Executive Summary

Business sustainability can be beneficial to both internal and external stakeholders. Stakeholders are those who have vested interests in a firm through their investments in the form of financial capital (shareholders), human capital (HC) (employees), physical capital (customers and suppliers), social capital (society), environmental capital (the environment), and regulatory capital (government). This chapter presents all types of capitals and their integrated contribution to and effects on business sustainability.

Introduction

Traditionally, business organizations have focused on the role of financial capital in creating value for shareholders. Recent move toward and acceptance of business sustainability encourages business organization to pay attention to other capitals in creating shared value for all stakeholders. The magnitude of environmental, ethical, social, governance (EESG) sustainability-focused investment is now more than $20 trillion. EESG funds require that corporations define their purpose of generating financial returns and achieving social and environmental impacts. For many years, the focus on profit maximization for shareholders worked in U.S. financial markets. Globalization and technological advances, and often disruption, have forced corporations to focus on the short-termism of meeting or beating analysts’ forecast expectations. However, corporations are now facing pressures from social activists and stakeholders to pay attention to the interests of customers, suppliers, employees, society, and the environment, among others, to create shared value for all stakeholders. Achievement of financial economic sustainability performance (ESP) and nonfinancial EESG sustainability performance requires business organizations and their board of directors and executives effectively utilize financial and nonfinancial capitals presented in this chapter.

Types of Capitals

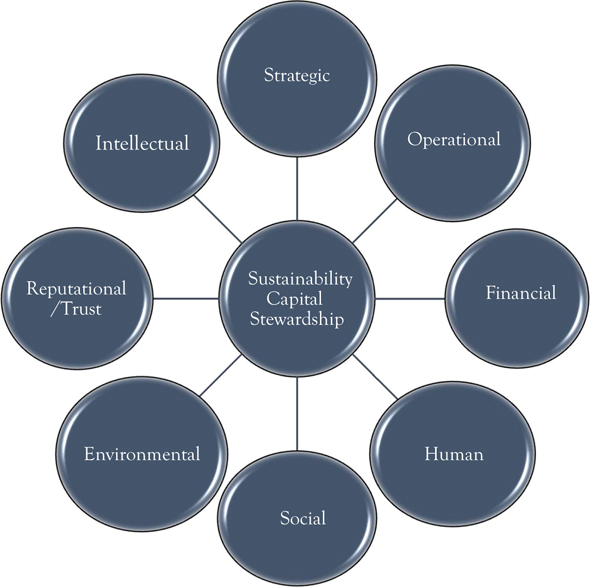

Business organizations have traditionally employed financial capital, both equity and debt capitals, in financing and acquiring assets to use in the operation in generating revenues with less focus on nonfinancial capitals. The recent move toward sustainability requires business organizations to utilize all types of financial capital (equity and debt) and nonfinancial capital (strategic, reputational, human, social, and environmental) to generate shared value for all stakeholders. Figure 2.1 presents sustainability capital stewardship and all associated capitals including strategic, operational, financial, human, social, environmental, reputational/trust, and intellectual. The Committee of Sponsoring Organizations of the Treadway Commission (COSO) and the World Business Council for Sustainable Development (WBCSD) issued “Guidance for Applying Enterprise Risk Management (ERM) to Environmental, Social and Governance (ESG)-related Risks” in October 2018.1 The COSO/WBCSD is intended to assist entities of all types and sizes to manage their sustainability ESG-related risks that affect their bottom-line financial earnings as well as business success and survival.

Figure 2.1 Sustainability capitals

There is no universal or agreed-upon definition of EESG-related risks also known as sustainability risk factors that may include the EESG-related risks and/or opportunities. Environmental risks are risks related to climate change, global warming natural resources, pollution, and waste and environmental opportunities. Ethical risks are failure of conducting business, ethically and legally in compliance with all applicable laws, rules, regulations, and standards. Social risks are risks related to HC, workplace conditions, product liability, stakeholder opposition, and social opportunities. Governance risks are risks related to corporate governance measures, noncompliance with all applicable laws and regulations, HC, product liability, stakeholder opposition, and social opportunity.

According to Paul Druckman, IIRC Chief Executive, there are over 1,000 businesses worldwide using Integrated Reporting in 27 countries.2 The IIRC suggests six capitals as follows: (1) financial capital, (2) manufactured capital, (3) intellectual capital, (4) HC, (5) social and relationship capital, and (6) natural capital, which organizations can utilize in creating shared value for all stakeholders.3 Management acts as the steward of strategic capital, financial capital, HC, social capital, and environmental capital, and acts as the active and long-term-oriented steward of all stakeholders including shareholders. Figure 2.1 shows eight sustainability capitals of strategic, financial, human, social, environmental, reputational/trust, intellectual, and manufactured. Some of these capitals are interrelated but they all collectively contribute to the creation of shared value for all stakeholders.

