9

Contract Costing

LEARNING OBJECTIVES

After studying this chapter you should be able to:

Know the meaning of contract costing.

Understand the features of contract costing.

Understand the contract-costing procedure.

Explain the types of contracts.

Ascertain the profits on incomplete contracts.

Understand the terms: certification of work, retention money, cost-plus contract, paid costing, cost esclation and final claim.

Compute cost and profit of contracts.

Explain the meaning of important key terms.

We have discussed in the previous chapter the specific-order costing, that is, job costing and batch costing. In this chapter, we are going to discuss “contract costing”, which is also a special form of job costing.

9.1 MEANING AND DEFINITION OF CONTRACT COSTING

The terminology of CIMA defines contract cost as, “the aggregated costs relative to a single contract designated a cost unit” Further, it defines contract costing as, “that form of specific-order costing which applies where work is undertaken to customer’s special requirements and each order is of long-term duration (compared with those to which job costing applies). The work is usually constructional and in general the method is similar to job costing”. From this definition, we can understand that contract costing is essentially a form of job costing. The cost of each contract is calculated separately. The work mainly involves a constructional activity. They are of a long duration.

9.2 SPECIAL FEATURES OF CONTRACT COSTING

- Activity: In contract, the work mainly involved is construction activity.

- Site: The work is carried out at the customer’s site, away from the factory premises.

- Duration: Contract work is generally of a long duration extending beyond an accounting period.

- Risk: It involves risk and uncertainty.

- Meet requirements of customers: Contract work is done as per the tastes and requirements of customers.

- Accounting contract: Like job costing, a job-order member is assigned to each contract. Costs are accumulated and ascertained for each contract.

- Identifiable: In contract costing, it is possible to identify each contract from the start to the finish.

9.3 CONTRACT-COSTING PROCEDURE

Just like job costing, the cost of each contract has to be ascertained separately. Treatment of items of expenses in contract accounts is explained in detail as follows (otherwise, steps in contract-costing procedure):

Step 1: Separate Number: Each contract is assigned a separate job number.

Step 2: Separate Account: A separate contract is to be opened and maintained for each contract.

Step 3: Charging Costs: All costs with respect to a particular contract are charged to respective contract accounts.

Step 4: Collection of Costs.

9.3.1 Accounting for Material

- Materials which are sent to site are charged to a particular contract account on the basis of material requisitions

- Purchases of material for a particular contract are charged to the respective contract account based on the invoices

- The transfer of materials from one contract site to another site is credited to the transferor’s contract account and charged to the transferee’s contract account based on the material transfer note

- The returns of material to stores are credited to the contract account on the basis of material return note

- At the end of the accounting period, the stock is valued and credited to the contract accounts

- While the amount is realized from the sale of defective items, the surplus is credited to the contract account

- Unused materials after the completion of contract is valued and credited to the contract account

- Wherever the contractee himself has supplied the materials for the contract, it is not charged to the contract account

9.3.2 Accounting for Labour

- All labourers whoever have worked at the site should be considered as direct labour and charged to the contract account

- The salary of supervisors and other staff, who spent their whole-time attention to a contract, should be charged to contract account

- In some cases, the wages of labour or supervisory or any other staff which cannot be identified with a particular contract will be apportioned among all the contracts on a suitable basis

- Where the contract comprises several sections and is required to ascertain the labour cost of each section, each worker should be given a job card and there should be accurate time-keeping records too.

- In case a number of contracts are in execution, then a separate wage sheet for each contract may be maintained.

- Or, at times, the whole of wages paid will be recorded on a “Wages Abstract” as follows:

9.3.3 Accounting for the Use of Plant

- The plant purchased for the specific use of a contract is to be charged to the contract account.

At the end of each accounting period, the written-down value of the plant is credited to the contract account.

The difference between these represents the cost or the value for the use of plant.

- Another approach is to debit the depreciation charge to the contract account.

- Where the plant is taken on hire, the hire charges are debited to contract account.

9.3.4 Accounting for Overheads

- Generally, the major portion of the expenses is specific and direct

- In case the numbers of contracts are more, the contractor may have a common office, common supervisory staff, and so on, and such common expenses incurred are to be apportioned to different contracts on a suitable basis

9.3.5 Accounting for Sub-Contracts

The contractors, at times, entrust some part of the work to petty contractors at a predetermined, agreed rates. Payments to such sub-contractors are charged to respective contract accounts.

9.4 TYPES OF CONTRACTS

Contracts are classified into:

- Fixed-price contract with escalation clause

- Cost-plus contract.

9.4.1 Fixed-Price Contract with Escalation Clause

Contracts of some nature extend over a long period, covering more than a few accounting periods. During such a lengthy period, there may be changes in the prices of materials, labour, and so on. At the time of acceptance of a contract, such factors have to be foreseen and estimated properly. If such factors are not taken into account, then the contractor may not be able to attain the profit target; and on account of this, even the work may come to a standstill. In order to safeguard against this, a special clause known as “escalation clause” is incorporated in fixed-price contracts. Escalation clause is a provision in a contract which provides the formula to determine the amount of escalation, namely, the amount by which the contract price is to be modified when the prices of goods or services forming part of the contract change.

Contracts with escalation clause are beneficial to both contractor as well as the contractee in case of high rise in the prices of materials, labour or other services. It protects the contractor from cost increases. At the same time, the customer is freed from paying more amounts unnecessarily. All future deliveries are governed by this clause.

9.4.2 Cost-Plus Contracts

Under this type of contract, the contractee agrees to pay the contractor the contract price plus an agreed percentage above the contract price or a fixed fee. Cost-plus contracts are generally used in Government only.

- Where the estimates cannot be made or predetermined, this is suitable.

- If the service is innovative and no precedent is available, then cost-plus contracts may fit.

9.4.2.1 Guidelines to be Followed in Cost-Plus Contracts

- Absorption-costing technique has to be employed

- Allocation and apportionment of expenses are to be based on the principles of equity

- The contract should contain clear-cut definitions of cost

- Depreciated charge of special equipments should be charged suitably

- Abnormal gains and losses should be excluded

- The method of pricing the issue of materials and the methods of labour remuneration should be agreed

- Predetermined rates should form a part of contract

- The “plus” factor should be included in the contract. It should be specified in an unambiguous manner

9.4.3 Advantages

- The contractor is assured of some extra amount, thereby getting a definite profit.

- The customer feels contended as he is charged at a reasonable fixed price to execute the work.

- The contractor is relieved of unnecessary and elaborate calculations as in the case of escalation-clause contracts

9.4.4 Disadvantages

- “Plus” factor is determined on the total cost. In order to attain more profit, the contractor is interested in increasing the cost. The customer gets affected.

- The customer is not in a clear-cut position to know exactly the cost of work till it gets completed.

9.4.5 Incomplete Contracts and Profit

As already stated, contracts may extend beyond an accounting period. In practice, it may be found that only a certain portion of the contract has been completed and the remaining is under progress. It may take time to complete. So, proper care should be taken while ascertaining the profits for the completed as well as the incomplete work. There is no problem in crediting the profit on the completed work to profit and loss account (P&L A/c). But the real difficulty arises in assessing the profit for the contracts who are still under progress.

9.5 GUIDELINES TO ASSESS PROFIT ON INCOMPLETE CONTRACTS

Standard costing principles should be adopted for the recognition of profit for each period. In case of incomplete contracts, only a certain portion of the profit can be taken to P&L A/c based on the work completed. The firm must provide for the unforeseen losses and contingencies. The following are the general guidelines that may be followed for the assessment of profit on incomplete contracts:

- Profit should be completed on the basis of “work certified”

- Uncertified work should be valued at

- In case the value of work certified is less than 25% or 1/4th of the contract price, then no profit has to be taken into consideration. The entire profit has to be kept as a reserve for meeting the contingencies.

- In case the value of work certified is >25% but < 50% of the contract price, [>1/4th bus <1/2]

Formula:

- 1/3 of profit after adjusting the percentage of cash received from the customer (contractee) to be credited to P&L A/c

- Balance amount of profit is kept as a reserve

- In case the value of work certified is ≥50% of the contract price, [≥1/2]

Formula:

- 2/3 of profit after adjusting the percentage of cash received from the customer to be credited to P&L A/c

- Balance amount of profit is kept as a reserve

- In case the contract is nearing completion <100% of the contract price:

Formula:

- Estimate the total cost of completing contract and then calculate the estimated profit

- Estimate the profit after adjusting for percentage of cash received and percentage of work certified

- Profit remaining as the reserve is shown as a deduction from the work-in-progress (WIP) on the Assets side of the Balance Sheet.

- In case there is any LOSS, the entire amount of loss should be debited to P&L A/c.

- As per A S-7 (Revised), Accounting for construction contracts, a foreseeable loss on the entire contract should be provided for in the financial statements irrespective of the amount of work done and the method of accounting followed.

- The journal entry for transfer of profit to P&L A/c and WIP for unrealized profit is as:

Contract A/c (With total profit) Dr …

To P&L A/c (with profit transferred)……

To WIP A/c (with profit kept as reserve)…

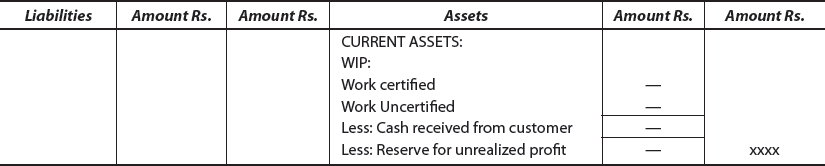

9.6 WORK-IN-PROGRESS

In contract accounts, the value of work-in-progress consists of the following two items:

- Work Certified and

- Work Uncertified

These are shown on the Assets side of the Balance sheet under “Current Assets” as depicted in the following:

Certification of work and “Retention Money”

- In case of large contracts, work should not have been completed; however, payments would be made to the contractors for the work done.

- As such, at the end of an accounting period, the customer agrees to pay a part of contract price depending on the progress of the work.

- This progress of work is to be assessed by the customer’s architect or engineer or surveyor, who after assessing will issue a certificate, which is termed as the work certified.

- This certificate contains the value of work done as on the date of assessment.

- Based on the value shown in “work certified”, the customer (Contractee) pays the amount to the contractor.

- But, the customer will not pay the entire amount of the value of work certified. Generally, 70% to 80 % will be paid, as per the terms of the contract.

- The balance (remaining 20% to 30% of the value of work certified) not paid is termed as the “Retention Money ”.

9.7 ACCOUNTING TREATMENT

Although there are two approaches to deal with the value of the work certified and the consequent payment, the most common approach is as follows:

- A memorandum of work certified is maintained.

- The cash received from the contractee is credited to his personal account.

- The value of work is debited to WIP account and credited to the contract account.

- The WIP is shown as an asset in the Balance Sheet after deducting the amount received from the contractee.

- On the completion of the contract, the contractee’s personal account is debited and the contract account is credited.

- Accordingly, the journal entries will be as follows:

- For the value of work certified:

WIP Dr

To Contract A/c.

- For the cash received from the contractee:

Bank A/c Dr

To Contractee’s A/c.

