Session E

Monitoring

performance against

budget

1 Introduction

Producing a correct and realistic budget takes time. Putting the information together can take you away from your main job of producing or providing a service and make you ask yourself if budgeting is really worth all the expense and effort.

We have seen the benefits, but unless budgets really work they are not worth preparing.

In this session we look at several ways in which budgets are used, and what makes them important, especially in terms of planning and control.

As a first line manager you will be involved in implementing the budget allocation of your section or department in detail. You will monitor operations and ensure that your work team works within budget as far as is possible, and will report on any differences from budget.

In this session you will see what costs you can control and which are uncontrollable. Knowing that will help you understand what actions you can take to make best use of the resources at your disposal and how to monitor those resources.

2 Budgetary control

All budgetary control systems follow basically the same steps:

![]() establish agreed budgets;

establish agreed budgets;

![]() report actual results to departmental managers;

report actual results to departmental managers;

![]() identify where actual performance differs from planned performance (these differences are called variances);

identify where actual performance differs from planned performance (these differences are called variances);

![]() analyse which department and which manager is responsible for the variances;

analyse which department and which manager is responsible for the variances;

![]() analyse why the variances have happened.

analyse why the variances have happened.

EXTENSION 5 Further aspects of budgetary control are featured in Budgeting for Non-Financial Managers by lan Maitland.

Activity 49

Acme Machine Tools Ltd prepared budgets for income from sales of machines (sales revenue) of £2,000,000 in the coming year. In the event, actual sales revenue turns out to be £1,750,000.

Identify two possible reasons why you think the variance (the difference between the planned and actual sales revenue) might have arisen, and who you think will be held accountable for the difference from the plan.

You may have thought of a number of possible reasons why the variance came about, but your suggestions can probably be grouped into these main areas:

![]() sales price per machine had to be lower than forecast;

sales price per machine had to be lower than forecast;

![]() the number of machines sold was fewer than forecast.

the number of machines sold was fewer than forecast.

Of course, these problems would have to be investigated in more depth to find out what was causing them. It might be something like poor delivery dates, low quality or a competitor putting a better or cheaper product on the market.

As to who would be held accountable or responsible, it will be whoever was responsible for preparing the sales budget, whether that was the sales director, sales manager or whoever. This person may not be directly to blame for the variance, but he or she carries the responsibility for the problem.

Depending on the causes identified, the sales director will wish to discuss the issues with other managers. Poor delivery dates may be down to the distribution manager or the production director; low quality may also be part of the production director's remit, or that of the research and development director.

In order to monitor what is happening, managers need budgetary control reports to be sent to them periodically, highlighting variances for which they are responsible. Regular control is more likely to prevent major problems at the end of the budget period.

2.1 Reporting actual results and

variances

Here is an extract from a budgetary control report for a manufacturing company.

| Budget | Actual | Variance | ||

| Sales revenue | 600,000 | 700,000 | 100,000 | Favourable |

| Less costs: | ||||

| Materials in factory | 250,000 | 280,000 | 30,000 | Adverse |

| Wages in factory | 100,000 | 120,000 | 20,000 | Adverse |

| Machine running costs | 45,000 | 50,000 | 5,000 | Adverse |

| Salaries in administration | 55,000 | 50,000 | 5,000 | Favourable |

| General administration | 20,000 | 15,000 | 5,000 | Favourable |

| Advertising | 15,000 | 20,000 | 5,000 | Adverse |

| 485,000 | 535,000 | 50,000 | Adverse | |

| Operating profit | 115,000 | 165,000 | 50,000 | Favourable |

As you can probably see from the figures above, a favourable variance indicates that:

![]() actual sales are greater than budgeted sales, or

actual sales are greater than budgeted sales, or

![]() actual costs are lower than budgeted costs.

actual costs are lower than budgeted costs.

An adverse variance indicates that:

![]() actual sales are lower than budgeted sales, or

actual sales are lower than budgeted sales, or

![]() actual costs are greater than budgeted costs.

actual costs are greater than budgeted costs.

In the example budgetary control report:

Sales - Costs = Operating profit.

You read just now that managers responsible for different budgets should periodically receive a budgetary control report, and should then be expected to explain variances. Usually senior management would be concerned with adverse variances of a certain size (some variance either way is almost inevitable), but favourable variances may also need investigation. This is because short cuts may have been taken to arrive at the apparent advantageous situation. Alternatively, managers may simply wish to learn from it for the future.

