Chapter 17

Understanding Financial Reports

In This Chapter

Loving the kudos with income, not loss

Feeling the heat? Read your Balance Sheet

Wallowing in profit with not a bean in your pocket

Plotting trends to see what the future intends

In this chapter, I don’t explain how to generate financial reports, but instead focus on how to understand financial reports. I address key questions such as ‘Why does this report show a profit yet there’s no cash in the bank?’, ‘Why don’t tax payments show up as an expense?’ and ‘How can I compare one year against another?’

Most business owners don’t expect bookkeepers to understand financial reports, and many accountants are concerned that bookkeepers aren’t sufficiently qualified to provide advice in this area. However, understanding the basic format of a Profit & Loss or Balance Sheet report is quite different to providing financial planning or taxation advice.

![]() A bookkeeper who isn’t afraid to produce financial reports, read them and consider the results is going to be a much better bookkeeper than someone who just does data entry and never considers the consequences. By lifting your skills this extra notch, you can be a great asset to any business (even if your value isn’t listed on the Balance Sheet).

A bookkeeper who isn’t afraid to produce financial reports, read them and consider the results is going to be a much better bookkeeper than someone who just does data entry and never considers the consequences. By lifting your skills this extra notch, you can be a great asset to any business (even if your value isn’t listed on the Balance Sheet).

Telling the Story with Profit & Loss

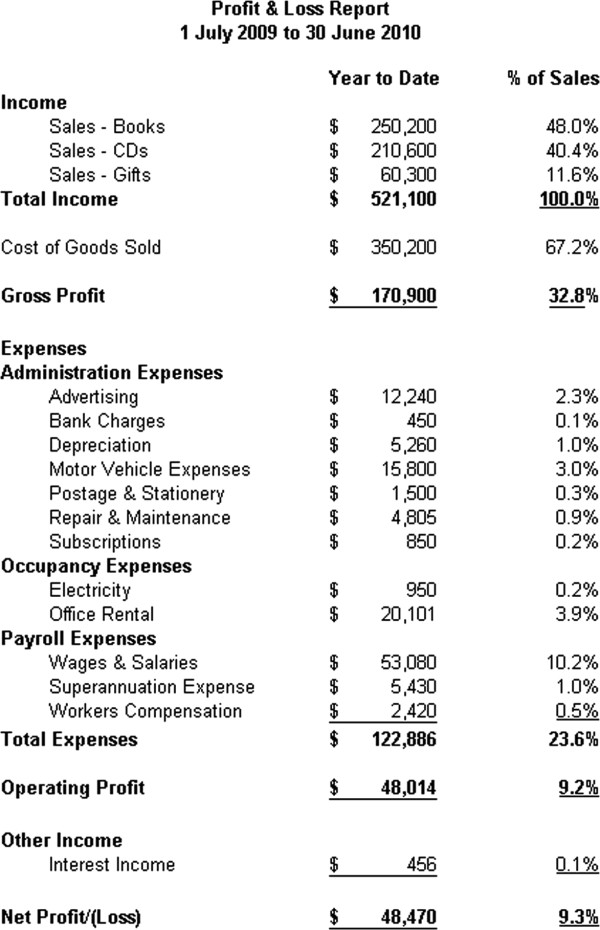

A Profit & Loss report is a story, telling you how your business has fared over the past few days, months or even years. It lists sales at the top, purchases and expenses in the middle and a final profit (or loss) figure at the bottom, giving a quick and simple indication of whether a business is blooming with health or is as sick as a dog. You can see a typical Profit & Loss report in Figure 17-1.

Figure 17-1: A typical Profit & Loss report.

![]() Although most Profit & Loss reports are pretty easy to understand, don’t be tempted into thinking that a profit is cause for partying and a loss is reason for a maudlin drinking bout. The important thing is to understand not only what the bottom line is, but why the business made a profit (or loss!) in the first place.

Although most Profit & Loss reports are pretty easy to understand, don’t be tempted into thinking that a profit is cause for partying and a loss is reason for a maudlin drinking bout. The important thing is to understand not only what the bottom line is, but why the business made a profit (or loss!) in the first place.