Work Uncertified:

- That part of work of the contract which has not been assessed by the contractee’s surveyor is known as “Work Uncertified”.

- This is valued at cost.

- This value is credited to the contract account and debited to WIP A/c.

- This will be transferred to the debit of contract account in the beginning of the next accounting period.

Simple Problems (Basic)

Illustration 9.1

1. Model: Simple Finished Contracts

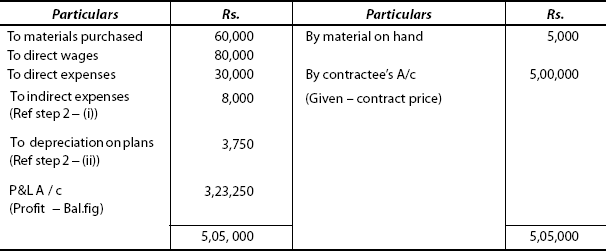

The following are the expenses of Renu & Co in respect of a contract which commenced on 1 April 2009.

| Rs. | |

|---|---|

Materials Purchased |

60,000 |

Materials on hand |

5,000 |

Direct wages |

80,000 |

Plant issued |

50,000 |

Direct expenses |

30,000 |

The contract price was Rs. 5,00,000 and the same was duly received when the contract was completed in December 2009. The charge indirect expenses at 10% on direct wages provide a 10% depreciation on the plant per annum.

You are required to prepare the contract A/c and the Contractee’s A/c.

Solution

Step 1 Open a Contract A/c (Ledger).

Step 2 Debit all the expenses (Expenses are to be entered on the debit side of the contract A/c)

Basic calculation:

- Indirect expenses: 10% on direct wages

= 10% of Rs. 80,000.

= 10/100 × 80,000 = Rs. 8,000.

- Depreciation = 10% p.a. on Plant

= April to December = 9 months.

= 10/100 × 9/12 × 50,000 = Rs. 3,750.

Step 3 Credit the contract price and materials on hand (These items are to be entered on the credit side of the A/c).

Step 4 Balance the figures. The balancing figure is profit or loss depending on the problem.

Step 5 Open a Contractee’s A/c. The contractor price is entered as ‘To Contract A/c’ on the debit side and “By Bank” on the credit side.

Illustration 9.2

Model 2: Treatment of Plant

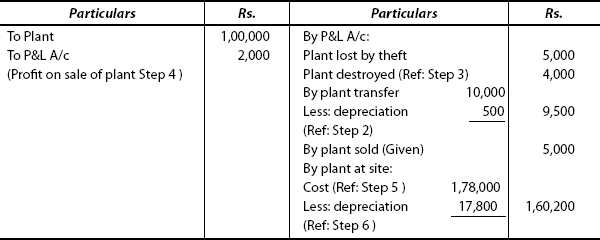

2. From the following information, you are required to show the treatment of plant in contract A/c:

- Plant issued to contract on 1 January 2009 – Rs. 1,00,000

- The plant costing Rs. 10,000 was transferred to another contract on 30 June 2009

- A plant costing Rs. 5,000 was stolen in transit and another costing Rs. 4,000 was destroyed by fire

- A plant costing Rs. 3,000 was sold for Rs. 5,000

- The plant at the end of December was valued by charging depreciation at 10 % per annum

Solution

Step 1: Plant issued is to be debited to contract A/c.

Step 2: Plant costing Rs. 10,000 that was transferred to another contract is to be credited to contract A/c after providing depreciation as follows:

Plant transferred: Rs. 10,000. |

|

Less: depreaction @ 10% p.a. |

|

|

= |

|

= Rs. 500. |

Step 3: Plant stolen and destroyed are to be transferred to be P & L A/c and credited to contract A/c at Rs. 5,000 + Rs. 4,000.

Step 4: Plant sold at Rs. 5,000 is credited to contract A/c. Its cost is Rs. 3,000 but sold for Rs. 5,000. So, there is a profit of Rs. 2,000 (Rs. 5,000 – Rs. 3,000). This profit on the sale of the plant is transferred to P&L A/c and debited to contract A/c.

Step 5: Plant at site is to be shown as follows:

Cost of plant at the end |

= |

Rs. 2,00,000 − Rs. 5,000 (stolen) |

|

|

−Rs. 4,000 (destroyed)− |

|

|

Rs. 10,000 (Transferred) − |

|

|

Rs. 3,000 (Plant sold) |

|

= |

Rs. 1, 78,000. |

Step 6: depreciation per annum @ 10% has to be provided =17,800

(Assume that the plant was stolen and destroyed at the beginning. If date is given, then depreciation for the respective period has to be calculated.)

Step 7: Preparation of contract A/c:

Illustration 9.3

Model 3: Transfer of profit: Unfinished contract

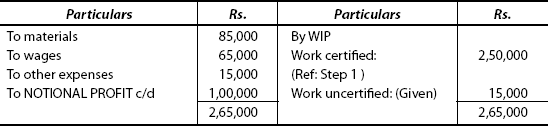

3. The following expenses were incurred on an unfinished contract during the year 2009:

Materials |

85,000 |

Wages |

65,000 |

Other expenses 15,000 |

|

Rs. 2,00,000 was received from the contractee, being 80%of the work certified. Work done but not certified was Rs. 15,000. Determine the profit to be credited to P&L A/c in the alternatives given as follows:

- Contract price is Rs. 15,00,000.

- Contract price is Rs. 6,00,000.

- Contract price is Rs. 3,25,000.

Solution

Step 1: Calculation of work—certified:

Method I:

80% work certified |

= |

Rs. 2, 00,000 |

100% work certified |

= |

? |

|

|

|

(Or) |

= |

Rs. 2,50,000. |

Method II: Cash received = 80%of work certified

If cash received is 80, then the work certified = 100

If cash received is Rs. 2, 00,000, then the work certified ![]()

NOTE: Any method may be adopted.

Step 2: Preparation of contract A/c

Step 3: This is the crucial step.

The ratio of work certified to total contract price has to be calculated.

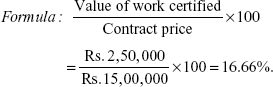

Percentage (Ratio) for case (a): Contract Price: Rs. 15,00,000.

That is, work certified is less than 25%.

Important Note

If the work certified is less than 25% (or 1/4th)—No profit should be taken to P&L A/c as per the principles that are to be adopted in dealing with an incomplete contract.

Hence, in this case (a), no profit is taken to P&L A/c.

∴ the entire notional profit of Rs. 1, 00,000 is kept in Reserve.

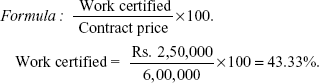

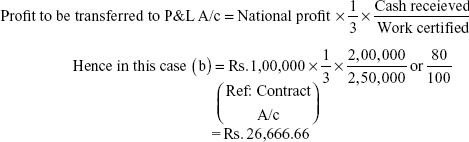

Step 4: Case (b) Contract price – Rs. 6,00,000.

Important Note

If the work certified is less than 50% but mote than 25%, then the profit to be transferred is to be ascertained by applying the formula:

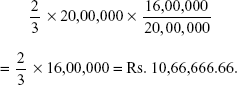

Profit to be credited to P&L A/c = Rs. 26,666.66.

Balance amount from profit = Rs. 1,00,000 – Rs. 26,666.66

= 73,333.34 which is to be kept as Reserve.

Step 5: Case (c) Contract price is Rs. 3, 25,000.

Important Note

If the work certified is more than 50% of the contract price, then the profit to be credited is determined by applying the formula:

Profit to be credited to P&L A/c = Rs. 53,333.33

Balance to be kept as reserve = Rs.1,00,000 – Rs. 53,333.33

= Rs. 46,666.67.

Illustration 9. 4

Model: 4 Computation of work uncertified

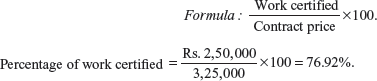

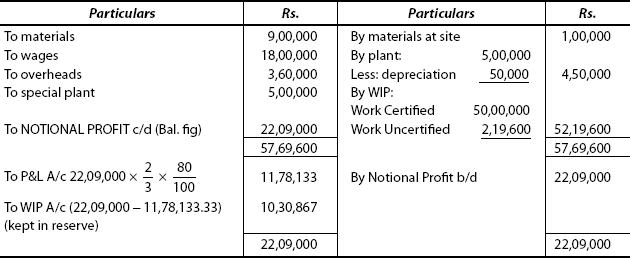

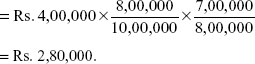

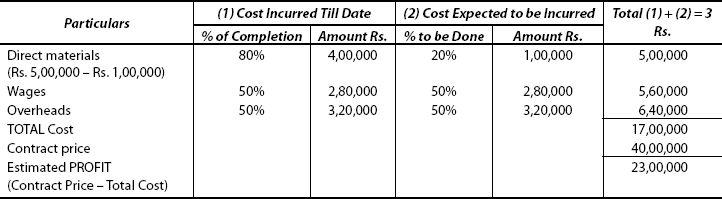

4. Vasanth Construction Co. has undertaken a contract for construction of a Conference Hall in a Star Hotel for a total value of Rs. 72 lakhs on 1 January 2009. It was estimated that the contract would be completed by 30 June 2010. You are required to prepare a contract A/c for the year ending 31 December 2009 from the following information:

| Rs. | |

|---|---|

Wages |

18,00,000 |

Materials |

9,00,000 |

Materials at site (on 31 December 2009) |

1,00,000 |

Special plant |

5,00,000 |

Overheads |

3,60,000 |

Work certified |

50,00,000 |

Depreciation at 10% per annum on the plant.

Cash received is 80% of the work certified, 10% of the value of materials issued, and 6% of the wages that may be taken to have been incurred for the portion of the work completed but not yet certified. Overheads that are charged as percentage of direct wages have been incurred for the portion of work completed but not yet certified. Overheads are charged as percentage of direct wages.

Solution

Step 1: Value of uncertified work is to be ascertained, which is added to work certified and shown as WIP on the credit side of the contract A/c in order to determine Notional Profit Expenses incurred:

| Rs. | |

|---|---|

(i) Materials – 10% of materials to be included in the completed work 10% of Rs. 9,00,000 |

90,000 |

(ii) Wages – 6% of wages – to be taken into account.6% of Rs.18,00,000 |

1,08,000 |

(iii) Overheads as percentage of direct wages: |

21,600 |

(iv) Work uncertified: (Add i + ii + iii) |

2,19,600 |

Step 2: As work certified is more than 50 % of the contract price, the formula to transfer Notional Profit to P&L A/c has to be applied

Step 3: |

Depreciation has to be found out: |

|

|

Plant: |

Rs. 5,00,000 |

Less: |

Depreciation @ 10%: 50,000 |

50,000 |

|

|

Rs. 4,50,000 |

Step 4: Preparation of contract A/c:

Illustration 9.5

Model 5: Estimated Profit & Transfer to P&L A/c

(Contract is nearing completion)

5. The expenditure on a contract till 31 March 2010 was Rs. 5,00,000 and the work certified was Rs. 8,00,000. The contract price is Rs. 10,00,000 and the contractee has paid Rs. 7,00,000 till 31.3.2010. The cost of work done but not certified on that date amounted to Rs. 1,00,000.