The ongoing challenges brought on by the COVID-19 pandemic while requiring management to simultaneously consider divergent economic, governance, social, and environmental issues enable management to effectively exercise stewardship over a broader range of business capital from financial capital to environmental, social, and reputational capital to ensure continuity and nonfinancial HC of protecting safety, health, and well-being of employees, customers, and suppliers. The relationship between business, society, and the environment is complex and often tense and becomes more relevant in the post-COVID-19 era because management is now required to be a good steward of all capitals from financial to human, environmental, and social.

Strategic capital relates to management strategic planning and being accountable for strategic plans, decisions, and actions. Strategic planning is a process of establishing purpose and mission, making decisions, taking actions documenting and communicating plans of actions throughout the organization to those who are affected by actions, evaluating compliance with actions, and holding individuals accountable. The strategic plans enable organizations to document their purpose, mission, values and vision, and values as well as establishing goals and the action plans to implement them. The economic order, stakeholder expectations, corporate culture, and business environment are changing in the post-COVID-19 era, and how business organizations define their purpose and measure the achievement of their success are changing too. Purpose determines why the organization exists, what is its mission, who are the stakeholders, and what are its objectives and strategies in achieving the objectives. The main objective function for any business organization has been and continues to be the creation of shared value for all stakeholders including shareholders, creditors, customers, suppliers, employees, government, society, and the environment. Changes in the purpose, mission, objectives, and strategies for business organization in the aftermath of the COVID-19 crisis are important to the long-term sustainability of the organization.

Every company should have its unique purpose determined in its charter of incorporation to maximize its positive impacts on all stakeholders including society and the environment and to minimize the negative impacts on multistakeholders. In case of nonexistence of and/or inadequate “Statement of Purpose,” all executives in the c-suite under the oversight function of the board of directors and approval by majority shareholders should establish an appropriate stakeholder-inclusive “Statement of Purpose.” The purpose of profit maximization and shareholder wealth creation has changed to create shared value for all stakeholders. To effectively achieve this new purpose, corporations are expanding their performance to both financial/quantitative economic performance (ESP) and nonfinancial/qualitative EESG sustainability performance. Sustainability has become an economic and strategic imperative with potential to create opportunities and risks for businesses.

Mission reflects the organization’s determination to stay with its purpose and its achievement in the short-, medium-, and long term. Companies are now adopting the corporate mission of profit with purpose in creating shared value for all stakeholders by shifting their goals to create shareholder value while fulfilling their social, environmental, and governance responsibilities. Corporate objectives have sustainably changed in the post-COVID-19 pandemic to survival in the short term, continuity in the medium term, and sustainability in the long term. The board of directors pay more attention to the well-being, safety, and health of their employees, customers, and suppliers.

In the aftermath of recent financial crises, it is not uncommon for investors to lose confidence in firms. The board of directors can rebuild trust by starting off with focusing on more long-term goals. While the board has fiduciary duties to carry out, a lot of times they fall prey to pressures of obtaining immediate results, which may deviate from the long-term picture. Instead, strategies should be implemented that would allow the firm to withstand short-term pressures. The board’s priorities should be more focused, which can be achieved by the board delegating duties to the committees that do not require the board’s full attention, allowing the board to focus on the priorities of the company. In order to rebuild trust, directors must always act in the best interests of the company, even if it means disagreeing with shareholders and risking reelection. Strong communication with shareholders should be established in order to understand their concerns, ideas, feedback, and if there is any disconnection in their views. Strategic capital reflects the organization’s value, vision, culture, purpose, mission, goals, objectives, plans of actions, and accountability.

Operational Capital

A firm’s operational capital reflects an organization’s resources in producing goods and services demanded by their constituencies and stakeholders that are not detrimental to society and the environment. Corporate culture of integrity and competency plays an important role in establishing policies, procedures, and processes to utilize maximization of the operational capital. The board of directors as representative of shareholders should design directions for operational efficiency and effectiveness and guide management to implement and maintain policies and procedures to achieve both financial ESP and nonfinancial EESG performance in creating shared value for all stakeholders including shareholders, creditors, employees, customers, suppliers, communities, society, and the environment. The board of directors should oversee that the organization is pursuing the goal of sustainability performance and compliance with all applicable laws, rules, regulations, standards, and best practices. While the board of directors should avoid micromanaging operation, it should provide strategic directions for management to continuously improve efficiency and effectiveness. Effective corporate governance measures should be placed to promote vigilant oversight function by the board of directors, effective managerial function by the management, and accountable and responsible actions by other corporate gatekeepers including auditors and financial advisors.

