Session C

Controlling and

reducing costs

1 Introduction

There are two main ways of controlling costs: effective monitoring (for which good information is needed) and active control. In this session we shall look first at how information can be collected and used, so that the person who controls costs is involved in monitoring them, and thus becomes highly cost-conscious.

Once costs have been collected (in cost units and cost centres), variances can be calculated. Most organizations accept that some level of variance is inevitable. However, at some point an adverse variance becomes unacceptable, and its adverse effects must be reduced. The first line manager may then be called upon to take more active control measures.

Sometimes a first line manager may be called on to reduce costs in a cost-cutting exercise. This is a more extreme form of cost control, which we shall also look at here.

Let's begin by looking at a few decisions in which cost information is very important.

2 Cost information and decisions

Consider the following Activity.

Activity 20

Below are three questions on cost. For each one, jot down what you think would be the kind of decision that will be made as a result of the question being answered.

![]() How many units of a proposed new product are likely to be sold, and what are the fixed costs? Once this question is answered, you would use the information to help you decide

How many units of a proposed new product are likely to be sold, and what are the fixed costs? Once this question is answered, you would use the information to help you decide

![]() How much does it cost to feed a patient in hospital for a week (a) using the hospital kitchen, (b) using an outside caterer? The answer to this question might lead the hospital authorities to investigate

How much does it cost to feed a patient in hospital for a week (a) using the hospital kitchen, (b) using an outside caterer? The answer to this question might lead the hospital authorities to investigate

![]() Can gas from a certain field be sold at more or less than the cost of extracting it? No further changes to working practices are possible. The answer to this question might lead to

Can gas from a certain field be sold at more or less than the cost of extracting it? No further changes to working practices are possible. The answer to this question might lead to

In the first instance, by knowing the fixed costs and a good estimation of likely sales, you can work out how the fixed costs can be spread over each unit sold. This will help in setting a price per unit to provide a profit. This is a pricing decision, based on break-even analysis.

In the second instance, hospital authorities can investigate whether it is cheaper to use their own kitchens and staff or to buy in the services of an outside caterer. There may well be things other than costs, such as the need to meet specific dietary needs or deal with rapidly changing volumes of patients, which affect the decision. This is a ‘make or buy’ decision.

Finally, gas fields in which the costs of extraction exceed the selling price are closed down because they are unprofitable. As with the earlier decisions, costs will not be the only things looked at, but they will be important. This is a closure decision.

The three kinds of decision we have looked at – pricing, ‘make or buy’ and closure – are major decisions made in a wide range of industries. Without collecting information about costs on a regular basis, organizations may not even know whether a particular process makes a profit or runs at a loss, or whether it would be cheaper for them to make something themselves or buy it in. Costs and cost information are therefore important to managers making a wide range of decisions.

2.1 Basic cost statements

A cost statement is often used to show the breakdown of costs so that the final cost of a product or service can be analysed.

Let's begin by looking at a manufacturing example. It's helpful in manufacturing to identify another cost: the total factory cost. This includes all the prime or direct costs plus all the indirect costs arising out of the need to keep the factory (but not the offices) running. Indirect costs are factory overheads.

Activity 21

Write down one example of an appropriate cost beside each item shown in the following cost statement for the production of a car. I've given examples of factory overheads to help.

| £ | £ | Example of appropriate cost | |

| Direct material | 2,500 | ||

| Direct labour | 2,500 | ||

| Prime cost | 5,000 | ||

| Factory overheads | 3,500 | Production line, lighting, heating, | |

| Total factory cost | 8,500 | health and safety expenditure | |

| Administrative overheads | 1,000 | ||

| Selling and distribution overheads (including dealer's profit margin) | 1,500 | 2,500 | |

| Total costs | 11,000 | ||

| Profit | 1,000 | ||

| Selling price | £12,000 |

You could have thought of all sorts of things, since the manufacture, selling and distribution of a car is a complex process involving many people.

Under the prime cost heading, you could have identified any of the raw materials that go into a car and the wages of anybody directly involved in production.

Administration could be anything to do with purchasing, payments, stock control or any of the paperwork involved in running a business.

Selling and distribution would include advertising, promotions, delivering cars to the dealers and getting them in showroom condition.

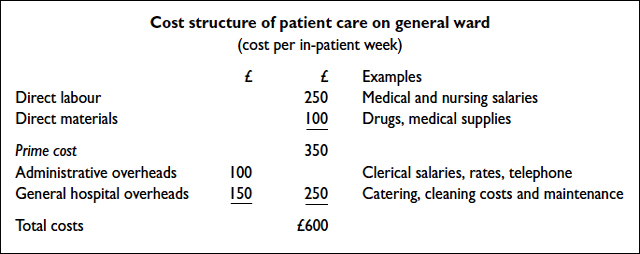

Now let's see how this sort of analysis can be used if we adapt it slightly for an organization, such as a hospital, which provides a service.

We'll say it costs about £600 a week to keep a patient in a general ward in hospital.

Once again, the costs are broken down into direct costs and overheads.

2.2 Cost units

Costs can be divided into direct costs and overheads. However, this analysis is only useful if the costs relate to an identifiable item, called a cost unit. In the example of the cost of producing a car, the car was the cost unit. In the case of the hospital, it was an in-patient week. Each organization defines its own cost units.

The most obvious cost unit is the finished product. For instance, a brewery may send out its beer in barrels or kegs which would be the cost units. A cement factory will probably send its cement out by the tonne, so will probably use a tonne of cement as a cost unit.

