10

Further Topics

10.1 More on Large Claim Reinsurance

While large claim treaties as discussed in Section 2.5 are not popular in practice (even if in particular on the facultative basis such contracts can occasionally be found), we want to illustrate here that from a mathematical perspective there are a number of elegant results on the quantities of interest available. We first deal with larger order statistics and subsequently look into large claims reinsurance and ECOMOR.

10.1.1 The Ordered Claims

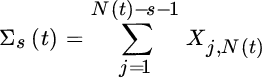

The sizes of the largest claims also depend on the random number of claims. Recall our notation for the order statistics

Consider an XL treaty with unbounded layer and retention x, and NR(t) denoting the number of claims for the reinsurer. The number of claims overshooting a retention x is at least equal to r if and only if the r largest order statistics overshoot the level x. Consequently

and

(which can already be found in Galambos [367]). Correspondingly, if N(t) comes from a Poisson process or Pascal process, so does NR(t) and these formulas lead to simple expressions for the c.d.f. of order statistics in terms of the respective sums (see Franckx [358] and Benktander [112] for the Poisson case and Kupper [519] as well as Ciminelli [214] for the Pascal case).

Let us consider the general case with independent claim number and claim size processes, and use the notation

for the probability of having fewer than r claims up to time t. Then from (5.6.37) we can write

Let us denote q = 1 − p = FX(x). Then by reversing the order of summation we easily find that

where the first term corresponds to the fact that not even r claims have turned up by time t. For the second term we use the well‐known equality

together with the definition (5.1.1) to obtain

where

If X is a continuous random variable with density fX, the corresponding density part (apart from a jump of size Πr(t) at the origin) is

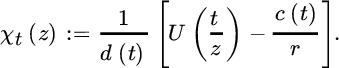

We now look into the one‐dimensional limit distribution of the rth largest order statistics (where r is kept fixed). Assume that there exist deterministic functions d(t) > 0 and c(t) such that when ![]()

where Vr is a non‐degenerate random variable. It is natural to assume here that ![]() . In terms of the tail quantile function

. In terms of the tail quantile function ![]() this means that for an extreme value index

this means that for an extreme value index ![]() and some auxiliary function a(x) > 0,

and some auxiliary function a(x) > 0,

cf. Definition 3.1. Take ![]() fixed. From (10.1.3),

fixed. From (10.1.3),

where

When ![]() both the integrand and the lower limit should tend to a reasonable limit. For the integrand it therefore seems natural to assume that the claim number process is nearly mixed Poisson, as defined in Section 5.3.1. Note, however, that the integrand is actually independent of the quantity t if the claim number process is mixed Poisson.

both the integrand and the lower limit should tend to a reasonable limit. For the integrand it therefore seems natural to assume that the claim number process is nearly mixed Poisson, as defined in Section 5.3.1. Note, however, that the integrand is actually independent of the quantity t if the claim number process is mixed Poisson.

The remaining convergence condition can then be formulated in the form that when ![]()

for a function ψ(x) to be determined. The latter condition can be identified with the extremal condition in terms of U if we choose ψt(0) = 1, c(t) = U(t) and d(t) = a(t) as in the condition on U. Under the two conditions we see that when ![]()

This result follows since for any fixed r, ![]() with

with ![]() while

while ![]() . Rewriting the extremal laws by an affine transformation, the result can be expressed in the following easier form:

. Rewriting the extremal laws by an affine transformation, the result can be expressed in the following easier form:

For ![]() and {N(t);t ≥ 0} near mixed Poisson, one has

and {N(t);t ≥ 0} near mixed Poisson, one has

where one of the three following cases emerges necessarily:

- γ > 0, c(t) = 0, d(t) = U(t) and ψ(y) = y−1/γ, y ≥ 0

- γ = 0, c(t) = U(t), d(t) = a(t) and ψ(y) = e−y

-

and ψ(y) = |y|1/|γ|, y ≤ 0.

and ψ(y) = |y|1/|γ|, y ≤ 0.

Notice that for a deterministic N(t) this result reduces to the classical extreme value laws discussed in Chapter 3. For the case r = 1 and N(t) discrete, see Galambos [367]. In this form the result is a special case of a more general weak convergence result in Silvestrov et al. [701] where even the independence condition between claim number and claim size processes is weakened considerably. It seems possible to derive more explicit statements in the case where FX is assumed to belong to Cγ with remainder conditions. In the mixed Poisson case particularly, no further complications should show up.

Moments.

