Reflect and review

1 Reflect and review

Now that you'll have completed your work on Working with Costs and Budgets, let's review our workbook objectives.

You should be better able to:

![]() identify different costs and how they behave.

identify different costs and how they behave.

You have looked at direct and indirect costs, and materials, labour and general overhead costs.

![]() Which types of cost are under your control? What flexibility do you have in controlling them?

Which types of cost are under your control? What flexibility do you have in controlling them?

Costs can be classified in order to analyse them in the workplace. This allows us to record and control costs.We have worked through costing and in doing so seen how costs occur. Everything that happens within the workplace leads to a cost in some way.

![]() As a first line manager, can you clearly identify the main areas of cost in your work area and are you aware of the types of cost? Do any areas need clarifying? Make notes of any points which come to mind below.

As a first line manager, can you clearly identify the main areas of cost in your work area and are you aware of the types of cost? Do any areas need clarifying? Make notes of any points which come to mind below.

![]() Is your role in controlling costs clear, bearing in mind some areas of cost may need clarification? Are you fully in control of costs which are your responsibility? Are clarifications or changes needed?

Is your role in controlling costs clear, bearing in mind some areas of cost may need clarification? Are you fully in control of costs which are your responsibility? Are clarifications or changes needed?

![]() appreciate how important it is to control costs.

appreciate how important it is to control costs.

Fixed and variable costs are also important in organizations. It is unlikely that you can do much about fixed costs, but you can make best use of resources under your control which may be measured as variable costs.

![]() Can you identify anything you can do to improve the way you manage resources under your control?

Can you identify anything you can do to improve the way you manage resources under your control?

![]() understand how standard costing techniques help to control cost.

understand how standard costing techniques help to control cost.

Some organizations use standard costing which can be determined as ideal, expected or current standards. If used in your organization, do you feel that they are determined and used in the best way to motivate your work team?

![]() Make a note of improvements you could recommend or put into action.

Make a note of improvements you could recommend or put into action.

Standard costs are used as a standard against which to measure our performance. Standard costing is a common way of arriving at variances from target, allowing first line managers to make adjustments and take action to keep costs down.

![]() Do you feel that all standard costs identified in your work area are appropriate? Should you recommend to your manager that the standards should

be altered, even if you found that standards were determined in a logical way? Why? Make a note of any changes you could propose.

Do you feel that all standard costs identified in your work area are appropriate? Should you recommend to your manager that the standards should

be altered, even if you found that standards were determined in a logical way? Why? Make a note of any changes you could propose.

![]() Do you receive information about variances in a timely way? Would earlier receipt of information improve your effectiveness and how could this be achieved?

Do you receive information about variances in a timely way? Would earlier receipt of information improve your effectiveness and how could this be achieved?

![]() Use different methods for controlling and reducing costs.

Use different methods for controlling and reducing costs.

To plan for the future, maintain control and measure performance we need detailed cost information. A good way of doing this is to allocate costs into cost centres against locations such as:

![]() departments;

departments;

![]() groups of machines;

groups of machines;

![]() individuals.

individuals.

For cost centres to operate properly, first line managers need to record and communicate accurate information about the hours worked, idle time, material costs and so on.

![]() Can you think of ways to improve communication in your workplace? Make a note of any suggestions you have for change below.

Can you think of ways to improve communication in your workplace? Make a note of any suggestions you have for change below.

![]() Do you feel costs are appropriately allocated at present? Suggest changes for a fairer allocation below.

Do you feel costs are appropriately allocated at present? Suggest changes for a fairer allocation below.

Maintaining a good cost control system takes effort and can be frustrating, especially when you are working hard to keep the costs down but still finding it difficult to keep within budget. Controlling costs is a test of leadership.You will need to be aware of cost overruns, be able to communicate problems to management and your work team, and involve your work team in keeping costs down.

![]() How do you communicate the importance of controlling costs? Do you use notices and change them regularly so they are not ignored? Do you talk directly to your work team about cost control? Make a note of any improvements you feel you can make.

How do you communicate the importance of controlling costs? Do you use notices and change them regularly so they are not ignored? Do you talk directly to your work team about cost control? Make a note of any improvements you feel you can make.

![]() Is cost control rewarded in your workplace? Should it be? Perhaps you have some thoughts you can write down now to discuss with your manager in the future.

Is cost control rewarded in your workplace? Should it be? Perhaps you have some thoughts you can write down now to discuss with your manager in the future.

![]() Understand what a budget is and how they are used.

Understand what a budget is and how they are used.

A budget is an expensive exercise unless it is constantly used during the period it relates to. We've seen that it can be used to compare actual performance with planned performance, and flexed to take into account changes in circumstances, or to forecast what will happen in certain circumstances and to make plans accordingly. It also helps management to set targets which ensure the profitability of the organization.

