6

KNOWING HOW YOU ARE GOING TO PAY FOR A HOUSE BEFORE YOU BUY

Before you make an offer to buy a house, you need to have a plan to pay for it. Your tenants can repay the money that you borrow if you pay a bargain price and borrow on better-than-market terms. The first step to making a profitable deal is to figure out how much income your tenants will generate.

You do not set the rent on a house; the market sets the rent. Some landlords try to rent their property for an amount equal to their loan payments. The tenants don’t care how much your loan payments are; they will pay the least amount of rent they can for the best house they decide they can afford. Tenants will compare the houses on the market and rent the one that is the best deal.

To determine how much rent you can expect to collect, you need to study your market. Good information is available because landlords advertise their houses on line and in your newspaper every week.

HOW MUCH CAN YOUR POTENTIAL TENANTS AFFORD TO PAY?

To determine the amount of rent you can collect, conduct a rent survey of your competing landlords. Identify your target neighborhoods and your price range for desired rent. Check rents on online sites that list rentals in your town, like Craigslist, and look for rental ads in your local paper.

Then look for houses advertised for rent in your price ranges and, if possible, in your target neighborhoods.

Once you’ve found a few listings, call the landlord and ask the questions any potential renter would ask (see below), noting his or her answers.

1. Have you rented the house?

2. How big are the house and yard?

3. Has the house be updated?

4. What appliances come with the house?

5. Is the yard fenced?

6. Is it on a busy street?

7. How much is the rent?

8. Will you accept kids and pets?

9. Is there a limit to how many people can live in the house?

10. How much is the security deposit?

11. How long must the lease be?

12. How long has the house been empty?

You cannot assume that all of the answers are true, but a smart landlord will be truthful. The answers are easy to check by looking at the house.

You want to sort through the responses and separate the smart landlords (those who are charging a reasonable rent and security deposit) from the others (those who are willing to rent to anyone).

A landlord who has low standards for tenants or who will rent to too many people, such as six college students, can charge more than market rate. After the bad tenant moves out and the landlord makes repairs to the house, he will net far less rent.

Likewise, some landlords will rent without requiring a last month’s rent or reasonable security deposit. They too can charge above-market rent, because they will let a tenant who has little money move in. These tenants often fall behind on their rent immediately because they don’t have any money!

Surprisingly, many landlords will not answer the phone or respond to an inquiry when they are paying a lot of money to support an empty house.

