1

What's the Big Deal About Blockchain?

Everyone is talking about crypto, the colloquial term for digital assets. Love it or hate it, it seems to be on everyone's lips. The fact is that crypto is now mainstream. From Main Street to Wall Street, your street to our street, everyone has an opinion. We would often go present to different groups, ranging from trade shows to investor summits, and even as little as three years ago people looked at us like we were aliens. Truly – aliens bringing some unfathomable concept and, clearly, not of this Earth. Things have changed quite a bit over the past few years.

Bitcoin is the most popular and well‐known of the crypto assets built on a blockchain. Yet Bitcoin is only one of thousands of crypto networks, applications, and protocols empowered through blockchain technology. Stories of teens driving Lamborghinis, or businesspeople who invested, then lost, all of their bitcoin by throwing away their wallet accidentally or forgetting a password permeated throughout. Riches were made and riches were lost, and everyone seemed to know about this volatile new asset. During this process, crypto has become somewhat of a dirty word. There is so much baggage around it that it's hard to actually cut through the noise and, with all the hype about making money, we see that the fundamentals and foundations of this amazing technology are generally overlooked and misunderstood. So let's start by understanding that blockchain technology is a breakthrough.

Blockchain, recently made possible through decades of computer science and mathematical innovations, enables computers in different locations to access, verify, and share their data. By doing so, blockchain technology overcomes one of the biggest computer software challenges of all time: how to share information quickly and reliably among separate, unaffiliated entities without the involvement of a centralized gatekeeper. This is known as the Byzantine Generals Problem and is discussed thoroughly in Chapter 12.

The breakthrough in solving this problem cannot be overstated, as it allows peers to transact business without an overlord. That may seem rather ho‐hum to you, but consider the simple act of handing your friend a 20‐dollar bill. You don't need to go to a bank or get permission; you can just do it. Well, before blockchain the only way to digitally exchange something was to go through that central third party. Now, you can just do it directly – like handing your friend a 20‐dollar bill. Four unique characteristics make blockchain revolutionary. Blockchain is:

- Decentralized: No central authority controls transactions occurring over the network.

- Immutable: Posted transactions are there forever and can never be deleted or changed by anyone.

- Transparent: Every transaction on the blockchain is public record and can be viewed by anyone on the network.

- Authenticated with cryptography: Blockchains use complex mathematical codes to store and transmit data to ensure the legitimacy of each transaction and participant, just like an old‐school signature. Every participant in the cryptoverse, via their crypto wallet, has a unique digital signature that's impossible to forge.