![]() Can you think of ways to improve the way budgets are used in your work-place? Make a note of any suggestions you have for change.

Can you think of ways to improve the way budgets are used in your work-place? Make a note of any suggestions you have for change.

![]() Are any budgets you use at work flexed to an appropriate extent? Write down your thoughts for future discussions with your manager.

Are any budgets you use at work flexed to an appropriate extent? Write down your thoughts for future discussions with your manager.

![]() Help to draw up workable budgets.

Help to draw up workable budgets.

Budgets are a way of bringing together all an organization's plans and presenting them in a way that allows people to monitor their progress against them. As a first line manager you will be involved both in generating information for budget preparation and in ensuring that variances from budget are monitored and acted upon.

How are budgets prepared in your workplace? Is the sequence correct – is the budget that contains the limiting factor prepared first, and then communicated widely? Make notes of any areas in which you feel that the sequence or communication of budgeting is inadequate, and make suggestions for improvements.

Are you involved in collecting information for the preparation of budgets? Is the information you collect actually used? What other items of information do you think would be useful? Are your budgets up to date? Make notes on any areas of your work where out-of-date budget information has presented you with difficulties.

![]() Use some budgetary control techniques.

Use some budgetary control techniques.

Looking at fairly simple examples, we've used some budgetary control techniques which would be used in your workplace. These include flexible budgeting and standard costing. If you are involved in setting the budget in your work area or are on a budget committee, the work you have done in this workbook should have increased the confidence with which you handle the techniques.

![]() Make a note of techniques you could use in assisting your planning and control.

Make a note of techniques you could use in assisting your planning and control.

2 Action plan

Use this plan to further develop for yourself a course of action you want to take. Make a note in the left-hand column of the issues or problems you want to tackle, and then decide what you intend to do, and make a note in column 2.

The resources you need might include time, materials, information or money. You may need to negotiate for some of them, but they could be something easily acquired, like half an hour of somebody's time, or a chapter of a book. Put whatever you need in column 3. No plan means anything without a timescale, so put a realistic target completion date in column 4.

Finally, describe the outcome you want to achieve as a result of this plan, whether it is for your own benefit or advancement, or a more efficient way of doing things.

3 Extensions

| Extension 1 | Book Author Edition Publisher |

Simple and Practical Costing, Pricing and Credit Control Keith Kirkland and Stuart Howard First edition, 1998 Kogan Page |

| Extension 2 | Book Author Edition Publisher |

Financial Planning using Spreadsheets Sue Nugus First edition, 1997 Kogan Page |

| Extension 3 | Book Author Edition Publisher |

Cost Control: A Strategic Guide David Doyle First edition, 1994 Kogan Page |

| Extension 4 | Book Authors Edition Publisher |

The Business Plan Workbook Colin Barrow, Paul Barrow and Robert Brown Fourth edition, revised 2001 Kogan Page |

| Extension 5 | Book Author Edition Publisher |

Budgeting for Non-Financial Managers Ian Maitland 1999 Financial Times Prentice Hall 1999 |

| Extension 6 | Book Edition Publisher |

Managing Budgets: Essential Managers Series 2000 Dorling Kindersley |

These extensions can be taken up via your ILM Centre. They will either have them or will arrange that you have access to them. However, it may be more convenient to check out the materials with your personnel or training people at work – they may well give you access. There are good reasons for approaching your own people; for example, they will become aware of your interest and you can involve them in your development.

4 Answers to self-assessment

questions

Self-assessment 1 on pages 16–17

1 Direct materials costs can be identified directly and in total with an item being produced, whereas indirect materials costs have a more general use in an organization and cannot be identified directly and in total.

2 As reporters have a regular wage and advertising staff receive commission:

![]() the wages of the advertising staff are VARIABLE COSTS;

the wages of the advertising staff are VARIABLE COSTS;

![]() the wages of the reporters are FIXED COSTS.

the wages of the reporters are FIXED COSTS.

3 a Direct labour cost CAN be TOTALLY identified with a particular product.

b Wages which CANNOT be identified with a particular product are

INDIRECT labour costs.

c Direct labour costs are often VARIABLE costs because they increase or decrease in proportion to the production being carried out.

4 The break-even number of members is £18,000/£15 1,200 members.

5 The wastage of components used in the production of hard disks should be under Sam's control. Sam is not likely to be involved in marketing and sales so advertising is not controllable by Sam, nor is Sam's basic salary which would be set by senior managers.

Self-assessment 2 on page 32

1 (a) A standard cost is a PREDETERMINED cost that is achieved by setting STANDARDS related to particular circumstances or conditions of work.