Financial Capital

Financial capital consists of both equity and debt capital. Financial ESP can be achieved by continuously improving capital productivity by optimizing supply chains, cost reengineering focused on reducing operating, production, and compliance costs, improving employee productivity and efficiency, and focusing on activities that create long-term, enduring, and sustainable financial performance. A focus on economic sustainability can also create opportunities for business innovation and growth by promoting sustainable products and services, new customer relationships, and new markets through environmentally friendly and socially acceptable products and services. ESP is measured in terms of long-term accounting-based measures (return on equity and sales), market-based measures (stock returns and market-book value), and long-term investments (R&D and advertising) and disclosed through a set of financial statements disseminated to shareholders in assessing the risk and return associated with their investments.

Human Capital

HC is an asset of skills processes by the labor force that can be utilized to generate other assets. HC is defined by the Organization for Economic Co-operation and Development (OECD) as “the knowledge, skills, competencies and other attributes embodied in individuals or groups of individuals acquired during their life and used to produce goods, services or ideas in market circumstances.”4 HC is defined as attributes of labor that increase productivity and viewed as investment in labor including education, training, skills, capacity, health, ability to adapt to achieve productive capacity, goals, and maintain innovative and create economic value. HC factors as part of nonfinancial EESG sustainability are relevant and material to investors.

HC is becoming more important as a valuable and productive asset for public companies and employees are becoming important stakeholders for several reasons. First, employee participation in the production and service processes is essential as employee productivity improves corporate performance. Second, employees are becoming shareholders by investing in the company’s shares through 401(K) and 529 plans and direct investment. Third, employees in many countries are given the opportunity to represent on the board of directors of public companies. Finally, the COVID-19 pandemic has caused business organizations to assess the HC risk by making safety, health, and well-being of employees, customers, and suppliers a prerequisite for reopening business. HC issues are relevant to the company’s management of human resources as key assets to delivering long-term value. These issues that affect the company’s bottom line through employee productivity, labor relations, and the health and safety of employees. HC is viewed as an important asset that contributes significantly to the long-term and sustainable value creation and value protection. There is a need for proper identification, measurement, recognition, and reporting HC.

One of the greatest concerns regarding HC is whether or how companies should get their stakeholders, especially their employees, involved in the process of making important corporate-level decisions, rather than pursuing the shareholder primacy model in which the benefits of shareholders are maximized. Some advantages of the shared governance (also known as codetermination) include better coordination, information flows between board and employees, employees’ loyalty and motivation, implicit contracts enforcement, and alignment of shareholders and employees’ interests. In the working paper “Labor in the Boardroom” in 2019, Jäger, Schoefer, and Heining exploit a 1994 reform experiment in Germany, which mandated the representation of worker-elected directors in the board of some stock corporations, while eliminating board seats of workforce representatives in others. The result of the experiment shows that workers’ participation in the board of directors actually increases capital by increasing production output per worker and reducing outsourcing. Despite no clear effect on financial capacity and profitability, shared governance is found to reduce interest payments over debt by an insignificant amount, and therefore, makes firms with worker-elected directors seem slightly less risky. It is also found that the lack of workforce representatives in the board tends to cause underinvestment, while codetermination can increase investment. However, too much worker bargaining power may result in some inefficiencies such as overinvestment. On top of that, if worker-elected directors only compose the minority of board seats, they tend to be more moderate to build rapport with other shareholders, rather than excessively voicing demands.5

The codetermination model is typically promoted in European countries, especially Germany. The publicly listed companies in Germany have supervisory boards overseeing their executive boards. These supervisory boards must have workforce representatives composing one-third or half of the seats if the companies have more than 500 employees according to Article 4(1) of the German Law on One-Third Participation and German Co-Determination Act of 1976. Article 96(2) of the German Stock Corporation Act also mandates companies with more than 2,000 employees to assign at least 30 percent of board seats to directors of each gender. The worker-elected directors are either employees working at the firms for at least one year, trade union members in the companies, or managerial staff. On top of the supervisory board, workers participation is represented in works councils. Works councils function similarly to trade unions, but their members are not necessarily trade union representatives. The number of work council members is proportionate to the number of employees in the companies, with the exclusion of senior managers (represented by other bodies), the distinguishment of manual and nonmanual employees, and gender equality. Compared to workers representation in the board, workers participation through company shares is less popular as German regulations discourage employee equity-based incentives with tax exemption threshold of €360 (which is significantly lower than the threshold of other countries in Europe, ranging between €2,065 and €6,000. At the “Ownership Day” conferences in 2015 and 2017, companies and experts signed an appeal to increase tax exemption threshold to €3,000, remove dividends and interests taxes, and simplify regulations. According to the appeal, only 14 percent of Germans are shareholders and only half of DAX 30 corporations provide their employees with equity-base incentive plans.6

