Chapter 6

Cryptocurrency and the People's Money

6.1 Deglobalization in the Digital Time

A key feature of the postwar globalization has been the booming of international finance. Not only have we seen booming payment flows on the back of growing trade financing but also a surge of the capital mobility induced by portfolio investments. Multinational corporations (MNCs) and financial institutions are managing their balance sheets globally. They can profit from carry trades that involve borrowing low-cost currency for high-yield investments, resulting in surging financial activities. Financial institutions are active in settling payment flows associated with their activities in debt and equity capital market, FX, and interest rate hedging as well as securities trading. The global might of cross-border finance distinguishes the contemporary version of globalization from that of the nineteenth century.

The world has been following the doctrine of international capital mobility for a few decades. As the Vatican of the international monetary system, the IMF has been pressing many economies to liberalize their capital and financial accounts. As an accomplice, the WTO has been promoting market access of financial institutions in other countries. US banks with access to US dollar liquidity were riding the tide of globalization. The ability to convert local currency into US dollar became the passport for participating in globalization. The New York Fed provided custodian services for many central banks, which supported the foreign currency needs of exporters and importers in their countries. All countries needed to comply with the US sanction rule. Modern international finance became a US-centric regime.

Deglobalization mirrors a regime shift from economic interdependence to independence. Protectionism is replacing multilateralism. Countries are beginning to question or ignore the central authority of supranational organizations. Rules and standards that were functioning well for a large group of countries in the past no longer appeal to political leaders of individual countries. Bilateral agreements have increasingly become a preferred trade policy option. When country A and country B find a win-win between them, they are willing to cut ties with country C even if a common deal for A-B-C generates a bigger gain in total. In a deglobalizing regime, the policy preference is to go peer-to-peer (P2P).

The concept of P2P transactions is shaping the recent development in the digital economy. Blockchain provides a new path for organizing payment systems on an electronic platform. The concept of distributed ledgers for processing bilateral payment flows contrasts the conventional model of a trusted intermediary. In blockchain, there is no single and central authority in governing the payment system. Participants share the power to book and validate transactions. This development challenges the authority of central banks and financial franchises at a time when society has begun to question the reputation of regulatory authorities and financial institutions in the aftermath of the global financial crisis (GFC).

With blockchain disrupting the architecture of global finance, cryptocurrency challenges the regime of fiat money. Proponents of cryptocurrencies suggest their inventions can replace trusted intermediaries and hence provide a cost saving to the economy (Bitcoin1). They claim that the system can improve financial access of underprivileged populations and small- and medium-sized enterprises (SMEs) (Libra2). Blockchain participants who help validate a block of transactions are rewarded with a new coin. Hence, the value previously enjoyed by licensed providers of financial services is shared amongst the participants. The system creates “money” when Bitcoin miners can prove their work. The idea that anyone can create the money is in stark contrast to our current regime, which relies on central banks to issue paper notes.

With the economy deglobalizing and decentralizing, the world is also looking for a consistent currency option. Prior to the twentieth century, the international monetary regime was not institutionalized. During that time, physical gold was widely accepted in the physical economy. It was apolitical and did not require a government to issue (although it did need an authoritative gold mint for quality assurance). As the global economy becomes more digital than physical, there is a quest for a compatible regime. Admittedly, none of the existing cryptocurrencies in the market have become common means for legitimate and genuine economic transactions. Bitcoin and Ether remain a special interest of speculative investors. Calling cryptocurrency money remains premature.

This chapter serves three purposes. First, it reviews the development of digital currencies. Our discussion will stay conceptual rather than technical. I also describe the recent development of the cryptocurrency market. Secondly, I attempt to assess whether cryptocurrency can be a qualified form of money. It is an important question. If cryptocurrency cannot perform the function of a medium of exchange, it will not be useful to denominate transactions. Lastly, we examine the implication of cryptocurrency on monetary policy. The conclusion in this chapter will help answer the question of whether cryptocurrency will be a global reserve currency, which will be the focus of the next chapter.

6.2 Bitcoin and Distributed Ledgers

6.2.1 The Basics of Blockchain

The past few decades have seen an explosive amount of research and development of financial technology. Fintech is already an acceptable term in the English dictionary.3 Blockchain, Bitcoin, distributed ledgers, and cryptocurrencies are all said to be disruptive and urge the financial industry to rethink their prevailing business model. Traditional models of financial intermediaries, including banking, insurance, wealth management, and securities trading, are being tested. On one hand, governments are assessing the risks and regulatory challenges brought by cryptocurrency; on the other, they see blockchain as an opportunity to transform public service delivery (David et al. 2019). Against the backdrop of the China–US trade war, the two countries are also perceived to compete on their leadership in disruptive technology.4 Their digital rivalry we postulated in the previous chapter is consistent with the overall theme of de-dollarization.

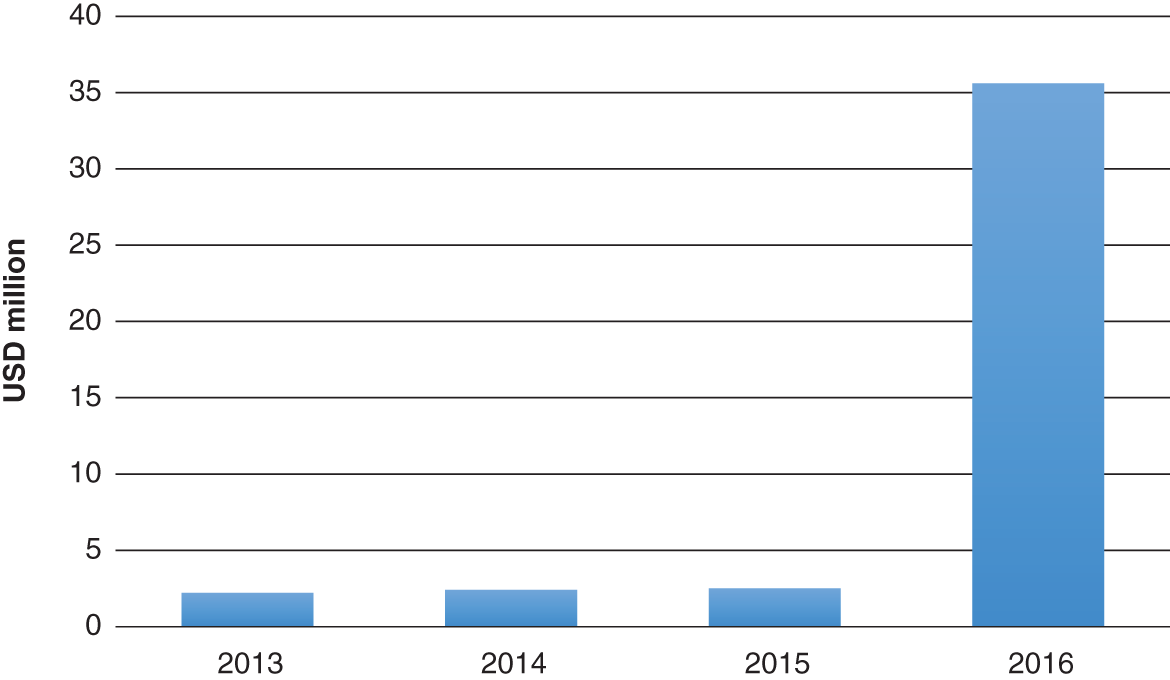

The reality is that it has taken almost a decade for the business community to consider blockchain in formulating their business strategy. In a global survey of 1,386 senior executives with sizeable companies in 2019, Deloitte found that more than half of respondents had considered blockchain a top-five strategic priority, 10 percentage points higher than in 2018 (Figure 6.1).5 In another executive survey by PwC, 84% of respondents said their companies were actively involved with blockchain.6 IDC, an international technology research firm, forecasted that total corporate and government spending on blockchain could reach USD 2.9 billion in 2019, led by investment by financial institutions of USD 1.1 billion. With an annual increase of 89% in 2018, the amount of investment is projected to surge tremendously to USD 12.4 billion by 2022.7

Figure 6.1 Business executive survey on blockchain.