2 The two reasons for setting performance standards in any organization are:

![]() to base costs upon them;

to base costs upon them;

![]() to measure actual performance.

to measure actual performance.

3 The standard cost of a vase is £2.50, calculated as follows:

Standard cost sheet

Direct materials: £8.00 ÷ 4 = £2.00

Direct wages: £7.50 ÷ 10 = £0.75

£2.75

4 Direct material cost variances comprise a usage variance and a price variance. Direct labour cost variances comprise an efficiency variance, an idle time variance and a rate variance.

5 A favourable variance indicates that actual costs are less than standard costs. An adverse variance indicates that actual costs are greater than standard costs.

Self-assessment 3 on page 68

1 a The components of prime cost are direct materials and direct labour.

b Factory overheads are added to prime cost to arrive at the total factory cost.

2 A cost centre is a location where costs can be identified, grouped together and then finally related to a cost unit.

3 A good cost system enables costs to be:

![]() collected;

collected;

![]() analysed;

analysed;

![]() controlled.

controlled.

4 The three keys to success are:

![]() Involvement;

Involvement;

![]() Communication;

Communication;

![]() Feedback.

Feedback.

5 Workers should be provided with information in a form they can relate to and at a time and place where the cost is incurred.

6 A checklist helps to channel thoughts and avoids the possibility of overlooking matters.

Self-assessment 4 on page 83

1 The four features of a budget are that it:

![]() is quantitative;

is quantitative;

![]() is prepared in advance;

is prepared in advance;

![]() relates to a particular period;

relates to a particular period;

![]() is a plan of action.

is a plan of action.

2 Budgets are essential for deciding at the outset whether an objective can be achieved and what actions this requires. They also give managers their targets and cost limits for the next period.

a Budgets are largely a waste of time unless they are actively USED in order to see whether the organization is MEETING its targets and keeping within its limits.

This helps to ensure that expenditure takes place according to plan.

b We use the term BUDGETARY CONTROL to cover the use of budgets to help an organization control its progress towards what it has set out to achieve.

Setting targets and encouraging people to adhere to them assists the organization through a disciplined approach.

c A budget will not be useful to an organization if it is managed so RIGIDLY that it does not permit some degree of flexibility.

Unless allowances are made for changes in circumstances, organizations can incur expenses and losses in trying to achieve the impossible.

Self-assessment 5 on pages 104–5

1 The five basic steps of budgetary control systems are to:

![]() establish agreed budgets;

establish agreed budgets;

![]() report actual results to departmental managers;

report actual results to departmental managers;

![]() identify where actual performance differs from planned performance using variances;

identify where actual performance differs from planned performance using variances;

![]() agree which department or who is responsible for variances;

agree which department or who is responsible for variances;

![]() analyse why variances have happened.

analyse why variances have happened.

2 A favourable variance indicates that actual sales are greater than budgeted sales, or actual costs are less than budgeted costs.

An adverse variance indicates that actual sales are less than budgeted sales, or actual costs are greater than budgeted costs.

3 a The goods purchased and sold by a greengrocer are controllable costs.

b The rent of a chair in a hairdressing salon is non-controllable.

4 The sales variance is calculated as follows.

| Budgeted sales revenue | 100 × £8.50 = £850 |

| Actual sales revenue | 90 × £7.00 = £630 |

| Total sales variance | £220 adverse |

(You could analyse the total sales variance as follows.

| Volume | 10 × £8.50 | £85.00 | adverse |

| Price | 90 × £1.50 | £135.00 | adverse |

| Total | £220.00 | adverse) |

5 The labour cost variance is:

| Budgeted cost | 16 × £20.00 = £320 |

| Actual cost | 24 × £13.00 = £312 |

| Variance | £8 favourable |

(You could analyse the total labour variance as follows.

| Volume | 8 × £20.00 | £160.00 | adverse |

| Price | 24 × £7.00 | £168.00 | favourable |

| Total | £8.00 | favourable) |

6 Flexible budgeting provides the opportunity to be able to take account of changes in circumstances and more closely monitor the position than is possible using fixed budgets.

7 The break-even number of tickets to be sold is calculated as:

| Sales price | £5.00 |

| Variable costs | £3.00 |

| Contribution per ticket | £2.00 |

Break-even point £200.00 £2.00 100 tickets

5 Answers to activities

Activity 15 on pages 24–5

Here are my completed calculations to compare with yours.

Standard cost sheet

| Direct materials: 5 metres at £6.10 | £30.50 |

| Direct wages: | |

| Moulder 1½ hours × £8.00 | £12.00 |

| Cutter 2½ hours × £10.00 | £25.00 |

| £67.50 |

So the standard cost of a table is £67.50.