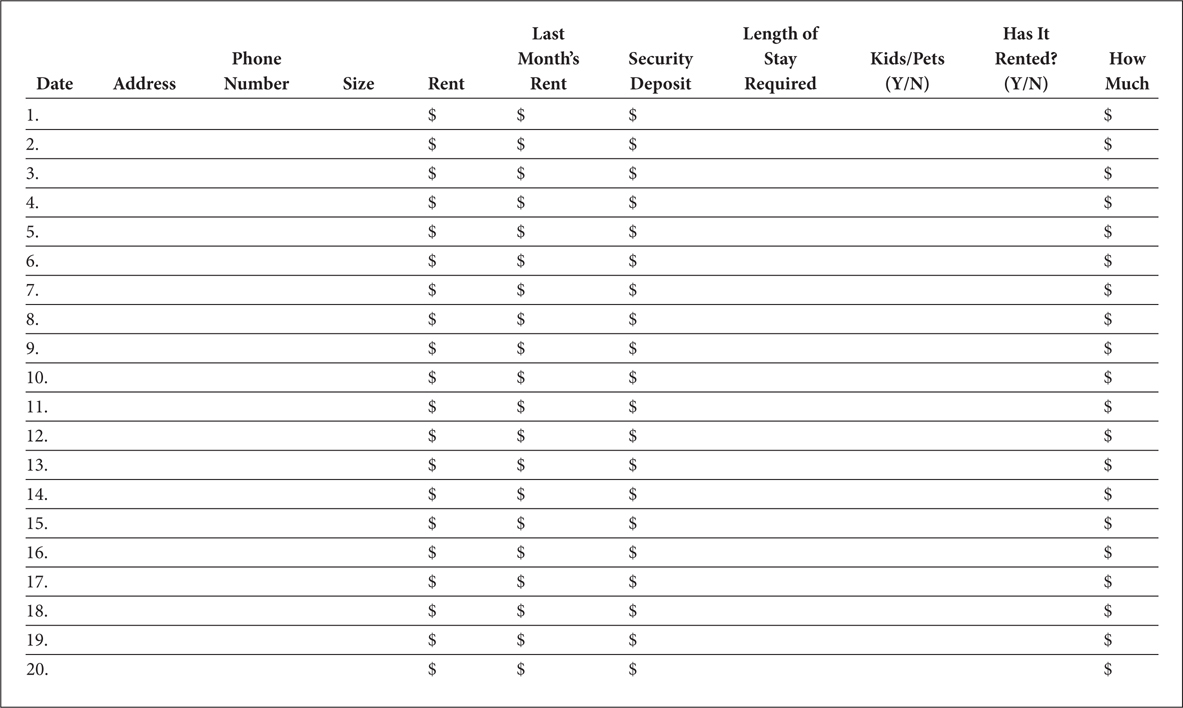

Prepare a chart like Table 6.1, and record the information you obtain when talking to the landlords. Next, go see the houses that have rented and the houses that are still for rent. Make notes about the neighborhood and the condition of the houses and start learning about your competition. Many landlords do not buy good properties, nor do they maintain the houses well. Try to buy in better neighborhoods, and keep your houses in good condition. This will reduce your vacancies because your houses will be the first to rent.

Table 6.1 Landlord Survey

Now that you have a good idea of what your competition is and have studied the amount of rents, deposits, and number of vacancies in your target neighborhood, you can make a good estimate of the amount of rent you can expect to collect.

RENTS AND PRICES GO UP, BUT AT DIFFERENT TIMES

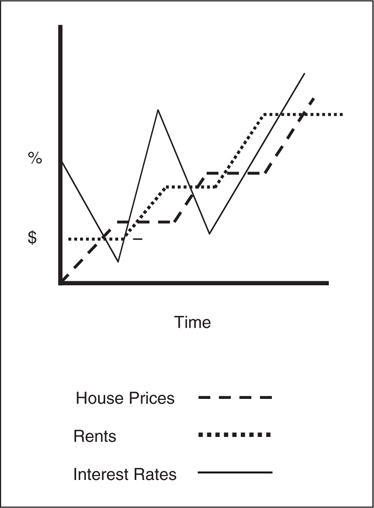

One big benefit of investing in houses is that your rents will increase significantly over the years, whereas your loan payments can remain the same until the loan is paid off. Rents tend to increase at the same rate as prices, but in different years.

In a hot real estate market, when prices are increasing rapidly, rents may be stable and may even drop. This is a result of low interest rates, which allow renters to buy houses and encourage builders to build. When interest rates are low and house prices are rising rapidly, many investors also buy houses and rent them. This increased supply of rental houses, coupled with many renters becoming homeowners, can keep rents low.

When interest rates rise, fewer renters can qualify to buy, and fewer investors buy houses for rental. These factors combine to cause a tight rental market, and rents rise as tenants compete for fewer houses. Understanding and recognizing these cycles in your town is important. Although rents will increase in the long run, these cycles often last several years at a time (see Figure 6.1).

FIGURE 6.1 The Impact of Interest Rates on House Prices and Rents

Notice that house prices increase in some years, are flat in others, and even occasionally drop. Although, when they drop, they rarely drop below the earlier low and when they recover, they often surpass the previous high.

This result is more pronounced in markets prone to big swings in prices. In a market where house prices just creep up every year, it will appear that rents and prices go up together.

Although rents and prices can experience short-term dips, in the long run both will increase with inflation. These dips will be larger in higher-priced properties.

HOW MUCH WILL YOU SPEND TO OPERATE THE HOUSE?

Every house will cost a different amount to operate. Well-designed and well-built homes that have been maintained and are well situated on good lots will be far less expensive to maintain than poorly designed and built homes on troublesome lots.

You want to buy a house that will produce the most income in relation to what it will cost to operate. You might think that a very small house that would be less expensive to maintain would be best. But you want a house that is large enough to attract a good long-term tenant, and you want it in a neighborhood that will reward you with appreciation.

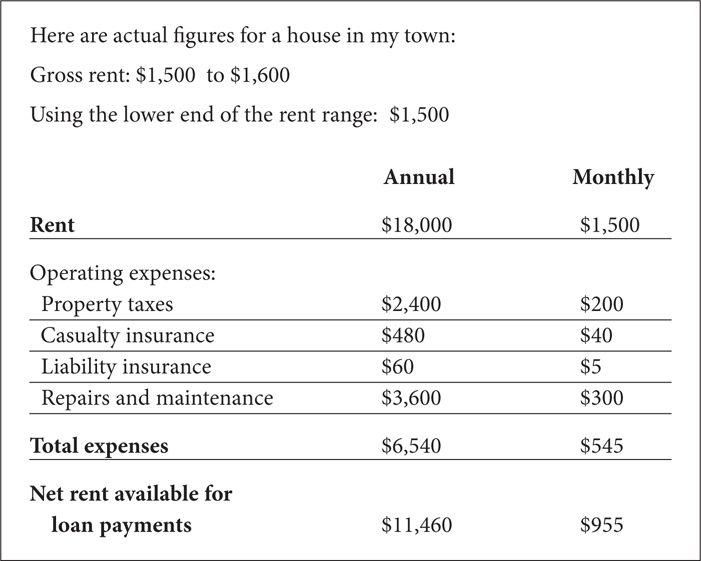

Use the worksheet in Figure 6.2 to project the income you will have to repay a loan.

