CHAPTER 13

Cash flow: the oxygen of investing

‘Cash flow is like oxygen: run out and it's all over very quickly.’ I've lost count of how many times John has told me that over the years — possibly a thousand or more!

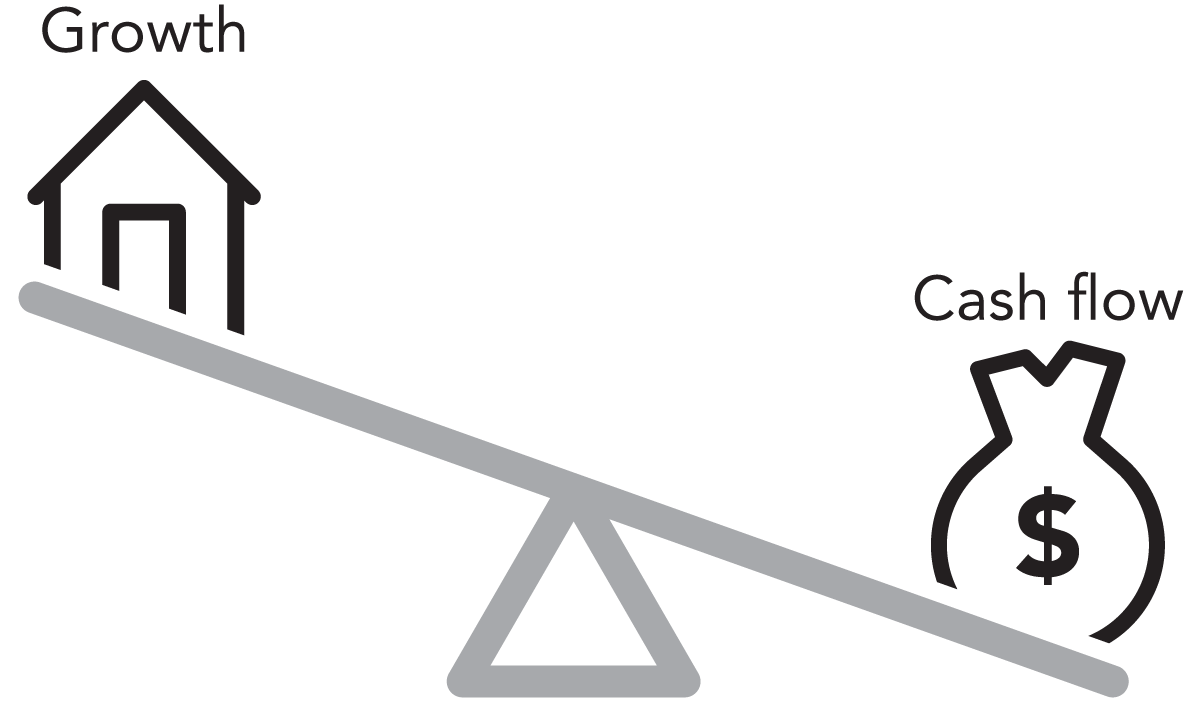

Going right back to basics: how do we define ‘cash flow’? In simple terms, it's the difference between cash coming in (such as rent or dividends) and cash going out (such as management fees, rates, insurances and bank interest). Cash flow and growth are interrelated in any investment, almost like a fulcrum or seesaw.

You can't have growth without sacrificing cash flow and you can't have cash flow without sacrificing growth. This is true whether you're buying property or investing in shares (or any other type of investment). Your return typically comprises a periodic cash flow return (i.e. a dividend in shares, or rent in property) as well as any increase in the asset's value (i.e. the value of the shares or the property).

For shares, your cash flow typically comes from dividends. If the company makes a profit, it generally chooses to pay you part of that profit by way of a dividend. If you have cash in the bank, the bank will pay you a percentage return for the privilege of holding your money. The bank then uses the money as it sees fit, either re-investing it elsewhere or lending it out at a higher rate of return than you're being paid.

Your cash flow from property comes from the rent paid by a tenant less any costs associated with holding the property. Typical holding costs when it comes to property are agent management fees; council rates for water, waste and sewerage; insurances (home and landlord) and maintenance. For more information on holding costs, see the appendix. Rental income was a godsend for a lot of people during COVID-19. Rental incomes held on residential property and, in most capital cities, were around 3–4 per cent of the property value. On the other hand, shares didn't fare so well, with a lot of companies unable to pay a dividend because they weren't making a profit. Cash returns from banks were also at record lows and the combination of these two factors caused widespread stress (and distress) among older, self-funded retirees with the bulk of their wealth held in shares and cash.

Managing cash flow

As far as how cash flow relates to property, any money you borrow (leverage) is going to have a cost. That means it's important to have a strong plan to manage your cash flow.

Say you bought an average block of land for $250 000. If you borrowed 80 per cent of the purchase cost, you would owe $200 000 and your investment would be $60 000 (20 per cent of the land cost, plus 4 per cent for purchase costs). See table 13.1 for a breakdown of these figures.

Table 13.1: your investment amount — land only (80% LVR)

| Land price | $250 000 |

| Purchase costs | + $10 000 |

| Debt | – $200 000 |

| Your investment | = $60 000 |

If you bought a block of land for $250 000 as an investment in a high-growth area, the land would probably be worth as much as $900 000 in 10 years. Using the same scenario as above, assuming you borrowed 80 per cent ($200 000), your initial investment of $60 000 would be worth $700 000 after 10 years (see table 13.2).

Table 13.2: return on investment (ROI) — land only

| Year 1 | Year 10 | |

| Land price | $250 000 | $900 000 |

| Debt | $200 000 | $200 000 |

| Your investment (incl. purchase costs) | $60 000 | $700 000 |

By any standards, that's an amazing return on your $60 000 investment, but the issue would be cash flow. You would have to pay interest on the money you borrowed — conservatively at 4 per cent. Therefore, the $200 000 you borrowed would cost you about $8000 per year ($200 000 × 4 per cent) plus rates (if you own property you have to pay water and council rates) and holding costs — roughly another $2000. Based on these assumptions, the total cost to hold the land would be $10 000 per year (see table 13.3). (Interest rates are closer to 3 per cent as I write, but let's stick to 4 per cent to be conservative.)

Table 13.3: cash flow — land only at 80% LVR

| Costs | Total |

| Interest | $8 000 |

| Holding costs | $2 000 |

| Total cash flow per year | = $10 000 |

Over 10 years, the total outlay would be $100 000 ($10 000 multiplied by 10 years). You'd still make good money — your $60 000 investment would be worth $600 000 ($700 000 less the $100 000 cash flow costs) — but it means you have to find close to $200 per week just to ‘cash flow’ the holding of your investment.

Your return would be 26 per cent per year, but if interest rates increased to 6 per cent or 7 per cent (as they have done historically), the land could finish up costing you as much as $540 per week. That's cause for stress right there! Not to mention hardly bullet proof.

You can see why a lot of people get anxious about anything to do with money and investing. This scenario would be like a massive step backwards from the controlled one we established earlier in this book. Also, in this scenario the interest and holding costs wouldn't be tax deductible because tax deductions only apply if there's a rental property on the land and it's made available to rent out (this is a recent change in policy).

More importantly though, this scenario is not an example of working smart. Working smart is getting a better balance between growth and cash flow. If you were working smart, you would still buy the land for $250 000, but you would also build a house by investing a further, say, $250 000. So the cost doubles to $500 000.

To be consistent with the example above, we'll assume you borrowed 80 per cent of $500 000. You would owe $400 000 and your investment (i.e. your contribution to the purchase) would be $120 000 (20 per cent of the house and land cost plus 4 per cent for purchase costs). In 10 years, the property might be worth $1 million (if you've bought in a high-growth area), so your investment would be worth $600 000 (see table 13.4).

Table 13.4: return on investment (ROI) — house and land only

| Year 1 | Year 10 | |

| Property price | $500 000 | $1 000 000 |

| Debt | $400 000 | $400 000 |

| Your investment | $120 000 | $600 000 |

The return isn't as good as if you'd bought only the land, but it's a good investment all the same (a return of 17 per cent per year against the 26 per cent per year return on land only). The advantage is the cash flow created by your rental income. The total interest would be 4 per cent per year — that's $16 000 per year. But you'd also receive rent — say $400 per week (or $20 800 per year).

The general rule of thumb is that your holding costs (rates, property management fees, insurance, maintenance, etc.) amount to 25 per cent of your rental income. That would give you a net income of $15 600 against the total loan interest of $16 000.

This means the property costs you only $400 per year to hold — that's $8 per week (see table 13.5)!

Table 13.5: cash flow — house and land at 80% LVR

| Rent | $20 800 |

| Holding costs (25% of rental income) | – $5200 |

| Net rental income | = $15 600 |

| Interest | – $16 000 |

| Total cost to you | = – $400 |

While the previous example of land only (see table 13.3) had a total cost of $10 000 per annum, this more balanced approach leaves you only $400 out of pocket per year. That's less than $10 per week — much more efficient and far less anxiety-inducing!

More importantly, if interest rates increased to 6 or 7 per cent, the property would cost you approximately $238 per week. In the scenario in table 13.3, this cost would be $540 (more than double).

What hasn't been factored into the higher interest scenario is a rental increase, which historically occurs during periods of high interest rates and serves to improve the overall picture. Having said that, I don't see interest rates increasing much over the next few years. The Reserve Bank of Australia has said as much, insisting a low interest rate environment will be the norm for the short to medium term. The rationale is that we have low inflation, and inflation and interest rates are interrelated. I've also used a conservative rental amount of $400 per week even though properties costing $500 000 would more likely achieve rent closer to $450 per week (depending on the location).

Remember, I've based all my calculations on interest rates of 4 per cent even though most property investors today would be securing interest rates of less than 3.5 per cent. The message is that you need to have a plan when it comes to cash flow and the plan should be to find a healthy balance between cash flow and growth, regardless of what asset you’re choosing to invest in. An investment property and investment property portfolio should cost no more than 10 per cent of your net after-tax pay to hold each year.

There's one more cash flow strategy John uses that I consider particularly important. In order to achieve cash flow reliability and predictability, he only buys brand new properties. One of the biggest unknowns with older property is the maintenance costs. New homes require very little maintenance and when they do, if you build with the right builders they will provide guarantees for most of the key construction elements, meaning you won't be out of pocket should something go wrong.

In other words, any major repairs will either be covered by your insurance or the builder, whereas not all major repairs can be covered by insurance on older properties. Of course, you only get those kinds of assurances if you build from scratch. In addition, you can claim the depreciation of a new house and this, as we'll see in a moment, is significant.

Negative gearing

In 1985, the Australian government introduced a tax incentive scheme referred to as negative gearing. This scheme is a form of financial leverage that enables investors to offset their expenses against income. If, over the period of the financial year, the expenses on a specific investment exceed the income generated by that investment, the difference (the ATO calls it a ‘loss’) can be subtracted from the owner's personal income, resulting in a tax refund.

It doesn’t just apply to property either. You might have heard of people depreciating — and deducting any interest and running costs associated with — a Ute they use for work purposes. It’s a similar concept (although taking out a loan and upgrading your work Ute that you don’t really ‘need’ would typically fall under the category of a bad debt).

When it comes to property (see table 13.5) if you receive net rent of $15 600 (i.e. after holding costs) and the property costs you $16 000 in interest, your ‘loss’ is $400. At tax time, the Australian Taxation Office (ATO) will subtract the $400 loss on your investment property from your gross income. So, say your income is $80 000, you would only pay tax on $79 600 (i.e. the ATO refunds the tax you shouldn't have paid). In this example, the ATO would refund you $130. This means that, technically, the property has only cost you $270 to hold throughout the year (i.e. $400 less the $130 returned in overpaid tax).

Contributing to the negative gearing equation is the ability for property investors to depreciate the cost of a new house over 40 years, with most of the depreciation able to be claimed in the first 10 years. So, if your house cost you $250 000 as part of your $500 000 investment property, you are able to depreciate 100 per cent of the $250 000 cost for the house, spread out over 40 years.

To do this, you need to obtain a depreciation schedule for your property from a quantity surveyor. This will typically allow you to depreciate $10 000 to $15 000 per year over the first 10 years. What this means is you get to treat that depreciation amount as a tax deduction, so you'll get a portion of it back as a tax refund even though you technically haven't ‘paid’ for it (often referred to as a paper loss).

In this example, you get to add the depreciation cost (which is a loss on paper only) of, say, $15 000 to the actual loss of $400, making your total loss on the investment property $15 400 (instead of $400). See tables 13.6 and 13.7 for the figures without depreciation and with depreciation, respectively.

Table 13.6: cost of holding a property (without depreciation)

| Without depreciation | |

| Rent | $20 800 |

| Holding costs (25% of rental income) | – $5200 |

| Net rental income | = $15 600 |

| Interest | – $16 000 |

| Total cost to you | = – $400 |

Table 13.7: cost of holding a property (with depreciation)

| With depreciation | |

| Rent | $20 800 |

| Holding costs (25% of rental income) | – $5200 |

| Net rental income | = $15 600 |

| Interest | – $16 000 |

| Depreciation | + $15 000 |

| Total cost to you | = – $15 400 |

The ATO will adjust your taxable income from $80 000 to $64 600, resulting in a refund of $5005 at tax time.

Instead of the property costing you $400 per year, you end up being $4605 ahead (i.e. your tax refund of $5005 less your $400 actual cost). Shrewd investors use this money to pay down their home loan (remember, home loans are in the category of a bad debt).

Although this is a theoretical scenario, it's an example of good debt in action. It's earning an income that covers the cost of that debt, resulting in a minimal net outlay. On top of that, if you've done your homework the property will grow in value without you having to fork out money from your own pocket.

We've looked at the power of investing in land (and more broadly an asset that grows in value), using leverage to accelerate your progress and the need to have a good plan around cash flow. I've discussed these three aspects of bulletproof investing in isolation because it's a lot to take in. However, what we ultimately need to do is combine the three and deal with them simultaneously. When we do, we can unlock the greatest opportunity of all. It's the secret sauce of all investment gurus: compound growth.