Source: Deloitte

What is blockchain? Since Nakamoto (2008) laid the concept in the seminal Bitcoin paper, there have been tons of explanations of this concept. A good starting point is, in fact, the original objective stated in the whitepaper:

What is needed is an electronic payment system based on cryptographic proof instead of trust, allowing any two willing parties to transact directly with each other without the need for a trusted third party.

The current architecture of the financial system is based on a trusted intermediary. If we want to transfer an amount of money to another entity, we can proceed in one of two ways. The most direct way is to draw real cash physically from our bank (or for some people, their basement), carry the paper notes in a suitcase (or an armored vehicle) and pass the money to the recipient. In this case, the trusted party is the central bank that issued the IOU. The risk is counterfeit money. In Hollywood movies, drug dealers also need to hire experts to validate the cash.

Another way is to instruct a bank to transfer the funds to a recipient bank. The two banks can be the same bank or different banks. But they are the trusted parties in between. We trust them because they are licensed and regulated by the governments. There is also an additional level of trust required for interbank payments, as any bank will assess the counterparty risk of another one, especially for cross-border transactions involving different time zones. A delivery risk called “Herstatt risk” could also result in a systemic collapse in payment chain.8

Blockchain is a conceptual model that can potentially bypass the trusted third party. The World Bank defines blockchain as “a particular type of data structure used in some distributed ledgers which stores and transmits data in packages called blocks that are connected to each other in a digital ‘chain’. Blockchain employs cryptographic and algorithmic methods to record and synchronize data across a network in an immutable manner.”9 Akin but not exactly the same as money supply, a digital coin is created through developing a chain of blocks. The number of transactions per block is a few thousand.10

Blockchain enables the development of distributed ledger technology (DLT), which challenges the conventional model of financial transactions (Figure 6.2). Currently, the financial sector is built on a centralized model. Banks, exchanges, and other financial institutions pool and settle financial transactions of multiple parties. Based on trust (or capacity to absorb loss through a capital buffer), these institutions act as an independent intermediary serving multiple parties. In contrast, a distributed system enables peer-to-peer transactions directly. In the context of blockchain, all individual parties are informed of the history of bilateral transactions of the whole system. A distributed ledger system also requires the individual to take responsibility for validating the transactions. Even though a blockchain distributed system does not require all nodes to verify every transaction, it does require a consensus based on a majority rule to approve the history. In DLT, the duties performed by banks and central banks are decentralized to the members.

Figure 6.2 Network arrangement – Centralized, decentralized, and distributed.

Source: Author, Blockgeeks

In discussing the meaning of distributed ledger, many bloggers differentiate between a decentralized system and a distributed system. The consensus is that as long as there is no single node taking full control, the system is decentralized. DLT is just an extreme case in which all individuals have the same level of authority. Vitalik Buterin, the founder of Ethereum, proposed three dimensions to describe the distribution system: architectural, political, and logical (de)centralization.11 Basically, architectural decentralization is about the arrangement of physical computers in the network. Political decentralization concerns the level of control in the network. Logical decentralization examines the uniformity of interface and data structures. Blockchain is politically decentralized (no one controls them), architecturally decentralized (no infrastructural central point of failure) but logically centralized.

Computers participating in a blockchain network are called the nodes. In the original version of blockchain, all nodes play the role of trusted third party. There is no need to have a bank to act as a custodian, as every miner has equal opportunity to create the money as long as they can provide a proof-of-work. In our current world, the central bank prints paper notes and stamps a serial number. In blockchain, everyone has a chance to create money if all (or a sufficient number of) nodes confirm it is not counterfeit, i.e. double-spending. It is similar to having two pieces of notes with the same serial number. Instead of having a central authority to verify the previous transactions, the approach is to publicly announce the transaction history and allow all nodes to agree on a unique history (Figure 6.3).

Figure 6.3 Transaction process in blockchain.

Source: Author

Nakamoto (2008) outlined the steps of creating a block, i.e. an electronic coin:

- New transactions are broadcast to all nodes.

- Each node collects new transactions into a block.

- Each node works on finding a difficult proof-of-work for its block.

- When a node finds a proof-of-work, it broadcasts the block to all nodes.

- Nodes accept the block only if all transactions in it are valid and not already spent.

- Nodes express their acceptance of the block by working on creating the next block in the chain, using the hash of the accepted block as the previous hash.

Validating the history of transactions is the most critical element in blockchain because this is a step to avoid counterfeit, which could have been done by changing the history of transactions. In Bitcoin, changing the history is difficult because the proof-of-work system is based on the Hashcash system. A hash is an output from the Secure Hash Algorithm-256 system, a unique and complex string of numbers produced from the algorithm. Only this 256-bit alphanumeric string is visible but not the original data. A nonce is added to a verified block. A miner needs to hash a block's header in such a way that is less than or equal to a target number of 4 leading zeros in the string (the last line below):

"Hello, world!0" => 1312af178c253f84028d480a6adc1e25e81caa44c749ec81976192e2ec934c64 = 2^252.253458683"Hello, world!1" => e9afc424b79e4f6ab42d99c81156d3a17228d6e1eef4139be78e948a9332a7d8 = 2^255.868431117"Hello, world!2" => ae37343a357a8297591625e7134cbea22f5928be8ca2a32aa475cf05fd4266b7 = 2^255.444730341..."Hello, world!4248" => 6e110d98b388e77e9c6f042ac6b497cec46660deef75a55ebc7cfdf65cc0b965 = 2^254.782233115"Hello, world!4249" => c004190b822f1669cac8dc37e761cb73652e7832fb814565702245cf26ebb9e6 = 2^255.585082774"Hello, world!4250" => 0000c3af42fc31103f1fdc0151fa747ff87349a4714df7cc52ea464e12dcd4e9 = 2^239.61238653

In this example, the process requires 4,251 attempts. As the blockchain continues to build up, the number of zeros required increases. Since all nodes receive information on the development in the network, they will consider the longest chain to be the correct chain and they will attempt to extend it. Any tie will be broken quickly as the next proof-of-work is found. When one branch becomes longer, the nodes that are working on the other branch will then switch to the longer one. This proof-of-work process requires expensive computational time and power. The miners who spend time on this proof-of-work process are rewarded with coins. Since the coins are created when the zero bits meet the specified target, it is called Bitcoin.

