21

Crypto as Diversification in a Total Portfolio

All total portfolios are looking for diversification of noncorrelated assets, which would include U.S. stocks, developed stocks, developing stocks, alternative assets (like gold, real estate, and commodities), bonds, cash, and crypto. In this chapter, we'll look at using crypto as a small percentage of a total diversified portfolio. We will also address how smart investors deploy crypto through hedging, buy and hold, and active versus passive strategies. As famed investor Jim Cramer says on his CNBC show Mad Money, “Diversification is truly the only free lunch.” We don't agree with a lot of what Cramer says, but on this point we are truly aligned.

Two of the best books I've read on portfolio diversification are David Swensen's Pioneering Portfolio Management and Unconventional Success. In those two books, he talks about how he changed the endowment fund model to add more alternative asset classes into the total portfolio he was managing for Yale University and how he achieved market‐beating returns. The key component is diversification. Investors want to add asset classes that have lower correlation to one another to improve risk‐adjusted returns – and it works.

Diversification is helpful because different asset classes react differently to market dynamics. For example, stocks (an asset class) react differently to inflation or economic growth than bonds do. The same goes for real estate. The appreciation of real estate (an asset class), especially residential real estate, will be affected differently by rising interest rates than stocks are. That's because the appreciation of residential homes is primarily affected by the rate of the 10‐year Treasury, the rate basis of most mortgages. Home prices can go up when rates go down because it is the monthly payment that most people are using to factor in their decision making. If incomes rise, people can afford to pay more for homes because their income is rising. However, when rates rise, that severely affects how much the monthly mortgage payment will be. A 1% increase in the interest rate can affect the monthly payment significantly. In comparison, stocks aren't nearly as affected by rates and businesses. This is why diversification of asset classes and the target percentage allocations for each is so important for generating optimized risk‐adjusted returns.

Safe‐Haven Assets – Gold and Bitcoin

A safe‐haven asset is an asset that is expected to hold or even increase in value during times of market turbulence. Gold and some selective equities like utilities have generally been seen as safe‐haven assets when markets tumble, and more and more we are seeing bitcoin demonstrating this behavior. We've been watching bitcoin for quite a while, and we see bitcoin shifting into safe‐haven behavior when:

- VIX is up (the fear index)

- SPY is down (risk assets as measured by the S&P 500)

- Then, if GLD is up (trading like a safe‐haven asset)

- Then, when BTC is also up (also trading like a safe‐haven asset)

We started with bitcoin trading like a safe‐haven asset in 2019 less than 20 days. Then by 2020, it was 53 days. In 2022, it's traded for 20 days as a safe‐haven asset by June, and I wouldn't be surprised if 2023 was higher than 53 days. We believe that as the years go on and as bitcoin becomes more widely adopted, it will trade more and more like a safe‐haven asset.

Generating Alpha – Market‐Beating Returns

Harry Markowitz created the idea of modern portfolio theory (MPT) and introduced that concept in “Portfolio Selection,” an article first published in the Journal of Finance in 1952. Markowitz was the first to talk about an investment portfolio and asset classes; he won the Nobel Prize in economics that year for his innovations with MPT because he devised a method to mathematically match an investor's risk tolerance to reward expectations through an ideal investment portfolio. Many know that in MPT there are three ways to generate alpha, simply market‐beating returns: portfolio construction, asset selection, and market timing. A market will have volatility or risk and generate a certain return. Risk is the same as volatility. If a market or asset has more volatility, it carries more risk. Market risk is known as beta. Investors looking for outperformance will need to affect improvement in one or more of these three areas. Most novice investors focus on market timing, but that's the least valuable over a long period. Most alpha is generated through portfolio construction and asset selection. I want to talk about how investing in bitcoin will help in portfolio construction.

There are several dimensions to portfolio construction that help generate alpha. We know that three event‐driven components largely generate an investment portfolio's performance:

- The annual global economic growth percentage and the rate of change of that growth;

- The expected inflation and the rate of change of that inflation; and

- Interest rates and the rate of change of those interest rates.

