CHAPTER 1

What It Takes to Drive Growth

The old Borg-Warner would have said “you can’t

organize the innovation process, that’s impossible.“ The

new Borg-Warner says “we have a process for everything

else, let’s have one for innovation.”

Simon Spencer, Borg-Warner’s first

Innovation Champion

How will you drive growth in your company? That’s really the key question, is it not? Of course, your company is growing—most firms today are. The challenge is that there’s a gap between the rate of growth they’ve been achieving and the rate of growth they want and need to achieve to remain competitive.

A Corporate Strategy Board study reveals how few firms are growing at rates uncommon in their industry—and sustaining that growth—over time. Researchers analyzed 3,700 companies with half a billion dollars or more in annual revenues over a seven-year period. Of these, only 3-3 percent showed consistently profitable top- and bottom-line growth and shareholder returns. Result: fewer than 21 of the firms (in other words, less than one percent) 14sustained this growth over the past two decades. These 21 companies didn’t just grow top-line revenue; they also outperformed the Standard & Poor’s index during the same period, with a 26 percent compound annual market cap growth versus 13 percent for average S&P companies.

Many companies today face their own version of the Growth Gap. They’ve realized that cost-cutting efforts and acquisitions of other companies, while important, cannot help them grow organically. If yours is among them, your challenge may be to help your company figure out a better way to deliver it. If you’ve been tasked with thinking of ways to drive revenue growth, you’ve probably been met with objections from others in your firm who want to:

Redoubh your firm’s efforts to cut costs and gain further efficiencies.

Companies have spent the past quarter century driving costs out of their operations by reducing headcount, consolidating and optimizing operations, and introducing new technologies. The results in productivity and profitability have been outstanding. Yet such efforts have not and will not increase top-line revenue; therefore they cannot fuel profitable revenue growth.

Spend more to beef up marketing and sales. A winning advertising campaign or sales effort can boost sales, increase market share, and drive revenue momentum. But ultimately, marketing and sales can only take you so far if growth is your objective.

Acquire other companies. Certainly this method of growth has been widely adopted, but the downside of putting all your chips on growth through acquisition has become more evident in recent years. Among the pitfalls: trouble in melding often incompatible cultures and leadership teams, overcoming regulatory and shareholder objections, a huge drain of management’s attention away from meeting customer needs, and the biggest of all, creating out of the merger/acquisition binge a slow-moving behemoth that cannot continue to grow from acquiring, and shows an incapacity to grow organically. Just 23 percent of acquisitions earn their cost of capital, according to a study by consulting firm McKinsey and Company that looked at deals made by 116 companies over an 11-year period. According to the report, the steep prices paid to capture other firms often lower growth rates rather than increase them.

15Chances are you have already tried these methods and that is why you are ready to jump-start growth in a fundamentally new way. But you may be skeptical that revamping innovation in your firm is the best way to go. Will innovation actually lead to a higher rate of growth? Yes it will. You can bank on it.

Why Innovation Is the Best Way to Stimulate Growth

A landmark study conducted by PricewaterhouseCoopers’ British Unit documents the connection: firms that master innovation grow faster than their peers and enjoy higher profit margins.

In analyzing the financial results of 399 companies based in seven countries, PWC found a significant “growth chasm” between companies it identified as most innovative and least innovative. Most innovative firms had more than 75 percent turnover of products and services introduced within the last five years. Those firms generated well above average total shareholder returns (greater than 37 percent, on average). The study found that:

- The proportion of new products and services is a key indicator of corporate success both in terms of revenue enhancement and total shareholder returns.

- There is a major gap between high and low performers. High performers average 61 percent of turnover from new products as compared to 26 percent for low performers. (Average for this seven-country sample was 38 percent of turnover from new products and services.)

- Nearly a quarter of all companies were generating 10 percent or less of their turnover from new products and services. Growth-wise, they have stagnated.

The implications of this study are clear. High-growth firms do a lot of innovating, while low-growth firms do it only incrementally. High-growth firms obsolete themselves by coming out with new products and services and entering new markets; low-growth firms lag in these areas.