Of course a full treatment of the behavior of the moments under a max‐domain of attraction is possible. We restrict our attention to a few direct results. Equation (10.1.3) can also be used to derive the consecutive moments of the order statistics. For ![]() we have

we have

The easiest way to prove this is by noticing that for a non‐negative random variable W and β > 0,

and that by (10.1.3)

The appearance of the quantile function is of course pleasing. It indicates precisely what information on the underlying two processes is needed. For the claim number process we need ![]() while the quantity

while the quantity ![]() incorporates the information requested on the claim size distribution.

incorporates the information requested on the claim size distribution.

The asymptotic expression of the moments under the domain of attraction condition is then easy if the claim number process is also near mixed Poisson. Indeed if ![]() with γ > 0, then for β ≥ 0 and

with γ > 0, then for β ≥ 0 and ![]()

When γ = 0 one can sharpen this result while using the full strength of the domain of attraction condition.

Combinations of order statistics.

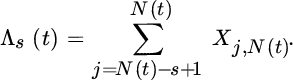

In this section we state a versatile formula that will allow us later to derive almost all desired expressions as special cases. In (10.1.1) we see that the first part of this ordered sample contains the small claims while on the right‐hand side of the scale we find the large claims; they are separated by intermediate claims. Let us use the following two abbreviations:

and

Here Σ refers to small while Λ refers to large. We easily arrive at properties of the claim fragments through the joint Laplace transform

where u, v, w ≥ 0. Conditioning on the number of claims at the time epoch t and interpreting Xr, N(t) = 0 whenever r ≤ 0, one can derive

Many special cases can be derived from this formula by properly choosing s, u, v and w. We give a couple of examples.

- For one order statistic. Choose u = w = 0 and take s = r − 1. Then we fall back on the Laplace transform of the order statistic XN(t)−r+1, N(t) as treated in (10.1.3).

- For all but the largest claims. Take now u = v = 0 and s = r − 1. ThenFor the special case where r = 1 we find the formula

for the transform of the sum of all but the largest claim. In the case of the Poisson claim number process this result goes back to Ammeter [38].

- For the smallest claims. Take u = 0 and again s = r − 1. ThenIf we invert this with respect to v we obtain the hybrid expression containing the distribution of XN(t)−r+1, N(t) and the transform of Σr−1(t). From the latter relation one can, for example, derive a further relation that gives information on the ratio between any of the claims and all the smaller ones. The resulting formula might be used to normalize that portion of the portfolio that corresponds to the smaller claims.

10.1.2 Large Claim Reinsurance

We can now use the above formulae to describe some general properties of quantities relevant in large claim reinsurance.

Distributional aspects.

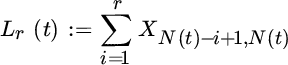

Denote the reinsured amount by

on the set 1{N(t)≥r}. By putting u = θ, s = r, and v = w = 0 in (10.1.6) we deduce

For the case of exponential claim sizes more explicit results can be obtained, as shown by Kremer in [505].

Weak limit.

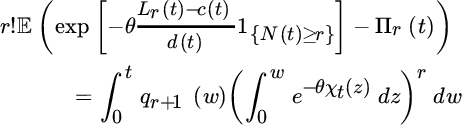

The above formula can be used to obtain the general form for the limit in distribution for the appropriately normalized expression Lr(t) when ![]() . As is the case of the limit behavior for the extreme order statistics we will assume that

. As is the case of the limit behavior for the extreme order statistics we will assume that ![]() for

for ![]() and that the counting process is mixed Poisson. A little reduction yields

and that the counting process is mixed Poisson. A little reduction yields

where

It is now quite obvious what we should do. We choose c(t) = rU(t) and d(t) = a(t); then ![]() . Therefore the right‐hand side tends to the limit

. Therefore the right‐hand side tends to the limit

Let us specialize a bit.

- If γ > 0, then one can replace a(t)/U(t) by its limit γ, yielding the somewhat simpler resultFor r = 1 the right‐hand side can also easily be written as a Laplace transform. The resulting expression for the limit in distribution coincides with that of the maximum from the previous section.

- For γ = 0, the inner integral reduces toUsing the structure variable we find for

The mean.

From the above Laplace transform we can immediately deduce the first few moments. We restrict attention to the mean. An easy deduction yields

We link the above expression with our knowledge about the classes Cγ used in the treatment of one order statistic. First make the change of variable v = w/t. Then replace ![]() . One easily finds that

. One easily finds that

Taking limits for ![]() shows that we need to assume that γ < 1. It then follows that

shows that we need to assume that γ < 1. It then follows that

Further comments.

- As can be expected, the calculation of premiums quickly runs into mathematically intractable formulas. This has been recognized by Benktander [112], who deals with a relation between XL and the largest claim situations. For the calculation of the pure premium, see Berglund [118] and references therein.