These are the input functions of the event‐driven aspect of managing a total portfolio. Bitcoin provides a few unique characteristics when combined in a complete portfolio. One is that it offers more diversification because it reacts differently to growth, inflation, and interest rate changes than other asset classes, such as stocks or bonds. We know this by looking at correlation over a long period of time. Many times, it can act like a risk‐on asset, but many times it does not.

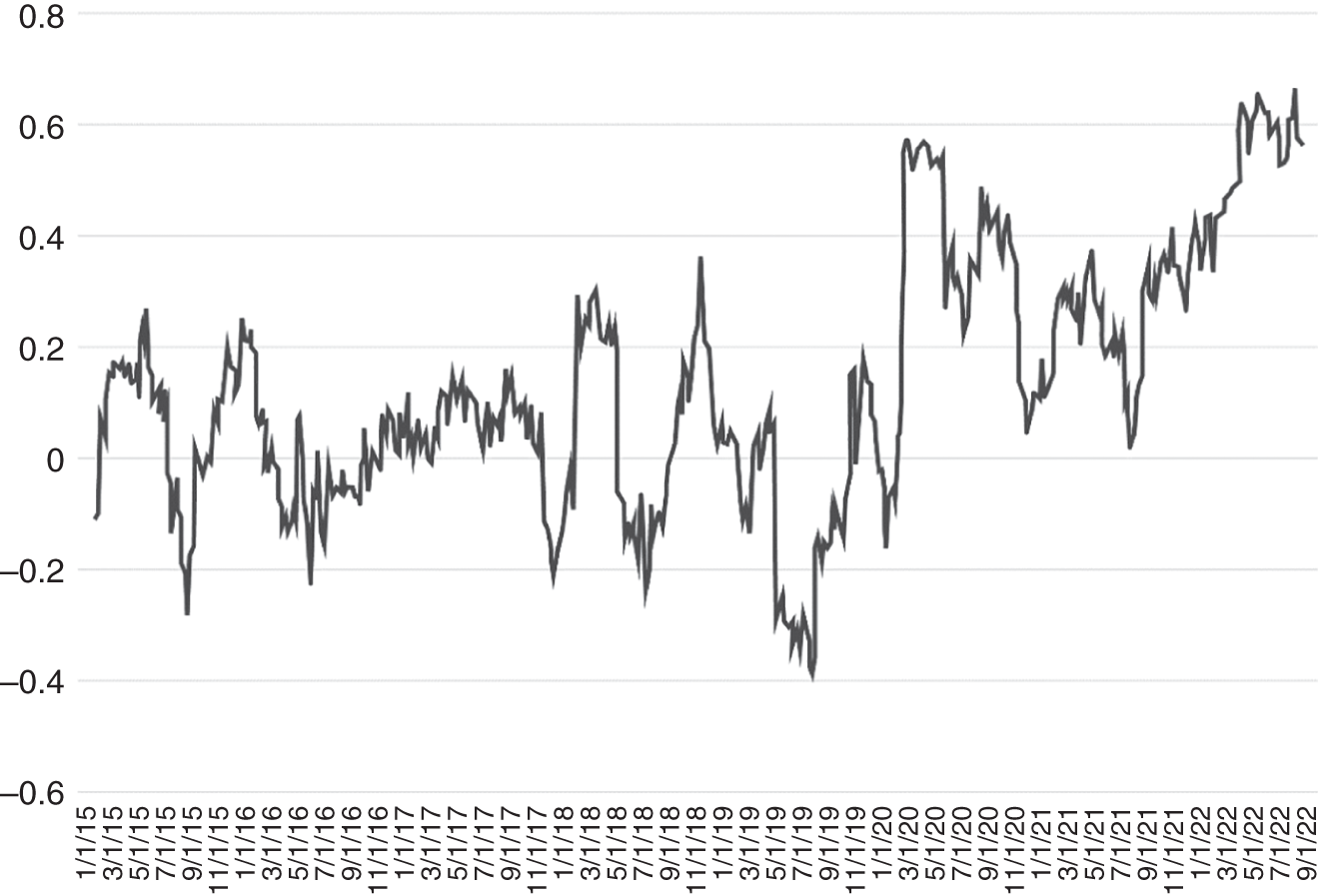

In 2020, bitcoin traded over 50 times (meaning 50 days of the tradable 365 days that year) like a safe‐haven asset, which we defined earlier in this chapter. We calculate a safe‐haven asset as when a volatility index, such as the ^VIX Index, is up and risk‐on assets, for example, the 500 largest stocks with the highest market capitalization like the S&P 500 Index, are down, and $BTC is still up (see Figure 21.1). Many times, gold acts like a safe‐haven asset if/when investors were losing faith in U.S. Treasuries (USTs). So, if you looked back in 2020, we measured 53 days of the whole year where bitcoin traded like a safe‐haven asset. That's a nice feature in one of your total portfolio's positions. I mentioned this in my first book, but the 60/40 model portfolio, where 60% of a portfolio is invested in stocks and 40% is invested in bonds, is dead! That strategy no longer works for several reasons; therefore, it's critical for today's investors to diversify so that not all of their portfolios behave the same way. There may be big days like March 12, 2020, when everything goes down (except volatility and interest rates), but there are many days where the correlation between bitcoin and stocks works in investors' favor.

Figure 21.1 Correlation of $BTC to $SPY, the S&P 500 Index

Bitcoin also provides different convexity, a portfolio's exposure to standard market risk. It's not an asset that is affected by interest rates, although it does have an indirect relationship to interest rates – or inflation or economic growth, for that matter. A couple of factors affect bitcoin as an asset: an investor can generate yield by holding bitcoin by lending, just like any foreign/fiat currency. An investor could lend out their bitcoin and earn something like 3% to 5% in yield. So, investors may want to think about that income compared to a “risk‐free” (LOL) UST. And suppose interest rates stay in a range. In that case, bitcoin has the opportunity to continue rising in price because it is an innovation with an increasing adoption rate – progressing through its innovation cycle (see Figure 11.1 in Chapter 11).