The genesis block of Bitcoin began in January 2009. The nodes continue to build up as the network continues to validate subsequent transactions. This process is still ongoing at the time of the publishing of this book. According to Blockchain.info, the Bitcoin blockchain approached 256GB at the end of 2019, equivalent to 18.1 million of Bitcoin. This figure equals the total size of all block headers and transactions accumulated so far. The design of Nakamoto is to limit the total supply to 21 million coins. The block reward began at 50 coins per block and was then halved every 210,000 blocks. This means that each block up until block 210,000 will reward 50 coins, but block 210,001 will reward just 25. The difficulty of solving the equation also changes every 2,016 blocks, i.e. two weeks/10 minutes. With an average of 10 minutes per block, a block halving occurs every four years.

Bitcoin is not the only blockchain coin. The genesis block of another cryptocurrency called Ethereum began in July 2015, generating a coin called Ether. Compared with Bitcoin, Ether seems to have enhanced some features. One particular breakthrough is smart contracts, which enable a wider range of applications beyond financial transactions.12 The idea was originally developed by Nick Szabo in 1997, proposing that a computer algorithm of cryptographic security function can enforce predefined legal obligations. Szabo's famous analogy is the vending machine: “Anybody with coins can participate in an exchange with the vendor. The lockbox and other security mechanisms protect the stored coins and contents from attackers, sufficiently to allow profitable deployment of vending machines in a wide variety of areas.” Similar to Bitcoin, new Ethers are created via the mining process but Ethereum does not set a maximum total number of Ethers. The reward rate is 5 Ethers per block and remains constant without decaying. Ethereum block times are in seconds, compared to Bitcoin's 10 minutes.

6.2.2 Cryptocurrency Market

Bitcoin gains its novelty as an application of blockchain technique. But blockchain is only one type of DLT. Broadly, DLT shares and synchronizes digital payment records across the network without a central administrator. There have been other types of DLT being developed since Nakamoto's introduction of the Bitcoin's version. Cryptocurrencies can enter circulation in different ways. In the case of Bitcoin, participants of the DLT system validate previous transactions. Whoever finishes the job first is rewarded with a new coin. For other cryptocurrencies, new coins are often sold via an initial coin offering (ICO), a virtual version of an IPO for fund raising. Cryptocurrency exchanges provide the buying and selling of cryptocurrencies in the secondary market. Similar to the “real world,” not all cryptocurrencies are listed for trading.

Since the birth of Bitcoin in 2008, a large number of alternative digital tokens have been created via ICOs. Many versions are essentially a variation or improvement of Bitcoin. For example, Ether retains the blockchain feature of Bitcoin, but the speed of validation is much faster due to a different hashing algorithm. Unlike Bitcoin, which aims to be an alternative electronic payment system, the primary purpose of Ethereum is to facilitate the operation of smart contracts and decentralized application platform called “dapp,” claiming that a programmable feature can facilitate developments of other fintech applications for borrowing, lending, and investing digital assets. In essence, Ethereum is a technology for secured obligations.

Although the first 10 years of cryptocurrency history has not fulfilled the original promise as an electronic payment currency, it has attracted massive speculative investment into this new asset class. Many crypto-assets have a short life cycle. Many different versions are created but do not have a high survival rate. Of almost 5,000 cryptocurrencies included on CoinMarketCap in December 2019, the top 10 accounted for more than 89% of the total market capitalization.14 Dark et al. (2019) cited that only around half of all cryptocurrencies included on CoinMarketCap have existed for more than one year. Bitcoin remained the dominant “currency” in the virtual market (see Table 6.1).

The short lifespan of many cryptocurrencies suggests that the digital currency world may follow in the footsteps of the real world and see a dominant global currency. The USD can maintain its dominance as the global reserve and payment currency despite concerted efforts of the euro and the Japanese yen in the past few decades. The transaction volume of Bitcoin in the secondary market is normally 30% of the total, according to CoinMarketCap. Just as many investors prefer the liquidity of US dollar assets, participants in the cryptocurrency market are also cautious about the uncertainty of new coins. In addition, many other coins are simply a slight variation of Bitcoin. Lack of differentiation means low motivation for investors to support new listings.

Table 6.1 Top 10 cryptocurrencies by market capitalization.

Source: Coinmarketcap.com, December 18, 2019

| Name | Symbol | Circulating unit | Market cap, USD |

| Bitcoin | BTC | 18,106,162 | 119,758,064,814 |

| Ethereum | ETH | 108,948,312 | 13,319,828,635 |

| XRP | XRP | 43,310,265,523 | 7,942,061,755 |

| Tether | USDT | 4,108,044,456 | 4,108,917,575 |

| Bitcoin Cash | BCH | 18,172,500 | 3,210,767,747 |

| Litecoin | LTC | 63,654,657 | 2,356,845,291 |

| EOS | EOS | 944,783,744 | 2,074,196,391 |

| Binance Coin | BNB | 155,536,713 | 1,920,564,553 |

| Bitcoin SV | BSV | 18,068,415 | 1,458,706,058 |

| Tezos | XTZ | 660,373,612 | 1,011,603,126 |

As an emerging asset class, the price of cryptocurrency is volatile, similar to the exchange rate of emerging market currencies in the financial market. At one point, the value of Bitcoin reached USD 20,089 per unit on December 17, 2017, compared with USD 785 the same date in 2016. But the boom did not last long, as the price tumbled to a low of USD 3242 on December 15, 2018 (Figure 6.4).

Price volatility has been a major obstacle for cryptocurrencies to perform the economic functions of conventional sovereign-backed money as (1) a means of payment, (2) a unit of account, and (3) a store of value. As the value is unstable, only speculative investors have an intention to hold a position. Genuine use of cryptocurrencies as a means of payment becomes very difficult.

Figure 6.4 Bitcoin price -monthly average.

Source: CoinMarketCap

To improve price stability, developers proposed a new form of cryptocurrency called stablecoins. There are two ways to do this. The most straightforward way is to anchor the value of digital coins to real-world assets, i.e. asset-backed stablecoins (ABSs). The other way is to regulate the supply and demand of coins through an algorithm.

ABSs attempt to improve price stability through pegging with financial assets in the real world. Just as some real-world currencies that are issued only if there is a corresponding increase in collateral (e.g. Hong Kong Dollar Currency Board System), stablecoins are created if there is an inflow of assets of the same value. The coins can be redeemed at a fixed price by selling these assets. The most popular ABS is Tether, having a code of USDT. It is backed by US dollar and has a stable value of USD 1 for each USDT. Price stability seems to secure the confidence of cryptocurrency investors. The trading volume of Tether is amongst the top of all listings on CoinMarketCap, even though its market cap is only 3% of that of Bitcoin.

ABSs actually derive price stability from sovereign currencies as opposed to DLT design itself. In principle, this method relies on the guarantee from central banks and seems to defeat the original motivation of blockchain. But the rationale is also in line with the story of many emerging market (EM) currencies. Typically, the EM currency crisis ended up with some international assistance through facilities from the IMF. In the aftermath of the Nixon shock, the US dollar became a fiat money without gold convertibility. The greenback also went through a period of turbulence and eventually got stabilized through an implicit anchor to petroleum (see Chapter 2 for detailed discussion about petrodollar recycling).