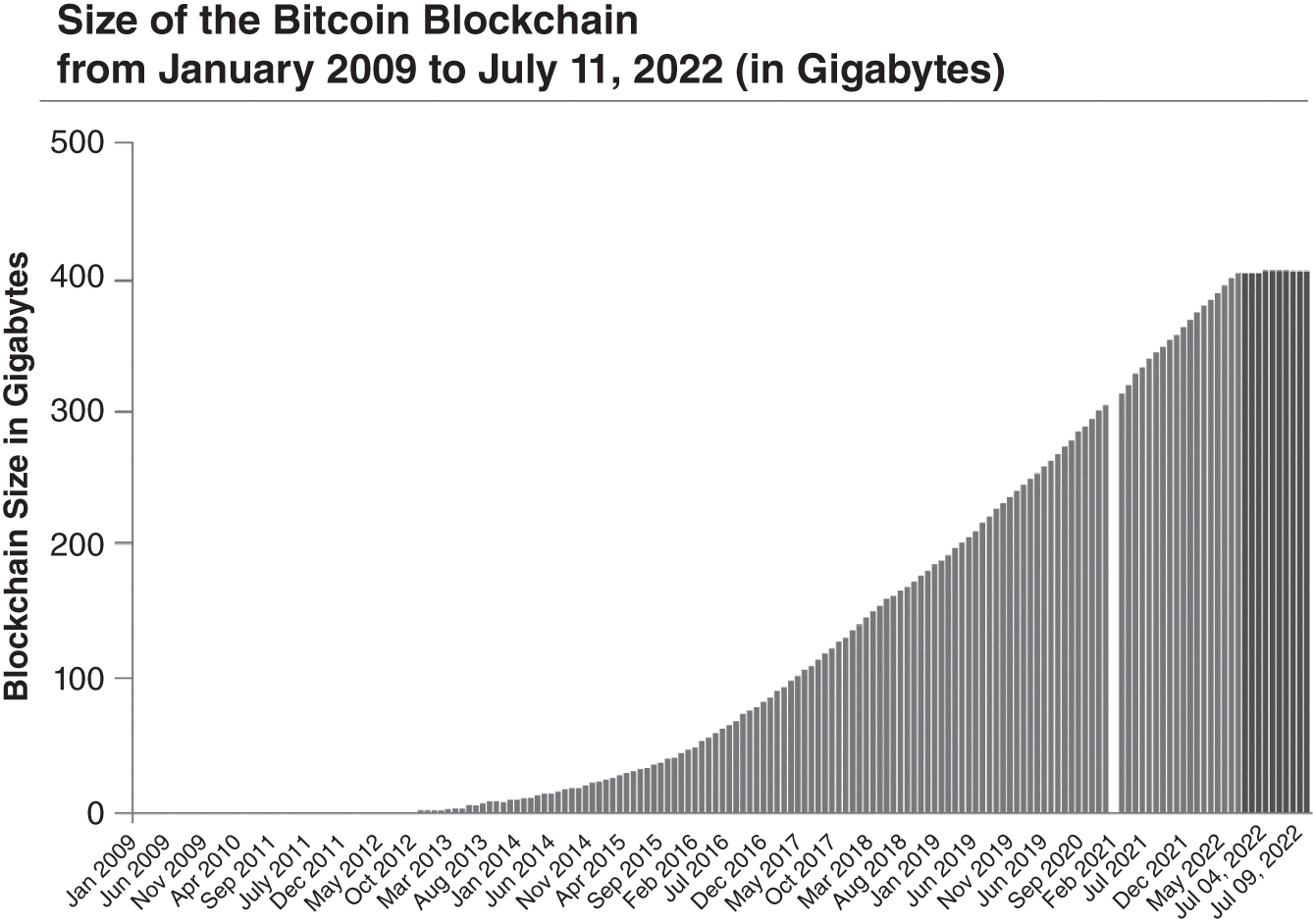

These features of blockchain position this technology as the biggest technological disruptor since the Internet. Blockchain, however, unlike many technology breakthroughs, is actualized by and empowers those who use it. As Vitalik Buterin, co‐founder of Ethereum, said, “Whereas most technologies tend to automate workers on the periphery doing menial tasks, blockchains automate away the center. Instead of putting the taxi driver out of a job, blockchain puts Uber out of a job and lets the taxi drivers work with the customer directly.” This is what we mean by peer‐to‐peer. To start giving this context let's look at Bitcoin, which is a blockchain that is a worldwide peer‐to‐peer financial network. It's the network and interaction directly between two people that is really important, and, as noted in Figure 1.1, the Bitcoin blockchain has grown significantly since its inception in 2009.

Figure 1.1 Bar Chart of Bitcoin Blockchain Size

Source: Blockchain © Statista 2022.

A Blockchain Is a Specialized Database

Google began when two graduate students in computer science and mathematics at Stanford, Larry Page and Sergey Brin, prototyped their search engine called BackRub (seriously). Page and Brin weren't planning on launching one of history's most successful companies. Rather, as computer scientists and academics the two friends saw the World Wide Web as a system of citation. In the world of academia, credible research is valued by how the author's work responds to citation (or reference), and by how future projects and publications cite the author's article or book. Well, the web to Page and Brin was simply a vast catalog of articles and information, but, without a way to cite (reference) other works, it would not realize its true potential. To Page, “the entire Web was loosely based on the premise of citation – after all, what is a link but a citation?,” John Battelle wrote in his landmark book The Search. If Page could “divine a method to count and qualify each backlink on the Web, as Page puts it, ‘the Web would become a more valuable place.’”

This may be strange now, but Page, Brin, and other computer scientists at the time saw the Internet as a graph. Each computer was a node, a data point, and each link on a web page connected the nodes. The result: “a classic graph structure.” Brin and Page envisioned a search engine as perfecting the academic citation model.