Activity 50

Refer back to the budgetary control report for the manufacturing company, shown above.

Below is a list of the managers who receive a copy. Against each job title, state the variance which you think each of them would have to explain.

Purchasing manager (reports to factory manager)

Factory manager

Marketing manager

You should have identified that the managers would have to explain the adverse variances as follows.

![]() Purchasing manager: materials in factory.

Purchasing manager: materials in factory.

![]() Factory manager: materials and wages in factory, machine running costs.

Factory manager: materials and wages in factory, machine running costs.

![]() Marketing manager: advertising.

Marketing manager: advertising.

2.2 Why have the variances happened?

As we saw in the budget preparation statement, problems are likely to be interrelated, so that what happens in one area may be the result of a decision made in another area.

It is worth investigating the sales variance as something might be gained for other aspects of the business from the successes being achieved here. The same can also be said in the areas of salaries in administration and general administration, where the favourable variances are significant.

Managers may not always be able to take action about variances, whether favourable or adverse. This is because:

![]() some costs will be non-controllable;

some costs will be non-controllable;

![]() some costs may arise in the department but the responsibility may lie elsewhere. For example, time wasted in one department may be caused by the failure of another department to supply information or materials.

some costs may arise in the department but the responsibility may lie elsewhere. For example, time wasted in one department may be caused by the failure of another department to supply information or materials.

Activity 51

This Activity may provide the basis of appropriate evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Think about your own organization.

a To whom do you report variances from budgets and how quickly do you need to report?

b Who, if anyone, reports variances to you?

c Why is it important for variances to be reported as required by your organization? How well are reports of variances followed up; are the causes always sought?

Your response will be related to your own job.

You are likely to report variances to your immediate line manager within a period depending on the significance of the variance. A major problem will require immediate reporting. In the same way, others may report to you.

The speed and extent of reporting depends on organizational policy and the trust you and your colleagues have in each other to deal with problems. You will presumably be able to take action on variances and take control of appropriate resources under your control, or make recommendations to your manager.

2.3 Non-controllable costs

Let's look a little more closely at what we mean by non-controllable costs. These are costs that are charged to a budget centre, the name given to a section of business on which a budget is built, such as sales or production, but which cannot be influenced by the actions of the people responsible for that budget centre.

Activity 52

Identify one example of what you think is a non-controllable cost that might be charged to the budget of your work area.

Here are some examples which came readily to my mind. I hope you can see that they are outside a manager's control.

![]() A portion of the rates charged to a departmental budget for the premises it occupies.

A portion of the rates charged to a departmental budget for the premises it occupies.

![]() Diesel fuel costs charged against the transport manager's budget where oil shortages cause prices to soar.

Diesel fuel costs charged against the transport manager's budget where oil shortages cause prices to soar.

![]() Heating costs in a work area where the heating system is controlled centrally.

Heating costs in a work area where the heating system is controlled centrally.

Since these are outside the control of the manager concerned, it's important to identify them separately. Let's look at why this is important.

Activity 53

Margaret Shaw is the manager of a school canteen with a monthly wages budget of £2,000. She receives a budgetary control report which tells her that the wages expenditure in her canteen for January, February and March has been £2,250 for each month.

Here are the reasons for overspending.

![]() January: extra staff employed to cover sickness.

January: extra staff employed to cover sickness.

![]() February: staff overtime to meet re-arranged schedules during annual school examinations.

February: staff overtime to meet re-arranged schedules during annual school examinations.

![]() March: implementation of a nationally agreed bonus scheme, which was not built into the budget.

March: implementation of a nationally agreed bonus scheme, which was not built into the budget.

We usually regard wages as a controllable cost. But is that entirely true in this case?

Decide whether the adverse variance in each month has been caused by controllable or non-controllable wages costs, and note briefly the reason for your decision.

| Controllable | Non-controllable | Reason | |

| January | ________________________________ ________________________________ |

||

| February | ________________________________ ________________________________ |

||

| March | ________________________________ ________________________________ |

Compare your answers with mine.

![]() January's variance is non-controllable. A reasonable allowance for sickness should be built into the budget, but extra cost caused by excessive sickness could hardly be controlled by the manager.

January's variance is non-controllable. A reasonable allowance for sickness should be built into the budget, but extra cost caused by excessive sickness could hardly be controlled by the manager.

