5. Innovation from the Bottom-Up

The dual financial and climate crises have finally awakened the sleeping giant. New York Times columnist Tom Friedman argues that the best way for America to “get its groove back” is to take the lead in solving the world’s big problems—to issue what he calls a “Code Green:” “In a world that is getting hot, flat, and crowded, the task of creating the tools, systems, energy sources, and ethics that will allow the planet to grow in cleaner, more sustainable ways is going to be the biggest challenge of our lifetime.”1 Activist Van Jones, Founder of Green for All, agrees: America’s challenge is to build the “green collar economy” where ordinary people benefit from the rapid deployment of energy efficiency and green technology: “That’s why the government needs to immediately launch a massive initiative like the Manhattan Project...or the Apollo Mission...to solve the riddles of clean energy and perfect these technologies.”2

And the good news is that after decades of denial, inaction, or, at best, incremental policy prescriptions, the alarm bell has now sounded in government. The Obama administration in the U.S. has now made green technology (and the creation of “green collar” jobs) a national priority, along with scores of other countries around the world, including China, Brazil, and India. Indeed, we are now flooded with proposals for massive government programs, corporate restructurings, stimulus packages, and moon-shot-style initiatives for green technology development. During times of crisis, the temptation is great to believe that a few smart people can design the Big Solution. The metaphor of “war” is often invoked—the war on terrorism, drugs, poverty, global warming, etc. Yet, with the exception of actual wartime military mobilizations, seldom have massive, centrally-directed initiatives succeeded.3

So if incremental governmental policies are insufficient, and large-scale, crash programs are likely to fail, then what can be done? Fortunately, there is a third way—a strategy for incubating thousands of small-scale, yet radical business experiments aimed at leapfrogging today’s unsustainable practices, each with the opportunity to grow and become one of tomorrow’s sustainable corporations. In order for the vision of a sustainable future to flourish, it will take an engaged private sector and entrepreneurship on an unprecedented scale. It is a strategy that taps into the entrepreneurial spirit in all of us—change agents in global corporations and NGOs, social entrepreneurs, the poor in underserved communities, investors, and public servants; a strategy that can unite the world—East and West, North and South, Rich and Poor—in a common cause, fostering peace and shared prosperity. But perhaps most importantly, it is a strategy that starts small and grows from the bottom up, starting from the base of the pyramid.

On the Horns of a Dilemma

Just as countries are struggling to find their way in this new world, so too are corporations searching for new strategies. Indeed, the majority of large companies seem to be mired in saturated markets that have few significant growth opportunities. Before the financial crisis plunged the world into a global economic slow-down, corporate leaders were content with the centralized globalization and “emerging market” strategies that had served them well throughout much of previous two decades. During this time, rich countries and rising middle classes in the developing world accounted for the majority of the market opportunity. Now, however, with the rich world likely to be mired in a prolonged period of slow growth, companies must turn their attention elsewhere—to the low-end segments that they previously ignored.

However, as we have seen, the rapid rise of global capitalism over the past two decades has been accompanied by mounting concerns over environmental degradation, labor exploitation, cultural hegemony, and loss of local autonomy, particularly in the Third World. The rising tide of antiglobalization, along with civil strife and growing insurrection throughout the developing world, make it apparent that corporate expansion at the expense of the poor and the environment will encounter vigorous resistance. This raises the question: Must corporations’ quest for future growth serve only to fan the flames of the antiglobalization movement?

Fortunately, there is a way out of this global “Catch-22”: The best way to both generate growth and satisfy social and environmental stakeholders is to focus on emerging markets. By this, I do not refer to incremental market expansion targeted at the wealthy few or rising middle classes in the developing world. Instead, I argue that the best path will be through a Great Leap Downward—to the base of the economic pyramid, where more than four billion people have been bypassed or damaged by globalization.4 It is here that companies will find the most exciting growth markets of the future—and the basis for a formidable future vision. It is here that the disruptive technologies needed to address the social and environmental challenges associated with economic growth can best be incubated and developed. And it is here where the solutions to the rich world’s environmental and economic problems will first be incubated.

Birth of BoP

I still vividly recall the conversation that started it all. It was the fall of 1997, and I had recently published an article in the Harvard Business Review (HBR) that examined the opportunity for the corporate sector to profitably pursue strategies for a more sustainable world. Global poverty, rising inequity, and environmental degradation in the Third World led the list of problems to be solved. The article, “Beyond Greening: Strategies for a Sustainable World,” went on to win the McKinsey Award as the best article in HBR that year. My strategy colleague at Michigan, the late C.K. Prahalad, had just completed a draft manuscript with Ken Lieberthal that would ultimately appear in HBR in 1998 as “The End of Corporate Imperialism.”5 He shared a copy of the paper and asked for comments and suggestions.

I remember being absolutely struck by the complementary nature of our thinking. In the paper, Prahalad and Lieberthal make a compelling argument for both the challenge and opportunity of serving the emerging markets in China and India, especially the tier below the wealthiest consumers in these countries that most multinationals had been preoccupied with up to that point. In our ensuing discussion about the paper, I remember making the comment that serving the next tier down from the top was indeed important, but this still left unexamined (and unserved) the vast majority of humanity in the lowest tiers of the global economic pyramid. Neither government (including the multilaterals) nor the nonprofit sector had been particularly successful in addressing this mounting problem over the past half-century. Aid and philanthropy were clearly insufficient to solve the problem.

At that moment, it became apparent to both of us that what was missing (and critically needed) was a logic for why (and how) the corporate sector might focus attention on understanding and serving the four billion poorest people at the bottom (or base) of the economic pyramid (BoP, for short). We developed a working paper in 1998 that went through literally dozens of revisions over the next four years before it was published in January 2002 as “The Fortune at the Bottom of the Pyramid.”6 (C.K. later published a book by the same title.) The concept of the BoP was born.

Significant momentum has now been established around this agenda, with literally dozens of colleagues from around the world now working actively in this arena.7 In 2000, the Base of the Pyramid (BoP) Learning Laboratory was founded at UNC’s Kenan-Flagler Business School.8 The BoP Learning Lab is a consortium of corporations, NGOs, and academics interested in learning how to serve the needs of the poor in a way that is culturally appropriate, environmentally sustainable, and profitable.9 A global network of BoP Learning Labs has since been spawned with partners in Mexico, Brazil, Argentina, Spain, the Netherlands, Denmark, India, China, and South Africa.10

In 2004, the BoP Learning Laboratory moved to Cornell University as part of the new center for Sustainable Global Enterprise at the Johnson School. Since the advent of the BoP Learning Lab, the World Resources Institute, the World Business Council for Sustainable Development, International Finance Corporation, the United Nations Development Program, U.S. AID, and the Inter-American Development Bank, among others, have launched major programs focused on the role of the private sector in alleviating poverty and catalyzing sustainable development. Over the past decade, it has thus become apparent that the BoP offers both enormous opportunities and challenges for companies accustomed to serving the wealthy at the top of the economic pyramid.

