Opportunities for Leadership Driven Management

Unknown to most people, strong financial control does exist in government. At the federal level,1 Congressional Oversight Committees, Agency Auditors General, the Office of Management and Budget, and the Government Accountability Office all work hard in their role as watchdogs, protecting the public from acts of “waste, fraud, and abuse.” The federal management control complex makes significant efforts and spends enormous funds to implement these controls.

Current controls are rule based, and the rules work like commandments of the “thou shall not” category, prescribing things that should not be done and listing penalties for violation. It is not the purpose here to critique the costs and benefits of these practices. We will assume that they are necessary and useful in preventing “sins of commission” and “mismanagement.

Unmanagement Offers Much Greater Opportunity Than Mismanagement

However, rule based federal management practice is mostly silent on what good management practice should do. The objective here is to explore cost management practices that are not currently being extensively used in government management. The potential savings and efficiency improvements from these largely unexploited management techniques may be significantly more important than currently used controls.

This is to say that “unmanagement” rather than “mismanagement” may be the greater problem and a tremendous opportunity. In a sense, then, we must also address “sins of omission” and consider what we should do proactively and aggressively to better manage government’s fiscal resources and their role in accomplishing the work of government. This is not an accounting issue; instead, it requires strong leadership driven management.

The Current State of Rule Based Federal Financial Management

The generally accepted definition of good management in government is spending 99.9% of the budget appropriation. This is not necessarily bad as far as it goes. Prohibition (“thou shall not”) of spending more than appropriated is a good thing. This strong prohibition against overspending the budget provides the foundation for the effective existing budgetary control process.

The strong prohibition of overspending comes from the Anti-Deficiency Act. The Act makes it a criminal offense for federal agencies to spend more than appropriated. The Supreme Court has also made it clear that the Executive Branch cannot defy the will of Congress by spending less than budgeted.

Spending less than 99.9% of budget is diligently avoided at all levels of federal agencies. Significant effort is made to spend funds because unspent funds are “lost” to the budget holder, and reduced spending levels make it harder to justify desired budget increases in the future.

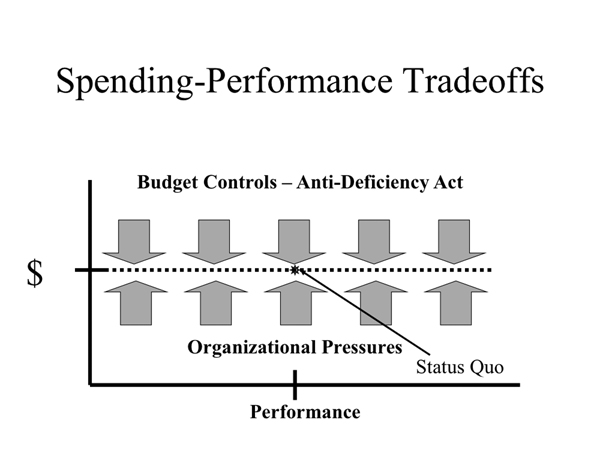

Figure 1.1. The twin pressures of organizational interest and the Anti-Deficiency Act mean that the budget gets spent regardless of performance.

Figure 1.1 shows that the pressures to avoid overspending and underspending budget work to keep spending at budget levels. Budget controls and the powerful Anti-Deficiency Act mitigate against increased spending while organizational pressures strongly discourage underspending. These pressures are independent of performance. In other words, statutory spending requirements can be met and 99.9% of the budget can be spent at all levels of performance.

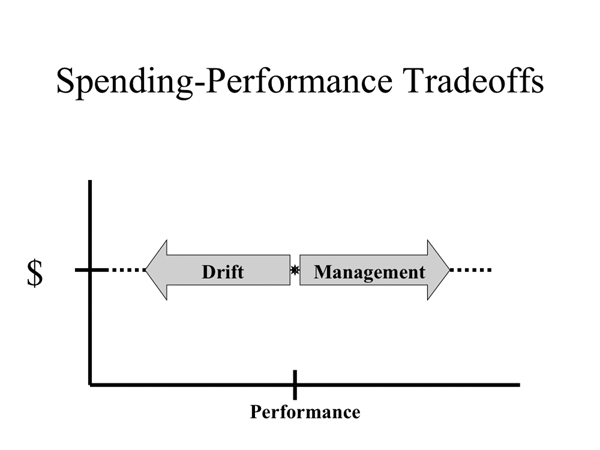

This current definition of good financial management is unsatisfactory, as it ignores how wisely the budget appropriation was spent. Good financial management should mean continuously improving the cost effectiveness of operations in ways that ultimately improve the overall effectiveness of government programs and missions. Figure 1.2 captures this management impact as an arrow driving increased performance within the spending constraint.

