Chapter 16

Example STP Flows of Equity Agency Trades – When Execution Venue is the London Stock Exchange

16.1 INTRODUCTION

There are a very large number of potential trade flows for equities, as the flow will vary according to whether the customer is an institutional investor or a private investor, and also according to what stock exchange the order is executed on. It is therefore not possible to provide examples of all the potential STP flows of equity trades in all the world’s major markets.

Two examples are provided in this chapter, in each case the order is to be executed on the London Stock Exchange. The examples are:

1. An agency trade with an institutional customer

2. An agency trade with a retail customer in the United Kingdom.

The chapter finishes by examining the growth of orders being executed using Direct Market Access (DMA).

16.1.1 Background to the London Stock Exchange and its trading platforms

In section 7.6.2 we learned that stock exchanges provide order-driven trading platforms, quote-driven trading platforms and hybrid trading platforms. Post-MiFID, the London Stock Exchange provides the following trading platforms.

LSE trading platforms for UK domestic securities

- SETS (hybrid platform): SETS is the London Stock Exchange’s hybrid trading service that combines electronic order-driven trading throughout the day with integrated market maker liquidity provision, delivering guaranteed two-way prices. It is used to trade all securities in the FTSE All Share Index as well as the more liquid AIM securities.

- SETSqx (hybrid platform): SETSqx (Stock Exchange Electronic Trading Service – quotes and crosses) supports four electronic auctions a day (at 08.00am, 11.00am, 15.00pm and 16.35pm) along with continuous standalone quote-driven market making. It is used to trade all UK domestic equities not traded on SETS.

- SEAQ (quote-driven platform): SEAQ is the quote-driven platform for fixed interest market and AIM securities not traded on either SETS or SETSqx.

LSE trading platforms for non-UK securities

- International Order Book (order-driven platform): An electronic order book for trading depository receipts.

- International Bulletin Board (order-driven platform): An electronic order book for trading international securities with a secondary listing on the London Stock Exchange.

- EUROSETS (order-driven system): Dutch trading service offering secondary market trading in liquid, large and mid-cap Dutch equities in the AEX and AMX indices.

- European Quoting Service (quote driven platform): Market making and trade reporting service for liquid MiFID securities not quoted on another exchange service.

Settlement agents involved in LSE trades and default value dates

All trades that are matched on the order book in an order-driven or hybrid platform need to be novated as the trade parties are anonymous. Therefore, all securities that are eligible for trading on the LSE’s order-driven and hybrid platforms are cleared, novated and netted by the LSE’s central counterparty, LCH.Clearnet Limited. Securities that are only eligible for trading on the LSE’s quote-driven markets (where trade parties are not anonymous to each other) are not cleared by LCH.Clearnet Limited.

All trades on the LSE, whether or not they are cleared by LCH.Clearnet Limited, are settled by the CSD for the UK – Euroclear UK and Ireland.

The default value date for transactions matched on an order queue is T + 3.

16.2 EQUITY AGENCY TRADES WITH INSTITUTIONAL INVESTOR CUSTOMERS

16.2.1 Process overview

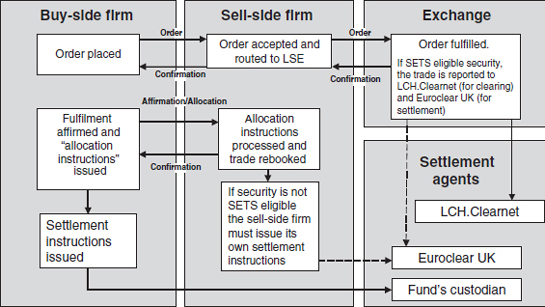

The process overview is summarised in Figure 16.1.

Figure 16.1 Process overview: LSE institutional agency trade

The figure shows two potential routes for the sell-side firm’s settlement instructions, depending on whether or not LCH.Clearnet has cleared and novated the trade.

16.2.2 Order placement

Orders may be placed by any of the following means:

- By telephone or fax

- By entering the order details into a secure web page provided by the sell-side firm

- By sending the sell-side firms a SWIFT message. SWIFT is covered more fully in section 11.1

- By entering the order details directly into the sell-side firm’s order management system. Typically, this would be facilitated by using a third-party “hub and spoke” order routing service. Providers of such services include Omgeo, Thomson Financial, Reuters and Bloomberg

- By using direct market access – see section 16.4.

16.2.3 Order execution

The sell-side firm will have already decided to execute this trade in an agency capacity on the LSE. It will have decided this using its execution policy that is a requirement of the MiFID regulations. This requirement was examined in section 8.4.2.