- Kupper [520] compares the pure premium for the XL cover at retention M with that of the largest claims cover at retention r. He specifically deals with the case where the claim size distribution is strict Pareto. For example, the effect of truncation on the largest claims depends strongly on the index of this claim, as shown in [519].

- Berliner [119] considers a set of interesting problems connected with the largest claims covers. He assumes the claim number process to be Poisson and derives the joint distribution of two large claims XN(t)−r+1, N(t) and XN(t)−s+1, N(t), and computes their covariance for the case of a strict Pareto law, as well as Cov(Lr(t), S(t)).

- Kremer [501] gives crude upper bounds for the pure premium under a Pareto claim distribution. The asymptotic efficiency of the largest claims reinsurance treaty is discussed in Kremer [502].

- Some practical aspects of large claim distributions have been treated by Schnieper [682]. Albrecher et al. [26] studied the joint distribution of larger and smaller claims for regularly varying claim distributions (see also Ladoucette and Teugels [525] for an overview).

10.1.3 ECOMOR

In some sense the ECOMOR treaty rephrases the largest claims treaty by giving it an additional SL character. However, one can also consider ECOMOR as an XL treaty with a random retention that follows the oscillations showing up, for example, by inflation.

Distributional aspects.

As defined in Chapter 2, the reinsured amount in an ECOMOR treaty is

Again the expression of the reinsured amount equals 0 if N(t) ≤ r. The special choice s = r, w = 0 and v = −ru in (10.1.6) gives us the following expression for the Laplace transform of the reinsured amount:

Weak limit.

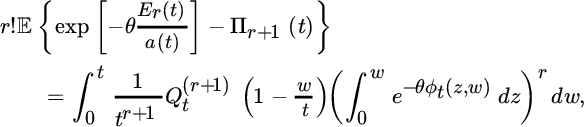

We use a procedure similar to the one for the largest claims reinsurance. So we start from the expression above where we normalize by the auxiliary function a(t) from the max‐domain of attraction. We have

where

Note that the very definition of Er(t) makes further centering unnecessary. We again assume that ![]() and that the counting process is mixed Poisson. It then easily follows that

and that the counting process is mixed Poisson. It then easily follows that

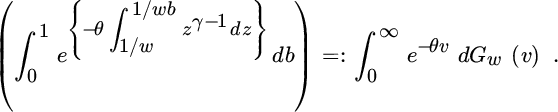

In general the resulting limit distribution seems very hard to recover. However, in the integrand we find for a fixed w a power of a Laplace transform

For 0 < γ ≤ 1 it is not difficult to show that then

which looks very much like a generalized Pareto distribution.

Still two values of γ seem to give something special.

- When γ = 0 then we get a simple expression in that thenwhich can be directly interpreted as the Laplace transform of a gamma distribution.

- When γ = −1 (as for the uniform distribution on [0, 1]) a simple calculation yieldsFor degenerate Λ the limit distribution is a product of independent exponentials.

The mean.

From the above relation we derive the expression for the first moment.

We again indicate what happens when the Cγ‐classes are in force. With the notation introduced for one order statistic, we see that we again need γ < 1. Then, as before,

illustrating the role played by the structure variable Λ.

Further comments.

As for the ECOMOR treaty, a few more explicit results can be found in the actuarial literature.

- Ammeter [39] points out how the exclusion of one or more of the largest claims has the result of reducing the expected amount of the remaining aggregate claim amount. In some cases even an infinite expectation becomes finite after such a reduction. He also points out how in a portfolio with Pareto distributed claim sizes there is a preponderance of small claims. See Albrecher et al. [26] for generalizations.

- For a general study of ECOMOR treaties, see Ladoucette and Teugels [523]. Crude bounds for the pure premium go back to Kremer [501]. For a study of LCR and ECOMOR treaties for more general claim number processes, see also Asimit and Jones [55].

- Here is another possibility for a large claims reinsurance treaty that imitates an ECOMOR treaty but that has a different kind of retention. Accumulating information on the largest claims, one can first get an estimate for the number of claims Kt(a) falling within a fixed distance a from the observed record claim within the time slot [0, t]. The average over this number of claims yields an alternative large claim reinsurance treaty. Information on the quantity Kt(a) can be found in Li et al. [540] and Hashorva [423]. For studies on the asymptotic behavior of the tail probability of Er(t) for exponentially bounded claim sizes, see Jiang and Tang [465] and Hashorva and Li [426]. Peng [610] studied the joint tail of the reinsured amounts in ECOMOR and large claim treaties.

- For a bivariate version of ECOMOR, see Hashorva [424, 425].