If you’re determined to jump-start growth in your company, PWC’s research provides proof that your efforts will pay off, will truly make the difference. If you take two companies with equal revenues and equal growth rates in the marketplace today and you upgrade the approach to innovation in one 16of the firms, while the other goes about business as usual, what happens? Over time, the innovating company is likely to benefit from a higher growth rate than its competitor. On average, the innovating firm, if it brings about a 10 percent increase in the percentage of new products and services introduced, this correlates to a 2.5 percent increase in that firm’s rate of revenue growth.

Other studies provide similar proof that innovation has the power to fuel growth. Boston Consulting Group, in conjunction with BusinessWeek magazine, now compiles an annual list of the World’s 25 Most Innovative Companies. Apple, Google, 3M, Toyota, Microsoft, GE, P&G, Nokia, Starbucks and others topped the 2006 list. When compared against the Standard & Poor’s 1200 Global Stock Index, the Most Innovative Companies (MICs) had a mean margin growth of 3-4 percent annually, compared to a .4 percent increase among the total index. MIC stock returns averaged 14.3 percent, compared to 11.1 percent for the mean index.

This book is not meant to be an academic treatise on innovation, but rather a practical guide to leading your firm towards a higher growth future. But first we’d better define what we’re talking about with this all-purpose word “innovation.”

What Innovation Is, and What It Isn’t

In its simplest rendition, innovation is coming up with ideas and bringing them to life. Hatching ideas is the “creative” part; bringing them to life successfully in the form of a new product or service or management method is what makes a raw idea an innovation.

To use “innovation” as a way to stimulate growth means that you offer customers something new. Something they cannot get anywhere else, something that solves their problem in a superior way or provides unique or exceptional value. To stimulate growth, you must come out with products and services and business models that cause customers to buy more of what you sell. To do that you’ll need to go after new customer groups with existing offerings, and in some cases, new customer groups with new offerings. Doing these things is the essence of innovation.

Because it’s such a multifaceted subject, we’ll analyze the various types of innovation in greater detail later in this chapter. For now, let’s acknowledge that you and your firm are already doing some of these things. In fact, if you’re like the majority of companies, you’ve probably already taken steps 17to improve the practice of innovation in your firm—most companies have. But also consider for a moment how innovation gets “practiced” in your organization today.

Despite it becoming a more urgent need, the way most firms go about innovation is still pretty similar to how they went about it yesterday. The approach is piecemeal, departmentally driven (R&D, new product development and marketing handle it), it’s ad hoc, seat-of-the-pants, and by no means comprehensive. I’ve often compared it to pandas mating: infrequent, clumsy, and quite often ineffective.

As a result, innovation has probably been primarily incremental and mostly concentrated on process innovation: operational efficiencies, cost-cutting and staff-reducing measures. Initiatives with names like Reengineering, Lean, Six Sigma, TQM, Lean Sigma, etc. are all forms of process innovation, and are concerned with improving the bottom line by increasing the spread between gross and net. As such, they cannot increase top-line revenue; they cannot fuel growth. Because no one has really been in charge of innovation, or of upgrading approaches in this arena, the focus is likely to be on delivering short-term quarterly results, minimizing risk, and executing better and faster.

Don’t get me wrong. There’s nothing wrong with process innovation. As we’ll see, it’s essential to organizational effectiveness, and always will be. There’s nothing wrong with product line extensions and filling in adjacencies and all the other things associated with incrementalism. Let’s acknowledge that operational excellence is what got your firm to where it is today. But you and others in your firm realize that what got you where you are isn’t what’s going to get you where you want and need to be to rev up growth.

The Purpose of Innovation: Create New Customer Value

To deliver growth from innovation requires that your idea do something that benefits customers: your new idea creates new value for the customer, unique value (they can’t get what you offer anywhere else but from you) and exceptional value—(you do more for the customer than other providers). Value encompasses the quality and uniqueness of the product or service, and the degree to which it satisfies the customer’s need or problem. Value is also the customer service and add-on services provided as part of the sale, together with the price of the offering or service.

18The purpose of innovation is to create new customer value. If customers perceive value in your new offering, they’ll pay you for it. This is the challenge companies face with respect to innovation: How do you develop ideas that indeed create new value for customers? Before we address that question, we need to further differentiate the types and degrees of innovation.