However, the problem of ABSs is the governance of reserve management. In April 2019, it was reported that Tether was not fully collateralized. Instead, only 74% of USDT were backed by cash and cash equivalents.15 Even though technically a currency did not need to be 100% collateralized, it raised the question about credibility.16 In addition, it was reported that Tether's sister company Bitfinex took a loan of USD 850 million from Tether.17 On November 20, 2018, Bloomberg reported that US federal prosecutors investigated whether Tether was used to manipulate the price of Bitcoin.18

One way to improve investor confidence in ABSs is to partner with established financial institutions or engaged regulators. An example is TrueUSD.19 The developer TrustToken collaborated with an accounting firm, which provided a real-time, third-party view of TUSD in circulation and their related collateralized fiat funds.20 They connected with an escrow bank, which looks after the holding of the US dollar collateral, as well as running Ethereum nodes to monitor TUSD supply. However, the use of an escrow bank in the case of TrueUSD is inconsistent with the original spirit of disintermediation. Improving governance involves some sacrifice of decentralization.

In 2019, Facebook also attempted to develop an ABS, called Libra.21 To drive the development of this cryptocurrency, they led a Geneva-based organization with many institutional members from both the financial and technology sectors. The idea of Libra is no different from an ABS as it is backed by a reserve comprised of a basket of bank deposits and short-term government securities denominated in a range of national currencies. In September 2019, Facebook announced that the reserve basket would be made up of 50% US dollar, 18% euro, 14% Japanese yen, 11% pound sterling, and 7% Singapore dollar.

Although linking to sovereign currencies should have relieved the concern of price volatility, regulators still cast doubt on the potential impact on financial stability given Facebook's massive penetration globally.22 Some members of the Libra Association, like PayPal, decided to opt out of the project.23 Without sufficient presence of household names in the financial service industry, it is still difficult to boost confidence in the ABS. Forming a membership organization of credible entities is akin to leveraging the franchise value of an escrow in the case of TrueUSD. The bottleneck is still the transfer of the value of trusts from regulated financial institutions to the hands of decentralized community.

Another way to address price instability without a trusted third party is to develop a protocol that can reduce price volatility. This is the approach of algorithmic stablecoins. This type of stablecoin relies on a protocol to manage the excess supply/demand in the market and attempts to smooth the market price. There are two types of algorithm. The first is built-in market intervention. The algorithm adds or removes coins from circulation. However, the automatic regulator intervenes the market by declaring some coins inactive. While algorithmic intervention is very innovative, there has not been a successful example to date, as noted in a comprehensive report by Bullmann et al. (2019).

The second type of stabilization scheme is to mimic the operation of a central bank in the real world. The model develops a program to conduct “open market operation.” If there is an excess supply of coins, the value of coins drops. The stablecoin algorithm will issue a bond at a discount to purchase and destroy the surplus coins. If demand exceeds supply, the algorithm will instruct a repo to redeem the liability from the bond holders.

However, early experience of this algorithm approach has not been convincing. NuBits was one of the early generations of algorithmic stablecoins dating back to 2014. The design was to rely on creating a market force so that people were willing to “arbitrage” or lock up their NuBits in a bond-like instrument. This scheme attempted to establish an interest rate parity so that the value could reach the equilibrium. However, with the lack of confidence in the future value of NuBits, very few participants were willing to lock up in the bond, crippling the price adjustment mechanism. The price of NuBits could not recover and the project was ceased.24

6.2.3 Decentralization, Scalability, and Forks

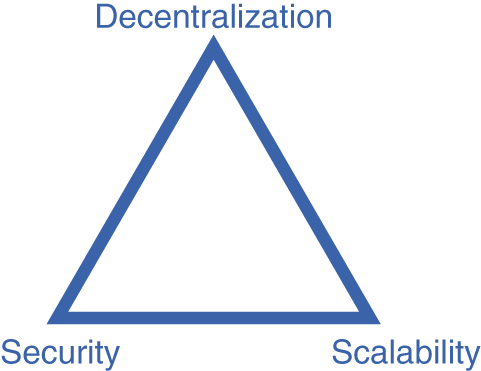

Bitcoin was only a beta version of blockchain. Despite all the promises it offered, the technology was still premature. There are still some technical issues to be addressed for cryptocurrencies to be a genuine payment currency. Particularly, there is a famous scalability trilemma. This trilemma was modified and discussed in the economics literature recently, labeled as blockchain trilemma (Abadi and Brunnermeier 2018).

The Scalability Trilemma is a terminology coined by Vitalik Buterin, the founder of Ethereum (Figure 6.5). He suggested that there existed some tradeoffs underlying the architecture of blockchain. Developers need to strive for an optimal design and juggle three components: decentralization, security, and scalability. Blockchain can build a decentralized and secure ledger system. These two elements should be complementary because there are always backup nodes in the system to retain true information. In a nutshell, DLT reduces the risk of a central point of failure. In our current financial system, if a central clearing house is hacked or comes across an operational failure, the whole system may collapse without a business continuity plan. In an extreme case where all participants perform the same clearing functions, all members effectively ensure a backup in real time for the whole system.

Figure 6.5 The Scalability Trilemma.

Source: Vitalik Buterin

The tech community pointed out a number of security risks that threatened distributed ledgers. Saad et al. (2019) provided a comprehensive review of different attacks facing public blockchains:

- Monopolizing or collusion: one or a set of entities that owns more than 50% of the total tokens outstanding, effectively owns the network. They could perform some malicious operation(s) on the network;

- Sybil attack or pseudonymous threat: one or a set of entities could forge multiple identities on a P2P system in order to effectively control a significant stake in ownership and/or decision making of the network;

- Penny spend or Distributed Denial of Service (DDoS) Attack—flood the network with low-value or malicious transactions in order to stop the network from running.

Of the three types of risks, the last two are general cybersecurity risks facing all network systems. Identity threat and Penny attack can happen in any electronic financial system. It is the first one the DLT needs to tackle. Ultimately, the degree of decentralization is the inverse of monopolization. Since having multiple nodes can reduce the chance of these attacks, decentralization can improve security.

However, decentralization in blockchain is costly as the network expands. Since decentralization and security are complementary, this trilemma can also be reduced to a tradeoff between the scalability and decentralization. The design of Bitcoin blockchain is scale-constrained because the protocol

- Imposes a limit on the amount of information they can contain, i.e. the restrictions that fewer than 10 transactions or one megabyte per second; and

- Takes roughly 10 minutes to validate a block.

This scalability limit began to constrain and become costly when high Bitcoin prices drew massive mining activities in the network in late 2017. When many miners raced for nominating new blocks, the network spent time on addressing the issue of orphan blocks, i.e. blocks already verified but had not been accepted by the network, resulting in a time lag. Given this time lag, many miners were still solving the mathematical problems for the same blocks without knowing the blocks had been solved.

Some developers have attempted to develop alternative consensus algorithms to reduce the burden stemming from proof-of-work. For example, in a proof-of-stake algorithm a new block is chosen, instead of solving the computationally expensive mining problem, based on combinations of random selection and other attributes, such as the coin age, i.e. the number of days the coins have been held.25 However, proof-of-stake seems to be more centralized than proof-of-work as the validation tends to favor blocks in nodes that have larger stakes, rather than giving equal chance to all nodes. These alternative consensus algorithms could increase the throughput significantly but involve a tradeoff between centralization and scalability.

