Chapter 19

The STP Flow of Futures and Options Transactions

19.1 INTRODUCTION

The examples in this section are based on futures and options listed on the Euronext.LIFFE exchange in London, which will be cleared by LCH.Clearnet Limited. However, the general principles that are described in the examples apply to all listed derivatives traded on any exchange, but when listed derivatives are traded on other exchanges the names of the exchanges, clearing houses and systems involved will vary from those used in the examples.

The following process steps are identical for futures and options:

- Order placement

- Order execution

- Trade agreement

- Regulatory trade reporting

- Settlement

- Mark to market

- Accrual of interest on collateral placed or received.

However, the trade amounts, as well as the general ledger and stock record posting process steps are different. Therefore the common processes are examined in section 19.2, and the instrument-specific process steps are examined in sections 19.3 for futures and section 19.4 for options.

19.2 FUTURES AND OPTIONS – COMMON PROCESS STEPS

19.2.1 Order placement

As each futures or options contract is unique to the exchange that developed it, the investor needs to submit the order to a sell-side firm that is a member of the exchange concerned. This may be achieved by any one of the following means:

- By telephone or fax

- By entering the order details into a secure web page provided by the sell-side firm

- By sending the sell-side firms a SWIFT message. SWIFT is covered more fully in section 11.1.

- By entering the order details directly into the sell-side firm’s order management system. Typically, this would be facilitated by using a third-party “hub and spoke” order routing service. Providers of such services include Omgeo, Thomson Financial, Reuters and Bloomberg.

- By using direct market access – see section 16.4.

19.2.2 Order execution

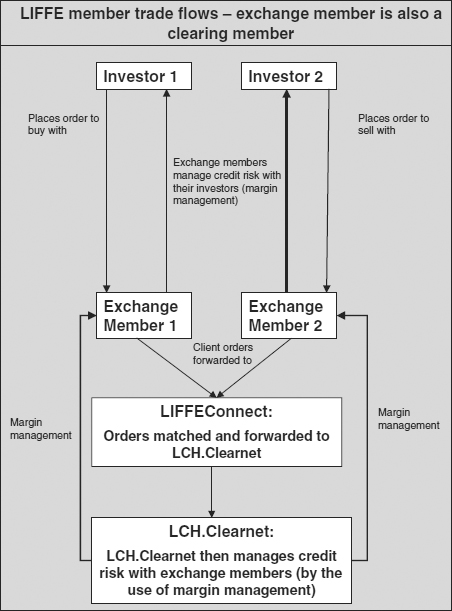

The order will always be executed by the sell-side firm as an agent. The process steps are explained by Figure 19.1, which was first seen in section 7.7.1:

Figure 19.1 LIFFE member trade flow

1. The investor places its order with the exchange member firm.

2. The member firm then places it on the order queue maintained by LIFFEConnect™; the order-driven platform run by Euronext.LIFFE.

3. As soon as the order is matched on LIFFEConnect, then LIFFEConnect:

- Informs the exchange member, who in turn needs to inform the investor

- Informs LCH.Clearnet, who then novates the trade.

19.2.3 Trade agreement

Trade agreement between the member firm and the exchange is facilitated by the exchange acting as a central matching engine. Trade agreement between the member firm and its client may be achieved by any or all of the following methods:

- The confirmation, affirmation and allocation model using FIX protocol messages

- Sending an email, fax or mail confirmation to the investor or sell-side firm and relying on the investor to take action only if it disagrees with its content

- Mutual exchange of confirmations via SWIFT – this method of trade agreement is little used for exchange traded contracts.

19.2.4 Regulatory trade reporting

Regulatory trade reporting is achieved by the exchange acting as a central matching engine.

19.2.5 Settlement

Because the trade party in an order-driven market is anonymous, all settlement obligations have been novated by LCH.Clearnet Limited.

All the messages between the parties, the exchange and the clearing house will use message formats and APIs supplied by the exchange and clearing house. SWIFT and FIX standards do not apply.

Note that the exchange member firm is not necessarily a member of the clearing house. A firm that is a non-clearing member of an exchange will deal with a general clearing member of the exchange who is in turn a member of the clearing house. The relationships between the parties involved where trades are cleared by a third-party clearer were examined in section 7.7.1.

19.2.6 Marking to market

Positions in exchange traded futures and options should be marked to market each day as explained in section 23.8, using the closing prices published by the exchange concerned.

19.2.7 Interest accrual

Interest should be accrued on any collateral placed or received. Interest accrual is explained in section 23.9.

19.3 FUTURES-SPECIFIC PROCESS STEPS

19.3.1 Trade amounts

Example

ABC Investment Bank sells 10 lots of the LIFFE FTSE June 2008 Index future on a date when the value of the index is 6500. As, according to LIFFE’s contract specification, 1 lot of the FTSE index future is worth £10 per index point we can extend the notional principal amount of the trade as:

Nominal amount * Price * Price multiplier/Price divisor = Notional principal

i.e.

10 lots * 6500 * 10/1 = 650 000.00

Margin and collateral calculations

Assuming that the clearing house requires an initial margin of 10% of notional principal,1 then there will be an initial margin payable to the clearing house of GBP 65 000.00.

If, on T + 1, the price of the index has risen to 6600, then the clearing house will require ABC to deposit additional margin with a value of GBP 10 000.00, calculated as:

Notional principal at close today = Notional principal on previous working day

These calculations are summarised in Table 19.1.

Table 19.1 Futures trade amounts

| Trade amount Date | Trade date | Trade date +1 |

| Lots sold | 10.00 | 10.00 |

| Price | 6500.00 | 6600.00 |

| Position | –10.00 | –10.00 |

| Price multiplier | 10.00 | 10.00 |

| Price divisor | 1.00 | 1.00 |

| Notional principal amount | –650 000.00 | –660 000.00 |

| Initial margin rate | 10.00% | n/a |

| Initial margin amount | –65 000.00 | n/a |

| Maintenance margin | 0.00 | –10 000.00 |

| Exchange fee (assume £1 per lot) | 10.00 | n/a |

| Clearing fee (assume £1 per lot) | 10.00 | n/a |

19.3.2 General ledger postings

The only general ledger entries to be posted are concerned with the deposit of collateral and the payment of exchange and clearing house fees. The entry for the payment of the initial margin and fees to the clearing house on trade date is as shown in Table 19.2. and the entry for the payment of variation margin on T + 1 is as shown in Table 19.3.

Table 19.2 Futures account postings on trade date – market side

Table 19.3 Futures account postings for payment of maintenance margin – market side

If ABC Investment Bank was processing the trade on behalf of an investor, then it would need to ask the investor for collateral, and to process “mirror images” of these entries to reflect its position versus the investor (see Tables 19.4 and 19.5).

Table 19.4 Futures account postings on trade date – customer side

Table 19.5 Futures account postings for payment of maintenance margin – customer side

Collateral can of course be supplied in the form of securities instead of cash. Clearing houses accept high rated liquid government bonds as collateral. If securities were used instead, then the entry would be passed in the stock record, see section 19.4.2 for an example of such an entry.

19.3.3 Stock record postings

Postings to reflect the establishment of the position

The entry to be passed on trade date is as shown in Table 19.6.

Table 19.6 Stock record posting to establish a futures or options position

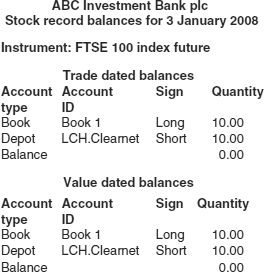

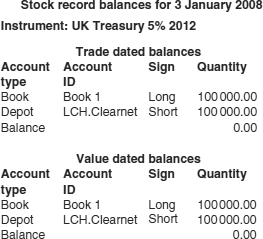

After posting this entry, the stock record now looks like Figure 19.2.

Figure 19.2 Stock record on completion of posting

Postings to reflect the use of securities as collateral

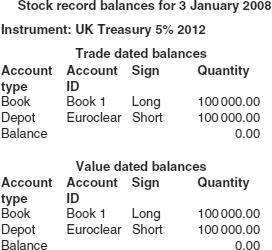

A government security could be used instead of cash to provide collateral. If this were the case, and ABC used 100 000 of the bond concerned as collateral, then the stock record before collateral was placed for the security concerned might look like Figure 19.3.

Figure 19.3 Stock record before collateral deposit

If collateral is to be used then Euroclear will need to be instructed to deliver it to LCH.Clearnet, and the entry shown in Table 19.7 (known as depot transfer) must be passed in ABC’s stock record.

Table 19.7 Stock collateral entry

And the stock record for the government bond would now be as shown in Figure 19.4.

Figure 19.4 Stock record after collateral deposit

19.4 OPTIONS-SPECIFIC PROCESS STEPS

19.4.1 Trade amounts

Example

ABC Investment Bank sells 10 lots of a call option on the FTSE 100 index with a strike price of GBP 8176.00 and an option premium price of GBP 110.75 per lot. As, according to LIFFE’s contract specification, 1 lot of the FTSE index future is worth £10 per index point we can extend the principal amount of the trade as:

Nominal amount * Price * Price multiplier/Price divisor = Principal

i.e.

10 lots * 110.75 * 10/1 = 11 075.00

Margin and collateral calculations

Assuming that the clearing house requires an initial margin of 10% of notional principal, then there will be an initial margin payable to the clearing house of GBP 1 107.50.

If, on T + 1, the price of the option has risen to GBP 115.00, then the clearing house will require ABC to deposit additional margin with a value of GBP 425.00, calculated as:

Notional principal at close today = Notional principal on previous working day

These trade amounts are summarised in Table 19.8.

Table 19.8 Options trade amounts

| Trade amount Date | Trade date | Trade date +1 |

| Strike price | 6 175.00 | 6 175.00 |

| Option price | 110.75 | 115.00 |

| Lots sold | 10.00 | 10.00 |

| Position | –10.00 | –10.00 |

| Price multiplier | 10.00 | 10.00 |

| Price divisor | 1.00 | 1.00 |

| Principal amount | –11 075.00 | –11500.00 |

| Initial margin rate | 10.00% | n/a |

| Initial margin amount | –1 107.50 | n/a |

| Maintenance margin | 0.00 | –425.00 |

| Exchange fee (assume £1 per lot) | 10.00 | n/a |

| Clearing fee (assume £1 per lot) | 10.00 | n/a |

19.4.2 General ledger postings

The trade date entries for the example trade in section 19.4.1 will be as shown in Table 19.9.

Table 19.9 Options account postings on trade date – market side

And the entries to reflect the payment of maintenance margin will be as shown in Table 19.10.

Table 19.10 Futures account postings for payment of maintenance margin – market side

If ABC executed this trade on behalf of a client, then they may also need to process the further “customer-side” entries that were shown in Tables 10.3 and 10.4, with the trade amounts relevant to this example.

19.4.3 Stock record postings

The stock record postings for options are the same as those for futures.

1 Initial margin calculations are, in fact, more complex than this as they will be based on a SPAN margin calculation covering all the positions held by ABC Investment Bank for this exchange and clearing house. The assumption of 10% was made simply because a figure needs to be provided for section 19.3.3.