“Not only was the engine good, but Page and Brin realized it would scale as the Web scaled,” Batelle wrote. “Because PageRank worked by analyzing links, the bigger the Web, the better the engine. That fact inspired the founders to name their new engine Google, after googol, the term for the numeral 1 followed by 100 zeroes. They released the first version of Google on the Stanford Web site in August 1996 – one year after they met.”1

We tell this story to make a point about innovation breakthroughs. In our daily lives, as we go about doing our jobs and getting stuff done, Google can seem like a utility service that mysteriously materialized on our computers. Of course, if we take a moment and think about it, we can dredge up a few relevant facts about how search engines came into our lives. Maybe inventing the wheel was an exception, but most technological breakthroughs happen as discoveries rooted in well‐established systems begin to take hold. Jared Diamond observed that technology has to be invented or adopted. We say it is almost always both. Blockchain technology, then, was first invented, then adopted.

Decentralized

It can be easier to start understanding blockchain as a new kind of database where data is stored on individual, independent computers that exist in locations all over the globe. This makes a blockchain network distributed, because it consists of many computers that are not all in one location. That's pretty easy to grasp.

Decentralization is a little different, however, because blockchains are also decentralized. The best way to think about decentralization is to think about your photos on your laptop. If you drop your laptop in the ocean, you've probably lost your snapshots of vacation on the Big Island sipping a frothy, fruity rum drink. You may retort “not so!” because you have a backup somewhere.

That's great; however, if that backup goes kaput, then, once again, your pictures of that mai tai in Hawaii are gone. A next step, of course, would be to have all your photos uploaded to “the cloud” – a central location – which then allows us to download to multiple devices. In this, we're getting closer, but we still have that pesky central location. If that location falls into a sinkhole, the means to synchronize across all devices fails. What if there were another structure that didn't rely on single points of failure? In this example, what if there were 100,000 computers that all had copies of your photos (for some of you, that's a scary thought, so let's just pretend it's only the photos you want people to see), and every time you take a new photo, every computer gets a copy. That is decentralized. No single point of failure, no point more important than any other. That is decentralization. Blockchains are decentralized because every computer can access all of the information on a blockchain, which makes them very robust. There is no central entity controlling any given blockchain interaction; it's all kept on track with ingenious cryptography and computer software.

Immutable

Almost every database technology in use today allows transactions to be altered or overwritten. This includes everything from bank balances to health records. In a blockchain, by contrast, once a transaction is written into a block it is there forever and can never be deleted or changed by anyone. Period. So, if Bob sends Sally one bitcoin (BTC), once that transaction is confirmed, Sally has one BTC. That transaction is irrefutable, written in stone, and can never be changed. It's written on the blockchain. The computers in the network validate it (agree), and everyone has access to that transaction record. If Bob says it didn't happen – and even if Bob takes Sally to court (that BTC may be worth $1 million someday!) – we could look for the transaction on the chain and know the facts. There are few places in the world where this kind of certainty exists, and it's essential not only for currency transactions but also for transactions of any type.

Immutability becomes very interesting when you're keeping records over long periods of time or conducting business that depends on a shared idea of value, title, ownership, or scarcity. Our current traditional economy requires trust at every turn. You trust the credit card machine company to debit the correct amount from your bank account when you are at the grocery store checkout counter. It would be best if you trusted that the store's bank and payment systems will operate as expected. You need to trust that the banks will honor their agreements. And so on and on and on. It's the whole reason brands are so valuable. They are marks of trust.

In the future crypto economy, trust will be less critical because you won't need a third party to facilitate and settle transactions. When you can deposit money into your cryptocurrency wallet, you're assured that the blockchain keeps track of everything. If you are interested in a work of art, you can see its provenance (the whole history of ownership and origin) on the blockchain. No third parties needed. No need for trust. Instead, everything is authenticated cryptographically. With applications built on blockchains and cryptocurrency, transactions occur peer‐to‐peer.

Before Google, the citational credibility of a web page was a black box; the Google search brings scientific transparency to the question of trust – it allows you to find and reference data all over the world. The blockchain provides its own brand of transparency into the custody of currency, supply chains, and sensitive data such as medical records.

Transparent

Another seminal quality of a blockchain is transparency. Everything that is ever written on the chain is visible to anyone at any time. This, in and of itself, is a marvel. You see, almost every other database in the world is exactly the opposite. Data is stored and you only get to see whatever the owner of the database wants you to see. In the blockchain world it is the opposite, and that is one of the great strengths of this technology.