![]() February's cost, however, is controllable. The manager should have anticipated this problem. Overtime costs for predictable events would certainly be regarded as being within the manager's control.

February's cost, however, is controllable. The manager should have anticipated this problem. Overtime costs for predictable events would certainly be regarded as being within the manager's control.

![]() March's extra costs are clearly non-controllable. National agreements lie outside the manager's control, and the budget will need to be adjusted to incorporate the extra payment.

March's extra costs are clearly non-controllable. National agreements lie outside the manager's control, and the budget will need to be adjusted to incorporate the extra payment.

We've said that it's important to discover who and what is responsible for any budget variance. This isn't a question of looking for someone to blame. The real issue is finding out why the variance has happened so that corrective action can be taken if necessary.

2.4 Causes of variances

At the beginning of this session we looked for reasons why there might be a variance on sales and decided that two of the likely causes are:

![]() the quantity sold is different from the quantity budgeted (volume);

the quantity sold is different from the quantity budgeted (volume);

![]() the selling price is different from the price budgeted (price).

the selling price is different from the price budgeted (price).

Let's see how the variance on sales for the manufacturing company referred to on page 87 would be presented in the budgetary control report for the sales director. First we need a little more detail.

Remember that the company budgeted to make £600,000 in revenue and actually made £700,000. Why did this happen?

On investigation, we discover that the company budgeted to sell 50,000 units at £12 per unit, but actually sold 56,000 units at £12.50 per unit. How does this information help us?

We need to analyse the total sales variance into a volume variance (selling 6,000 more units than expected) and a price variance (selling units at 50p more than expected).

This can be presented as follows. (Don't worry too much about the maths at this point.)

| Budget | Actual | Variance | |

| Sales volume | 50,000 units | 56,000 units | £72,000 Favourable |

| Selling price | £12.00 | £12.50 | £28,000 Favourable |

| Sales revenue | £600,000 | £700,000 | £100,000 Favourable |

Having broken down the causes of the sales variance, the company needs to discover the underlying reasons.

Perhaps, in this case, the unit price was increased because another supplier went out of business and supplies were scarce, or because less discount was offered to customers. There could be all sorts of reasons.

We've seen that it's important to analyse sales variances by:

![]() volume;

volume;

![]() price.

price.

We can analyse any variance on costs in a similar way.

Activity 54

Remember our manufacturing company has an adverse variance of £30,000 on the cost of materials in the factory. Jot down the two headings under which you think those cost variances could be analysed.

You may not have used the same words as I have but anything on similar lines is acceptable.

![]() Volume

Volume

Did the business need more materials than budgeted to produce the units?

![]() Expenditure

Expenditure

Did it have to pay more for the materials than budgeted?

All types of costs can be analysed in this way but we're just going to concentrate on two:

![]() labour;

labour;

![]() materials.

materials.

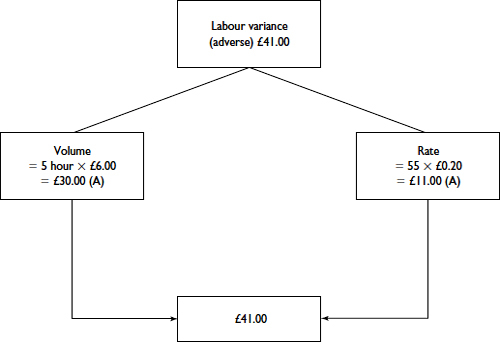

Activity 55

A job is budgeted to take 50 hours and the labour per hour is £6.00. The actual hours taken are 55 and the hourly rate paid is £6.20.

Calculate the labour cost variance and suggest two reasons which you think might have caused the variances in time and the rate.

Budgeted cost = _____________ × _____________ = _____________

Actual cost = _____________ × _____________ = _____________

Variance = _____________ (A/F)

Here are my calculations to compare with yours.

Budgeted cost = 50 × £6.00 = £300

Actual cost = 55 × £6.20 = £341

Total variance = £41.00 (A)

We can break down the total variance like this.

![]() For the volume variance, calculate the number of excess hours worked (55 – 50 = 5) and multiply this number by the budgeted hourly rate of pay (£6).

For the volume variance, calculate the number of excess hours worked (55 – 50 = 5) and multiply this number by the budgeted hourly rate of pay (£6).

![]() For the rate variance, calculate the difference between the actual rate paid and the budgeted rate (£6.20 – £6.00 = £0.20) and multiply this number by the actual hours paid (55).