The Tip of the Iceberg

As just noted, for much of the past half-century, corporations have chosen to focus their attention exclusively at the top of the world economic pyramid, especially the very top where 75 million to 100 million highly affluent “Tier 1” consumers reside.11 This is a cosmopolitan group, to be sure, composed of upper-income people in developed countries, especially the U.S., Western Europe, and Japan, and the few rich elites from the developing world.

With the fall of communism in the late 1980s, however, multinational corporations rushed into so-called “emerging markets”—Russia and its former allies, along with China, India, and Latin America—with the expectation that they would be the next great business bonanza. Unfortunately, by the early twenty-first century, corporate momentum in emerging markets had slowed considerably. The prospect for hundreds of millions of new middle-class consumers in the developing world had been oversold. The Asian and Latin American financial crises in the late 1990s put a damper on the rate of foreign direct investment (FDI). The events of September 11, 2001, further slowed the advance. And the recent global financial crisis all but flattened what Tom Friedman refers to as the emerging “flat world” of the global middle class.12

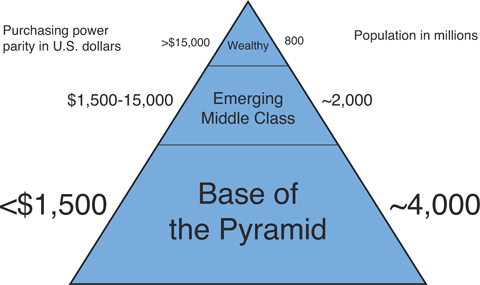

With the benefit of hindsight, we can now see more clearly why most multinationals’ global and emerging market strategies have not realized their full potential: They were neither very global nor particularly oriented toward emerging markets. In the developing world, most FDI has targeted only the few “large market” countries, such as China, India, and Brazil. And even there, most MNC emerging market strategies have focused exclusively on the 800 million or so wealthy customers or perhaps the rising middle classes, ignoring the vast majority of people considered too poor to do business with (see Exhibit 5.1).

Exhibit 5.1 The Global Pyramid

Source: Adapted from Prahalad, C.K. and Hart, S. 2002. “The fortune at the bottom of the pyramid.” Strategy+Business, 26: 54-67, with assistance from Ted London.

Many reasons have been offered to justify and explain corporate preoccupation with the top of the economic pyramid in emerging economies. Some, for example, have suggested that such customers are more similar to American, European, and Japanese consumers, which MNCs are accustomed to serving, and thus present less “psychic distance” than do the impoverished inhabitants of shantytowns and rural villages. Others point to the lack of important institutions in the developing world (such as rule of law and intellectual property), which makes conventional MNC operations all but impossible.13

Not surprisingly, then, most MNC strategies have aimed to tailor existing products to fit the needs of the top of the pyramid in the developing world. The incremental product changes and modest cost reductions associated with this strategy, however, have not succeeded in reaching the vast majority of people. The net result is that the four billion plus people at the base of the economic pyramid—fully two-thirds of humanity—have been largely ignored by corporations. They have been bypassed by globalization, their needs are being poorly met by local vendors, and they are increasingly the victims of corruption and active exploitation by predatory suppliers and intermediaries.14 Much like the proverbial iceberg with only its tip in plain view, this huge segment of the global population—along with its massive potential market—has remained largely invisible to the corporate sector.

GE’s Ecomagination initiative (described in detail in Chapter 4, “Clean Technology and Creative Destruction”) provides a case in point. Without detracting from Ecomagination’s bold intent and clear, rigorous process, it is also important to point out its limitations. Indeed, virtually all of the Ecomagination products serve the needs of current, wealthy (or emerging middle class) customers at the top of the economic pyramid. Comparatively little attention has been given to the world’s 4 billion poor at the base of the economic pyramid who lack reliable, affordable solutions related to energy, transportation, water, materials, and financial services.

Where GE’s new technologies might apply to solving the problems of the world’s poor (e.g., desalination technology, wind energy, advanced membrane technology), they have typically been large-scale, capital-intensive applications premised on existing business models. In fact, most Ecomagination products and technologies continue to focus on centralized solutions. This should not come as a great surprise given the company’s large-scale, industrial past, but it does represent a potential blind spot in the Ecomagination strategy. For example, the wind energy business seems to be organized exclusively around “big wind”—the massive utility-scale wind turbines that lend themselves to connection to the existing grid system.

Only recently has the company begun to entertain the commercialization of small-scale, distributed technologies such as distributed solar, point-of-use water treatment, and portable, small-scale health devices—what I refer to as “Green Sprout” technologies. In fact, in a 2009 Harvard Business Review article, GE CEO Jeff Immelt, along with co-authors Vijay Govindarajan and Chris Trimble state emphatically that the future of the company depends on becoming adept at what they call “reverse innovation”: the ability to incubate low-cost innovations in the developing world and then migrate them up-market to the developed world.15 As we will see later in this chapter, this idea is entirely consistent with the one that my colleague Clay Christensen and I have been arguing for nearly a decade. However, the fact that a global corporation like GE now recognizes publicly that this is the only way to avoid being pre-empted by the emerging innovators from the developing world is indeed an important tipping point.

With stagnation in the established markets of the world economy and rising antiglobalization sentiments, opportunities for serving the base of the pyramid are becoming increasingly attractive, given that the BoP space is largely decoupled from the vicissitudes of the “global economy.” In fact, concealed below the surface of the purchasing power parity numbers is an immense and fast-growing economic system that includes a thriving community of small enterprises, barter exchanges, sustainable livelihoods activities, and subsistence farming.16 Indeed, it is estimated that well over half of the total economic activity in the developing world takes place outside the formal economy, in the so-called informal or extralegal sector.17

The base of the pyramid is also rich in assets, although most are unregistered and, therefore, remain invisible. In his book The Mystery of Capital, Hernando de Soto estimates that there are well over $9 trillion in unregistered assets (houses, equipment, and so on) in the rural villages and urban slums of the world.18 Because the poor typically do not hold legal title to these assets, they remain trapped and underleveraged, protected only by the informal property systems enforced by local strongmen.

