Congrats! We have reached the most interesting part of financial accounting, that is, Final Accounts.

These are in the true sense the financial statements of the company. It is compulsory for the Board of Directors of the company to present in its Annual General Meeting (AGM) the financial statements before the company. It reflects the financial position of the company at the end of the period.

The overall financial performance of the company, which is of main interest to the managers and corporates, is ascertained through Final Accounts.

Financial Statements include:

- Balance Sheet

- Profit and Loss A/c

- Cash Flow Statement

- Statement of changes in equity, if applicable

- Any explanatory note forming part of or annexed to the above statements

Financial Statements: A set of accounting documents prepared for a business entity that cover a particular time period and describe the financial health of the business.

|

Financial statements |

Business activities |

|

Income statement Revenues Expenses |

Operating activities |

|

Statement of cash flows Operating activities Investing activities Financing activities |

Operating activities Investing activities Financing activities |

|

Balance sheet Current assets Long-term assets Current liabilities Long-term liabilities Equity |

Operating activities Investing activities Operating activities Financing activities Financing activities |

It has to be prepared according to the format given in Schedule III of Companies Act 2013. Various accounting standards have to be followed in its preparation.

We will be dealing with the first three very important statements now.

The Cash Flow Statement

A Cash Flow Statement is a statement that describes the movement by way of net increase or decrease in cash and cash equivalents of an organization in a particular period. Cash equivalents are those short-term investments and securities that can be readily converted into cash, say, within a period of three months or less.

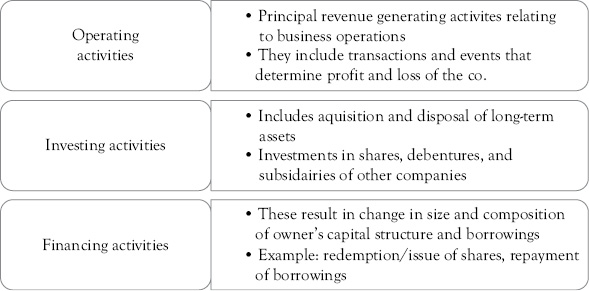

The first step comprises ascertaining the cash flow activities, that is, whether the activities caused “inflow” or “outflow” of cash.

The next step is to segregate such activities into three categories:

- Operating activities

- Investing activities

- Financing activities

The total cash flow from, or used in, the above activities has to be calculated separately.

Let us look into each activity one by one.

There are two types of methods to ascertain cash flow of the company during the year.

Indirect Method

This method is preferably used and hence we will focus on gaining an understanding about it.

In this method, only the manner of calculating the cash flow from operating activities changes. Everything else remains the same as in the case of the direct method.

In this method, we just have to:

- Determine the adjusted profit by adding or subtracting the noncash and nonoperating items to and from the net profit charged in the income statement

- Make adjustments for net increase or decrease in current assets and current liabilities

- Subtract direct taxes paid during the period

- Adjust extraordinary items that normally do not occur in the business to ascertain true profit

That is it! We arrive at net cash flow from operating activities through the indirect method.

|

Cash flow from operating activities |

|

|

Cash inflow

|

Cash outflow

|

|

Cash flow from investing activities |

|

|

Cash inflow

|

Cash outflow

|

|

Cash flow from financing activities |

|

|

Cash inflow

|

Cash outflow

|

Pro formas for preparation of cash flow will help in better understanding this.

Format for Cash Flow From Operating Activities—Indirect Method

|

Particulars |

Analysis (only for understanding) |

Amount (Rs.) |

|

Net profit before tax and extraordinary items Adjustments for Depreciation Foreign exchange investments Investments Gain or loss on sale of fixed assets Interest dividend |

From income statement Noncash item Nonoperating item Nonoperating item Nonoperating item Nonoperating item |

xxx xxx xxx xxx xxx xxx |

|

Operating profit before working capital changes |

xxx |

|

|

Adjustments for current assets or liabilities Trade and other receivables Inventories Trade payable |

Since decrease in working capital = cash inflow and increase in working capital = cash outflow |

xxx xxx xxx |

|

Cash generated from operations |

xxx |

|

|

(Add) Interest paid (Less) Direct taxes |

Nonoperating item Have to be deducted to arrive at operating profit |

xxx xxx |

|

Cash before extraordinary items |

xxx |

|

|

Adjustments for extraordinary items |

Nonoperating item |

xxx |

|

Net cash flow from operating activities |

xxx |

|

Cash Flow from Investing Activities

|

Particulars |

Analysis (only for understanding) |

Amount (Rs.) |

|

(Less) Purchase of fixed assets (Add) Proceeds from sale of fixed assets (Add) Interest received (Add) Dividend received |

Since it involves cash flows on acquisition or disposal of long-term investments Income from investments will go into investing activities |

xxx xxx xxx xxx |

|

Net cash flow from investing activities |

xxx |

|

Cash Flows From Financing Activities

|

Particulars |

Analysis (only for understanding) |

Amount (Rs.) |

|

(Add) Proceeds from issue of share capital (Add) Proceeds from long-term borrowings (Less) Repayment of long-term borrowings (Less) Interest paid (Less) Dividend paid |

Since it results in change in size and composition of capital structure Payments made to sources of funds go into financing activities |

xxx xxx xxx xxx xxx |

|

Net cash flows from financing activities |

xxx |

|

Consolidated Summary

|

Particulars |

Amount (Rs.) |

|

Cash flow from operating activities |

xxx |

|

(Add) Cash flow from investing activities |

xxx |

|

(Add) Cash flow from financing activities |

xxx |

|

Net increase or decrease in cash |

xxx |

|

(Add) Opening balance of cash and cash equivalents |

xxx |

|

Closing balance of cash and cash equivalents* |

xxx |

*Closing balance of cash at the end should match the closing balance as given in the Balance Sheet.

We will now consider a question for better understanding.

Question

The following data for Ryan Ltd are provided.

|

Income statement |

(Amount in Rs.) |

|

|

Sales Cost of goods sold Gross margin Operating expenses (including depreciation expense of Rs. 37,000) Other income or expenses Interest expense paid Interest income received Gain on sale of investments Loss on sale of plant |

(23,000) 6,000 12,000 (3,000) |

6,98,000 (5,20,000) |

|

1,78,000 (1,47,000) |

||

|

31,000 (8,000) |

||

|

23,000 (7,000) |

||

|

Income tax |

16,000 |

Comparative balance sheets

|

March 31, 2015 |

March 31, 2014 |

|

|

Assets Plant assets Less: Accumulated depreciation Investments (long term) Current assets: Inventory Accounts receivable Cash Prepaid expenses Liabilities Share capital Reserves and surplus Bonds Current liabilities Accounts payable Accrued liabilities Income tax payable |

7,15,000 (1,03,000) 6,12,000 1,15,000 1,44,000 47,000 46,000 1,000 |

5,05,000 (68,000) 4,37,000 1,27,000 1,10,000 55,000 15,000 5,000 |

|

9,65,000 |

7,49,000 |

|

|

4,65,000 1,40,000 2,95,000 50,000 12,000 3,000 |

3,15,000 1,32,000 2,45,000 43,000 9,000 5,000 |

|

|

9,65,000 |

7,49,000 |

Analysis of selected accounts and transactions from 2014 to 2015

- Purchased investments of Rs. 78,000

- Sold investments for Rs. 1,02,000

- Purchased plant assets for Rs. 1,20,000

- Sold plant assets that cost Rs. 10,000 with accumulated depreciation of Rs. 2,000 for Rs. 5,000

- Issued Rs. 1,00,000 of bonds at face value in exchange for plant assets on March 31, 2015

- Repaid Rs. 50,000 bonds at face value at maturity

- Issued Rs. 15,000 shares of Rs. 10 each

- Paid cash dividend Rs. 8,000

Prepare Cash Flow Statement.