Putting income under the microscope

When you look at income in a Profit & Loss report, bear the following in mind:

![]() Income figures on a Profit & Loss report don’t include GST. For this reason, the income figures on your Profit & Loss report may not match with the income figures on your sales and GST reports.

Income figures on a Profit & Loss report don’t include GST. For this reason, the income figures on your Profit & Loss report may not match with the income figures on your sales and GST reports.

Unless you specifically request a cash-based Profit & Loss report, the income on a standard Profit & Loss report shows income that the business earns, and not cash that the business receives. For example, imagine I make a single sale during March for $10,000, and no sales in the month of April, but I receive payment for my March sale on 1 April. In this scenario, my Profit & Loss reports show $10,000 income in March and zilch in April, even though April is when I received the cash.

Some accountants like to separate non-trading income, such as interest or investment income, into a heading called Other Income that sits at the bottom of a Profit & Loss report.

![]() When you look at the income on a Profit & Loss report, ask yourself whether the income section of this report provides enough information. For example, do you also want to see how much income is generated from different business divisions, locations, jobs or projects?

When you look at the income on a Profit & Loss report, ask yourself whether the income section of this report provides enough information. For example, do you also want to see how much income is generated from different business divisions, locations, jobs or projects?

![]() Traps for the unwary

Traps for the unwary

All financial reports, such as Profit & Loss and Balance Sheet reports, show figures not including GST. That’s because GST isn’t really income or an expense, rather GST is something that you owe to the government (when you collect GST on sales) or something you are owed from the government (when you pay GST on expenses).

Seems easy, but do keep your wits about you when comparing one report against another. For example, although a Profit & Loss report doesn’t include GST, some sales reports may, depending on the software. A budget doesn’t include GST, but a cashflow report usually does.

I like to group income into at least four or five categories (something I talk about in Chapter 2), but within these categories, I often like to track the income from individual cost centres. This kind of detailed tracking is usually only practical if you use accounting software. In MYOB, the jobs and categories features provide a way to get more detail about income sources; in QuickBooks, the best approach is to use either Customer/Job details, or class tracking.

Weighing up gross profit

Cost of sales accounts are variable expenses that relate directly to sales (for more on the topic, see Chapter 2). Cost of sales accounts appear below the income accounts in a Profit & Loss report; the total of these accounts is called cost of goods sold.

If you deduct total cost of goods sold from total income, you arrive at a figure called gross profit. For example, in Figure 17-1, the total income is $521,100, the total cost of goods sold is $350,200 and the gross profit is $170,900. The percentage of gross profit against sales — 32.8 per cent in Figure 17-1 — is called the gross profit margin.

![]() As a bookkeeper, make sure you report gross profit correctly, and that the Profit & Loss report includes all variable expenses in the cost of goods sold section of the report. In the perfect world, even if total sales fluctuate and total cost of goods sold fluctuate, the gross profit margin itself should always remain relatively constant.

As a bookkeeper, make sure you report gross profit correctly, and that the Profit & Loss report includes all variable expenses in the cost of goods sold section of the report. In the perfect world, even if total sales fluctuate and total cost of goods sold fluctuate, the gross profit margin itself should always remain relatively constant.

![]() Be wary of miscellaneous accounts

Be wary of miscellaneous accounts

One of my pet hates is seeing any amount on a Profit & Loss report called Miscellaneous Income, Miscellaneous Expense or General Expenses. These accounts are invariably dumping grounds for all the transactions that the bookkeeper can’t find a home for.

If any of your reports include a total for Miscellaneous Income, Miscellaneous Expense or General Expenses, go do a transaction report for that account. Weed through every transaction and for each one, find a better home for it to live (and, if you’re not sure where, ask the company accountant for assistance).

Oh yes, and if you’re the culprit who has been dumping transactions into these accounts, stop right now! Instead, create an expense account called Suspense and allocate anything that you’re not sure about into this account. At the end of every month, email a transaction report for this account to the company accountant, and ask for help allocating these transactions correctly.