One very good Army garrison commander described the cost management and control process as being like sailing into the wind. Ships can sail into the wind only by adjusting the angle of the sails properly, steering at the correct angle into the wind, and tacking back and forth skillfully into the wind. However, he related that “as soon as you stop working the sails and let go of the rudder, the prevailing winds take over and you go in the opposite direction.” (Colonel Mike Boardman, Garrison Commander, Fort Huachuca. See chapter 8, for more on the Fort Huachuca implementation of organization based control.)

Figure 1.2 labels this phenomenon as “drift”: the natural tendency of people and organizations toward inefficiency and less challenging performance.

Conflicted Roles in Rule Based Management Practice

Rule based management processes do well in relatively simple matters but suffer when complex judgment is required. For example, traffic laws can prescribe the rules of the road. They can mandate speed limits, required stops, and even specified levels of equipment maintenance. Penalties exist for noncompliance (if caught violating) by traffic police (at a cost). The rules, however, cannot prevent lapses in judgment or ensure safe driving.

Figure 1.2. At any given spending level, there is a tension between the natural “drift” of organizations toward lower performance and the offsetting goal of management to increase it.

The nature of rule based processes creates a conflicting role for the rule making power in government. Consider the role of Congress in financial management and control. It holds the purse strings and it sets the rules.

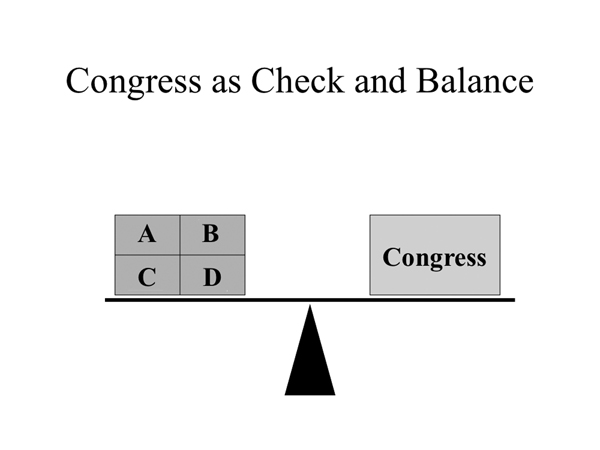

The historical, constitutional role of a rule maker such as Congress is as a check and balance to the power of the Executive Branch. Congress uses its hearings, its budget and appropriation authority, and its Government Accountability Office and Congressional Budget Office to influence spending by Executive Branch agencies. Fulfilling this role generally results in an arm’s length, sometimes adversarial, approach in which Congress exercises its oversight powers. Figure 1.3 shows Congress balancing the power of Executive Branch departments A, B, C, and D.

However, financial behavior of the Executive Branch is not independent of Congress. Congress is an integral and essential part of the financial management process in three ways.

First, Congress is solely responsible for appropriating the budget. The Executive Branch proposes and Congress disposes. Second, Congress has passed strict laws to ensure that the budget levels it appropriates are not overspent. Its Anti-Deficiency Act makes overspending the budget a criminal action punishable by fines and imprisonment. Third, it has been established that the Executive Branch is not permitted de facto budget setting power by neglecting to spend funds appropriated by Congress.

Figure 1.3. Congress (and often centralized agency headquarters) has a role to check and balance departments A, B, C, and D.

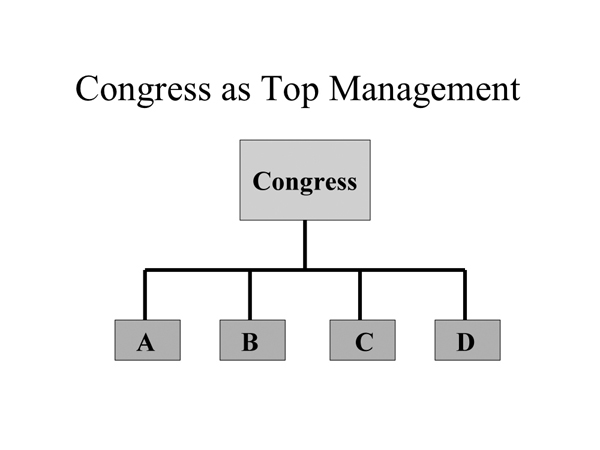

In this role, Congress assumes the top level of the financial management hierarchy. It is ultimately responsible for setting policies and funding outcomes. Hierarchies are common organizational structures, and the top of a hierarchy is usually recognized as the top management of that hierarchy.

