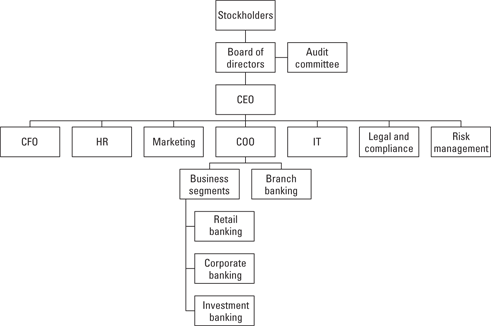

Figure 7-1: The organi-zational structure of a conventional commercial bank.

Chapter 7

Contrasting Conventional and Islamic Commercial Banking

In This Chapter

![]() Understanding the many functions of commercial banks

Understanding the many functions of commercial banks

![]() Eyeing commercial banks’ organizational structure

Eyeing commercial banks’ organizational structure

![]() Spotting the divisions between conventional and Islamic commercial banks

Spotting the divisions between conventional and Islamic commercial banks

Once upon a time, the joke was that if you didn’t trust your money to be safe in a bank, you stuffed it into a mattress or perhaps buried it in the backyard in a Mason jar or two. But can you honestly imagine life today without commercial banks? Even if you don’t have a savings account (which I won’t lecture you about; I’ll leave that one to your parents or spouse), I’m going to take a gamble and assume that you have a checking account with a commercial bank. And a credit card (or two or six) issued by a commercial bank. And a car loan held by a commercial bank. And perhaps a mortgage held by a commercial bank.

In recent years, in the midst of financial crises and bailouts and public furor over the seeming lack of accountability for many banking functions, some people have lost sight of the fact that commercial banks are essential service organizations. Without them, the Western way of life would change dramatically. (Can you imagine paying cash for every purchase you make?)

Conventional commercial banks and Islamic commercial banks have many common features, including an array of services that both provide. But some key differences center on the relationship between the bank and the customer and on how funds can be used. In this chapter, I introduce Islamic commercial banks by first reviewing the functions of commercial banks and looking at their structures. I then home in on how conventional and Islamic commercial banks differ conceptually.

Reviewing the Functions of Commercial Banks

In a nutshell, commercial banks are intermediaries: They channel the savings of individuals, governments, and business organizations into investments or loans. They help you safeguard your money, invest it, and secure the credit to make major purchases. If you own a business, a commercial bank helps you raise necessary capital, offers advice about financial transactions, and/or helps you engage in trading. In other words, commercial banks stand in the middle of financial transactions.

Here’s what this role entails for conventional commercial banks:

![]() They accept money. Conventional commercial banks secure money from individuals, business organizations, and governments. That money may be excess funds (those not needed for immediate use) or money given to the bank specifically for investment. The entities making deposits are rewarded by knowing their money is secure and by earning a set amount of interest.

They accept money. Conventional commercial banks secure money from individuals, business organizations, and governments. That money may be excess funds (those not needed for immediate use) or money given to the bank specifically for investment. The entities making deposits are rewarded by knowing their money is secure and by earning a set amount of interest.

![]() They invest or loan money. Whatever money the bank collects is invested or offered to individuals, business organizations, and governments in the form of loans. Again, interest is the key to these transactions in the conventional system: The bank invests money for the sake of earning interest and loans money based on interest rates that are profitable for the bank.

They invest or loan money. Whatever money the bank collects is invested or offered to individuals, business organizations, and governments in the form of loans. Again, interest is the key to these transactions in the conventional system: The bank invests money for the sake of earning interest and loans money based on interest rates that are profitable for the bank.

Islamic commercial banks also stand in the middle of financial transactions, but the give and take of funds looks slightly different:

![]() They accept money. Islamic commercial banks also receive money deposits from customers looking for security and/or the opportunity to make an investment. The money received for safeguarding is guaranteed. If depositors are looking for investment opportunities, they enter into a profit and loss sharing (PLS) agreement that can result in gains or declines depending on how the bank uses their money.

