2

Bitcoin, the First Application of a Blockchain

We won't overlabor Bitcoin as there are plenty of books that dive deep into this origin story. Because Bitcoin is Bitcoin, however, we have to start here. Bitcoin was the first crypto superstar, created in response to the chaos of the 2008 financial crisis. During this time lenders failed consumers in a public way, feeding a growing distrust of big banking. Banks received far more than just bailouts. Profits were allowed to stay private while losses were socialized—the public, instead of the banks, shouldered the burden. Bitcoin, by far the most well‐known and trusted token, was born out of destruction.

Bitcoin's pseudonymous creator, Satoshi Nakamoto, responded by creating an alternative digital currency that did not rely on too‐big‐to‐fail central banks and other murky authorities such as the Securities Investor Protection Corporation (founded and funded by brokers to more or less insure investors who lose money at financially troubled member firms). Nakamoto's whitepaper influenced developers and investors worldwide. He proposed a peer‐to‐peer (P2P) payment system that did not require third‐party confirmation. Banks, governments, and other central authorities aren't required to settle every transaction, noting that “what is needed is an electronic payment system based on cryptographic proof instead of trust, allowing any two willing parties to transact directly with each other without the need for a trusted third party.” Given the distinctions identified in the previous chapter, perhaps this section of the Bitcoin whitepaper makes more sense now:

Transactions that are computationally impractical to reverse would protect sellers from fraud, and routine escrow mechanisms could easily be implemented to protect buyers. In this paper, we propose a solution to the double‐spending problem using a peer‐to‐peer distributed timestamp server to generate computational proof of the chronological order of transactions. The system is secure as long as honest nodes collectively control more CPU power than any cooperating group of attacker nodes.1

Nakamoto defines a token or electronic coin as “a chain of digital signatures,” where each owner transfers the coin to the next by digitally signing a hash of the previous transaction and the public key of the next one and adding these to the end of the coin: “A payee can verify the signatures to verify the chain of ownership.” We are stressing this because the origin and intent were important, and blockchain is the breakthrough upon which Bitcoin was built.

How to protect privacy and identity, and maintain crypto security? Nakamoto identified the tradeoff found in the traditional banking model. Sure, our information is private, relatively, but the companies and entities that facilitate the bank's transactions are behind closed doors. The bank is a black box that we cannot see into. Nakamoto's answer was to make everything transparent so that “the public can see that someone is sending an amount to someone else, but without information linking the transaction to anyone.”

A blockchain opens the closed doors with the hash we discussed in Chapter 1. Hashes are put together to form a chain, with each additional timestamp reinforcing the ones before it. This is our blockchain. The blockchain identifies each participant and their action so all can see. Imagine if you received a record and timestamp of the investors and service fees and vendors that benefit from or participate in each Venmo transaction.

And so crypto's first hero, Bitcoin, was born. Fourteen years later as we write this, hundreds of millions of people worldwide, particularly the younger generations, trade and trust bitcoin and other cryptocurrencies (while the U.S. savings bonds their parents trusted aren't seen as spectacular savings vehicles because – well – they aren't). Bitcoin is considered by many to be a viable, alternative digital currency. It can be used at Starbucks and Home Depot, has been endorsed by seminal investors Paul Tudor Jones and Stan Druckenmiller (to name just two), has earned favor at big banks such as BlackRock, and is even legal tender in some countries. Bitcoin is available to anyone around the world with a smartphone and can be sent halfway around the world in a matter of minutes for a fraction of the cost to wire or transmit funds otherwise. Bitcoin was the first successful blockchain. Thanks to its success, there are now thousands more digital coins and tokens. Some will survive; most will not.

Crypto assets, the tokens that are used by blockchains for various purposes, represent a new asset class for investors. They are not correlated to stocks, bonds, or gold, although there can be periods of high correlation. They can increase in both price and value without the economy growing. They can be used to generate real interest income or to represent real goods or digital goods. Owning crypto assets helps an investor diversify by providing an asset class that is not solely U.S. dollar–denominated. Crypto assets are, of course, still new and therefore still volatile, as 2022 reminded us, but as the market matures, we foresee that they will become increasingly attractive to more and more people.

