14

BUYING AND SELLING HOUSES TO PRODUCE CASH FLOW—TODAY

Buying and selling a house for a quick profit is exciting work and can produce short-term cash flow. It is different from investing in a house; it takes more time and has more risk.

Buying and selling requires certain skills and takes a serious commitment of time. Many people who attempt this strategy are unsuccessful, because they underestimate the amount of skill and time it takes to buy and sell for a profit.

Buying and holding a house for a long-term profit requires less skill, because time is on your side. You can buy a house at a retail price, and if you hold it long enough, you will make a profit. The longer you hold a property in a good location, the more money you will make.

As an investor, you will acquire the skills you need as you research your area, talk to hundreds (yes, hundreds) of sellers, and negotiate and close deals.

When you have the needed skills, you can buy some houses for investment and others to increase your cash flow today. If you are trying to transition from working for someone else to being a full-time real estate investor, buying and selling a couple of houses a year can give you the cash you will need for down payments and living expenses.

If you are already a full-time investor, you are constantly looking for good deals. Sometimes you will find houses that you do not want to buy and rent. Rather than just passing on such a property, buy and sell it for a profit.

To qualify as a good long-term investment, a house should be well designed, well built, be in a neighborhood that will attract long-term tenants, and appreciate at an above-average rate. Most who buy to resell are less particular about which house and in which neighborhood they buy.

TIME IS YOUR FRIEND AS AN INVESTOR, BUT NOT WHEN YOU ARE BUYING AND SELLING

When you are buying and selling houses for short-term profit, time works against you. It may take you several months to find and buy a good deal. After you close on the deal, every day you own it the holding costs (interest, taxes, insurance, advertising, repairs) reduce your profit. To make a profit, you need to sell before your profits are eaten up by your holding costs.

Your annual profit from buying and selling houses depends on several factors:

1. How far below the market you buy each house

2. How many houses you are able to buy a year

3. How long it takes you to sell and close

4. How much you can sell for

Some investors buy multiple houses and wholesale them quickly to other investors, but make only a little on each house. Others buy just a few houses and sell at a retail price to make a larger profit per house.

ANNUAL PROFIT = PROFIT PER HOUSE × NUMBER OF HOUSES BOUGHT AND SOLD

The key to making a profit is buying a house at a below-market price and then reselling as quickly as possible. You cannot sell a house in a short time at an above-market price. The higher the price, the longer it will take to sell.

If you can find a house that you can buy 15 to 20 percent below the market in two months, close the purchase and fix it up in two months, and sell and close it in two more months (an optimistic time table), you are on track to buy and sell two houses a year. If your goal is to make $60,000 a year, you need to net $30,000 profit per house.

This can be a good business if you are a skilled buyer and able to invest time and energy to the work and able to buy below the market consistently. Many who buy to resell are not accomplished negotiators and buyers. They buy marginal deals and try to make a profit by selling at above-market prices.

You want to be good at buying and selling for more reasons than just making money. The more houses you buy and sell in a year, the more you have to work and the more risks you take. You want to be skillful enough and professional enough in your work to make your efforts worthwhile and insulate you from litigation.

Many legal issues arise and a good number of lawsuits result from buy/sell transactions that go awry. The other party (it could be either the buyer or the seller) feels as if she has been taken advantage of, or a flaw in the property surfaces after the closing. Sometimes these issues can only be resolved with a lawsuit, but a lawsuit can eat up years of profits.

FIVE STEPS TO MAKING MONEY BUYING AND SELLING HOUSES

1. Identify the price range of houses in your town that sells the fastest. You want to buy houses to resell in this price range. A Realtor can give you this information. Typically, it is a house you would call a starter house or one step above that house. It is often just below the median-priced house in a town. Often there is a large inventory of these houses, and although there is competition to buy, these houses are easier to sell.