For the rate variance, calculate the difference between the actual rate paid and the budgeted rate (£6.20 – £6.00 = £0.20) and multiply this number by the actual hours paid (55).

You may have suggested some of the following for the causes of the variances.

The volume variance might be caused by:

![]() slack work practices resulting from poor supervision;

slack work practices resulting from poor supervision;

![]() machine breakdowns;

machine breakdowns;

![]() technical problems;

technical problems;

![]() bottle-necks, leading to material shortages.

bottle-necks, leading to material shortages.

The rate variance might be caused by:

![]() overtime or bonus payments

overtime or bonus payments

![]() unbudgeted pay award.

unbudgeted pay award.

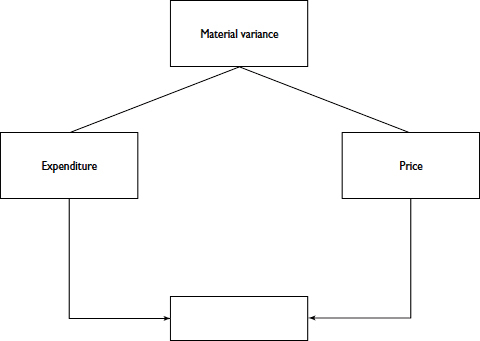

Now let's look at the cause of a total materials variance.

Activity 56

A job is budgeted to use 1000 kilos of material at £3.00 per kilo.

The actual usage is 1200 kilos, but the price is £2.50 per kilo.

Calculate the total material cost variance, and analyse that into the price and expenditure variances. Write your answers on this diagram.

The answer to this Activity can be found on page 125.

3 Flexible budgets and budgetary

control

In what we have said about budgetary control so far, we have assumed that we were using fixed budgets.

This means that, before the beginning of the period to which the budget relates, costs are budgeted for, and the budgeted costs remain the standard against which actual costs are compared, regardless of what happens during the budget period.

By using a flexible budget, on the other hand, we can make adjustments to costs if circumstances vary from the original budget.

A flexible budget is defined by the Chartered Institute of Management Accountants as:

‘a budget which is designed to change in accordance with the level of activity attained’.

A flexible budget in fact consists of a series of budgets. Each one is based on a different level of sales or output. As an example, a company might budget for three possible levels of output; costs are then calculated for each level.

EXTENSION 6

Managing Budgets, a title in the Essential Managers series by Dorling Kindersley, describes the usefulness of using spreadsheets in budgeting. By using spreadsheets, a change in level of activity of, say, 5% can quickly and easily be made.

Despite the extra effort required in preparing these, flexible budgets can be very useful. Software packages certainly enable flexible budgets to be prepared easily and cheaply.

The first thing we have to do is to analyse costs into:

![]() fixed costs, which do not vary with the level of production and sales;

fixed costs, which do not vary with the level of production and sales;

![]() variable costs, which do vary with production and sales.

variable costs, which do vary with production and sales.

Let's look at the difference this makes in practice.

We shall first assume that all costs are variable; that is, that they will vary in line with sales and production volumes. If we predict that production and sales will fall within the range of 2,000–3,000 units, we can work out the costs for both these figures.

Suppose each unit costs £5. Then the total costs for 2,000 units will be £10,000, and the total costs for 3,000 units will be £15,000.

The flexible budget would then look like this.

| Budget 1 | Budget 2 | |

| Production/sales | 2,000 units | 3,000 units |

| Costs | £10,000 | £15,000 |

In this case, the 2,000 units in Budget 1 is the lowest expected production/sales figure; the 3,000 units in Budget 2 is the highest expected figure. The actual figures are expected to fall somewhere in between these two.

Say now that actual performance is to produce and sell 2,500 units. In the budgetary control report, since sales have turned out to be within the expected range, the budget figure written in for sales will be the same as the actual figure. The actual cost can then be compared with the expected costs for that figure. In the case above, the budgetary control report might appear as follows.

| Budget | Actual | Variance | |

| Production/sales | 2,500 units | 2,500 units | |

| Costs | £12,500 | £12,000 | £500 (F) |

Here the actual sales turned out to be 2,500 units (which is within the budgeted range), so the ‘new’ expected costs are 2,500 £5 £12,500. The actual costs were £500 less than this, so the variance is favourable.

Of course, not all costs are in practice variable; there are always some fixed costs.

Activity 57

Let's assume that we regard 50% of our costs as fixed and 50% as variable. The fixed costs are £5,000.