Figure 1.4 depicts Congress at the top of the financial management hierarchy, providing all funding and direction to Executive Branch departments A, B, C, and D.

Figure 1.4. Congress (and centralized agency headquarters) represents the top of the financial management hierarchy.

These contrasting roles of checks and balances and financial executive are not unique to Congress. They are common to many government organizations. The Office of Management and Budget seeks both oversight and financial leadership over federal departments. Departments seek both oversight and financial leadership over their agencies, and so forth.

These contrasting, and somewhat schizophrenic, roles raise interesting questions of practical effectiveness. Yet Congress purports to be interested in resource consumption within the Federal Government. It seems to be the underlying theme indicated in the Chief Financial Officers Act and the Government Performance and Results Act.

Consider that the Chief Financial Officers Act states that “billions of dollars are lost each year through fraud, waste, abuse, and mismanagement among the hundreds of programs in the Federal Government. These losses could be significantly decreased by improved management.” Similarly, a major objective of the Government Performance and Results Act is to “improve Federal program effectiveness and public accountability.” Furthermore, the Federal Financial Management Improvement Act states that one of its goals is to “improve performance, productivity and efficiency of Federal Government financial management.”2

These and other laws clearly indicate that Congress believes it has a role in improving the financial management of the Federal Government. Achieving this goal begs the question of whether the traditional checks-and-balances role is compatible with the leadership role.

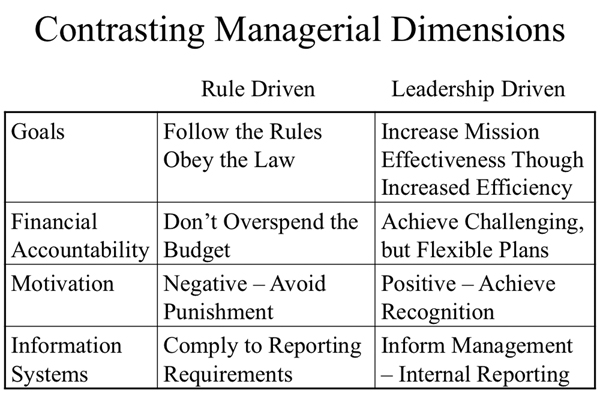

Rule Driven Differences to Leadership Driven Management

Rule based management centers on laws, regulations, restrictions, and compliance audits. It appears similar to that of the legal process in which attorneys work in a rule driven, but adversarial, manner. The oversight process exhibits the dynamics of a legalistic approach. Evidence is sought and the jury of legislators, top managers, or the public is influenced. The goal of the process is to expose wrongdoing, and the process becomes inherently adversarial. Wrongdoing is most easily proved when actions are shown to violate established laws, rules, or principles: The success of this process requires rules and tests for compliance to the rules. These behaviors are common to the role of checks and balances.

On the other hand, effective management from the apex of the financial management chain of command would seem to require a more leadership driven approach. The leader, whether coach or captain, is part of the team. The leader, of course, must comply with the rules of the game. However, his role is much broader. Simply playing by the rules does not win the game. The leader must grow people, design processes, and deploy strategies to develop a winning team. There is not one way to do this. While every team plays by the same set of rules in any sport, there are many ways to play the game. The leader seeks to find the best combination of capabilities and opportunities to improve team performance.

Whereas the rule maker makes a rule, the leader makes a plan. The rule maker publishes the rule, while the leader trains personnel and teaches the plan. The rule maker seeks to prove or disprove compliance through an audit, and the leader tests the plan through interaction and review. The rule maker exposes wrongdoing in order to punish. The leader seeks to understand mistakes in order to learn from them. The rule maker penalizes wrongdoing, whereas the leader corrects mistakes and builds from what’s right. The rule maker follows up by closing loopholes in the rules, whereas the leader evolves to a new and better plan.