Unlike the “underground” economy at the top of the pyramid, which is driven by the desire to avoid paying income taxes (just ask your waiter or carpenter), the informal sector at the base of the pyramid exists because of the difficulty and expense of becoming legally registered due to corruption and archaic rules. It has been estimated, for example, that it takes thousands of dollars, several hundred steps, and more than a year of effort to officially register a business in most developing countries today.19 Small wonder, then, why the extralegal sector is thriving while the formal economies in many developing countries today show little or even negative growth. The challenge is to connect the informal and formal economies in a productive and mutually beneficial partnership.

In short, the emerging market opportunity may be much larger than previously thought. However, the new untapped source of promise is not the wealthy few in the developing world or even the rising middle-class consumers—it is the billions of aspiring poor who are seeking to join the market economy for the first time. Effectively reaching the base of the pyramid, however, calls for disruptive innovation on a massive scale and the creation of entirely new, more sustainable industries in the process.20 And unlike Mao Zedung’s Great Leap Forward in China, which ended up taking the country backward during the Cultural Revolution, the Great Leap Downward to the BoP may ultimately incubate more sustainable ways of living for people at the top of the pyramid.

Creative Creation

As Clay Christensen so eloquently explains in his path-breaking book, The Innovator’s Dilemma, disruptive innovations involve products and services that initially aren’t as good as those that historically have been used by customers in mainstream markets and that, therefore, can take root only in new or less-demanding applications among nontraditional customers.21 Examples include transistor radios, small cars, personal computers, solar energy, and online investing; in each case, the initial offering was seen as different—even strange—from the standpoint of the mainstream market. Recall that transistor radios were initially adopted by teenagers, small cars by the cost-conscious, personal computers by artists and academics, solar energy by “greens,” and online investing by the Internet-savvy.

Well-managed companies are pressured to invest in innovations that target markets large enough to sustain corporate growth rates and enhance overall profit margins. To them, pursuing disruptive innovations seems irrational. This allows disruptive innovators to incubate their businesses in the safety of markets that resource-rich competitors are motivated to ignore and then to grow up-market by attacking a sequence of market tiers that are the least attractive investment options facing the leaders.

Disruptive innovations typically enable a larger population of less-skilled or less-wealthy people to begin doing for themselves things that historically could be done only through skilled intermediaries or by the wealthy. Disruptions have thus been a fundamental mechanism for creating new growth businesses and improving our standard of living. Joseph Schumpeter’s notion of creative destruction tells only half the story: In reality, before a disruptive innovation destroys industry leaders and incumbent technologies, a long and fruitful period of “creative creation” typically occurs. Indeed, the social good is well served through disruption, which has, over the decades, created millions of jobs, generated hundreds of billions of dollars in revenues and market capitalization, and raised standards of living by making available cheap, high-quality products and services. We have gained more through creative creation than we have lost through creative destruction.

For example, until the late 1970s, only employees of large companies and universities had access to computers—and that access could be had only by giving punched cards to the expert in the mainframe center who ran the job. Minicomputer makers such as Digital Equipment listened diligently to their customers, and their customers told them that the nascent technology of personal computing was a waste of time. It was a quirky new gadget only for artists, kids, and hippies, not something intended for the sophisticated technologists in large corporations and universities that controlled access to computing. Not surprisingly, the early market for PCs, led by upstarts such as Apple, was to be found among artists, academics, and other members of the counterculture.

But as PC technology evolved and developed, its performance improved, even on dimensions that were important to the mainstream market. Gradually, PCs began eating into the lower end of the minicomputer market. When companies such as IBM and Compaq entered the business, they were able to make computing accessible to a much larger population of average—and, ultimately, lower-income—non–computer scientists and nonprogrammers. Now that the masses could use computers without the level of training of experts, the technological progress and industry growth that followed enabled average people to do many more things than had been possible on mainframes run by experts.

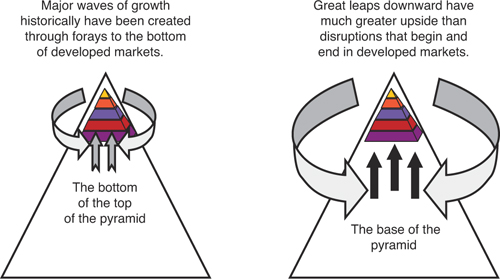

Because computers and a host of other industries (such as automobiles, consumer electronics, and financial services) were disrupted, extraordinary waves of growth occurred. In each instance, we enjoyed higher quality, lower cost, and greater convenience. Those who are better off today include many more people than those few who could afford it before the disruptions. Disruptive innovators have generated hundreds of billions of dollars in revenue and market capitalization and created tens of millions of jobs in the process. And yet firms have achieved all this, as the left side of Exhibit 5.2 suggests, by dipping only slightly down from the peak of the population pyramid—by going from the wealthiest and highest skilled of those living in developed countries into the tiers of lower skills and income in those same developed countries.

Exhibit 5.2 The Upside of Disruptive Growth: The Great Leap Downward

Source: Adapted from Hart, S. and Christensen, C. 2002. “The great leap: Driving innovation from the base of the pyramid.” Sloan Management Review, 44(1): 51-56.

The disruptive technologies that were developed to reach just down to these tiers cannot be easily deployed toward even lower-income consumers—it is very difficult to remove cost from a business model aimed at higher-income customers without affecting its quality or integrity. But new waves of disruptive technology deployed by companies making a Great Leap to the BoP can have extraordinary potential to generate growth because they have even more upside once they have taken root. Indeed, the low-cost structure needed to serve the base of the pyramid presents the opportunity to later add cost and features to products and move up-market to tiers of higher income and affluence. In short, the farther down the income pyramid the technology begins, the more upside growth potential exists over the life of the innovation.

Driving Innovation from the Base of the Pyramid

As Clay Christensen and I have argued, the base of the pyramid is the ideal market for new disruptive technologies for at least two reasons.22 The first is that business models forged in low-income markets can travel profitably to more places than can business models defined in high-income markets. Honda’s success with motorcycles provides an example. In the 1950s, Honda began selling motorized bicycles to small distributors in the crowded and impoverished Japanese cities that were rebuilding from the ruin of World War II. The company developed a business model that could make money selling at very low price points. When Honda entered the United States market in the early 1960s with its disruptive Supercub, the product’s simplicity and low price point enabled a much larger population—people who lacked the money or boldness to own Harleys—to buy and use motorcycles. Honda’s base in impoverished Japan gave it a huge competitive advantage in disrupting the American motorcycle makers because it could make money at prices that were unattractive to the established leaders.