10.2 Alternative Risk Transfer

There are several alternatives to traditional reinsurance available in the market, summarized under the term alternative risk transfer (ART). They increase the efficiency of the marketplace and can also be particularly helpful at times when traditional reinsurance capacity is limited (e.g., after major natural catastrophes such as Hurricane Andrew in 1992 or Hurricane Katrina in 2005). Some ART solutions take a more integrated approach to reduce the risk over time (rather than treating the various types of risks separately), providing additional diversification over time in connection with underwriting cycles, counterparty risk, and coverage of large catastrophes. Others provide alternatives in the nature of the relationship between insurer and reinsurer by creating a secondary market where one can enter or leave coverage in a more flexible way than in classical reinsurance treaties. In terms of volume, ART nowadays constitutes about 15% of the total reinsurance business, measured in terms of dedicated capital (Source: JLT Re).

In this section we briefly discuss some of these alternative possibilities, and for more details see the references at the end of the section. In general, the risk transfer can be via alternative risk carriers and alternative products.

Alternative carriers.

Next to self‐insurance (which can be both regulated and non‐regulated and is particularly popular in the USA), reinsurance pools act like a mutual, where each insurance company can cede its risk and its premiums of a specific risk class, for instance for very large risks. Risk‐retention groups are based on a similar concept of pooling for companies to get access to certain types of liability insurance. As another example, captives are popular vehicles to lower insurance premiums as well as transaction costs. Typically located in a tax‐friendly environment, captives are insurance or reinsurance companies which insure the risks of their parent company in a cost‐effective manner. In that way, access to the global reinsurance market can be obtained, which due to the larger diversification possibilities of reinsurers may lower premiums through reduced capital cost. In addition, this allows a certain degree of time diversification (captives are usually allowed to hold equalization reserves, whereas according to the current accounting standards insurance companies are not). For smaller captives, it is also popular to operate as a reinsurance captive, which insures the risk of its parent as a reinsurer of a first‐line insurance company, to which the risk was first transferred. A particular advantage of such a construction is that from a regulatory perspective it will then be treated as a reinsurer, for which different rules apply.

Particularly in times when traditional reinsurance premiums are very high or coverage is not available at all (which happened after Hurricane Katrina), an alternative are so‐called reinsurance side‐cars, where investors deposit funds and in turn participate in the premiums and claims of the insurance company (typically in the form of a QS‐type treaty for a line of business, with a retention for the company that ensures alignment of interests of the two parties). The deposit equals the reinsurance contract limit (so it is a fully collateralized reinsurance form where counterparty risk is eliminated), so the investors’ liability is limited to the amount of the deposit.

Sidecars are only one way for capital market investors to gain exposure to insurance risk. In general, the capital market is a major alternative risk carrier, particularly through insurance‐linked securities (see below).

Finite risk reinsurance.

If in addition to insurance risk transfer there is also a significant weight on other goals in a product, one speaks of structured reinsurance. A particular example is finite risk reinsurance, which is a combination of risk transfer and risk financing between an insurer and a reinsurer in a form that is tailored towards the concrete needs of the insurer. While a substantial goal of the transfer is to enhance the insurer’s financial results, for tax reasons it has to contain a (limited) amount of insurance risk transferred to the reinsurer in order to be classified as reinsurance. Such contracts have a duration of several years and combine loss experience and investment returns. They formalize a longer‐term relationship between the two parties which has a time diversification component, as the reinsurer can count on incoming premiums and the insurer on agreed coverage to known conditions over a longer time horizon.

There are retrospective and prospective variants. An example of the former is a loss portfolio transfer, where the insurer transfers outstanding claims from some long‐tailed business of previous years to the reinsurer, and in turn pays a premium consisting of the net present value of these claims plus fees. In that way he passes on risks related to the timing and amount of loss development. In adverse development covers the IBNR losses are also included. Here the claims reserves are not transferred to the reinsurer, but the reinsurer only covers losses that exceed the reserves which the insurer has already built up, and for this transfer a premium is paid (this can be set up like an XL or SL contract on the adverse loss development and is also very convenient in cases of mergers or take‐overs of a company).

Prospective variants of finite risk reinsurance include spread loss treaties, where for the transfer of specified losses (with annual and overall limits) the insurer pays premiums to the reinsurer onto an “experience account” and these premiums (minus fees and expenses) are then invested. At the end of the contract period, the balance is settled with the insurer, exposing the reinsurer to the counterparty risk that the insurer may not be able to pay a potential negative balance. Finally, finite quota share arrangements can include over‐ or undercompensation of claims over prespecified periods of time.

Integrated products.