Complete the flexible budget and the budgetary control report in this instance.

| Flexible budget | ||

| Budget 1 | Budget 2 | |

| Production/sales | 2,000 units | 3,000 units |

| Costs – fixed | £5,000 | |

| – variable | £5,000 | |

| Total costs | ||

| Budgetary control report | |||

| Budget | Actual | Variance | |

| Production/sales | 2,700 units | 2,700 units | |

| Costs | £13,000 | ||

As half the costs (£5,000) were fixed, they remain the same in Flexible Budget 2, even though sales are 1,000 more than in the first budget. But for Flexible Budget 2 we must calculate the expected variable costs for 3,000 units, as these do vary. We do this by working out the variable cost per unit from the first budget, and applying that to 3,000 units: £5,000/2,000 units £2.50 per unit.

The variable costs for Flexible Budget 2 are then:

£2.50 × 3,000 units = £7,500.

So the total costs for Budget 2 are:

£5,000 fixed costs + £7,500 variable costs = £12,500.

The completed table is therefore as follows.

| Flexible budget | ||

| Budget 1 | Budget 2 | |

| Production/sales | 2,000 units | 3,000 units |

| Costs fixed | £5,000 | £5,000 |

– variable |

£5,000 | £7,500 |

| Total costs | £10,000 | £12,500 |

Turning to the budgetary control report, the actual sales are 2,700 units and the actual costs are £13,000. We work out the flexible budget costs for 2,700 units as follows.

£5,000 fixed (£2.50 2,700) £11,750.

This gives an adverse variance of £1,250 (£13,000 £11,750).

So the completed table should look like this.

| Budgetary control report | |||

| Budget | Actual | Variance | |

| Production/sales | 2,700 units | 2,700 units | |

| Costs | £11,750 | £13,000 | £1,250 (A) |

3.1 The advantages of flexible budgets

Flexible budgeting is helpful to management in a wide variety of organizations where it is important to be able to take account of changes in circumstances.

Flexible budgets are particularly useful at:

![]() the planning stage;

the planning stage;

![]() the end of the budget period, in order to revise figures to match reality and to plan for the future.

the end of the budget period, in order to revise figures to match reality and to plan for the future.

Using flexible budgets at the planning stage lets you consider the consequences of output being greater or less than expected, within a certain range.

So, if your planned output and sales are 10,000 units, flexible budgeting will allow you to consider in advance what will be the implications of achieving only 8,000, or what will be the opportunities of achieving 12,000 units.

Activity 58

The outpatient department of a busy district hospital plans for 25,000 out-patient visits a year. Resources – doctors, nurses, secretarial back-up, waiting rooms, etc. – are geared to cope with 25,000 visits. Management use flexible budgeting to consider in advance the problems associated with there being 20,000 or 30,000 visits.

Identify three problems which might be anticipated if there are as many as 30,000 visits.

The problems may appear endless. Among these are:

![]() failure to meet agreed service standards;

failure to meet agreed service standards;

![]() over-tired doctors and other staff;

over-tired doctors and other staff;

![]() overcrowding;

overcrowding;

![]() increased litigation.

increased litigation.

A flexible budget will show what the cost implications are across the board resulting from a change, so that managers can:

![]() think ahead;

think ahead;

![]() anticipate problems;

anticipate problems;

![]() arrive at possible solutions.

arrive at possible solutions.

4 Non-financial budgets

Let's look briefly at non-financial budgets. All the budgets we've looked at so far have been concerned with money, but we can use the same techniques to help us plan for other key factors.

Here, for example, is how they can be used to provide information for management decisions on the allocation of resources in a hospital.

| Medical specialism | Beds available | Occupancy (%) |

| Surgery | 80 | 75 |

| Medical | 105 | 80 |

| Geriatric | 110 | 94 |

| Maternity | 38 | 89 |

| Gynaecology | 20 | 80 |

Now this may not appear like a budget, but the hospital managers are:

![]() planning for bed usage;

planning for bed usage;

![]() recording their resources (beds);

recording their resources (beds);

![]() recording the actual outcome (percentage occupancy);

recording the actual outcome (percentage occupancy);

![]() presumably using the information for future plans.

presumably using the information for future plans.

Activity 59

Take a look at the above table.

![]() Which service is most efficiently managed?

Which service is most efficiently managed?

![]() Which service may be worth reducing?

