMOs. Newer issues tend to have minimal clean-up call provisions designed to pay off the bonds when the remaining balance falls below a certain low level. The market considers as fairly favorable terms that permit the bonds to be called at par, 10 or 15 years after issue, when the outstanding balance of the tranche has declined by 10% to 20% of its original amount. These also are the most common. Less favorable terms stipulate a higher remaining balance or a shorter period, or both. Investors are advised to carefully examine the call provisions of Z-bonds before trading them.

Z-bonds have considerably longer expected durations than coupon payers with similar average lives because the principal balance grows over time. This can be seen by comparing a Z to a coupon payer with the same principal structure (sequential, support bond, etc.) and similar average life at the same pricing speed. For example, FHLMC 1727 Z, a support Z, and FNMA 93-204 J, a support payer, are both 20-year bonds at 125% PSA (on November 28, 1994) backed by 6.5s. FHLMC 1727 Z has an average life of 20.4 years at 125% PSA, FNMA 93-204 J an average life of 21.5 years. At this speed, the Z-bond has a modified duration of 15.4, while the payer has a modified duration of 9.8. At slower prepayment speeds the divergence is even greater: at 90% PSA the Z-bond has an average life of 23.4, but a duration of 16.7, the payer an average life of 24.0 and duration of 10.3. Only at speeds which significantly shorten the average lives of these support bond structures does the Z-bond’s duration converge to that of the comparable payer. At 250% PSA, the Z-bond shortens to an average life of 6.1 years, with a modified duration of 3.6 and the payer to an average life of 6.2 years with a duration of 3.5. An option-adjusted analysis produces a similar result: The Z has an expected duration of 15.9, the payer 10.0. Given this pattern of price sensitivity, investors should expect Z-bonds on a total return basis to underperform CMO payers and Treasuries with comparable average lives and maturities in bearish scenarios. On the other hand, as a result of the accrual mechanism, Z-bonds tend to outperform comparable Treasury zeroes in rising rate scenarios. In bullish scenarios, the long duration of the Z-bond produces high rates of return, although the Z-bond loses its advantage over comparable securities as it shortens dramatically in more sharply declining yield interest rate scenarios.

MORE FUN WITH ACCRUAL BONDS

Under some market conditions, structurers have made more creative use of the basic accrual mechanism. The variations on the accrual theme include PAC Zs and structures containing an intermediate- as well as long-term Z-bond or a series of Z-bonds of various average lives. Other structures turn the accrual mechanism on and off, depending on the amount of excess principal available after scheduled payments are met. As complex and exotic as these structures may appear at first glance, the same basic principles at work in traditional Z-bonds continue to apply. And in most cases, any additional complexity is accompanied by considerable additional value for investors with particular objectives and investment criteria.

PAC Zs

PAC Zs combine the cash-flow characteristics of a standard Z-bond with the greater certainty of a PAC regarding the amount and timing of actual payments. When prepayments occur within the range defined by the PAC collars, the PAC Z will accrue to a scheduled principal balance over a fixed period and make scheduled payments thereafter. As with more familiar, coupon-paying PACs, any excess cash-flow is absorbed by support bonds as long as they are outstanding. Similarly, the coupon interest earned on the PAC Z’s outstanding balance during the accrual period is used to support earlier classes in the structure, and the balance of the PAC Z is increased by an equal amount. For prepayment levels within the PAC collars, the structure eliminates reinvestment risk over a defined accrual period, and then provides predictable payments until maturity. This structure is particularly well suited to matching liabilities. The fact that PAC Zs are issued in a range of average lives (typically 5, 7, 10, or 20 years) increases their applicability. Furthermore, the call and extension protection provided by the planned payment schedule means that the duration of the investment is less likely to increase as interest rates rise (or decrease as interest rates decline) than is the duration of a standard or support Z. That is to say, the PAC Zs are less negatively convex than standard or support Zs. For this reason, active portfolio managers should consider using the PAC Z to lengthen the duration of their portfolios in anticipation of market upswings.

STRUCTURES WITH MORE THAN ONE Z-BOND

It is also possible to issue two or more Zs from a single structure. Considerable variety is possible in structuring deals with multiple classes of Z-bonds, but two common strategies have been to issue a sequential series of Zs with a range of average lives (5, 7, 10, and 20 years, or 7, 10, 15, and 20 years, for example), or a pair of Z-bonds having intermediate- and long-term average lives (5- and 20-year bonds or 10- and 20-year bonds are common examples). In the case of an intermediate- and long-term average life pair, the bonds do not necessarily pay in sequence, but more typically pay down before and after intervening coupon-paying classes. Both strategies have been employed in traditional CMOs as well as in structures containing PAC bonds.