It is estimated that the contract will take a further period of 3 months to complete and will necessitate an additional expenditure of Rs. 1,00,000.

You are required to ascertain the amount to be credited to P&L A/c on 31 March 2010. Also state the different amounts of profit that may reasonably be credited to the P&L A/c.

Solution

STAGE I: First, the notional profit is to be determined by preparing the contract A/c as follows:

Step 1: As expenditure to complete the contract is given in the question and as the contract is nearing completion too, the estimated profit has to be determined as follows:

| Rs. | |

|---|---|

(i) Total cost of contract |

5,00,000 |

Add:(ii) Additional estimated expenditure to complete contract |

1,00,000 |

(iii) Estimated total cost of contract (i) + (ii) |

6,00,000 |

(iv) Contract price (given) |

1,00,000 |

(v) Estimated profit step(iv) – step(iii) |

4,00,000 |

Step 2: This estimated profit of Rs. 4,00,000 may be credited to P&L A/c by any one of the following ways:

Approach I: Formula: ![]()

Substituting the values in the above formula, we get:

Rs.3,20,000 is to be transferred to P&L A/c and the balance (Rs. 4,00,000 – Rs. 3,20,000) Rs. 80,000 has to be kept in reserve.

Approach II: Formula to transfer part of estimated profit to P&L A/c is:

Substituting the values in the above formula, we get:

Rs.2,80,000 is to be credited to P&L A/c and the balance (Rs. 4,00,000 – Rs. 2,80,000) Rs.1,20,000 has to be kept in reserve.

Approach III: Formula: ![]()

Substituting the values in the above formula, we get:

Rs. 3,33,333.33 is to be credited to P&L A/c and the balance (Rs. 4,00,000 – Rs. 3,33,333,33) Rs. 66,666.67 is to be kept in reserve.

Approach IV: Formula: ![]()

Substituting the values in the above formula, we get:

The balance (Rs. 4,00,000 – Rs. 2,91,666.67) Rs.1,08,333.33 is to be kept in reserve.

Illustration 9.6

Model: Computation of Profit & WIP

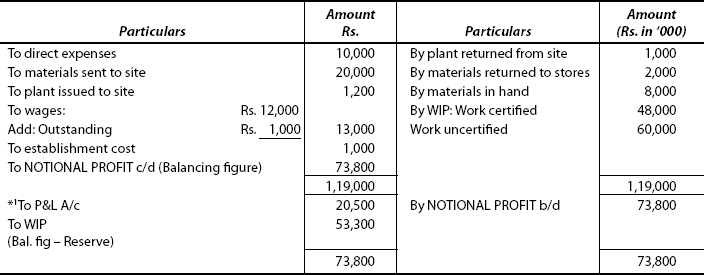

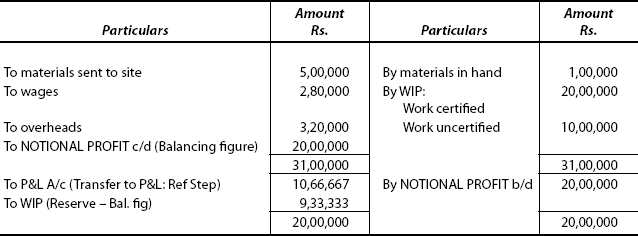

BMR & Co. Ltd, a contractor, is currently engaged in the construction of a Mall in one of the Metros. From the following information as on 31 December 2009, you are required to calculate:

- Cost of WIP at the year end,

- Profit to be transferred to P&L A/c

| Rs. in ‘000 | |

|---|---|

Direct expenses |

10,000 |

Materials sent to site for construction |

20,000 |

Plant issued to site |

1,200 |

Plant returned from site |

1,000 |

Materials returned to stores |

2,000 |

Labour working in site |

12,000 |

Material remaining in site |

8,000 |

Outstanding wages |

1,000 |

Uncertified work |

48,000 |

Certified work |

60,000 |

Cash received |

50,000 |

Establishment cost |

1,000 |

Contract price |

1,30,000 |

Solution

Prepare the contract account first as follows:

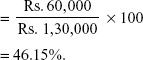

*1 Stage of completion of work is calculated as:

Step 1: Formula: ![]()

Step 2: Substituting the values in the formula we get,

Step 3: This is >25% but <50%.The formula to ascertain profit to be credited to P&L A/c is

Step 4: Substitute the values, we get:

Step 5: Rs. 20,500 is to be transferred to P&L A/c.

Step 6: Balance (Rs. 73,800 – Rs. 20,500) = Rs. 53,300 is to be transferred to WIP (Reserve).

II: Calculation of WIP as on 31 December 2009:

| Rs. in ‘000 | |

|---|---|

Step 1: Work certified |

60,000 |

Step 2: Work uncertified |

48,000 |

Step 3: Add (Step 1+Step 2) |

108,000 |

Step 4: Less: Provision (Ref: Contract A/c: WIP) |

53,300 |

|

54,700 |

|

50,000 |

Step 5: Less: Cash received 5 |

50,000 |

Step 6: WIP at the end of the year |

4,700 |

Illustration 9.7

Model: Estimated Profit on Completion of Contract

VRS Ltd is engaged in construction of a Flyover Project in Chennai. From the following information as on 31 March 2010 you are required to calculate:

- Profit to be transferred to P&L A/c (i.e., estimated profit to date on the contract)

- Estimated profit on completion of the contract

- Cost of the WIP at the year end.

Contract price |

Rs.40,00,000 |

Work certified |

Rs.20,00,000 |

Uncertified work |

Rs.10,00,000 |

Surveyor’s estimation of work completed:

Direct labour |

50% |

Direct materials |

80% |

Overheads |

50% |

Materials sent to site |

Rs.5,00,000 |

Labour |

Rs.2,80,000 |

Overhead |

Rs.3,20,000 |

Materials in hand |

Rs.1,00,000 |

Solution

(Based on the estimate of the work completed)

(a)

1. Calculation of profit transferred to P&L A/c:

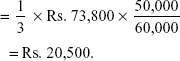

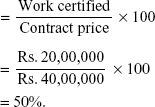

Step 1: The stage of completion is computed by using the following formula:

Step 2: Work has reasonably advanced to 50%.Formula to ascertain the profit to be credited to P&L A/c is:

Step 3: Substituting the values we get:

Step 4: WIP:

Balance (Rs. 20,00,000 – Rs. 10,66,667) = Rs. 9,33,333.33.

(b) Estimated profit on the completion of contract is to be computed

(c) Calculation of WIP as on 31 March 2010

| Rs. | |

|---|---|

Step 1: Work certified |

20,00,000 |

Step 2: Uncertified Work |

10,00,000 |

Step 3: Add (Step 1 + Step 2) |

30,00,000 |

Step 4: Less: Provision (Ref: Contract A/c:) |

9,33,333 |

|

20,66,667 |

Step 5: Less: Cash received |

16,00,000 |

Step 6: W.I.P. at the end of the year |

4,66,667 |

Illustration 9.8

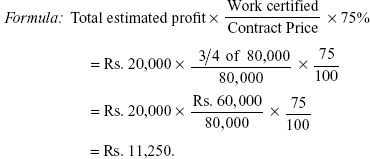

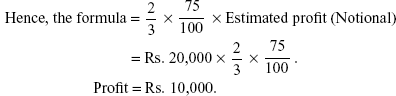

Model: Calculation of Profit

The total contract price of a contract is Rs. 80,000. Three-fourth of the work has been approved by the contractee. The costs incurred so far for the contract are Rs. 40,000.It is estimated that Rs. 20,000 will be required further to complete the contract. The contractee pays 75% of the work certified by him.

- You are required to calculate the profit to be credited to P&L A/c

- Calculate the profit if the estimated further costs are not given in the question

Solution

|

|

Rs. |

(a) Step 1: Contact price |

|

80,000 |

Step 2: Less: Total estimated costs |

Rs. |

|

(i) Costs incurred: |

40,000 |

|

(ii) Costs estimated to be incurred: |

20,000 |

60,000 |

Step 3: Total estimated profit (Step 1 – Step 2) |

|

20,000 |

Step 4: Profit to be credited to P&L A/c: |

|

|

(b) It the estimated further costs are not given:

-

Profit

=

Value of work certified – cost of work certified

=

Rs. 60,000 (3/4 of Rs. 80,000) − Rs. 40,000 (cost incurred)

=

Rs. 20,000.

- As work has been completed 3/4th, that is, 75%, this is>50%.

Illustration 9.9

Model: Profit on Contract

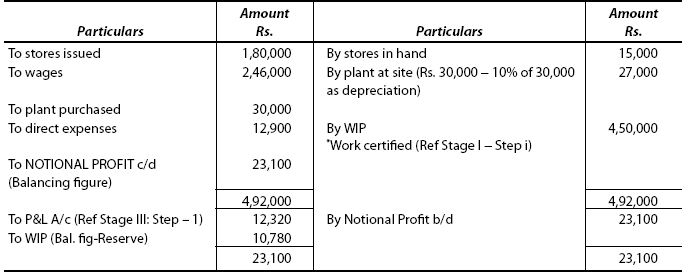

Vijay & Co. obtained a contract for the construction of a residential building of Rs. 9,00,000.Building operations are started on 1 April 2009 and at the end of the financial year, that is, 31 March 2010, they received from the party a sum of Rs. 3,60,000 being 80% of the amount of the surveyor’s certificate. The following additional information is available:

| Rs. | |

|---|---|

Stores issued to contract |

1,80,000 |

Stores on hand as on 31 March 2010 |

15,000 |

Wages paid |

2,46,000 |

Plant purchased for the contract |

30,000 |

Direct expenses |

12,900 |

Plant to be depreciated @ 10% |

|

You are required to prepare an account showing profit on contract up to 31 March 2010. Also discuss whether Vijay & Co. would be justified in taking the full amount of this profit to the credit of their P&L A/c.

Solution

STAGE I: (i) First, the work certified is calculated as follows:

Cash received by the contractor = Rs.3,60,000

This is 80%of the Surveyor’s Certificate.

80%of the work certified = Rs.3,60,000

100% of the work certified |

= |

x (assumption) |

80% × x |

= |

100% × Rs. 3,60,000 |

|

|

|

|

= |

Rs. 4,50,000. |

∴ Value of work certified |

= |

Rs. 4,50,000. |

(ii) Contract work has not been completed but has been advanced reasonably, that is, 50% ![]() . Hence, the company is not entitled to credit the entire amount to P&L A/c. The formula to be used is

. Hence, the company is not entitled to credit the entire amount to P&L A/c. The formula to be used is

STAGE II: Preparation of Contract Account

STAGE III: Profit to be transferred to P&L A/c

Step 1: Write the formula to Compute Profit. (The work has been advanced to 50%.)