Bitcoin also reacts to inflation a bit differently. Bitcoin reacts more to monetary inflation than consumer price inflation. Monetary inflation relates to central banks and the money supply, whether the central bank is increasing the circulating supply of currency. Price inflation relates to prices rising in the economy. So, if the Fed and other central banks print more and more money, then bitcoin does better pricewise because it's a scarce asset. Just check the Federal Reserve's own website and see the almost‐perfect indirect relationship between the price of bitcoin and M2 money supply (which is the money supply, including consumer and bank credit).

Near‐infinite money is chasing finite resources and chasing scarcity. We know this because in the past decade, fine art, rare wines, and rare cars have outperformed the S&P 500 substantially by something like 173%. Right now, it's making more sense in terms of risk/reward for an investor to invest in scarcity over productivity. For example, here are forecasts and estimates for the beginning of Q4 2022 for the three major global macro factors—global growth, expected inflation, and interest rates: when things are good, growth is higher than real return on bonds, which is interest rate minus inflation. At the time of this writing, this is not the case. In general, you're losing money as inflation eats away purchasing power. The headwinds are strong!

In Q4 2022, the three macro factors are:

- Expected growth 1.4% (for 2022 and beyond)

- Expected inflation 8.3% (for 2022 and beyond)

- Interest rates 3.7% (for the 10‐year UST)

Global economic headwind then is –3.2% (Growth – Real return, with real return being Rates – Inflation).

Add to this the fact that the USD is the world's reserve currency and it's strong against all other fiat currencies. This creates recession‐producing deflationary pressure.

Looking at these three metrics you can tell that if growth is 3% and expected inflation is 7%, then companies will have a harder time generating profits. So, suppose you're a lazy investor, or just a rational one. In that case, you can easily see that it's going to be, at least in terms of risk‐adjusted returns, an easier or better investment to invest in something scarce versus trying to do the calculus to figure out how productive something is.