In general, multiple accrual classes in a CMO interact with the rest of the structure in the same way a single traditional Z-bond does, supporting the repayment of earlier classes, which themselves may either pay current-coupon interest or accrue it. In a series of Zs, the longer Zs lend stability to the shorter Zs, just as they would to coupon-paying bonds with earlier final maturities. Accrual from the later Zs can be used to retire earlier Zs when they become current-paying bonds, just as if they were coupon-paying bonds.

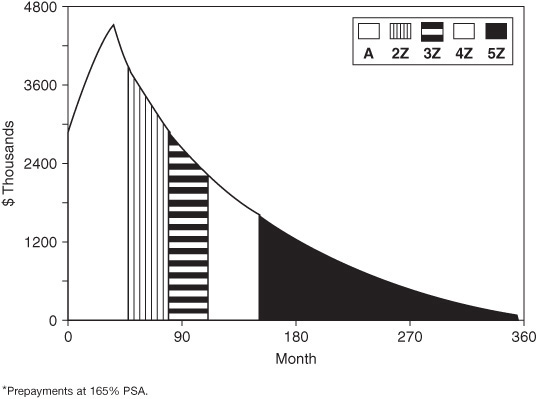

The cash flows from a sequential-pay CMO containing a series of 5-, 7-, 10-, and 20-year Zs preceded by a 2-year coupon-paying tranche are shown in Exhibit 28–10. This example was constructed using the same collateral and pricing speed as in the previous examples containing a single Z. The last tranche, 5Z, is the same size as in the previous example as well, and for this reason has the same average life at various prepayment speeds. For the sake of discussion, the first tranche is also the same size as the first tranche in the traditional CMO with a Z-bond, $136 million. As indicated in Exhibit 28–11, the large amount of accrual bonds in the structure has the effect of shortening the average life of this bond from 3 years at 165% PSA in the single Z example, to 2 years in this. (Readers will note that this example is not necessarily realistic. Structurers would be concerned to issue larger amounts of short-term average life bonds that can be sold at lower yields for greater arbitrage profits, manipulating the coupon and offer price, and so forth.) Exhibit 28–11 lists the average lives of the first five classes at various prepayment speeds. In general, intermediate-term Zs demonstrate considerable stability. This is more evident when the 7- and 10-year Zs are compared to the 7- and 10-year coupon-paying bonds from earlier examples in Exhibit 28–8. The 10-year is supported by a 20-year Z, and is noticeably less variable than one in a CMO without a Z. As would be expected, given the larger amount of accrual being passed to successively shorter bonds in the current example, the 5-year Z-bond is considerably more stable than a comparable 5-year standard payer supported by a single Z. The general result is that the shorter Zs in a series of Zs are “cleaner,” that is, they have progressively less average life variability than otherwise comparable coupon-paying bonds. Intermediate-term average life Zs interspersed among coupon-paying classes in a structure supported by a 20-year Z (the other common strategy) will benefit similarly. They will be more stable than otherwise, and the degree of stability will depend on the size of the Z-bond supporting them.

EXHIBIT 28–10

Total Principal and Interest Payments of a Sequential-Pay CMO with a Series of Z-Bonds*

EXHIBIT 28–11

Average Lives at Various Prepayment Speeds of the Bonds in a Sequential-Pay CMO with a Series of Z-Bonds

The consequences of multiple-Z strategies are that they produce bonds possessing relatively stable cash-flow patterns—not as stable as PACs with decent collars, but more stable than traditional sequential-pay bonds. These stable bonds also possess the partial shield against reinvestment risk that is a chief attraction of traditional Z-bonds, and they make it available in any array of expected lives, broadening the appeal of Z-bonds to investors with intermediate- rather than long-term horizons.

Tricky Zs

Another twist is the “trick” Z, in which the accrual mechanism is turned on or off under certain conditions. One such condition might be a date; for example, the rule of allocating cash flows between classes might be “accrue until such and such a date” instead of the traditional “accrue until A, B, and C tranches are retired.” Or, the decision to accrue the Z-bond might depend on the amount of principal available to make payments to the nonaccrual bonds currently paying. The use of such rules results in bonds with performance characteristics that can be very different from the Z-bonds discussed previously.