In multi‐year/multi‐line products several business lines are bundled together and/or over a longer time horizon, which leads to a smoothing of the aggregate risk and hence to lower premiums. A disadvantage is counterparty risk for the insurer, and it can also be non‐trivial to cooperate across business lines within the insurance company.

Multi‐trigger products.

Here the reinsurer pays losses only contingent on a second event, which typically is correlated to the insurer’s financial result. For instance, the reinsurer will only pay if the losses exceed a certain threshold and at the same time a stock index, commodity price, exchange rate etc. is below a prespecified level. Such an arrangement will lead to considerably lower premiums, but still may serve the overall financial result of the insurer well. At the same time, the reinsurer can also benefit from this variant, as resulting capital needs will decrease, particularly if there are several such contracts with independent triggers in the portfolio.

Contingent capital.

This refers to the option for the insurance company to raise debt or equity capital for prespecified conditions, in case there is a severe aggregate insurance loss experience or another prespecified event occurs. It can be seen as a put option on the own shares with a predefined strike value. By setting up the conditions before financial distress, fresh capital can in such a case be acquired in a much cheaper way than on the market. In fact, this is a means of financing rather than a transfer of insurance risk. As a variant of this idea, in recent years contingent convertible bonds (“CoCo” bonds) have become increasingly popular (particularly since in many countries this is now considered as regulatory‐efficient capital), and recently products have been issued that as a trigger combine the occurrence of natural catastrophes and the solvency ratio of the company.

Industry loss warranties (ILW).

These contracts resemble reinsurance contracts, but the loss under consideration is the loss of the entire insurance industry arising from an event (measured through some index1) rather than the individual loss experience. The market for such contracts has considerably grown over the last years, with reinsurance companies and hedge funds being typical protection providers. A disadvantage for the insurer is that the reinsured amount is not based on their own loss experience, even if the industry index will usually be reasonably correlated. However, the resulting discrepancy (referred to as basis risk) may lead to inefficiencies.

Insurance‐linked securities (ILS).

In broad terms, these are financial instruments whose values are driven by insurance loss events. They enable insurance risk to be (directly) placed on the capital market (insurance securitization). Among the most important examples are catastrophe bonds (CAT bonds), which are bonds with the additional feature that the investor will not receive the coupon (or even not the principal) if a certain trigger related to the occurrence of natural catastrophes is hit. In turn, the coupon in the absence of that trigger is substantially higher. Such bonds are traded over the counter and can increase the insurance capacity for risks for which it is difficult to find traditional reinsurance. The initiator of the CAT bond is the insurance company that seeks this protection. The trigger can be the individual loss experience of the issuer due to a catastrophe or (more often) an index representing the average catastrophe loss experienced by the insurance sector in a prespecified time interval and business line. Finally, it is very common nowadays to have parametric triggers, that is, a physical measurement (such as wind speed, magnitude of an earthquake etc.), as this is a reliable, “objective”, and usually easily accessible trigger for investors (whereas for a trigger linked to the individual loss experience of the issuer there are obvious moral hazard issues and the final settlement can take much longer). One then speaks of an index transaction (instead of an indemnity transaction). However, triggers based on an index or parametric triggers again introduce basis risk for the issuer (on the plus side, the insurer does not have to pass on the actual claim data to the outside in this case).

In practice, there is usually a special‐purpose vehicle (SPV) that acts as an intermediary (located in a tax‐friendly environment), which then issues a conventional reinsurance policy to the insurance company. The SPV uses the premium payments of the insurance company to pay the coupons to the investor, and if the event is triggered (or maturity of the bond is reached without the trigger), the amount in the SPV is paid out to the insurer and the investors according to the bond specifications. One particular advantage of the CAT bond is that – in contrast to traditional reinsurance – there is no counterparty risk for the insurer (unless the construction involves further parties like swap providers), since the reinsured amount is already available in the SPV (or the trust account). At the same time, for investors this can be an attractive product, since the underlying trigger event will typically be independent of other investments and the excess coupon can be considerable (in the long run, it will of course be determined by demand and supply, as well as the concrete loss experience of previous years). Conceptually, CAT bonds represent a secondary reinsurance market, where the investor (who takes the reinsurer’s role here) has more flexibility to leave or enter the “contract” along the way. In recent years the CAT bond market has increased considerably in size. Further ILS products (with, however, a much smaller market) are, for example, longevity swaps and products related to embedded‐value securitization and extreme mortality securitization. Altogether, the global ILS risk capital outstanding in 2016 exceeded 25 billion US$ (Source: Artemis).