Figure 1.5. The differing roles in rule driven and leadership driven management.

Consider four crucial dimensions of management: (a) goal setting, (b) accountability, (c) motivating, and (d) information systems (Figure 1.5).

The goal of an oversight process is to write comprehensive rules that, when obeyed, provide the desired outcome. Continuous process improvement, however, requires billions of efforts by millions of people because achievable improvements are embedded throughout the organization. Success requires a culture in which the goal is to increase mission effectiveness by improving efficiency. Such a goal appeals to dedicated personnel who have committed their lives and careers to the missions they manage.

Financial accountability is currently based on not overspending the budget. The current definition of good financial management in the Federal Government is to spend 99.9% of the budget. It does not matter how wisely it is spent, as long as spending does not exceed 100%.

Consider the budget mechanism as it relates to cost management. First, the budget cycle is relatively long. Management at the operating levels of federal organizations probably sees an 18-month period elapse from the time the budget is submitted until the budget year is over and the accounting process completed. Furthermore, no useful learning is possible because no variances exist. Everyone has worked diligently to spend 99.9% of the budget.

Worse, the budget process motivates spending in the fourth quarter to avoid underspending the budget. This motivation occurs at all levels of the organization. The Department level, of course, responds to the wishes of Congress to spend money appropriated as Congress has directed. Lower levels in the organization, however, seek to protect their budget levels by avoiding the suggestion that they could do with less.

No one wants to admit the budget is too high. Even if it is too high, who knows, maybe someone in the future will really need that budget, which brings us to the concept of need. Defining “needs” drives federal organizations. Many times managers have expressed interest in cost measurement, not to manage better but to express their needs better. We have created a culture that spends an enormous amount of time defining, defending, and, ultimately, denying needs when we would be better off spending some of that time continuously reducing needs.

The enormous effort federal organizations spend in defining their needs is particularly ironic, considering the underlying economic philosophy of the former Soviet Union: “From each according to ability: to each according to needs” resulted in similar overemphasis on needs and an underemphasis on developing abilities.

Financial management leadership requires a process of creating challenging but flexible plans throughout all levels of the organization. No learning occurs if plans are so conservative that they are always achieved; therefore, plans need to be somewhat challenging. This implies that missing a plan is not a crime. Accountability needs to be tempered with judgment.

Motivation of the federal agency in a legalistic oversight process is to avoid punishment. One unintended consequence of this type of motivation is that enormous efforts, and costs, are spent to avoid the negative. While leaders must sometimes use negative motivation, it seems clear that positive motivation has a very important role.

Adversarial processes are useful in the legal system in which plaintiff and defendant argue their cases and the judge or jury decides. It is harder to see the benefit of this style between a first-line supervisor and her workers or between a first lieutenant and his platoon. Although rank and hierarchy must be respected, cooperation may provide better results. The oversight process seeks to improve by exposing what is wrong. The leadership process seeks to improve by building on what is right while recognizing that perfect is the enemy of good.

Both styles create employee and organizational motivations. The oversight process motivates compliance. The leadership process should motivate creativity.

Information systems in the oversight process are directed at providing auditable information to the overseer. This external reporting process often requires considerable energy and expense. Highly defined and relatively rigid measurement processes ensure that consistency and auditability characterize external reporting systems.3

Continuous process improvement requires information that is relevant and useful to operating managers at all levels within the organization. This is an internal reporting process. Measurement processes for internal reporting systems emphasize fit and functionality and usually require significant customization to provide the needed functionality and credibility at reasonable cost.

Good financial management depends on sound general ledger accounting systems. Progress has been made since the Chief Financial Officers Act in establishing this foundation. However, it should be recognized that the job of these systems is to produce an aggregated external report once per year. Management information requirements for continuous improvement may be several orders of magnitude more detailed and more frequent. Furthermore, the existence of an auditable external report does not guarantee sound internal management. Most companies that file for bankruptcy have clean financial opinions.

Example of Dysfunctional Rule Driven Motivation: Budgetary Slack

To illustrate the motivational differences between legalistic and leadership modes, look at the common budgetary practice of building “padding” or “slack” into budgets. Slack is defined as the difference between spending plan and budget received. The criminal penalties of the Anti-Deficiency Act motivate significant slack.