Another way to address the scalability problem is to alter the protocol in order to relax the constraint on transaction requirement for a block formation. Since there is an inherited inefficiency built within the Bitcoin model, changes in protocol are required to reduce the welfare loss (Chiu and Koeppl 2018, Kang and Lee 2019). In August 2017, the Bitcoin community came up with an upgrade in protocol called Segregated Witness (SegWit), which aimed at increasing the scale while keeping the existing chain preserved.26 It was named SegWit because the proposal involved removing the unlocking signature (“witness” data) from the original portion and appending it as a separate structure at the end. This SegWit plan was meant to enable another payment solution called Lightning Network, a “Layer 2” payment protocol on top of Bitcoin for faster and cheaper micropayments bilaterally in a P2P network.27 Some cryptocurrencies like Litecoin tapped this architecture. But this design was not short of weaknesses, such as liquidity shortage, as it needed to borrow from the original network.

In the blockchain community, agreeing on a protocol change in the same chain is called soft fork. However, there is an unhappy version called hard fork. While the mining community of Bitcoin were formulating SegWit, a group of miners decided to develop a new code that allowed for a more aggressive block size (8 megabytes). The name was Bitcoin Cash. Since most Bitcoin users decided to stay, the spinoff one needed to build a new chain and hence a new cryptocurrency. The story of Bitcoin Cash and other “altcoins” highlighted the difficulty in reaching a compromise solution in the mining community.28

The issue of “soft forks” and “hard forks” originated from the Scalability Trilemma. This problem attracted some academic interests, which formalized the tradeoffs from the perspective of industrial organization. Biais et al. (2018) developed a theory for forking in a proof-of-work blockchain. They analyzed the behavior of miners in a stochastic, game theoretic framework. In their model, there existed a case where a miner anticipated all others to fork, and mined a new branch. Therefore, the rational response was to follow them and develop a new chain. This type of game theoretic modeling was also used to study the stability of distributed computing system as a Byzantine Generals Problem (Lamport et al. 1982). To avoid system failure, members in the system must agree on a concerted strategy. However, some of these actors could be unreliable. The beauty of proof-of-work and transparent system in Bitcoin was to overcome the Byzantine problem.

Abadi and Brunnermeier (2018) modeled the blockchain trilemma in a theoretical framework of coordination game, describing the incentive structure of amongst three parameters: (1) decentralization, (2) information correctness, and (3) cost efficiency. Their model provided an analytical framework characterizing fork behavior as well as comparing DLT and centralized intermediation system. When network externalities are weak, coordination among the blockchain community becomes fragile and the community is susceptible to hard forks. The implication is that online retail platforms might be better suited to a blockchain, as the network could benefit from joining the strong existing network.

In fact, the fundamental belief about information sharing in a DLT framework could also be a risk, as it may propel collusion, defeating the original purpose of decentralization. Cong and He (2019) suggest that generating decentralized consensus in blockchain also inevitably leads to greater observability of the network activity recorded on the blockchain. But the increase in observability actually fosters collusion among sellers. The early promise about the ease of entry and enhanced competition in a DLT may not necessarily be welfare improving. The authors suggested future design should regulate the use of the consensus-generating information for the purpose of collusion.

To quicken the solving process of the longest chain, one proposed approach is service payment. In a generic blockchain, the only reward is the new coin to the new block builder. By offering varying amounts of transaction fees, miners can be motivated to validate the history. In 2016, transaction fees became an emerging phenomenon. Using a game-theoretic framework, Easley, O'Hara, and Basu (2019) analyze the economics of transaction fees (Figure 6.6). They propose that higher transaction fees are induced by long waiting time facing the users. However, with users paying increasing transaction fees, their participation will eventually drop, prolonging the time of chain building. Transaction fees are not a solution to solve the scalability problem.

Figure 6.6 Transaction fee of blockchain.

Sources: Blockchain.info; Easley et al. 2019

It appears that the subsequent developments of alternative algorithms have not solved the problem of scalability facing the generic blockchain. Dark et al (2019) believed alternative consensus algorithms, such as byzantine fault tolerance or proof-of-authority, are unlikely to be implemented in widely used public cryptocurrencies because of the centralization needed for proposing and/or validating blocks. The general conclusion is that a sacrifice of decentralization to some degrees is needed. Despite the massive transaction value in the cryptocurrency exchange, the DLT system cannot support the volume of transactions required for running a real economy. It needs another technological breakthrough in order to make cryptocurrency a realistic currency for a country.

6.3 Can Cryptocurrency Replace Money?

6.3.1 Is It a Medium for Payment?

Is cryptocurrency money? Economists typically answer this question religiously, examining the nature of cryptocurrencies using a ruler provided by Jevons (1875). Reports issued by central banks or supranational organizations routinely start with a textbook definition of money with a list of functions money performs in the contemporary context: (1) a medium of exchange; (2) a unit of account; (3) a store of value; and (4) a standard of deferred payment.

In a transaction or exchange, counterparties are willing to accept money because it is a countable and divisible unit that stores value for future use. Therefore, if an item can perform the first three functions, it is a payment currency and is good for cash on delivery. The function of deferred payment describes the ability to create credit, a concept parallel to money supply. It is one step beyond the generic definition of currency and involves an assessment of financial infrastructure. In the fiat money regime, central banks first issue the base money (i.e. the genesis node of “I owe you”) before going through the credit creation process. Therefore, it boils down to two questions: (1) Can cryptocurrency be used for payment? (2) Can it be used to extend liability?

The first question is the most important. Medium of exchange or payment is the most basic function of currency. Cash differs from investment on the asset side of a balance sheet. The former is more fungible than the latter. Bank for International Settlements (BIS) described DLT-based digital currencies:

First, in most cases, these digital currencies are assets with their value determined by supply and demand, similar in concept to commodities such as gold. However, in contrast to commodities, they have zero intrinsic value. Unlike traditional e-money, they are not a liability of any individual or institution, nor are they backed by any authority. As a result, their value relies only on the belief that they might be exchanged for other goods or services, or a certain amount of sovereign currency, at a later point in time.

BIS Committee on Payments and Market Infrastructures, November 2015 (BIS 2015)

The BIS report opined two qualifications for a payment currency: (1) It needs to have “intrinsic value” like commodities; and (2) The value of a currency should come from backing by an authority.

There is an impression that cryptocurrencies offer zero intrinsic value. However, the consumable value generated by gold or silver is not really the basis for pricing their fundamental value. In financial theory, intrinsic value means the present value of expected future cash flows. Sovereign-backed currencies in the form of coins and paper notes do not generate cash flows. There are also saving account deposits in currencies of which the issuing central banks implement zero or negative interest rate policy. Sovereign backing cannot guarantee value (e.g. EM currencies in crisis). As long as it is seen as an asset with a market valuation, the item can perform the store of value function (which could be poor if market pricing is very volatile).