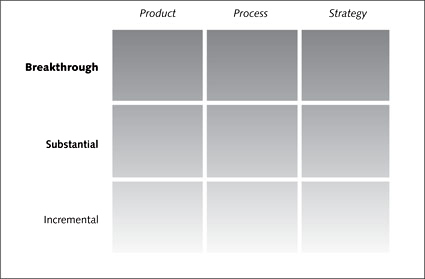

The Three Types of Innovation

The matrix in Figure 1 shows the three types of innovation: product, process, and strategy. In the highly competitive, rapidly evolving environment of the 21st century, achieving rates of growth that are uncommon in your industry (uncommon in your region of the world), means that you must be able to manage innovation in these three distinct arenas. Each arena is critical, and being adept in only one of them is likely not sufficient to achieve the growth you seek. Let’s take a careful look at these arenas.

Type 1: Product Innovation

Products have traditionally been defined as tangible, physical goods or raw materials ranging from toothpaste to steel beams, from computers to industrial adhesives, from jet aircraft to automobiles to soybeans. All the objects around you at this moment that were manufactured by a company constitute products.

But to confuse matters a bit, in recent years, service sector firms (healthcare, insurance, financial services, professional services, to name only a few) have begun to refer to their offerings as “products” as well. When Merrill Lynch introduced its highly successful Cash Management Account in the early 1980s, this “product” vaulted this service company to the top of its industry.

Adding to the breakdown in traditional boundaries, product manufacturers increasingly surround their products with services, for instance, when car manufacturers offer emergency roadside assistance. General Motors sells cars, but its customers buy certain automobiles with services as part of the deal. OnStar, an onboard global positioning satellite-enabled communication channel, gives GM customers the ability to know exactly where on Earth they are, and to summon emergency help if they need it.

Despite the recent trend of service firms and manufacturers alike to use the term “products” to describe their offerings, services and service businesses’

19

“products” tend to be different. Foremost among them, they can often be intangible as opposed to tangible and physical (an insurance policy as opposed to a snowboard). They also tend to be produced and consumed at the same time and to involve a higher degree of human involvement in their delivery (think health care and hospitality). And they tend to be difficult or impossible to stop imitation through the use of patents.

So while there are differences, products and services have common traits, especially when it comes to the subject of innovation. We will use the term products to describe the offerings of both types of firms.

And now for the definition: Product/service innovation is the result of bringing to life a new way to solve the customer’s problem that benefits both the customer and the sponsoring company.

Type 2: Process Innovation

Process innovations increase bottom-line profitability, reduce costs, raise productivity, and increase employee job satisfaction. The customer also benefits from this type of innovation by virtue of a stronger, more consistent product or service value delivery. The unique trait about process innovations 20is that they are most often out of view of the customer; they are “back office.” Only when a firm’s processes fail to enable the firm to deliver the product or service expected does the customer become aware of the lack of effective process.

For manufacturing companies, process innovations include such things as integrating new manufacturing methods and technologies that lead to advantages in cost, quality, cycle time, development time, speed of delivery, or ability to mass-customize products, and services that are sold with those products.

Such innovation is important and will continue to be.

Process innovations enable service firms to introduce “front office” customer service improvements and add new services, as well as new “products” that are visible to the customer. When Federal Express introduced its unique tracking system in 1986, customers saw only a tiny wand, used by drivers to scan packages. Yet while the rest of this sophisticated system was invisible, customers could “see” immediately that they could now track their packages at every point from sender to receiver, and this added value to their service experience and gave Federal Express a decided advantage.

Process innovation will continue to be vitally important to company growth for the simple reason that without process excellence, product or strategy innovation is impossible to implement. Indeed, while thousands of books have been written about varying methods of process improvement, the innovation process, in most firms has, thus far, received short shrift.

Type 3: Strategy Innovation

Strategy innovation, sometimes called business model innovation, includes all the things you do that surround your product to add value to your customer’s experience. In contrast to process innovations, which are largely unseen by the customer, strategy innovations directly touch the customer and add tangible new value.