Let's say that Fred sends one bitcoin to Mary. This will be written on the blockchain, and no one can ever deny that this occurred. When you combine this with the concept of immutability, this becomes a powerful recordkeeping system and an unalterable chain of title. Whether used for tracking products from farm to table, validating the ownership of any physical good, from art to autos, or affirming accounting entries and money transfers, there is no question of the activity that has taken place and, importantly, it is visible to anyone.

We want to be clear at this point that it is the transaction that is visible; your identity is not. I was recently sending a friend a transaction using Venmo, which has this feature that your transactions can be publicly visible. That's weird. I don't know about you, but generally I don't want the whole world to know when I send money to someone. So, in the Fred/Mary example, we don't have to worry about this because blockchains are pseudonymous, meaning that while your transactions are visible, your identity is not (unless, of course, you disclose it publicly, but that is your choice). Everyone can see that a transaction happened, but they do not necessarily know who the parties on either end of the transaction are.

No, this does not make blockchain a hotbed for criminals. As we will learn in Chapter 9, money has to come on to the chain somewhere and off the chain somewhere. It's possible to trace the flow of money to these endpoints, which tend to be tied to humans. In almost all cases your activities can be traced back to you. Frankly, we want this to be the case because this allows us to confirm ownership, chain of title, transaction activity, and so on. All of this and more will be discussed further as you dive into this work, but the important part is that this is the best of both worlds. You can transact while generally maintaining anonymity and yet there is still a permanent record that can be traced if needed.

Cryptographically Secure

Our current economy still relies on the power of our unique signatures. We put our “John Hancock” on something and that is our bond, our agreement. Signatures have been so important up until now that some states, like Texas, still require a “wet” actual physical signature on important documents like mortgages. The challenge with digital signatures has always been the concern that they can be copied. Enter cryptography.

Cryptography is the art of using technology to secure data so that it can only be accessed by the desired party, and such parties have what is known as a “key.” Think of cryptography as a lock on your data that can only be accessed with the right key. Blockchains like Bitcoin also require signatures in order for transactions to occur. The reason we can trust them is because blockchains use cryptography techniques and the only ones who can authorize a transaction are the ones who hold the specific keys. Bitcoin uses complex mathematical codes to store and transmit data to ensure the legitimacy of each transaction and participant. They are unique, just like an old‐school signature is unique. This brings us to your wallet. A wallet is a place where crypto assets can be stored. They are cryptographically secure addresses (just like your house has an address) that anyone can send assets to. But the only way to transmit assets from a wallet is with your key. When you enter your key, you are “signing” a transaction. Every key/wallet combination creates a unique digital signature that's impossible to forge. We discuss wallets in more depth later in Chapter 2.

The unique digital signature in a blockchain is authenticated and can't be repudiated; the hash is unique to origin, so one can't later deny sending a message. The mathematical nature of the hash can't be reversed, and no two or more messages have the same coding. Each is locked, like a chain, bearing an invisible tag like a barcode that cannot be removed.

We all know that natural scarcity and rarity create value. Cryptography not only makes it easier to establish the authenticity of someone conducting a transaction, it can also create verifiably rare digital assets that mimic scarcity rarity in the natural world, like gold and diamonds.

Crypto apps built on a blockchain, like Bitcoin and Ethereum, require a “consensus mechanism” to settle transactions and secure the network. Bitcoin uses a proof‐of‐work (PoW) consensus mechanism that involves using powerful computers (aka bitcoin miners) running nonstop. Right now, it takes an enormous amount of energy and a certain amount of expertise and dedication to mint a bitcoin, for example. Just like a one‐of‐a‐kind, handmade couture gown takes more time (and costs more) than a mass‐produced gown, bitcoins are not easy to make. Bitcoin's creator engineered scarcity by designing the software to stop making bitcoin at 21 million coins.

But PoW is only one consensus mechanism. Another is proof‐of‐stake (PoS) – and it is not energy‐intensive. Instead, it's based on users staking their crypto assets (and risking losing them) to secure transactions on the blockchain. For example, the popular blockchain Ethereum is transitioning to PoS. Once Eth 2.0 is fully in production, Ethereum will be the second‐biggest blockchain, and it will be running on PoS. In Chapter 11, we'll explore the ongoing evolution of these two technologies for forging coins.