FIGURE 6.2 Calculating the Income a House Will Produce

This assumes that you will manage the property yourself. If you plan to pay a manager, plug in his fee.

HOW MUCH CAN YOU BORROW AND REPAY WITH THE RENT YOUR TENANTS PAY?

Interest rates change constantly. When you buy a house for investment, try to borrow on a long-term, fixed-interest-rate loan. Then you will be able to predict your cash flow accurately and benefit as rents increase and your loan payment stays constant.

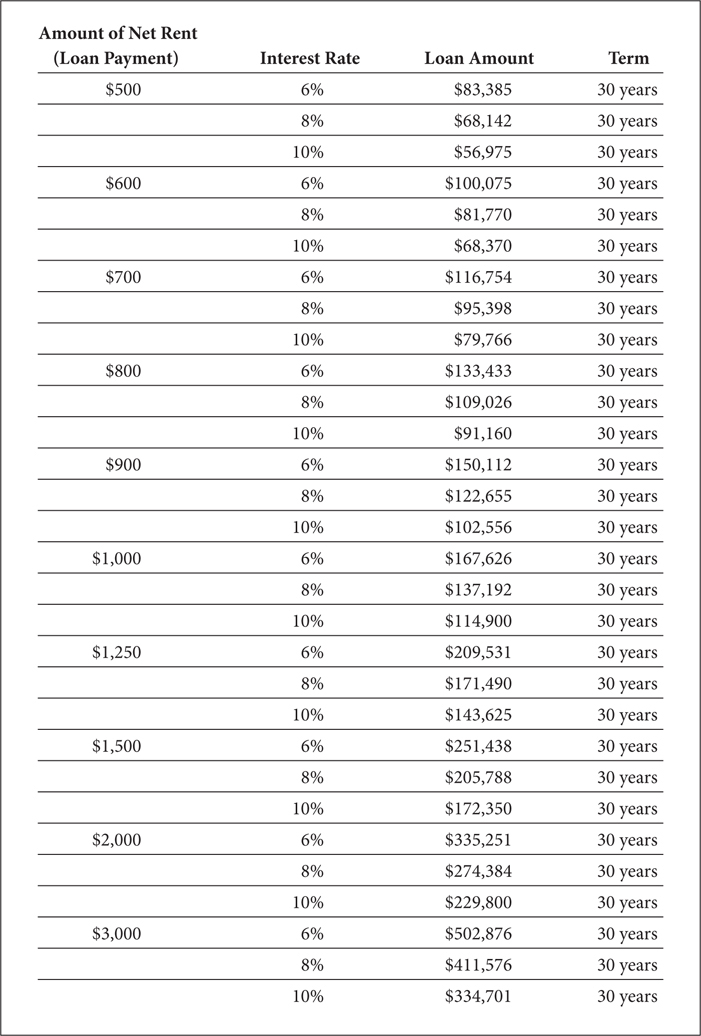

Table 6.2 shows you the amount that you can afford to repay with the rent you collect at different interest rates. Use this chart as a guide when you are calculating how much you can afford to repay with the net rents that a property would generate.

Table 6.2 How Much Can you Repay with Different Rents?

Then calculate the exact payment any loan would have using a financial calculator. You can buy one at any large office supply store or download an app onto your phone.

Study Table 6.2 so that you become familiar with how much you can borrow to buy houses that produce certain amounts of net rent (rent after expenses). Identify the range of rents in your town, and remember these numbers. Now you can make an offer knowing that the rents will cover your payments if you borrow on terms with these payments.

ALWAYS BORROW FOR THE LONGEST AVAILABLE TERM

Using the word always will cause you to struggle with this idea, and this is good. Can we agree that a loan with a lower payment is a safer loan for you to owe? If you had to lower your rents to keep your house full, the longer-term loan would give you the lowest possible payment.

When you borrow to buy property, the longer-term loan allows you to borrow more money. You can buy a property with less of your cash invested. Although thirty-year loans are common, as rates rise, longer-term loans may be available.