CMO issuers have tinkered with the accrual mechanism of Z-bonds to create CMO classes that alternate between paying interest and accruing interest. These special-purpose classes are structured with a set of rules that turn their accrual mechanism on or off according to certain cash-flow conditions. These accrual rules are often designed to help preceding classes meet their cash-flow schedules and/or expected maturity dates. For example, issuers included these variable-accrual bonds in CMO structures to help earlier classes meet the 5-year maturity requirement for inclusion in thrift liquidity portfolios. These benevolent Zs pay as follows: when cash flows from the mortgage collateral are insufficiently large enough to retire the liquidity bonds according to schedule, their accrual mechanisms are turned on and corresponding coupon from the collateral is applied to the earlier classes; when cash flows are sufficient to retire the liquidity bonds on schedule, their accrual mechanisms are turned off and the bonds act like standard coupon payers. Incorporating a conditional accrual rule into a bond class is an effective way to reduce extension risk on earlier classes. Of course, the extension risk is not eliminated but is instead largely transferred to the benevolent Z and other, later bond classes.

Another wrinkle is to permanently transform Z-bonds into coupon-paying bonds when certain cash-flow levels are met. An early example of this Z-bond structure was issued as the last of nine classes in FNMA 89-15. This bond was not marketed with any distinguishing label. The other bonds in the structure were a series of PACs and TACs followed by a support bond dubbed an “S” bond. The Z-bond pays as follows: any excess above the scheduled PAC and TAC payments is distributed to the Z-bond as an interest payment; if the amount is lower than the amount that was accrued, the shortfall is accrued; if the amount is greater, the excess is distributed as principal; beginning in the month following the first payment of a complete interest payment, the so-called Z class distributes interest each month. As a consequence, one month of exceptional prepayment experience could trigger the conversion to coupon bond. Thereafter, the average life would be shorter than it would otherwise have been, owing to the fact that a portion of its cash flows is dispersed over what would have been the accrual period. Any protection against reinvestment risk offered by this “chameleon” bond is ephemeral at best. Once converted, the bond behaves like any other support bond.

Even PAC Zs have been subjected to genetic alteration. The first PAC Z issued, the fifth tranche in Ryland Acceptance Corporation Four, Series 88, for example, accrued only until the date of its first scheduled payment or until non-PAC classes in the deal had been retired. Until that date, the PAC Z was the first PAC in line for excess cash flows should the support bonds be paid down, and after that date, the last in line. This meant it had greater call risk during the accrual period. As a result, its average life was only stable at or below the pricing speed. The resultant average life volatility was more typical of a reverse TAC, which does not extend, but has considerable call risk.

Jump Zs

Another Z-bond innovation is the jump Z. Generically, the jump Z is a bullish support Z-bond that is designed to convert to a current payer and to be paid down from excess principal when prepayments accelerate. Under bullish scenarios, this bond “jumps” ahead of other bond classes in the order of priority for receiving from principal payments. Once triggered, a jump Z typically receives all excess principal (above scheduled PAC payments) until it is retired. Conceivably, holders of the jump Z could receive these payments early in the expected accrual period. This acceleration of principal can shorten the bond’s average life significantly: A Z-bond issued with a 20-year average life might shorten to less than 1 year. Since these bonds typically have low coupons and are issued at significant discounts to par (in the eighties), jump Z holders realize high returns in a rally. In general, a jump Z priced at a deeper discount traded at a tighter spread, because investors assigned more value to the jump feature. Many investors purchased jump Zs to offset the negative convexity of their other mortgage securities and to enhance the performance of their mortgage-backed securities portfolios in bullish scenarios.

Jump Z-bonds have been issued with an extremely diverse set of jump rules. Although apparently lacking uniformity or standardization, these rules have the common objective of increasing the bonds’ performance in bullish economic environments. Jumps can be activated by an event associated with a market rally: rising prepayment rates, declining interest rates, or increased cash-flow. However, most jump Zs were structured with prepayment triggers: The bonds shortened when prepayment rates on the underlying mortgage collateral rose above a CMO’s pricing speed or some other predefined prepayment level. Generally, prepayments above the pricing speed shortened the average life of the jump Z considerably. In structures containing TAC bonds, jump Zs were often designed to shorten when prepayments exceed the speed that defines the TAC schedule. In addition to prepayment triggers, CMO issuers also structured jump Zs with interest rate triggers that were activated when Treasury yields fall below some threshold level. Interest rate triggers eliminated the need for investors to accurately forecast prepayment rates, and ensured that jump Z holders would benefit even in a market rally that was not accompanied by rising prepayments. In general, the closer the jump trigger is to actual prepayment speeds or current interest rates, the more valuable the jump Z.