10.2.1 Notes and Bibliography

The first implementation of a contract that resembles a CAT bond can be traced back to about 3000 BC (and hence long before the first insurance policy was issued!), when the Babylonians issued maritime loans in which the borrower did not have to repay the loan in case of a loss due to certain accidents (see Holland [451]). CAT bonds and other insurance derivatives in their modern forms started to be traded in the USA after Hurricane Andrew in 1992. In Europe, the concept became popular when the WinCAT coupon (a convertible bond with a trigger related to hail or storm) was issued by Winterthur Insurance in 1997. The model risk related to that product was studied by Schmock [680]. For early descriptions of the developments and discussions, refer to Doherty [296, 300], Gorvett [403], Swiss Re [723], Munich Re [584], and Doherty and Richter [298].

Excellent general surveys on alternative risk transfer are Lane [528], Culp [237], Liebwein [543], and the handbook edited by Barrieu and Albertini [84]. See also Gastel [375, Ch.8], Mürmann [586], and Banks [78]. For a rich source on convertible bonds, refer to De Spiegeleer and Schoutens [260]. Niedrig and Gründl [591] studied the effects of CoCo bonds on the solvency capital situation of insurance companies. Gibson et al. [389] investigated the choice between reinsurance and securitization of natural catastrophes from the viewpoint of information flow.

The ILS market did not grow as fast as anticipated in the beginning. For an attempt to explain this from a behavioral economics perspective, see Bantwal and Kunreuther [80]. Barrieu and Loubergé [86] suggested possible modifications of the product structure. For general reflections about the tradeoff between traditional reinsurance and securitization see Doherty and Schlesinger [302] and Cummins and Trainar [239]. The valuation of ILS products naturally is an interesting academic topic, since actuarial and financial pricing techniques have to be merged in a meaningful way. An early paper in this direction was Embrechts and Meister [333]. Time change techniques in catastrophe option pricing can be found in Geman et al. [378]. Later discussions include Cox et al. [230], Cox and Pedersen [231, 232], Embrechts [324], Dassios and Jang [251], Jaimungal and Wang [461], Lee and Yu [532], and Mürmann [582, 583] as well as Haslip and Kaishev [427] and Gatzert et al. [376]. For adaptations to models based on Cox processes, see Lin et al. [544]. A game‐theoretic approach is given in Subramanian and Wang [714]. An empirical analysis of pricing practice of CAT bonds over a long time horizon can be found in Braun [161]. For computational issues in relation to the pricing of CAT bonds, see, for example, Vaugirard [753], and for QMC simulation refer to Albrecher et al. [21, 22]. Dieckmann [294] discusses a consumption‐based equilibrium model for pricing CAT bonds. Bäuerle [90] studied the stochastic control problem to dynamically mix reinsurance and CAT bonds under basis risk. Securitization is also becoming an important instrument for risks in life insurance. For a recent study on the design and pricing of an inverse survivor bond for annuity securitization, see Lorson and Wagner [547].

An early discussion on finite risk reinsurance can be found in Hess [437], see also Von Dahlen [762]. Time diversification is an important element in these constructions, particularly since equalization reserves are nowadays typically not exempted from tax). Dacorogna et al. [244] studied the quantitative effect of time diversification for catastrophe risk from a shareholder perspective. For consideration of time diversification in terms of self‐insurance on the individual level, see Gollier [397].

10.3 Reinsurance and Finance

As the title suggests, the focus of this book is on actuarial and statistical aspects of reinsurance. We want to emphasize that the concrete implementation of reinsurance in practice also has a considerable financial function for the ceding company. While some financial aspects of the risk transfer have entered the discussion at various places in the book, it is beyond its scope to provide a representative treatment of this element. Instead, we give some references and remarks here.

An excellent book for this topic is Liebwein [543]. Wilson [792] is a rich recent source concerning the formalization of the concepts of value and capital of financial institutions, and also contains sections that are specific to (re)insurance. Klaasen and Van Eeghen [489] give a detailed account of the concept of economic capital. The role of capital and capital management for insurers and reinsurers in view of risk‐based regulation is discussed in Dacorogna [243]. For an introduction to dynamic financial analysis and its connections with reinsurance, see Kaufmann et al. [483], De Waegenaere et al. [266], and Eling and Parnitzke [321].