Toyota and Sony followed the same recipe and enjoyed decades of success while taking on the market leaders in developed countries. In fact, the industries that constituted the engine of Japan’s economic miracle from the 1960s to the 1980s all followed the disruptive strategy of attacking markets that established competitors wanted to avoid because their likely revenue and profits seemed unattractive. Disruption was the nation’s strategy for economic development. The reason Japan’s economy suffered from no growth for most of the 1990s was that its institutions did not permit new waves of disruptive innovation to be launched against its multinational giants, the very companies that were yesterday’s disrupters.23

In addition to having more adaptable business models, disruptive innovators compete against nonconsumption—that is, they offer a product or service to people who otherwise would be left out entirely or would remain poorly served by existing products. This is the second reason the base of the pyramid offers better markets for new growth businesses. When companies searching for growth fight against capable competitors to win the business of savvy customers in established markets, the barriers to success are formidable. But when they bring a disruptive product to customers who have been poorly served or even actively exploited, the customers are delighted to have simple products with modest functionality.

Consider a Chinese company called Galanz, which has achieved extraordinary growth through a Great Leap Downward.24 In 1992, Galanz decided to enter the market for microwave ovens, even though the firm was a textile and garment manufacturer at the time. The global market for microwaves was mature and shrinking, and it was hard to differentiate products because most of them were good enough to do what people wanted them to do. Manufacturing had migrated to countries where labor costs were low and consumption was concentrated in developed countries. In China, only 2 percent of all households owned a microwave oven. Most families did not have kitchens large enough to accommodate the available models, which had been designed to fit into homes in the West.

Rather than pursue the obvious strategy of using inexpensive Chinese labor to make lower-cost ovens for export, Galanz’s founder Qingde Liang chose to compete against nonconsumption in the domestic market. Galanz developed and introduced a simple, energy-efficient product at a price that was affordable to China’s vast middle and lower-middle classes and small enough to fit in their kitchens. As sales steadily climbed, Liang stimulated demand by using the company’s ever-declining cost per unit to reduce the product’s price. Galanz’s domestic market share rose from 2 percent in 1993 to 76 percent of a much larger market by 2000. Armed with a business model that could earn attractive profits at low price points, Galanz moved up-market to manufacture larger machines that had more features. It began to disrupt the microwave oven markets in developed countries by marketing its machines on a private-label basis to large MNC producers of home appliances. By 2002, it had become the largest producer of microwave ovens in the world, with a global market share of 35 percent.

Connecting the World

Galanz’s success demonstrates the possibility for disruptive change to affect people in the middle of the pyramid. But the feasibility of disruptive business models has also been demonstrated in numerous experiments at the very bottom, where more than four billion people earn less than $1,500 in purchasing power parity annually. Perhaps the best-known such experiment occurred in the Grameen family of enterprises in Bangladesh, described in Chapter 3, “The Sustainable Value Portfolio.” The original Grameen Bank, one of the originators of microcredit in the developing world more than 30 years ago, has since spawned several other ventures, including Grameen Telecom, launched in the late 1990s, which focused on bringing information and communication technology to rural Bangladesh in the form of “village phones.”

Iqbal Quadir originally conceived of the idea of rural connectivity in 1993, after his New York firm’s computer network went down. It reminded him of his childhood days in rural Bangladesh when he used to waste entire days walking long distances because there was virtually no phone service outside of the city.25 More than half of humanity (three billion people) is still without reliable telecommunications service. Telephone service in rural areas has been slowed by the size of the capital investment required to extend the wireline infrastructure profitably from urban areas. Grameen Telecom’s mission has therefore been to bring telecommunications service to the rural poor in Bangladesh (average per capita income of $286 per year). At this income level, the existing business model for telephone service would not be feasible—only disruption could do the job.

Accordingly, at the initiation of Professor Yunus, two independent companies were formed in 1997, one for profit (GrameenPhone), and another not for profit (Grameen Telecom). GrameenPhone is a consortium made up of four partners: Telenor of Norway (51 percent), Grameen Telecom (35 percent), Marubeni of Japan (9.5 percent), and Gonophone Development Company (4.5 percent). GrameenPhone was the recipient of the telecommunications license. It focused on serving all urban areas in Bangladesh by building a nationwide cellular network. Grameen Telecom buys bulk airtime from GrameenPhone and retails it through Grameen borrowers in the rural villages. Initially, few gave the venture much hope because only the richest city-dwellers in Bangladesh could afford their own mobile phones. But by changing its business model, Grameen Telecom was able to pilot-test and launch a venture that has proved to be highly profitable. Grameen Bank loaned the money to women in rural villages to establish them as independent entrepreneurs to sell mobile phone services. They received loans of up to $175 to purchase a mobile phone and a small solar recharger unit. The loan also included the necessary training needed to use and service the equipment. The pilot project started in 1997 with 950 villages, but in Bangladesh alone, there was a potential market for tens of thousands of “village phones.”

The results of the pilot test were impressive.26 Village phone operators increased their income on average by about $300 per year, raising their status in their villages considerably. Most of these women spent their additional income on education and health care for their children, providing an additional development bonus. For users of the phone service, there was considerable consumer surplus. Rather than making the time-consuming and expensive trip to secure information about crop prices or to place orders with distributors through a slow, unreliable postal system, users could now simply place a call. Each call saved the average user $2.70 to $10—a whopping 2.5 to 10 percent of household monthly income. Significant reduction in travel, combined with the avoidance of a wireline infrastructure, provided significant environmental advantages as well.

The business model also proved to be very profitable for the company. The rural phones in the pilot project booked three times the revenue per phone as their urban counterparts ($100 per month in revenue for a village phone versus about $30 per month in the city). If extended to all of rural Bangladesh, it was estimated that the business could generate revenues in excess of $100 million per year. If a similar model were applied to rural India and China, tens of billions of dollars of revenue would be possible.

In fact, the performance of GrameenPhone has exceeded even the wildest dreams of those involved with the pilot project.27 By 2006, net profits had grown to nearly $200 million. Demand for rural phone services was so strong that additional phone ladies were necessary in many villages. By the end of 2008, there were nearly 354,000 phone ladies spread across more than 70,000 villages. If you do the math, this means that GrameenPhone was now approaching one billion dollars in revenue in Bangladesh alone. This is all the more impressive when it is realized that until 2004, the government denied access to the wireline infrastructure, meaning that all calls had to be made from one Grameen phone to another. Phone ladies were earning, on average, about $750 per year in 2006. While it may not sound like much in places like the United States or Western Europe, this level of income moved the phone ladies’ families squarely into the middle class. Leveraging the success of the model, the Village Phone program was introduced in a handful of other countries by 2008, including Uganda and Rwanda.