The definition of money is context specific. Currency evolves in accordance with the development of human history. Davies (2002) provides a comprehensive account of different monies from wampum (shell beads) to modern monetary regime. Gold is considered an important monetary reserve because it stores value. But it is not a good medium for payments. Gift cards from Amazon or Starbucks are not legal tender and cannot be used outside their respective stores. But they are payment currencies within the specific network of stores. National currency is officiated administratively by law. But the nature of legal tender is no different from gift cards. If a local currency of an unknown country is not recognizable internationally, it is only acceptable within a country but cannot function as a currency outside the country. Residents in the country may prefer Amazon's gift card than their own currencies.

Likewise, the question of whether cryptocurrency is a medium for payment can only be answered on an ex-post basis. Legal status is not a crucial factor. In fact, Bitcoin or other DLT currency was pointedly motivated by the desire to challenge sovereign power. The status of national currency depends on geographical and regulatory considerations as well as economic factors including price stability and investor orientation. If Bitcoin or Ether becomes increasingly popular, they can be used to denominate underlying assets. They can be used to value debt and equity instruments. Companies can also pay dividends or other payables in cryptocurrencies. The payments can be used to compute discount cash flows, the definition of intrinsic value in the theory of finance.

After a decade of development, Bitcoin is beginning to be accepted by some merchants, although its use is only limited to a dozen of non-mainstream retailing (e.g. Microsoft,29 KFC Canada30). The actual providers of goods and services that claim to accept Bitcoin do not seem to take a currency position on their balance sheets. They require an intermediary to cash out (e.g. Expedia31). The reality is that a company financial statement is still denominated in traditional money. A unit of account is a function of money. But this function also requires a certain level of acceptance, which is based on convention or history. Merchants may be willing to accept cryptocurrency as a means of payment as they expect the price to rise. An exchange or trading platform is still required to connect cryptocurrencies to sovereign currency.

Investment motive is as important as medium of exchange. Garratt and Wallace (2018) point out that people are willing to hold Bitcoins because they treasure the potential capital gain in the future. There can be multiple equilibria. If this belief collapses due to some stochastic shocks, the Bitcoin mania will cease. However, there also exists a scenario that cryptocurrency defeats sovereign currency. It is too early for policymakers to rule out cryptocurrency. Therefore, cryptocurrency could be viewed as both investment goods and medium of exchanges. At this stage, it is more the former.

Athey et al. (2016) conducted a large-scale empirical study to examine the use of cryptocurrencies. They examined a list of approximately 220,000 entities, took about 78 million Bitcoin addresses, and grouped them into 27 million distinct “entities.” Their study found that as of mid-2015, the price of Bitcoin was sensitive to beliefs about the future value and less sensitive to current transaction volume for its own sake.

6.3.2 Can Cryptocurrency Create Credit?

In Economics 102, total money supply is created in a fractional reserve banking system. Central bank issues paper notes and coins as the seed money. The currency in circulation either sits with commercial banks as deposits or is stuffed in people's wallets. At the maximum, a bank can lend a fraction of its deposits and the proceeds become a fraction of deposits in another bank. The recipient bank, in turn, lends out a fraction of this fraction of deposits to the third bank. The fractions are one minus the reserve requirement ratios (RRR) applied to each bank. The reserve sitting with the central banks and the currency in circulation equals the monetary base. The total money supply, typically defined by total deposits held by all commercial banks, is multifold the monetary base.

Blockchain may substitute a part but not the whole of the monetary system because the money creation process is very different. Blockchain is a ledger recorder booking the payment flows amongst parties. The payments are not necessarily borrowing and lending activities. The distributed ledgers may potentially replace the payment booking system of our financial system. The coins may be a candidate to replace the currency issued by central banks as they can fulfil the requirement of medium of exchange, store of value, and unit of accounting. However, the system by itself does not embed mechanism to extend M0 to M2. To make cryptocurrency a board money, it needs an extra layer of infrastructure for credit creation.

Interest rate is an important element in the monetary system as it induces credit creation. It is the price paid to lenders for forgoing present spending. Central banks use it to influence macroeconomic activity. In Bitcoin, the ledgers can record the net balance of all network members and the aggregate balance should be the total amount of coins in circulation. Network members can borrow and lend coins amongst themselves. But there is no single authority to set a benchmark interest rate. Bitcoin network does not identify account payment or receivable information and publish a market interest rate. (The smart contract feature of Ethereum can perform this function.) The interest rate benchmark likely comes from the sovereign currency system. Bitcoin lenders and borrowers likely refer to similar rates of US dollar loans (or other currency), adjusted for expected change in “exchange rate” of Bitcoin against the US dollar.

Some fintech companies launched crypto-backed loans that allowed holders of cryptocurrencies to utilize their assets as collateral for cash in US dollar, euro, or stablecoins. Some lenders offered up to 90% loan-to-value ratio. The interest rate appeared to be akin to normal US dollar loans. Some fintechs explored the use of Secured Automated Lending Technology (SALT) based on the technology of smart contracts.32 This type of platform facilitated sovereign currency borrowing using blockchain-based assets as collateral. One provider, Youholder, also allowed borrowers to use other cryptocurrencies (e.g. ETH) to back their loans in euro, dollar, and also Bitcoin. Using the language of finance, borrowing BTC using ETH could be expressed as shorting BTC/ETH. Some fintechs seemed to perform like a bank. Celsius Network, for example, claimed to pay interest to members’ deposits, using the BitGo Trust Company as a custodian of their crypto wallets.33 Members could borrow at an interest rate higher than the deposit rates.

Technically, a blockchain system does not need a bank. In reality, the blockchain community needs to draw resources from the real world because their ecosystem has not developed to a self-sufficient stage. They interact with the financial system of the real world on two fronts:

- Fund raising: To develop their systems, companies in the virtual world need financial support from the real world in the form of seed money. Venture capital and workers are still rewarded in sovereign currency.

- Currency exchange: Buying and selling of cryptocurrencies involves conversions between sovereign currencies and cryptocurrencies. Crypto exchanges or fintech companies receive sovereign currency and maintain bank accounts in formal banking systems.

While the blockchain ecosystem has developed channels to facilitate the credit flows between cryptocurrency and sovereign cash, almost no financial institutions are willing to go out on a limb because of regulatory concern. In some jurisdictions, banks ban the purchase of Bitcoin using their credit card. Regulators are the gatekeeper to limit the exposure of formal financial institutions to crypto assets. In addition, many fintech sites are not available to citizens in some jurisdictions, as they are not licensed to provide financial services in these countries. The real world has established accounting treatment (e.g. US GAAP) for airlines’ frequent-flyer programs, valuing the mileages as a liability item. Unless similar treatment is extended to cryptocurrency, there will still be a gap between the formal financial sector and the blockchain economy.

6.4 Regulatory Responses

The rapid development of cryptocurrencies has aroused the interests of governments, financial regulators, and central banks. There are typically two types of responses. On one hand, central banks see cryptocurrencies as a risk. Financial institutions are warned to be cautious about the potential use of cryptocurrencies as a tool for money laundering or terrorist finance. Central banks are also concerned that cryptocurrencies could undermine the effectiveness of monetary policy. Paul Krugman believes cryptocurrency is a bubble and may set the monetary system back 300 years.34 On the other hand, governments do see the DLT as an opportunity to enhance financial service delivery. Many countries have started to develop their official version of digital currencies. They also explore the opportunity to upgrade payment infrastructure via mobile wallets.