Answer

Step I

Relax! It is easy!

Step II

As discussed above, we will start with the net profit as per the Income Statement and adjust it for all noncash and nonoperating items.

Then, we will take each element of the Balance Sheet separately along with its given concerned additional information, in order to ascertain what effect it each has on the cash flows of the company—that is, whether it causes inflow or outflow of cash—while simultaneously segregating such elements into operating, investing, or financing activities.

Step III

So! Let us start with the Income Statement.

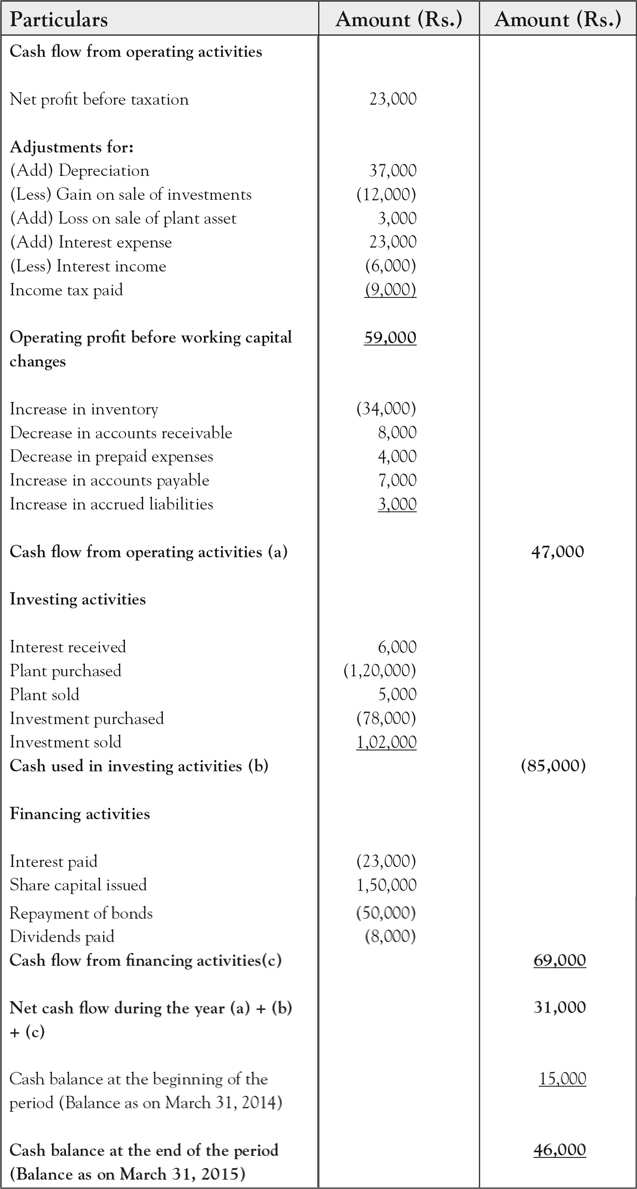

- The income statement shows net profit before tax as Rs. 23,000.

Adjustments for the following shall be made:

- Depreciation on plant assets is just the normal wear and tear that occurs with time and hence does not involve any cash outflow. So, we will add back Rs. 37,000 to the profits since it has been charged in the income statement to arrive at the profit.

- Gain on Sale of Investments can be said to be the profit earned from the sale of particular investments by the company. Since it is just a profit, it does not involve any cash flow directly. Moreover, since it is a nonoperating activity, Rs. 12,000 will be subtracted from the net profit.

- Loss on Sale of Plant, as mentioned above, is only a loss arising from the sale of its plant by the company, which again does not involve any cash flow directly. Hence, Rs. 3,000 will be added back since it has been subtracted to arrive at the profit in our cash flow statement.

- Interest Expense paid is the interest that is paid by the company to its various sources of finance, in the form of dividends, interest on loans, debentures, bonds, and so on. As it involves cash outflow, Rs. 23,000 will be classified as cash used in financing activities since it is the cost the company has to pay as a result of its financing activities.

Hence, it will be added back to the profit to arrive at cash flow from operating activities since it is not an operating expense.

- Interest Income received is the interest received by the company on the investments done by it in the form of dividends, interest on loans given, and so on. Rs. 6,000 received would have involved cash inflow and hence we will include it as cash flow from investing activities.

So, it will be subtracted from the profits to exclude it from operating activities.

- Income Tax in the income statement denotes total tax expense for the year, that is Rs. 7,000, which may or may not have been paid or partially paid and partially a new provision for next year would have been made. In this case, a provision of Rs. 3,000 has been made for the next year (as per Balance Sheet as on March 31, 2015).

Additionally, tax payable of the previous year of Rs. 5,000 (as per Balance Sheet as on March 31, 2014) is paid in the current year. Hence we will only take into account income tax that is paid during the current year that sums up to Rs. 9,000 out of which Rs. 5,000 is rom the previous year and Rs. 4,000 is the current year’s expense. We will include this under cash used in operating activities as it forms a part of the operational part of the business.

Step IV

Now, we move on to the Balance Sheet. Here, we will have to draw a comparison between the two given Balance Sheets to identify any increase or decrease in assets and liabilities that would involve movement of cash.

-

Plant Assets are specifically given to have been purchased for Rs. 1,20,000, which would have involved outflow of cash. Hence we would take it as cash used in investing activities since it is a part of investing activities carried out by the company.

Moreover, Plant was also sold for Rs. 5,000, as given in the additional information, which would have involved inflow of cash. Hence this would also be included as cash flow from investing activities.

-

Investments (Long Term), as given in the additional information, have been purchased for Rs. 78,000; this would have involved outflow of cash. So, accordingly, we will take it under cash used in investing activities.

Similarly, Investments of Rs. 1,02,000 were also sold during the year as per the information given in the analysis of selected accounts. This would have caused cash inflow and so we will include it under cash flow from investing activities.

We now move on to Current Assets.

- Inventory has increased from Rs. 1,10,000 at the beginning of the year, that is as per Balance Sheet on March 31, 2014, to Rs. 1,44,000 by the end of the year, that is as per Balance Sheet on March 31, 2015. This means that we have increased our stock by Rs. 34,000, thereby blocking more funds. Thus, it would have caused outflow of cash indirectly, as the funds are blocked and cash inflow will not be possible until we sell our stock. It will be included as cash used in operating activities and deducted from the profit as it forms part of the working capital that is directly related to business operations.

- Accounts Receivable has decreased from Rs. 55,000 from the beginning of the year to Rs. 47,000 at the end of the year. This implies that we have received payment of Rs. 8,000 during the year, because of which our total accounts receivable has decreased. This process would have involved inflow of cash and hence we would include it under cash flow from operating activities and add it to the profit.

- Cash balance has increased from Rs. 15,000 at the beginning of the year to Rs. 46,000 at the end of the year due to cash flows from various activities as being discussed. Hence, the cash balance at the beginning of the year, adjusted with the net increase or decrease in cash during the year, should be equal to the cash balance at the end of the year. This would imply that we have worked out the question correctly.

- Prepaid Expenses have decreased from Rs. 5,000 at the beginning of the year to Rs. 1,000 at the end of the year. This means we have not paid for the current year expenses and the same has been adjusted from what we had paid in advance the previous year. Hence by not paying the current year expenses, we have saved our cash, which is equivalent to cash inflow. Rs. 4,000 will be thus included in cash flow from operating activities and would be added to the profit.