By 2006, the company had invested $1 billion overall in Bangladesh (compare this figure to the $268 million in total foreign investment in Bangladesh in 2003). A study that year concluded that the mobile phone industry in Bangladesh created a total value add of $812 million, of which $256 million was retained by the operators and used to pay employee wages and taxes. The remaining $650 million, about 1 percent of GDP, went to dealers, suppliers, operators, and support services. In all, the report estimated that the mobile phone industry contributed, directly or indirectly, to more than 250,000 income opportunities (not including the work of the phone ladies themselves).28 By 2008, the company had a subscriber base of 18 million and provided network coverage to nearly 98 percent of Bangladesh’s population. Its employment base had also grown to a total of 5,000, with another 150,000 people directly dependent on GrameenPhone for their livelihood.29

Most recently, the incomes of phone ladies have begun to decrease as their numbers (as well as those of competitors) have swelled in what were previously the underserved villages of Bangladesh. Rural phone service has now become a competitive business! Accordingly, GrameenPhone began expanding its service to include rural Internet access, through the use of Internet kiosks. N-Logue, an emerging telecom player in India, adopted a similar business model but has developed new technology to dramatically lower connection costs in rural areas using wireless local loop (WLL) technology that separates voice and data traffic. The revenue and profit potential for this business is enormous.30 Indeed, over the past few years, several new players have entered this space, including ITC’s e-Choupal, and Drishtee.

Whereas fixed and mobile wireless technology is not performance- or cost-competitive with wireline access to the Internet in developed nations, it is vastly superior to the alternative in much of the developing world: nonconsumption. Telecommunications giants in developed countries have spent billions on 3G and 4G technology and spectrum licenses, hoping to provide enough bandwidth for current customers to do wirelessly the things for which they now use the wireline Internet. These investments have crippled many of these companies, and they are unlikely ever to produce adequate returns. Far better is to compete against nonconsumption at the base of the pyramid—and migrate from that profitable base toward successively more sophisticated customers and applications in global markets.

The case of Grameen Telecom illustrates how disruptive business model innovation can incubate sophisticated technologies at the base of the pyramid in ways that offer tremendous growth potential for businesses and positive social and environmental benefits for the rural poor. Innovating from the bottom up holds the potential to generate enormous growth and to address the root causes of antiglobalization sentiments, facilitating sustainable development.

Food, Health, and Hope?

A Great Leap Downward might also serve to reverse the present course of the agricultural biotechnology and genetically modified (GM) plant and animal industries, which continue to struggle for economic viability and social acceptance. Most early efforts to bring this technology to market were aimed at rapid penetration of the mainstream market. For example, despite its mantra of “Food, Health, and Hope,” Monsanto focused virtually its entire strategy during the 1990s on designing genetically engineered seeds to lower costs for farmers growing commodity crops (such as corn, soybean, and cotton) in the developed world, especially the United States.

Reducing chemical and input usage through genes that made the plants pest-resistant (such as Bt Cotton) or resistant to the application of herbicides (such as Roundup Ready) made such seeds hard for farmers in the United States to resist because they were under intense margin pressure from food processors and manufacturers. The large-scale and centralized nature of the American agribusiness system meant that producers rapidly purchased GM seeds and planted crops. Indeed, the acreage dedicated to GM crops in the United States increased from virtually zero in 1995 to more than 60 million acres by the end of the 1990s.31

However, as we have seen, attempts to expand beyond the United States met with growing opposition. In Europe, environmentalists and consumers began to resist the importing and planting of such seeds. A backlash movement was set in motion and focused on several issues. First, consumers perceived no benefit from eating GM crops. Indeed, only farmers benefited from the first generation of seeds, and consumers were asked to take whatever risk there might be (such as allergic reaction), with no compensating health or nutrition benefit. Second, environmentalists grew more concerned that unforeseen ecological problems could be unleashed by the rapid rate of GM adoption by farmers, including the possibility of crossing with wild plants and the production of “super weeds.” Third, critics from the developing world grew increasingly concerned that a few MNCs might come to control the world’s seed supply, denying poor, small-shareholder farmers around the world the ability to save seed and engage in other age-old agricultural practices. Food manufacturers and retailers began to boycott GM crops, in some cases paying a premium for conventionally grown foods. By the late 1990s, the backlash had become so severe that Monsanto and other agricultural biotechnology producers were forced to scale back their business operations and reconsider the future of GM food.

The recent bioagricultural experience provides important lessons in technological innovation and commercialization. Disruptive innovation theory would predict that the attempt to pit GM foods against the established options in complex mainstream markets so soon would be fraught with difficulty. Reducing farmers’ cost is not enough to guarantee acceptance of a radically new technology when customers already are well satisfied with the quality, quantity, and affordability of present food alternatives. Indeed, the greatest need for additional nutrition and agricultural productivity resides not with American agribusiness, but rather, at the base of the pyramid, where billions of small-shareholder farmers labor to produce crops, frequently for their own consumption, at very low levels of efficiency and productivity.

Properly designed and introduced, GM seeds might dramatically improve the lives of small farmers by lowering costs, enhancing pest resistance and productivity, conserving water and soil, and increasing nutritional value of foods made from such crops as rice, sweet potatoes, and cassava. Through microcredit and other forms of collaboration with small farmers, it might be possible to design a business model that results in a whole new approach to sustainable agriculture. Incubating such experiments from the ground up rather than introducing the technology on a massive scale from the top down also might encourage a more reasoned understanding of any significant environmental issues. Eventually, these approaches to agriculture might become so productive and successful that they could move up-market to out-compete the chemical- and energy-intensive agribusiness model prevalent in the United States. When we are building major new growth markets with new technology, the shortest distance between two points often is not a straight line. This is true even for the most sophisticated new clean technologies, such as solar energy, LED lighting, and biofuels. The base of the pyramid can be the best place to start, as we explore next.

Power to the People

Consider the case for distributed generation of power. The electric power infrastructure in the developed world is based upon large, centralized power facilities (fueled by coal, oil, gas, or nuclear technology) and an extensive grid system for the transmission and distribution of power. Incremental innovation has improved the efficiency of these power plants over the years, but significant inefficiencies still exist in generation and distribution. For example, nearly half the power generated is lost in distribution over an aging power grid. And despite calls for moving to a next-generation “smart grid,” extending power lines to distant rural areas is capital intensive (costing, on average, $10,000–$20,000 per mile), and the pricing required to recoup those massive investments limits consumption. As a consequence, there are still more than two billion people in the world with no access to dependable electric power. These people instead burn dangerous and polluting fuels such as kerosene, diesel, candles, and dung.