Cost units can be used by organizations that provide a service too.

Activity 22

Jot down what you think might be the cost units used by:

![]() swimming baths

swimming baths

![]() a school canteen

a school canteen

![]() letter delivery at Royal Mail

letter delivery at Royal Mail

Swimming baths would probably use a bather as a cost unit. A school canteen could use individual meals produced as a cost unit. Royal Mail is a more difficult problem. You could have suggested an individual letter or package for the sorting office, or an individual address for delivery staff.

In fact, a business can analyse any part of the workplace and work out appropriate cost units. For example, some of the cost units we might find in a car factory are:

![]() final product – cost per car;

final product – cost per car;

![]() electricity cost – cost per kilowatt hour the production line is running;

electricity cost – cost per kilowatt hour the production line is running;

![]() computer running cost – cost per computer minute of operation;

computer running cost – cost per computer minute of operation;

![]() canteen – cost per canteen meal.

canteen – cost per canteen meal.

In a complex organization, analysing costs at a more detailed level like this will help the people responsible for those costs to monitor them, and take action if necessary.

This leads us to the subject of cost centres.

3 Cost centres

A cost centre is a location where costs can be identified, grouped together and then finally related to a cost unit.

A cost centre is, in other words, a collection point for costs.

By a ‘location’ I mean something like:

![]() a department within a particular workplace;

a department within a particular workplace;

![]() a work area;

a work area;

![]() a machine or group of machines;

a machine or group of machines;

![]() a person, e.g. a hospital consultant.

a person, e.g. a hospital consultant.

The advantages of breaking down costs and collecting them in a number of cost centres are that:

![]() information on costs can be collected more easily;

information on costs can be collected more easily;

![]() information on costs in different parts of the organization can be provided;

information on costs in different parts of the organization can be provided;

![]() managers of particular cost centres can be given standards against which costs can be controlled.

managers of particular cost centres can be given standards against which costs can be controlled.

Identifying costs in cost centres helps to control costs in the various parts of the organization, and to control how each unit or department spends money.

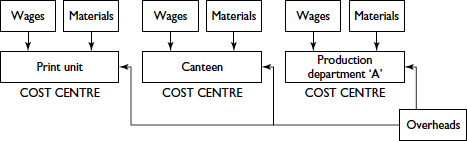

The diagram below shows an example of three cost centres within an organization. Each cost centre collects:

![]() costs of materials and labour used within the centre;

costs of materials and labour used within the centre;

![]() a proportion of the overheads for the whole organization.

a proportion of the overheads for the whole organization.

Collection of costs in cost centres

Activity 23

Look at the diagram on the previous page and decide into which cost centres you would collect the following costs:

Paper for digital print machine ________________________________

Cook's wages ____________________________________________

Wages of machine operator working in Department A _______________

It looks as though paper for the digital print machine is a print unit cost; the cook's wages are a canteen cost; and the machine operator's wages are a cost incurred in production Department A. Each cost centre would collect the costs relevant to it.

The canteen and the print unit are providing a service to other parts of the organization. So we can distinguish between two types of cost centre:

![]() service centres, and

service centres, and

![]() product centres.

product centres.

An important aim of a manufacturing organization is to make goods; that's how it earns its income. All services (such as the canteen, the stores, the maintenance department and so on) exist only to assist in that aim. Therefore, all costs must be finally transferred from the service centres to the product centres. The total costs of the product centre will then be spread over the cost units it produces.

For a building firm, the total cost of building houses is made up of many different individual costs. If the firm provides safety helmets for its workers, the cost of the helmets may be initially part of the materials costs for a ‘safety department’ cost centre. Ultimately these costs must appear in the cost of each house, the cost unit.

You may be thinking that this process sounds rather complicated and difficult to manage. It is, if it is not organized properly. Collecting costs is a detailed process that can only be done effectively by using cost codes for every item of cost. It is very often the role of the first line manager to ensure that the correct cost codes are created and used. So let's look at them now.

3.1 Cost codes

A good cost system enables costs to be:

![]() collected;

collected;

![]() analysed;

analysed;

![]() controlled.

controlled.

This means that we have to be able to find out precisely what expenses have been incurred in any part of the workplace, and we have to know how much we are spending in the workplace as a whole on different sorts of expense (overtime, electricity, stationery, etc.).

To help us do this a system of cost codes is often used. This will mean having two types of code:

![]() a special code for each cost centre, which will identify any costs incurred in that cost centre;

a special code for each cost centre, which will identify any costs incurred in that cost centre;

![]() a special code for each type of cost – such as stationery – wherever it occurs throughout the workplace.

a special code for each type of cost – such as stationery – wherever it occurs throughout the workplace.

By combining the cost centre code (for the accounts department, for example) and the code identifying the type of cost (stationery), we can identify how much has been spent on any particular item in any particular cost centre, and so control costs throughout the organization.

Let's look at how a cost coding system works.

Each workplace uses certain groups of numbers to mean particular things. These groups usually contain enough spare numbers for new kinds of cost to be added to the list of codes. For instance, a workplace with seven different cost centres may allocate the group of codes 01, 02, 03, . . . 18, 19 to cost centres, providing plenty of room to expand the list.