Next come the Liabilities.

- Share Capital has increased from Rs. 3,15,000 at the beginning of the year to Rs. 4,65,000 at the end of the year, that is, by Rs. 1,50,000. This implies that the company has issued 15,000 new shares of Rs. 10 each, as also given in the additional information. We would have received cash against such issue; hence, we will include it under cash flow from financing activities since the issue of shares is a source of finance for the company.

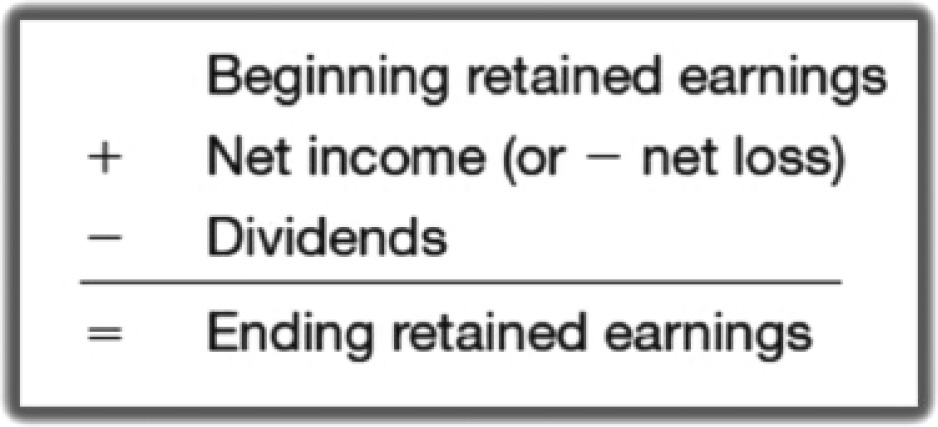

- Reserves and Surplus can also be known as retained earnings. These are appropriation of profits that, is, the company reinvests a certain amount of profit earned during the year with itself. It does not involve any movement of cash. Hence we will not consider it for our cash flow statement.

- Bonds have increased from Rs. 2,45,000 to Rs. 2,95,000, that is, by Rs. 50,000. It has also been provided that the company has issued bonds to the extent of Rs. 1,00,000 in exchange for Plant Assets. This implies that there must have been no cash inflow from the issue of such bonds. Further, it is also provided that bonds of value of Rs. 50,000 were repaid, which means there would have been a cash outflow of Rs. 50,000. Thus, the net increase in bonds involved no cash inflow. Only the repayment done will be taken under cash used in financing activities.

Next we move on to Current Liabilities.

- Accounts Payable have increased from Rs. 43,000 to 50,000. This implies that we have not made payments that were supposed to be made to the tune of Rs. 7,000, that is, we have saved our cash outflow, which can also be regarded indirectly as cash inflow. Hence we will record it under cash flow from operating activities and add the same to the profit.

- Accrued Liabilities have increased from Rs. 9,000 at the beginning of the year to Rs. 12,000 at the end. This means that we have not paid certain liabilities that were due, thereby saving on our cash outflow. Indirectly, we can say that there has been a cash inflow from operating activities since we have saved cash and cash saved is cash earned!

- Income Tax treatment has already been discussed above.

Step V

Check whether any item has been left unaccounted for, including in the additional information provided.

- Cash Dividend, of Rs. 8,000 like in this case, has been left to be included in our cash flow statement. Payment of cash dividend would have involved cash outflow; hence, it will be included in cash used in financing activities since the issue of shares is a means of finance for a Co and dividend is paid on the share capital.

Step VI

We are done!

Now we just need to present what we have discussed above in the following manner:

Ryan Ltd.

Cash Flow Statement

For the year ending March 31, 2015

Let us take another example.

Question

The following information about Gamma Ltd. is given for the year 2014.

|

Particulars |

Amount (Rs.) |

|

Net profit |

25,000 |

|

Dividend |

8,535 |

|

Provision for income tax |

5,000 |

|

Income tax paid during the year |

4,248 |

|

Loss on sale of assets |

40 |

|

Book value of assets sold |

185 |

|

Depreciation charged to Profit and Loss A/c |

20,000 |

|

Profit on sale of investments |

100 |

|

Carrying amount of investments sold |

27,765 |

|

Interest income on investment |

2,506 |

|

Interest expenses of the year |

10,000 |

|

Interest paid during the year |

10,520 |

|

Increase in working capital (excluding cash and bank balance) |

56,081 |

|

Purchase of fixed assets |

14,560 |

|

Investment in joint venture |

3,850 |

|

Expenditure on construction work in progress |

34,740 |

|

Proceeds from calls in arrears |

2 |

|

Receipt of grant for capital project |

12 |

|

Proceeds from long-term borrowings |

25,980 |

|

Proceeds from short-term borrowings |

20,575 |

|

Opening cash and bank balance |

5,003 |

|

Closing cash and bank balance |

6,988 |

Prepare Cash Flow Statement for the year 2014.

Answer

Let us crack it!

Step I

Start with the analysis of the question by taking each item one by one and identifying under which activity it will be placed.

So, let us start!

As discussed earlier, we will first start with profit before tax as per Income Statement and adjust it for nonoperating and noncash items. Hence to arrive at profit before tax, we will have to add back provision for income tax of Rs. 5,000 to the net profit as it would have been made from profit only.

Step II

Analyze each item to decide its treatment.

- Dividend

Financing activity

Financing activity - Provision of income tax Add back to profit

- Income tax paid Deduct from operating profit as cash outflow

- Loss on sale of assets Add back to net profit

- Book value of assets sold Sale price (book value – loss) will be included in investing activities

- Depreciation Add back to profit

- Profit on sale of investment Deduct from profit

- Carrying amount of investment sold Sale price (carrying amount + profit) will be included in investing activities

- Interest income on investment Investing activity

- Interest expense of the year Will not be included in financing activity since not paid

- Interest paid during the year Financing activities

- Increase in working capital Operating activities

- Purchase of fixed asset Investing activity

- Investment in joint venture Investing activity

- Expenditure on construction Investing activity

- Proceeds from calls in arrears Financing activities as it relates to financing through shares

- Receipt of grant for capital project Financing activities

- Proceeds from long-term borrowing Financing activities

- Proceeds from short-term borrowing Financing activities

We will now present it according to the format.

Cash Flow Statement of Gamma Ltd.

For the year ended December 31, 2014

|

Particulars |

Amount (Rs.) |

Amount (Rs.) |

|

Cash flows from operating activities Net profit before tax (25,000 + 5,000) Adjustments for: Depreciation Loss on sale of asset (Less) Profit on sale of investment (Less) Interest income on investment Interest expense Operating profit before working capital changes |

30,000 20,000 40 (100) (2,506) 10,000 57,434 |

|

|

Changes in working capital Cash generated from operations Income tax paid Net cash used in operating activities Cash flows from investing activities Sale of assets (185 − 40) Sale of investments (27,765 + 100) Interest income on investment Purchase of fixed asset Investment in joint venture Expenditure on construction Net cash used in investing activity Cash flows from financing activities Proceeds from calls in arrears Receipt of grant for capital project Proceeds from long-term borrowings Proceeds from short-term borrowings Interest paid Dividend Net cash used in financing activity Net increase in cash and cash equivalent Opening balance of cash and cash equivalent Closing balance of cash and cash equivalent |

(56,081) 1,353 (4,248) 145 27,865 2,506 (14,560) (3,850) (34,740) 2 12 25,980 20,575 (10,520) (8,535) |

(2,895) (22,634) 27,514 1,985 5,003 6,988 |

That is it! We are done with Cash Flow!