Watching expenses, dollar for dollar

You may be wondering what there is to understand when looking at expenses on a Profit & Loss report. After all, an expense is just an expense, isn’t it? Well, maybe not quite. Keep two things in mind:

![]() Expenses are different from expenditure. Expenditure includes not just regular expenses, but also money spent on capital equipment. (You allocate capital expenditure to an asset account in the Balance Sheet, and not to an expense account in the Profit & Loss.) Therefore, while a Profit & Loss report shows all business expenses, it doesn’t show all business expenditure.

Expenses are different from expenditure. Expenditure includes not just regular expenses, but also money spent on capital equipment. (You allocate capital expenditure to an asset account in the Balance Sheet, and not to an expense account in the Profit & Loss.) Therefore, while a Profit & Loss report shows all business expenses, it doesn’t show all business expenditure.

Unless you specifically request a cash-based Profit & Loss report, expenses show up in the Profit & Loss as soon as you record the bill, regardless of when you pay the supplier.

In addition to understanding how expenses appear on a Profit & Loss report, take action if the report itself looks like a dog’s breakfast (there’s nothing worse than a Profit & Loss report that lists pages of expenses in no particular order):

![]() If a business has a lot of expenses, group them into headings. Refer back to Figure 17-1, where I break expenses into Administration Expenses, Occupancy Expenses and Wages & Salary Expenses.

If a business has a lot of expenses, group them into headings. Refer back to Figure 17-1, where I break expenses into Administration Expenses, Occupancy Expenses and Wages & Salary Expenses.

Within each heading, keep expenses in alphabetical order. If you’re using accounting software, you may need to re-number your expense accounts in order to get them to print in order.

If you get an expense account with a piddly amount in it at the end of 12 months (less than $100 or so), get rid of it by combining this account with another similar expense account. The less clutter, the better.

![]() Calculating depreciation is usually a task that falls to the company accountant, and not the bookkeeper. If you’re generating a draft Profit & Loss report for management to review, you may want to add a note that depreciation isn’t included, and the profit may be overstated.

Calculating depreciation is usually a task that falls to the company accountant, and not the bookkeeper. If you’re generating a draft Profit & Loss report for management to review, you may want to add a note that depreciation isn’t included, and the profit may be overstated.

Painting a Picture with the Balance Sheet

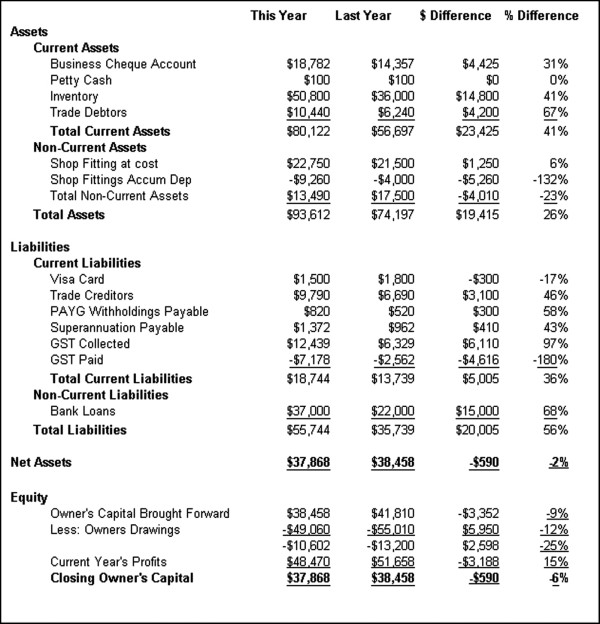

A Profit & Loss report tells a story about what’s going on in a business over any period of time. In contrast, a Balance Sheet shows a candid snapshot of how much a business owns and how much it owes at any point in time.

In Figure 17-2, my sample Balance Sheet starts by listing assets (such as the bank account, stock on hand, furniture, computer equipment and so on), and then moves to liabilities (credit cards, supplier accounts, loans and the like). The bottom line finishes with a flourish, calculating the difference between assets and liabilities. This figure represents the equity: the owner’s or shareholders’ stake in the business.

Figure 17-2: A Balance Sheet provides a snapshot showing the assets and liabilities of a business.