The sell-side firm will charge the customer the same price that it obtained on the exchange, plus a commission for its services. The investor may also need to pay certain charges. If the trade is a purchase by the investor, then the end investor will also need to pay the stamp duty which was explained in section 10.7. If the trade (whether it is a purchase or a sale) has a principal value of GBP 10 000.00 or more, then the investor will need to pay PTM levy, which was also explained in section 10.7. These fees will be collected by the sell-side firm and held in a balance sheet account of the type “fees and charges”. The sell-side firm will then be debited for these amounts by the CSD, who will pay them to the appropriate authorities.

16.2.4 Trade amounts

Example

On 4 February 2008 for value date 7 February 2008 ABC Investment Bank executed an agency trade on behalf of XYZ Fund Managers. XYZ purchased 10 000 shares in Megacorp at £1.50 per share, ABC charged XYZ a commission of 0.50% of the principal value.

The trade amounts are as shown in Table 16.1.

Table 16.1 Trade amounts for agency purchase on LSE

| Principal amount | 10 000 shares | Number of shares |

| Trade price | £1.50 | Price per share |

| Commission rate | 0.50% | |

| Principal value | GBP 15 000.00 | Principal amount * Trade price |

| Commission | GBP 75.00 | Principal amount * Commission rate |

| Stamp duty | GBP 75.00 | Principal amount * Stamp duty rate |

| PTM levy | GBP 1.00 | The PTM levy is always £1.00 |

| Customer-side trade consideration (of XYZ’s trade with ABC) | GBP 15 151.00 | Sum of principal value + Commissions + Fees |

| Market-side trade consideration (of ABC’s trade with the exchange) | GBP 15 000.00 | Principal value |

16.2.5 Trade agreement

For institutional equity trades, agreement between the buy-side firm and the sell-side firm will normally use the confirmation, affirmation and allocation model that was examined in section 12.1.2. For the market-side trade, the exchange acts as a central matching engine.

16.2.6 Regulatory trade reporting

Regulatory trade reporting is achieved by the exchange acting as a central matching engine.

16.2.7 Settlement

Market-side settlement

If the security is SETS eligible, then the exchange will report the trade both to LCH.Clearnet, who will clear it, novate it and settle it and to Euroclear UK and Ireland who will settle the net liability for that security by the member firms concerned. If it is not SETS eligible, then the sell-side firm that is executing it and the market maker that it dealt with will both need to issue settlement instructions.

Customer-side settlement

The buy-side firm (XYZ) will need to issue a settlement instruction to its custodian to receive 10 000 shares in Megacorp from ABC against payment of GBP 15 151.00 on value date 7 February 2008, and the sell-side firm (ABC) will need to issue instructions to Euroclear UK and Ireland to deliver 10 000 shares in Megacorp from XYZ against payment of GBP 15 151.00 on value date 7 February 2008. The format of the settlement instructions and the formats of the status and settlement messages that the settlement agents might send to the trade parties were provided in section 12.2.

16.2.8 General ledger postings for the trade and the settlement

Trade dated postings

Using the example trade in section 16.2.4 the entries passed by ABC Investment Bank on trade date will be as shown in Table 16.2.

Table 16.2 Trade date entries: institutional equity purchase

16.2.9 Settlement date postings

The sell-side firm expects that both sides of the trade will settle on the same day. However, this is not guaranteed as there could be an STP exception on either the market side or the customer side. On the date that the trades do settle (assuming that they settle in full) the entries – for the market side trade – where ABC has to pay for the securities – will be as shown in Table 16.3.

Table 16.3 Market-side settlement date entries

For the customer-side trade – where ABC will receive payment for the securities – the entries will be as shown in Table 16.4.

Table 16.4 Customer-side settlement date entries

16.2.10 Stock record postings for the trade and the settlement

Trade date postings

The postings on trade date will be as shown in Table 16.5.

Table 16.5 Stock record postings on trade date

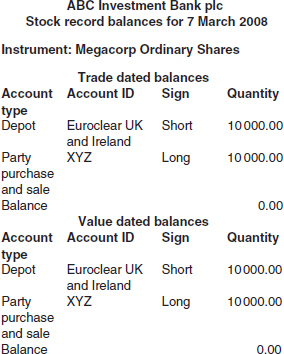

As a result of these stock record postings, the stock record will look like Figure 16.2, reflecting the fact that on a trade dated basis ABC owes stock to XYZ and is owed stock by its market counterparty.