Model: Retention Money & Normal Loss of Materials

Illustration 9.10

A public works contractor secured a contract at a price of Rs. 10,00,000. The work began on 1 July 2009 and the contract ledger showed the following items debited up to 31 March 2010:

| Rs. | |

|---|---|

Materials |

1,80,000 |

Wages |

2,10,000 |

Direct charges |

10,000 |

Plant |

32,000 |

The measurement on March 31 reads as follows:

| Rs. | ||

|---|---|---|

Total work done certified till date |

|

4,80,000 |

Total work done as per last measurement |

|

4,20,000 |

Total work done for the month |

|

60,000 |

Less: Retention Money@ 10% |

|

6,000 |

|

|

54,000 |

Materials returned to stores |

Rs. |

|

Materials on site: |

10,000 |

|

Less: 20% |

2,000 |

8,000 |

Amount payable |

|

62,000 |

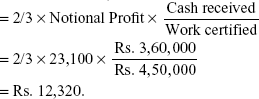

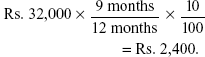

You are required to prepare a proforma account for the contract showing the profit earned till date, and indicate by means of a note on the basis of which you arrive at the amount which might be credited to P&L A/c. Allow for a depreciation on the plant @ 10% per annum.

Solution

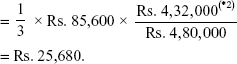

Basic calculations:

*1(i) Depreciation on the plant:

*2(ii) Cash received: Work certified –Retention money

= Rs. 4,80,000 − (10% of 4,80,000) 48,000

= Rs. 4,32,000.

STAGE III: Calculation of profit to be transferred to P&L A/c:

Step 1: Stage of completion of work is calculated as follows:

Formula: ![]()

Substituting the values, we get:

Step 2: As the value of work is less than 50%, the formula to be used for crediting profit to P&L A/c is:

Substituting the values we get,

Step 3: Amount of profit to be transferred to P&L A/c is Rs. 25,680.

Step 4: Balance of notional profit, that is, Rs. 85,600 – Rs. 25,680 = Rs. 59,920 is to be transferred to WIP and kept as a reserve to meet the contingencies.

Illustration 9.11

Model: Balance Sheet Entries

A company undertook a contract for construction of large housing apartments. The construction work commenced on 1 January 2009 and the following data are available for the year that ended on 31 December 2009.

| Rs.(in ‘000) | |

|---|---|

Contract price |

70,000 |

Work certified |

40,000 |

Progress payments received |

30,000 |

Materials issued to site |

15,000 |

Planning and estimate costs |

2,000 |

Direct wages paid |

8,000 |

Materials returned from site |

500 |

Plant hire charges |

3,500 |

Wage-related costs |

1,000 |

Site-office costs |

1,356 |

Head-office expenses apportioned |

750 |

Direct expenses |

1,804 |

Work uncertified |

298 |

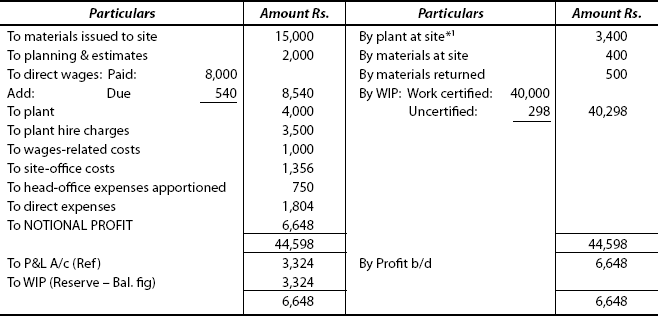

The contractors own a plant which originally cost Rs. 40 lakhs and it has been continuously in use in this contract throughout the year. The residual value of the plant after 5 years of life is expected to be Rs.10 lakhs. Straight Line Method of depreciation is in use.

As on 31 December 2009, the direct wage that is due and payable amounted to Rs.5,40,000 and the materials at site were estimated at Rs.4,00,000.

- Prepare the contract account for the year ended 31 December 2009

- Show the calculation of profit to be taken to P&L A/c of the year

- Show the relevant balance-sheet entries

Solution

Basic calculations:

∴ Plant at site = Rs.40,00,000 – Rs.6,00,000 = Rs.34,00,000.

*1NOTE:

- Plant at cost (Rs.40 lakhs) is directly debited to contract A/c.

- Plant at cost (after deducting depreciation as shown above) is to be credited to contract A/c.

- Plant hire charges—a separate item—are to be debited to contract A/c.

Students should thoroughly understand these steps (of the plant), while preparing the contract Account.

- Wages:

Wages paid: Rs.80,00,000

Add: Due as on 31 December 2009: Rs.5,40,000

Rs.85,40,000 = or Rs.8,540 (in’000)

Now, contract Account is to be prepared as follows:

STAGE II: Calculation of profit to be undertaken to P&L A/c

Step 1: Stage of completion of work ![]()

Substituting the values, we get:

Step 2: As the work has reached an advanced level,

i.e., >50%, the formula used is:

Substituting the values,

Hence, the amount to be transferred to P&L A/c = Rs.3,324

Step 3: The balance (Rs.6,628 – Rs.3,324) = Rs.3,324 is to be transferred to WIP, to be kept as a reserve to meet the contingencies.

STAGE III: Extracts from Balance Sheet is to be shown as follows:

Illustration 9.12

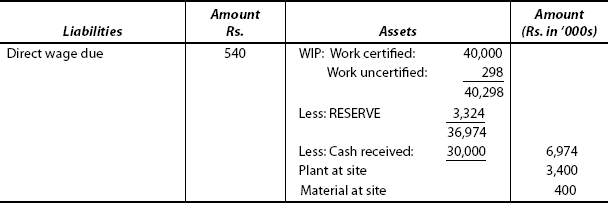

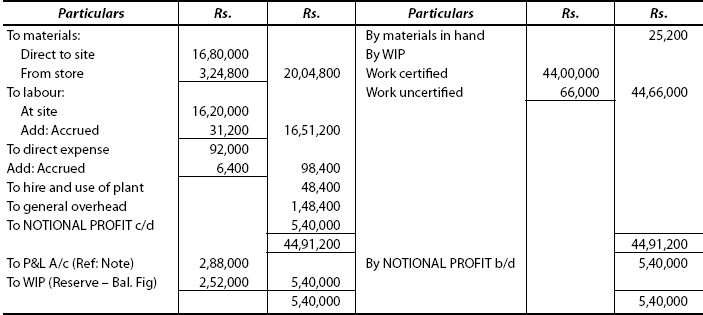

Model: Contractee Account Retention of % for a specified period

XL & Co. Ltd has undertaken the construction of a bridge over the River Cauvery for Trichy Municipal Corporation. The value of the contract is Rs. 50,00,000 subject to a retention of 20% until one year after the certified completion of the contract and the final approval of the Corporation engineer. The following are the details as shown in the books on 31 December 2009:

| Rs. | |

|---|---|

Labour on site |

16,20,000 |

Materials direct to site Less returns |

16,80,000 |

Materials from store |

3,24,800 |

Hire and use of plant—plant upkeep Account |

48,400 |

Direct expenses |

92,000 |

General overhead allocated to the contract |

1,48,400 |

Materials in hand on 30 June 2009 |

25,200 |

Wages accrued on 30 June 2009 |

31,200 |

Direct expenses accrued on 30 June 2009 |

6,400 |

Work not yet certified at cost |

66,000 |

Amount certified by the Corporation engineer |

44,00,000 |

Cash received on account |

35,20,000 |

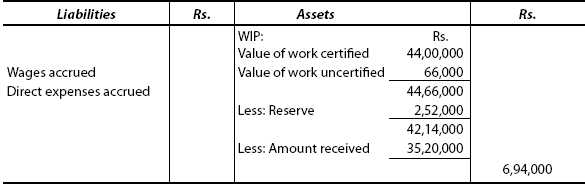

You are required to prepare

- Contract account

- Contractee’s account and

- Show how the relevant items would appear in the Balance Sheet

Solution

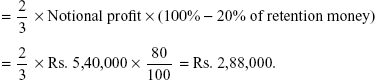

NOTE 1: Calculation of profit to be taken to P&L A/c: As values of work completed has reached the advance level, the formula that is to be used is as follows:

Balance (Rs. 5,40,000 – Rs. 2,88,000) = Rs.2,52,000 has to be transferred to WIP and kept as a reserve to meet the contingencies.

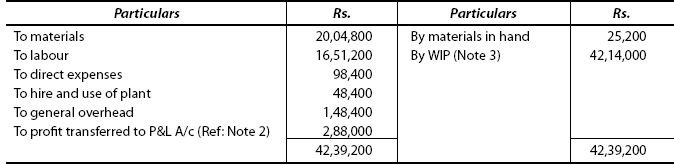

NOTE 2: Total profit made to date may be arrived at by another approach:

| Rs. | ||

|---|---|---|

Total expenditure on the contract: |

|

39,51,200 |

Less: Value of materials in hand |

|

25,200 |

|

|

39,26,000 |

Value of work certified = |

44,00,000 |

|

Value of work uncertified = |

66,000 |

44,66,000 |

Total profit to be made (difference) |

|

5,40,000 |

∴ Profit to be transferred: 2/3 × 5,40,000 × 80/100 |

|

Rs.2,88,000 |

Profit to be carried forward to reserve = |

|

Rs. 2,52,000 |

NOTE 3: Value of WIP:

| Rs. | |

|---|---|

Value of work certified: |

44,00,000 |

Value of work uncertified |

66,000 |

|

44,66,000 |

Less: Reserve (Note:2) |

2,52,000 |

|

42,14,000 |

Based on the Notes 2 & 3, and if it is desired that the contract work should show the value of WIP and only the amount of profit has to be taken to P&L A/c, then the contract account will vary accordingly and appears as follows:

Important Note

Now, the students may note the difference in the approaches of preparing contract A/c—if WIP is to be shown in the contract A/c, then this procedure has to be adopted. That is, from Note 2 to preparation of contract A/c, that is, this stage. Otherwise, students could follow the usual procedure up to Note-1 stage in this solution.

(b) Preparation of Contractee’s Account

(c) Items to be shown in the Balance Sheet

Illustration 9.13

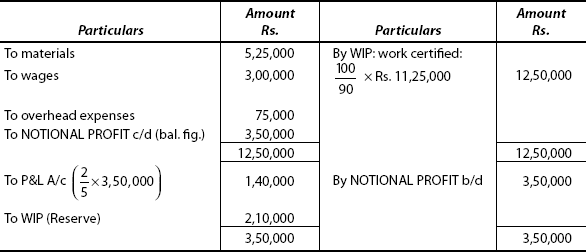

Model: Contract A/c & Contractee’s A/c for 2 years

RBS Ltd took up a construction work of a building at a contract price of 30,00,000. During the first year, the following amounts were spent as against a sum of Rs. 11,25,000 which represented 90% of the work certified and received by the contractor.

|

Rs. |

Materials |

5,25,000 |

Wages paid to workers |

3,00,000 |

Overhead expenses |

75,000 |

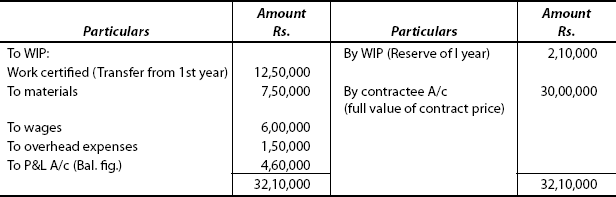

During the second year, the firm spent the following amounts:

|

Rs. |

Materials |

7,50,000 |

Labour cost |

6,00,000 |

Overhead expenses |

1,50,000 |

In the second year, the contract was completed and a sum of Rs.17,50,000 was received by the contractor. Prepare the contractor and contractee’s account for both the years and calculate the profit.