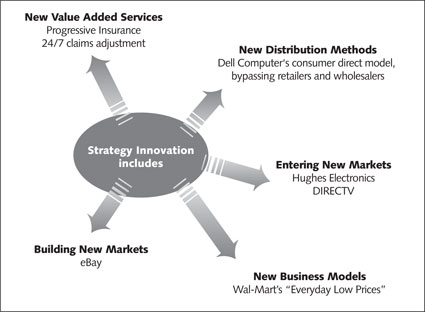

Strategy innovation includes new approaches to marketing or advertising your offerings, introducing new sales methods, new approaches to customer service or positioning your brand. Strategy innovation results when your firm changes the customer groups it targets and how it “goes to market,” meaning how it distributes its offerings to end customers (Figure 2).

An important type of strategy innovation is when a firm decides to

21

market its existing products, services, or expertise to new customer groups. That’s what defense contractor Hughes Electronics did when it began its DIRECTV division in the early 1990s, using its expertise with satellites to begin beaming cable channels and movies to home satellite dishes. More commonly, when a firm such as a traditional retailer decides to additionally sell its wares via the web, that’s strategy innovation.

Much of the highly visible innovation occurring today is strategy innovation. Dell Computer’s very business model was a prime example of strategy innovation because it represents a dramatically different way of manufacturing and selling personal computers. Dell chose not to distribute its products through the then-standard channel—to wholesalers or resellers, who sold to retailers, who then sold to end customers. Instead Dell sold directly to end customers.

Other innovations rounding out Dell’s revolutionary business model were strategic in nature as well: from the beginning, Dell didn’t manufacture a single computer until it received a customer’s order. And the product was then manufactured to order, rather than creating an inventory of standardized products to be stored until sold in one warehouse or another.

22Similarly, firms ranging from eBay to Amazon.com represent strategy innovations when compared to the way their respective industries traditionally did business. Southwest Airlines was a strategy innovator in the airline industry. Its business model is based on offering customers low fares in exchange for their giving up such amenities as preassigned seating, meals, nonstop flights, the ability to book using a travel agent, and other value-added services—all aspects of Southwest’s business model that differed from competitors.

Costco pioneered warehouse club retailing, a strategy innovation. “Category killers” with names like Office Depot, Home Depot, Staples, Borders, PetSmart, IKEA, and CompUSA, all pioneered new business models in their time. Wal-Mart pioneered a new business model that disrupted thousands of traditional merchants in the U.S. and other countries. Wal-Mart offered many of the same products as traditional merchants, but offered “everyday low prices” to lure customers with a perception of greater value. As a result of their success, many traditional department stores and merchants were forced out of business.

Strategy Innovation. Strategy innovations are those that don’t involve your product, but that touch your customer. Your customer can see them, feel them, and appreciate them. Let’s look at some common types of strategy innovation along with some examples of their power to drive revenue growth.

New Value-Added Services. Progressive Insurance has grown at double-digit rates by constantly pioneering new value-added services. Progressive’s onsite claims adjustment service settles accident claims with the client on the spot, 24 hours a day, seven days a week. And Progressive’s website quotes not only its own rates, but those of its competitors as well, even when the competitors’ rates are less.

New Distribution Methods. Dell Computer’s strategy innovation was to rethink distribution. Dell bypassed distributors and retailers to sell directly to corporations and consumers, giving the company a price advantage and adding value to customers.

New Business Model. Wal-Mart’s “everyday low prices” business model was an innovation in the retail sector, in contrast to having markdown sales to stimulate business.

23New Market Channels. Innovation-adept companies constantly look for new market channels and territory through which to sell their products, and new products to sell in existing markets.

Branding. Intel’s strategy involved not changing its products or processes but branding its products to create greater consumer awareness.

Building New Markets. eBay didn’t just enter a new market that previously existed; they built a new market from scratch. Before eBay, garage sales and swap meets were where used items got bought and sold; today eBay helps people buy and sell billions of dollars in merchandise.

Not All Innovations Jump-Start Growth

The degree to which an innovation adds or creates new value for customers is the degree to which it contributes to your growth. What innovation-adept companies do is to put in place an ongoing process to indentify and nurture high-potential ideas in each of these categories. Ideas that will change the game. Ideas that will change the rules of competition. Ideas that move the growth needle!