When you are beginning to invest, you need to use your available cash sparingly. Buying with a low down payment is a better strategy than using much of your cash for a down payment. If your house sits empty for two months before you rent it, you will need cash for payments.

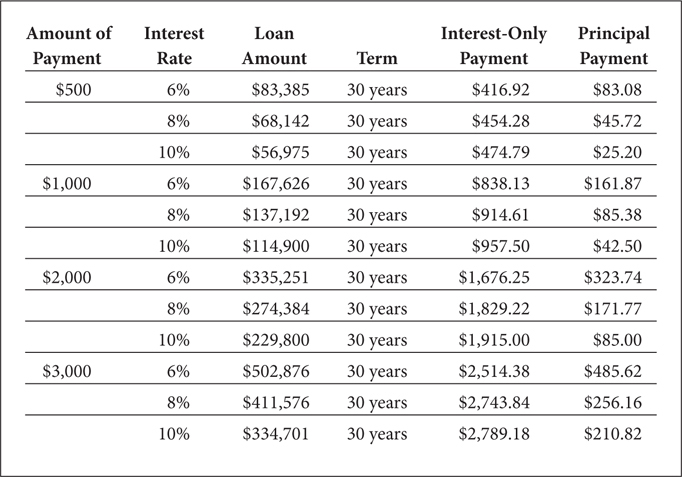

Even with a thirty-year amortization schedule, you are paying a considerable amount of principal each month. Compare the thirty-year amortizing loan with an interest-only payment (see Table 6.3).

Table 6.3 Even Thirty-Year Loans Have Large Principal Payments

You can pay off a loan before its due date. However, when you are still in the property-acquisition mode and can use your cash to buy a house that will make you a 20 percent or higher annual return, why would you want to use that cash to pay off a loan that is only costing you 6, 8, or even 10 percent?

After you have acquired all the properties that you want, you can shift gears and begin to pay off your debt. Owning free-and-clear real estate is a good strategy.

When you begin, focus on buying properties with long-term financing. After you own many properties with long-term loans, you can then use your cash flow to begin reducing your debt. How long does it take to pay off a thirty-year loan? About ten minutes. You just write a check for the balance. Just because you borrow on thirty-year terms does not mean that you have to wait thirty years to own your houses free and clear. Later you will learn how to pay off your debt and get your houses free and clear in far less than thirty years.

SCHAUB’S 10/10/10 RULE FOR BUYING AT A PROFIT

My 10/10/10 rule for buying a house states that when you buy, you make no more than a 10 percent down payment, pay no more than 10 percent interest, and buy at least 10 percent under the market. This rule of thumb will help you to put together offers to buy houses that will pay for themselves.

1. Pay no more than 10 percent down. A smaller down payment is better for you in several ways.

First, you have more liquidity. In the event that you have to resell the house quickly, it will be easier to find a buyer who can put 10 percent down than one with a larger down payment.

Second, you have less risk because you have less to lose. The lender has more to lose when you borrow using the property as the collateral for your loan.

Third, you can buy more houses if you use your cash sparingly.

When you make a smaller down payment, your rate of return on your investment increases. Suppose that you put $30,000 down and buy a house that produces $2,000 a year in cash flow plus $4,000 a year in appreciation and principal paydown. Your profit, expressed as a ratio of the annual profit the property produces divided by the amount of money you have invested, is $6,000/$30,000, or 20 percent. This is your rate of return on your investment.

If you bought the same house with $10,000 down, your cash flow would drop as your loan payment increased. Suppose that you had zero cash flow and the same $4,000 in appreciation and principal paydown. In this case, your rate of return would be $4,000/$10,000, or 40 percent. By doubling the return on your investment, you cut in half the time it will take you to reach your financial goals.

2. Pay no more than 10 percent interest on the money you borrow to finance. House interest rates vary with time—even when rates are low, some investors are paying more than 10 percent to finance property. Whatever the interest rate a bank is charging, you can borrow at a lower rate from sellers and other investors.

Since interest is the largest component of your payment, the rate of interest that you pay determines in large part how much profit you will make on the house. Work hard to get the best possible interest rate when you borrow.

3. Buy at least 10 percent below the market. Buying at a below-market price makes you a profit the day you buy. In addition, it reduces the amount of money that you have to borrow to buy the house, which increases your cash flow.

It also makes the deal safer and more liquid. If you needed to sell in a hurry, you could sell to someone else at a below-market price and get your down payment back and hopefully a little profit.