Now we will move on to the next and the final level, that is, preparation of Profit and Loss A/c and Balance Sheet.

Direct Method

We shall now learn the direct method of presenting the Cash Flow Statement. In this method, only “Cash Flow from Operating Activities” is calculated differently as compared to the indirect method. Calculation of cash flow from investing and financing activities remains the same.

We directly take all the operating activities that involve cash flow instead of adjusting the net profit as in the indirect method.

Let us take an example to make it clearer.

Example

Prepare a Cash Flow Statement of X Ltd. from the following Summary Cash Account for the year ended March 31, 2013.

Summary Cash Account for the year ended 31.3.2013

|

₹ '000 |

₹ '000 |

|||

|

Balance on 1.4.2012 |

50 |

Payment to suppliers |

2,000 |

|

|

Issue of equity shares |

300 |

Purchase of fixed assets |

200 |

|

|

Receipts from customers |

2,800 |

Overhead expense |

200 |

|

|

Sale of fixed assets |

100 |

Wages and salaries |

100 |

|

|

Taxation |

250 |

|||

|

Dividend |

50 |

|||

|

Repayment of bank loan |

300 |

|||

|

Balance on 31.3.2013 |

150 |

|||

|

3,250 |

3,250 |

|||

Answer

Step I

We will first calculate cash flow from operating activities. For this, we will have to segregate all the operating activities that involve cash flow.

In the question, cash flow from operating activities will be calculated in the following manner through the direct method.

Cash Flow Statement of X Ltd.

For the year ended March 31, 2013

|

Cash flow from operating activities Receipts from customers Less: Payment to suppliers Less: Overhead expense Less: Wages and salaries Less: Income tax paid Cash flow from operating activities (a) |

|

Amount 2,800 (2,000) (200) (100) (250) 250 |

Step II

We now move on to cash flow from investing and financing activities, which would be calculated in the same manner as in the indirect method.

|

Cash flow from investing activities Proceeds from sale of fixed assets Less: Payment for purchase of fixed assets Net cash used in investing activities (b) Cash flow from investing activities Proceeds from issue of shares Repayment of bank loan Payment of dividend Net cash used in financing activities (c) Net increase in cash (a) + (b) + (c) Cash at the beginning of the period Cash at the end of the period |

|

Amount 100 (200) (100) 300 (300) (50) (50) 100 50 150 |

Profit and Loss A/c

This is the Income Statement of a company. It shows the net profit earned or the loss incurred by the company through its business operations for the period. It can be said to be the “report card” of the business, which shows the net profit earned or loss incurred by the company as a result of its working.

It is of the utmost importance to especially managers and entrepreneurs who are interested to know the ultimate result of their operations and management, that is, whether they have been successful in earning profits or they ended up making losses. Also, it helps them in ascertaining the exact amount of money spent on different expenses. This helps them in controlling costs, and increasing efficiency and profitability of the business.

As discussed earlier, the balance of all the nominal accounts are transferred to the Profit and Loss Account. All the incomes, gains, expenses, and losses are recorded here, which can be summed up as follows:

Points to note:

- Only items of revenue nature, that is, those that pertain to day-to-day working of the company and are only for the said period, are recorded here.

- Transactions relating only to business operations are included here. Transactions relating to financing and investing activities of the company are not included.

- All the expenses and incomes that have become due during the period, whether paid or not, are included here. This is as per the accrual system of accounting.

- Outstanding expense will be added to the expense as it relates to the current period.

- Prepaid expense will be subtracted from the expense as it does not relate to the current period.

- Accrued income will be added to the income as it relates to the current period.

- Prepaid income will be subtracted from the income as it does not relate to the current period.

The Profit and Loss A/c is prepared as per the format prescribed by the statute. Companies have to strictly follow it and present it in the manner prescribed.

Whatever may be the presentation requirements, the basic essence remains that it shows the ultimate “result” of the business done by the company.

Let us now have a look at the format for the preparation of the Profit and Loss statement of a company.

Format

Name of the Company…………………….

Profit and Loss Statement for the Year Ended ………………………

Rupees in ...........

|

Particulars |

Note No. |

Figures for the current reporting period |

Figures for the previous reporting period |

|

i. Revenue from operation |

x x |

x x |

|

|

ii. Other Income |

x |

x |

|

|

iii. Total Revenue (i + ii) |

x x x |

x x x |

|

|

iv. Expenses Cost of Materials Consumed Purchases of Stock-in-Trade Changes in inventories of Finished Goods, Work-in-Progress and Stock-in-Trade Employee Benefit Expenses Finance Costs Depreciation and Amortisation Expenses Other Expenses Total expenses |

x x x x x x x xxx |

x x x x x x x xxx |

|

|

v. Profit before Tax (iii – iv) |

xxx |

xxx |

|

|

vi. Less Tax |

(x) |

(x) |

|

|

vii. Profit after Tax (v – vi) |

xx |

xx |

No need to get confused!

We will understand this in a detailed manner.

Before that, there are some points to be noted from the above Performa:

- The detailed analysis of the amounts reported in the Profit and Loss Statement has to be given in the Notes to Accounts as per Column 3, where the corresponding note number has to be given. We will look into such notes in the succeeding chapters.

- The previous years’ figures also have to be reported along with the current year’s figures as per Column 4.

Let us now analyze each item of the Profit and Loss Statement in the format.

Items Under Various Heads Appearing in Profit and Loss Statement

Revenue from operations

- Net sales

- Sale of scrap

- Trading commission received

- Cash discount received

- Revenue from services

Other income

- Rent received

- Dividend and interest received

- Profit on sale of fixed assets or investments

Cost of material consumed

- Opening stock of materials + net purchases – closing stock of materials

Purchases of stock-in-trade

- Net purchases

Changes in inventories of finished goods, work-in-progress, and stock-in-trade

- Opening stock – closing stock

Employee benefit expenses

- Wages

- Salaries

- Staff welfare expenses such as canteen expenses

- Contribution to provident funds and other staff welfare funds

Depreciation and amortization expenses

Finance costs

Amount of interest paid by the company on its borrowings

Other expenses

Includes expenses other than the above six heads of expenses. These could be:

- Telephone expenses

- Rents and taxes

- Selling and distribution expenses

- Advertisement expenses

- Loss on sale of fixed assets or investments

- Cash discount allowed

- Bad debts

- Provision of bad and doubtful debts

Provision for tax and tax rate

Let us take a question for better understanding.

Question

Prepare Profit and Loss Statement from the following Trial Balance of Zed Chemicals Ltd. for the year ended March 31st, 2015.

Hari Chemicals Ltd.

Trial Balance as on March 31, 2015

|

Particulars |

Rs. In ‘000 |

Particulars |

Rs. In ‘000 |

|

Inventory Furniture Discount Loan to directors Advertisement Bad debts Commission Purchases Plant and machinery Rentals Current account Cash Interest on bank loans Preliminary expenses Fixtures Wages Consumables Freehold land Tools and equipment Goodwill Trade receivables Dealer aids Transit insurance Trade expenses Distribution freight Debenture interest |

680 200 40 80 20 35 120 2,319 860 25 45 8 116 10 300 900 84 1,546 245 265 440 21 30 72 54 20 8,535 |

Equity shares Capital (Shares of Rs. 10 each) 11% Debentures Bank loans Trade payables Sales Rent received Transfer fees Profit and loss A/c Depreciation provision: Machinery |

2,500 500 645 281 4,268 46 10 139 146 8,535 |

Additional Information: Closing Inventory on March 31st, 2015: Rs. 8,23,000

Answer

Each item in the Trial Balance will go either in the Profit and Loss Statement or Balance Sheet.