Unlike in most European countries, the shareholder primacy is more popular in the United States. As shareholders’ benefits are maximized, no workers are involved in the corporate decision-making process and riskier investment is usually made. Even with the help of labor unions, worker bargaining power is still low if the issues are beyond the terms and conditions of the National Labor Relations Act (NLRA). Amendments to labor laws should be made on both state and federal levels to enable employees’ participation, engagement, and impacts on the nomination, and election of corporate board of directors. Recently, there have been proposals from the Reward Work Act and the Accountable Capitalism Act to mandate one-third to 40 percent board seats to be assigned to employees. These proposals encourage the stakeholder theory to replace the shareholder primacy model even though the implementation of codetermination policy can be challenging in the United States.7

Environmental Capital

The environmental capital is relevant to environmental impacts of the operation either through the use of natural resources and the nonrenewable, as inputs to the supply chain production or through harmful releases into the environment that could affect bottom-line financial earnings. The environmental capital is crucial to the long-term sustainability of business organizations and their growth and innovation as well as the economic prosperity worldwide in leaving a better environment for next generations. Environmental capital is the natural resources employed and are available to an organization consisting of both renewable resources such as plants and clean air, and nonrenewable assets such as oil and gas. Environmental capital reflects the impact of an organization’s operation on the environment including negative values such as contamination, pollution, and desertification. Natural capital is part of the environment including fertile soils, geology, air quality, clean water, and all living organisms, which affect the triple bottom line of people, profit, and the planet. Organizations should preserve the environment and leave a better environment for next generations.

Social Capital

The social capital is relevant to the company’s management of relationships with key outside stakeholders including suppliers, customers, local communities, the public, and the government. Social capital is relevant to human rights, responsible business practices, local economic development, customer privacy, and other social matters. The perceived social injustice and unrest in recent years have made social capital more relevant and important to business organizations. Social capital involves the effective functioning of social groups through interpersonal relationships, a shared sense of identity, a shared understanding, shared norms, shared values, trust, cooperation, and reciprocity. Social capital is a measure of the value of resources, both tangible (e.g., public spaces, and private property) and intangible (e.g., actors, HC, and people), and the impact that these relationships have on the resources involved in each relationship, and on larger groups. It is generally seen as a form of capital that produces public goods for a common purpose. Social capital is defined by the OECD as “networks together with shared norms, values and understandings that facilitate co-operation within or among groups.”8 In this definition, the networks are broadly considered as real-world links between groups or individuals including friends, family, colleagues, and local, national, and international communities. The shared values reflect respect for people’s safety and security as well as safety, health, and well-being of others.

Social capital has been used to explain the improved performance of diverse groups, the growth of entrepreneurial firms, superior managerial performance, enhanced supply chain relations, the value derived from strategic alliances, and the evolution of communities including positive impacts of human interaction. The positive impacts of social capital are tangible or intangible factors such as useful information, future opportunities, and innovative ideas that can be generated from personal relationships and networks within and outside an organization that enable productive work environment that adds to the bottom-line earnings. Social capital is a set of shared values that enables individuals to work together in a group to effectively achieve a common purpose and goal that help them all. Social capital can be attributed to the factors and characteristics that describe how people are able to band together in society to live harmoniously. In business, social capital can contribute to a company’s success and sustainable performance by promoting a sense of shared values, mutual respect, and common goals.

Manufacturing Capital

The manufacturing capital is very broad and consists of issues that pertain to the integration of environmental, human, and social issues into the company’s value-creation and value-protection processes. These issues are resource recovery, product innovation, use phase and disposal of products, and efficiency and responsibility in the design. Enhancing accountability and stewardship for the broad base of capitals (financial, manufactured, intellectual, human, social and relationship, and natural) and emphasizing their interdependencies. Manufacturing capital is often used interchangeable with operational capital in describing activities and related resources relevant to customer relationships, trademarks and trade names, supplier relationships, franchises, and licenses. The value of the relationships that a business organization establishes with its customers, and employees can contribute to maintaining manufacturing capital that can be used in the production of goods and services and thus contribute to the long-term sustainability of the business.