NOTE: Consider only 2/5th of the notional profit that is to be taken to the credit of the profit and loss in the first year, as the work done is less than 50%.

[I.C.W.A. Inter – Modified]

Solution

As specific instruction is given (in the illustration—i.e., Question), instead of 1/3rd in the usual procedure, 2/5th of the notional profit has to be considered for taking into P&L A/c.

(a) Contract Account for the first year.

(b) Contract Account for the second year

(c) Contractee’s Account at the end of the first year

(d) Contractee’s Account at the end of the Second year

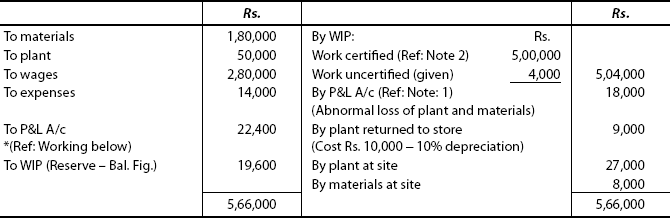

Illustration 9.14

Model: Plant & Materials loss

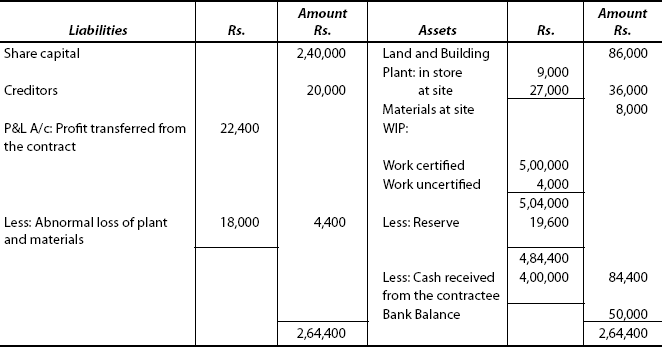

Vas Ltd. was engaged on a contract of which the contract price was Rs. 10,00,000, on 1 January 2009.

Of the plant and materials charged to the contract, the plant which costs Rs. 10,000 and materials which cost Rs. 8,000 were lost in an accident.

On 31 December 2009, the plant which costs Rs. 10,000 was returned to the store, the cost of work done but uncertified was Rs.4,000 and the materials costing Rs.8,000 were in hand on site.

Charge 10% depreciation on the plant, crediting two-thirds of profit received with P&L A/c and compile a contract Account and Balance sheet from the following:

| Rs. | Rs. | |

|---|---|---|

Share capital |

|

2,40,000 |

Creditors |

|

20,000 |

Cash received on contract – 80% of work certified |

|

4,00,000 |

Land and Building |

86,000 |

|

Bank balance |

50,000 |

|

Charged to contract: |

|

|

Materials |

1,80,000 |

|

Plant |

50,000 |

|

Wages |

2,80,000 |

|

Expenses |

|

14,000 |

|

6,60,000 |

6,60,000 |

Solution

- In this problem, plant and materials were given as lost in an accident. Total costs (for both, i.e., plant Rs.10,000 + materials Rs.8,000) of Rs.18,000 are treated as abnormal loss and charged to P&L A/c.

- 80% of work certified = Rs.4,00,000.

- As direction is given in the problem itself, 2/3 × Notional Profit × Work Certified formula has to be used.

*1 Profit to be transferred to P&L A/c

= ![]() × Notional Profit ×80%

× Notional Profit ×80%

= ![]() × Notional Profit ×80/100

× Notional Profit ×80/100

Balance (Rs.42,000 – Rs.22,400) Rs. 19,600 is to be transferred to WIP and kept as a reserve to meet contingencies.

Illustration 9.15

Model: Two Contracts & Material transfer from one to another

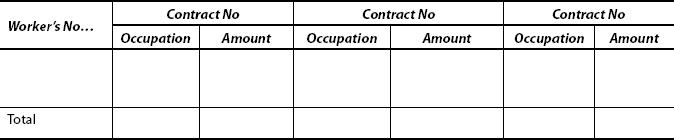

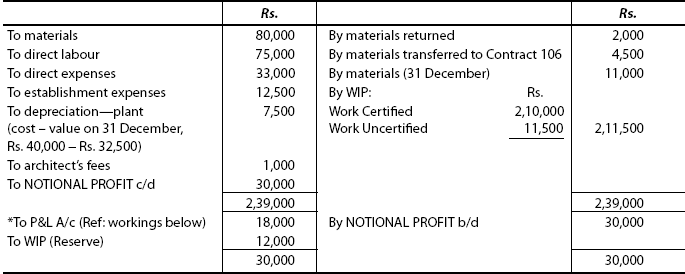

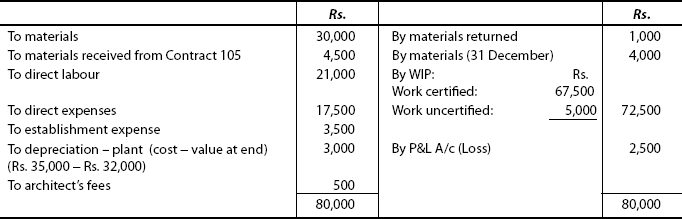

RR Construction Ltd is engaged on two contracts, Contract No, 105 and 106 during the year 2009. The following particulars are obtained at the end of the year 31 December 2009.

| Contract 105 Rs. | Contract 106 Rs. | |

|---|---|---|

Contract price |

3,00,000 |

2,50,000 |

Materials issued |

80,000 |

30,000 |

Materials returned |

2,000 |

1,000 |

Materials on site |

11,000 |

4,000 |

Direct labour |

75,000 |

21,000 |

Direct expenses |

33,000 |

17,500 |

Establishment expenses |

12,500 |

3,500 |

Plant installed at cost |

40,000 |

35,000 |

Value of plant (December 31) |

32,500 |

32,000 |

Cost of work not yet certified |

11,500 |

5,000 |

Value of work certified |

2,10,000 |

67,500 |

Cash received from contractees |

1,89,000 |

62,500 |

Architect’s fees |

1,000 |

500 |

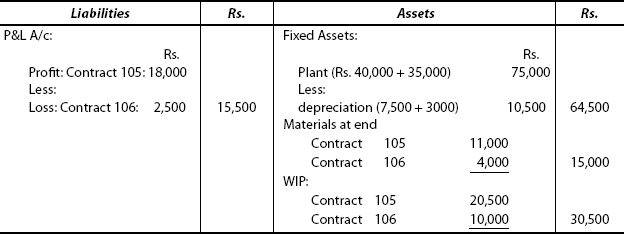

During the period, materials amounting to Rs. 4,500 have been transferred from Contract 105 to Contract 106. The date of commencement of Contract No.105 is 1 April and Contract No. 106 is1 September. You are required to show:

- Contract Accounts

- Contractee’s Accounts, and

- Extract from Balance Sheet as on 31 December, clearly showing the calculation of WIP.

[I.C.W.A. (Inter) – Modified]

Solution

- Contract Accounts are to be prepared separately, as in the manner in the previous illustrations.

- However, the values relating to contracts are to be shown in the Balance Sheet.

- Material transfer has to be dealt with cautiously.

1.

* Profit to be transferred to P&L A/c has been arrived at as: ![]()

Balance (Rs. 30,000 – Rs. 18,000): Rs. 12,000 is transferred to WIP.

1.

2.

2.

| (a) For Contract 105: | Rs. |

|---|---|

Work certified |

2,10,000 |

Work uncertified |

11,500 |

|

2,21,500 |

Less: Reserve |

12,000 |

|

2,09,500 |

Less: Cash received |

1,89,000 |

*1WIP for 105 = |

20,500 |

| (b) For Contract 106: | Rs. |

|---|---|

Work certified |

67,500 |

Work uncertified |

5,000 |

|

72,500 |

Less: cash received |

62,500 |

*2WIP for 106 = |

10,000 |

3. Extracts from Balance sheet as on 31 December 2009

FOR PROFESSIONAL COURSE

Recognition of Profits on Incomplete Contracts:

Accounting Standard (AS) – 7 – Revised 2002

The main principle envisaged in (AS) – 7 – Revised is explained as follows:

- The basic principle of ascertaining profits on incomplete contracts is to provide credit to share of profit on the outcome of a contract which can reasonably be foreseen.

- In computing the total estimated profit on the contract it is essential and unavoidable to take into account:

- Total costs incurred till date

- Total estimated future costs to complete the contract.

- The estimated future cost of rectification and guarantee work

- Any other future work to be undertaken

- These [Total Estimated Cost of Contract (i to iv above)] are then compared with the Total Contract Value to ascertain Estimated Profit/Loss on contract.

- It should be further noted that the profit taken in any year is to be calculated on a cumulative basis having regard to profit taken in the earlier years.

- The amount to be shown in the years P&L A/c will be the appropriate proportion of this total profit (with special reference to the work done to date) LESS any profit already taken in the previous year.

- Further (AS) – 7 dealing with “Construction Contracts” stipulates that when the outcome of a construction contract can be estimated reasonably, contract revenue and contract costs associated with the construction contract should be recognized as revenue and expense, respectively, by reference to the stage of completion of the contract activity at the reporting date.

- An expected loss on the construction should be recognized as an expense immediately.