Let's look at a selection of likely cost codes for a general hospital.

| Hospital cost centres | Codes | Items of expenditure | Codes |

| Ward 1 | 001 | Ward sister's salary | 025 |

| Ward 2 | 002 | Staff nurse's salary | 026 |

| Ward 3 | 003 | Cleaner's wages | 107 |

| Theatre 1 | 098 | Medical equipment | 400–449 |

| Theatre 2 | 099 | Drugs | 450–500 |

| Pharmacy | 171 | Laundry assistant's wages | 181 |

| Physiotherapy department | 264 | Cleaning materials | 600–630 |

| Laundry | 351 | Cook's wages | 197 |

| Canteen | 400 |

Sister's salary on Ward 2 will be coded 002 025. Cleaning materials for Ward 3 could be coded 003 610 or 003 622 or 003 630, because the range indicates different codes for different types of cleaning material.

Activity 24

Cost codes must be clear and well understood for them to be effective. A code for ‘sundry expenses’ is often overused.

Work out codes for the following. Where you have a range of numbers, choose any one from within that range.

![]() Theatre 1 staff nurse's salary ––––––––––––––––––– –––––––––––––––––––

Theatre 1 staff nurse's salary ––––––––––––––––––– –––––––––––––––––––

![]() Theatre 2 medical equipment ––––––––––––––––––– –––––––––––––––––––

Theatre 2 medical equipment ––––––––––––––––––– –––––––––––––––––––

![]() Physiotherapy department medical equipment ––––––––––––––––––– –––––––––––––––––––

Physiotherapy department medical equipment ––––––––––––––––––– –––––––––––––––––––

![]() Drug coded 459 and ordered for the pharmacy ––––––––––––––––––– –––––––––––––––––––

Drug coded 459 and ordered for the pharmacy ––––––––––––––––––– –––––––––––––––––––

![]() Canteen cook's wages ––––––––––––––––––– –––––––––––––––––––

Canteen cook's wages ––––––––––––––––––– –––––––––––––––––––

The answer to this Activity can be found on page 124.

Activity 25

Here is a list of some costs in the hospital to which cost codes have been allocated. One of them seems rather suspicious and would need to be checked out. (Tick the suspect code.)

098 107 ![]()

001 026 ![]()

400 457 ![]()

According to these cost codes, the canteen has been ordering drugs (400 457)! This sounds very worrying and needs investigating urgently.

What this activity shows us is that information on costs is not only used to help us minimize costs – it also helps to make sure that costs are only occurring where they should be.

A system of cost codes means that everybody in the workplace describes each kind of cost in the same way. Information about costs is simplified and is presented in a standard way, making it easier to interpret and analyse.

Cost codes, made up of cost centre code and type of cost code, also mean that every single cost can be traced to a certain cost centre, improving control.

Identifying certain kinds of expense by the same code throughout the work-place means that you can also see how much you are spending on certain things (overtime or electricity, for instance), overall. This will help in deciding how best to utilize resources, to minimize expenditure or to reduce total costs.

4 Control through cost centres

Whether the cost centre is a work area, a machine or a group of machines or a team of people, it could well be you, as first line manager, who is responsible for maintaining the cost centre and controlling the associated costs.

You might have to:

![]() requisition materials (materials);

requisition materials (materials);

![]() authorize and collect time sheets (labour);

authorize and collect time sheets (labour);

![]() control the level of overhead costs in your work area, such as electricity or telephone use.

control the level of overhead costs in your work area, such as electricity or telephone use.

Let's look at how materials and wages costs are collected in appropriate cost centres.

The collection and application of overhead costs is rather more complex, but we'll look at that later.

4.1 Cost centres and materials costs

A first line manager may have the responsibility for:

![]() raising a materials requisition for goods in the workplace stores which are needed for the job;

raising a materials requisition for goods in the workplace stores which are needed for the job;

![]() raising a purchase requisition for goods needed for the job, which are not in the stores and so have to be specially bought;

raising a purchase requisition for goods needed for the job, which are not in the stores and so have to be specially bought;

![]() taking care of materials once they are in the work area.

taking care of materials once they are in the work area.

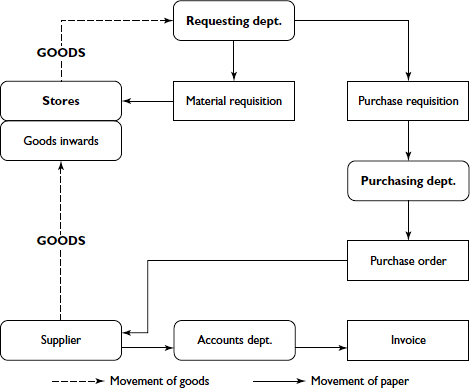

The diagram below shows an outline of the movement of paperwork and goods which take place when items are requested. The sharp-edged boxes denote paperwork, and the round-edged boxes denote locations.

Movement of paperwork and goods

Activity 26

Look at Figure 2 and identify three people or departments, apart from the requesting department and the supplier, who have a part to play in the materials costing system.

Against each one write down briefly what you think their responsibilities are.

Here is my breakdown of the roles played by various departments in the materials costing system.

![]() Purchasing department/purchasing officer:

Purchasing department/purchasing officer:

![]() ordering goods;

ordering goods;

![]() keeping lists of approved suppliers;

keeping lists of approved suppliers;

![]() checking supplier's prices.

checking supplier's prices.

![]() Goods inward department:

Goods inward department:

![]() receiving goods;

receiving goods;

![]() checking quality and quantity of goods supplied;

checking quality and quantity of goods supplied;

![]() issuing goods-received notes to accounts department.

issuing goods-received notes to accounts department.