As of February 2021, according to numerous sources, Bitcoin had a market capitalization of more than $1 billion, with over 300 million people having used or owning cryptocurrencies. The leading nation for crypto users is India, with about 180 million users in 2021, while the United States was second with 27 million crypto owners. More than $110 billion is traded in cryptocurrency per day, according to Blockchain.com.

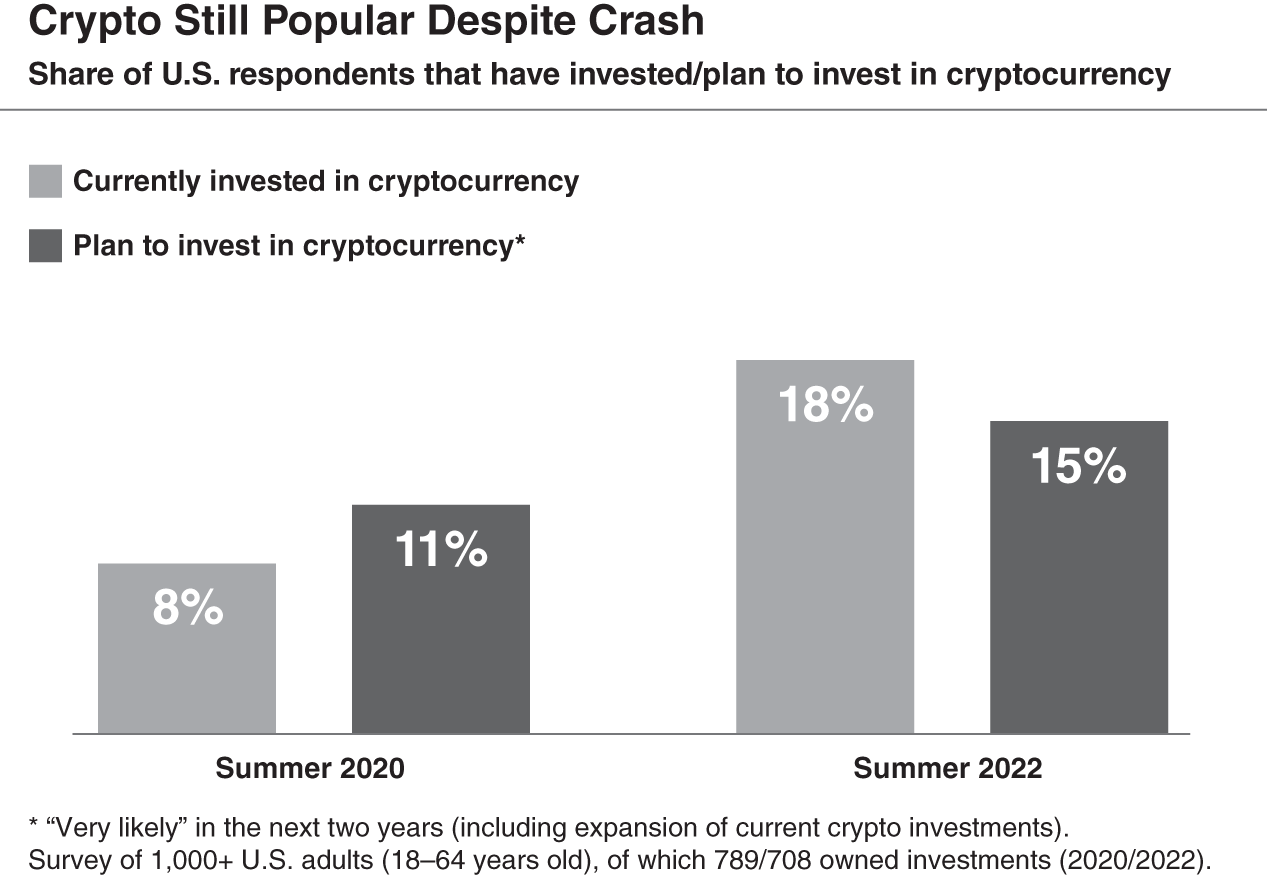

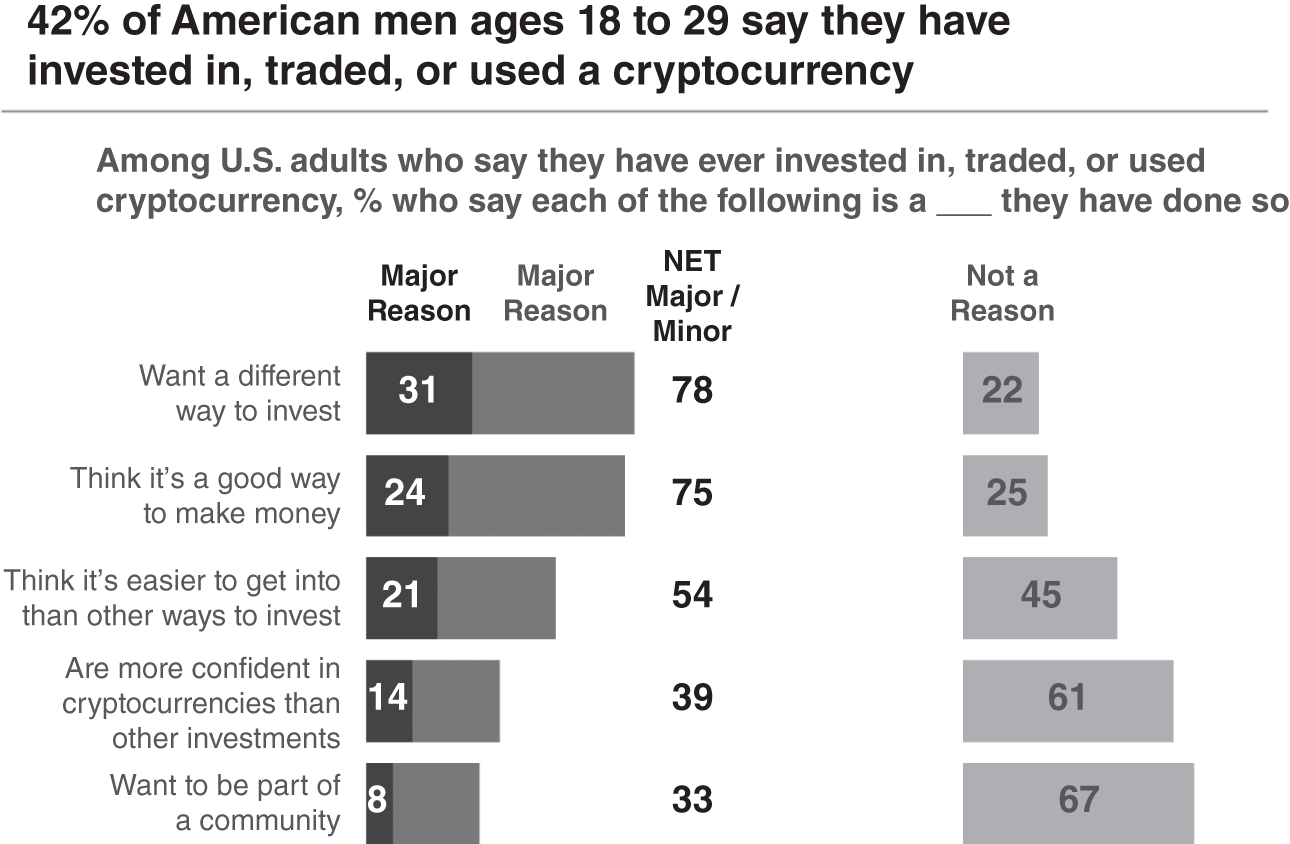

Most U.S. adults have heard at least a little about cryptocurrencies like bitcoin or ether, a Pew Research study found in 2021 (see Figure 2.1), with 16% of people saying they had invested in, traded, or otherwise used one. Nearly 9 in 10 Americans told Pew that they had heard at least a little about cryptocurrencies; about one quarter said they had heard a lot about them. Men ages 18 to 29 were particularly likely to have used cryptocurrencies (see Figure 2.2).

We cite these numbers to illustrate the rapid growth and scale of the crypto markets but, look, they are still young, and these can be risky investments, as noted by the 46% of investors in the survey who have done worse than expected. That's where this book comes in, to add some context and clarity. “An investment in knowledge pays the best interest,” Ben Franklin said. And if you are uncomfortable in this new world, that's good news, too, because, in the words of investor Robert Arnott, “What is comfortable is rarely profitable.”