Nonmoney Examples of Blockchain Technology

Bitcoin is the king of blockchain and everyone knows it. Bitcoin is a money use case; that is, it is designed to be currency and do the things currency would do. We'll dive deep into this in Chapter 2; however, the fact that bitcoin is money is a big part of the reason many people think that all crypto is money. The fact is, there are endless applications for blockchain technology. We'll discuss this throughout the book but just to get you started, the following are three examples, which we find compelling, that are in use today.

Decentralized Finance

One of the first successful uses of blockchain technology is decentralized finance, known as DeFi. We discuss this more fully in Chapter 4, but as an overview, DeFi platforms allow people to lend or borrow funds from others, speculate on price movements on assets using derivatives, trade cryptocurrencies, insure against risks, and earn interest in savings‐like accounts. DeFi makes it possible for anyone with a smartphone to put money into a savings account, get a collateralized loan, and make or receive a digital payment. DeFi platforms are basically software programs that run 24/7 and allow anyone to use them – a far cry from the protocols at most banks. This makes DeFi a free‐market playground of crypto apps that many are enjoying and, in the process, making money. As a caution, however, if you choose to explore this world of protocols, we just want to send a word of wisdom to always be prudent with your money, never invest more than you are prepared to lose, and always be aware that scammers are out in force, just as they are in most other marketplaces.

Supply Chain Management

Blockchain technology is already being adapted into our supply chains, markets, information technology systems, and points of purchase. There are growing cases where this technology reduces fraud in the counterfeiting of luxury brands and high‐value goods, helps companies recognize how ingredients and finished goods are passed through each subcontractor, and lessens losses from counterfeit and gray‐market trading.

“Major brands have already begun partnering with tech firms and other entities in response to rising demands for improved brand protection. LVMH (Louis Vuitton SE), for instance, working closely with Microsoft and ConsenSys, has created Aura Ledger to provide proof of authenticity of luxury items and trace their origins from raw materials to point of sale and beyond to the used‐goods markets,” reports GlobalTrade, the trusted logistics and global trade outlet. Pretty soon, when you see that Louis Vuitton bag that should be $10,000 for sale for the bargain price of $1,500, you won't just need to rely on your gut and logic to determine that it's not real – you'll be able to use blockchain technology to verify this very thing.

It's not just luxury brands that are stepping in, but the biggest business drivers on the planet. The buttoned‐down blue‐chip giant, IBM, for example, has an entire practice devoted to blockchain supply chain solutions. Consulting giant McKinsey & Company is urging clients to consider integrating blockchain. According to the none‐too‐radical business analysts at Deloitte, “Blockchain‐driven innovations in the supply chain will have the potential to deliver tremendous business value by increasing supply chain transparency, reducing risk and improving efficiency, and overall supply chain management.” Among many examples, companies have integrated blockchain to track the responsible sourcing of tuna in Indonesia, secure digital media usage and sharing rights, and manage business‐to‐business (B2B) trade and supply chain finance products.

The Society for Human Resource Management documents how blockchain can verify identity, credentials, education details, and payroll management. And we have insider reports that media companies are adopting blockchain technology to eliminate fraud, stop piracy, and protect intellectual property rights of content.

Ultimately, this is where the power of a peer‐to‐peer, immutable, decentralized network comes into play. Transactions are permanent, traceable, and aren't subject to manipulation. This makes them perfect for this job.

Additional Examples

This is just the beginning. Blockchain technology is the foundation for Dapps (decentralized applications), platforms, and protocols, which in turn make it easy to send and receive money across borders, clear and settle financial transactions, manage supply chains, enable device‐to‐device transactions in the Internet of Things, create more reliable property and asset registries, and improve record‐sharing in health care, among others. The benefits – greater speed, transparency, lower cost, and ease of access and control of one's own data – offer tremendous opportunities for expanding global commerce and improving the lives of everyone on the planet. All of this can be a little dry, but we believe it's important to understand the fundamentals – this will make it much more valuable in later chapters as we explore the breakthroughs. Rather than stay theoretical, in the next few chapters, we will introduce the most important applications for blockchain technology that are already proving useful and effective without controversy.