![]() Stores department:

Stores department:

![]() storage and care of goods in store;

storage and care of goods in store;

![]() keeping records of receipts and issues to and from stores and current balances of items held;

keeping records of receipts and issues to and from stores and current balances of items held;

![]() issuing purchase requisitions when stock levels fall;

issuing purchase requisitions when stock levels fall;

![]() issuing supplies for certain jobs on receipt of a proper materials requisition note.

issuing supplies for certain jobs on receipt of a proper materials requisition note.

![]() Accounting department:

Accounting department:

![]() receiving and checking invoices against orders and goods received notes;

receiving and checking invoices against orders and goods received notes;

![]() keeping accounting records for the entire workplace;

keeping accounting records for the entire workplace;

![]() paying the supplier;

paying the supplier;

![]() costing materials for particular jobs;

costing materials for particular jobs;

![]() recording cost information.

recording cost information.

Activity 27

Look back at Session B on standard costing. How do you think a standard cost statement for making a particular item or providing a particular service would help a first line manager in requesting materials and controlling their cost?

I hope you can see that a standard cost statement helps the practical process in at least two ways. First, the manager can see what items are needed for a product or service, such as wire mesh and timber for a rat cage. Secondly, the manager can see how much they are expecting to pay for that material.

Without this sort of information, the materials requisition might just as well say: ‘enough stuff to make a rat cage, and hang the expense!’

4.2 Cost centres and labour costs

You are likely to be directly involved in the control and recording of labour costs. Your position gives you a degree of authority over your work team and responsibility for:

![]() controlling timekeeping, particularly important if you are monitoring a flexi-time system;

controlling timekeeping, particularly important if you are monitoring a flexi-time system;

![]() controlling quality of performance;

controlling quality of performance;

![]() recording time spent on individual jobs, if applicable;

recording time spent on individual jobs, if applicable;

![]() passing time records to the appropriate department for analysis.

passing time records to the appropriate department for analysis.

Other departments which will be involved to some extent in the labour costing system are:

![]() wages department;

wages department;

![]() accounts department;

accounts department;

![]() personnel department.

personnel department.

Time sheets or similar forms to record time spent at work are used to help in the calculation of labour costs.

The time sheet, illustrated above, has to be analysed before being passed to the wages department.

Activity 28

Using the information on the time sheet, fill in the blank spaces below, assuming a normal working week of 40 hours.

| Regular time ______________ hours at £6.00 | £ _________________ |

| Over time ______________ hours at £9.00 | £ _________________ |

| Gross earnings | £ _________________ |

The answer to this Activity can be found on page 124.

The first line manager is usually directly responsible for confirming that the records of how much time the work team has spent are true. In a flexi-time system, appropriate core time must be confirmed (i.e. employees should be at work when required) as well as attending for the appropriate total time within the flexible working pattern. But the team leader's responsibilities for labour cost control don't end here.

Typical additional responsibilities would include:

![]() allocating time to individual jobs;

allocating time to individual jobs;

![]() allocating an appropriate grade of staff to a particular job;

allocating an appropriate grade of staff to a particular job;

![]() controlling the amount of time spent on individual jobs by each member of the work team;

controlling the amount of time spent on individual jobs by each member of the work team;

![]() keeping idle time, such as travel time, to a minimum.

keeping idle time, such as travel time, to a minimum.

I hope you can see that knowing how much time should be spent by what kinds of staff, and how much that time should cost, will be useful to the manager in performing these tasks. As with materials, this information will come from the standard cost card.

To the practical responsibilities we can add the ‘paperwork responsibilities’ which go with the job:

![]() confirming that cost details shown for each job are correct;

confirming that cost details shown for each job are correct;

![]() passing costs per job to the accounts department for analysis;

passing costs per job to the accounts department for analysis;

![]() verifying idle time costs;

verifying idle time costs;

![]() passing details of idle time costs to the accounts department so that it can be properly accounted for. (Generally it needs to be apportioned on some reasonable basis over all jobs.)

passing details of idle time costs to the accounts department so that it can be properly accounted for. (Generally it needs to be apportioned on some reasonable basis over all jobs.)

Cost control is only worthwhile if it saves more for an organization than the costs of its operation. Too much time or paperwork and you should question its relevance.

A computer report which analyses time and services provided, is normally the key document in transferring labour cost information from a particular work area to whoever is responsible for summarizing cost information.

Activity 29

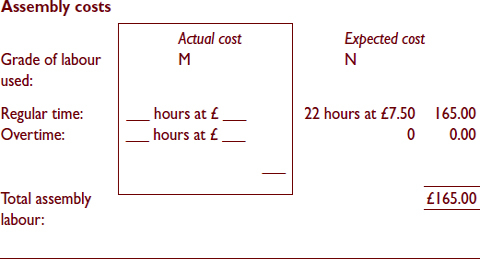

A Brown, whose time sheet we saw in Activity 28, spent the whole of Monday, Tuesday and Wednesday starting and completing the assembly of Product X.

Fill in the actual labour cost for Product X on the computer report below. What does the comparison against the expected cost tell you?

PRODUCT X

The comparison against expected cost tells me

You should have come up with the following calculation.

PRODUCT X

I hope you can see that the cost has exceeded what was expected. This was because a lower grade of employee was used, who spent more time than was expected, including overtime.

How could the first line manager have controlled this overrun of costs? It depends on the circumstances. Perhaps a grade N employee was not available, or was sick. If so, the manager needs to consider reworking the work schedules so that the right numbers of the right grades of staff are always available. Perhaps training could be implemented to upgrade the grade M staff.