A cardinal rule of real estate is that it is easier to buy than to sell. When you are the buyer, you are in control. You can choose how much to offer and decide whether to buy or pass. When you are selling, you can lower your price and offer terms to attract buyers, but you cannot make them buy. You can lead a buyer to a good deal, but you can’t make them buy.

2. Identify several neighborhoods that have houses for sale in the price range you want to buy and sell. Look for signs of opportunity, like the opportunities listed in Chapter 4. An empty house, any house that is not well maintained, or a house with a bad tenant all signal opportunity.

Walk the streets in the neighborhoods that interest you and look carefully at each house on the street. You will notice houses that you would not see driving the street. Talk to the neighbors. Knock on doors and ask if they know of any houses in the neighborhood for sale. This is the most effective way to find a good deal. Good deals are rarely listed.

Most houses that are opportunities are not even for sale. There will be no sign in the yard and no ad in the paper. Many people in trouble simply hope that their problem will solve itself and take no action to solve it. This is why walking through a neighborhood and knocking on doors is such an effective way to find a good deal.

3. Once you find a good deal, research it. Find out what the owner paid and what others have paid for similar houses on the street recently.

4. Now set a minimum profit goal. A more expensive house that may be harder to resell should command a larger profit. Likewise, a house that needs considerable work and will consume a lot of your time and money needs to produce a larger profit.

For a beginning buyer, a profit goal of 10 percent of the purchase price is a good minimum target. That is net profit, after repairs and holding costs

5. Start keeping a journal. Every time you buy a house, write down in your journal the following points:

• Why you thought that this house would be a good deal

• How you came up with your first offer

• How the buyer responded to the offer

• What the offer was that was accepted

• What you would offer if you could start over

Before you make your next offer, review the last offer that you had accepted and try to make this next offer a little better for you. As you become more skilled, increase your profit-per-house goal. Experienced buyers command 20 percent or greater profits.

If you are willing to work for less than a 10 percent profit, get a real estate license and collect a commission. You don’t have to take the risk, make a down payment, or pay the carrying costs that being in the buy/sell business requires. In the process of getting a license, you will learn the laws that regulate agents in your state. Hopefully, you will learn about contracts, deeds, closing statements, title insurance, and other facets of the real estate business.

If you intend to receive a 10 percent return on your money (and consider a return on your time as well), then you need to work on your skills and devote the time required to buy and sell houses for profit. The 10 and 20 percent figures are just profit targets. Anyone who actually has bought and sold a property will tell you that you don’t always make as much as you plan to make. Sometimes you get lucky and make more, but it often takes longer to sell or costs more to make repairs than you planned, and your profit is less than your target.

A REALTOR WHO WORKED FOR LESS THAN A COMMISSION

A Realtor bought a house from me that needed updating. I had owned it for about ten years and had rented it to the same tenant for that entire time. The house had more than doubled in value, and the Realtor made me an offer I did not refuse.

She fixed it up and sold it several months later for about a $5,000 gross profit (not counting her holding costs or taxes). She would have made more money listing and selling it without spending the time and investing the money to fix it up and market it.

You can make more than $5,000 per house when you buy and sell, but there are no guarantees. Other investors have sold houses to me for less than they paid after trying unsuccessfully to sell for a profit.

A long-term investor can wait patiently for a strong market, keeping a house rented until the time is right to sell, and harvest a large profit. A short-term “flipper” does not have that luxury.

After you buy a house at a bargain price, you have to sell it for more than you paid for it, plus your holding costs, plus any money you have to invest to improve the house. Short-term profits you make from buying and selling are subject to the higher tax rates applied to ordinary income, not the capital gains rate available on investment property gains.

Taxes will become a greater concern once you begin to make a lot of money. Learn to make money first, and then learn how to reduce your taxes. If you are broke, you don’t need a good tax strategy or asset-protection plan. You need assets and income.