![]() If an auditor wants to check a set of accounts, their main tactic is usually to verify the balance of every single account in the Balance Sheet. (Why? Because if both the opening and the closing Balance Sheets for any given period are correct, the auditor can be sure the report that connects the two, namely the Profit & Loss report, is also correct.) As a bookkeeper, feel free to take a leaf out of the auditor’s book and aim not only to understand every account on the Balance Sheet, but be confident that the balance of every account is correct also.

If an auditor wants to check a set of accounts, their main tactic is usually to verify the balance of every single account in the Balance Sheet. (Why? Because if both the opening and the closing Balance Sheets for any given period are correct, the auditor can be sure the report that connects the two, namely the Profit & Loss report, is also correct.) As a bookkeeper, feel free to take a leaf out of the auditor’s book and aim not only to understand every account on the Balance Sheet, but be confident that the balance of every account is correct also.

Sketching assets, black as ink

At first glance, understanding the assets section of a Balance Sheet is simple. Assets are just a list of what the business owns, right? Sure. But in order to make sure you understand the assets section of a Balance Sheet, you may want to dig a little deeper:

A standard Balance Sheet starts by listing all bank accounts and cash balances. Easy to understand, but as a bookkeeper, you want to make sure that every single one of these balances is correct, up to date and matches with bank statements for the same period.

Next on a Balance Sheet, also included in current assets (for definitions of current, non-current and intangible assets, refer to Chapter 2), you get Accounts Receivable and Stock on Hand. Your job is to check that Accounts Receivable matches against the Aged Receivables report, and that Stock on Hand matches against your inventory valuation report for that period. (I explain this process in much more detail in Chapter 15.)

![]() Non-current assets are next on the scene, shown at historical cost (in other words, the original cost of the asset) less depreciation. Beware that historical cost isn’t necessarily a good indicator of what an asset is worth. Land and buildings in particular tend to increase in value over time, and historical cost doesn’t reflect this. (For more about asset values and depreciation, refer to Chapter 13.)

Non-current assets are next on the scene, shown at historical cost (in other words, the original cost of the asset) less depreciation. Beware that historical cost isn’t necessarily a good indicator of what an asset is worth. Land and buildings in particular tend to increase in value over time, and historical cost doesn’t reflect this. (For more about asset values and depreciation, refer to Chapter 13.)

![]() If you’re doing a super-conscientious job, don’t forget to compare the value of fixed assets on your Balance Sheet against the values on your depreciation schedule. (After all, isn’t this a more worthy task than updating your Facebook status?) For more details, refer to Chapter 13.

If you’re doing a super-conscientious job, don’t forget to compare the value of fixed assets on your Balance Sheet against the values on your depreciation schedule. (After all, isn’t this a more worthy task than updating your Facebook status?) For more details, refer to Chapter 13.

Intangible assets come last, and include assets such as company formation expenses, franchise purchase fees, goodwill, intellectual property and trademarks. With intangible assets, bear in mind that the value shown on the Balance Sheet doesn’t necessarily reflect an asset’s real worth. Goodwill in particular may be overstated or understated, as the value in the Balance Sheet usually only shows the amount a business paid for goodwill, and this payment could have been many years ago.

![]() Opening balances and other headaches

Opening balances and other headaches

If you’re using accounting software, you may find that the Balance Sheet you generate doesn’t match up with the Balance Sheet from your accountant. This discrepancy has two likely causes: Either you didn’t set up opening balances correctly when you first installed the software, or you haven’t adjusted your Balance Sheet to match the accountant’s at year end (or maybe both!).

The best approach for setting up opening balances depends on the software you’re using. Usually, you can’t set up every opening balance straight away, because the company accountant takes a few months to finalise accounts for the previous year. No worries — even if many months go by until you receive a Balance Sheet for the year just gone, you can still go back and complete your opening balances.

If the cause of your problem is that the accountant made adjustments to your previous year’s figures, and you haven’t yet brought the Balance Sheet into line with the accountant’s, then you need to take a different tack. I talk more about year-end procedures in Chapter 18.