Bitcoin is also affected by growth. If the economy is growing, then bitcoin will progress faster through its adoption cycle (see S Curve). As more and more people invest with bitcoin or accept bitcoin, the price of bitcoin will go higher because it is a network good. Network goods have network effects. Network effects follow Metcalf's law in that it's nonlinear, meaning the value proportional to the network good is in relation to the number of users. We discuss this in greater detail in the Age of Autonomy® book.

Bitcoin is also a very reflexive asset, which is to say, if it goes up, it goes up a lot, and if it goes down, it goes down a lot. Having reflexive assets in a portfolio adds an extra dimension so that you do not have to deploy as much capital to get an outside return. It's almost like having leverage (same but different). The way you capture value inside a reflexive asset is by the duration it's held. If you hold bitcoin for over three years, then you're going to (or most likely going to) generate positive return, at least as history has shown.

Therefore, it makes perfect sense to include some percentage of bitcoin in a total portfolio. It's a scarce asset. It's the cleanest way to invest in scarcity because it's one of the only assets in the world with a precisely known quantity that's treated by the investment community with financialization—meaning the financial industry is building exchanges, derivatives, and futures on it. Bitcoin clearly adds real benefit to a diversified total portfolio. The amount to invest in bitcoin is up to you as the investor. So, how much? The answer is definitely not 0%.