An early discussion of the influence of reinsurance on the stock value of an insurance company is given by Doherty and Tinic [303]. Zanjani [803] studied the effects of capital costs on catastrophe insurance markets, see also Harrington et al. [421] for a discussion of the extent to which insurance derivatives can reduce the need for equity capital. Froot [361] suggests a framework for capital structure decisions of (re)insurers. For a discussion of the valuation effects of reinsurance purchases in terms of firm leverage see Garven and Lamm‐Tennant [374] and Garven [372]. Blazenko [142] provides an early study of reinsurance from an economic perspective. For an equilibrium model in reinsurance and capital markets in which professional reinsurers arise endogenously, see Plantin [624]. Upreti and Adams [748] investigated reinsurance as a strategic function in insurance markets through its impact on product‐market outcomes, whereas Garven et al. [373] provide empirical evidence how the lengths of the relationship between insurer and reinsurer have positive effects on the insurer’s profitability and credit quality. Altuntas et al. [34] investigated the capital structure of insurance companies and concluded that on the global level it is quite heterogeneous, as it also entails heterogeneous reinsurance demands. Rymaszewski et al. [662] discuss the benefits of pooling risks in the context of insurance guarantee funds, which can be interpreted as obligatory reinsurance (see also Schmeiser et al. [672]).

The impact of foreign exchange risks on reinsurance decisions is studied in Blum et al. [143] and Jacque et al. [460].

Financial pricing of (re)insurance contracts (i.e., applying financial asset pricing theory, empirical asset pricing, and mathematical finance tools to price insurance products) has become quite a prominent topic in the last two decades. Chang et al. [198] determined equilibrium reinsurance premiums within an option framework in terms of the underwritten risks by the ceding company and the first‐line premiums. Incompleteness of the reinsurance market is the starting point of Kroll et al. [509]. A discussion on its effect on insurance pricing is given in Castagnolli et al. [186]. Financial pricing by line of business is discussed in Phillips and Cummins [616], as well as Gründl and Schmeiser [412]. It is quite natural to look for arbitrage‐free pricing also in the context of reinsurance contracts. In loose terms, the Fundamental Theorem of Asset Pricing asserts that in the absence of arbitrage possibilities, the pricing functional ψ must be a positive and linear functional defined in the Hilbert space L2. Then, by virtue of the Riesz representation theorem, one can express ψ as an expectation with respect to a modified (distorted) random variable (for some heuristic explanations in this application context, see Sherris [697]), that is, one looks for a corresponding risk‐neutral probability measure. The reinsurance market is incomplete (illiquid), and so there is no unique choice for such an adjustment of the physical probability measure. There are, however, various justifications for certain choices of a risk‐neutral probability measure, including the minimal martingale measure and the minimal entropy martingale measure, for example see Møller [580] and Jang and Krvavych [462], as well as Kreps [507], Sondermann [706], and Schweizer [685] for earlier work. Venter [754] and Venter et al. [756] provide further explanations from a practical perspective. For a combined model where trading can occur on financial as well as on reinsurance markets, see De Waegenaere et al. [265]. The pricing of CAT bonds also falls into this category, so we also refer to the references in the previous section. A unifying recent overview on the topic is Bauer et al. [89], see also Zweifel and Eisen [812]. For a survey on hybrid (re)insurance/financial instruments and their pricing, see Cummins and Weiss [242].

10.4 Catastrophic Risk

We have dealt with catastrophic risk already in earlier sections (particularly in the context of CAT bonds in Section 10.2), but due to its importance for reinsurance companies, we would like to finish with some more comments and references on the topic. There is first the difficult task of describing the concept itself in a quantitative way. It is not straightforward to agree on a concrete definition of a catastrophic claim; an early attempt can be found in Ajne et al. [10]. Clearly, a catastrophic claim falls into the category of large claims, where from the statistical side one may see an additional challenge in the fact that usually there are very few data points for a systematic study available, and the available ones are often only rough estimates of the true value, even long after the catastrophe has occurred. At the same time, it will often be difficult to make the data points comparable. For some general observations about links between catastrophes and insurability, see Schnieper [681], Zeckhauser [805], Gollier [396], Smith [703], and Punter [637]. Paudel et al. [608] is a comparative study on implemented public and private insurance systems for natural catastrophes.

A general survey on modelling and managing catastrophic risk is Banks [79], but see also Kozlowski et al. [499], Meyers [574], and more recently Woo [794] as well as Krvavych [511]. Pricing of financial products solely from knowing the aggregate amount of catastrophic claims is covered in Christensen and Schmidli [213]. For surveys see Epstein [339], Anderson and Dong [42], Aase [3], and d’Arcy et al. [250]. In O’Brien [593] hedging strategies are introduced to deal with catastrophe insurance options. The appearance of such options on the financial market has given rise to interesting discussions. Securitization of catastrophe risks by capital, CAT options, and reinsurance has been dealt with by Krieter et al. [508], Albrecht et al. [33], Pentikäinen [612], Balford et al. [83], and Meyers et al. [575]. For a general approach, see Jones and Casti [469]. Forecasting using extreme value methods has been illustrated in Coles and Pericchi [222], and see also Lescourret and Robert [539].