Drawing liabilities, red as blood

Liabilities include everything that a business owes to others, such as credit card accounts, supplier bills, GST owing and bank loans. Make sure that you give the liabilities in your Balance Sheet the love they deserve:

![]() Make sure the balances of any credit cards equal credit card statements for the same period.

Make sure the balances of any credit cards equal credit card statements for the same period.

Check out the balance of Accounts Payable and make sure this balance is the same as the Aged Payables report for the same period. (If not, Chapter 15 can come to the rescue.)

Make sure any loans that appear in the Balance Sheet match with bank loan statements for the same period. You may also want to double-check the balances of any hire purchase accounts.

Sculpting equity, cast in gold

The equity section of a Balance Sheet represents the interest that shareholders or an owner has in the business, including both capital contributed and the profit or loss built up over time. And, as I explain in Chapter 3, because debits always equal credits, total equity always equals the difference between assets and liabilities.

If you’re looking for a more intuitive understanding of equity, maybe a real-life example will help. Imagine you pitch up in the desert with two mates, Bruce and Wayne. You have ten bucks in your pocket when you arrive. The state of play is

Assets $10 Liabilities $0 Equity $10

After a fabulous game of poker, you still have ten bucks but you owe Bruce two dollars and Wayne owes you three dollars. You’re one dollar ahead! The state of play now is

Assets $13 Liabilities $2 Equity $11

In other words, you still only have $10 in your pocket, but the equity in your noble poker business has increased. To calculate equity, you add up all the assets (including things like cash, customer accounts owing, motor vehicles and so on), and then subtract all the liabilities (stuff like credit cards, supplier accounts outstanding and loans).

The equity section of your Balance Sheet always equals the difference between assets and liabilities. If total equity is a positive figure, the business has made a profit over time and some of this profit has been left in the business (either that, or the business owner/shareholders have put their own capital into the business). If total equity is a minus figure, that means the business has made a loss over time or that business owners/shareholders have taken out more than they have put in (or a combination of both).

Understanding the Relationship between Profit and Cash

I can’t believe how often clients ask, ‘Veechi, my reports say I’m making heaps of profit, but how come there’s nothing in the bank?’ Similarly, I occasionally witness clients who are wallowing in cash and living the high life, even though their Profit & Loss reports are decidedly gloomy.

![]() The long and short of it all — profit doesn’t equal cash and cash doesn’t equal profit.

The long and short of it all — profit doesn’t equal cash and cash doesn’t equal profit.

Why there’s profit but no cash

Why is it that sometimes a Profit & Loss report shows that a business is doing well but there’s no cash anywhere to be seen? I set out a few possible explanations here:

The tax hounds have got in on the act: The sad truth of the matter is that as soon as a business makes any profit, it has to pay tax. Tax payments chew up cash, but usually don’t show on Profit & Loss reports (see the sidebar ‘Where tax fits in’ for more details).

The cash has gone towards buying new equipment: Any new gear that costs more than a certain amount (between $100 and $1,000 depending on whether the business operates in Australia or New Zealand and what tax concessions are available — see Chapter 13 for details) isn’t immediately tax-deductible and so doesn’t show up as an expense on the Profit & Loss report, but gets listed as an asset instead.

The business has repaid loans: Loan repayments don’t usually show up as expenses, meaning that loan repayments gobble up cash but don’t affect the profit.

Customers owe heaps of money: If a business bills a customer in April, the Profit & Loss report shows this income in April, even though the business may not receive the cash until weeks or months later. If you look at the Profit & Loss report for the whole year and customers owe more at the end of the year than they did at the beginning, the difference is a direct drain on cash.

![]() Where tax fits in

Where tax fits in

Business owners and bookkeepers often get confused about where income tax payments appear in a Profit & Loss report.

If a business has a sole trader or partnership structure, then any income tax payments are of a personal nature, and don’t show up as an expense in the Profit & Loss, and instead get allocated to Owner’s Drawings or Partner’s Drawings. (If only I could claim my tax payments as a tax deduction, life would be that much sweeter . . . )

If a business has a company structure, then income tax payments show at the very bottom of the Profit & Loss report, so that you have a total called Net Profit before Company Tax, followed by a total for Company Tax, followed by a final total called Net Profit after Company Tax.