Thus, 10/10/10 is the worst deal you should make. You should make every attempt to buy a house with a lower down payment, borrow at a lower interest rate, or buy it for less than 10 percent below the market.

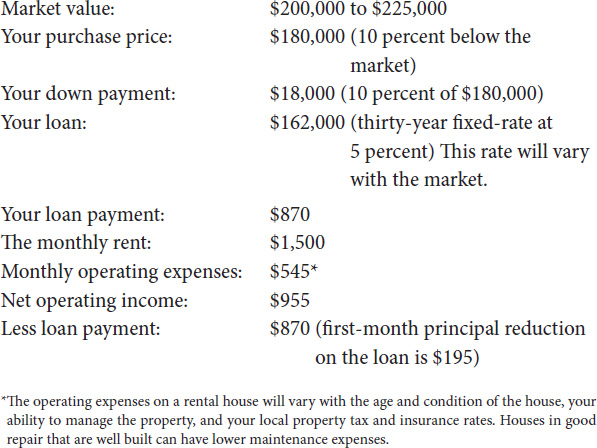

If you bought a $200,000 rental house in my town today using 10/10/10, your purchase would look like this:

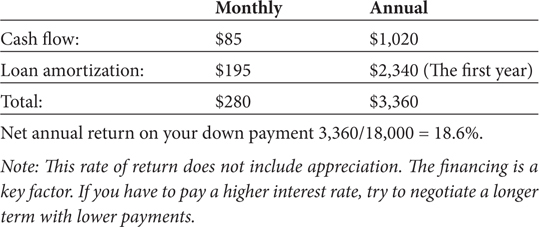

Calculating the net return on your down payment:

Never use potential appreciation to talk yourself into buying a property. Buy one that gives you an acceptable return on your investment without appreciation, and then the appreciation will make a good deal even better.

YOUR FIRST $18,000 GROWS TO $194,000 IN A DECADE

If you hold this house until the house doubles in value ($400,000) and it takes ten years, the loan balance would be $139,016. If you sell the house for $400,000, you would net before taxes about $260,000. If you can invest $18,000 for ten years and receive $260,000 at the end of that time, you have earned an annual compounded rate of return of just over 30 percent. If it takes fifteen years, your rate of return is 19.4 percent. If it takes twenty years your rate of return is 14.2 percent. This does not include the cash flow that the property produces that we discussed above, nor does it account for tax benefits or costs.

This rate of return is as high as it is because of two factors: First, the prudent use of leverage that allowed you to buy an asset worth $200,000 with an $18,000 cash investment that then would pay for itself. Second, the continuous investment of your money in a profitable asset for a long period of time. This combination of “positive leverage” and a long-term strategy allows investors to accumulate millions of dollars in net worth in a fraction of their lifetime.

FORMING YOUR BUYING STRATEGY

Before you make an offer, take the time to really know the neighborhood. Walk, don’t drive, up and down the street and the streets around the house. Meet the neighbors. Notice what’s going on in the neighborhood. Are there a lot of houses for sale or for rent? Are all the houses well maintained? Do you notice any empty houses?

Look for other opportunities. Sometimes you will find a better deal by walking and talking to others who live in the neighborhood. Ask the neighbors if they know of anyone who is selling. You will be surprised at how much the neighbors know and how much they will tell you.

Research both recent sales and properties now on the market to get a good feel for prices. Rather than trying to establish an exact price for a house you are looking at, give yourself a range of prices, for example, $200,000 to $240,000. Now you know that if you can buy at the low end of that range or below, it’s a good deal.

SET A MINIMUM ACCEPTABLE PROFIT FOR THE HOUSE

There is some risk every time you buy a house. You will invest a considerable amount of time when you buy, rent, and sell a house. Although you are not guaranteed a profit, you should buy at a price that gives you a high probability of making a profit.

The more expensive the house you invest in, the larger your minimum profit should be. You take a smaller risk buying a less expensive house. It is easier to rent and easier to resell. You take a greater risk when you buy a more expensive house. You need to buy it further below the market to compensate yourself for that risk. If you had to resell it immediately, you would have to discount the price to get rid of it quickly.

The difference between your minimum profit and my advice to buy a house at least 10 percent below the market is the result of combining a discounted price with favorable financing that allows the house to produce a profit from rents. A more expensive house will have less of its profit from rental income and more from a bargain purchase.

Following are some examples of house prices and minimum profits. This is not a science. These numbers should make you consider the relationship between the risks you are taking and the price you should pay for a house. You need to adjust the discount to account for the quality and location of the house and the market for houses at the time. You may decide that there is little risk in buying a higher-quality house in a strong market, especially if you can buy it with favorable financing.