Blockchain Technical Components

In order to really understand Bitcoin or any blockchain, we need to have a fundamental understanding of how a blockchain works. Unfortunately, most people skip this step and simply want to jump on the bitcoin train, but understanding how a blockchain works will shape your entire investment strategy. These are the fundamentals that most skip, so this is where we are going to start.

A blockchain is software that runs on a computer server just like any other server‐based application, just like a web server hosts a website, for example. The software components of a blockchain are programmed in code. These include blocks, which store transactions (data), the hashing function, which organizes the transactions and allows for searching/sorting, and the consensus mechanism, which keeps all the nodes in the network synced and accurate and allows transactions to be approved. The software also includes any functionality to create a wallet or sign (approve) a transaction.

The server is the computer hardware that may run one or more instances of the blockchain software. An instance of the software is a node. The network is merely the connected servers, each of which may have one or more nodes running on it. Since anyone can run the blockchain server software, the network is a globally decentralized network that runs on the Internet, just like other server‐based software.

Transactions

A transaction is a single entry on the public ledger. It's broadcast to all the nodes in the network. Any time a user sends a token from one wallet to another, that's a transaction. A transaction is data that is recorded inside a block, and a block will have one or more transactions stored in it.

The most important function, and where the big innovation lies with blockchains, is consensus. Consensus is the process of all of the nodes agreeing on whether a transaction is valid or not. In order for a transaction to be considered valid, 51% of all the nodes must agree. If they do, the transaction is grouped together with other transactions and permanently stored in a new block, which all nodes then have a copy of. This process is called gaining consensus and we'll discuss this in more detail in the Consensus Mechanism section later in this chapter. The critical part is that consensus allows blockchains to stay in sync, protect the data, and know that all the other nodes and copies of the public ledger are identical within the entire system. This is unprecedented and allows us to have a peer‐to‐peer system without requiring a trusted third party like a bank or a company. As peers, the nodes can agree and confidently confirm that the transaction is valid. We'll unpack this further in a later section.

Blocks

A block consists of a collection of ordered transactions, and each block is then connected to the last minted block. This is why we call it a blockchain, because it is an ever‐growing linked set of blocks. Now, we mentioned ordered transactions. Order is important because if Sofia sends Bill one bitcoin and Bill sends Otto one bitcoin, Sofia's transaction must happen first. That may seem basic, but it's really a fundamental point.

The software only allows the creation of a block, which it then links to the previous block. It cannot alter transactions once the block is written, so the entire data structure has the property of being immutable – that is, it cannot be changed over time. This is a compelling characteristic because it allows the software to enforce the committed information. We can know with certainty that no one came in and tinkered with any element of the system to change any amounts or other aspects of the transaction. This is very different than a traditional data structure like a database, where records can be edited or deleted by design. Pretty much all data that we store is in a database of some type, and as such one has to trust the company, the database system administrator, the company that made the database, and so on. There are many layers of trust required. With a blockchain, the environment does not require trust of a third party. It is trustless.

In the traditional/legacy economic system we've had since the beginning of time, every participant in an economic transaction would require some form of trust. In the new decentralized economy, trust is no longer required.

Hash/Hashing Function

A hashing function isn't as scary as it sounds. Put simply, the hashing function provides a number that helps data be structured. This is called a hash, and delivers several features. First, the data can be encrypted and cryptographically secure. We're not going to dive into cryptography here but let's just say that a cryptographically secure number is very hard for other computers to guess. This level of security is where “crypto” comes from, and it is a distinguishing factor of blockchain technologies. Second, the hash maintains the proper order of blockchain transactions, and it also connects the blocks together, creating a chain of blocks (blockchain).

The specific implementation of the hashing function and the ability to create cryptographically secure data sets is what makes blockchain technology so unique, and it solved the Byzantine Generals Problem (BGP). Solving this problem is the breakthrough that you need to understand, and which we discuss in Chapter 12.

Miners and Proof‐of‐Work Consensus

The consensus mechanism is a critical component to the blockchain, as the trusted third party cannot be removed without the ability to have all the participants agree on the order and status of such a dynamic system. This agreement is called consensus.