Alternatively, the situation may have been outside the manager's control. Product X might have been planned to arrive when grade N staff were available, but have been delayed by another department.

Now that we have raised the issue of control, let's have a look for a moment at the question of idle time.

Common causes are:

![]() equipment breakdown;

equipment breakdown;

![]() power failure;

power failure;

![]() waiting for work to be scheduled;

waiting for work to be scheduled;

![]() waiting for materials or tools;

waiting for materials or tools;

![]() waiting for instructions.

waiting for instructions.

Idle time is not normally charged directly against the job, but is regarded as a production overhead, or overhead incurred in providing a service. But if the fault can be traced to one particular department, it may be charged against that department.

For instance, say a factory maintenance programme, scheduled to be completed over a weekend shutdown runs late and production time is lost once everybody is back at work.

It seems obvious that in this case the fault can be traced back to the maintenance department and the cost of the idle time will be charged to it. In that case all the managers in the maintenance department have got some explaining to do.

4.3 Cost centres and overheads

Some overheads belong entirely to one cost centre, while some can be shared among several cost centres.

Where an overhead can belong entirely to one cost centre we say that it is allocated to the appropriate cost centre. The first line manager of that cost centre will bear the responsibility for controlling these overhead costs within the cost centre.

Activity 30

Think of two overhead costs from your own workplace which could be allocated entirely to one cost centre.

It's unlikely that we've thought of the same things, but here are a couple of examples that spring to mind:

![]() the wages of a manager in the food hall of a large superstore will be allocated to the food hall cost centre;

the wages of a manager in the food hall of a large superstore will be allocated to the food hall cost centre;

![]() the cost of an advertising promotion will be allocated to the marketing cost centre.

the cost of an advertising promotion will be allocated to the marketing cost centre.

Activity 31

Here are some more overhead costs, which are similar in that they can be allocated entirely to individual cost centres. Against each one, write down which of the following three classes of overheads it belongs to: production overheads, administration overheads or selling and distribution overheads.

![]() Wages of managers working entirely within a particular production department.

Wages of managers working entirely within a particular production department.

![]() Paint, oil and grease used in a certain production department.

Paint, oil and grease used in a certain production department.

![]() Wages of receptionists.

Wages of receptionists.

![]() Travelling expenses of sales staff.

Travelling expenses of sales staff.

The first two costs are production overheads, the wages of receptionists are likely to be an administrative overhead and the travelling expenses of the sales staff are a selling overhead. Each of these could be allocated directly and entirely to one cost centre, and the responsibility of controlling them is that of the cost centre manager.

Often, though, overhead costs have to be spread over a number of cost centres. These costs are controlled first of all in one cost centre and then apportioned between other cost centres, using an agreed method of deciding how they should be shared out or apportioned.

Here are some overhead costs that might be apportioned among various departments. I've also shown the cost centre where the cost would initially be controlled, and suggested a possible method for apportioning the cost between all departments.

| Type of cost | Cost centre where cost is initially controlled | Possible method of apportionment |

| Rent and rates | Property manager | Floor area occupied by various departments |

| Lighting and heating | Plant engineer | Building volume occupied by various departments |

| Insurance of equipment | Administration manager | Value of equipment in various departments |

Activity 32

In the space provided below, write down which cost centre you think should initially control each overhead and suggest a method by which they could fairly be apportioned.

| Type of cost | Cost centre where cost is initially controlled | Possible method of apportionment |

| Staff welfare | ||

| Advertising for staff | ||

| Building repairs |

Here are my suggestions. You may have thought of other equally reasonable suggestions, so don't feel that our answers have to be the same.

Where possible it is preferable to allocate overheads directly to cost centres, if there are clear and agreed bases for doing so rather than to apportion them between cost centres, as the overheads are identified as being generated by, or the responsibility of, those cost centres.

| Type of cost | Cost centre where cost is initially controlled | Possible method of apportionment |

| Staff welfare | Personnel manager | Number of staff per department |

| Advertising for staff | Personnel manager | Number of vacancies notified per department |

| Building repairs | Building and works manager | Floor area per department |

There is no hard-and-fast method of apportioning overheads. But methods should be logical.

How much control can first line managers have over costs that have been apportioned to them, rather than allocated to them directly?

The answer is somewhere between very little and none.

Looking at the example above, you should be able to see that the first line manager of a department cannot control at all how much the personnel manager spends on staff welfare. Whether they are charged at all for advertising staff vacancies can be controlled to some extent by limiting the number of staff being recruited. But how much per vacancy the personnel department spends is beyond their control.

Activity 33

How far can a departmental first line manager control the costs apportioned to the department for building repairs?

How much money the Building and Works Manager spends is beyond the first line manager's control, as is (in the short term) the chargeable floor area occupied by the department. The only way the first line manager can exercise some control is in trying to ensure that the department doesn't cause building repairs to be necessary.

It is not necessary for you to know more about the accounting process of allocating, approving or transferring costs. It is this awareness of costs, not accounting manipulations, which is the key to success. Cost consciousness is important managerial behaviour. Apart from being aware of information on costs how is a cost-conscious attitude fostered?

5 Cost consciousness

We've seen that controlling and keeping down costs demands continued effort. You have to be permanently on the look-out for performance levels

falling, materials and equipment being wrongly used, bottlenecks, idle time, untidy and slipshod ways of working and so on.

Clearly you can only do so much yourself. You need the support of the work team in looking for and maintaining ways of keeping down costs, and in keeping records of what is actually happening in your work areas.