Why there’s cash but no profit

It may be easy to grasp why a business may not have any cash even though the business is turning a profit. However, what about the opposite scenario, where a business is rolling in cash but the Profit & Loss reports look decidedly gloomy? In many ways, this situation is even worse, because the business owner can all too easily get lulled into a false sense of security, spending beyond their means.

Here are some reasons why cash may be rosy but profit grim:

![]() The business receives a loan: Loans are both a blessing and a curse. When a business receives a loan, the sudden influx of cash can burn a hole in the thickest of pockets.

The business receives a loan: Loans are both a blessing and a curse. When a business receives a loan, the sudden influx of cash can burn a hole in the thickest of pockets.

Creditors are building up: A business can get by for quite a while making a loss but staying afloat, simply by running up outstanding accounts. If a business starts to stretch out suppliers to 60, 90 or even 120 days, it not only generates a fair amount of bad feeling, but wads of cash also.

Stock is running down: If stock levels go down, the business has more cash available. Simple as that.

Reporting where cash came from, and where it went

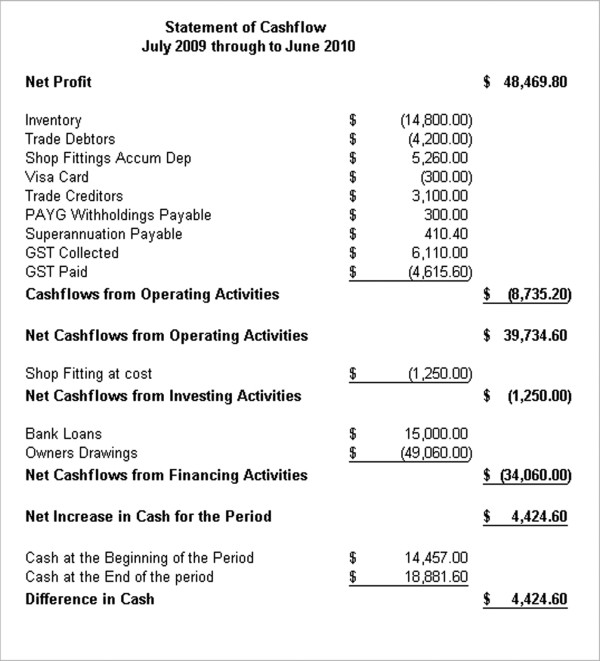

![]() When looking at cashflow, accountants sometimes refer to a Statement of Cashflow, a special report that examines the cashflows in and out of a business, and goes a long way towards explaining the mystery of why a business has a handsome profit, but no cash, or vice versa. Although fairly complex to assemble by hand, many accounting software packages offer this report as standard.

When looking at cashflow, accountants sometimes refer to a Statement of Cashflow, a special report that examines the cashflows in and out of a business, and goes a long way towards explaining the mystery of why a business has a handsome profit, but no cash, or vice versa. Although fairly complex to assemble by hand, many accounting software packages offer this report as standard.

In Figure 17-3, I show a Statement of Cashflow report that connects the Profit & Loss report in Figure 17-1 with the Balance Sheet in Figure 17-2. The Difference column in the Balance Sheet shows how I arrive at the figures on this report. Cash outflows (cash going out of the business) show as negative amounts; cash inflows (cash coming in to the business) show as positive amounts.

The top section of my Statement of Cashflow report shows business operating activities used up $8,735 of cash, with $14,800 going to an increase in stock holdings. Investment activities show that new shop fittings chewed up $1,250 in cash, and financing activities show that the owner’s personal drawings sucked up $49,060. The fact that the business had more cash in the bank at the end of the period than it did at the beginning is mainly attributable to the $15,000 bank loan it received.

![]() Many people think that a cash-based Profit & Loss report does the same job as a Statement of Cashflow report. Not true. As you can see from Figure 17-3, a Statement of Cashflow includes a lot of information that you don’t get on a cash-based Profit & Loss, such as details about bank loans, owner’s drawings and new equipment purchases.