Figure 2.1 Crypto Chart of U.S. Investors

Source: Statista Global Consumer Survey © 2022, Statista. / Public Domain CC BY 4.0.

Figure 2.2 Exposure to Crypto

Source: Statista Global Consumer Survey © 2022 Pew Research Center.

Additional information: Pew Research Center. Note: Those who did not give an answer are not shown.

What's Unique About Bitcoin

While there are thousands of crypto assets, Bitcoin is the granddaddy of them all. It possesses many characteristics that give it unique importance to the investor. Following are the essentials:

- Bitcoin's supply will never exceed 21 million bitcoin. The anti‐inflationary nature of Bitcoin bears even more importance as we experience sustained inflation in the global economy. For every 210,000 blocks that get produced, which occurs roughly every four years, the reward for mining a bitcoin is halved. This means that the inflation rate decreases by half because the only way for bitcoin to get minted into the system is through the block reward to miners.

- Bitcoin is akin to digital gold. Bitcoin is not a traditional investment like a stock, but a currency in and of itself and is classified as a commodity by the Commodity Futures Trading Commission (CFTC). As with any commodity, bitcoin is produced and used. Bitcoin miners expend work by labor, equipment, and energy to create bitcoin. There is a cost of production just like with gold or any other precious metal and, unlike fiat currency, is not an attempt to create value out of thin air. It retains its traded value no matter what governments do with their monetary systems. It does not have counterparty risk and is not a liability on another party's balance sheet.

- Bitcoin is validated by triple‐entry accounting. This is a fancy way of saying that every transaction is audited as it is written, something that is now only possible because of blockchain technology.

- Bitcoin is sound money, which means its value has been set by the marketplace and it performs the functions of money well by having the six characteristics of good money:

- Divisibility

- Durability

- Portability

- Uniformity

- Acceptability

- Scarcity

What's important to consider here is that bitcoin far outperforms gold in these characteristics. Bitcoin is more divisible than gold. Bitcoin uses eight decimal points of precision, meaning the smallest amount of bitcoin (BTC) transferable is 0.00000001 BTC. Gold can't get to that level of precision for divisibility. Bitcoin is more durable than gold; it is merely letters and numbers that form a public key that can be stored in a computer or even on anything physical. If desired, a person could etch the key into gold. Bitcoin is more portable than gold. We can send 10 billion dollars' worth of bitcoin around the world in 15 minutes, and it would cost up to a few dollars. There is no need for an army of planes to transport 24 tons of gold with bitcoin. One key to bitcoin's intrinsic value is the built‐in payment and storage network. A bitcoin is a bitcoin is a bitcoin. It's math and, therefore, highly uniform. There is no purity test for bitcoin. Bitcoin is accepted at exchanges worldwide, thousands of stores, and places of business. No one can buy a plane ticket or cup of coffee with gold, but they can with bitcoin. Finally, it's scarce – even more scarce than gold. There will only ever be 21 million bitcoin mined. Gold continues to be mined and will continue to grow its supply.

Bitcoin as digital gold will allow us to build credit, currency, lending, financing, and equity ownership just as gold allows us to build these things in traditional finance. Bitcoin as gold is key to building stablecoins, decentralized finance, and a host of digital financial infrastructure needs we will discuss throughout this book.

A Global, Public Payments Network

Bitcoin, at its core, is a worldwide public payments network. It's public infrastructure that allows anyone in the world to pay anyone else, without a bank account, without approval from a central authority, and without the need to worry about borders or trust or any of the past barriers. That's the innovation! This is a breakthrough from the past. It's this innovation that allows us to do something we couldn't do prior to the invention of Bitcoin.

Prior to Bitcoin, the only real way to send a payment internationally was through a set of middlemen, all taking their cuts and adding friction (cost) to the process. Ask anyone who's tried to send remittance or wires to another country. It can cost anywhere up to 20% in fees and take days. Even wires can take days.

