Trends Are an Investor’s Best Friend

Tom Lydon

Of all the things you can teach yourself to become a better investor, the best thing is to learn how to identify trends. You probably do it now, to a degree. Perhaps when you heard that oil was nearing $100 a barrel in 2008, you noticed the uptrend. When you heard about bidding wars over houses, you noticed that real estate was trending higher, too. Although you might be familiar with what a bear market or a bull market looks like, to spot trends, you’ll have to zoom in a little closer.

Often by the time news of a trend spreads to the point where it’s cocktail-party fodder, the bulk of the profits have been made. What you need to do instead is learn to spot trends as early as possible in order to enjoy the longest ride possible.

Figure 1 shows the long upswings the market has experienced, followed by equally long corrections. In some cases, these corrections have been devastating. For example, investors who bought in late 2002 would have realized nice gains until about 2007, when the bottom dropped out.

Figure 1 S&P 500 Index, 1997 to 2008

Had you patiently waited as the S&P 500 climbed and climbed, then hung on as it fell, you would have seen six years go down the tubes.

Believe it or not, you don’t have to just sit there. Very few people predicted either of these two bear markets, but investors could have avoided much of the damage to their portfolios simply by following the general market trends.

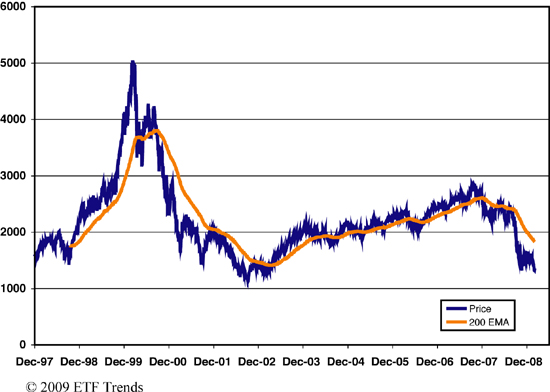

There is a simple approach that has been used to identify trends for decades. It involves a simple mathematical calculation that identifiesgeneral market trends. It’s a strategy I’ve used for my own clients for many years. The concept is simple. Take a look at Figure 2. Imagine if you were in the market when the S&P 500 rose above its 200-day moving average, and you were out when it fell below that mark. You could have avoided extended losses simply by being out, and you could have profited by being in at the right times.

Figure 2 S&P 500 Index with 200-day moving average, 1997-2008

But don’t stop here. You can apply this trend following strategy anywhere—to any time period, in any market, with any security type. Go ahead and apply the same logic to the devastating technology-driven bear market of 2000–2002 in Figure 3.

Figure 3 NASDAQ Composite with 200-day moving average, 1997-2008

If you are among the millions who bought technology stocks in the 1990s, only to hold them through one of the most devastating bear markets, you lost as much as 60%–70% in many cases and have still not even come close to recouping that money. But just as damaging as losing money is the loss of time.

Buy-and-Hold’s Funeral March

You may be thinking, “Whatever happened to the buy-and-hold strategy? It has worked for me for 40 years.” Well, that may be true, but take my word for it—and the word of many others: It won’t work moving forward.

You might want to be sitting down for this: Buy-and-hold is dead. (And there’s no Easter Bunny, either.) Wall Street’s mantra is losing steam and support fast and furiously. Investment pioneers Benjamin Graham, Warren Buffett, and Burton Malkiel spewed the virtues of buy-and-hold for years. But the ugly truth is if you are among the investors who have followed this strategy so far this century, you have lost money.

In fact, Buffett reportedly lost more than $16 billion in 2008, enough to make Graham squirm in his grave. While that figure doesn’t represent the average investor’s losses, it shows just how disastrous buy-and-hold can be.

The bottom line is: Buy-and-hold simply hasn’t worked. If you’re already in retirement or are planning retirement, you might be in a terrible situation. The fact that you’ve lost money and that there’s nothing you felt you could have done about it has had a drastically negative effect on your future plans. You might have considered going back to work part-time, or you might have had to call off retirement for now. It’s an ugly scenario for someone to be in, and it’s even uglier when you consider that many people could have avoided it altogether.

The country is in the middle of a major influx of baby boomers who are now moving into retirement, but many of them are finding themselves in the uncomfortable position of having to put off what, just five years ago, was a certainty.

For example, let’s say that you’re a buy-and-hold investor who had planned on retiring in 2009. You’re turning 66, you know that you have the money to do it, and you are ready. But then a crash comes. Now you’ve lost 40% of your portfolio. Suddenly, retirement for you seems as far away as childhood. And when will you have the time to make up the money lost? The closer you are to retirement, the less you can afford to hang on and ride both the ups and downs.

You can find evidence of this by looking at the wheel-spinning the markets have been doing: Had you invested in the S&P 500 in 1997 and held on to it through all the ups and downs until early 2009 (and maybe even later), you would be below where you started. All told, that’s more than ten years of investing with little to show for it outside of dividends. And what’s more, you’d be 12 years older. Those of you who are planning for retirement or who are in retirement can tell the rest of you about the pain.

“It’s time to unlearn a common myth about investing,” Jim Cramer told viewers on CNBC in late 2008. “The best way to invest is not to buy a bunch of stocks and just sit on them.” This doesn’t happen often, but I agree wholeheartedly with Cramer. Outside of raging bull markets like the one we experienced in the 1990s, the strategy of buying stocks and holding on to them for eternity no longer works. During bear markets, you stand to lose a whole lot of money, and in sideways markets, your assets will flatline.

But here’s the rub: The term sideways market is somewhat misleading. There’s plenty of market activity, but it’s in the form of a sharp downward move, followed by a sharp upward move. Sideways markets can wear on your emotions. They’re extremely frustrating and, most important, they burn up a lot of time. Have you ever gotten stuck in the snow or mud? The sensation that your wheels are spinning wildly as you dig a deeper and deeper hole is not unlike the feeling some get in markets that are going nowhere fast.

There are a handful of periods in this century where the market has made no money for ten years or more. For example, an investment in stocks that made up the S&P 500 Index during the periods of 1929–1942 (13 years), 1966–1982 (16 years), and 1997–2009 (12 years) would have amounted to no more than a break-even investment.

From 1997 until 2009, the S&P 500 fell in value an average of 0.4% per year. Through the end of 2008, after two devastating market collapses, the S&P 500 returned 7.1% since 1950 and 7.8% since 1980. In 2000–2008, the S&P’s performance was down a dismal 4.7%, including dividends. You don’t have to retrace the past decade or more to see the damage this outdated strategy can cause.

Listen: Life is short. All of us only have so much time to save for our golden years. I don’t know about you, but I certainly don’t have ten years’ worth of retirement savings to just up and lose—and then slowly but surely make it up until I’m back where I was before, hoping that there’s not another bust before I’m sent back to the starting line again. You and other investors simply cannot afford to suffer the drastic losses we saw in the recent bear markets.