Figure 16.2 Stock record on trade date

Settlement date postings

The postings that are made on the date that the trades settle will be as shown in Table 16.6.

Table 16.6 Stock record postings on settlement date

If the market-side trader settled on time but the customer-side trade failed, then the stock record for 7 March would look like Figure 16.3.

Figure 16.3 The stock record on settlement date

The stock record is therefore now reflecting the fact that:

1. The market counterparty has delivered the 10 000 shares to our Euroclear account.

2. We owe the shares to XYZ, and if there were a dividend or a corporate action with a record date on any date prior to the actual settlement date then ABC will owe the proceeds to XYZ. Dividend and corporate actions processing are examined in sections 23.5 and 23.6.

16.3 EQUITY AGENCY TRADES WITH PRIVATE INVESTOR CUSTOMERS

16.3.1 Order placement

Specialist securities firms that deal with the private investor may be known as private client stockbrokers, private banks or wealth managers. As stated in section 7.4, these firms often act in a discretionary capacity, which means that the firm itself generates the orders on behalf of the investor. In addition, firms of this type usually provide a safe-custody service for their clients, which means that securities are not normally delivered to them. When private investors place the orders themselves (rather than rely on their broker using its discretionary authority) they will normally use one of the following methods:

- By telephone

- By entering the order into a web portal provided by the firm concerned.

There are a number of significant differences between the way that orders are placed by private individuals and the way that orders are placed by buy-side firms acting for institutional investors:

1. Buy-side firms normally place orders in terms of an express share quantity, e.g. “buy (or sell) 1000 Tesco shares”; while retail customers may express the order in the same terms or may instead express a buy order as “Invest £1000 in Tesco” or a sell order as “sell £1000 worth of Tesco”. £1000 in this context is the consideration (the net amount payable or receivable by the customer including commissions and fees).

2. Buy-side firms are usually content to express orders in terms of “at best” or “at limit” and wait for the confirmation message to tell it the exact price of the trade, but retail investors expect price certainty – they want to know the exact price of the shares concerned before they will agree to the order being executed.

3. Many retail investors have difficulty in meeting the T + 3 value date convention, as the UK banking system is not yet geared up for making relatively low value payments within three business days. If they want to pay the broker by cheque there is both a postal delay and a cheque clearing delay; if they want to pay using a debit card, then this form of payment usually clears on T + 4.

These issues make it impractical for the broker receiving the order to place it on the SETS queue, because:

1. There is no price certainty on SETS at the point of order – only when the order is matched.

2. There is no facility in SETS to enter an order in terms of its consideration – SETS orders can only be entered in terms of nominal amounts.

3. All SETS trades settle on T + 3.

As a result of these issues, private client brokers have developed web portals that are used both by clients entering trades directly and by the brokers’ own call centre staff taking telephone orders that are able to:

1. Interface with software provided by retail service providers (RSPs). RSPs are specialist principal dealers that:

- Guarantee prices at the point of order entry

- Provide extended settlement facilities – normal value date is usually T + 10.

2. Poll all the RSPs and determine which one is offering the best price.

3. Given the price supplied by the most competitive RSP, the target consideration supplied by the investor, the broker’s commission schedule and the rules and rates of stamp duty and PTM levy, calculate the nominal amount that the client needs to buy or sell.

4. Provide a secure web portal for the investor to enter and authorise the order, and submit debit card or bank details to the broker.

The LSE defines RSPs on its website as:

An RSP is an automated quoting system similar to a computerised market maker – it is electronically connected to brokers who normally request quotes from several RSPs and trade on the best price.

- RSPs trade in a principal capacity (i.e. trade on their own account) and these off book executions must be traded under the rules of, and reported to, a Recognised Organisation (investment exchanges recognised by the FSA and overseas equivalents) such as the London Stock Exchange.

- Though a broker is treated as a market counterparty and therefore can trade at any price, RSPs take on the best execution responsibility owed to a typical private investor and will always, at least, match the best bid and offer (BBO or touch) displayed by the Exchange.

This form of trading is aimed primarily at private investors, so maximum dealing sizes are restricted and there is no direct interaction with the order book.

16.3.2 Order execution

Figure 16.4 shows the interactions between the user of a web portal, the private client broker’s systems and the RSP’s systems.

Figure 16.4 Execution of an order with an RSP

16.3.3 Trade agreement

The trade agreement for the customer-side trade is that the broker sends the customer a confirmation message (by post and/or email) and the customer takes no action if he agrees to its contents. The trade agreement process for the market-side trade is that the exchange acts as a central matching engine.