Reputational/Trust Capital

The evolution of trust in the now stakeholder era of capitalism has grown increasingly difficult to manage. Research examines global governance and the rule of law with the changing face of leadership, ethical technology, and more.9 Currently, corporations are instructed to make trust and reputational strength difficult to achieve. Business purpose should be molded into an applied enterprise instead of a static set of promises. Corporations should begin investing in aligned and effective governance within as well as leadership, employee engagement, and ethical sourcing for green investment decisions and responsible tax policies to build up their reputation and trust capital. Good reputation with stakeholders including shareholders, employees, creditors, customers, suppliers, and communities can take many years to build and can be easily and immediately destroyed with unintentional mistakes and irregularities, and/or intentional fraud to deceive stakeholders.

Corporate culture plays a crucial role in the trust capital. Speaking of culture, Wilcox states that: “There are, however, three proverbial certainties that have developed around corporate culture: (1) We know it when we see it, and worse, we know it most clearly when its failure leads to a crisis. (2) It is a responsibility of the board of directors, defined by their ‘tone at the top’. (3) It is the foundation for a company’s most precious asset, its reputation.” To assess culture of a company, several business metrics such as worker retention, customer satisfaction, legal issues, and so on can be used.10 Regarding the popularity of shareholder primacy in the United States, the management aims at maximizing the benefits of shareholders. This principal–agent model usually leads to the misalignment of interests, which can be detrimental to trust or reputational capital. Therefore, a reduction in the power of shareholders, or in other words, an increase in power of other stakeholders, especially employees, can be the solution to problems related to integrity in corporate cultures.11 Moreover, stakeholders now require more transparent communication, which challenges the board of directors to maintain a balance among transparency, confidentiality, and independence.12

Intellectual Capital

Intellectual capital refers to the intangible assets that contribute to a company’s bottom line earnings as well as long-term sustainability performance and business continuity and survival. Intellectual capital presents resources and intangible assets consisting of organizational investments and processes in developing intellectual capital, the expertise of employees, and all the effort of knowledge contained within the organization. Intellectual capital presents structural capital including the nonphysical infrastructure, processes, databases, and information technology platforms of the organization. Intellectual capital enables other capitals including operational, financial, and HC to function effectively. Structural capital consists of policies, processes, patents, and trademarks, as well as the organization’s image, information infrastructure, proprietary software and databases, information technology platforms and innovation, and research and developments.

The business recovery and transformation are essential strategic planning for coping with growing challenges caused by the COVID-19 pandemic. Executives and management team of business organizations under the oversight of the board of directors should consider all possibilities and scenarios under which an organization can survive, recover, and continue sustainable performance by utilizing existing information technology. Business risk assessment and supply chain management can play important roles in the recovery process. Many business organizations have made significant modifications and adjustments to business operations and practices by using intellectual capita and information technology in response to challenges brought on by the COVID-19 pandemic. These organizations are also making changes to their communication, reporting, and control systems using their intellectual capital and information technology and virtual platforms. The finance function is in a better position to evaluate the available instinctual capital and virtual platforms and make suggestion for their adoptions.

Conclusion

Management has traditionally provided stewardship of an organization’s resources and its capitals in making strategic decisions that protect interests of all stakeholders. Management as the steward of all business capitals should focus on the long-term interests and well-being of multistakeholders is relevant and applicable to corporate governance in the post-COVID-19 era as business organizations are more concerned about safety, health, and well-being of their employees, customers, suppliers, and other stakeholders. Management, as the steward of business resources and related capital discussed in this chapter, has the primary role for improving sustainability performance and managing related risks, maximizing utilization of all capitals from strategic to financial, reputational, manufactured, human, social, and environmental in order to create shared value for all stakeholders. Stakeholder interests in a firm are equity capital, HC, social capital, and compliance capital. Thus, management acts as the steward of strategic capital, financial capital, HC, social capital, and environmental capital and acts as the active and long-term-oriented steward of all stakeholders including shareholders.

Chapter Takeaways

• Employ the stewardship theory with a keen focus on all capitals from strategic to financial, reputational, manufactured, social, environmental, and human in creating accountability and stewardship for all capitals and stakeholders.

• Management, as the steward of business resources, has the primary role for improving sustainability performance and managing related risks, maximizing utilization of all capitals from strategic to financial, reputational, manufactured, human, social, and environmental in order to create shared value for all stakeholders.

• Any environmental initiatives pertaining to reducing pollution levels or saving energy costs may require huge upfront capital expenditures but in the long run will also reduce contingent and actual environmental liabilities.