At the same time, there is growing investment in the distributed generation of power (DG), including such technologies as solar photovoltaics, wind, fuel cells, and microturbines. In fact, venture capital investment in DG is now in the billions each year, up from only about $100 million in 1996. These technologies generate small quantities of electricity (less than 1mW) near the actual point of use, thereby avoiding the need for expensive distribution. DG technologies also lend themselves to the use of renewable fuels (such as the sun or wind, as well as biomass—crop and animal waste—in the case of fuel cells and microturbines). Biofuels made from non-food plants such as perennial grasses, jatropha, or jute, can also be produced for distributed use.

Engineers and marketers are struggling against a stringent standard, working to bring down the cost of these technologies to make them competitive with conventional sources of power in the developed world, where the existence of a sunk-cost grid system and subsidies for fossil fuels wipe away any cost advantage associated with distributed generation. In these markets, cost-accounting systems and rate structures tailored to the centralized generation of power using fossil fuels make it difficult for such technologies to gain a foothold in the mainstream markets because they have yet to achieve cost parity in the eyes of the consumer. Photovoltaic electricity, for example, still costs about $0.50 per kilowatt hour, compared to 7¢–15¢ per kilowatt hour for grid-connected electricity. Customers in the developed world are also understandably leery about taking on the additional risks and responsibilities of solar panels or fuel cells while the after-sale service infrastructure remains in its infancy.

But DG faces few of these obstacles among the rural poor in the developing world. It may be decades before the electrical grid system is extended to provide service to those who currently lack access to dependable electric power. As a consequence, the rural poor spend a significant portion of their income—as much as $10 per month—on candles, kerosene, and batteries to have access to lighting at night and periodic electrical service.32 Furthermore, generating electricity using kerosene and batteries is expensive, costing $3–$5 or more per kilowatt hour. If offered a viable substitute, these people might abandon these dangerous, polluting, and expensive technologies in favor of clean, efficient, and renewable electric power. Yet few producers of DG have focused on the rural poor at the base of the pyramid as their early market for these technologies, despite the fact that the market is potentially huge and is populated by people who would be delighted with technologies that cannot compete along the metrics used in developed markets.

The crucial breakthrough for sustainable energy technologies, therefore, will not be in a laboratory. Instead, sustainable energy must be incubated and refined where the technology can be profitably deployed through disruptive strategies, in markets where it does not compete against established technologies. This means producers must tailor the technology for use in poor rural areas and develop production, sales, service, and microfinancing packages that enable nonconsumers to gain access.

Consider the innovative technology and business model created by the nonprofit Light Up the World (LUTW).33 Dedicated to bringing a safe source of light at night to the billions of people without electric power around the world, LUTW teamed with Stanford University to develop an affordable rural (off-grid) lighting system that combines solar photovoltaics with light-emitting diode (LED) technology.

LED is an emerging lighting technology that is extremely energy-efficient (80–90 percent more efficient than incandescent light bulbs), long-lived (lasts 8–10 years), and durable (virtually unbreakable). Despite these advantages, however, to date, LEDs have been limited to niche applications in the developed world such as traffic signals, brake lights, and electronic displays, where vibrant color and durability are important. In recent years, however, white LED technology has been developed that holds the potential to replace light bulbs in the mainstream lighting market. Yet even though all the large lighting companies (including GE, Philips, and Osram-Sylvania) have growing LED businesses, there have been few commercial inroads into this vast market, despite the potential for massive energy and financial savings. We can explain this in part by the large installed base of light fixtures (which will not accommodate LEDs). It is also a result of the propensity for top-of-the-pyramid consumers to benchmark any substitute lighting technology against conventional incandescent bulbs, which cost less than a dollar but last only a matter of months (LEDs cost 10 times as much but last for nearly a decade). Indeed, the slow rate of compact fluorescent bulb adoption has already demonstrated the difficulty of changing consumer preferences to a substitute with a higher first cost but a lower life-cycle cost.

Of course, none of these problems exists if we focus instead on the billions of rural poor without access to electricity. There is no installed base of light bulb fixtures, nor are there any preconceived notions about how an electric lighting system should operate. And by combining the highly energy-efficient LED lighting arrays with solar power, we can dramatically reduce total system cost, downsizing the solar panel needed to power the system. Indeed, LUTW and Stanford have been able to design a system that includes the LED lighting arrays, the solar panel, the battery, wiring, and controls in a “rural lighting system” package that can be sold for as little as $50 retail.

For a poor family making less than $500 per year, this would be equivalent to the purchase of a car by a top of the pyramid family. Because the family is already spending as much as $5–10 each month on candles, kerosene, lanterns, and batteries, all that is required is a microfinancing package, along with a reliable local microentrepreneur to sell and service the equipment. This is precisely the approach that LUTW and Stanford have taken in launching a commercial venture to serve this market. Indeed, over the past few years, literally dozens of DG start-up companies have begun to spring up across the developing world, including players like SELCO, Cosmos Ignite, Duron Energy, D.Light, Barefoot Solar, Shanghai Roy Solar Company, and Tata BP Solar, to name a few.

A distributed business model like this could tap into a potential market of more than two billion people. With the volume and experience from the sale and service of solar and LED at the base of the pyramid, it would be only a matter of time before this technology became so efficient—and affordable—that it began to eat its way into the low-end markets in urban areas, perhaps starting with shantytowns, where grid-based electric power is expensive and unreliable. For example, the Solar Electric Light Company (SELCO), a for-profit enterprise that serves the middle-of-the-pyramid market with full-scale solar home electric lighting systems that sell for as much as $500 each, has a growing business in India and Southeast Asia. Ultimately, such systems could become so attractive and affordable that even the wealthy at the top of the pyramid would find them difficult to resist.

Given the enormous growth potential of this business model, it comes as no surprise that electronics giant Philips launched such a commercial venture in rural India during 2005. Philips (along with British Petroleum) is also pilot testing a smokeless stove for use in rural areas that dramatically reduces fuelwood requirements (and hence deforestation). Use of the stove also saves rural women significant amounts of time otherwise spent hunting for and collecting firewood. As with DG, there are now dozens of smokeless stove start-up companies, each with its own particular twist on technology and business model.

Sustainable energy pioneers who focus on the base of the pyramid could set the stage for one of the biggest business bonanzas in the history of commerce because extensive adoption and experience there would almost certainly lead to dramatic improvements in cost and quality. If firms such as Philips create a business model that can be profitable in these markets, solar energy has a chance. But this is the only strategy by which this technology can succeed without massive and ongoing government subsidy. Could we now be witnessing the start of the real clean-tech revolution, driven by bottom-up innovation on a massive scale? Or will change on the necessary scale still require us to jettison some mental baggage when it comes to driving clean-tech innovation from the base of the pyramid?