Activity 24 on page 43

Since some of our codes provide a group of numbers, your suggested cost codes may not be exactly the same as mine, but I hope you can see how cost codes are actually made up.

Here are the numbers I would use:

![]() Theatre I staff nurse's salary: 098 026

Theatre I staff nurse's salary: 098 026

![]() Theatre 2 medical equipment: 099 400 (or any number to 449)

Theatre 2 medical equipment: 099 400 (or any number to 449)

![]() Physiotherapy department medical equipment: 264 400

Physiotherapy department medical equipment: 264 400

![]() Drug coded 459 and ordered for the pharmacy: 171 459

Drug coded 459 and ordered for the pharmacy: 171 459

![]() Canteen cook's wages: 400 197

Canteen cook's wages: 400 197

Activity 28 on page 48

I hope we can agree on the following figures:

| Regular time 40 hours at £6.00 | 240.00 |

| Overtime premium 3 hours at £9.00 | 27.00 |

| Gross pay for week | £267.00 |

Activity 56 on page 96

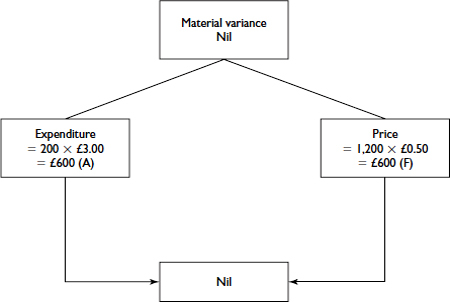

Budgeted material cost = 1,000 kilos × £3.00 = £3,000.

Actual material cost = 1,200 kilos × £2.50 = £3,000.

Variance nil

In this case, the lower price exactly counters the extra cost from using 200 kilos more than were budgeted for.

6 Answers to the quick quiz

7 Certificate

Completion of this certificate by an authorized person shows that you have worked through all the parts of this workbook and satisfactorily completed the assessments. The certificate provides a record of what you have done that may be used for exemptions or as evidence of prior learning against other nationally certificated qualifications.

superseries

FIFTH EDITION

Workbooks in the series:

| Achieving Objectives Through Time Management | 978-0-08-046415-2 |

| Building the Team | 978-0-08-046412-1 |

| Coaching and Training your Work Team | 978-0-08-046418-3 |

| Communicating One-to-One at Work | 978-0-08-046438-1 |

| Developing Yourself and Others | 978-0-08-046414-5 |

| Effective Meetings for Managers | 978-0-08-046439-8 |

| Giving Briefings and Making Presentations in the Workplace | 978-0-08-046436-7 |

| Influencing Others at Work | 978-0-08-046435-0 |

| Introduction to Leadership | 978-0-08-046411-4 |

| Managing Conflict in the Workplace | 978-0-08-046416-9 |

| Managing Creativity and Innovation in the Workplace | 978-0-08-046441-1 |

| Managing Customer Service | 978-0-08-046419-0 |

| Managing Health and Safety at Work | 978-0-08-046426-8 |

| Managing Performance | 978-0-08-046429-9 |

| Managing Projects | 978-0-08-046425-1 |

| Managing Stress in the Workplace | 978-0-08-046417-6 |

| Managing the Effective Use of Equipment | 978-0-08-046432-9 |

| Managing the Efficient Use of Materials | 978-0-08-046431-2 |

| Managing the Employment Relationship | 978-0-08-046443-5 |

| Marketing for Managers | 978-0-08-046974-4 |

| Motivating to Perform in the Workplace | 978-0-08-046413-8 |

| Obtaining Information for Effective Management | 978-0-08-046434-3 |

| Organizing and Delegating | 978-0-08-046422-0 |

| Planning Change in the Workplace | 978-0-08-046444-2 |

| Planning to Work Efficiently | 978-0-08-046421-3 |

| Providing Quality to Customers | 978-0-08-046420-6 |

| Recruiting, Selecting and Inducting New Staff in the Workplace | 978-0-08-046442-8 |

| Solving Problems and Making Decisions | 978-0-08-046423-7 |

| Understanding Change in the Workplace | 978-0-08-046424-4 |

| Understanding Culture and Ethics in Organizations | 978-0-08-046428-2 |

| Understanding Organizations in their Context | 978-0-08-046427-5 |

| Understanding the Communication Process in the Workplace | 978-0-08-046433-6 |

| Understanding Workplace Information Systems | 978-0-08-046440-4 |

| Working with Costs and Budgets | 978-0-08-046430-5 |

| Writing for Business | 978-0-08-046437-4 |

| For prices and availability please telephone our order helpline | +44 (0) 1865 474010 |

| or email | [email protected] |