They accept money. Islamic commercial banks also receive money deposits from customers looking for security and/or the opportunity to make an investment. The money received for safeguarding is guaranteed. If depositors are looking for investment opportunities, they enter into a profit and loss sharing (PLS) agreement that can result in gains or declines depending on how the bank uses their money.

![]() They invest or loan money. Money is given to individuals, businesses, or governments in need based on a PLS agreement or another type of sharia-compliant contract (see Chapter 6) rather than a set amount of loan or investment interest.

They invest or loan money. Money is given to individuals, businesses, or governments in need based on a PLS agreement or another type of sharia-compliant contract (see Chapter 6) rather than a set amount of loan or investment interest.

Later in the chapter, I delve deeper into what these differences mean; for now, focus on the similarities in these descriptions. Conventional and Islamic commercial banks are more similar than they are different. Keep this fact in mind to make your study of Islamic banking less daunting.

Later in the chapter, I delve deeper into what these differences mean; for now, focus on the similarities in these descriptions. Conventional and Islamic commercial banks are more similar than they are different. Keep this fact in mind to make your study of Islamic banking less daunting.

Generally, commercial banking operations — whether in conventional or Islamic banks — are divided into two main categories: primary functions (the main reasons the banks exist) and secondary functions (services that help customers in various activities and that earn extra income for the bank). In this section, I explore how both kinds of operations look in conventional and Islamic banks.

Exploring primary functions

Commercial banks receive money from customers and use that money to earn income. If banks don’t receive any deposits from customers, they can’t survive. These two statements are absolutely true for both conventional and Islamic banks; receiving money from customers and using money to earn income are the primary functions of commercial banks. In the real world, these functions play out in the form of checking, savings, and money market accounts; time deposits; and loans.

Checking, savings, and money market accounts

The three types of accounts I describe here function as receptacles for the deposits individuals and organizations make to commercial banks. The purpose of deposits differs according to the depositors’ needs. For example,

![]() People with a low income may deposit their money for security reasons.

People with a low income may deposit their money for security reasons.

![]() Investors may deposit money to earn extra income with surplus cash.

Investors may deposit money to earn extra income with surplus cash.

![]() Businesses make bank deposits to ease business transactions.

Businesses make bank deposits to ease business transactions.

The following sections give a brief overview of what these three accounts accomplish for the customer and for the bank.

Checking accounts

The checking account is probably the most familiar commercial banking product. Outside the United States, this account may also be called a demand account or a current account. Whatever you call it, this type of account makes depositing and withdrawing money as needed (using ATM cards, deposit slips, and/or checks) easy for a customer. As long as the money is available in the account, the customer faces no limits on the withdrawal of cash. These accounts pay a low rate of interest or no interest. Sometimes a bank charges a fee to maintain this account if customer deposits are lower than a certain limit. Generally, a checking account safeguards money and helps individuals and businesses carry out day-to-day financial activities.

The Islamic version of this type of account is called a qard hasan or wadia account, which has features similar to checking accounts but pays no interest. The account holder’s deposit is guaranteed, and the depositor is allowed to withdraw the money without any limitations. (I discuss this type of account in detail in Chapter 9.)

The Islamic version of this type of account is called a qard hasan or wadia account, which has features similar to checking accounts but pays no interest. The account holder’s deposit is guaranteed, and the depositor is allowed to withdraw the money without any limitations. (I discuss this type of account in detail in Chapter 9.)

Savings accounts

Another common deposit account, the savings account, allows customers to earn interest income. Customers can open savings accounts with relatively small deposits. A commercial bank may place some limits on withdrawals from a savings account — for example, by charging the customer for making more than a certain number of withdrawals each month, but the reward of a savings account is potentially greater than that of a checking account. A bank generally expects depositors to keep their hands off that money though.

Islamic commercial banks also have savings accounts, but the return given by the bank is different from the interest paid by a conventional bank. Islamic banks have investment savings accounts offered on a profit and loss sharing (PLS) basis. No fixed income (interest rate) is guaranteed to the depositor. Instead, an Islamic bank shares the profit it makes from the funds (and the loss, if one occurs) according to the contract between the customer and bank.