Jump Z-bonds can be classified as cumulative or noncumulative, as well as “sticky” or “nonsticky.” A cumulative trigger is activated when since-issuance prepayment rates, or other cumulative measures of prepayment experience, exceed some threshold value. In contrast, a noncumulative trigger only requires prepayments to satisfy the jump condition during a single period. Holders generally prefer noncumulative triggers, since a single month of abnormally high prepayments could force early retirement of their discount security. The adjectives stick and nonstick indicate whether a jump Z-bond will revert back to its original priority in the CMO structure if jump conditions are no longer met. Once triggered, a sticky Z will continue to receive principal payments, even if prepayments subsequently decline below the threshold value. On the other hand, a nonsticky Z can revert back to an accrual bond once its jump rules are no longer satisfied. Holders generally assign the greatest value to jump Zs with noncumulative sticky triggers, because a single increase in monthly prepayment rates could force early retirement of the entire bond class. For jump Zs backed by unseasoned mortgage collateral, a tiny increase in prepayments could trigger a jump: A small increase in CPR can translate into a large PSA spike when prepayments are benchmarked off the early part of the PSA ramp.

The other common approach for creating a jump Z-bond—preceding it with a TAC and other support bonds in a PAC structure—was described earlier. The jump Z acts like a traditional support bond and absorbs volatility from both PACs and TACs. Preceded by a TAC, the jump Z receives principal when principal payments from the underlying collateral and Z accrual exceed the amount required to meet the PAC and TAC schedules. The degree to which the bond’s average life will shorten depends on its jump rules and the overall deal structure. Jump rules control whether the bond jumps in front of the TAC class when payments break the TAC schedule (sticky Z) or receives only excess payments above the PAC and TAC schedules (nonsticky Z). All else being equal, the average life of a sticky Z is likely to shorten more than a comparable nonsticky Z. Preceded by PACs, TACs, and other support bonds, these jump Zs have a negligible amount of extension risk since they are typically structured as the last support class in the CMO. In addition to their jump rules, the average life variability of jump Zs is also affected by the features of their preceding PAC bonds. For example, PAC lockouts, typically 1 to 2 years in length, can accentuate the shortening of jump-Z average lives. Since no scheduled principal payments are made during a lockout, there is a much larger amount of cash-flow available to pay down a jump Z in the event it is triggered.

This simple form of jump Z (simple to visualize and analyze) does not involve any modification of the standard accrual mechanism: The Z’s share of interest is added to principal payments used to pay down earlier bonds according to the schedules and order of priorities established for the deal. Some early jump Zs, however, had modified accrual mechanisms that imposed conditions under which accrual would be turned on or off. These rules can control how coupon interest is paid both before and after the bonds have jumped. Perhaps the most common example of accrual manipulation occurs with jump Zs that pay only a portion of their coupon interest and accrue the shortfall. The exact amount of interest that a jump Z will pay, after being triggered, often depends on the number and size of the support classes that the bond jumped over. For example, when preceded by both Level I and II PACs, the amount of coupon interest paid to a jump Z-bond will depend on whether it jumps over the secondary PACs. If the jump Z remains subordinate to the Level II PACs, then part of the jump Z’s coupon interest can be used to support the second-tier PACs.

KEY POINTS

• Traditional accrual bonds in a CMO structure, commonly referred to as Z-bonds, are structured so that they pay no coupon interest until they begin to pay principal.

• Z-bonds offer investors some of the longest durations and highest yields available in the derivative mortgage-backed securities market, as well as a cash-flow pattern well suited to matching long-term liabilities.

• The interaction of the Z-bond with earlier bonds in the CMO structure is a key determinant both of its own behavior and that of the other bonds in the structure.

• Numerous innovations have been introduced that provide accrual bonds with desirable investment characteristics, including greater stability or accelerated return of principal in rallies, and have widened the availability of intermediate-term Zs.