So, in order to prepare the Profit and Loss Statement, we have to follow the following steps:

Step I

First, identify all those incomes and expenses that will be a part of our Income Statement.

Let us make a list of them:

Expenses ![]() Given on Debit side of Trial Balance

Given on Debit side of Trial Balance

- Changes in inventory

- Discount

- Advertisement

- Bad debt

- Commission

- Purchases

- Rentals

- Interest on bank loan

- Preliminary expenses

- Wages

- Consumables

- Dealer aids

- Transit insurance

- Trade expenses

- Distribution freight

- Debenture interest

Incomes ![]() Given on Credit side of Trial Balance

Given on Credit side of Trial Balance

- Sales

- Rent received

- Transfer fees

Step II

We will now start filling in the format the incomes and expenses at relevant places.

All the calculations and details should not be provided in the main Profit and Loss Statement but in the Notes to Accounts.

Let us see how it will be done.

Hari Chemicals Ltd.

Statement of Profit and Loss for the Year Ended March 31, 2015

|

Particulars |

Note No. |

Figures as at the end of March 31, 2015 |

|

|

Revenue from operations |

42,68,000 |

|

|

|

Other income |

7 |

56,000 |

|

|

Total revenue (A) |

43,24,000 |

|

|

|

Expenses |

|||

|

Cost of material consumed |

8 |

23,19,000 |

|

|

Change in inventory of finished goods |

9 |

(1,43,000) |

|

|

Employee benefit expenses |

10 |

9,00,000 |

|

|

Finance cost |

11 |

1,36,000 |

|

|

Other expenses |

12 |

5,11,000 |

|

|

Total expenses (B) |

37,23,000 |

||

|

Profit before tax (A − B) |

6,01,000 |

||

|

Provision for tax |

- |

No information of tax is given |

|

|

Profit for the period |

6,01,000 |

We have got the profit for the year! Was it not easy?

Now we just have to prepare the Notes to Accounts as mentioned earlier, which describes all the items on the face of the Profit and Loss Statement in detail.

Notes to Accounts

|

Particulars |

Amount (Rs.) |

Amount (Rs.) |

|

|

7. |

Other Income Rent received Transfer fees |

46,000 10,000 56,000 |

|

|

8. |

Cost of materials consumed Add: purchases |

23,19,000 |

|

|

9. |

Changes in inventory of finished goods, WIP & Stock in trade Opening inventory Closing inventory |

6,80,000 8,23,000 |

(1,43,000) |

|

10. |

Employee benefit expense Wages |

9,00,000 |

|

|

11. |

Finance cost Interest on bank loans Debenture interest |

1,16,000 20,000 1,36,000 |

|

|

12. |

Other Expenses Consumables Preliminary expenses Bad debts Discount Rentals Commission Advertisement Dealers’ aids Transit insurance Trade expenses Distribution freight |

84,000 10,000 35,000 40,000 25,000 1,20,000 20,000 21,000 30,000 72,000 54,000 5,11,000 |

|

We can see that all the items we had included in Step I have been taken into consideration for the preparation of the Profit and Loss Statement.

Step III

Prepare the Balance Sheet from it!

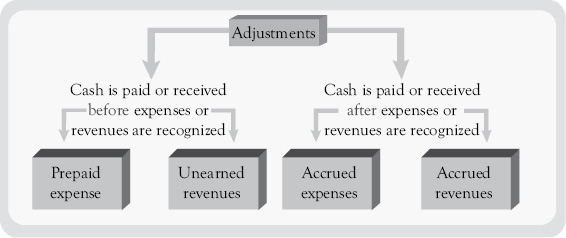

Adjustments

There are certain adjusting entries that need to be made at the end of the year for appropriate presentation of accounts. They mostly are due to the difference between expense and expenditure and revenue and receipts.

Some cases are discussed here:

Case I

Prepaid expense, that is, recorded costs to be apportioned between two or more accounting periods.

For example, Rs. 5,000 is paid for insurance out of which Rs. 2,000 pertains to the following year.

Answer

Here, only Rs. 3,000 out of Rs. 5,000 shall be taken as expense of the current year. Hence, Rs. 2,000 will be deducted from Rs. 5,000 in the Profit and Loss account. The remaining Rs. 2,000 will be treated as a prepaid expense and taken to the Balance Sheet under current assets.

Case II

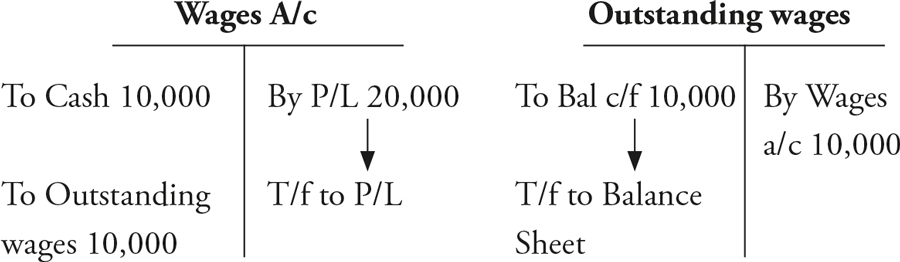

Outstanding expenses, that is, expenses incurred but not paid during the year.

For example, Rs. 20,000 wages have been earned by the employees but only Rs. 10,000 has been paid to them. The rest is still due.

Answer

In this case, the whole of Rs. 20,000 is the current year expense and hence it should be charged to the Profit and Loss A/c. But, since Rs. 10,000 has not been paid and is still due, this will be carried forward to the next period as outstanding expense in the Balance Sheet under current liabilities.

Case III

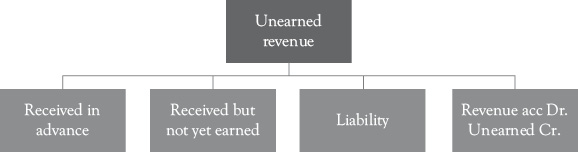

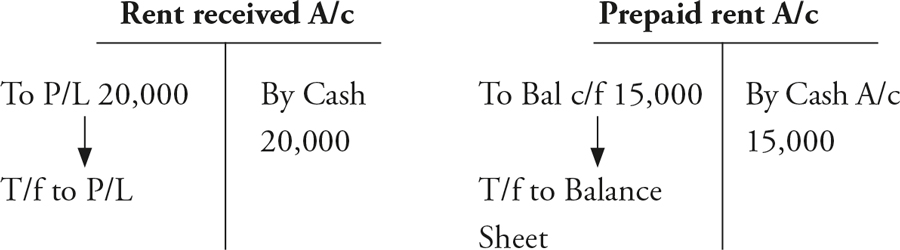

Unearned income, that is, income though received, not yet earned.

For example, Rs. 35,000 rent received out of which Rs. 15,000 is for the next year.

Answer

This means that only Rs. 20,000 is the income for the current year; the rest is income received but not yet earned, that is we have not yet earned the right to receive that income. Hence, Rs. 20,000 that pertains to the current year will be charged to the Profit and Loss A/c whereas Rs. 15,000 that is for the next year will be shown as prepaid income in the Balance Sheet under current liabilities.

Case IV

Accrued income, that is, income that is earned but not received.

For example, earned Rs. 45,000 as fees but received only Rs. 25,000.

Answer

Here, though the income we have earned for the current year is Rs. 45,000, we have received only Rs. 25,000. This means that Rs. 20,000 is accrued or due. Thus, we will treat the whole of Rs. 45,000 as income in the Profit and Loss A/c whether received or not and take the remaining Rs. 20,000 as accrued income in the Balance Sheet under current assets.