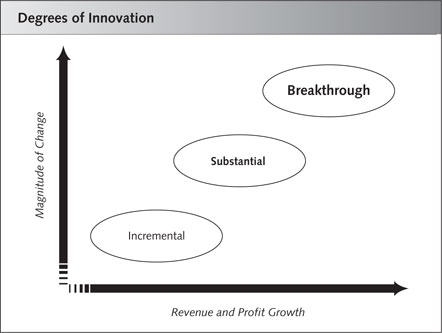

Not all innovations, of course, have an equal impact on customers, or on a company’s rate of growth or wealth-creating ability. All product, process, and strategy innovations can be categorized further into three basic degrees: incremental, substantial, and breakthrough (Figure 3)·

Incremental Innovation

While small or even insignificant in degree of financial impact to the firm’s bottom line, incremental improvements can engender greater customer satisfaction, increase product or service efficacy and otherwise have positive impact. Similarly, process innovations of incremental degree increase productivity, and lower cost for the firm.

Incremental innovations have this in common: they seldom require more than minor changes in customer or company behavior to implement. 3M’s introduction of a new color Post-it Note qualifies as an incremental product innovation, while Post-it Notes represented a breakthrough product innovation. Implementing a suggestion program—a process innovation—requires employees to change behavior very little since submitting ideas is optional.

24

In the service sector, incremental innovation occurs when a hotel simplifies its guest check-in procedure; a supermarket chain makes check approval easier than summoning the manager; a bank redecorates its lobby; a retirement home upgrades signage to address seniors’ failing eyesight; an international airline upgrades its first-class cabin to include fully reclining sleeper seats.

Incremental process innovation has gotten a bad rap in recent years on the assumption that incrementalism is the enemy of genuine innovation. One reason for this is that in many firms, incremental innovation has replaced the quest for more significant innovation—those that add more value to customers and, as a result, bolster the business accordingly. Incremental innovations are often quickly matched by competitors, which cancel out any “first mover” benefit to the initiating firm’s bottom line. Worse, if a firm is spending its time thinking merely about incremental innovation, it probably isn’t spending time reinventing the product category or attacking its own value proposition with a radically improved one.

25Constant improvements are essential to companies engaged in pioneering new markets or rolling out radically different products. They know that thousands upon thousands of incremental innovations are a necessary and beneficial part of the process. So incrementalism is a good and necessary endeavor, and needs to be supported. But the cumulative effect of incrementalism without vision is that a company stops inventing its future with radically better products and services and markets.

Substantial Innovations

Substantial innovations are mid-level in significance both to customers who benefit from them and to the sponsoring company that believes they will significantly help the firm grow and create new wealth. Substantial innovations of the product/service variety fall short of being breakthroughs, but enable and ensure that the organization meets or exceeds its goals to grow the business, increase market share, and lower its cost of doing business (substantial-level process innovation).

Substantial improvements in your existing products and services or introducing new-to-the-company products and services represent significant improvements for both the service-providing company and for the customer.

Breakthrough Innovations

New products, services, or alterations of your strategy that yield a significant increase in revenues and net profits are breakthrough innovations. It is impossible to define in dollars and cents how much revenue an idea must bring to the top line to classify as a breakthrough because it depends on the size of your company and what it takes to significantly drive growth. So, breakthroughs must be self-defined, but need to be major if you are serious about going after them. When we asked how large an idea had to be to be designated a breakthrough at the Chemicals Division of Royal Dutch/Shell, the answer was $100 million or more to the top line.

Process improvements that generate a significant reduction in costs or an equivalent increase in productive output are also breakthroughs. Breakthrough inventions can sometimes lead to breakthrough-level innovations for numerous companies. Breakthrough inventions are giant leaps forward for humankind that lack proprietary patents and may not provide “first mover” advantage to a single company, but instead spawn an entire new industry.

26

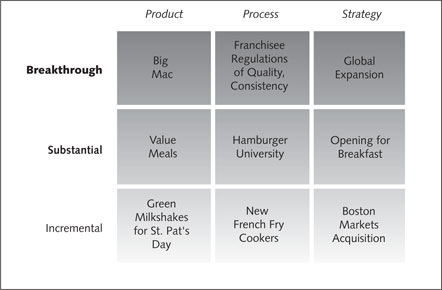

Figure 4. McDonald’s Corporation has innovated successfully in each of the important parts of the grid. As an exercise, try filling out this grid for your company.