If one person tries to keep costs down on their own by turning off lights when they go out, it will have little effect. But if that person can persuade a dozen others to do the same, increasing amounts can be saved.

So what can we do to make the work team aware of the costs and become enthusiastic about keeping them down?

Activity 34

This Activity may provide the basis of evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Suggest two ways in which you think you could make your work team more cost conscious. How would you implement your suggestions?

Typical answers might include:

![]() getting the work team more involved;

getting the work team more involved;

![]() encouraging them to make suggestions;

encouraging them to make suggestions;

![]() offering prizes for suggestions on how to keep costs down;

offering prizes for suggestions on how to keep costs down;

![]() passing on information about costs;

passing on information about costs;

![]() telling them when costs increase or decrease.

telling them when costs increase or decrease.

Perhaps you might talk to your work team or put up notices and then follow up with meetings, discussions and so on.

If you are compiling an S/NVQ portfolio you may be able to use notices and testimony from your work team members and your manager as the basis of possible acceptable evidence.

5.1 Spotting the need for cost

consciousness and control

To be really successful at being conscious of costs and hence controlling them, you have to be aware of those areas of your work team's operations where costs may be a problem. One way to do this is by analysing costs in terms of variances. As we have seen, these show both the cause of the cost and its size. Together the analysis allows us to both spot a problem and do something about it.

Activity 35

Look at the possible adverse variances below. Against each one, jot down what you could do to affect them.

Materials

Adverse price variance

Adverse usage variance

Labour

Adverse efficiency variance

Adverse rate variance

Adverse idle time variance

Overheads

Adverse price variance

You will probably have jotted down answers based on what is familiar to you, but in general I expect our answers will not be very different from each other.

| Materials price variance | Check that the best price possible is being obtained for materials from suppliers |

| Materials usage variance | Check that there is not excessive wastage in the process |

| Labour efficiency variance | Check that staff are working effectively and have all the equipment and training that they need to do so |

| Labour rate variance | Check that staff of the right grade are being used on appropriate work, and that unnecessary overtime is not being worked |

| Labour idle time variance | Check that work is flowing smoothly into the work team, and that there are no hold-ups such as for machine breakdowns |

| Overhead variance | Check that the work team is not incurring unnecessary overheads and that prices obtained are reasonable. |

One other factor to bear in mind: it is always possible that the standard against which variances are measured has become out of date. This means that it is not your control of costs that is in question, but the relevance of the variances in the first place.

The three keys to success in raising cost consciousness are:

![]() involvement;

involvement;

![]() communication;

communication;

![]() feedback.

feedback.

5.2 Involvement and communication

Cost consciousness means treating costs in the workplace as though your money was going to be used to pay for them. Successfully finding ways of keeping costs down means keeping an eye on your spending all the time, rather than looking for one good idea. In the end your job and the money you earn depend on a successful operation, of which controlling costs is an important element.

We need to communicate with people about cost if we want them to become involved. The trouble is, much of the information used in the workplace to monitor costs is likely to be in the form of financial statements that are not easy to understand and which can easily put people off.

You and other team leaders need to give your team members information about costs in terms that are relevant, timely and in an appropriate place.

Activity 36

Here are two ways of communicating information about a quarterly electricity bill.

Tick whichever you think would make you more conscious of the cost of the electricity you are using.

We can make a case for saying that either of these would be effective for different people. Let's look at (a) first.

Sometimes the sheer size of a sum of money, like the cost of this electricity bill, can give people a jolt. £2,321.41 sounds a lot more serious than 6p per photocopied sheet.

However, large figures quickly baffle us and tend not to mean a lot. Electricity bills of £1,500, £2,400 or £13,967 all sound equally terrifying if our quarterly bill at home is about £100.

It's all too easy to feel that such a large sum is nothing to do with us. We feel that we didn't contribute much to the bill in the first place and there is nothing we can do to reduce it.

Knowing that each photocopy we take costs 6p is likely to make a bigger impression, because it relates directly to what we are doing, particularly if we have to use a counter that charges copies directly to our budget.

So, I would say that (b) is more likely to raise peoples awareness of the costs and prompt them to try to do something about them than (a).

This sort of information doesn't just have to be in the form of some kind of notice. Just saying something like:

‘This aluminium wrapper is £50 a roll now. I don't think we should let it get knocked about.’

or

‘We've just spent £200 having these blades reset. Better make sure that no grit gets in there.’

may have a similar effect.

Activity 37

Refer back to the two notices about costs.

Which do you think is a more effective place to display the information these notices contain: on the canteen notice-board or above the photocopier?

Information about costs will make more impact if it is provided where the cost is about to be incurred and just as it's going to be incurred.

What we read as we are about to use a piece of equipment is harder to avoid than information on the canteen notice-board.

Of course, like many notices, we can get used to them in time and fail to see them. It is useful to replace them with new and different, but striking, notices regularly.

We can say that information about costs needs to be:

![]() in a form we can relate to;

in a form we can relate to;

![]() at the time and place the cost is incurred.

at the time and place the cost is incurred.

5.3 Feedback

Now let's look at feedback – the response you give to the work team's efforts to keep costs down or to their suggestions for cost savings.

Activity 38

Suppose somebody in your workplace suggests a change to a certain process that will reduce costs. The change is approved and made, and there is an article about it in the house newspaper. Write down two important pieces of information that you would hope to find in the article.

You may have had several ideas but I hope among them would be:

![]() the name of the person who made the suggestion;

the name of the person who made the suggestion;

![]() how much money it will save.

how much money it will save.