Case V

Depreciation

It is the loss in the value of a fixed asset during its useful life due to normal wear and tear. Every year a certain amount of value of the asset is written off in the Profit and Loss A/c as an expense by the name of depreciation expense.

But, instead of subtracting the amount of depreciation from the asset, it is credited to a separate account known as Accumulated Depreciation Account. It has two advantages:

- The asset is shown at the original cost in the Balance Sheet.

- The total depreciation accumulated on such asset till date is also shown separately.

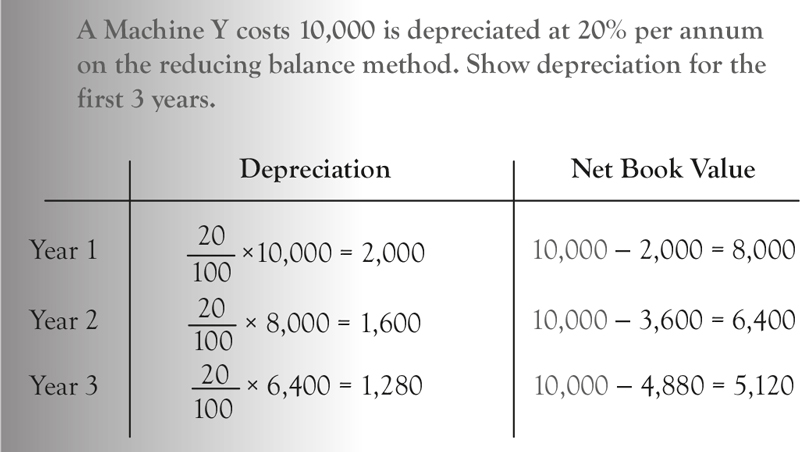

For example, depreciation is provided in the straight line method on the asset costing Rs. 30,000 having six years of useful life.

Answer

Here, we first need to calculate the depreciation amount to be written off in the Profit and Loss A/c. Being a straight line depreciation, the same amount of depreciation each year should be charged over its useful life. Hence in this case it would be: 30,000 divided by 6, which comes to Rs. 5,000 each year. It would have the following treatment:

It would be presented in the following manner in the Balance Sheet:

Equipment, at cost..................................................... |

30,000 |

Less: Accumulated depreciation.............................. |

5,000 |

Net equipment............................................... |

25,000 |

There are the following methods and formulas to calculate depreciation:

|

Method |

Explanation |

Depreciation amount or formula |

|

Straight line depreciation |

Same amount is charged each year calculated on the useful life of the asset |

Cost - Scrap ------------------------- Useful life |

|

Diminishing value method |

Depreciation amount is calculated as a percentage on written down value, that is, the depreciated value of the asset |

Example

|

Sum of years’ digit method |

Depreciation is calculated on the basis of number of years of the useful life of the asset |

(Acquisition cost − Salvage value) × (Remaining useful life or Sum of years’ digit) |

Case VI

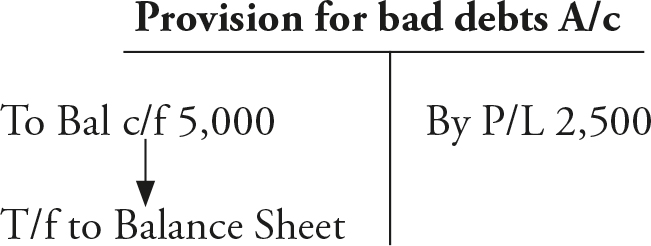

Provision for bad or doubtful debts, that is, provision for receivables whose collection is uncertain.

For example, provision of 5 percent on debtors, which is Rs. 50,000, has to be made during the year.

Answer

Provision for doubtful debt is made by the company to prepare itself for uncertainties arising out of collections from debtors. This is done to present the debtors at their realizable value and not at an inflated value. Hence here, provision of 50,000 × 5 percent (Rs. 2,500) will be made and charged to the Profit and Loss A/c. The same amount will be shown as short-term provision under current liabilities in the Balance Sheet.

Case VII

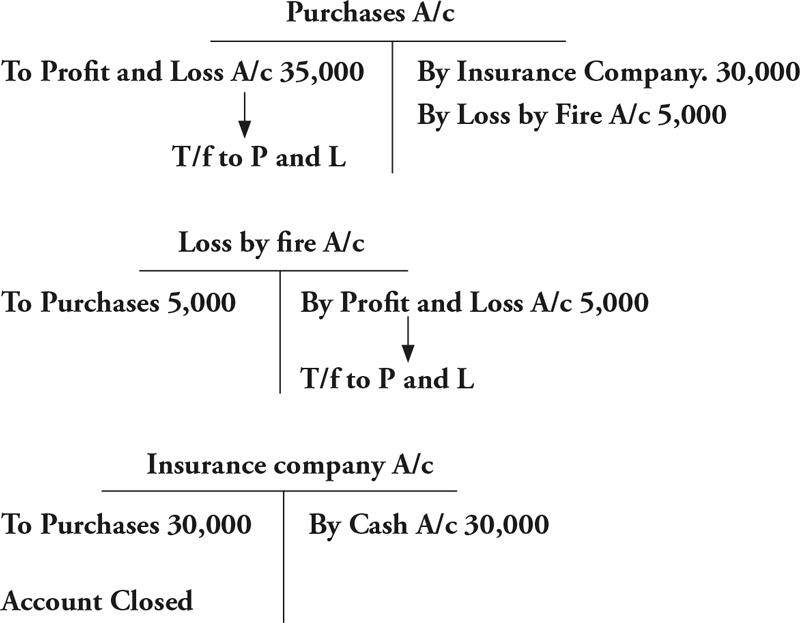

Loss by fire or theft

For example, stock in the godown worth Rs. 35,000 was destroyed by fire. Insurance company accepted the claim for Rs. 30,000.

Answer

Loss by fire or theft in a company has two aspects.

- The total stock decreases or we can say that the purchases decrease because the loss takes place from the stock in the godown which as our purchase.

- If the stock was insured, the company can recover the amount insured from the insurance company. Hence, there would be no loss to the company up to the amount insured. Only the excess amount will be the actual loss.

Thus, only Rs. 5,000 in this case would be the loss of the company since the remaining amount would be paid by the insurance company.

The following journal entries will be passed.

1. Insurance Company A/c Dr. | 30,000 |

Loss by Fire A/c Dr. | 5,000 |

To Purchases | 35,000 |

(Loss by fire recorded and insured amount receivable from insurance company.)

2. Profit and Loss A/c Dr. | 5,000 |

To Loss by Fire A/c | 5,000 |

(Loss transferred to Profit and Loss A/c)

3. Cash or Bank A/c Dr. | 30,000 |

To Insurance Company. | 30,000 |

(Amount received from Insurance company.)

Let us see its effect on the ledgers:

Balance Sheet

This is the ultimate statement that has to be prepared by a company to know the exact position of the business, that is, where it stands. It states what sources have been used by the company for financing and where such sources have been deployed.

It consists of Assets, Liabilities, and Equity, where

Assets = Liabilities + Equity

Uses of funds = Sources of funds

This always holds true since whatever funds are procured by the company should have been employed somewhere. This is stated by the Balance Sheet.

Given here for your reference is the format of the Balance Sheet:

Format of the Balance Sheet

Balance Sheet

Name of the Company..............