Which service may be worth reducing?

Geriatric beds are occupied 94% of the time and are used very efficiently. Compared with this, surgery beds are only 75% occupied and this may indicate that the service could be reduced.

Of course, the ‘beds available figure’ is just the tip of the planning iceberg. Allocating new beds implies that more nursing staff, medical staff and back-up resources will need to be allocated to the specialist areas. Percentage occupancy figures do not indicate costs.

So, you can see the budget process can help manage in a wide range of areas; it need not be restricted to financial statements.

5 Standard costing and budgetary

control

Standard costing is really a continuation of budgetary control. Let's see what it is and how it relates to budgetary control.

Here is how the Chartered Institute of Management Accountants defines standard cost.

‘Standard cost is a predetermined calculation of how much costs should be under specified working conditions and standard costing is therefore a system which uses standards for costs (and revenue) to allow detailed control by the use of variances.’

Using standard costs enables us to work out what performance should be under certain conditions, so that we can identify variances and so control actual performance.

Perhaps this sounds rather similar to what we have already said about budgeting, particularly using fixed budgets.

Both standard costing and budgeting are:

![]() concerned with setting performance standards for the future;

concerned with setting performance standards for the future;

![]() aids to control.

aids to control.

They are not, however, the same thing.

The important difference is that:

![]() budgets are concerned with totals – such as the costs of an entire department;

budgets are concerned with totals – such as the costs of an entire department;

![]() standard costs are concerned with individual units; each item of production, for instance, will have a standard cost.

standard costs are concerned with individual units; each item of production, for instance, will have a standard cost.

Activity 60

If standard costing is concerned with individual units, do you think that this involves more or fewer people in budgetary control than in budgeting? Give reasons for your answer.

Standard costing takes budgetary control ‘further down the line’, and involves more people in having responsibility for meeting standards in their particular area of work. The advantages of having people involved are:

![]() if unit costs are applied widely and lots of people are monitoring them, it is possible to identify variances on a much wider range of items, so improving control;

if unit costs are applied widely and lots of people are monitoring them, it is possible to identify variances on a much wider range of items, so improving control;

![]() the setting of standards gives everybody a target to aim for and is likely to make more people cost conscious.

the setting of standards gives everybody a target to aim for and is likely to make more people cost conscious.

Self-assessment 5

1.List five basic steps of budgetary control systems.

2.State what is indicated by favourable and adverse variances.

3. Identify whether the following are controllable or non-controllable costs.

| Controllable | Non-controllable | |

| a The produce purchased and sold by a greengrocer. | ||

| b The rent of a chair in a hairdressing salon. |

4. Prizewinning Blooms expects to sell 100 bunches of red roses at £8.50 per bunch on Valentine's day. Sales are hit by a newspaper promotion of chocolates and the business is only able to sell 90 bunches by reducing them to £7.00 per bunch.

Calculate the total sales variance and indicate if it is favourable or adverse.

5. Jack Simmons has received an estimate for painting a room of £320, being 16 hours at £20. As the painter was unable to complete the job and a less qualified person completed it, the actual cost was for 24 hours at £13 per hour.

Calculate the total labour cost variance and indicate if it is favourable or adverse.

6. Briefly explain why flexible budgeting is useful to management.

7. A local theatre group has fixed costs of £200. It sells tickets for £5.00 each of which £3.00 is taken up by variable costs. How many tickets must the group sell to break even?

Answers to these questions can be found on pages 123–4.

6 Summary

![]() Budgets must be put to use to achieve optimum results in organizations, in order to justify the time and effort involved in preparing them.

Budgets must be put to use to achieve optimum results in organizations, in order to justify the time and effort involved in preparing them.

![]() Budgetary control allocates responsibility to managers who must achieve a plan, and allows for the identification and analysis of variances.

Budgetary control allocates responsibility to managers who must achieve a plan, and allows for the identification and analysis of variances.

![]() Managers are held responsible for cost variances if these costs are within their control.

Managers are held responsible for cost variances if these costs are within their control.

![]() Budgetary control can be achieved through fixed or flexible budgets, but flexible budgets are more useful.

Budgetary control can be achieved through fixed or flexible budgets, but flexible budgets are more useful.

![]() Non-financial budgets can provide management with useful information.

Non-financial budgets can provide management with useful information.

![]() Budgetary control is improved by a system of costing such as standard costing.

Budgetary control is improved by a system of costing such as standard costing.