Consider the position of a manager who faces criminal penalties for overspending the budget. Building in a safety margin of 10% or so would be very prudent. Problems may occur during the year that require funding. These can be funded from the budget slack, if available.

Significantly more difficult problems ensue if slack was not planned. Perhaps the organization could get additional budget by submitting a supplemental budget request. This may be politically difficult, if not impossible. If additional budget infusion is not possible, drastic spending cuts may be required. Contracts and staffs might have to be slashed quickly to cut funds outflow. These cuts might have to be made where possible rather than where best.

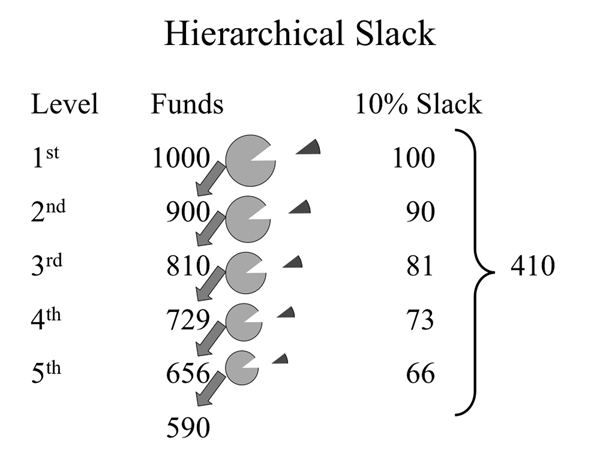

Consider, however, the impact in a five level organization if each level reacts to the legal threat by keeping 10% of its budget in reserve as slack. The top level keeps 10% and passes 90% down to its subordinate organizations. The subordinate organizations keep 9% (10% of its 90%) and pass down 81% (90% of its 90%) to their subordinates. Several similar cascades show the fifth level of the organization only spends 59% of the original budget (90% of 90% of 90% of 90% of 90%).

Figure 1.6. If five levels of an organization each retain 10% budget for contingencies, only 59% reaches the working sixth level.

Five levels that each build in a 10% safety margin create an organization-wide safety margin of 41%! (See Figure 1.6.) It should not be a surprise to learn that a lot of government spending occurs in the last quarter of the fiscal year as agencies scramble to spend all the leftover slack!

Imagine an alternative management philosophy based on the leadership model. Such a model might “capture” the huge slack currently used to defend against antideficiency violations. Once captured, that slack could be better planned to finance unfunded requirements and other programs designed to enhance the mission effectiveness of the organization.

Leadership Driven Management Opportunities

Government organizations can run better. They can run much better. The goals of this book are (a) to document practical solutions that have already been proven effective in government organizations and (b) to provide a framework for understanding the critical requirements for success in a simple theoretical framework in a manner that will help other organizations duplicate the successes.

Part I of this book will begin with cost informed decision making, undoubtedly the least complex and most obvious opportunity. Decisions, such as acquisition or policy making, usually involve a host of criteria. Cost is usually not the only concern, but any decision made in the absence of cost information will undoubtedly overvalue some other criterion.

- Chapter 2 will discuss the first and more important requirement for success: aggressive, knowledgeable leadership.

- Chapter 3 will cover the second critical requirement: smart staff support, costers, and cost analysts.

- Chapter 4 will show recent case examples of cost informed decision making from the United States Army Central Command headquartered at Camp Arifjan, Kuwait.

Part II will expand the complexity and persistence of cost usage that can be found in cost managed organizations. These organizations manage costs in a variety of ways that undoubtedly include multitudes of cost informed decisions made at many points within the organization. This is a very different management paradigm than that found in the budgetary control process. Experience has shown that several types of leadership driven management control processes are likely to be highly effective in improving the efficiency of government operations.

- Chapter 5 will outline the first additional requirement needed to move from cost informed decision making to a cost managed organization: an interactive, learning oriented cost management process.

- Chapter 6 will cover the second additional requirement needed to build a cost managed organization: good cost measurement.

- Chapter 7 will describe organization based control processes that drive cost management by relying on accountability relationships found in the organizational chart.

- Chapter 8 will present the 10-year-long case study of implementing an organization based control process at the Fort Huachuca Garrison.4

- Chapter 9 will describe role based control processes that seek to improve the efficiency and effectiveness of organizations linked by their roles in a common purpose but not via an organization chart.