In the case of the original blockchain, Bitcoin, Satoshi Nakamoto applied an innovative upgrade to previous research in this area by creating the proof‐of‐work (PoW) consensus mechanism. Under PoW, computers run software that is working to create the next valid hash. These computers are called miners. A miner must spend resources, such as energy/electricity, to do this, as unique, cryptographically secure hashes are hard to find! The first miner who does this wins the block reward and earns the right to mint, or create, the block. Blocks on the Bitcoin blockchain are minted roughly every 10 minutes, although the timing is dynamic as we don't exactly know when a new hash will be found. It's then required for the other miners to verify the block – where they agree that all of the transactions are correct – and update their own public ledgers. This ensures that all copies of that ledger are identical.

At this point we do want to note that there are a couple of risks that could compromise a blockchain. If a hacker could successfully attack a blockchain's consensus mechanism, they might be able to alter the order of transactions and/or double‐spend. Double‐spending is when a user within the system, a hacker, spends the same token twice (or more – sometimes many more – times). Imagine going into a jewelry store, buying a $2,000 ring, or a $2,000,000 ring, and using the same $100 bill 20 times, or 20,000 times. That would be theft on a grand scale and is one of two main ways a blockchain could be hacked.

Another risk is what's called a 51% attack. A 51% attack is when one (or more) miners gain control of more than 50% of the mining hash rate. If an attacker controls more than 50% of the network's hash rate, they can control and interrupt the recording of new blocks in that blockchain. This prevents other miners from completing blocks and allows for repeated double‐spending. It's a big deal! Thankfully no major blockchain, like Bitcoin or Ethereum, has ever had a successful 51% attack. This is what makes blockchains so unbelievably secure. A miner would have to spend an enormous number of resources, making a 51% attack economically infeasible.

Now, a successful 51% attack has occurred. In 2018, the blockchain Bitcoin Gold (BTG) incurred enormous losses. That blockchain was a fork (copy) of the Bitcoin blockchain during the “Bitcoin Blocksize War,” which resulted in many different blockchains competing to be the best Bitcoin. This was possible because all of the software is publicly available: anyone can make a copy and make changes to it. Many did this, but just making new software doesn't mean that it's going to be accepted. There were dozens of forks of the Bitcoin open‐source software and tons of “Bitcoin innovators” (we say this while stifling a chuckle) who were trying to “improve” Bitcoin by creating their own version. We might couch this a little differently and say that there were many opportunists who wanted to control the evolution of Bitcoin because, in doing so, they would then have a greater chance of growing wealth with their version. There is a book, The Blocksize War, that covers this period and set of events in detail if you'd like to know more. It was a key time when many decisions were made and the idea of Bitcoin Maximalism (those who only believe in bitcoin and eschew all other variants) was encapsulated and coalesced. Suffice it to say, the other Bitcoin variants were unsuccessful. The only version I can think of that still exists is Bitcoin Cash and I hope we can all agree that blockchain is worthless, although I suppose Roger Ver, its creator, would disagree. Back to the point. BTG was a blockchain that was created, but it wasn't adopted by the same number of miners that run the current Bitcoin blockchain. Because of that, a group was able to control over 51% of the nodes, and thereby “hack” the chain. Think of it like this. It's possible to bribe a jury of 12 – all you need are seven people to align. It's difficult, however, to bribe a jury of hundreds of thousands or millions. Worth noting, the other successful 51% attacks of any note that occurred were on the Ethereum Classic and Verge blockchains. We would never invest in any blockchain that has had a successful 51% attack for obvious reasons.

Block Rewards

So, why are miners spending incredible amounts of energy to find the next cryptographically secure hash? Well, this is another ingenious part of the network. In the case of bitcoin there is a fixed number of 21 million that will ever exist. The bitcoin is held in a reserve pool, however, and it is not available for use unless it is released to the Bitcoin network. The reason there is so much buzz about mining is that the first miner to create the next valid, cryptographically secure hash earns some bitcoin! This is called a block reward and it's the whole point. Currently there are approximately 19.2 million bitcoin in circulation out of the 21 million that have been created. Every time a miner earns a block reward, a small amount of bitcoin is released and becomes publicly available. Importantly, the miner that earns the block reward has initial control of these coins and, with the price of bitcoin, it's easy to see how this can be very profitable.