- Profit or loss as estimated in the Memorandum Format is given as follows:

Particulars Rs. Rs. TOTAL CONTRACT VALUE LESS:

–(i) Costs incurred to date

–(ii) Estimated future costs to complete the work

–(iii) Estimated cost of Rectification and Guarantee work

–TOTAL ESTIMATED COST OF CONTRACT

–ESTIMATED PROFIT/LOSS ON CONTRACT

– - The estimated profit is to be adjusted against the formula as follows:

- The amount of profit to be recognized in the CURRENT PERIOD is to be determined on cumulative principles as follows:

Rs. Profit to date

–

Less: Profit recognized at the end of the previous period =

–

Profit recognized in the CURRENT PERIOD =

–

Illustration 9.16

The following cost data relate to a construction company:

Rs. Contract price

50,00,000

Cumulative figures:

To end of previous period – Profit recognized:

2,00,000

To end of current period – Total costs:

25,00,000

Cost of work certified:

20,00,000

Estimate future costs to completion:

15,00,000

Estimated rectification costs, 10% of contract price

You are required to calculate:

- Estimated contract profit

- Profit to date

- Profit in current period

Solution

- Calculation of Estimated Contract Profit: (Memorandum Form) (As per (AS) – 7 (Revised))

Particulars Rs. Rs. (a) TOTAL CONTRACT VALUE

50,00,000

Less: (i) Cost incurred to date

25,00,000

(ii) Estimated future cost to complete contract

15,00,000

(iii) Estimated cost of rectification(10% of contract price)

5,00,000

(b) Total estimated costs of contract

45,00,000

*(c) Estimated contract profit (a) – (b)

5,00,000

- Profit to date is calculated as follows:

Substituting the values in the above formula, we get:

- Calculation of Profit in Current Period:

Rs. Profit to date

2,22,222.22

Less: Profit recognized at the end of previous period (given);

2,00,000.00

∴ Profit in current period:

22,222.22

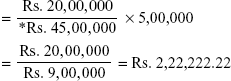

Illustration 9.17

Model: Estimated Profit

A fabrication company undertakes long-term contracts which involve the fabrication of pre-stressed concrete blocks and the erection of the same on the construction site:

The following information is supplied regarding the contract which is incomplete on 31 March 2010:

| Rs. | |

|---|---|

Cost incurred: |

|

Fabrication costs to date: |

8,40,000 |

Direct materials |

2,70,000 |

Direct labour |

2,25,000 |

Overheads |

13,35,000 |

Escalation costs to date |

45,000 |

Total |

13,80,000 |

Contract price |

24,57,000 |

Cash received on account |

18,00,000 |

Technical estimate of work complete to date: |

|

Fabrication: |

|

Direct materials: 80% |

|

Direct labour & overheads = 75% |

|

Erection = 25% |

|

You are required to prepare a statement of

- The estimated profit on completion of contract

- The estimated profit to date on the contract

[I.C.W.A. Inter – Modified]

Solution

Statement showing

- the estimated profit to date and

- on completion of contract

* Estimated profit is to be calculated as follows:

(i) Estimated profit to date:

Contract price – Total cost = Total estimated profit

Rs. 24,57,000 – Rs. 18,90,000 = Rs. 5,67,000.

Illustration 9.18

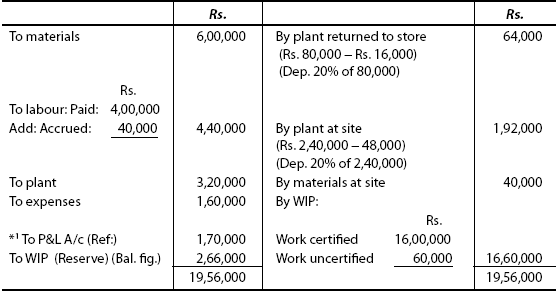

Model: Actual & Estimate Contract Particulars—Ascertainment of Profit.

VPR Ltd commenced a contract on 1 January 2009. The total contract was Rs. 40,00,000 (estimated by the contractee) and was accepted by VPR Ltd at 10% less. It was decided to estimate the total profit and take to the credit of P&L A/c that the proportion of estimated profit on cash basis which the work completed bore to the total contract price. Actual expenditure in 2009 and estimated expenditure in 2010 are given as follows:

| 2009 Actual Rs. | 2010 Estimated Rs. | |

|---|---|---|

Materials |

6,00,000 |

10,40,000 |

Labour: Paid |

4,00,000 |

4,80,000 |

Accrued |

40,000 |

– |

Plant purchased |

3,20,000 |

– |

Expenses |

1,60,000 |

– |

Plant returned to store (on cost) |

80,000 |

2,00,000 |

|

on 31 December 2009 |

on 30 September 2010 |

Materials at site |

40,000 |

– |

Work certified |

16,00,000 |

Full |

Work uncertified |

60,000 |

– |

Cash received |

12,00,000 |

Full |

The plant is subjected to annual depreciation @ 20% of cost. The contract is likely to be completed by 30 September 2010. You are required to prepare the contract Account.

[C.A. (Inter) – Modified]

Solution

Hint:

4. Contract Account is to be prepared based on the figures relating to Actual, i.e., 2009.

5. Profit to be taken to P&L A/c is to be determined after preparing the estimated contract account.

6. The estimated contract account is to be prepared based on the figures relating to actual and estimated.

*1 Profit to be taken to P&L A/c in 2009 contract Account.

NOTE: Accrued wages for 2009 would be paid in 2010. So, the wages for 2010 actually are Rs. 4,40,000.

PROFESSIONAL COURSES (ADVANCED-LEVEL PROBLEMS)

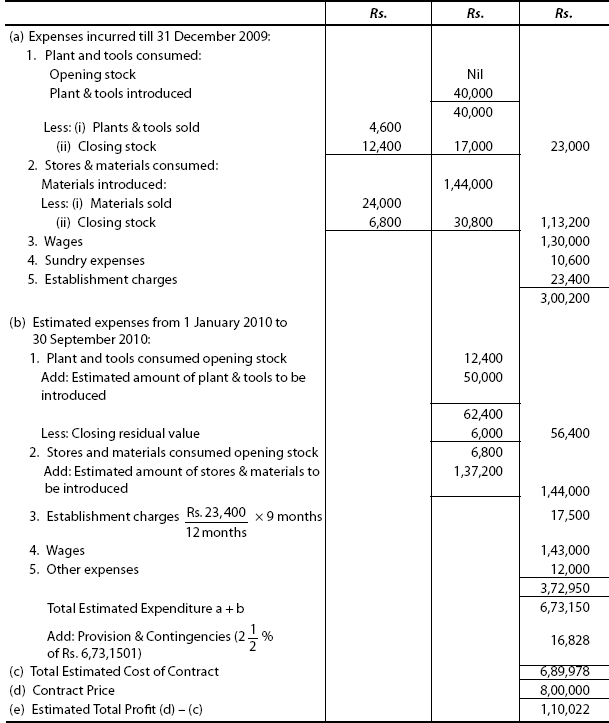

Illustration 9.19

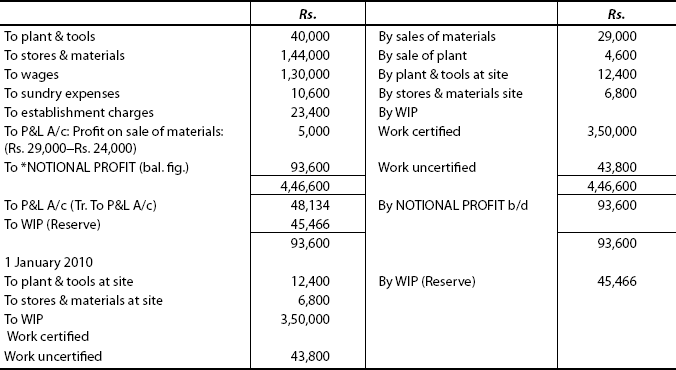

PVS contractors has been engaged in a construction work. The contract price being Rs. 8,00,000. Work commenced on 1 January 2009 and the expenditure during the year were: Plant and tools – Rs. 40,000, Stores and materials = Rs. 1,44,000, Wages – Rs. 1,30,000, Sundry expenses – Rs. 10,600 and Establishment charges – Rs. 23,400.

Certain materials costing Rs. 24,000 were unsuited to the contract and were sold for Rs. 29,000. A portion of the plant was scrapped and sold for Rs. 4,600.

The value of the plant and tools on the sites on 31 December 2009 was Rs. 12,400 and the value of stores and materials on hand was Rs. 6,800. Cash received on account was Rs. 2,80,000 representing 80% of the work certified. The cost of the work done but not yet certified was Rs. 43,800; and this was certified for Rs. 50,000.

PVS contractors decided

- to estimate what further expenditure would be incurred.

- to compute from the estimate and expenditure already incurred, the total profit that would be made on the contract and

- to take to the credit of P&L A/c for the year 2009 that portion of the total which corresponds to the work was certified by 31 December 2009. The estimate was as follows:

- That the contract would be completed by 30 December 2010.

- That the wages in the contract in 2010 would amount to Rs. 1,43,000.

- That the cost of stores and materials required in addition to those stocked on 31 December 2009 would be Rs. 1,37,200 and that the further expenses relating to the contract would amount to Rs. 12,000.

- That a further Rs. 50,000 would have to be laid out on plant and tools and that the residual value of plant and tools on 30 September 2010 would be Rs. 6,000.

- That the establishment charges would cost the same per month as in 2009.

- That

of the total cost of the contract would be due to defects, temporary maintenance and contingencies.

of the total cost of the contract would be due to defects, temporary maintenance and contingencies.

You are required to prepare the contract account for the year ended 31 December 2009 and show your calculation of the amount credited to P&L A/c for the year.

[C.S. (Inter) – Modified]

Solution

I Basis calculations:

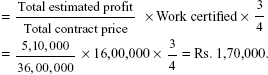

1. Calculation of work certified

Cash received by the contractor: Rs. 2,80,000.

80%of the value of work certified: Rs. 2,80,000

100%of the value of work certified

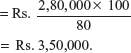

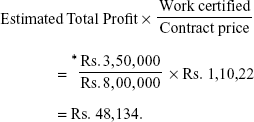

*1 (Ref: Total estimated Profit calculation).

*12. Calculation of Profit to be transferred to P&L A/c.

As per the direction in the problem, the profit is to be estimated as follows:

Balance Rs. 45,466 (Rs. 93,600 – Rs. 48,134) is to be kept as a reserve.

Illustration 9.20

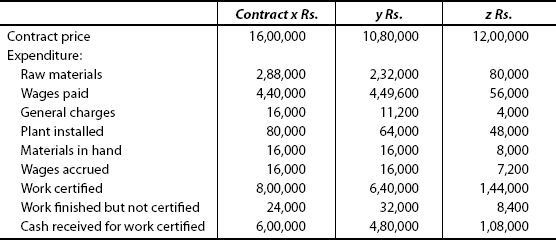

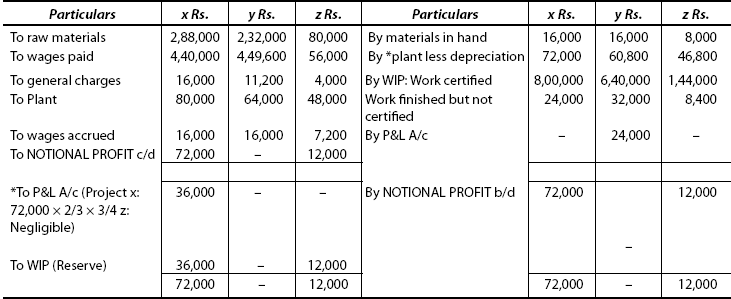

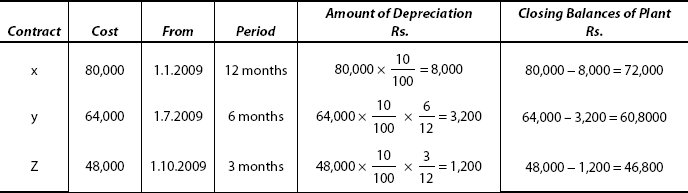

Model: Three Contract Accounts

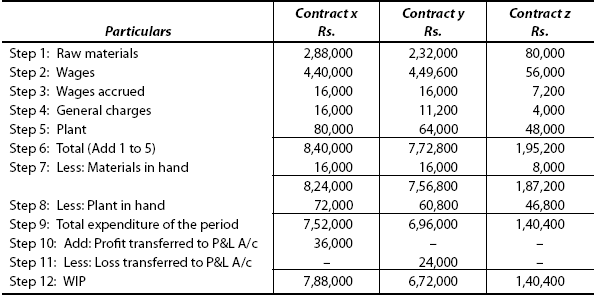

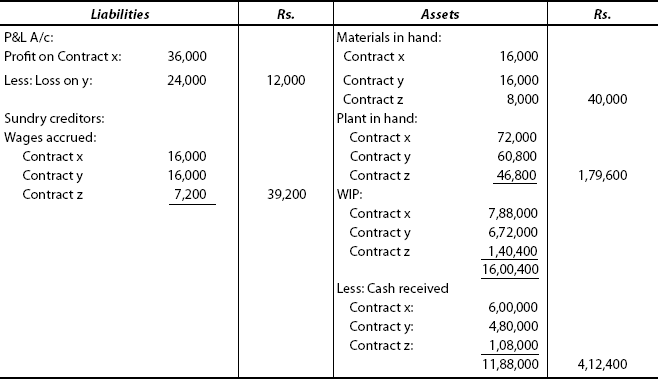

Three contracts x, y and z commenced on 1 January, 1 July and 1 October 2009, respectively, were undertaken by ABC Ltd, and their accounts on 31 December 2009 showed the following position:

The plant was installed on the date of commencement of each contract, and depreciation is to be taken at 10%p.a.

You are required to prepare the contract accounts in a tabular form and show how they would appear in the Balance Sheet as on 31 December 2009.

[C.S. (Inter) – Modified]

Solution

Calculations: 1. Depreciation on Plant

Illustration 9.21

Model: Profit to be taken to P & L A/C Different methods

An expenditure of Rs. 3,88,000 has been incurred on a contract to the end of 31, March 2010. The value of work certified is Rs. 4,40,000. The cost of work done but not yet certified is Rs. 12,000. It is estimated that the contract will be completed by 30 June 2010, and an additional expenditure of Rs. 80,000 will have to be incurred to complete the contract. The total estimated expenditure on the contract is to include a provision of 2½%for contingencies. The contract price is Rs. 5,60,000 and Rs. 4,00,000 has been realized in cash upto 31 march 2010.

You are required to calculate the proportion of profit to be taken to the profit and loss Account as on 31 March 2010 under different methods.

[B.Com (Hons)-Delhi

C.S. (Inter)-I.C.W.A. (Inter)

M.Com Madras University]

Solution

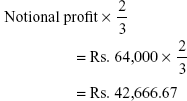

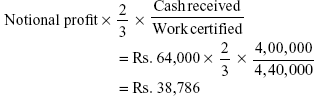

The Notional Profit is to be transferred to P & L A/C: (2/3 because the contract has reached the reasonable level of completion i.e > 50%)

Method I:

Method II:

Method III: Computation of Estimated Profit

Estimated profit may be calculated in the following different methods:

| Rs. | ||

|---|---|---|

Contract price |

|

5,60,000 |

Less: Cost incurred (total exp.) |

3,88,000 |

|

Estimated additional cost |

80,000 |

|

Provision for contingencies (3,88,000 + 80,000)× |

12,000 |

4,80,000 |

∴ Estimated profit = |

|

80,000 |

Profit to be transferred to P & L A/c are to be calculated as follows:

Method IV:

Method V:

Method VI:

Results will vary on account of basis applied for apportionment of profit that is to be taken to P&L A/c.

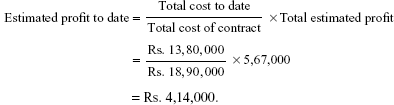

Illustration 9. 22

Model: Cost Escalation claim

VRV Ltd undertook a contract for Rs. 10,00,000 on 1 June 2008. On 31 May 2009, when accounts were closed the following details were obtained:

| Rs. | |

|---|---|

Materials purchased |

2,00,000 |

Wages paid |

90,000 |

General expenses |

20,000 |

Plant purchased |

1,00,000 |

Materials on hand on 31 May 2009 |

50,000 |

Wages accured on 31 May 2009 |

10,000 |

Work certified |

4,00,000 |

Work certified |

4,00,000 |

Cash received |

3,00,000 |

Work uncertified |

30,000 |

Depreciation on plant |

10,000 |

The above contract contained an escalation clause which read as follows:

“In the event of price of materials and rates of wages increase by more than 5%, the contract price will be increased accordingly by 25%of the rise in the cost of materials and wages beyond 5%in each case”.

It was found that since the date of signing the agreement the prices of materials and wage rates increased by 25%. The value of work certified does not take into account the effect of the above clause.

You are required to prepare the contract account

[B.Com (Hons) – Delhi – C.A. (Inter);

[I.C.W.A. (Inter) C.S. – (Inter) – Modified]

Solution

NOTE:

- All expenses in relation to the contract are to be debited to contract A/c.

- WIP, materials in hand and net of contract escalation are to be credited to the contract A/c.

- Profit arrived to be apportioned and to be transferred to P & L A/c and WIP accordingly.

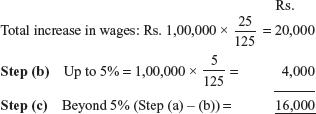

STAGE I: Escalation charges are to be computed as under:

Step 1. Effect of increase in the price of materials:

Step (a) Material purchased = Rs. 2,00,000

Less: Materials in hand = Rs. 50,000

Materials consumed = Rs. 1,50,000

|

|

Rs. |

|

|

|

|

|

|

Step (c) Beyond 5% = [Step (a) – Step (b)] = 24,000

Step 2: Effect of increase in Wage Rate:

Step (a) Wages paid: |

Rs.90,000 |

Add: Accrued wages: |

Rs. 10,000 |

Total wages |

Rs. 1,00,000 |

Step 3: Total Increase: Rs.

Step 1(c) + Step 2 (c) (Rs. 24,000 + Rs. 16,000) = 40,000

*Step 4: Increase in contract = |

Rs |

Price: (25% increase beyond 5% level) = |

10,000 |

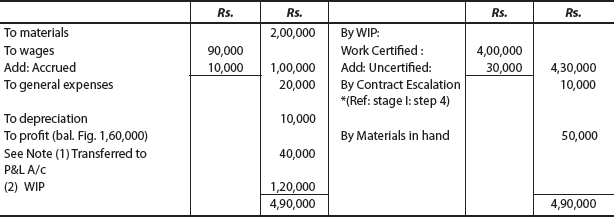

STAGE II: Preparation of Contract Account

Note: As the work completed falls – >25% but <50%, 1/3rd of profit earned has reduced on cash basis and transferred to P&L A/c.

Summary

Contract cost may be defined as the aggregate costs relative to a single contract designated a cost unit. Contract costing is a form of job costing.

Special features of contract costing: (i) construction activity (ii) work as customer’s site (iii) long duration (iv) work as per customer’s requirements (v) cost accumulation for each contract (vi) high risk and uncertainty and (vii) identifiable at each stage contract costing procedure. Ref: Text.

Types of contracts: (i) fixed price contract with Escalation clause & (ii) cost plus contract. Main features, advantages and disadvantages of each type is explained is detail. For guidelines to assess profit on incomplete contracts refer the text.

Special features of As-7 (Revised) relating to accounting for construction contracts are discussed in detail. Ref: Text. Value of WIP consists (i) work certified & (ii) work uncertified progress of work would be assessed by the customer’s engineer or surveyor who in turn would issue a certificate known as ‘work certified’. The customer would pay to the contractor on the basis of certificate. Usually the entire amount will not be paid. The balance of unpaid amount on the value of work certified is termed as ‘Retention money’. For accounting treatment refer the text.

Key Terms

Contract Costing: A form of specific-order costing which applies wherever work is undertaken to specific requirements of customers, work being long duration.

Fixed-Price Contract with Escalation Clause: To compensate the price rise in future, a special clause is incorporated into fixed-price contracts.

Cost-Plus Contracts: The actual allowable costs incurred in executing a contract plus an agreed percentage of these costs or a fixed fee payable to contractors.

Retention Money: The amount which the customer retains till the date of final completion of work.

Work Certified: Percentage of work completed to be approved by the contractee or his nominee, forming the basis for payment and profit computation.

Work Uncertified: Work would have been completed (to a certain percentage) but not approved by the contractee or his nominee.

Incomplete Contracts: Contracts that have not been completed and treated as WIP.

QUESTION BANK

Objective Questions

I: State whether the following statements are true or false

- Contract costing is a form of job costing.

- Completion of contracts will not be more than that of an accounting period, as they are of short duration.

- In contract, the work mainly involved is construction activity.

- Costs are accumulated and determined for each contract.

- It is difficult to identify each contract.

- In contract, the work is done at the contractor’s premises.

- Cost-plus contract and fixed-price contract are one and the same.

- Deductions are made from the progress payments by customer and full amount is not paid for the value of work done.

- The contractor is compensated for the increase in costs by escalation clause.

- The actual cost of the contract includes abnormal costs.

- The costs which are incurred for contracts are mainly of direct nature.

- Overhead is insignificant in contract costing.

- As profit is stated as a percentage of cost in cost-plus contracts, it is advantage to contractors.

- Loss arising on incomplete contracts should be defined to P&L A/c.

- Profit is generally recognized only after the entire work is completed.

Answers:

1. True |

2. False |

3. True |

4. True |

5. False |

6. False |

7. False |

8. True |

9. True |

10. False |

11. True |

12. True |

13. False |

14. True |

15. False |

|

II: Fill in the blanks with apt word(s)

- Contract cost may be defined as the aggregate cost relative to a ______ designated a cost unit.

- In a contract, work is mainly involved in ______ activity.

- Generally, contracts are of ______ duration.

- Contract-costing method is similar to ______ .

- The contract work is carried out according to ______ of customers.

- Progress payments are made on the basis of ______ .

- Deductions that are made from progress payments are called __________ .

- To encourage an early completion of contracts, ________ clause and _____ clause are incorporated in contracts.

- The contractor is compensated for price rise by including ________ clause.

- There are two types of contracts: 1: fixed-price contract and 2: _________ .

- The costs which are incurred for contracts are mainly of _________ .

- Apportionment of administration overheads are done on the basis of _________ .

- Payments to sub-contractors are charged to respective _________ .

- Where no cost estimate is possible ________ contracts are suitable.

- When the completion stage of contract is less than 1/4, the total expenditure on contract is transferred to _________ .