Generally, a savings account is set up based on a mudaraba contract, where the depositor is the investor and the bank acts as a fund manager. The investor and fund manager share the return between them. I devote Chapters 9 and 10 to a thorough explanation of this and other investment techniques applied in Islamic banks.

Money market accounts

The money market is a specific type of savings account that is insured by the federal government. Both conventional banks and brokerage firms manage these accounts, which they invest in short-term financial instruments. The interest rates paid on money market accounts are based on interest rates in the current money markets. These rates tend to be higher than those paid on traditional savings accounts, as does the minimum deposit. Islamic commercial banks don’t offer products that specifically compare with money market accounts.

Time deposits

A time deposit is a certificate of deposit or savings account with a fixed term. The customer deposits money for a predetermined period in exchange for a fixed return. Generally, the period of time is 3, 6, or 12 months or from 1 to 5 years. When you open a time deposit, you agree to the period and the interest income you get. You can withdraw money from this account only with a written notice, and often you pay a penalty (such as a loss of interest) if you withdraw principal before the fixed term is complete.

Islamic commercial banks offer investment accounts, products similar to time deposits. When a customer opens an investment account, he agrees to the period of deposit and the profit or loss sharing ratio between him and the bank. The basic difference between conventional and Islamic banking with regards to this type of account is that a customer’s deposit is guaranteed and a fixed amount of money is promised as the return in a conventional system; in Islamic commercial banks, the deposit isn’t guaranteed, and the customer doesn’t know the amount of return until he receives a statement of account. As with savings accounts, time deposits in the Islamic system work based on mudaraba contracts, which I detail in Chapter 10.

Loans

Conventional commercial banks lend money to individuals, organizations, and governments in exchange for payments of interest income. The interest rate for a loan is decided by the type of the loan, its period, and the repayment schedule. Conventional commercial banks lend money based on the credit rating of the customer or in exchange for secured assets.

Islamic commercial banks don’t offer loan transactions in exchange for a fixed return. However, Islamic banks do use the funds they collect from customer deposits to invest in activities based on a profit and loss sharing basis. In Chapter 10, I explain these types of Islamic financial products in detail. Also, some Islamic banks give loans to needy people with no rate of return expected. This type of loan is called a qard hasan loan, and it’s offered by Islamic banks as a way to fulfill their social responsibility.

Delving into secondary functions

Commercial banks perform many important activities beyond accepting deposits and using those funds to earn money. The so-called secondary functions of commercial banks fall into two broad classifications — agency functions and utility functions — that I cover in the following sections. Even if you aren’t familiar with those classifications, these functions comprise regular activities that banks undertake for their customers.

Agency functions

Any commercial bank works as an agent. It’s involved in the following financial transactions on its customers’ behalf:

![]() It collects and pays checks, dividends, interest income, interest charges, rents, and insurance premiums per the standing orders of its customers.

It collects and pays checks, dividends, interest income, interest charges, rents, and insurance premiums per the standing orders of its customers.

![]() It purchases stocks and bonds according to customer requirements and instructions.

It purchases stocks and bonds according to customer requirements and instructions.

![]() It corresponds with other banks and financial institutions on behalf of customers.

It corresponds with other banks and financial institutions on behalf of customers.

Both conventional and Islamic commercial banks provide similar agency functions. However, Islamic banks can’t process interest payments or receipts, which aren’t allowed in the Islamic finance industry because of Islam’s governing sharia law (see Chapter 1).

Utility functions

Commercial banks provide general utility functions to customers and to the general public, often in the interest of society, for a fee or for free. Commercial banks help their communities by providing the following services.

Safe-deposit boxes or safe lockers

Assume that you have gold or diamonds worth millions of dollars. (A nice thought, right?) Keeping those valuables in your home isn’t particularly safe (unless you’ve already spent millions building your own version of Fort Knox), so commercial banks provide safe locker or safe-deposit box services. Both conventional and Islamic banks provide safe deposits; they may do so for a fee or for free depending on your relationship and contract with them.