Balance Sheet as at..............

|

Particulars |

Note No. |

Figures at the end of the current reporting period |

Figures at the end of the previous reporting period |

|

1 |

2 |

3 |

4 |

|

I. EQOTY AND LIABILITIES 1. Shareholders Funds (a) Share Capital (b) Reserves and Surplus (c) Money received against share warrants 2. Share application money pending allotment 3. Noncurrent Liabilities (a) Long-term borrowings (b) Deferred tax liabilities (Net) (c) Other Long term liabilities (d) Long-term provisions 4. Current Liabilities (a) Short nam borrowings (b) Trade payables (c) Other current liabilities (d) Short term provisions |

|||

|

II. ASSETS 1. Non-Current Assets (a) Fixed Assets (i) Tangible Assets (ii) Intangible Assets (iii) Capital work-in-progress (iv) Intangible assets under development (b) Non-current Investments (c) Deferred Tax Assets (Net) (d) Long term loans and advances (e) Other non-current assets 2. Current Assets (a) Current Investments (b) Inventories (c) Trade Receivables (d) Cash and cash equivalents (e) Short-term loans and advances (f) Other current assets |

|||

|

TOTAL |

Let us now consider the constituents of:

- Assets

- Equity

- Liability

Assets

It consists of the following:

-

Noncurrent Assets: Those assets which are not current assets.

(a) Fixed Assets

(i) Tangible Assets: Assets which can be physically seen and touched

- Land

- Building

- Plant and Equipment

- Furniture and Fixture

- Vehicles

- Office Equipment

- Others

It is necessary to give the following information regarding each class or kind of fixed tangible asset.

a. Original cost

b. Addition (purchase)

c. Deductions (sale)

d. Total depreciation written off or provided for up to the end of the year.

(ii) Intangible Assets:

- Goodwill

- Brands or trademark

- Computer software

- Mastheads (name of newspaper or magazine printed at the top of the page) and publishing titles

- Mining rights

- Copyrights and patents

- Recipes, formulas, models, and designs

- Licenses and franchise

(iii) Capital Work-in-Progress:

Self-constructed item of property, plant, and equipment

(iv) Intangible Assets Under development:

Patents, intellectual property, and so on, which are being developed by the company

(b) Noncurrent Investments:

Investments that are held not with the purpose to resell but to retain them

(i) Trade Investments: Investments made by the company in shares or debentures of another company, not being its subsidiary, to promote its own trade and business

(ii) Other Investments: Those which are not trade investments.

- Investments in property

- In equity shares

- In preference shares

- In debentures

- In mutual funds

- In partnership firms

- In government securities

(c) Deferred Tax Asset (Net):

A deferred tax asset comes into force when taxable income is more than the accounting income.

(d) Long Term Loans and Advances:

Expected to be received back in cash or in kind after 12 months from the date of the B/S.

(i) Capital Advances: Advances for acquiring fixed assets

(ii) Security Deposits: Deposit for electricity, telephone, and so on given for a period beyond 12 months

(iii) Other loans and advances

- Long-term loan to employees

- Long-term advance to suppliers , and so on

(e) Other Noncurrent Assets

- Long-term Trade Receivables–receivable 12 months from the date of the B/S if the operating cycle is less than 12 months or beyond the operating cycle if the operating cycle is more than 12 months

- Others

- Insurance claim receivable

- Debts due by directors or other officers of the company

-

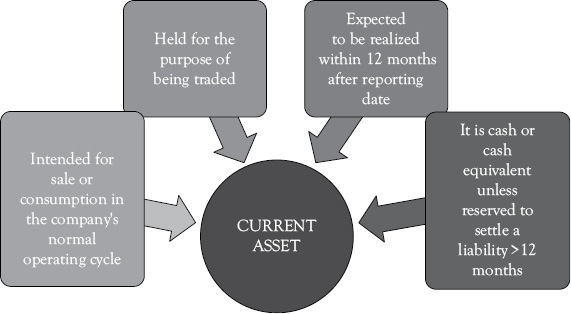

Current Assets

Current assets are those that satisfy any of the following conditions:

(a) Current Investments: Those investments which are held to be converted into cash within a short period, that is, within 12 months from the date of purchase of the investment.

Investments in partnership firms

In equity shares

In preference shares

In debentures

In mutual funds

In government securities

Short Term Investment

Marketable Securities

(b) Inventories: Refers to stock held for the purpose of trade in the normal course of the business, that is, for manufacturing or trading of goods.

(i) Raw Materials

(ii) Work-in-Progress

(iii) Finished Goods

(iv) Stock-in-Trade

(v) Stores and Spares

(vi) Loose Tools

(vii) Goods-in – Transit

(c) Trade Receivables:

Refers to the amount due on account of goods sold or services rendered in the normal course of business. It includes:

- Debtors

- Bills Receivable

(d) Cash and Cash Equivalents:

- Balance with banks

- Cheques, drafts in hand

- Cash on hand

- Earmarked balances with banks (e.g., for unpaid divided)

- Balances with banks held as margin money.

- Bank deposits with more than 12 months maturity

(e) Short-term Loans and Advances:

Expected to be realized within 12 months from the B/S date or within the operating cycles, if the operating cycle is more than 12 months.

- Loans and advances to related parties

- Others

(f) Other Current Assets

- Prepaid expenses

- Dividend receivable

- Interest accrued on investments

- Advance Tax

3. Contingent Liabilities and Capital Commitments:

(a) Contingent Liabilities: These liabilities refer to the claims that are uncertain to arise because they are dependent on an incident in the future.

They are not recorded in the books of accounts but disclosed in the Notes to Accounts.

- Claim against the company not yet acknowledged as debt

- Liabilities for bills discounted

- Guarantee given by the company

(b) Capital Commitments

A future liability for capital expenditure in respect of which contracts have been made.

- Uncalled amount on partly paid up shares

- Estimated amount of capital contracts remaining to be executed and not provided for (penalty)

- Other commitments: For example, arrears of cumulative dividend

Equity

It consists of the following:

-

Shareholders’ Funds

- Share Capital—Both equity and preference

- Reserves and surplus that is earned capital—capital reserve, security premium, capital redemption reserve, revaluation reserve, balance in profit and loss, that is, surplus or retained earnings

- Money received against share warrants

- Share application money whose allotment is pending

Liabilities

-

Noncurrent Liabilities

- Long-term borrowings

- Deferred tax liabilities

- Other long-term liabilities

- Long-term Provisions

-

Current Liabilities

- Short-term borrowings

- Trade payable

- Other current liabilities

- Short-term liabilities

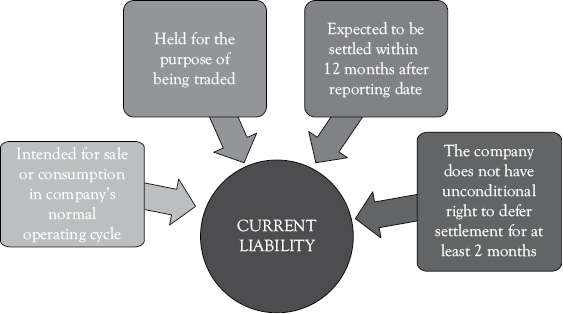

Current liabilities are those that satisfy any of the following conditions:

Working Capital = Current Assets − Current Liabilities

What is an Operating Cycle?

Operating cycle is the total time taken by a company to follow the whole process of converting its inventory into cash, that is, time taken to sell the inventory and realize cash.

Example

Let us continue with our previous question and prepare the Balance Sheet after the Profit and Loss Statement.

Answer

Those items in the Trial Balance that did not form part of the Profit and Loss Statement will become part of the Balance Sheet.

Step I

We will make a list of such items that should be included in the Balance Sheet.