- Chapter 10 will present an application of this technique used to manage the roles and responsibilities of support functions for more than 15 years at the Navy’s SPAWAR Systems Center Pacific research facility.

- Chapter 11 will describe output based control processes that use views of full or controllable costs to focus understanding and improvement on an organization’s product or service.

- Chapter 12 will show the highly effective processes developed at the Bureau of Engraving and Printing to manage the cost of currency production for over twenty years.

Part III, the final section, will take a more futuristic view where appropriate elements of all previous chapters are integrated across the organization to build a truly cost managed enterprise. I know of no significant-sized government operation at this level of cost management maturity.

- Chapter 13 will discuss implementation issues of organizations facing transformation to improved cost effectiveness.

- Chapter 14 will close with conclusions.

Leadership Driven Management Lessons Learned

The idea of better cost management in government is not new. There have been numerous legislative attempts, as noted. Senior leaders such as U.S. Army Secretary Luis Caldera have also tried. (See Figure 1.7.) Unfortunately, most people in the Army did not “get the memo.”

The hard-learned lesson, however, is that it takes more than paper to change entrenched management practices. Good management cannot be directed by memo, no matter how well written.

Good management must be leadership driven.

Successful implementation of a leadership driven management process requires four elements. Obviously, leaders are the highest priority of a leadership driven paradigm. Efforts to establish leadership driven management teach us that very strong staff support to the leader is also a prerequisite to success. The need for a “government-applicable” process is also clear. Finally, it would be hard to imagine a cost management process that did not need cost measurement. The reader who wishes to focus on these requirements should visit the following chapters.

- Aggressive, knowledgeable leaders will be addressed first. These managers must understand the costs of their decisions and aggressively drive improvement (chapter 2).

- ACEs (Analytic Cost Experts) are covered next. This staff runs the process while becoming the trusted financial advisors to operating management. It is arguably the most challenging requirement (chapter 3).

- The interactive, learning oriented review process will then be covered as we move from cost informed decision making to interactive cost management processes that work through behavioral change. The workable process must provide an organizationally compatible, institutionalized forum for discussion, improvement of idea conveyance, and decision making (chapter 5).

- The last requirement for success is cost measurement capability. Historically, this is the area that has received the most attention. In reality, little actually happens without managers to execute, processes to institutionalize and facilitate, and staff to analyze and advise (chapter 6).

Conclusions

It seems that the typical mode of management in government could best be described as a rule driven management process typified by oversight. Government oversight tends to be a centralized, rule driven, and somewhat legalistic approach. Congress exercises oversight of the Executive Branch. The Office of Management and Budget exercises oversight of the Departments. The Departments exercise oversight of their agencies and so forth down the organization structure.

Rule driven management plays a valuable, although limited, role. However, one definition of “an oversight” as a noun is “something overlooked or missed.” Government management through oversight unfortunately overlooks and misses the opportunities offered by other management techniques.

Both rule driven, legalistic oversight and leadership driven approaches have advantages and disadvantages. The rule driven approach seems to make the most sense in checking and balancing. However, the limits of lawmaking and policy making seem to be substantial. If Congress or Agency level policy makers could significantly affect financial management practice by decree or legislation, we would probably not be having this discussion. If changing human behavior and interaction were so simple, we should also be able to rid ourselves of crime, hate, laziness, greed, and jealousy.

Rule driven oversight can only go so far in promoting better management. It seems to best perform the function of establishing boundaries. Significant improvement in federal financial management will likely require increased emphasis on a leadership driven financial management approach.

This book will provide examples of effective, government implemented cost management and control practices. Most significant, these examples have stood the test of time in their organizations. The goal of this effort is to propose some theoretical structure to these accomplishments and to evaluate critically the needed ingredients for them.

It is likely that history will have much to say about how the government of the United States has spent (often borrowed) resources over the last few decades. It appears illogical to assume that such behavior can continue indefinitely. It seems more likely that government resources will be increasingly constrained. Government agencies at all levels are likely to be embroiled in a Cost War: the struggle to accomplish their missions in an environment of constrained resources.5

While traditional oversight will always have its purpose, it is time to consider, fund, and implement leadership driven management processes. It is hoped that Cost Management and Control in Government offers some beneficial aid for fighting the cost war that far exceeds the cost of its reading.

Figure 1.7. Secretary of the Army memorandum.