Chapter 21

Stock Lending, Repos and Funding

21.1 INTRODUCTION

As well as being bought and sold, securities may be lent and borrowed, and also used as collateral for firms that need to borrow cash. There are two broad categories of transactions of this type – stock loans and repos. The word repo is short for sale and repurchase agreement.

The term “stock lending” is usually used to describe a transaction where:

1. The motivation of the borrower (of stock) is to acquire a specific quantity of a given stock to meet a commitment to deliver.

2. The motivation of the lender (of stock) is to provide the securities the borrower requires, and to attract collateral to protect itself against default.

A repo transaction, by contrast, is one where:

1. The motivation of the lender (of stock) is to borrow cash at a better rate of interest than it would if it borrowed on an unsecured basis.

2. The motivation of the borrower (of stock) is to lend cash on a secured basis.

In other words the business purpose of a stock loan is to enable one party to lend securities to another, and the business purpose of a repo is to allow one party to use securities as collateral for its cash borrowing. In processing terms the two transaction types share the following characteristics:

- They both use collateral to reduce the lender’s credit risk

- They both employ the concepts of nominal ownership and beneficial ownership which preserve the lenders rights to any income or other benefits provided by ownership of the security being lent.

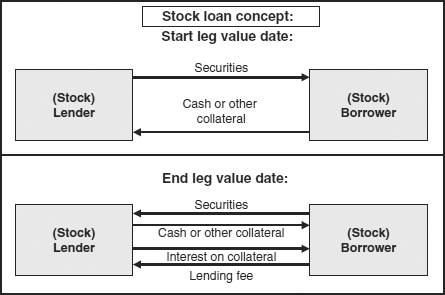

21.1.1 Stock loan conceptual example

The underlying concept behind a stock loan may be expressed by Figure 21.1

Figure 21.1 Stock loan conceptual example

The transaction has a start leg and an end leg. On the value date of the start leg the lender delivers securities to the borrower in exchange for collateral. The purpose of the cash collateral is to provide the lender with security in case the borrower does not return the securities that were borrowed. On the value date of the end leg the securities are returned to the borrower and the collateral is returned to the lender. At the same time, the lender is paid a lending fee, and the borrower is paid interest on the collateral.

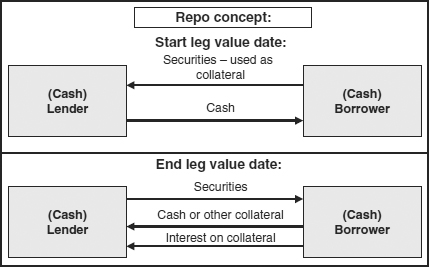

21.1.2 Repo conceptual example

Conceptually, a repo is slightly different, as shown by Figure 21.2.

Figure 21.2 Repo conceptual example

The repo also involves an exchange of cash for securities in both legs of the transaction, but this time the lender of cash is using the securities as collateral in case the borrower is unable to return the cash at the end of the loan period.

This exchange of cash for securities in both transaction legs is the underlying principle of all forms of stock loan and repo, but there are a number of differences between different forms of transactions which are examined in the appropriate sections of this chapter. However, the principle is that the lender of securities is also the borrower of cash and the borrower of securities is also the lender of cash.

Stock lending is a large and growing business. The international trade organisation for the securities lending industry is the International Securities Lending Association (ISLA). According to a June 2004 survey, their members had EUR 5.99 billion worth of securities available for lending. In the US, the Risk Management Association publishes quarterly surveys among its (US-based) members. In June 2005, these had USD 5.77 billion worth of securities available.

21.1.3 Who are the borrowers and why do they borrow securities?

Investment firms borrow securities for a number of reasons, including:

1. They have sold short, and therefore need to borrow stock in order to settle their sales on the correct value date. Market makers sell short as part of their function of providing liquidity to the market, but stock may also be sold short because the seller expects the price of the stock to fall, and therefore it will be able to buy it back later at a lower price.

2. Hedge funds in particular use stock lending as part of strategies to influence the management of the company concerned; particularly in matters relating to mergers and acquisitions. If a hedge fund borrows stock, then it can vote the borrowed stock at company meetings.

3. Any buy-side or sell-side firm may have a situation where securities that it has bought cannot be delivered for some reason. If they have, in turn, sold the stock to another party, then they of course will be unable to deliver what they have not received. They therefore borrow stock to cover for delivery failures.