Back in the 2000s, I ran a software services company. We were headquartered in LA, but we had acquired a software developing company in Monterrey, Mexico, that had a few dozen developers. The service was called nearshore, distinct from offshore. With offshore software development, you're connecting with a team in India or Russia, someplace that's on another continent, as the name implied. Nearshore is done in the Americas, where you're connecting with a team in another country, but you're using the same time zones. There are a lot of benefits to nearshore over offshore. Invariably, I'd be sending a wire every month to our development center down in Mexico. The wire might take only an hour (or two) to send, but the settlement typically took over a week. There was human intervention throughout the review process and with both banks. We were charged wire fees and even though we had a bank in Mexico with the account in U.S. dollars, our Mexican counterparts would need to convert U.S. dollars to Mexican pesos at some point to pay expenses and salaries. Of course, foreign currency transactions take 5–8% when converting so right off the bat they were losing money just on conversion to local currency. The transactional pipeline was like a clogged artery due to intermediaries and fees throughout the process. Conversely, with Bitcoin, the transaction and settlement process can happen, typically in under 2 hours. In 2022, we're coping with currency fees and big volatility with the price of bitcoin in various sovereign fiat currencies, but we can envision a day when most transactions can stay within the Bitcoin ecosystem. Even with those conversion fees, Bitcoin doesn't require a bank account or permission from anyone to use. Anyone can create a wallet for free, thus reducing friction and inefficiency. More simply put, if you have a smartphone or a computer, anyone can send money to anyone else elegantly and efficiently.

Public versus Private

We discussed in Chapter 1 the pseudonymous nature of Bitcoin, which is a public blockchain. This means that anyone can use it and all data is visible. Public blockchains, for example, include Ethereum, Solana, and Curve. But there are also private instances of blockchains. You can think of an analogy to the Internet where the Internet is a public network of computer networks and an intranet is a private network. A company intranet is only accessible by individuals in that company. Public means anyone can access it; private means only a limited number, generally defined by a company, group, or organization, can.

Private blockchains, such as Hyperledger from IBM, create private solutions for supply chain management, cross‐border trade, banking solutions, and digital ticketing solutions. It's permissioned, meaning you'll need to create an account and get company permission to use the system.

Consider the similarity of the analogy to that of private intranets and the public Internet. Which of the previous made the biggest difference to society during the Age of Information, intranets or the Internet? The answer is that the Internet's public infrastructure made the biggest difference. Like public blockchain, the Internet doesn't require permission to use. It significantly reduced friction in communications, for it's the Internet that allows anyone to send an email or post a web page and communicate nearly freely with anyone else in the world. That was the power of the Age of Information. Well, we have another amazing technology here, and understanding these fundamentals will make you a better investor.

Economic Empowerment and Bitcoin

We're going to unpack this later in Chapter 15; however, it's worth noting that, in the same way that billions of human beings from Calcutta to Cape Town to Chicago carry an affordable cell phone, Bitcoin is leveling access to digital money transactions for humanity.

With Bitcoin, anyone with a smartphone can put money into a savings account, apply for a loan, and make or receive a digital payment. This is revolutionary, especially in countries where it's almost impossible for ordinary people to obtain a bank account, credit, or loans. A Nigerian who lacks access to a bank account but wants to receive money from relatives abroad without paying exorbitant fees can do so easily, quickly, and cheaply with Bitcoin. There are thousands of other commercial applications that can improve the lives of billions of people.

This isn't just in emerging markets, either. As noted in a Forbes interview with the always eloquent Chris Giancarlo, affectionately known as Crypto Dad for his early support of cryptocurrencies as former commissioner of the Commodity Futures Trading Commission,2 and current president of the Digital Dollar Foundation:

In the online world, the digital dollar gets more interesting. Basically, if you shop online today, you can't use fiat currency for peer‐to‐peer payments. You must go through intermediaries. A digital dollar, however, would give you the same ability to make direct peer‐to‐peer payments online with digital dollars that you can in the physical world with paper currency. And not just for online shopping.

Take a grandmother working in Philadelphia who has a granddaughter in the Philippines, for example. The granddaughter back in the Philippines sends her grandmother a text message with pictures of her birthday party blowing out birthday candles. That photo is received by the grandmother in an instant. But when the grandmother wants to send $100 back to her granddaughter as a birthday gift, it takes days and costs anywhere between $7 to $17 dollars in transaction fees. With a digital dollar, the transfer would be the same as a text or a photo, all in an instant of time. And when the money arrives, it is $100 worth of immediately spendable U.S. money, and no intermediary is needed to verify the funds or charge processing fees. A digital dollar would be very effective as a means of greater inclusiveness for communities whose needs historically have been underserved by retail banks and financial service providers.