Many people think that a cash-based Profit & Loss report does the same job as a Statement of Cashflow report. Not true. As you can see from Figure 17-3, a Statement of Cashflow includes a lot of information that you don’t get on a cash-based Profit & Loss, such as details about bank loans, owner’s drawings and new equipment purchases.

Figure 17-3: A Statement of Cashflow explains the difference between profitability and cash in the bank.

Putting Results Under the Microscope

Sometimes a set of financial statements doesn’t provide quite enough information, especially if you want to look at the stability of a business.

If I’m doing a detailed analysis into the health of a business, I like to get hold of at least three years’ worth of financials, so that I can graph sales and expenses and examine the overall trends. This level of scrutiny often yields a surprising amount of information.

![]() As a bookkeeper for a business, you can provide extra insights for management by doing this extra level of financial analysis. In this section of the chapter, I explain how to compare one year’s results against another’s, and how to do some simple ratio calculations.

As a bookkeeper for a business, you can provide extra insights for management by doing this extra level of financial analysis. In this section of the chapter, I explain how to compare one year’s results against another’s, and how to do some simple ratio calculations.

Comparing this year against last year

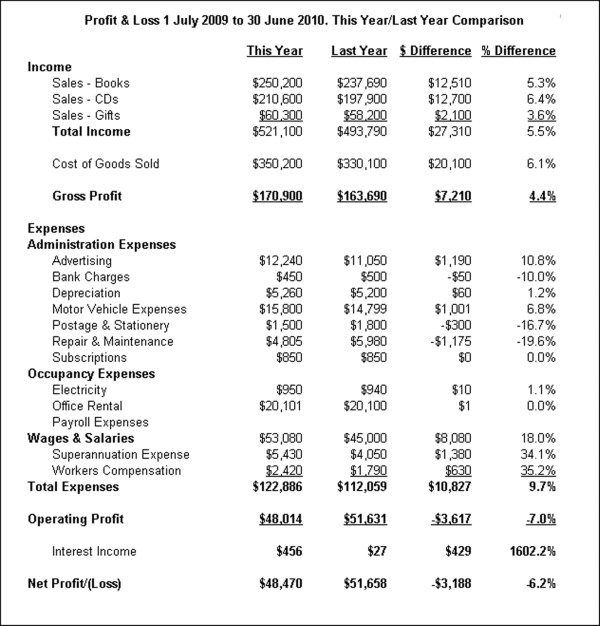

![]() If a business has been operating for more than a couple of years, you can tell a great deal by comparing the results of the current year against the results of the previous year. I like to go through both the Balance Sheet and the Profit & Loss reports and compare last year’s result against the current year’s result for every single account. In particular, I like to calculate the difference between the years on both a dollar basis and a percentage basis, as I do in Figure 17-4 (if the accounting software doesn’t provide this information as standard, I send the report into Excel and create a custom report myself ).

If a business has been operating for more than a couple of years, you can tell a great deal by comparing the results of the current year against the results of the previous year. I like to go through both the Balance Sheet and the Profit & Loss reports and compare last year’s result against the current year’s result for every single account. In particular, I like to calculate the difference between the years on both a dollar basis and a percentage basis, as I do in Figure 17-4 (if the accounting software doesn’t provide this information as standard, I send the report into Excel and create a custom report myself ).

I can’t tell you exactly what to look out for, because every business is different, but all you need is an eye for detail and a decent dose of common sense. For example, check out Figure 17-4, which compares a Profit & Loss report from one year to the next. Here are just some of the questions a report like this would make me ask:

On a positive note, sales are up by 5.5 per cent. Looks healthy, but how do other businesses in the same industry compare? Also, what was the inflation rate for that year?

On a gloomy note, gross profit hasn’t quite increased by the same percentage. Unless a business changes pricing policies, the gross profit percentage normally increases at the same rate as sales. Is there a mistake in the accounts or is the business genuinely making a tad less profit on every sale?

Expenses are all pretty consistent, with the notable exception of a whopping increase of 18 per cent in wages, which represents over $8,000 in additional costs. Why did wages go up so much? Was this change warranted?