Assets ![]() From debit side of Trial Balance

From debit side of Trial Balance

- Inventory

- Furniture

- Loan to directors

- Plant and machinery

- Current account

- Cash

- Fixtures

- Freehold land

- Tools and equipment

- Goodwill

- Trade receivables

Equity and liability

From credit side of trial balance - Equity share capital

- Debentures

- Bank loans

- Trade payables

- Profit and Loss Account

- Depreciation provision

Step II

Place the above mentioned items in the list under appropriate heads in the Balance Sheet.

Again, the details of each item should be shown separately in the Notes to Accounts.

Hari Chemicals Ltd.

Balance Sheet as on March 31, 2015

|

Note no. |

Amount (Rs.) |

Analysis (only for understanding) |

||

|

Equities and liabilities |

||||

|

(1) |

Shareholders’ funds |

|||

|

(a) Share capital |

1 |

25,00,000 |

|

|

|

(b) Reserves and surplus |

2 |

7,40,000 |

|

|

|

(2) |

Noncurrent liabilities |

|||

|

(a) Long-term borrowings |

3 |

11,45,000 |

|

|

|

(3) |

Current liabilities |

|||

|

Trade payables |

2,81,000 |

|

||

|

Total |

46,66,000 |

|||

|

Assets |

||||

|

(1) |

Noncurrent assets |

|||

|

Fixed assets: |

||||

|

(a) Tangible assets |

4 |

30,05,000 |

|

|

|

(b) Intangible assets |

2,65,000 |

|

||

|

(2) |

Current assets |

|||

|

(a) Inventories |

8,23,000 |

|||

|

(b) Trade receivables |

4,40,000 |

|||

|

(c) Cash and cash equivalents |

5 |

53,000 |

|

|

|

(d) Short-term loans and advances |

6 |

80,000 |

|

|

|

Total |

46,66,000 |

|||

Notes to Accounts

|

1. Share capital Authorized: Equity share capital of C 10 each Issued and Subscribed: Equity share capital of C 10 each |

G 25,00,000 25,00,000 |

||

|

2. Reserves and Surplus Balance as per last balance sheet Balance in profit and loss account |

1,39,000 6,01,000 7,40,000 |

||

|

3. Long term Borrowings 11% Debentures Bank loans |

5,00,000 6,45,000 11,45,000 |

||

|

4. Tangible Assets |

|||

|

Gross block |

Depreciation |

Net Block |

|

|

Freehold land |

15,46,000 |

15,46,000 |

|

|

Furniture |

2,00,000 |

2,00,000 |

|

|

Fixtures |

3,00,000 |

3,00,000 |

|

|

Plant and Machinery |

8,60,000 |

1,46,000 |

7,14,000 |

|

Tools and Equipment |

2,45,000 |

2,45,000 |

|

|

Total |

31,51,000 |

1,46,000 |

30,05,000 |

|

5. Cash and cash equivalents Current account balance Cash |

45,000 8,000 53,000 |

||

|

6. Short-term loans and Advances Loan to directors |

80,000 |

Let us take one more example

Example

From the following particulars of Y Ltd., prepare its Balance Sheet as on March 31st, 2013 along with notes to accounts.

|

Particulars Issued equity share capital 7,000 shares @ Rs. 10 each Issued and subscribed 6% preference share capital Rs. 1,000 @ Rs. 100 each Calls in arrear Rs. 3 on 100 shares |

Amount 70,000 1,00,000 |

|

500, 5% debentures of Rs. 1,000 each Short term loan from bank Debtors Provision for doubtful debts Provision for taxation General reserve Statement of P/L (Dr.) Marketable securities |

5,00,000 10,000 5,000 200 1,000 4,000 6,000 500 |

Answer

Step I

We will take each item one by one and identify the head under which it would be presented.

Equity share capital |

Share capital |

|

Preference share capital |

Share capital |

|

Calls in arrears |

Share capital (will be subtracted since it is not yet paid) |

|

Debentures |

Noncurrent liabilities, since it is long term |

|

Short-term loan from bank |

Current liabilities, since it is for short period |

|

Debtors |

Current assets |

|

Provision for doubtful debts |

Current liabilities, since it is only for current period |

|

Provision for taxation |

Current liabilities, since it is only for current period |

|

General reserve |

Reserves and surplus |

|

Statement of P/L (Dr.) |

Reserves and surplus (will be shown as negative amount since it is a debit balance) |

|

Marketable securities |

Current assets, since it is for short term |

Step II

We will now present it in an appropriate manner along with the notes to accounts.

Balance Sheet of Y Ltd.

As on March 31, 2013

|

Particulars |

Note No. |

31.03.2013 |

31.03.2012 |

|

1 |

2 |

3 |

4 |

|

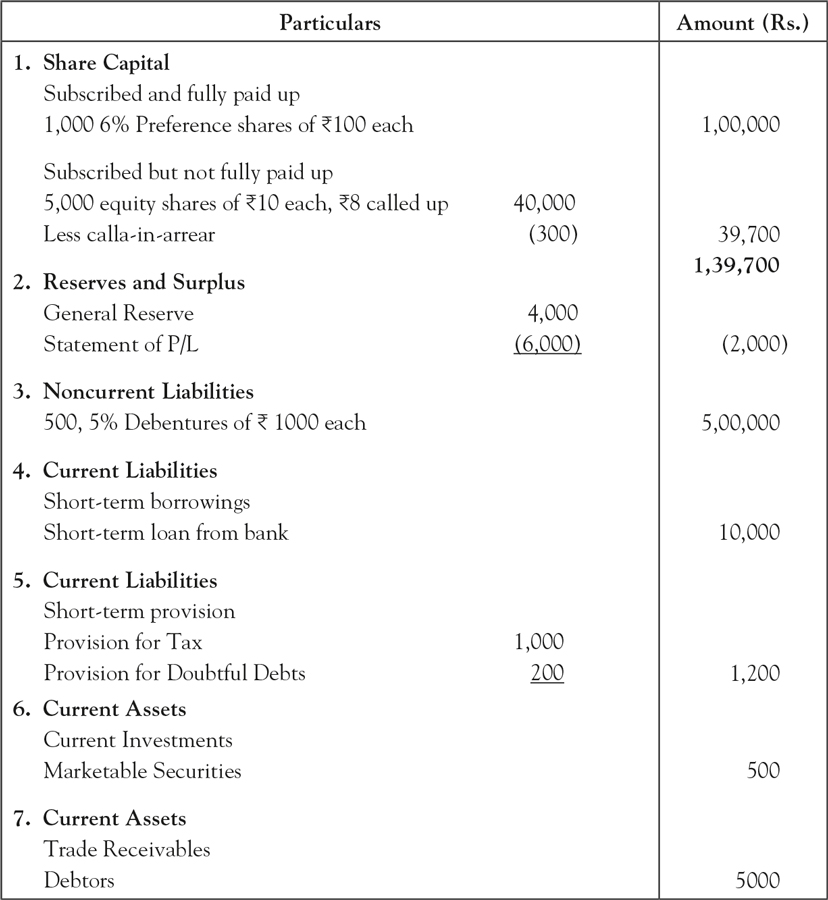

I. EQUITY AND LIABILITIES Shareholders Funds (a) Share Capital (b) Reserves and Surplus Non-Current Liabilities Long-term borrowings Current Liabilities (a) Short term borrowings (b) Short term provisions |

1 2 3 4 5 |

1,39,700 (2,000) 5,00,000 10,000 1,200 |

|

|

TOTAL |

|||

|

II. ASSETS Current Assets (a) Current Investments (b) Trade Receivables |

6 7 |

500 5,000 |

|

|

TOTAL |

Notes to Accounts: