Chapter 15

The Stock Record – Using the Double-entry Convention to Control Positions and Security Quantities

Securities firms need to record stock (including listed futures and options in this context) quantities and balances as well as money amounts and balances. The business principles and software application structures (double-entry bookkeeping, unique accounts and the use of account selection parameter tables and the underlying data used by these tables) that have been used to record money amounts may also be used to record stock quantities.

The stock quantity equivalent of a general ledger is often known as the stock record or stockrecord. The stock record shows both the ownership of securities and the location of the stock. It is often a component of the main settlement system, but may also be a standalone application with interfaces to the main settlement system. Some packaged stock record applications employ the terminology of “long” and “short” as alternatives to “debit” and “credit”, respectively, others use the debit/credit terminology. When they use debit and credit terminology different vendors do not use it consistently, as some applications are based in the premise that:

A purchase of stock is a debit of money and a credit of stock.

While the business logic of other applications is based on the premise that:

A purchase of stock is a debit of money and also a debit of stock.

To avoid ambiguity this book will use the long/short terminology.

Look again at the example trade that we used in Chapter 14.

On 3 January 2008, ABC Investment Bank’s trading book number 1 sold 10000 shares in Sony Corporation to Client A at £11.30 per share, for value 7 January 2008. The Bank did not charge the client commission on this trade, so the amount payable by Client A is also £113 000 – 10000 shares * £11.30. As ABC purchased the shares for an average price of £11 each, it has made £3000 profit on this deal. ABC’s settlement agent is Euroclear.

Assuming that the long position that was sold had already settled, the positions in the stock record before this trade was executed would be as shown in Table 15.1.

Table 15.1 Stock record positions on trade date

| Book 1 | Long 10 000 | The book is long because it owns the stock |

| Euroclear depot | Short 10000 | The depot is short because it owes this firm the stock |

Between trade date and settlement date the stock record positions are as shown in Table 15.2.

Table 15.2 Stock record positions on value date

| Client A | Long 10000 | The client is long because we owe it the stock |

| Euroclear depot | Short 10000 | The depot is short because it owes this firm the stock |

On settlement date the stock record goes flat because we deliver the stock to Client A, and Euroclear no longer owes it to this firm.

When the firm is processing coupons, dividends and corporate actions (see sections 23.3 to 23.6) it will use the stock record to ascertain which entities to pass the entitlements to, and which entities to claim the entitlement from.

The full list of account types within a typical stock record application is shown in Table 15.3.

Table 15.3 Stock record account types

| Account type | Purpose of the account type |

| Book | To record the quantity of securities bought and sold in the firm’s trading books or portfolios, and the identities of the books concerned |

| Depot | To record the position in the depot, and the identities of the depots concerned |

| Party purchase and sale | To record the value of securities bought and sold that have not yet settled, and the identities of the trading parties concerned |

| Custody | To record any security quantities that we are holding on behalf of clients, and the identity of the safe-custody clients concerned |

| Party borrow and lend | To record which trading parties this firm has borrowed stock from or lent stock to, and the quantities that have been borrowed or lent |

| Book borrow and lend | To record which trading books are borrowing or lending securities |

It is necessary to produce two views of the stock record, one showing the positions for each account type on a trade dated basis, and the other on a value dated basis.

The trade dated version may be used to identify:

1. Book positions that require to be revalued – refer to section 23.8.

2. The actual position in the depot. This information is needed for dividend, coupon and corporate action proceeds (refer to sections 23.2 to 23.6) and also for depot reconciliation (refer to section 23.10).

While the value dated version may be used to identify:

1. Book positions on which coupon, dividend and corporate action proceeds are due – refer to sections 23.2 to 23.6

2. Safe custody positions on which coupon, dividend and corporate action proceeds are due – refer to sections 23.2 to 23.6

3. Trading parties (including borrowing and lending counterparties) to whom we owe or need to claim coupon, dividend and corporate action proceeds – refer to sections 23.2 to 23.6

4. Book positions on which interest needs to be accrued (refer to section 23.9).

The expected movements between the trade dated stock record and the value date stock record may be used to identify stock borrowing requirements and stock lending opportunities, which are discussed in Chapter 21.

Stock record example

On 3 January 2008, ABC Investment Bank’s trading book number 1 purchased 10000 shares in Sony Corporation to Client A at £11.30 per share, for value 7 January 2008. ABC’s settlement agent is Euroclear. The trade does not settle until 10 January 2008.

Figure 15.1 to 15.3 show ABC Investment Bank’s trade dated and value dated stock record balance reports for Sony shares on 3 January, 7 January and 10 January, respectively.

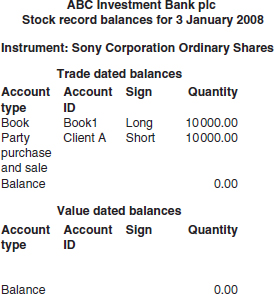

Figure 15.1 The stock record on 3 January

The trade dated and value dated stock record balances for 3 January are as shown in Figure 15.1.

There are no value dated balances as the trade has not yet reached value date. When the trade reaches value on 7 January, the stock record report looks like that shown in Figure 15.2.

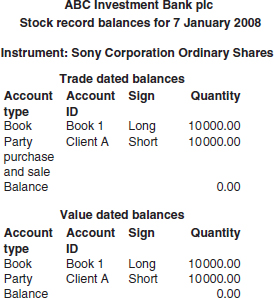

Figure 15.2 The stock record on 7 January

No entries have been passed on 7 January, as no actual events took place (the trade did not settle); but the trade dated positions are now the same as the value dated positions. By the time that the trade settles, on 10 January, the stock record report looks like that shown in Figure 15.3.

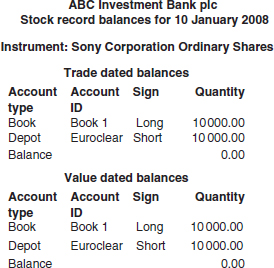

Figure 15.3 The stock record on 10 January

The difference between the stock record of 7 February and that of 10 February is accounted for by the following entry:

Long: Client A 10 000 shares

Short: Depot Euroclear 10000 shares

Note that the stock record balance for an individual security is always zero, as the double-entry bookkeeping convention has been employed throughout the processing.