Once your taxable income from buying and selling exceeds $30,000 a year, talk with a certified public accountant (CPA) who owns real estate himself about options that can reduce your tax liability. Using a corporation or limited-liability company (LLC) to buy and sell properties can reduce your tax bill and give you some liability protection. There are both advantages and disadvantages to using an entity to buy and sell, so get good advice before you spend the money to form one.

WHICH HOUSES TO BUY AND WHICH HOUSES NOT TO BUY

There are some houses you should not buy at any price. There are houses that are beyond repair at a reasonable cost (unless you are buying at below the lot value) and houses in neighborhoods where there are no owner occupants and no trend toward more owner occupants. When a neighborhood is entirely owned by landlords, your only buyers will be other landlords. You might be able to sell to them at a profit, but they will be tough negotiators, and often these pros will want you to finance the property.

The ideal house to buy is one in a neighborhood with many owner occupants who maintain their property, a neighborhood where buyers will want to live and will pay a retail price when they buy. A house that needs only carpet, paint, and minor repairs is safer to buy than one that needs a total rehab. The more work a house needs, the more money you will have to invest and the longer it will take you to make a profit. The more money you have invested, the more pressure you have to resell quickly. That often leads you to accept a lower offer than you planned.

SELLING HOUSES THAT NEED WORK IN “AS IS” CONDITION

CASE STUDY: THE HOUSE OF THE RISING WATER

I bought a house from a bank that had neglected to maintain it. The bank had allowed a roof to leak for months during the rainy season, and the water in the house was getting deeper by the week. The ceilings had fallen in, the kitchen cabinets had fallen off the walls, and all the drywall was soaked.

This house needed work!

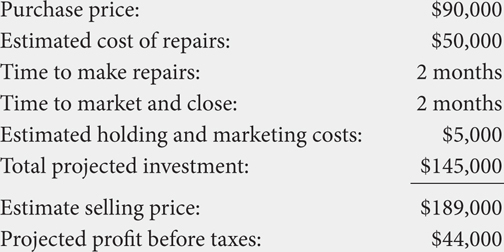

I put together the following projection of the cost to buy and repair the house and then to sell it:

Once I had a contract to buy the house from the bank, I put a for sale sign in the yard. I had several calls, because many buyers are looking for bargains that need work. There was one family who wanted to buy the house but did not have enough money or credit to buy it; however, they did have the ability and resources to do the work needed. Never sell a house that needs work to a buyer unless the buyer can convince you that he can do the work needed.

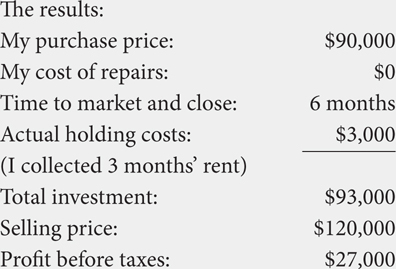

I agreed to sell them the house on a one-year lease/option contract in “as is” condition with a $1,000 down payment at a price of $120,000. I gave the buyers three months’ reduced rent ($100 a month) and had them agree in the written contract specifically what work they would do during that three months.

Their plan was to get the house in livable condition in the first three months. Working with friends from their church, they were able to clean out the house, repair it, move in, and get it financed at a bank with an appraisal of $189,000 within six months. They borrowed enough money to pay me in full and recover most of their expenses.

Although I made less money, I significantly reduced my risk and time invested. If the buyers had not closed on their contract, I would have owned a much better house than I turned over to them.

When you have a house that needs this much work, typically you go over budget on both time and money. When you can take an acceptable profit and let someone else take the responsibility for the work, you free up your time to look for the next good deal. You also eliminate or at least reduce your risk.

Selling a house with a small down payment has risks. If the house needs a lot of work and your buyers do some or all of that work, the work they contribute is the equivalent of a bigger down payment. If a house needs no work, require a larger cash down payment. If the sale falls through, you need enough cash to make any needed repairs to the house and remarket it.