Bitcoin has been perceived as a vehicle in the underground economy and a means to support illegal activities. In 2014, the Financial Action Task Force (FATF) of BIS published an extensive report on digital currency issues, noting that “convertible virtual currencies that can be exchanged for real money or other virtual currencies are potentially vulnerable to money laundering and terrorist financing.” It also provided guidance on a risk-based approach to handling virtual currency payments for products and services, aiming to enhance the global consistency and the effectiveness of the Anti-Money Laundering/Counter-Financing of Terrorism (AML/CFT) standards.

Another regulatory response is to develop a central bank's version of digital currencies, i.e. Central Bank Digital Currency (CBDC). Since the money is issued by central banks, CBDC is virtually an electronic version of paper notes and coins. The rationale is to provide a safe and secure digital currency for retail transactions. Currently, electronic transactions via credit or debit cards are still going through the banking system. For CBDC to be meaningful, central banks should aim to develop some electronic tokens that are counterfeit resistant and transferable without going through banks. This was the approach of Riksbank, which explored the development of e-krona in view of declining cash balance (Griffoli et al. 2018).

Many countries develop CBDC for other, different reasons. They include antitrust, risk management, cost efficiency, and financial inclusion (see Table 6.2). In general, policymakers believe digital currency can improve financial inclusion. The idea is that there are still some segments of the population that have no access to (costly) financial services. Digital option can facilitate their transactions. However, in the case of China, the story also concerns public–private competition. Although internet giants like Alibaba and Tencent are considered very successful businesses, there has been some concern about their monopolistic power. Internet business enjoys strong network externalities that support natural monopoly (just like the US dollar). If platform operators begin to levy the users, consumers will have very few alternatives. Given this consideration, CBDC appears to be a legitimate development.

Table 6.2 Rationale for Developing CBDC.

Source: IMF (Griffoli et al. 2018)

| Anti-monopoly | Operationalrisks | Cost efficiency | Financial inclusion | |

| Bahamas | X | |||

| Canada | X | |||

| China | X | X | X | X |

| CBCS | X | X | X | |

| ECCB | X | X | X | |

| Ecuador | X | |||

| Norway | X | |||

| Senegal | X | |||

| Sweden | X | X | ||

| Tunisia | X | |||

| Uruguay | X | X |

Unfortunately, CBDC unlikely presents any major breakthrough in upgrading our financial architecture. The industry has already tapped the mobile technology quite successfully during the past decade. One example is RFID. Retail payments can be easily done via payWave at the point of purchase, enhancing the speed of card-based or phone-based transactions. Other examples are Alipay, which has replaced the use of cash in China. In the case of WeChat Pay, Tencent can combine the spending pattern with their social media platform. Combined with the application of big data technique, these private sector solutions drive the technological improvement in their service delivery. Regulators can only react to the technological development passively.

From a macroeconomic perspective, CBDC is nothing more than a “save the paper” version of traditional currency. The digital cash will likely be a list of unique serial numbers, similar to the string printed on the paper notes. This development does not introduce any fundamental change to the fiat money regime, i.e. CBDC is still the central bank's liability to the public. In blockchain, money is not created by a central authority. The supply of currency is purely a function of computational power of the network. The concept of CBDC does not close the gap between sovereign and cryptocurrency.

6.5 Implication on Monetary Policy

The economics literature to date has mainly focused on the microeconomic structure of blockchain. Academic economists seem to have little concerns about the impact of cryptocurrencies on the monetary policy and financial stability. In terms of market capitalization, the cryptocurrency market capitalization was about USD 190 billion by the end of 2019. This is less than 5% of the balance sheet of the US Fed (USD 4.1 trillion). As discussed in the previous section, regulators mainly see the cryptocurrency as a potential source of financial instability. Central banks only appreciate the feature of DLT and do not view cryptocurrencies as an alternative medium of exchange and even store of value. The authorities do not accept the view that privately developed cryptocurrency will replace sovereign currencies.

However, there is no reason for policymakers to be complacent. In the digital world, new trends are constantly being executed at lightning speed. Financial regulators may cut the tie between the formal banking system and privately run cryptocurrency. But society may have already accepted cryptocurrency as a common form of payment. If the economy turns out to be cryptonized instead of dollarized, central banks could be marginalized. Monetary policy will be ineffective. The situation will be very similar to the experience of many emerging markets in which local residents prefer foreign rather than local currency. The local central bank cannot use interest rate policy to influence inflation or the exchange rate.

Increasing use of an alien currency also affects the external balance of an economy. Some countries, such as Venezuela35 and China,36 cracked down on cryptocurrency exchanges, as they feared the negative consequences to financial stability. While AML/CFT as well as consumer protection are usually the cited reasons for regulatory tightening, the action can also curb capital outflows because cryptocurrency is indeed an efficient method for cross-border payments. This new asset class will risk the external balance of some countries, especially if the economy is vulnerable. In these countries, cryptocurrencies are particularly popular. Local residents are willing to pay a higher price for the coins. The price is virtually the exchange rate against the local currency. Cracking the cryptocurrency exchanges is a form of capital control.

Therefore, central banks need to understand the very nature of cryptocurrency. First, the supply of cryptocurrency is not controlled by a foreign central bank. To deal with an official foreign currency, a local central bank needs to read the monetary policy of another central bank (e.g. US Federal Reserve). This does not apply to cryptocurrency because its “money supply” is based on an algorithm. Actually, the supply function of Bitcoin is easier to predict than the preference of different Federal Open Market Committee (FOMC) or monetary policy committee (MPC) of other central banks. Secondly, cryptocurrency can be regarded as a non-interest-bearing asset. In considering exchange rate management, covered or uncovered interest rate parity does not apply. Thirdly, there is no global authority like the IMF or BIS to regulate international affairs. In blockchain, any change in protocol is decided by consensus of the network members. Cryptocurrency follows a different rule of law.

Fernández-Villaverde and Sanches (2016) analyzed the competition between cryptocurrency and sovereign money. They showed that privately issued money can create problems for monetary policy implementation if a central bank follows a money growth rule. It is crucial for private money issued by profit-maximizing entrepreneurs (or a network of them) to be capped (such as Bitcoin) so that its existence still allows a price stability scenario. One important insight from this study is that the competition can help uplift the discipline of fiat money issuers, as they need to ensure the attractiveness of fiat money over cryptocurrencies.

Many central banks adopt an explicit inflation target in controlling money supply. This contrasts the supply of Bitcoin, which is based on proof-of-work as opposed to economic targets. Schilling and Uhlig (2018) characterize this difference as when there exists an inflation target central bank with the presence of Bitcoin issued by a decentralized network. Equilibrium condition is derived through the tradeoff between currency holding for speculation and using for payments. An important message of this study is when a central bank issues money in such a way to have achieved the inflation target of above unity, there are conditions where the value of Bitcoin becomes zero. Under this condition, sovereign currency can compete away cryptocurrency.