The automobile, the invention of electricity, the discovery of penicillin, the Internet, and the World Wide Web are all breakthrough inventions. While the automobile was a breakthrough in terms of how people transported themselves from place to place, no single company could claim to have benefited exclusively from having invented it or had the legally protected right to market it. And it’s the same with the Internet, television, and lots of other products.

On the other hand, some new products, services, processes, and business models do have proprietary patents and simultaneously give temporary monopoly to the sponsoring firm—it is this type of innovation that we focus on in this book.

Two Breakthrough Examples

When Gillette, facing intense competition from cheap disposable razors, decided to develop its Sensor shaving system in the early 1990s, the product became a breakthrough almost immediately. Radical innovation? Hardly. The market was familiar—men with whiskers. The product category was familiar too. The innovation came in the strategic decision to go up-market and not compete on price. And it came in the superior value it delivered to

27Radical Innovations

Radical innovations are those that require your company to develop a whole new business or product lines based on new ideas or technologies or cost reductions, and that transform the economics of the sponsoring business and disrupt entire industries.

The important point is that not all radical innovations become breakthrough innovations, and not all breakthrough innovations are radical. Radical innovations that become breakthroughs provide customers whole new ways of solving their problems or meeting their needs, and in some cases they actually create new needs. Moreover, they require the sponsoring firm to be a first mover, or at least a fast follower, a subject about which we’ll have more to say in a later chapter.

When you analyze breakthrough ideas, you find that some are radical innovations. Indeed, in a major study of radical innovations, such as DuPont’s biodegradable fiber, GE’s digital X-ray system, and others, a team of Rensselaer Polytechnic Institute researchers concluded that:

- Radical innovations can be stimulated by concerted effort, as opposed to waiting for happy accidents to occur.

- Radical innovations often take ten or more years to develop into a commercial product and additional time to build the market.

- Radical ideas need to have different processes and funding to guide their development.

- Radical ideas often require multiple champions to see them from idea to implementation.

While we’re all for radical innovations, they are not what this book is primarily about. We don’t want to wait 15 to 25 years for a payout, and we assume you don’t either. Fortunately, many ideas that become breakthroughs are not that radical, or that risky, for that matter.

the user, and the difficult-to-copy, 22-patent product and marketing campaign that was the result of a billion-dollar investment.

When Volkswagen decided to launch an updated, restyled version of its famous Beetle, which had been discontinued in North American markets due to an inability to meet strict emissions standards in the 1970s, the result was an instant breakthrough for Volkswagen AG. Radical innovation? Hardly. Obvious moves for these two companies? Not at the time.

What about at your company, have you had any breakthroughs lately? Maybe it’s time for a new approach.

28Designing Your Firm’s Innovation Process

You and your firm can enjoy the rewards that Vanguard firms now enjoy as a result of taking action to improve how innovation is practiced. Now that you know what innovation is, we’re almost ready to talk about how to cause more of it to start happening in your firm. But before we do, I’d like to invite you to take the assessment below and see how your company rates. The assessment is included in our online executive study ecourse called “Inside the Innovation Elite,” which features some of the most important concepts in this book. Visit our website at www.innovationresourse.com for more information or to download this assessment for yourself and others in your firm.

Assessing Your Firm’s Innovation Adeptness

Before you continue on to the next chapter, take a moment to gauge your company’s current practices and attitudes with respect to innovation. As you respond to the following 10 questions, if you believe “a” best represents your firm, give yourself 3 points; if “b,” give yourself 2 points; if “c,” give yourself one point. After you’ve answered all the questions, tally up your score and refer to the interpretations that follow.

- My company’s approach to innovation is:

- systematic, all-enterprise (3 points)

- we have made improvements but still have a ways to go (2 points)

- we have not even begun to tackle this (1 point)

- In our company, we have developed effective ways to measure innovation progress.

- agree completely (3 points)

- we have attempted to implement innovation metrics, but they have not been effective in guiding our efforts forward (2 points)

- we haven’t yet attempted to measure innovation at all (1 point)

- 29Innovation at our company is supported by the leader and the top team.