The final net profit result is disappointing: Despite a solid increase in sales, the net profit is actually less than the previous year, primarily due to an increase in wages that far exceeds the increase in sales, and a decline in the gross profit margin. Does management realise this has occurred, and what steps do they intend to take to turn this trend around?

This process isn’t rocket science, is it? I suggest you waste not a moment longer: Chuck this book unceremoniously on the floor and go compare a current year’s Profit & Loss report against a previous year’s. I bet you can spot at least ten things worth investigating before the day is done.

Figure 17-4: Compare this year against last year as part of checking your work.

Calculating ratios

Open any accounting theory book and you soon find a chapter chock-a-block full of ratios: Calculations that look at the relationship between one financial figure and another and, from the result, arrive at conclusions about the health of a business. You get ratios for accounts receivable, asset usage, liquidity, profitability, rate of return, working capital and much more.

I’m going to keep things simple right now — after all, you’re probably not responsible for analysing the financial results of BHP — and concentrate on three important ratios: Your accounts receivable ratio, your stock turnover ratio, and your quick ratio.

Accounts receivable ratio

Your accounts receivable ratio is a quick measure of the success of your debt collection activities (a delightful topic that I deal with in more detail in Chapter 20).

To calculate this ratio, simply divide total sales for the past 12 months by the current value of accounts receivable. For example, if total sales for the last 12 months were $250,000 and the business is currently owed $50,000, the accounts receivable ratio is:

$250,000/$50,000 = 5

If you get really excited by this calculation, go one step further and divide the number of days in a year by this ratio:

365/5 = 73

This ratio means that it takes an average of 73 days for customers to pay up, which incidentally would be a pretty pitiful average in anyone’s book.

Stock turnover ratio

Your stock turnover ratio is an important measure of how well a business manages stock levels. To calculate this ratio, you first divide total cost of sales by average stock on hand (valued at cost) for the past 12 months, and then you divide 365 (the number of days in the year) by this result.

For example, in Figure 17-2, the closing stock on hand was $50,800, and the total cost of sales for the same period was $350,200, so the stock turnover is:

$350,200/$50,800 = 6.89

This means that stock turns over about seven times per year. To calculate the ratio, you divide the number of days in the year by this result.

365/6.89 = 53

This stock turnover ratio of 53 means that stock turns over, on average, every 53 days. Of course, some stock probably turns over much more frequently, and other stock sits on the shelf for months getting dusty, but this ratio provides an average.

![]() The higher the stock turnover ratio, the less money (relatively speaking) a business has tied up in stock, which means higher sales for the same amount of space. The lower the stock turnover ratio, the more likely it is that a business is carrying dud stock or buying more than it needs at one time.

The higher the stock turnover ratio, the less money (relatively speaking) a business has tied up in stock, which means higher sales for the same amount of space. The lower the stock turnover ratio, the more likely it is that a business is carrying dud stock or buying more than it needs at one time.

In order to assess whether a stock turnover ratio is reasonable, or not, you need to compare this business against other businesses of a similar kind. For example, a retailer selling fresh food is going to have a really high stock turnover ratio, but a retailer selling furniture is going to have a much lower stock turnover ratio.

Quick ratio (acid test)

The acid test ratio (also known as the liquid or the quick ratio) measures the liquidity of a business by looking at the relationship between current assets and current liabilities. This ratio is particularly brutal in that it specifically excludes the value of stock from current assets, with the justification being that stock is sometimes a problem to sell in a hurry, and isn’t always readily convertible to instant cash.

For example, total current assets in Figure 17-2 equal $80,122, but if I deduct stock from that figure, I arrive at a figure of only $29,322. Current liabilities equal $18,744.

To calculate my acid test ratio:

$29,322/$18,744 = 1.56

A ratio greater than 1 (where current assets less inventory are worth more than current liabilities) is a healthy sign, because this indicates that the business can pay its current liabilities without being dependent on the sale of inventory. A ratio less than 1 is supposedly a warning sign, at least as far as banks are concerned. Having said this, the weight a bank puts on the acid test ratio depends very much on the kind of business concerned.