Insurability of natural catastrophes can only be achieved in a sustainable way if there is an equilibrium between losses and premium income, over both time and in space. However, the geographical distribution of the claims is often difficult to assess. Insurance companies therefore typically use a bottom‐up approach in which they use scientific/expert knowledge in connection with the time and size of a natural catastrophe (e.g., with high‐resolution physical models for weather parameters), and calibrated in terms of risk exposure (this can involve very detailed information from engineering on building structures, see Heneka and Ruck [436] for an illustration). Missing data are often estimated by expert knowledge, and parameters in the model are sometimes hard to determine in the presence of sparse and inaccurate loss data. Nevertheless, in recent decades scientists have built up an impressive toolkit to quantify respective risks, and nowadays there exist several commercial firms who professionally assess the risk for certain natural catastrophes in specific regions and who offer their services to the (re)insurance industry. When studying the patterns of natural catastrophes and building models, one also needs to carefully consider and incorporate systematic changes in risks due to climate change (see Botzen [155] for a general discussion). When possible covariates for a partial explanation of systematic changes can be identified, extreme value techniques with covariates, as discussed in Chapter 4, can be very helpful in the analysis. Here there is also still a lot of potential for future research.

In view of the above, techniques from credibility theory can be appropriate, but from the point of view of heavy‐tailed distributions. Also, alternative proposals to the credibility paradigm have to be developed. Moreover, many data from the realm of catastrophic risk are censored, so that techniques as discussed in Chapter 4 can be helpful. For some further statistical issues, including the influence of inflation, see Cozzolino et al. [233]. For USA‐based natural disasters and their impact on reinsurance, see Patrat et al. [607]. Maccaferri et al. [554] is a survey of the relevance of the various natural disaster risks for European countries and the development of the respective insurance markets, particularly focusing on flood, storm, earthquake, and drought. A long‐term empirical study of adaptive premium strategies for catastrophe insurance can be found in Born and Viscusi [153]. Niehaus [592] summarized research contributions on the question to what extent the allocation of catastrophe risk is consistent with notions of optimal risk sharing, and how respective efficiency could be increased.

We mention here some examples of models or collections of claim data for specific types of natural catastrophes.

- Catastrophic wind losses and connected XL covers have been considered in Sanders [665]. For Japan, see Mayuzumi [565] and for Europe refer to Matulla et al. [564]. For concrete models of country‐wide storm losses see, for example, Dorland et al. [305], Donat et al. [304], Klawa and Ulbrich [490], and Prettenthaler et al. [633].

- Hurricanes are treated in Burger et al. [173], Watson and Johnson [776], Cole et al. [220], and Pita et al. [620].

- Hail insurance is dealt with by Benktander [113] and Brown et al. [164], and for a recent hail model, see Mohr et al. [579].

- Flood losses have been studied in Merz et al. [572, 573], Jongman et al. [470], and Prettenthaler et al. [631, 632]. For a study of the implications of climate change on flood risks in Europe, see Feyen et al. [348].

- For earthquakes, see Ryder et al. [661], Wakuri et al. [764], Bertogg et al. [130], Crowley et al. [235], Asprone et al. [67], and Chen et al. [202].

- Business interruptions are dealt with in Zajdenweber [802], and see also Rose and Lim [656] and Rose and Huyck [655].

Man‐made and other types of catastrophes are equally challenging to deal with. We list a few examples below.

- For risk assessment of terrorism, see Monahan [581]. For the role of insurance in covering such risks see, for instance, Kunreuther [515], Ericson and Doyle [340], Thomas [743], and Swiss Re [725].

- A recent overview of the field of cyber risk is given in Eling and Wirfs [322]. For an empirical analysis of the insurability of cyber risk see Biener et al. [132]. While the size of some of such claims can be moderate, there is a considerable potential for catastrophic cyber losses, for example see Coburn et al. [219].

- Actuarial risks related to pandemic diseases also have potential to be disastrous, for examples see Swiss Re [724] and Van Broekhoven et al. [750]. For integration of pandemic risk into an internal model, see Planchet [623], and a general actuarial modelling approach to this topic can be found in Feng and Garrido [346].

Some reinsurance companies offer interesting illustrative material to catastrophes, see, for instance, the web‐sites http://www.swissre.com and http://www.munichre.com, where information on recent catastrophes and their actuarial consequences is regularly updated. For recent general reflections on the development of reinsurance and its role in dealing with catastrophes, see Haueter and Jones [429].