21.1.4 Who are the lenders and why do they lend securities?

1. Traditional fund managers do not sell short, and are sometimes referred to as “long only” fund managers in this context. They are prepared to lend stock because of the fee they receive for doing so.

2. The fee they receive has to be offset against the interest they pay on the collateral they hold, so it may seem that the returns are not great. However, the fund manager is then able to reinvest the collateral and so enhance the total return of the fund.

3. Market makers have to finance their inventory of long positions. One of the ways they can do this is to use those long positions as collateral for funds they borrow to finance their trading books. If they supply securities as collateral, then they will normally expect to pay a lower rate of interest than if they had no collateral to supply. For example, ABC Investment Bank may be rated Baa by Moody’s, and with this rating it would expect to pay 6% interest on a bank loan. However, if it supplies securities issued by the US government as collateral, then because the US government is rated Aaa it might be able to attract funds at 5.5%.

4. Central banks use repos to provide liquidity to financial institutions. They will lend cash to the institutions in the country for which they are responsible, provided that the institutions supply securities as collateral.

5. Settlement agents lend securities to their customers in order to earn fees for providing the service.

21.1.5 Legal and beneficial ownership

Under UK law, the borrower of the securities becomes the nominal owner of them – if the securities are in registered form, then they are registered in the name of the borrower; if they are in certificated form, then the name of the borrower appears on the certificate.

The rights of the lender are protected, however, as it remains the beneficial owner, which means that although the borrower receives all dividends, coupons and any other corporate action proceeds that are paid during the period of the loan, it has an obligation to repay any proceeds received of this kind to the lender.

There is no doubt in law about the responsibility of the borrower to return any benefits paid to it during the course of the loan to the lender.

However, the borrower also acquires the right to vote at any company meetings that take place during the life of the loan. This is why hedge funds borrow stock to influence the companies whose shares have been borrowed. There is considerable debate about whether this practice is good for corporate governance. In January 2004 Paul Myners produced a report “Review of the impediments to voting UK shares”, one of the conclusions of which was:

[Beneficial owners] should also have a clear voting policy and be aware of the implications of other activities and arrangements on their ability to exercise voting rights. For example, stocklending affects the voting rights attached to the shares, as the lender does not retain the right to vote. When a resolution is contentious I recommend that the stock lent is automatically recalled, unless there are good economic reasons for not doing so.

21.1.6 Collateral and margin

Both stock lending and repo transactions require the borrower to pay collateral to the lender. Collateral may be supplied in one of three forms:

- Cash

- Other securities to the same value as the amount borrowed

- A letter of credit.

21.1.7 Cash as collateral

Where cash is supplied, then the two parties agree that the amount of cash should be equal to the market value of the securities (including accrued interest to the start leg value date) plus a “safety margin” known as haircut.

The lender of the securities pays interest on this collateral to the borrower. During the life of the transaction the securities lent and the collateral placed are revalued each day. If the value of the securities lent has increased, then the lender can demand that the borrower supplies it with additional collateral in the form of a margin payment. This is illustrated by the sample transaction in section 21.2.1.

21.1.8 Securities as collateral

In the case of a stock loan, instead of supplying cash as collateral, the borrower may supply other securities as collateral provided that they have the same or higher market value as the cash. Lenders may have other requirements in this respect, for example they may specify that the securities have to be government bonds issued by an OECD country or corporate bonds issued by companies resident in an OECD country with a specified minimum credit rating.

In the case of a repo it is cash that is borrowed, and securities are normally used as collateral. Lenders (of cash in this context) usually have quite stringent specifications as to which securities they are prepared to accept as collateral.

Use of multiple securities

Both transaction types support the possibility of using more than one security as collateral at the same time.

Collateral substitution

When securities are supplied as collateral, they may be substituted during the life of the transaction. If the borrower finds that it needs the securities it has supplied to be returned (usually because it has sold them) it may agree for the original securities to be returned and replaced with other securities of a similar quality and value.

21.1.9 Letters of credit as collateral

In this context a letter of credit is a document issued by the borrower’s bank that essentially acts as an irrevocable guarantee of payment to the lender, should the borrower not be in a position to return the securities.

Understandably, most lenders prefer cash. Therefore there is a role for specialised stock lending intermediaries, one of whose functions is to convert non-cash collateral to cash collateral. The role of the intermediaries is examined in section 21.5.

21.2 STOCK LENDING AND BORROWING TRANSACTIONS

Stock lending and borrowing transactions may involve just one borrower and one lender, or they may involve a borrower, a lender and a lending intermediary. One of the main differences between stock loans and repos is that for stock loans, the lender is paid a fee for lending the stock. There is no such fee involved in a repo transaction.

Stock loans may be agreed for a fixed period (term loans) or for an indefinite period (notice loans). Many types of securities may be borrowed and lent including a wide range of government bonds, corporate bonds and equities of all kinds.

21.2.1 A simple stock lending transaction

Stock loans can be complex transactions, especially if they use securities or letters of credit as collateral but this example transaction covers all the common elements of such a trade:

1. On 3 March 2008, XYZ Fund Managers agrees to lend 10 000 shares in Tesco plc to ABC Investment Bank “until further notice”. Value date for the commencement of the loan is agreed as 6 March 2008. On 3 March, the bid price of Tesco shares is £5.00 per share.

2. The parties agree that:

- ABC is to supply XYZ with collateral of 102% of the current market price of Tesco, in the form of cash. XYZ will pay ABC 5% interest on this cash; calculated on an actual/365 day basis. The 2% difference between the market value and the collateral required is known as the “haircut”

- ABC will pay XYZ £0.001 per share per day lending fee.

- The settlement of the interest and the lending fee will be netted against each other when the loan is concluded, or on 1 April, whichever is the earlier.

- If the price of Tesco rises above £5.00 per share, XYZ has the right to ask ABC to make a margin payment of 10 000 shares * (market price – £5.00) * 102%.

3. The loan starts, as agreed, on 6 March.

4. On 17 March, the price of Tesco rises to £6.00 per share, and XYZ asks ABC to make a margin payment on 18 March.

5. On 24 March, the two parties agree to terminate the loan, with value 25 March.

Such a transaction would cause the deliveries of securities and payments of cash by the two parties shown in Figure 21.3. The example shows only a single price change, on 17 March, but in the real world the securities lent would be revalued each day, and this might cause additional margin payments to be made every working day if the price of Tesco shares were rising, or collateral to be refunded if the price were falling. Additional margin payments may be made in cash, or, if the original collateral was placed in the form of securities, by depositing additional securities with the lender.

We can summarise these cash flows as follows:

Figure 21.3 Simple stock lending transaction

Cash value of start leg = Market value of amount borrowed + Haircut

Cash value of end leg = Cash value of start leg * (1 + (Interest rate % * Interest days/Interest year) – Agreed lending fee per day * Duration of transaction)

21.2.2 Automated lending services provided by settlement agents

Settlement agents such as CSDs, ICSDs and custodian banks offer automatic borrowing and lending services to those participants that require them. If the agent sees that Member A is unable to deliver 500 shares of a particular stock to meet a sale commitment, it will find another participant (Member B) that can lend the stock to Member A. Member A will be charged a fee by the agent, the majority of which will be paid to the other party. When the agent sees that Member A no longer needs the borrowing, it will automatically be repaid to Member B. Members A and B are unaware of each other’s identity, and in the event of the default of Member A, the agent has to purchase the stock to return to B. For this reason, members that wish to participate in automated borrowing services have to “pledge” their depot positions to the agent. In other words, the member firm’s entire depot positions in all securities are treated as collateral. This allows the agent, in the event of default by Member A, to sell any securities in its account to provide the funds to purchase the stock that has to be returned to the lender.

21.3 REPO TRANSACTIONS

Repo is short for “sale and repurchase”, and as its name implies it is a sale of stock with an agreement to repurchase it at a later date and:

- The seller is lending (or selling) stock and borrowing cash

- The purchaser is borrowing (or buying) stock and lending cash – from this party’s perspective, the transaction is known as a “reverse repo”.

Because the aim of the transaction is to reduce the interest costs of the lender, a much smaller range of securities is acceptable to purchasers. The repo market is mainly concerned with highly rated government debt.

There are two forms of repo transaction – classic repo and buy-sellback.

21.3.1 Classic repo

Classic repo example

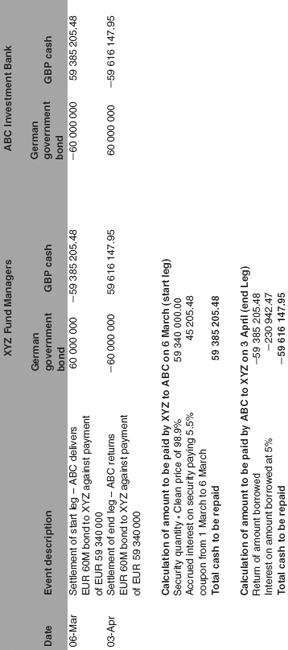

On trade date 3 March 2008 ABC Investment Bank enters into a repo agreement with XYZ Fund Managers. ABC is the borrower of cash and XYZ is the lender of cash.

ABC wishes to use EUR 60 000 000 face value of a German government bond paying a 5.5% annual coupon on 1 March each year as collateral. Coupons on this bond are calculated on the actual/actual basis:

Value date of the start leg is 6 March 2008

Value date of the end leg is 3 April 2008

The clean market price of the government bond on trade date is 98.9%

The two parties agree the repo rate (the interest on the cash borrowing at 5%), calculated on the actual/360 basis.

Such a transaction would cause the deliveries of securities and payments of cash by the two parties shown in Figure 21.4.

Figure 21.4 Simple classic repo transaction

We can summarise these cash flows as follows:

Cash value of start leg = Nominal amount of bond * (Clean price + Accrued coupon)/100

Cash value of end leg = Cash value of start leg * (1+ Repo rate% * Repo days/Repo year)

In this example, we have started with a nominal amount of a bond, and given the market price and coupon rate of that bond we have calculated that ABC is able to borrow EUR 59 385 205.48.

This would be useful if the seller (cash borrower) wanted to fund a position in this particular security, but many repo deals are predicated on the fact that a seller (cash borrower) wishes to use repos to raise an amount of cash to fund positions in general. In that case, the parties need to calculate the nominal amount of the bond that is to be used in the transaction.

The formula for calculating “cash-driven repos” is:

Nominal amount required = Cash amount to be borrowed/Dirty bond price on trade date

Hence if a firm wished to borrow EUR 100 000 000.00 using the same government bond that has a clean price of 98.9% then the calculation is:

Nominal of EUR 101 122234.50 = 100 000 000/0.989

This nominal amount would of course need to be rounded up or down to the nearest denomination in which this particular bond can be traded and settled.

Other characteristics of classic repos

- Fixed date or notice: Like stock loans, classic repos may be for either a fixed term or “until further notice”.

- Haircuts: Classic repo trades, like stock loans, also include a haircut. This is not shown in the example in Figure 21.4 for the sake of simplicity.

- Margin calls: Both trade parties to a classic repo manage credit risk by issuing margin calls to each other. The seller will require extra cash if the price of the security rises; the buyer can require extra securities if the price falls.

- Collateral substitution: This is possible for classic repos.

- No separate stock lending fee: Unlike stock loans, classic repos do not involve the buyer (lender of cash) paying the seller a stock lending fee. The only charge payable is the interest on the amount borrowed calculated at the repo rate.

21.3.2 Buy-sellback

A buy-sellback is a form of repo where the two legs of the transaction (although they are dealt on the same trade date) are treated as separate transactions, and the purchaser does not directly pass any coupon payments back to the seller. Instead, the price of the second leg is adjusted by the value of the coupon that the seller did not receive.

The cash values of each leg of a buy-sellback transaction that did not involve a coupon period during its term are identical to those of a classic repo, but the calculation of the trade price is expressed using the following formulae:

End-leg clean price = End-leg dirty price – Accrued coupon to end leg value date = Cash repaid at the end/Bond nominal amount * 100 – Accrued coupon to end data

- Fixed date or notice: Buy-sellbacks are always for a fixed period, open transactions are not permitted.

- Haircuts: Buy-sellbacks, like classic repos and stock loans, may include a haircut.

- Margin calls: As the two legs of the transaction are not linked, it is not possible for either party to issue margin calls to the other party. As a result, both parties may be exposed to a higher degree of credit risk than in the other transaction types.

- Collateral substitution is not possible for buy-sellbacks.

- No separate stock lending fee: Unlike stock loans, buy-sellbacks do not involve the buyer (lender of cash) paying the seller a stock lending fee.

- Single security per transaction: Unlike classic repos and stock loans, buy-sellbacks can only be concerned with a single security per transaction.

- Coupon compensation: In the case of stock loans and classic repos, the nominal owner makes a separate payment to the beneficial owner of any coupon proceeds received by the (stock) borrower during the life of the transaction. For buy-sellbacks, however, the end leg cash amount repayable is adjusted as follows.

Without a coupon payment the formula would be:

End leg cash amount = Cash value of end leg = Cash value of start leg * (1 + repo rate% * Repo days/Repo year)

But this is now adjusted to become:

End leg cash amount = Cash value of start leg * (1 + Repo rate% * Repo days/Repo year) – Coupon received * (1 + Repo rate * Days from date of coupon payment to repo maturity/Days in year)

Deliveries by value

Securities firms of all kinds, but market makers in particular, often want to use their whole inventory as collateral to fund that inventory. Their problem is determining which stock they can lend. They are obviously not in a position to lend stock that they need to deliver today for their sales that reach value today. CSDs operate a special service for such firms, called delivery by value (DbV). The way that DbV works is that the market maker and a specialised intermediary (see section 21.5) agree that the market maker needs to borrow, say, £10 000 000 to finance its trading book “overnight” (i.e. for one day). Both parties input a special DbV transaction that just quotes this amount, and the collateral amount (say, £10 500 000 including haircut) that the intermediary needs. That evening the CSD selects securities to the value of £10.5 million in the market maker’s account that are:

1. Not needed for delivery to clients; and

2. Do not have a record date or payment date for coupons, dividends or corporate action proceeds today

and transfers them, against payment, to the intermediary’s account. The following day the CSD returns the securities to the market maker and the cash to the intermediary. The market maker then re-evaluates its funding requirements for the next day and the process is repeated.

In essence, then, a delivery by value (although it is technically considered as a stock loan rather than a repo) can be thought of as a fixed term repo for one day where multiple securities of many kinds (not just highly rated government bonds) are acceptable as collateral.

Tri-party repo

Settlement agents also provide tri-party repo facilities for their customers, where they act as the “third-party” custodian for the securities held as collateral. Instead of delivering the securities to the buyer, the seller delivers them to the third party, which acts as the buyer’s custodian. The advantages of tri-party are:

- Administrative simplicity, especially for fund managers and corporates who may lack the administrative and systems capabilities that banks use to process repos

- Easier administration of collateral substitutions and margin calls.

However, there is a disadvantage to the buyer. Because the seller does not itself hold the collateral, and the buyer can substitute collateral so easily, the buyer is unable to use the securities in a reverse repo transaction.

The services offered by the third-party settlement agent include:

- Providing daily collateral valuation reports to both the buyer and the seller

- Ensuring that the securities used as collateral conform to the buyer’s requirements for currency of issue, credit rating, haircut and liquidity.

All tri-party fees are paid by the seller.

21.4 SUMMARY OF THE DIFFERENCES BETWEEN THE VARIOUS TRANSACTION TYPES

The differences between the various transaction types examined in this chapter can be summarised in Table 21.1.

Table 21.1 Summary of transaction attributes

21.5 THE ROLE OF SPECIALIST LENDING INTERMEDIARIES (SLIs)

There are a number of firms that act as specialist lending intermediaries (SLIs). There are several reasons why their presence is required. Let us extend the examples in sections 21.2.1 and 21.3.1 to see how their presence makes a deeper and more liquid market.

The examples both covered two parties dealing direct with each other for a short period for relatively small transactions. This could only be possible if ABC and XYZ know of each other’s existence, but it is often the case that a borrower is not aware of the identities of the potential lenders. But if ABC wanted to borrow 1 million Tesco shares for seven months and use German government bonds as collateral then it might run into some or all of these problems:

1. It can’t find a lender willing to lend such a large amount

2. It can’t find a lender willing to lend for such a long period

3. It can’t find a lender prepared to accept non-cash collateral

4. It may become aware of a suitable lender, but it has no credit information about that lender, and neither does the lender have any credit information about ABC Investment Bank. As neither party has granted a credit limit (credit limits are examined in section 24.5.1) to the other, it may not be possible to carry out the transaction very swiftly.

In any of these circumstances, it can put the lending request to an SLI. SLIs include stock lending divisions of investment banks, as well as specialist niche firms. SLIs have a list of fund manager clients who are prepared to lend securities and will divide a large loan request into a number of smaller parcels, and/or for shorter periods. If one of its clients needs its stock back after, say, one month, then it will reassign that part of the loan to another client.

It also deals with the problem that the borrower doesn’t want to provide cash collateral, but the lenders insist on it. It takes the government bond and does a repo transaction with it with the cash to provide to the lenders.

SLIs act as principal in transactions, making a small margin on collateral interest rates and stock lending fees. Because they act as principal, then their customers only need to grant a single trading party credit limit – to the SLI itself.

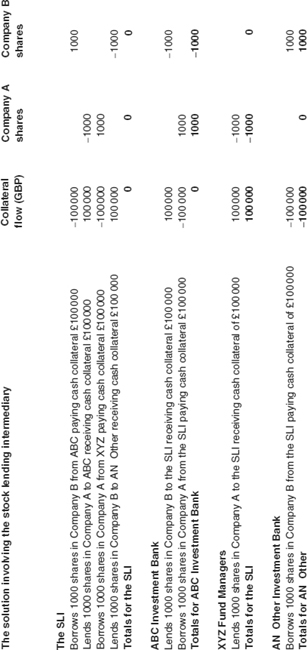

The following example shows how the SLI would meet the requirements of three of its customers by carrying out a series of linked stock lending transactions.

The scenario

1. ABC Investment Bank wishes to borrow 1000 shares in Company A. It is not willing to provide cash collateral but is willing to provide 1000 shares in Company B.

2. XYZ Fund Managers is willing to lend 1000 shares in Company A but insists on GBP 100 000 cash collateral.

3. AN Other & Co. wishes to borrow 1000 shares in Company B and is prepared to provide GBP 100 000 in collateral.

Assume that 1 share in Company A has the same (constant) price as 1 share in Company B.

The SLI will act as party to the stock lending transactions shown in Figure 21.5. As a result of these transactions, both ABC and AN Other are able to borrow the stock they require, ABC’s transactions are neutral in terms of cash collateral and XYZ gets the cash collateral it requires. All the transactions are neutral from the SLI’s perspective – it holds no cash or security positions. The type of operation that the SLI is running is often known as “matchbook lending”.

Figure 21.5 Linked transactions involving an SLI

On a larger scale, this is the type of activity that the SLI is doing when it borrows stock in the delivery-by-value transaction that was described earlier in this chapter.

21.6 BUSINESS APPLICATIONS TO SUPPORT STOCK LENDING AND REPOS

Firms that are active in the stock lending and repo markets often use dedicated front-office applications to support these activities. In other firms, the functionality may be provided by the main settlement system.

The key requirements of the application used to support these activities are the abilities to:

- Project future cash flow

- Project future depot positions

- Mark borrowed, lent and repo positions to market

- Support the relevant messages to trade parties and settlement agents

- Post the appropriate financial accounting entries in the general ledger

- Post the appropriate stock movement entries in the stock record.

21.6.1 Cash flow projections

Once the settlement instructions for all trade types have been sent out, both trade parties have to ensure that they will have the cash available to pay for their purchases, and the stock available to deliver for their sales.

However, the aims of cash management are broader than this. Cash flow management aims to optimise the use of the firm’s cash, so that:

- Overdrawn nostro accounts are avoided wherever possible. Positions should instead be funded by repos or money market loans which generally charge a lower rate of interest than an overdraft.

- If it is not possible to avoid overdrafts, the overdrawn balances are held on accounts that charge the lowest rates of interest.

- Excessively large positive cash balances are also avoided – under normal market conditions the firm can expect to receive higher interest on money market deposits and reverse repos than it can on nostro accounts.

Therefore most main settlement systems incorporate a cash flow projection module. This may be presented to users as either a report or a real-time enquiry.

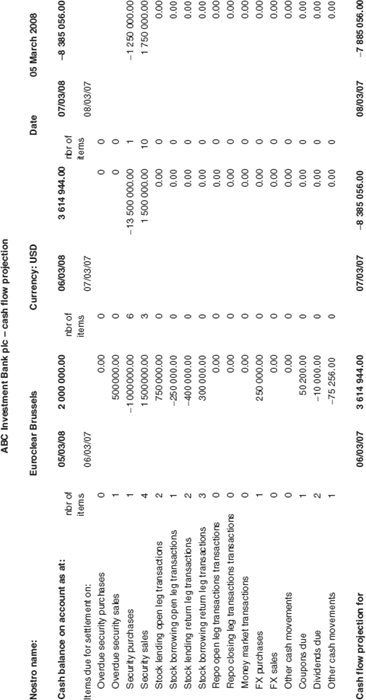

Figure 21.6 shows examples of a cash flow projection produced at the close of business on 5 March 2007 for ABC Investment Bank’s USD bank account with Euroclear Brussels for the next three working days.

Figure 21.6 Cash flow projection before funding activities

In the real world, the cash flow projection would show the expected cash movements for all the firm’s bank accounts in all currencies (one page for each individual currency bank account) for the next five working days. The figure only shows three days, the last two days have been omitted in this example in order to simplify it.

We can see the following information in the cash flow projection:

1. The closing balance of our USD account at Euroclear for today (5 March) is USD 2 000 000.00.

2. The enquiry then lists the numbers of trades and total net values of all the various trade types (security purchases, sales, stock lending transactions, FX transactions, etc.) that are due to settle on 6 March. Included among these are one overdue security purchase with a value of USD 1 million, and one overdue unsettled security sale with a value of USD 1.5 million. These trades should have settled on or before 5 March but have failed to settle for some reason.

3. If you add the value of all the transactions that should settle on or before 6 March to the 5 March cash balance, then we have a projected balance on this account for 6 March of USD 3 614 944.00.

4. The process is then repeated for 7 March when the projected balance of the account is USD 8 385 056, and 8 March when it becomes USD 7 885 056.

21.6.2 What the cash flow projection shows us

The conclusions we can draw from looking at this cash flow projection are:

1. On 6 March, we have excess funds of USD 3.61 million on this account.

2. On 7 March, we have a shortage of USD 8.35 million on this account

3. On 8 March we have a shortage of USD 7.85 million on this account.

21.6.3 Possible actions the firm could take to fund the account correctly

Excess funds on 6 March

For 6 March, the firm’s treasurer could put USD 3 million on overnight deposit for 6 March, to earn a higher rate of interest than Euroclear pays on a nostro account. If we assume that the firm could earn 4% overnight, then the following day (when the deposit matures) USD 3 000 333.33 will be paid back into the account (interest being calculated as 3 000 000 * 4% * 1 day/360 days in a year).

Inadequate funds on 7 and 8 March

The firm may be able to resolve this issue by any one of the following means:

1. Perhaps it has excess funds on another nostro that it could transfer into the account.

2. It could borrow USD 8.5 million for two days on the money markets at, say, 5%.

3. If it has government bonds that it could use as collateral, it could borrow USD 8.5 million indefinitely by using these bonds as collateral for a repo transaction, paying only 4% interest.

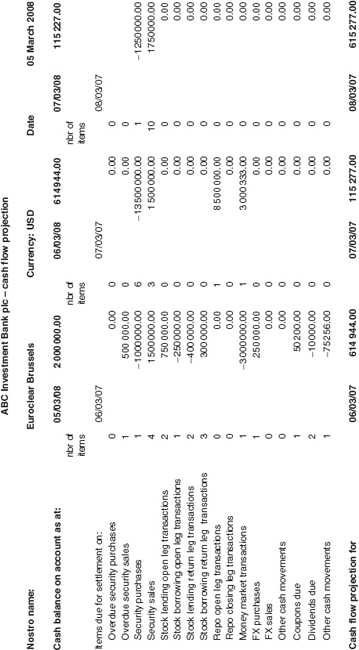

If it takes the third option – the repo – then the revised cash flow projection is shown in Figure 21.7. The new transactions are highlighted. You will see that the treasurer has been able to keep the projected balances on this account at between USD 0.11 million and USD 0.61 million for the period – ensuring that the account is funded adequately for the period, and that any excess funds are swept into higher interest bearing vehicles.

Figure 21.7 Cash flow projection after funding activity

21.6.4 Depot movement projections

A firm that is active in these markets needs to know at all times:

- Which securities it needs to borrow to cover short positions and delivery failures

- Which borrowed securities it is now in a position to return

- Which securities are available to lend to others

- Which securities it is in a position to use as collateral for repos

- Which securities it has used in repo transactions that it now needs to return.

Therefore a firm will require a depot movement projection that serves the same function for securities as the cash flow projection. However, while it is a viable option to present the cash flow projection in the form of a printed report, the depot movement projection needs to be presented in the form of a screen-based enquiry because the sheer number of individual securities concerned makes a printed report impractical.

Such an enquiry will be based on the stock record described in Chapter 15 and might be presented in the form shown in Figure 21.8.

Figure 21.8 Depot movement projection

21.6.5 Marking positions to market

In order to ensure that the value of collateral placed with the firm is at least equivalent to the value of securities and cash lent by the firm then the firm needs to mark the net value of stock loan and repo positions with each trading party to market. The mark-to-market process is explained in section 23.8. Part of the mark-to-market process is the accrual of interest on both the cash collateral and also any bonds involved in the transactions. Accrual of interest on positions is examined in section 23.9.

21.6.6 Relevant SWIFT messages for repo and stock ending activities

The messages shown in Table 21.2 are used between the trade parties for stock loans and repos.

Table 21.2 SWIFT messages relevant to stock lending and repo activity

| Message no. | Message name | Additional information |

| MT503 | Collateral claim | Requests new or additional collateral, or the return orrecall of collateral |

| MT504 | Collateral proposal | Proposes new or additional collateral |

| MT505 | Collateral substitution | Proposes or requests the substitution of collateral held |

| MT506 | Collateral and exposure statement | Provides the details of the valuation of both the collateral and the exposure |

| MT507 | Collateral status and processing advice | Advises the status of a collateral claim, a collateral proposal, or a proposal/request for collateral substitution |

| MT516 | Securities loan confirmation | Confirms the details of a securities loan, including collateral arrangements. It may also confirm the details of a partial recall or return of securities previously out on loan |

| MT526 | General securities lending/borrowing message | Requests the borrowing of securities or notifies the return or recall of securities previously out on loan. It may also be used to list securities available for lending |

| MT581 | Collateral adjustment message | Claims or notifies a change in the amount of collateral held against securities out on loan or for other reasons |

There are no specific settlement messages for these transactions – the messages that the trade party sends to and receives from its settlement agent are the same messages that were described in section 12.2.

21.6.7 Accounting entries to be posted in the general ledger

Start leg entries – from the perspective of the securities borrower

On trade date the entries shown in Table 21.3 are passed. If the firm was lending securities, the entries would be reversed.

Table 21.3 Trade date postings when securities borrowed

On settlement date the entries shown in Table 21.4 are passed.

Table 21.4 Settlement date postings when securities borrowed

Entries posted on payment of a margin call

If the firm is required to deposit additional collateral as a result of a rise in the price of the securities borrowed then the trade date entries are as shown in Table 21.5.

Table 21.5 Accounting entries to be passed on trade date for a margin call

If the price of the securities had fallen and the firm was in a position to claim a return of collateral then the signs would be reversed. The entries to be passed on actual settlement date are as shown in Table 21.6.

Table 21.6 Accounting entries to be passed on value date for a margin call

End leg entries – from the perspective of the securities borrower

On the trade date of the end leg of the transaction the entries shown in Table 21.7 are passed.

Table 21.7 Trade date entries for end leg

On the actual settlement date of the transaction the entries in Table 21.8 would be posted.

Table 21.8 Settlement date entries for end leg

21.6.8 Stock movement entries to be posted in the stock record

Start leg entries – from the perspective of the securities borrower

The stock record entry shown in Table 21.9 will be passed on the trade date of the start leg of the loan.

Table 21.9 Stock record postings on trade date – stock borrow start leg

And the entry shown in Table 21.10 will be passed on the settlement date of the start leg.

Table 21.10 Stock record postings on settlement date – stock borrow start leg

Entries posted when quantity borrowed is substituted, increased or decreased

When collateral is substituted, then the entries shown in Tables 21.9 and 21.10 are repeated for an increase in the amount borrowed and repeated with the signs reversed if there is a decrease in the amount borrowed. If the transaction is a repo and the instrument being used as collateral is substituted, then there will be a reversal of the entries passed for the original instrument shown in Tables 21.9 and 21.10, and replacement entries for a new instrument.

End leg entries – from the perspective of the securities borrower

On the trade date and settlement date of the end leg the entries that were passed on the start leg (adjusted by any collateral substitutions entries posted since then) need to be reversed.