If we are to be aware of costs, we want to know how much we're saving by our efforts. Certainly, if we're going to maintain an interest in costs, we need to know that we're making progress. By recognizing who suggested the cost saving, further emphasis is placed on its importance.

Of course, not all suggestions are necessarily good ideas.

Activity 39

Somebody in your work team suggests changing your computer stationery supplier. He has spoken to a representative from an alternative supplier and obtained some prices. On the face of it, it looks as though the alternative supplier's prices are less than you are currently paying. Investigating further, you find that the prices apply only to larger volume purchases than you would make and that the existing supplier has a better reputation for quality and reliability.

Tick the appropriate box to indicate if you would:

a let the subject drop because telling your work team member might discourage him from making further suggestions |

|

b tell him that it wasn't a workable idea |

|

c thank him for taking the trouble to find out about the alternative supplier and explain who you weren't going to take up the suggestion |

You probably chose (c).

It is easy to understand that, even though the suggestion isn't taken up, people need feedback on their ideas if they are to maintain an interest. However, it's not easy to remember to supply that feedback when we're under a lot of pressure to do all sorts of other jobs.

It's worth making the effort, however. If you don't encourage cost consciousness, even when it is not directly useful, it won't be there when you need it.

EXTENSION 3 Chapter 7 of David Doyle's book Cost Control: A Strategic Guide looks at cost responsibility and awareness in some depth.

6 Checklists for controlling costs

Finding ways of controlling costs and keeping them down depends upon thinking about every situation in the workplace and asking whether we are making the best possible use of the resources involved and doing the task in question in the most efficient way.

The questions we need to ask ourselves, and the answers we will get, will vary with the job and the workplace.

I hope you will find the following checklists help you to channel your thoughts as you examine your work area to ensure you have your workteam operating efficiently. Use the space provided to make your own notes.

6.1 Checklist for the work team

![]() Do I use people with the right amount of skill for the job in hand?

Do I use people with the right amount of skill for the job in hand?

![]() Do I use highly paid people for low level work? If so, why? Can it be avoided?

Do I use highly paid people for low level work? If so, why? Can it be avoided?

![]() Are salaries reviewed regularly?

Are salaries reviewed regularly?

![]() Is all our overtime necessary?

Is all our overtime necessary?

![]() What causes idle time?

What causes idle time?

![]() Lack of materials?

Lack of materials? ![]() _________________________________

_________________________________

![]() Lack of available equipment?

Lack of available equipment? ![]() _________________________

_________________________

![]() Lack of precise instructions?

Lack of precise instructions? ![]() __________________________

__________________________

![]() Lack of supervision?

Lack of supervision? ![]() ________________________________

________________________________

![]() Is the work team good about timekeeping?

Is the work team good about timekeeping?

![]() Are all the members of the work team fully trained?

Are all the members of the work team fully trained?

![]() Is the work team fully competent?

Is the work team fully competent?

![]() Do their skills need bringing up to date?

Do their skills need bringing up to date?

![]() Is career development taken seriously?

Is career development taken seriously?

![]() Are they willing to try new ideas?

Are they willing to try new ideas?

![]() Is there any information they would like to know about the workplace, the organization or the product?

Is there any information they would like to know about the workplace, the organization or the product?

![]() How often do I make a point of chatting to them about themselves and the job?

How often do I make a point of chatting to them about themselves and the job?

![]() Do I ever have to explain what I want done several times?

Do I ever have to explain what I want done several times?

![]() Should I write instructions for any tasks the work team do?

Should I write instructions for any tasks the work team do?

![]() Are written instructions up to date, in the right place and readable?

Are written instructions up to date, in the right place and readable?

![]() Do I give the work team feedback on their performance regularly (not just when things go wrong)?

Do I give the work team feedback on their performance regularly (not just when things go wrong)?

![]() What is our absenteeism record like?

What is our absenteeism record like?

![]() How many of the work team have left in the past two years? Why?

How many of the work team have left in the past two years? Why?

![]() Have the work team any special skills or knowledge which we're not using?

Have the work team any special skills or knowledge which we're not using?

![]() What records do I keep to help make the best possible use of the work team?

What records do I keep to help make the best possible use of the work team?

6.2 Checklist for materials

![]() Do we use the cheapest materials for the purpose without reducing the quality?

Do we use the cheapest materials for the purpose without reducing the quality?

![]() Do we run out of materials? Why?

Do we run out of materials? Why?

![]() Do we have any out-of-date materials? Why?

Do we have any out-of-date materials? Why?

![]() Are any materials damaged during storage?

Are any materials damaged during storage?

![]() What control have I over:

What control have I over:

![]() production materials?

production materials?

![]() consumables – bags, stationery, paper, oil, grease, packing materials, cleaning materials, etc.?

consumables – bags, stationery, paper, oil, grease, packing materials, cleaning materials, etc.?

![]() Is scrap or waste material increasing/decreasing? Is work having to be done again to reach appropriate standards? Why?

Is scrap or waste material increasing/decreasing? Is work having to be done again to reach appropriate standards? Why?

![]() Is the workplace clean and tidy? How often do I check housekeeping?

Is the workplace clean and tidy? How often do I check housekeeping?

6.3 Checklist for overheads

![]() Do I report equipment faults as soon as they occur?

Do I report equipment faults as soon as they occur?

![]() Do I keep a record of the date and reason for machine failure?

Do I keep a record of the date and reason for machine failure?