Chris is referring to a digital dollar here, which is on the agenda of the U.S. government, but the same analogy holds true for bitcoin as well as stablecoins and any other crypto asset today. In fact, one could argue that we wouldn't even be talking about a digital dollar had Bitcoin not jumped onto the scene and grown into the juggernaut it is today.

A Regulatory Head Start

It's important to acknowledge that Bitcoin and Ethereum, the two most popular crypto assets, have already passed regulatory scrutiny with officials from both parties, the CFTC and the SEC.

The CFTC monitors virtual currencies for fraud and risk and publishes substantial guidance for the investing public. As stated by the CFTC, “While its regulatory oversight authority over commodity cash markets is limited, the CFTC maintains general anti‐fraud and manipulation enforcement authority over virtual currency cash markets as a commodity in interstate commerce.” We applaud the CFTC for its innovation and leadership in bringing legitimacy to Bitcoin and Ethereum. At times, the SEC and CFTC have effectively coordinated oversight, monitoring, and enforcement in cracking down on fraud and Ponzi schemes. A great deal of what will happen with the regulation of crypto protocols will unfold over the next few years.

We saw one of the more promising 2022 bills was sponsored by Senators Debbie Stabenow (D‐MI) and John Boozman (R‐AR), giving the CFTC the leading role in overseeing the two largest cryptocurrencies and the platforms on which they are traded. The bill passed the Senate in August 2022; this bill or parts of it are likely components of what will ultimately become law.

In the bill, “oversight of the remaining cryptocurrencies would be divided between the CFTC and the Securities and Exchange Commission though the process for making those determinations is not yet clear,” the Washington Post reported. “The two agencies have been jockeying for more authority over digital assets, contributing to confusion in Washington over how to classify and regulate cryptocurrencies and the economy that has sprung up around them. The bill aims to provide some clarity by deeming as commodities both bitcoin and ether which together account for roughly two‐thirds of the cryptocurrency market.”

Bitcoin versus bitcoin

A quick note on capitalization. While we all know the rules for capitalization in writing, the rules are a little different for the world's most popular digital asset. In writing, you'll often see references to Bitcoin and also references to bitcoin. I can say that when I first saw this, I was quite confused and thought the inconsistencies just to be mistakes (that everyone seemed to make). Nope! As it turns out, these two things are distinct.

Bitcoin refers to the actual blockchain, a network of hardware running specific software. It's the whole enchilada. We don't often think of it this way, but it is really the most correct way to view Bitcoin: as a worldwide payment network. The other use, “little b” bitcoin, refers to the actual asset. So, when you see “Jim sent Jake one bitcoin,” you can be sure that the reference is to the actual coin itself, not the entire network.

Getting Started with Bitcoin

Okay, so maybe at this point you've done all your due diligence and you want to actually own some crypto for yourself. We know that this can be daunting, so for those looking for a step‐by‐step checklist, this section is for you.

Exchanges

To begin with, let's look at purchasing directly off of an exchange:

- Do your homework and pick an exchange. If you invest a modest amount, you must choose a cryptocurrency exchange or trading service. You can buy, sell, and hold bitcoin and other cryptocurrencies through the exchange. We recommend using an exchange that allows you to withdraw your crypto to your online wallet, which is the most secure option. While there are many trustworthy exchanges, Coinbase, Kraken, and Gemini are the most user‐friendly, with reasonable fees and robust security. Binance caters to a more advanced trader, offering more serious trading functionality and a better variety of altcoin choices but is not available to citizens of the USA and many others. CNET and Forbes are credible sources for updating your list of exchanges. CNET recommends Bitflyer, Gemini, Coinbase, Kraken, and crypto.com as the “best crypto exchanges let[ting] you easily trade coins and tokens while keeping your assets safe and your fees low.” Forbes Advisor cites Gemini, Bityard, Kraken, crypto.com, and Coinbase as their “best for beginners,” and adds KuCoin to their best exchanges list. We expect that this list will evolve over time, so be sure to check in with a reliable source to see who is currently recommended.