16.3.4 Regulatory trade reporting

Regulatory trade reporting is achieved by the exchange acting as a central matching engine.

16.3.5 Settlement

Market-side settlement

If the security is SETS eligible, then the exchange will report the trade both to LCH.Clearnet, who will clear it, novate it and settle it, and to Euroclear UK and Ireland, who will settle the net liability for that security by the member firms concerned. If it is not SETS eligible, then both the broker and the RSP need to submit settlement instructions to Euroclear. The settlement messages sent to and received from the firm’s settlement agents were described in section 12.2.

Customer-side settlement

The investor takes no action. Because the normal practice is for the brokers to hold the securities in custody for the investor, in the case of a purchase by the investor the broker needs to issue an instruction to transfer the securities from its main depot account at Euroclear to its safe custody depot at Euroclear on value date. If the investor has sold, then the broker needs to issue an instruction to Euroclear to transfer the securities from its safe custody depot account at Euroclear to its main depot account.

Some investors may not wish the broker to hold the securities in custody on their behalf. They may require the securities to be registered in their name, in which case a physical certificate should be printed by the registrar and sent to them. If this is required, then for a purchase the broker needs to issue a stock transfer form to Euroclear which it will pass on to the registrar concerned.

If the investor is selling certificated securities, then most brokers will require physical delivery of the certificates in advance of processing the order so that they are not exposed to credit risk or delivery risk. When the broker has received the certificates and processed the order it will need to send the stock transfer form (signed by the client) to Euroclear.

16.3.6 General ledger postings for the trade and the settlement

The general ledger postings for a retail trade on trade date and settlement date are the same as those for an institutional agency trade. Refer to sections 16.2.8 and 16.2.9.

16.3.7 Stock record postings for the trade and the settlement

Trade date

The stock record postings on trade date for this type of trade are the same as those for an institutional agency trade. Refer to Section 16.2.10.

Settlement date postings

Assuming that the broker is holding the securities in custody for the client, the postings that are made on the date that the trades settle will be as shown in Table 16.7.

Table 16.7 Stock record postings on settlement date – safe custody purchase

If this were a safe-custody sale then the signs would be reversed. The stock record after settlement of a customer purchase of 10 000 shares now looks like Figure 16.5.

Figure 16.5 Stock record after safe-custody settlement activity

The stock record now reflects the fact that this firm has to credit the customer with any dividends, coupons or corporate action proceeds while we are holding the securities in custody on its behalf.

16.4 DIRECT MARKET ACCESS

16.4.1 Introduction

Direct Market Access (DMA) is defined as the automated process of routing a securities order directly to an execution venue, therefore avoiding intervention by a third party. Execution venues include exchanges, alternative trading systems and electronic communication networks. To simplify, DMA enables the buy-side firm or investor to place orders directly onto the order queues of investment exchanges, avoiding the need to submit the order to an exchange member firm in the traditional manner described in section 16.2.

DMA has the potential to “cut out the middleman”; or to put it another way, to disintermediate the exchange member firm. However, many of the providers of DMA services are themselves exchange member firms, others are technology suppliers that have acquired exchange membership for the purposes of opening it to investor clients.

One of the original drivers for the growth of DMA was the growth of algorithmic trading, which is defined as the “placing a buy or sell order of a defined quantity into a quantitative model that automatically generates the timing of orders and the size of orders based on goals specified by the parameters and constraints of the algorithm”. If an investor is using algorithmic trading technology, then the timing of the order to the second is critical. Conventional order flow techniques are simply too slow to have the desired result. In addition, DMA is a more anonymous way of trading – it allows hedge funds in particular to offload large quantities of stock without tipping off the market.

DMA is available for listed futures and options as well as securities.

According to a survey conducted in 2004 by the Tower Group, DMA accounted for 33% of all orders originated by buy-side firms in the USA in that year. This was up from just 11% in 2000, and Tower Group expected DMA to account for 40% of all US-originated orders by the end of 2006. They found that commissions on DMA orders averaged only about one cent per share. For this reason, many sell-side firms were offering a range of services to their DMA customers including the supply of algorithmic trading analytics, often as part of a prime brokerage service. In the past few years, many investment firms have opened up their DMA trading platforms to private investors.

16.4.2 DMA technology

At the simplest level, DMA is just access to the sell-side firm’s order execution technology. DMA changes the way that orders are placed and executed, but not the way they are agreed, reported to regulators, settled or accounted for.

There are a number of specialised DMA package applications available on the market, and a number of traditional front-office system packages have been adapted to provide DMA.