![]() Is all our equipment regularly maintained?

Is all our equipment regularly maintained?

![]() How fully used is the equipment for which I am responsible?

How fully used is the equipment for which I am responsible?

![]() Could we get rid of any out-of-date machines?

Could we get rid of any out-of-date machines?

![]() Can I improve the layout of the equipment in my work area?

Can I improve the layout of the equipment in my work area?

![]() Are any machines standing idle? Why?

Are any machines standing idle? Why?

![]() Do we switch off lights and power when they are not needed?

Do we switch off lights and power when they are not needed?

![]() Do we backup overnight whenever possible? Do we reroute calls through a cheaper call provider, or use email?

Do we backup overnight whenever possible? Do we reroute calls through a cheaper call provider, or use email?

![]() What changes would I like to introduce in the way we work which will make us more efficient?

What changes would I like to introduce in the way we work which will make us more efficient?

![]() Which departments do I need to help me to do this?

Which departments do I need to help me to do this?

7 Cost reduction

So far we have looked at controlling costs within a situation where the same level of operations is being carried out. But there are times when an organization has to make difficult decisions about what it is doing, how and where.

A business may be losing money, or a non-profit organization may have lost funding. There may be no choice but to ‘cut costs’ by:

![]() closing down parts of its operations;

closing down parts of its operations;

![]() ceasing to make an unprofitable product or to provide a service that is not cost-effective;

ceasing to make an unprofitable product or to provide a service that is not cost-effective;

![]() outsourcing a service that is currently provided in-house, so that it is provided more economically by someone outside the organization.

outsourcing a service that is currently provided in-house, so that it is provided more economically by someone outside the organization.

Although these decisions will be made by senior managers, as a first line manager you may become caught up in this cost reduction process.

More than ever, it is important in this case to:

![]() have information (on what costs need reducing and how and when this will be done);

have information (on what costs need reducing and how and when this will be done);

![]() communicate with your work team (to provide information and feedback and to involve them).

communicate with your work team (to provide information and feedback and to involve them).

In some ways cost reduction can be said to be a more extreme form of cost control; but as it usually involves a cutback in the scale of operations it is a more difficult and painful process, often leading to redundancies, and the sale of buildings and machinery.

Activity 40

The School Meals Service has informed all school meals managers that their individual meals service must break even or be closed down and replaced by private contractors.

Isabel Smith, a school meals manager, can produce and sell a maximum of 1,000 meals per week.

She is told her weekly fixed overheads are £2,000. Education authority policy is to charge £1.50 per meal and Isabel cannot alter this.

She calculates that the variable costs per meal, all raw materials, are £0.50.

Work out the break-even for Isabel's canteen.

![]()

We can see that Isabel's position is fairly desperate! Here are her break-even calculations.

![]()

She cannot produce 2,000 meals because her limit for production and sales is 1,000. Unless she is allowed to increase prices drastically, close-down seems inevitable.

If she could raise her prices to £2.50, her surplus would be £2.00 per meal and, if she could sell her maximum number of meals (1,000), she would just break even.

Activity 41

This Activity may provide the basis of appropriate evidence for your S/NVQ portfolio. If you are intending to take this course of action, it might be better to write your answers on separate sheets of paper.

Have you been faced with such a problem as described above, requiring you to control your resources or make recommendations for the use of your resources so that costs can be cut?

Write down the tasks you had to complete and the reasons you were given for the changes needed.

Your response will be related to your own job. Perhaps you had to contribute to a decision whether a member of your work team should be made redundant or to think about whether a new piece of equipment would prove cheaper than one or two new people in the long term.

Self-assessment 3

- a Name the two types of cost included in prime cost.

b What additional costs are added to prime cost to arrive at the total factory cost?

- State what is meant by a cost centre.

- Identify the three characteristics of a good cost system.

- State the three keys to success in making a work team more cost conscious.

- How would you ensure that a worker's attention was drawn to information about costs?

- Why is it useful to use a checklist when examining your work area for ways to decrease costs?

Answers to these questions can be found on page 122.

8 Summary

![]() Managers need cost information to make decisions.

Managers need cost information to make decisions.

![]() Direct costs are related to the individual unit produced, e.g. cost of raw materials.

Direct costs are related to the individual unit produced, e.g. cost of raw materials.

![]() Overhead costs cannot be directly attributed to any one unit of production or service provided.

Overhead costs cannot be directly attributed to any one unit of production or service provided.

![]() Cost units are identifiable items against which the costs of a company, department or other defined part of the organization can be related.

Cost units are identifiable items against which the costs of a company, department or other defined part of the organization can be related.

![]() Cost centres are locations where costs can be conveniently collected and grouped.

Cost centres are locations where costs can be conveniently collected and grouped.

![]() A cost coding system can be used for tracking every cost in the workplace.

A cost coding system can be used for tracking every cost in the workplace.

![]() Direct material and labour costs are collected in cost centres and charged directly to the job. Overheads are also applied to job costs; many are estimates.

Direct material and labour costs are collected in cost centres and charged directly to the job. Overheads are also applied to job costs; many are estimates.

![]() To make the work team cost conscious:

To make the work team cost conscious:

![]() involve them;

involve them;

![]() pass on information;

pass on information;

![]() given them feedback.

given them feedback.

![]() Information about costs needs to be:

Information about costs needs to be:

![]() in simple terms which we can relate to;

in simple terms which we can relate to;

![]() available where and when the costs are incurred.

available where and when the costs are incurred.