- Register on the exchange. You will generally need to provide the same personal information and payment details that you would for a brokerage or bank account. While the philosophy of anti‐authority and anonymity behind crypto is essential to some, the reality is that to use a major exchange and to ensure that your funds don't get lost or locked up, you'll need to go through a know your customer/anti–money laundering process, also known as KYC/AML. This process allows you to be identified while at the same time allowing the exchange to confirm that you are not a bad actor. We recommend that you avoid exchanges that do not require your identification, as these are far more likely to be security risks.

- Place an order. After choosing an exchange, you will need to put money into your account before beginning to invest. When you've funded your account, you're prepared to make your first purchase. Various platforms have slightly different protocols. Some, like Coinbase, are designed for the beginner and walk you through step‐by‐step; it's very much like buying a stock through an online broker. Others, like Coinbase's pro edition, allow you to view charting and create more complex types of orders, and have lower fees. Unlike a stock, you can purchase any amount of crypto. If you have $100, you can buy $100 worth of bitcoin, ether, or any other crypto. The exchange will do the math and you will have crypto deposited in your wallet on the exchange. (More on wallets in a second.) We recommend that you start with the basics, then move up to the more advanced exchanges where you can take advantage of market, limit, and stop‐limit orders. It's also worth noting that many exchanges provide ways to set up recurring investments, allowing clients to dollar‐cost average into their assets of choice.

Your Wallet

That should be pretty straightforward, but now you have some options. You can keep your funds on an exchange, or you can move them off the exchange and into your own wallet. A wallet is a cryptographically secure address that you control, and this is one of the main points of blockchain technology as it allows you to hold your funds directly and outside of an exchange. This personal wallet ensures that you have control over the private key to your funds.

If your funds are in your wallet, then you are the responsible party and, importantly, no one can take them from you. This of course requires a certain level of responsibility, just like keeping cash in a safe in your own home, so you will need to keep that in mind. When you open a wallet, you will get a public key and a private key. The public key allows anyone to send funds to you; the private key should be kept secret and safe, and this key allows you to send funds from the wallet. Always keep your private keys safe, for if you lose your key, you lose access to your funds. This doesn't mean that you actually lose the money, but it would be inaccessible.

You want to be sure to understand that exchange‐based wallets, like wallets on Coinbase, are only as secure as the exchange itself. “Exchange wallets are custodial accounts provided by the exchange. If the exchange is hacked, investor funds are compromised,” Investopedia explains. This is because, just like with your money at a bank, the exchange is a counterparty. Of course, this risk exists in any situation where someone is holding your funds, such as those who were nipped in the savings and loan crisis where approximately 1,043 out of the 3,234 savings and loan associations in the United States closed from 1986 to 1995, some leaving depositors without recourse to access their funds.3 This leads us to the phrase “not your key, not your coin,” which is heavily repeated within cryptocurrency forums and communities.

When first considering this concept, we were confused ourselves. How do my funds get transferred into a digital wallet? The answer is that they don't. Wallets don't actually hold your tokens. Instead, they hold your keys and allow access to your funds on the blockchain. Wallets can be “hot” (software‐based) or “cold” (hardware‐based and not connected to the Internet). Think of a hot wallet as a software wallet that resides on your computer or phone. These wallets generate the private keys to your coins on these Internet‐connected devices and store them for you so you don't have to keep remembering them. A cold wallet is hardware‐based, resides offline, and holds your private key on a software‐protected file inaccessible to the Internet. There are many popular software wallets; Trezor and Ledger are the two most well‐known. The big advantage of a hardware wallet is that your private keys at no time encounter a network‐connected computer or potentially vulnerable software. For those who want to simplify this process, there is one other option, known as a “paper wallet,” which prints your public and private keys on paper, which can then be laminated and stored. A big disadvantage of paper wallets, however, is that you are required to enter your private key every time you wish to send funds, and any time you type your key into a computer or phone there is risk, either from Internet threats or nosy neighbors. We don't recommend paper wallets.

Wallets have one failsafe to recover private keys. When a wallet is created you will be presented with a seed phrase. A seed phrase is a list of 12 to 24 words that are unique to the wallet. This is the one artifact that you must save when creating a wallet, which many people store on paper and leave in a hidden or secure location. There are metal kits that can be purchased that allow you to store your key (literally, the words printed in metal) so that they cannot be destroyed by fire, water, and so on. If you ever lose access to your wallet, you can recover the wallet with your seed phrase.