Note that every miner is important, and if a miner wasn't the one to create a new hash and win the block reward, then they'll perform a verification, which is the process of confirming the transactions, specifically the order of transactions within the newly minted block. They help reinforce that the original miner ordered the transactions. This is how all copies stay in sync in the decentralized environment wherein they all operate. If a miner goes offline for a period, they can come back online, obtain the hash number for all the blocks they missed, and update their ledger to the latest state.

Aligned Incentives

Another aspect of the new digital, decentralized economy is that all participants, from creators to miners to users, have aligned incentives. Since no one person or collection of people “owns” a blockchain outright, it's the groups of participants who work together who ensure the proper running of the blockchain and its ecosystem. The reason they do this is that they all want to “win.”

The three primary groups are the users (the blockchain's functional users), the miners, and the developers. Each group is incentivized to work in the best interest of the blockchain and its ecosystem. Miners win by earning block rewards. The creators of the blockchain win if their blockchain is used by users. Users win if they can participate in the blockchain to accomplish whatever that blockchain is designed to accomplish. Generally, each of these groups will hold tokens and (simplistically) and want those tokens to increase in price. We could do an entire book on the study of tokens and their fundamental economics (tokenomics), but that's for another time. For purposes of this discussion, we're going to simplify and focus on value. If a blockchain provides value, just like if a business provides value, then it will garner usage. The more users in a system, the more value that system will have and the more demand for tokens there will be. In general, if a blockchain has more demand than supply of tokens, that token price will increase. We do have to say that this economic alignment is important, but too many people are caught up in price increases for price increases' sake and are missing the point. Successful ventures are the ones that provide value. Those that do will win and grow. Those that don't, over time, won't.

Other Consensus Mechanisms

Bitcoin has come under fire for its energy usage in its PoW consensus mechanism. While we don't expect it to change, we do want to highlight that many other blockchains use different, more efficient mechanisms.

This is part of the evolution of Satoshi Nakamoto's original work. Different mechanisms include proof of stake (PoS), proof of capacity (PoC), proof of history (PoH), and proof of activity (PoA). We're not going to unpack the differences in each of them here, but suffice it to say that they all require nodes that must reach some sort of agreement in order for transactions to be confirmed and blocks to be written. The one additional mechanism we do want to highlight is proof of stake.

Proof of stake (PoS) is a consensus mechanism that is used by many new blockchains and has a very different way of coming to agreement. Instead of miners, PoS chains have validators. Validators aren't spending energy trying to find the next hash, as in PoW systems. Instead, validators become a part of the network by pledging some of the tokens. They stake the native token of the blockchain, which means that the token is locked up and cannot be otherwise used. In exchange for this, they get to participate in the functioning of the network and can earn rewards just like in PoW.

Validators are responsible for the same tasks that miners do in a PoW chain. There is still a primary validator who confirms that a transaction is correct, writes the block, and receives the reward, while the rest validate that transaction. The difference here is that the validator who gets the privilege of writing the block is selected randomly, with a higher weighting generally given to those validators who have staked more of the token. There is risk, however, as nodes that are dishonest may lose their staked tokens.

As of this writing Ethereum has just completed “The Merge,” which was their conversion from a PoW consensus mechanism to a PoS consensus mechanism. Anyone can be a validator if they stake 32 or more ether, the native token of Ethereum. Those who are taking more risk by staking more ether have a greater chance of getting selected to write the next block and earn the reward. This was a huge technological feat and accomplishment and sets the stage for additional improvements to the blockchain, namely increasing speed and reducing cost, over the coming years.

PoS has gained popularity due to its energy efficiency and accessibility to more validators. Whereas bitcoin mining using PoW requires a significant investment in computing power, almost anyone can run a validator by pledging some of the native currency of the blockchain. We believe PoW consensus is required for cryptocurrency, or coins that are providing the money use case. It's required because there needs to be a cost of production when it comes to minting new money. We've learned from history that it cannot be free to mint new money. However, we believe all other blockchain use cases can be built on top of a blockchain using a PoS consensus mechanism. As time goes on, we expect more innovative consensus mechanisms to make their way into this growing ecosystem.

Note

- 1. John Battelle, The Search: How Google and Its Rivals Rewrote the Rules of Business and Transformed Our Culture (New York: Portfolio, 2005).