- agree completely (3 points)

- our leadership sends mixed signals when it comes to innovation (2 points)

- our leadership does not support innovation activity (1 point)

- Our organization has produced a number of breakthrough ideas in the past, and we currently have ideas in our pipeline that could become breakthroughs for tomorrow.

- agree completely (3 points)

- we haven’t launched a breakthrough idea in recent memory (2 points)

- we have not discussed nor evaluated any big ideas that might produce a breakthrough for our company (1 point)

- In our company, there is a key person driving our overall innovation effort.

- agree completely (3 points)

- there are people who are more responsible for our innovation efforts than others, but there is not a single individual who is driving innovation at our company (2 points)

- no one is championing the innovation efforts at our company (1 point)

- In our company, we have systems in place that get us out in the market listening to customers on a regular basis.

- we listen regularly and are good at this (3 points)

- we did this once but it was awhile ago (2 points)

- we know we need to do this but somehow never find the time (1 point)

- 30We have an organized system in place that goes beyond focus groups and surveys to help us understand the unarticulated needs of customers.

- we are doing some interesting things in this area (3 points)

- we only occasionally survey customers and conduct focus groups (2 points)

- these methods were news to me (my company has never tried to identity unarticulated needs) (1 point)

- We constantly look at ways to strengthen the process by which we come up with ideas and bring them to life.

- our idea factory is humming and we continuously look to improve our processes in this area (3 points)

- we look at our idea factory as traditional R&D and new product development, and have taken only minor steps to enlarge our idea inputs (2 points)

- our idea factory seems to deliver only incremental ideas and is badly in need of retooling (1 point)

- In my company, we have enough people with the ability to champion ideas to fruition.

- agree completely (3 points)

- we have a few but not nearly enough who really have what it takes (2 points)

- disagree completely (1 point)

- Our organization recognizes and rewards entrepreneurial behavior and doesn’t punish people when they fail.

- I agree with this statement

- I can’t think of very many ways we truly recognize and encourage people who stick their necks out on an innovation project (2 points)

- Our company does nothing to recognize or reward entrepreneurial behavior

Scoring

If you scored from 24 to 30 points:

Congratulations! Your company is a stellar standout when it comes to innovation. To keep up the good work, use this book as a refresher course; look at what the Vanguard firms are doing to improve innovation effectiveness and for ideas you might borrow.

And remember, even though you scored in the highest category, consider retaking the quiz and looking at those questions where you rated your firm less than outstanding.

If you scored from 17 to 23 points:

While your organization has obviously taken steps to improve innovation capability, you will benefit from designing and implementing a more systematic approach—one that keeps innovation “on the radar” at all times. This book can help. Your score shows that so far, your efforts have not paid off. If you do nothing to further innovation, you may even be in danger of falling back into old habits and patterns. Use the ideas in this book as a springboard to build consensus for moving forward with designing a more robust systematic innovation process.

If you’re the CEO, ask your management team to read this book. This will help you and your top team communicate about the pertinent issues. And it will reinforce your commitment to innovation and get your entire team on board with the initiative.

Invite additional key colleagues to take this assessment. Compare your colleagues’ overall scores with your own. In what best practice areas do you and your colleagues agree? In what areas do you find disparity?

If you scored from 10 to 16 points:

Your organization needs a great deal of work to make innovation a core competence and a vehicle for driving growth. The step-by-step process outlined in the chapters ahead can help. As you read and absorb the message of this book, I suggest you speak casually with your colleagues and fellow managers. Try to understand why innovation is not yet on the agenda in your organization and what it would take to gain support for launching an innovation initiative. What does your firm most need to do: Drive growth? Do a better job of differentiating your offerings? Come up with new products, services, processes and strategies?

32If you believe that you are one of the few people in your organization who “gets it,” consider becoming the point person for innovation in your firm. The fact that you are reading this book proves that you have an interest in this subject. Who might you invite to join you? Ask yourself who else in your firm might you share this book with to begin the awareness-building process?

Chances are you did not score your company as an innovation stalwart. So if you’re ready, what follows is a discussion of the essential issues you must wrestle with in order to transform your company and generate growth.