Wallets, just like the wallet in your back pocket, require a certain amount of responsibility. If you lose your physical dollar‐bill wallet, you lose the money inside it. This is the same for your crypto wallet, but this is the trade‐off that we have. If we want to control our own money, then we have to take the proper safeguards. Such is the price of autonomy!

PayPal and Other Secure Options

Bitcoin, ether, litecoin, and bitcoin cash can be purchased directly through PayPal, and Venmo. Crypto purchased on Paypal may be transferred off Paypal, however crypto purchased on Venmo must, for now, stay on Venmo. According to Venmo’s website: “At this time, it is only possible to buy, sell, and hold crypto on Venmo. Venmo does not currently support using crypto as a way to pay or send money on Venmo, using crypto as a way to make purchases, or peer‐to‐peer crypto trades.” So your crypto will reside on the Venmo network until such time as you choose to convert it to cash.

Bitcoin ATM

We collectively marveled back in 2018 when, upon driving down the street, we saw a “Bitcoin ATM” sign in our local liquor store. Sure enough, these machines exist, and they function much like your regular ATM, except that instead of dispensing cash, a Bitcoin ATM requires you to insert your cash into a machine, which it processes, then converts it to bitcoin, which is then moved to your online wallet. As of this writing, about 200 Walmart stores have these machines at their coin kiosks. The machines charges you a purchase and conversion fee for exchanging your money to bitcoin. It is worth noting that both fees are pretty steep compared to those of other options, but these machines allow cash to be converted without going through an exchange. Ah, how the world has changed.

On Risk

Many years ago I was an avid skydiver, and over the years I've amassed 320 jumps, including some 20 with a wingsuit. Skydiving is one of the most exhilarating and, strangely, peaceful experiences I have ever had. Once I leave the plane and surrender to the pull of gravity, for me, it's like feeling one with everything in the world. Regular skydivers will generally share their version of this, but it all just comes down to one thing: the awesomeness of being in the air. In order to skydive you have to sign a waiver because, the fact is, throwing yourself out of an airplane is risky. It turns out the actual incident rate is much lower than for things we do every day, like driving in a car. In fact, you are over 4,000 times more likely to be in a fatal car crash than a skydiving accident. You don't need to sign a waiver for getting into a car, but, let's face it, that's commonplace and stepping into an uncommon environment such as skydiving is just unusual, so it gets people's attention. A death from skydiving could be from the cause of equipment malfunction, an error during the skydive, an error of the pilot of the plane, someone running into you and knocking you out, a dust devil (tiny tornado), a rock falling out of the sky, and so on. The point is, when you arrive at the skydive, you'll sign a waiver, which is a very scary piece of paper letting you know that this is risky and if anything happens to you, regardless of what it is, then it's on you. If you want to jump, you take the responsibility. If you don't, you don't.

Know Your Risk Envelope

While investing in crypto assets is not fatal, of course, none of this is risk free. You need to be aware that money could be lost because of market conditions, your error, counterparty error, technology error, and so on. It is important to keep this in mind. Should you choose to invest, and many do, be aware that you could, for a variety of reasons, lose all of your investment. This is also true of just about any kind of investment, but because crypto is new and still maturing, it gets a lot of press, mostly about the bad things that happen. In alignment with this, the CFTC put together an advisory that is not dissimilar to that skydiving waiver, designed so that you can make an informed choice. Here is an excerpt of this advisory:

The bottom line is this: Investing has risk, so ensure that you operate inside of the parameters you are most comfortable with, and never invest more than you are willing to lose

Notes

- 1. https://bitcoin.org/bitcoin.pdf.

- 2. https://www.forbes.com/sites/jasonbrett/2020/04/26/why-chris-giancarlo-considers-a-digital-dollar-mission-critical-for-the-world/?sh=55b74ec43c41.

- 3. https://en.wikipedia.org/wiki/Savings_and_loan_crisis#Consequences.

- 4. https://www.cftc.gov/LearnAndProtect/AdvisoriesAndArticles/understand_risks_of_virtual_currency.html.