6

Activity-based Costing (Cost Allocation) System

After studying this chapter you should be able to:

Understand the meaning and definition of activity-based costing system.

Know the important terms associated with activity-based costing system.

Explain the features and significance of activity-based costing system.

Understand the steps involved in the implementation of this system.

Differentiate between traditional costing system and the activity-based costing system.

Identify and select cost-allocation bases to use for allocation of indirect costs to the products.

Compute cost per unit of the product using activity-based costing system for absorption of overhead costs.

Explain all the significant key terms in respect of this system.

In Chapter 5, we have discussed the classification of overhead, items covered by each classification and allocation and apportionment of overheads. Mostly, companies have been manufacturing a limited variety of products. In such concerns, indirect costs constitute a small percentage of total costs. Hence, the task of allocation of indirect costs was easy, concise and accurate. But, of late, in an era of competition, business concerns have been launching a variety of products or services. With ever-increasing attitude for product diversity, the practice of using a single overhead rate to allocate costs to products will result in inaccurate cost results. Hence, the necessity arises to invent costing system to suit the needs of manufacturing concerns producing a variety of products. Activity-based costing system is a new technique which is aimed at the absorption of overheads in firms that produce a variety of products. In this chapter, salient features of this system, method of installing the system and determination of cost per unit of product for absorption of overheads are explained in detail.

6.1 MEANING AND DEFINITIONS

The very name of this system implies that cost would be based on activities performed in the process of production or services. The underlying fact is that products cannot consume resources straightaway. In fact, several activities are indispensable to produce a product or render a service. Such activities consume resources, where the factor “cost driver” (to be discussed later) plays a crucial role. This means that all indirect costs (overhead costs) are to be identified with each such activity that acts as a cost driver—which is mainly responsible for the incurrence of such indirect costs. The number of activities depends upon two factors: (1) number of products produced and (2) the complexity of operations. Next to cost-driver “cost centres” play another important role in this system. Overhead costs are identified with cost centre and assigned to each product or job or process on the basis of number of activities involved. Not only are overhead costs identified and assigned properly under the technique, but also cost management decisions such as product mix, price fixing and product designs are carried out perfectly.

The terminology of CIMA defines activity-based costing system as “a technique of cost attribution to cost units on the basis of benefits received from indirect activities e.g., ordering, setting up, assuring quality.”

According to Horngreen, Dasar and Foster, “Activity-based costing (ABC) is a system that focuses on activities as fundamental cost objects and utilises cost of these activities as building blocks or compiling the costs of other objects.”

To put in simpler terms, ABC may be explained as a technique which involves identification of costs with each cost-driving activity. This is made as the basis for the absorption of costs over different products.

6.2 KEY TERMS

Before discussing the technique of ABC, we have to understand certain key terms associated with this system, which are as follows:

6.2.1 Cost Objects

As explained earlier in the introductory chapter, cost object is anything in respect of which a separate measurement of cost is desirable. But, here, the ABC system focuses on individual activities as the fundamental cost concepts such as products, customers, services and locations.

6.2.2 Activities

An activity is an event, task or unit of work with a special purpose. To choose activities that form the basis of ABC system, a number of tasks performed in an organization should be evaluated by a team of experts to be constituted especially for the purpose. For this, activities are broadly divided into two groups: (1) support activities and (2) production process activities. Support activities include scheduled production, setup machine, purchase materials and custom order. Production process activities include machine products and assembled products.

6.2.3 Cost Pool

The term “cost pool” is used in the place of cost centre. The same definition holds good. So, cost pool may be defined as a location, function, items of equipment in respect of which costs may be ascertained and related to cost units for cost purposes. A cost pool should be homogeneous. That means, in a homogenous cost pool, all the costs possess similar cause and effect relationship with their respective cost allocation basis. An import aspect to be considered is that the number of cost pools should be increased to allocate the costs to each activity accurately, but at the same time much care should be taken to maintain each of such cost pool in a homogenous manner. Cost pool is nothing but a grouping of individual cost items.

6.2.4 Cost Drivers

Cost driver is

- a variable (such as level of activity)

- that casually affects costs

- over a given period of time.

The causes or reasons for occurrence of overhead costs are called ‘cost drivers’.

There is a cause and effect relationship between a change in the level of activity or volume and a change in the level of total costs. For example, if product design costs change with the number of parts in a product, the number of parts is the cost driver of product design costs; kilometers driven is the cost driver of distribution costs.

The cost driver of a variable cost is the level of activity or volume whose change causes proportionate changes in variable costs. For example, the number of vehicles assembled is the cost driver of the cost of steering wheels.

In the short run, costs will not have cost driver but will have a cost driver in the long run. For example, take the costs of testing luxury brand cars, say X, introduced in the market. These costs consist of testing department equipment and technical and other staff. These costs cannot be changed. They are fixed in the short run. However, in due course, that is, in the long run, the testing department will increase in proportion to volume of production. Hence, in the long run, volume of production is a cost driver of testing costs. Some more examples of cost drivers are as follows:

- purchase orders

- production orders

- material receipts

- machine time

- setup hours

- power consumed

- beds occupied

- Computer hours logged

- Quality inspection

- Shipments

6.2.5 Cost Hierarchies

A cost hierarchy categorized cost into different cost pools on the basis of

- types of cost drivers (transaction, duration or intensity drivers)

- cost allocation

- cause and effect relationship

ABC systems adopt a cost hierarchy having four levels:

- output unit-level costs

- batch-level costs

- product-sustaining costs and

- facility-sustaining costs.

These hierarchy levels are used to identify cost allocation bases which are cost drivers of costs in activity cost pools. Let us discuss each level briefly:

- Output unit-level costs: These are the cost of activities performed on each unit of product or service, for example manufacturing operations costs. The cost of activities increases in proportion to the volume of production or sales.

- Batch-level costs: These are the costs of activities performed on each batch (not each unit)—a group of units of products or services. The cost of activities increases in proportion to the volume of production or sales, for example procurement costs.

- Product-sustaining costs (service-sustaining costs): These are the costs of activities undertaken to support products or services irrespective of the number of units or batches, for example marketing costs to launch new products

- Facility-sustaining costs: These are the costs of activities which cannot be traced to individual products. They are common to all products. They support the entire activities of an organization, for example general administration costs.

6.3 SALIENT FEATURES OF ACTIVITY-BASED COSTING SYSTEM

The following are the special features of ABC system:

- Activity based: The ABC system is based on activities. Activities consist of different functions that are associated with cost objects.

- Activity cost centre: This is also called cost pool—the overhead cost is identified to an activity and assigned to each activity cost centre.

- Use of cost drivers: The causes of occurrence of overheads are called cost drivers. These are used to assign costs to products.

- Accumulation of overhead costs: Accumulation of overheads is done on the basis of various activities. A single unit—the entire organization—is not taken into account. No blanket rate is applied.

- Traceability: Overhead costs can be traced easily. Hence, cost data are more reliable and accurate.

- Elimination of non-value-added activities: The cost of the product would be less since the non-value-added activities are eliminated—as they do not contribute anything to the value of the product.

- Costs in proportion to cost driving activities: On ABC system, overhead costs are charged to different products in proportion to the cost-driving activities.

6.4 IMPLEMENTATION OF ACTIVITY-BASED COSTING SYSTEM

Steps that are involved in ABC system are explained as below: (R. Cooper and R.S. Kaplan in their book The Design of Cost Management Systems have discussed in detail how to implement an ABC system. The following steps are in line with those suggested by these expert authors. Students may refer this book for further details.)

Step 1: Analysis of existing costing system: The costing system that is being operated at present has to be studied and analysed. Necessary alterations have to be carried out so as to accommodate the ABC system.

Step 2: Identification of activities: After reviewing the existing costing system arises the important task of identifying activities. Preferably a committee comprising of managers from design, manufacturing, distribution, administration and accounting is constituted to identify activities. The committee evaluates a number of activities. For this, a cost—benefit analysis has to be performed. A few activities which are considered essential are selected. These activities form the basis of activity-based costing system. Cost hierarchy level is to be chosen for each activity.

Step 3: identification of products: The next step is to identify the products which are chosen cost objects (products).

Step 4: identification of direct costs of the products: Direct costs such as direct materials cost, direct manufacturing costs and other direct costs may be identified. The immediate past actual cost may be referred and taken as a yardstick.

Step 5: Selection of cost allocation bases: Identifying the cost allocation bases defines a number of activity pools into which costs must be grouped in activity-based costing system. Cost allocation basis is selected to use for allocating indirect costs to the products. Different activities that have been selected in Step 2 would be taken as bases for allocating indirect costs to products.

Step 6: identification of indirect costs associated with cost-allocation base: Overhead costs are to be assigned to activities based on cause and effect relationship between the cost-allocation base for an activity and the costs of the activity.

Step 7: Computation of rate per unit of each cost allocation base: Activity-cost rates are to be calculated using the cost-allocation basis, and the indirect costs of each activity are to be computed. This is done by dividing total costs by the quantity of allocation base. Care should be taken in the selection of cost allocation base (e.g., square metre, setup hour, machine hour). Cost hierarchy category should be chosen (output unit level, batch-level, product sustaining and facility sustaining) so as to suit the respective activity. This step is explained in Figure 6.1.

Figure 6.1 Computation of rate per unit of each cost allocation base

Step 8: Computation of indirect costs allocated to the products: The total quantity of the cost-allocation base used for each activity for each type of product is to be multiplied by the cost allocation rate calculated in the previous step. From this, cost per unit may be computed by dividing this total amount by the quantity of each activity.

Step 9: Computation of total costs of products: Add all the direct costs (calculated as in Step 4) and all indirect costs (calculated as in Step 8) to arrive at the total costs of products.

The essence of installing an ABC system is as follows:

- ABC system identifies all costs used by products. It is immaterial whether the costs are variable or fixed in the short run. It identifies all resources used by products.

- While allocating costs to products, choice of hierarchy costs is important. Total costs are first determined by using cost hierarchy level. Then the per-unit costs may be determined by dividing total costs by the number of units produced.

Illustration 6.1

A company manufacturing two products furnishes the following data for a year:

The annual overheads are:

|

Rs. |

Volume-related activity costs |

: 4,50,000 |

Setup-related costs |

: 9,00,000 |

Purchase-related costs |

: 6,50,000 |

You are required to calculate the cost per unit of product A and B based on:

- Traditional method of charging overheads

- Activity-based costing method.

[C.A.P.E. Modified]

Solution

(a) Traditional method or charging overheads

Step 1: For traditional method of charging overhead, first machine hour rate is computed (blanket rate) as follows:

Formula:

Substituting the values in the above formula, we get:

Step 2: Overhead cost per unit is determined as follows:

Statement of Overhead Cost per Unit

(b) Activity-Based Costing Method

Instead of blanket rate, overhead rate is to be calculated individually for each activity (cost pool) as follows:

Step (1) Calculation of machine hour rate for volume-related activities

Formula:

Substituting the values in the above formula, we get:

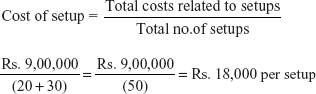

Step (2) Calculation of cost of one setup (for setup-related costs)

-

Formula:

Step (3) Calculation of a purchase order (purchase-related costs)

-

Formula:

-

Substitute the values:

Step (4)

Statement of Overhead Cost per Unit (ABC Method)

6.5 COMPARING ABC SYSTEM WITH TRADITIONAL COSTING SYSTEM

ABC system and traditional costing system differ in the following aspects:

- Basis: Under traditional costing system, overhead costs are identified to each department, whereas each activity serves as a basis for the identification of overheads in ABC system. In ABC system, activities are used as bases instead of departments under traditional costing system.

- Terminology: Usage of terms differ in ABC system. “Cost pool”, “cost driver” are such terms, whereas in traditional costing system “allocation” or “apportionment”—more popular in usage—are used. One finds it difficult the usage of new terminology under ABC system.

- Accounting treatment: Traditional costing system uses reallocation of overhead costs to production centres or service centres (departments). But ABC system uses separate rates for separate activity centres. (Refer to Illustration 6.1 for easy comprehension of accounting treatment.)

- Enhances efficiency: Product costing and price fixing are more effective if ABC system is adopted as costs are allocated to each activity—large number of activities accurately, whereas under department costing system this is not adopted. Hence, ABC system enhances the efficiency of an organization in toto.

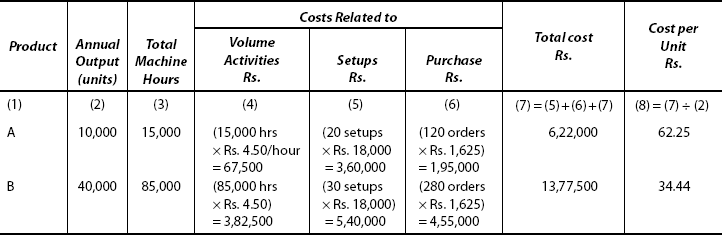

Illustration 6.2

XYZ Ltd has collected the following data for its two activities. It calculates activity cost rates based on cost-driver capacity:

The company makes three products X, Y and Z. For the year ended 31 March 2010, the following consumption of cost driver was reported:

|

Kilowatt |

Quality |

Product |

Hours |

Inspection |

x |

5,000 |

2,000 |

Y |

3,000 |

1,000 |

Z |

2,000 |

1,000 |

Required:

- Compute the costs allocated to each product from each activity

- Calculate the cost of unused capacity for each activity

- Discuss the factors the management considers in choosing a capacity level to compute the budgeted faxed overhead cost rate.

[C.A.P.E. Modified]

Solution

Step 1: Basic calculations

Calculation of rate per unit of cost driver

- Power:

- Quality inspection:

- Power:

Step 2: Preparation of cost allocation statement

To Each Product

From Each Activity

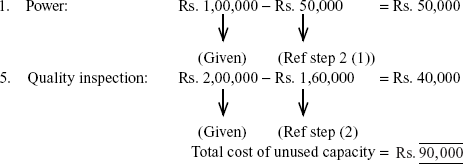

Step 3: Calculation of cost of unused capacity

Step 4: Factors for determining capacity level

While selecting a capacity level to compute budgeted fixed overhead rate, the factors to be considered are:

- Effect on pricing decisions

- Effect on cost of the product

- Effect on profit

- Effect on performance evaluation

- Effect on management of capacity and measures to overcome the difficulties.

6.6 LIMITATIONS OF ABC SYSTEM

- Cost of activity pools: Identifying activities and estimating costs of activity pools is difficult and expensive.

- Measurement of cost drivers: To identify and measure cost drivers for such chosen activity pools is a difficult exercise and costly affair.

- More clerical work: ABC systems require many calculations to determine the costs of products and services. Such calculations are complex, time-consuming and costly.

- Misidentification of costs: ABC system requires more activities—more activity pools. Hence more allocations are needed to compute activity costs for each cost pool. This exercise results in misidentification of costs of different activity cost pools. This will provide inaccurate results.

- Huge measurement errors: When the number of cost pools is large, it is natural that measurement errors will be large. In such a scenario, activity-cost information may be misleading.

- Adaptability Factor: This system requires a change on account of changes in respect of new products and new technology. Measure of activity performance changes frequently. In practice, it is difficult to adapt this system as it requires knowledge to comprehend new terminology and skill to handle suitable accounting procedure.

- Evolutionary stage: ABC system is in nascent stage. It is still not popular in most of the countries except Japan and the United States. They too are interested in this system because the cost of product has come down as “non-value-added activities” are eliminated. They want to capitalize on this advantage and introduce activity-based costing system in many corporations in their country.

Summary

Activity-Based Costing (ABC) system is a new technique aimed at the absorption of overheads in firms which produce a variety of products. Cost would be based on activities, as several activities are involved in the process of production. This is a technique which involves identification of costs with each cost-driving activity.

Cost object is anything in respect of which a separate measurement of cost is desirable.

Activity is an event, task or unit of work with a special purpose.

Activities are divided into two groups: support activities and production process activities.

Cost pool is nothing but a grouping of individual cost items. More or less cost pool and cost centre denote the same meaning.

Cost driver is a variable which casually affects costs over a given period of time.

Cost hierarchy levels are used to identify cost allocation bases—There are four levels: out-put unit level costs, batch-level costs, product or service-sustaining costs, facility sustaining costs.

Features of ABC system are (i) Activity based, (ii) Activity cost centre, (iii) Use of cost drivers, (iv) Accumulation of overhead costs (v) Traceability (vi) Elimination of non-value-added activities and (vii) Costs in proportion to cost driving activities. The steps involved in implementation of ABC system are: (i) Analysis of existing costing system; (ii) identification of activities; (iii) identification of products; (iv) identification of direct costs of products; (v) Selection of cost allocation bases; (vi) identification of indirect costs associated with cost-allocation base; (vii) Computation of rate per unit of each cost allocation base; (viii) Computation of indirect costs allocated to the products and (ix) Computation of total costs of products.

Comparison of traditional accounting method of charging overhead with ABC system can be best understood through illustration 6.1.

Key Terms

Activity-Based Costing: “A technique of cost attribution to cost units based on benefits received from indirect activity e.g., ordering, setting up, assuring quality”.

Cost Objects: Individual activities such as products, customers, services, locations—the fundamental cost concepts in ABC system.

Activities: Event, task or unit of work with a special purpose—choosing activities form the basis of ABC system.

Cost Pool: A location, function, items of equipment in respect of which costs may be ascertained and related to cost units for cost purposes.

Cost Driver: The cause for occurrence of overhead costs.

Cost Hierarchies: Categorizes cost into different cost pools to identify cost allocation bases.

QUESTION BANK

Objective Questions

I. State whether the following statements are true or false

- Under ABC system, cost would be based on activities performed in the process of production or services.

- In ABC system, cost object is anything in respect of which a separate measurement of cost is possible.

- Activities form the basis of ABC system.

- Cost pool and cost centre are synonymous terms.

- The causes for the occurrence of overhead costs are called “cost drivers”.

- A cost hierarchy means the cost should be ascertained on the level of hierarchy of management.

Answers:

1. True |

2. False |

3. True |

4. True |

5. True |

6. False |

|

|

II. Fill in the blanks with suitable word(s)

________________ costs are identified properly under ABC system of accounting technique.

Identification of indirect costs with each activity is known as ____________.

________________ form the basis of ABC system.

________________ is the technique which involves identification of costs with each cost-driving activity.

Cost objects are ______________ in ABC system.

“Cost pool” is used in the place of _____________ in ABC system.

Cost driver is a _______________ that affects costs over a given period of time.

The causes for occurrence of overhead costs are called _________________.

In the short run, costs will not have _____________.

A ____________________ categorizes cost into different cost pools on the basis of cost drivers and cost allocation.

Answers:

Overhead

Cost driver

Activities

ABC system

Cost centres

Cost centre

variable

cost driver

Cost driver

Cost hierarchy

Short Answer Questions

Define “Activity-based costing” system.

Name the four important elements involved in ABC system.

Define the term “cost objects” in relation to ABC system.

Explain “Activities”.

What do you mean by “cost pool”?

What is meant by “cost driver”?

Give examples of cost drivers.

Name the categories of cost drivers.

Essay Type Questions

Define activity-based costing system. Enumerate its special features.

Explain in detail the stages involved in designing an ABC system?

What are the uses of ABC system?

What are the limitations of an ABC system?

Distinguish between traditional costing system and activity-based costing system.

What are the different stages involved in ABC system of costing? Illustrate.

Do you think ABC system can be adopted successfully in India? Substantiate with suitable reasons your answer.