Measuring Risk‐Adjusted Returns

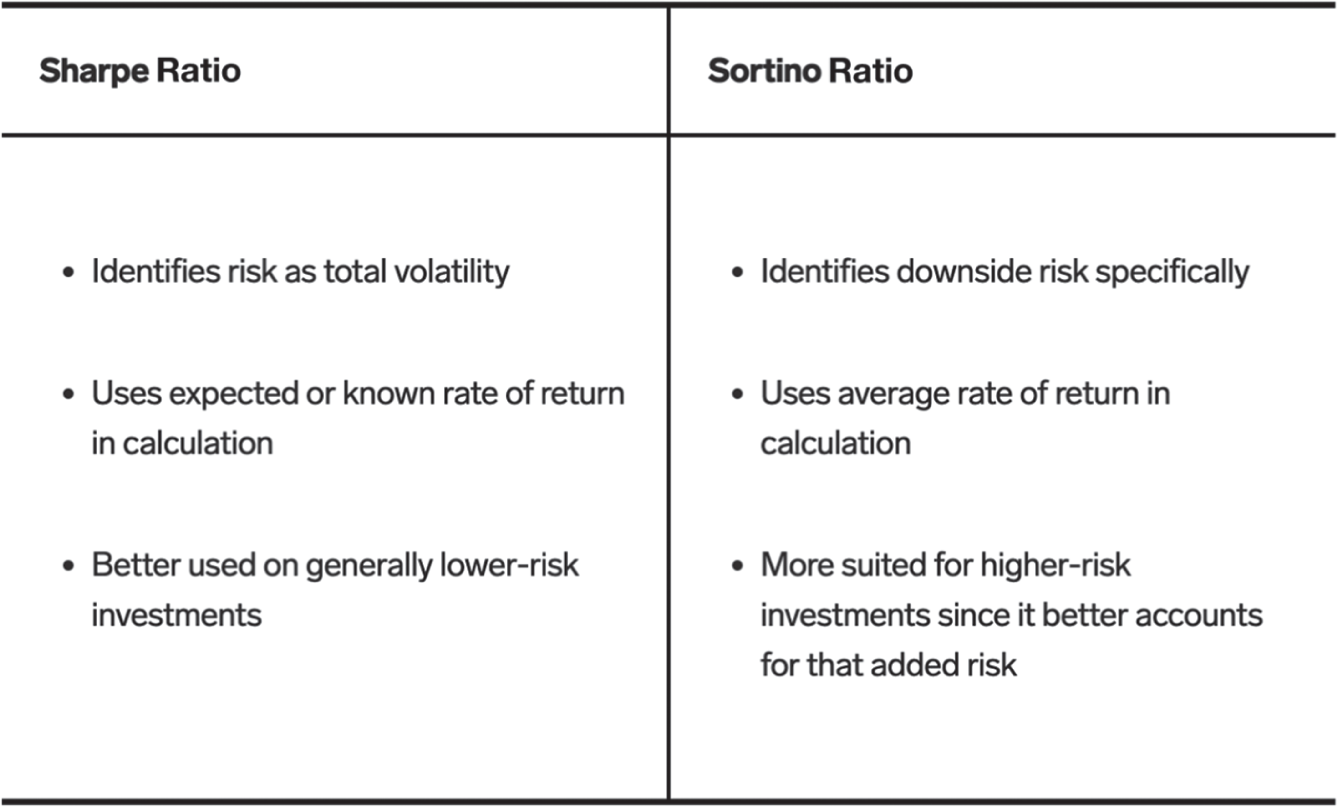

It's all well and good if you can generate 70% in one year; however, how much risk did you take to generate that return? An investor who can take less risk to generate that kind of return is better off. We can calculate risk‐adjusted return by a Sharpe ratio or a Sortino ratio. These are slightly different, but their intention is the same: to calculate and communicate a risk‐adjusted return (see Figure 21.2). If you look up a mutual fund on Morningstar or Yahoo! Finance, you can see that each has a Sharpe ratio and/or a Sortino ratio. A Sharpe ratio of 0 means that your returns match a “risk‐free” return, like a U.S. Treasury. Yes, the industry still thinks of a Treasury as a risk‐free asset, but if you've read my first book you know that a Treasury has gone from a risk‐free return to a return‐free risk. A Sharpe ratio of 1.0 is considered acceptable or good, and a ratio 2.0 or higher is excellent. A Sortino ratio, created by Frank A. Sortino, is similar to a Sharpe ratio, but it accounts more for downside risk. This is going to give you a better understanding of an investment or investment manager because upside risk should be good, right? So, the Sortino ratio takes into account the standard deviation of the downside, not the general standard deviation like the Sharpe ratio. Suffice it to say that either one of these ratios will give an investor a much better understanding of an investment's performance than just looking at its return because it indicates how much risk was taken to achieve said return.

Figure 21.2 Difference Between Sharpe and Sortino Ratios

Adding Bitcoin to a Total Portfolio

Because of bitcoin's volatility and low correlation to other markets, like stocks or bonds, adding it as diversification in a total portfolio is valuable. The best way to manage a volatile asset is through holding duration and position‐sizing. If you're adding an extremely volatile asset into a total portfolio, you'll want to make sure to hold it for three years or longer and keep a smaller position than, say, your stock or bond allocation. You're not going to add bitcoin as 30% of your portfolio. But a 2%, 3%, or 5% allocation might make sense.

I was on the road with Ric Edelman a few years ago when he was putting on a Digital Asset track at several investment conferences. One of the conferences was TDAmeritrade's LINC Conference. Ric had an outstanding presentation that walked through what having a 1% allocation to bitcoin would do in a total portfolio. Even if bitcoin went to 0, it wouldn't greatly affect the performance of the total portfolio. And, if bitcoin really performed, it could add value in the returns.

In Ric's presentation, he demonstrated that adding a small position into bitcoin greatly improves a total portfolio's risk‐adjusted returns. That's due, in part, to the fact that bitcoin has a 3+ Sharpe ratio if you hold it over three years. Adding small positions in other crypto assets just extends the same concept. It's important to note that the higher the volatility of a digital asset, the smaller the position size may be in a crypto portfolio. Having a crypto portfolio that may be 5% of a total portfolio and having 5–10 digital assets in that crypto portfolio may well be the best way to improve a total portfolio's diversification and risk‐adjusted returns. And remember: the goal would be to hold these digital assets for three‐plus years. Unless you're spending significant time researching and managing your digital asset portfolio, I wouldn't recommend having more than 5% to 10% allocated to digital assets, and bitcoin would be the highest allocation inside that crypto portfolio.