To doubters, cryptocurrency plays no role in economics. Fundamentalists believe the idea of a digital token is completely flawed because cryptocurrency does not inherit the features of traditional money. To them, a qualified medium for payments should be one that holds value. It is a matter of trust. Sellers are willing to receive digital tokens when they know they can exchange it for something at least as valuable. However, price volatility of many cryptocurrencies deters acceptance. The general expectation is that the mania of cryptocurrency will eventually vanish. Policymakers can continue to acknowledge the technological aspect of blockchain and appreciate the security feature of DLT. They can continue to assume that the current monetary policy regime remains intact.

The major problem of this assumption is double standard. Both fiat money and cryptocurrency do not carry intrinsic value. The foundation of the US dollar or other G10 currencies is the confidence in the political-economic conditions of the issuing countries. However, this foundation is not unshakable. The trust is based on an assumption that their central banks will maintain price stability. However, history suggests that the policy of many central banks has not been really disciplined. If Bitcoins can coexist with sovereign currency under some conditions as postulated by Schilling and Uhlig (2018), it will gradually substitute sovereign money. With the rise of anti-authoritarianism, public belief in sovereign currency is dissipating.

Network externalities are the foundation of the US dollar. People are willing to hold it because it is highly convertible. It is freely usable in purchasing goods and services or converting into other currencies. Like the US dollar, cryptocurrency is also borderless and global. The power of network externalities can also apply to cryptocurrency. The more people use it, the more it will gain acceptance. Economists can rule out cryptocurrency as money based on some criteria from a textbook. But the real world can ride roughshod over the economists’ verdict.

When cryptocurrency becomes a global standard, the law and order of the international monetary regime will be redefined. Global monetary affairs will witness a power shift. Currently, the stablecoin still needs to promote itself by pegging with a sovereign currency. In the future, central banks may need to build a cryptocurrency reserve to support fiat money. Banks and other financial institutions will rediscover their value proposition. First movers in the crypto community will reap the benefits and capture the value added. Fintech would provide a whole new way to organize blockchain-based lending, depositing, and investing. The impact of Satoshi Nakamoto's paper is no less than the Nixon shock.

Notes

- 1 Bitcoin.org. (https://Bitcoin.org/Bitcoin.pdf).

- 2 Libra.org. (https://libra.org/en-US/wp-content/uploads/sites/23/2019/06/LibraWhitePaper_en_US.pdf).

- 3 https://www.merriam-webster.com/dictionary/fintech.

- 4 Washington Post. March 7, 2019. (https://www.washingtonpost.com/opinions/global-opinions/china-is-racing-ahead-of-the-united-states-on-blockchain/2019/03/07/c1e7776a-4116-11e9-9361-301ffb5bd5e6_story.html).

- 5 Deloitte. 2019 Global Blockchain Survey. (https://www2.deloitte.com/content/dam/Deloitte/se/Documents/risk/DI_2019-global-blockchain-survey.pdf).

- 6 PWC. Blockchain in Business. (https://www.pwc.com/gx/en/issues/blockchain/blockchain-in-business.html).

- 7 IDC. Worldwide Blockchain Spending Guide. March 4, 2019. (https://www.idc.com/getdoc.jsp?containerId=prUS44898819).

- 8 On June 26, 1974, counterparty banks around the world paid Deutsche Marks to Herstatt in Cologne, expecting Herstatt to reciprocate and pay out USD during local banking hours in the US. But Herstatt declared bankruptcy that day and never fulfilled its leg of these FX transactions, leaving numerous institutions with huge losses.

- 9 World Bank. (2017). Distributed Ledger Technology (DLT) and Blockchain. Fintech note no.1.

- 10 The number of transactions per block can be viewed on https://www.blockchain.com/charts/avg-block-size?.

- 11 Vitalik Buterin. (2017) (https://medium.com/@VitalikButerin/the-meaning-of-decentralization-a0c92b76a274).

- 12 Ethereum.org. (https://ethereum.org/).

- 14 CoinMarketCap.com. (https://coinmarketcap.com/).

- 15 Bloomberg. April 30, 2019. (https://www.bloomberg.com/news/articles/2019-04-30/tether-says-stablecoin-is-only-backed-74-by-cash-securities).

- 16 Forbes. March 14, 2019. (https://www.forbes.com/sites/francescoppola/2019/03/14/tethers-u-s-dollar-peg-is-no-longer-credible/#7c3fb4e3451b).

- 17 Brave NewCoin. October 10, 2019. (https://bravenewcoin.com/insights/stablecoin-battle-heats-up-with-class-action-lawsuit-filed-against-tether).

- 18 Bloomberg. November 20, 2018. (https://www.bloomberg.com/news/articles/2018-11-20/Bitcoin-rigging-criminal-probe-is-said-to-focus-on-tie-to-tether).

- 19 TrustToken.com. (https://www.trusttoken.com/trueusd).

- 20 CoinDesk. March 5, 2019. (https://www.coindesk.com/trueusd-stablecoin-soon-to-have-real-time-monitoring-of-dollar-backing).

- 21 Libra. (2019). Libra White Paper. (https://libra.org/en-US/wp-content/uploads/sites/23/2019/06/LibraWhitePaper_en_US.pdf).

- 22 Bloomberg. December 18, 2019. (https://www.bloomberg.com/news/articles/2019-12-18/fed-s-brainard-raises-red-flags-over-facebook-s-libra-project).

- 23 Fortune. November 20, 2019. (https://fortune.com/2019/11/20/paypal-ceo-dan-schulman-libra/).

- 24 Coin Telegraph. December 13, 2018. (https://cointelegraph.com/news/major-stablecoin-basis-to-close-return-funds-to-investors-sources).

- 25 https://blackcoin.org/blackcoin-pos-protocol-v2-whitepaper.pdf.

- 26 https://github.com/Bitcoin/bips/blob/master/bip-0141.mediawiki.

- 27 Bloomberg. March 15, 2018. (https://www.bloomberg.com/news/articles/2018-03-15/technology-meant-to-make-Bitcoin-money-again-is-going-live-today).

- 28 Wall Street Journal. December 23, 2017. (https://www.wsj.com/articles/Bitcoin-cash-litecoin-ether-oh-my-whats-with-all-the-Bitcoin-clones-1514037600).

- 29 Microsoft. https://support.microsoft.com/en-us/help/13942/microsoft-account-how-to-use-Bitcoin-to-add-money-to-your-account.

- 30 CBC News. January 13, 2018. (https://www.cbc.ca/news/canada/saskatoon/kfc-canada-cryptocurrency-blockchain-Bitcoin-bucket-1.4486698).

- 31 Expedia. https://www.expedia.com/Checkout/BitcoinTermsAndConditions.

- 32 Salt Lending.com. (https://saltlending.com/).

- 33 Celsius Network. (https://www.bitgo.com/clients/client-story-celsius-network).

- 34 New York Times. July 31, 2018. (https://www.nytimes.com/2018/07/31/opinion/transaction-costs-and-tethers-why-im-a-crypto-skeptic.html).

- 35 Business Insider, March 14, 2017. (https://www.businessinsider.com/venezuela-bitcoin-use-popularity-restrictions-and-crackdown-2017-3).

- 36 Bloomberg, November 27, 2019. (https://www.bloomberg.com/news/articles/2019-11-27/all-you-need-to-know-about-china-s-latest-crypto-crackdown).