Answers:

- Single contract

- construction

- longer

- job costing

- specific requirements

- architect’s

- deduction money

- penalty bonus

- escalation

- cost-plus contract

- direct costs

- sales value

- contract account

- cost-plus contract

- WIP

III: Multiple choice question: choose the correct answer

- Where the job is of large and longer duration, the suitable method of costing is

- Contract costing

- Job costing

- Batch costing

- Backflush costing

- When no estimates can be possible, the suitable method is

- Fixed-price contract

- Cost-plus contract

- Fixed-price contract with escalation clause

- All of these

- To compensate the price rise, one of the following clauses is provided:

- Penalty clause

- Bonus clause

- Escalation clause

- None of these

- Profit in incomplete contract is known as notional profit because

- It is not real profit

- Real profit will be ascertained when the work is complete

- There is no such incomplete contract

- The profit is only an approximation

- Loss arising to incomplete contract is

- Transferred to P&L A/c

- Debited to WIP

- Debited proportionately to WIP

- Not dealt in cost accounts

- WIP in contract means

- Work certified

- Work certified and work uncertified

- Work uncertified only

- None of these

- Contract Costing is suitable of

- Bakery

- Brick

- Construction

- Chemicals

- Cost of a contract is determined by preparing

- Cost sheet

- Profit and Loss Account

- Balance Sheet

- Separate ledger account

- When a contract work is completed to the extent of 20%of the contract price, profit to be credited to P&L A/c is

- Nil

- Full amount

of profit

of profit of profit

of profit

- Profit remaining as Reserve is

- Transferred to P&L A/c

- Deducted from WIP

- Not taken into account in costs

- Debited to cost price of contract

Answers:

1. (a) |

2. (b) |

3. (c) |

4. (d) |

5. (a) |

6. (b) |

7. (c) |

8. (d) |

9. (a) |

10. (b) |

Short-Answer Questions

- What do you mean by “contract costing”?

- What are the main features of contract costing?

- Distinguish between job costing and contract costing?

- Name the industries that are suitable for contract costing?

- What are the two types of contracts?

- Explain: “Escalation clause”.

- What is meant by “Cost-plus contract”?

- What is “Surveyor’s certificate”?

- What is “Retention money”?

- How would you deal with “Materials” in contract costing

- How would you deal with “plant” in contract costing?

- How will you show “WIP” in contract costing?

- How will you calculate profit on an incomplete contract?

- Explain the term: “work certified”.

- Explain the term: “work uncertified”.

Essay Questions

- Define “contract costing”. What are the special features of contract accounting?

- Explain the steps involved in ascertaining the cost of each contract.

- How would you deal with incomplete contracts and profit?

- What are the different methods of incomplete contracts in the Balance Sheet?

- Explain the salient features of Account Standard in respect of accounting for construction contracts.

- In contract-cost accounts it may be necessary to make a charge for the use of plant and machinery. Explain briefly two methods of dealing with the charge and state in what circumstances you would adopt each method.

Exercises

[Model: Treatment of Plant]

1. A plant costing Rs. 75,000 was issued to a contract on 1 January 2009. Plant costing Rs. 5,000 was transferred to another contract on 30 June 2009. A plant costing Rs. 2,500 was stolen. Another plant worth Rs. 2,000 was destroyed by fire. A plant costing Rs. 1,500 was sold for Rs. 2,000. Charge depreciation is @ 10%p.a. Ignore the depreciation for plant stolen, destroyed and sold. Show the extracts from contract Account relating to plant.

[Ans: Closing balance of plant Rs. 57,600

Depreciation on plant Rs. 6,400

Total debit to contract A/c Rs. 75,500

Total credit to contract A/c Rs. 68,850]

[Model: Treatment of WIP]

2. A contractor undertook a contract for Rs. 5,00,000 on 1 January 2009 to be completed over a period of two years. His accounting year ends on 31 December 2009. Show at value the WIP on 1 January 2010 which will appear in the contract A/c in each of the following cases:

- WIP on 1 January 2010 Rs. 75,000 (including Rs. 3,000 estimated profit which was taken to P&L A/c in 2009)

- WIP on 1 January 2010 Rs. 75,000 (including Rs. 3,000 estimated profit was not taken to P&L A/c in 2009)

- WIP on 1 January 2010 Rs. 75,000 (excluding Rs. 3,000 estimated profit which was taken to P&L A/c in 2009)

- WIP on 1 January 2010 Rs. 75,000 (excluding Rs. 3,000 estimated profit which was not taken into P&L A/c in 2009)

[Ans:

- Rs. 75,000

- Rs. 75,000

- Rs. 73,000

- Rs. 72,000]

[Model: Transfer to P&L A/c]

3. How much profit, if any, would you allow to be considered in the following case:

|

Rs. |

Contract cost |

11,20,000 |

Contract value |

20,00,000 |

Cash received |

10,80,000 |

Uncertified work |

1,20,000 |

Deduction made from bills by way of security deposit 10%

[Ans: Notional profit: Rs. 2,00,000

Profit to be considered: Rs. 1,20,000]

4. The following expenses were incurred on a contract that was still unfinished on 31 December 2009:

|

Rs. |

Materials |

1,50,000 |

Wages |

1,30,000 |

Other expenses |

95,000 |

Rs. 7,50,000 was received from the contractee being 75%of work certified. Work uncertified was Rs. 37,500. You are required to calculate the profit to be credited to P&L A/c:

- If the contract price was Rs. 20,00,000

- If the contract price was Rs. 30,00,000

- If the contract price was Rs. 50,00,000

[Ans: Notional Profit: Rs. 6,62,500

Profit to be transferred to P&L A/c:

- Rs. 3,31,250

- Rs. 1,65,625

- Nil ∵ Less than 25%of work completed]

[Model: Completed Contracts—Simple]

5. The following is the summary of transactions as on 31 December 2009, relating to a special contract completed during the year:

|

Rs. |

Materials purchased |

7,500 |

Materials issued from stores |

2,500 |

Wages |

12,200 |

Direct expenses |

1,470 |

Work on cost |

25% of direct wages |

Office on cost |

10% of prime cost |

Contract price |

Rs. 30,000 |

You are required to prepare a contract account keeping in view that material returned amounted to Rs. 1,200.

[Ans: Profit: Rs. 2,235 Office on cost: Rs. 2,245]

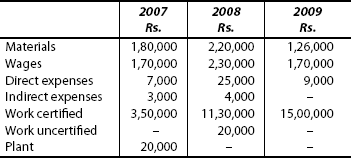

6. Geo Construction Co. undertook a contract for construction of a building from 1 July 2009. The contract price was Rs. 6,00,000. He incurred the following expenses:

|

Rs. |

Materials issued |

36,000 |

Materials in hand at the end |

6,000 |

Wages |

30,000 |

Direct expenses |

1,20,000 |

Plant purchased |

60,000 |

The contract was completed on 31 December 2009 and the contract price was duly received. Provide depreciation @ 20%p.a. on plant and charge indirect expenses @ 20%on wages. Prepare contract account in the books of the company.

[Ans: Profit: Rs. 4,08,000]

[Model: Incomplete Contracts (Loss on Contract)]

7. Vasant & Co. undertook a contract, the contract price being Rs. 3,00,000. The contract commenced on 1 January 2009. During the year the work certified was valued at Rs. 1,50,000 of which 75%was received. Work uncertified amounted to Rs. 30,000. The following expenses were incurred:

Materials – Rs. 90,000, Labour – Rs. 60,000, Plant – Rs. 30,000, Direct expenses – Rs. 24,000 and Indirect expenses – Rs. 15,000. At the end of the year wages accrued were Rs. 6,000, Materials in hand was Rs. 3,000 and plant in hand was Rs. 4,500. Prepare contract account.

[Ans: Loss on contract: Rs. 37,500]

[Model: When certified work is less than 25%of the contract price]

8. A construction company took a contract for the construction of a certain building on 1 January 2009. The contract price was agreed at Rs. 40,00,000. The company had made the following expenditure during the year:

|

Rs. |

Direct materials purchased |

1,00,000 |

Materials issued from stores |

1,50,000 |

Direct labour |

1,50,0000 |

Plant |

4,00,000 |

Direct expenses |

1,00,000 |

From the following information, prepare a contract account and find out the value of tender:

|

Rs. |

Direct materials purchased |

1,00,000 |

Value of plant on 31 December 2009 |

3,00,000 |

Stock of materials at site |

50,000 |

Materials returned to stores |

10,000 |

Cash received from contractee |

7,00,000 |

Cost of work not yet certified |

40,000 |

[As the work certified is less than ![]() th (25%) of the contract price, no profit would be taken to P&L A/c. WIP = Rs. 5,40,000]

th (25%) of the contract price, no profit would be taken to P&L A/c. WIP = Rs. 5,40,000]

[Model: Work certified is 1/4th or more than 1/4th but less than 1/2 of the contract price]

9. ‘x’ undertook several contracts and his ledger contained a separate account for each contract. On 30 June 2009, the account of the Contract No 108 showed the following amount expended there on:

|

Rs. |

Materials directly purchased |

2,70,000 |

Materials issued from stores |

2,40,000 |

Plant purchased |

10,80,000 |

Wages |

3,66,000 |

Direct expenses |

36,000 |

Proportion of establishment charges |

81,000 |

|

10,68,000 |

The contract price was for Rs. 22,50,000 and up to 30 June, Rs. 8,70,000 has been received in cash which represented the full amount certified less 20%as retention money. The materials on site unconsumed valued at Rs. 22,500. The contraction plant was to be depreciated by Rs. 24,000.

Prepare the contract account showing what profit thereon has been earned to date. And also state what amount should be taken to the P&L A/c of the period.

[Ans: Notional Profit: Rs. 2,58,000; Profit to be taken to P&L A/c = Rs. 68,799]

[Model: Value of work certified is 1/2 (50%) or more than 1/2 of the contract price.]

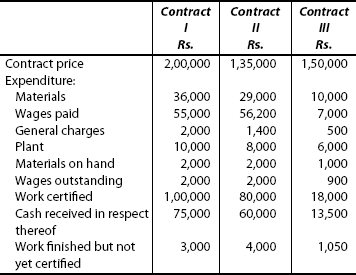

10. The following is the information relating to Contract No. 115.

|

Rs. |

Contract price |

12,00,000 |

Wages |

3,28,000 |

General expenses |

17,200 |

Raw materials |

2,40,000 |

Plant |

40,000 |

As on date, the cash received was Rs. 4,80,000 being 80%of work certified. The value of materials remaining at site was Rs. 20,000. Depreciate plant by 10%. Prepare contract account showing profit to be credited to P&L A/c.

[Ans: Notional Profit: Rs. 30,800; Profit transferred to P&L A/c: Rs. 16,426]

11. M/s Verma Building Contractors began to trade on 1 January 2009. The following was the expenditure on contract for Rs. 9,00,000.

|

Rs. |

Materials issued from stores |

2,25,000 |

Materials purchased |

60,000 |

Plant installed at cost |

1,05,000 |

Wages paid |

3,60,000 |

Direct expenses paid |

33,000 |

Establishment expenses |

30,000 |

Direct expenses accrued due |

4,500 |

on 31 December 2009 |

|

Wage accrued due on |

3,000 |

31 December 2009 |

|

Of the plant and materials charged to the contract, the plant which cost Rs. 7,500 and materials costing Rs. 6,000 were lost. Some parts of the materials costing Rs. 3,750 were sold at a profit of Rs. 750. On 31 December 2009 the plant which cost Rs. 3,000 was returned to stores and the plant which cost Rs. 2,250 was transferred to some other contract.

The work certified was Rs. 7,20,000 and 80%of the same was received in cash. The cost of work done but uncertified was Rs. 4,500. Charge depreciation on plant was at 10%p.a. You are required to prepare the contract account for the year that ended on 31 December 2009, by transferring to P&L A/c the portion of profit, if any, you consider reasonable.