The Great Convergence

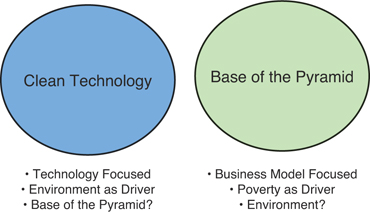

I would argue that the examples of bottom-up innovation offered here represent more the exception rather than the rule to date. More commonly, clean-tech entrepreneurs and BoP business innovators operate in isolation from one another. Each has evolved with its own particular dominant logic and core assumptions. In some respects, each represents a separate “world” with its own set of beliefs, priorities, and culture (see Exhibit 5.3).

Exhibit 5.3 Two Different Worlds

At the risk of over-simplification, Clean Technologists typically see the road to success as paved by new, “sustainable” technologies that dramatically reduce or eliminate the human footprint on the planet. The focus is on technology development and early penetration of high-end “green” markets at the top of the pyramid, with the promise of eventual “trickle down.” BoP advocates, in contrast, focus on new business models for reaching and serving the poor. Confronting poverty and finding new avenues for growth are the primary foci, and there is often little attention paid to the environmental implications of such strategies.34

The crucial next step is, therefore, to consciously merge these two mindsets in a Great Convergence. This convergence of thinking recognizes that clean technologies (especially the distributed “Green Sprout” variety) are almost always “disruptive” in character—they threaten incumbents in current served markets at the top of the pyramid. As a result, the base of the pyramid is often the best place to focus initial commercialization attention. At the same time, the Great Convergence also recognizes that successful BoP strategies must be environmentally sustainable to avoid taking all of humanity over the proverbial environmental cliff.

Unlike the traditional model of industrialization, which relies heavily on conventional (unsustainable) technology, the Great Convergence seeks instead to fuel growth through the incubation and rapid commercialization of distributed green technologies from the bottom-up. The challenge is to combine the advanced technology of the Rich World with the entrepreneurial bent and community focus of the BoP. Learning how to build upon, and not over, ancient foundations and local knowledge is key. Through such a strategy, the villages and slums of the developing world could become the breeding ground for the Clean-Tech Revolution. However, declining industrial cities in the developed world also offer the opportunity to “start again” with thousands of acres of vacant and abandoned land in places like Detroit, Michigan, and a population hungry for new opportunities.

Unfortunately, most effort to date has been focused on driving clean technologies into the “developed” markets at the top of the income pyramid, often with little result. Given the perverse incentives and incumbent inertia that exists, this should come as little surprise—just witness what happened at Copenhagen with the climate change negotiations. As Van Jones, Tom Friedman, and others have pointed out, as long as “green” remains synonymous with “rich,” it will never change the world. Because the BoP provides the best early opportunity for innovators seeking to stake out the future in the full range of emerging clean technologies, governments would be wise to construct policies that encourage their technologists and entrepreneurs to immerse themselves in this space: Just as companies that ignore this enormous opportunity do so at their peril, so too do countries and states that place all of their focus on eco-efficiency or rebuilding centralized infrastructures in existing settlements—they risk missing what comes next.

A New Development Paradigm

The theory of disruptive innovation suggests that existing mainstream markets are the wrong place to look for major new waves of growth. Indeed, forcing a potentially disruptive innovation into a conventional business model, thereby moving it into head-on competition with incumbents, may only ensure its early demise. Instead, we argue that the vast, underserved market at the “base of the pyramid” is an ideal place for the incubation of new, sustainable technologies through a bottom-up form of innovation.

Our thinking about the potential rewards resulting from a great leap to the base of the pyramid extends this strategy as a framework not just for corporate growth, but also for more balanced and sustainable macroeconomic development in poor countries. Such an approach is potentially significant because existing strategies for economic development now appear to be all but bankrupt.35 Import substitution, for example, which emphasized the development of domestic capacity to serve established home markets, was discredited more than 20 years ago; its protectionist stance failed to produce competitive or efficient national producers.36

More recently, the export-led growth strategies advocated by the so-called Washington Consensus have come under increasing fire as well.37 By asserting that developing countries can generate growth by producing commodities and goods for export to the top of the pyramid, the doctrine of export-led growth has resulted in excess capacity and global deflation. Indeed, after a decade of international financial crises, mounting Third World debt, environmental devastation, and rising inequity, the Washington Consensus is crumbling. It now appears clear that the only way to spur sustainable growth for the long term is to design a development strategy that focuses on the unmet needs in the developing world itself, the base of the pyramid. Indeed, bottom-up innovation holds the prospect of lifting the poor out of poverty, averting environmental meltdown, and opening the way to sustainable growth for the global economy.

Consider the case of Mexico. Since signing on to the North American Free Trade Agreement (NAFTA) more than a decade ago, the country has been caught in a no-win situation. By opening its borders to foreign investment, Mexico became a haven for Maquiladora plants near the U.S. border and new export-oriented MNC assembly facilities in search of low labor costs or lax environmental enforcement. There can be no doubt that these foreign direct investments created factory wage jobs in the short term. Unfortunately, few of these investments provide any long-term development payoff for Mexico.

There are two reasons for this conundrum. First, as even lower-cost locations (such as China) became more attractive, many of the plants and assembly facilities closed their doors and moved overseas, leaving Mexico’s workers high and dry. Like unemployed factory workers in the U.S., they are victims of the global “race to the bottom” for the lowest wages and operating costs. Second, the export-oriented investments in Mexico have provided few of the skills or capabilities needed to compete more effectively in the game of global capitalism. Indeed, few Mexican companies are now better able to compete against the highly sophisticated U.S., European, and Japanese multinationals for the top of the pyramid markets as a result of these investments. In short, low factor costs alone do not translate into knowledge or skills that have value in the highly competitive marketplace of today’s global capitalism.

The combination of NAFTA and the draconian structural adjustment policies imposed on Mexico by the International Monetary Fund have served only to hasten the country’s slide into rising inequity, social rebellion, and financial meltdown—witness the recent spike in drug-related violence that threatens the country’s stability. It should come as no surprise, then, that some enlightened business leaders and government officials in Mexico have become increasingly interested in the base of the pyramid as a potential way out of this trap: By using the power of commerce as a vehicle for serving the needs of the country’s massive underclass, Mexico can incubate entirely new enterprises with the unique capabilities needed to become the globally competitive companies of the future.38 Just like China, India, and Bangladesh, Mexico could become a wellspring for the truly disruptive—and sustainable—enterprises of the twenty-first century.

Taking the Great Leap

If history is any guide, most of the growth opportunities in the vast, underserved space at the base of the pyramid will be seized by entrepreneurs (such as Grameen, Tata, and Galanz) in developing countries, just as the opportunities in impoverished postwar Japan were captured by innovators such as Sony, Matsushita, Honda, and Toyota. In addition, countries such as China, India, Brazil, and Mexico may well make the Great Leap to the BoP their primary strategy for national economic development. Indeed, we may be witnessing the birth of the next generation of multinational corporations, nurtured in the base of the pyramid through bottom-up innovation and ready to take on the high-cost structures and rigid management models of the existing MNC incumbents.

Today’s global corporations, however, should not assume that such an outcome is inevitable; they, too, can seize these growth opportunities before they become threats. As is always the case in pursuing disruptive innovation, however, such companies will need to manage these new opportunities independently from their mainstream incumbent businesses. Even more importantly, they will have to build new business models that include strategies, organizational structures, and management processes actually suited to conditions at the base of the pyramid. Reaching the base of the pyramid requires radical business model innovation. However, actually raising the BoP through enterprise requires that managers and entrepreneurs think about the full range of social and environmental benefits (and costs) resulting from their strategies. It is to this objective that we turn our attention in the next chapter.

Notes

1. Tom Friedman, Hot, Flat, and Crowded (New York: Farrar, Straus, and Giroux, 2008), 5–6.

2. Van Jones, The Green Collar Economy (New York: HarperOne, 2008), 6.

3. This section is adapted from Stuart Hart, “Taking the Green Leap,” Cornell University, Working Paper, 2009.

4. Parts of this chapter are excerpted from Stuart Hart and Clayton Christensen, “The Great Leap: Driving Innovation from the Base of the Pyramid,” Sloan Management Review 44(1) (2002): 51–56.

5. C.K. Prahalad and Ken Lieberthal, “The End of Corporate Imperialism,” Harvard Business Review July–August (1998), www.hbsp.harvard.edu/hbr/index.html.

6. C.K. Prahalad and Stuart Hart, “The Fortune at the Bottom of the Pyramid,” Strategy+Business January (2002): 54–67.

7. Including C.K. Prahalad, Michael Gordon, Bob Kennedy, and Ted London (University of Michigan), Clayton Christensen (Harvard Business School), Miguel Angel Rodríguez and Joan Enric Ricart (IESE Business School), Sanjay Sharma (Concordia University), Allen Hammond (Ashoka), Nicholas Guttierez (Tec Monterrey), Jim Johnson and Lisa Jones (University of North Carolina), Miguel Angel Gardetti (IEEC-Argentina), Oana Branzei (Western Ontario University), Stef Coetzee (Stellenbosch University), Jac Geurts and Erik van Dam (Tilburg University), Reuben Abraham and V. Chandrasekar (Indian School of Business), and Professors Yunhuan Tong and Xudong Gao (Tsinghua University).

8. At the suggestion of my UNC colleague, Ted London, we changed the name from “bottom” to “base” of the pyramid to remove any hint that those on the lower end of the income scale are in any way inferior to those at the high end of the income scale.

9. The BoP Learning Lab’s contributing members have included DuPont, HP, J&J, P&G, Nike, IBM, SC Johnson, Ford, Dow, Coke, and Tetrapak. Nonprofit organizations such as the Grameen Foundation, ApproTEC, Tata Energy and Resources Institute, and the World Resources Institute are also actively involved.

10. See www.bopnetwork.org.

11. Portions of this section are excerpted from Prahalad and Hart, “The Fortune at the Bottom of the Pyramid.”

12. Tom Friedman, The World Is Flat (New York: Farrar, Straus, and Giroux, 2005).

13. For an extended discussion of this issue, see Ted London and Stuart Hart, “Reinventing Strategies for Emerging Markets: Beyond the Transnational Model,” Journal of International Business Studies 35 (2004): 350–370.

14. C.K. Prahalad and Allen Hammond, “Serving the World’s Poor, Profitably,” Harvard Business Review 80(9) (2002): 48–57.

15. Jeffrey Immelt, Vijay Govindarajan, and Chris Trimble, “How GE is Disrupting Itself,” Harvard Business Review October (2009): 3-11.

16. Ted London and Stuart Hart, “Reinventing Strategies.”

17. Hernando de Soto, The Mystery of Capital: Why Capitalism Triumphs in the West and Fails Everywhere Else (New York: Basic Books, 2000).

18. Ibid.

19. Ibid.

20. Parts of the following section are excerpted from Stuart Hart and Clayton Christensen, “The Great Leap.”

21. See Clayton Christensen, The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail (Boston: Harvard Business School Press, 1997).

22. Stuart Hart and Clayton Christensen, “The Great Leap.”

23. Clayton Christensen, Thomas Craig, and Stuart Hart, “The Great Disruption,” Foreign Affairs 80(2) (2001): 80–95.

24. My thanks to Clay Christensen for this example.

25. Iqbal Quadir, presentation at the Wharton Global Compact Conference, University of Pennsylvania, 17 September 2004.

26. For details, see Muhammad Yunus, Banker to the Poor (Dhaka: The University Press Limited, 1998); D. Richardson, R. Ramirez, and M. Haq, Grameen Telecom’s Village Phone Programme in Rural Bangladesh: A Multi-Media Study (Guelph, Ontario: TeleCommons Development Group, 2000).

27. Nicholas Sullivan, You Can Hear Me Now (San Francisco: Jossey-Bass, 2007). Thanks also to Muhammad Yunus and Iqbal Quadir for personal conversations regarding GrameenPhone and Grameen Telecom.

28. Ibid.

29. “GrameenPhone 2007 Annual Report.”

30. J. Howard, C. Simms, and E. Simanis, Sustainable Deployment for Rural Connectivity: the N-Logue Model (Washington, D.C.: World Resources Institute, 2001).

31. Erik Simanis and Stuart Hart, The Monsanto Company (A): Quest for Sustainability, www.globalens.com, 2009.

32. Light Up the World Foundation, LUTW_factsheetdec23.pdf, p. 5.

33. Light Up the World, www.lightuptheworld.org.

34. This section is adapted from Stuart Hart, “Taking the Green Leap.”

35. Thomas Palley, “A New Development Paradigm: Domestic Demand Led Growth,” Foreign Policy Focus September (2002): 1–8.

36. See Jagdish Bhagwati, In Defense of Globalization (New York: Oxford University Press, 2004).

37. See, for example, Joseph Stiglitz, Globalization and Its Discontents (New York: W. W. Norton & Company, 2002).

38. The BoP Learning Lab in Mexico, based at EGADE-Tec Monterrey is actively engaging several Mexican companies, including Cemex, Bimbo, and Amanco, in developing such strategies.