Traveler’s checks

Imagine that you plan to go on vacation, perhaps taking a six-week tour of architectural hot spots throughout Europe. (Another nice thought.) Can you imagine taking thousands of dollars in cash along with you to make sure you can pay for every lovely meal or must-have souvenir? These days, credit cards have generally eliminated this issue. But in the not-so-distant past, not every wallet contained a credit card. (Ask your grandparents if you don’t believe me!) And wallets that didn’t contain credit cards often relied on the safety of traveler’s checks (often spelled cheques) that could — and still can — be purchased at commercial banks for a fee or commission. Both conventional and Islamic banks provide this service.

Letters of credit

Commercial banks issue letters of credit (LC) for their business customers in order to ease their international business transactions. (You can read about such a scenario in Chapter 8.) A letter of credit is a financial guarantee by the bank to the beneficiary on behalf of the customer. Conventional banks charge a fee and interest to provide letters of credit. An Islamic bank doesn’t consider the letter of credit as a guarantee; instead, it’s a fee-based transaction to facilitate a trade, so the arrangement is technically different from what occurs in conventional banks. The Islamic letter of credit can be based on wakala, musharaka, or murahaba — products I cover in Chapter 9.

Credit cards

For better or worse, credit cards are now an integral part of society. Commercial banks provide credit card services to their customers and to the general public. Conventional credits cards, of course, are based on interest. The bank establishes a time period during which a customer can pay off her debts. If the customer doesn’t make the payments within the given time, the bank charges interest on top of the principal.

Credit cards issued by Islamic banks differ considerably. In essence, they function the way debit cards do in the conventional banking model. When the Islamic credit-card holder makes a transaction, the amount is directly debited from his bank account. So the cardholder can make transactions only for the amount that he has deposited in his bank account. No interest charges are involved. (Note that some more-complicated Islamic credit card models are available in some markets, but I don’t get into those products in this book.)

Trade information and data services

If you’re a business customer, a commercial bank (whether conventional or Islamic) can provide you with trade information and statistical data to help you make your business decisions. (Generally, this information relates to international business transactions.) The bank fee depends on your relationship with the bank.

Studying the Structure of a Commercial Bank

Knowing the structure of commercial banking can help you identify the key people and operations of any bank. Broadly speaking, a bank’s organizational structure is designed according to the bank’s primary functions: The structure is intended to help the bank receive funds through various sources and utilize those funds to make money. But if you search online or peruse the annual reports of banks looking for the organizational structure of commercial banks, you quickly realize that all banks aren’t structured equally. Structures differ according to each bank’s specific requirements.

To give you a starting point for this discussion, Figure 7-1 illustrates a generic organizational structure of a conventional commercial bank. I created it by combining structural features found in a variety of conventional commercial banks.

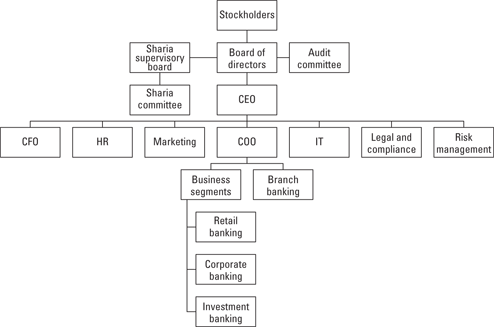

Finding a single organizational structure for Islamic banks is also impossible, so I created Figure 7-2 to offer a generic organizational structure of an Islamic bank. Note that a bank’s sharia supervisory board may report directly to shareholders, and in some cases the sharia board may have subunits such as regional sharia committees; see Chapter 16 for details about the possible structures related to the sharia board.

Figure 7-2: The organi-zational structure of an Islamic commercial bank.

As you can see, Figures 7-1 and 7-2 have a lot in common. Keep these figures in mind as I walk you through the main players and operations that comprise a commercial bank structure.

Stockholders

In both Figure 7-1 and Figure 7-2, you can see that stockholders are the people at the top. If you’re a stockholder in a commercial bank, you’re a powerful person indeed. Stockholders are the investors and the primary resource supporting the bank’s existence.

Board of directors

The board of directors oversees the operations of the bank and is responsible for supervising the bank’s affairs by exercising effective corporate governance (a topic I tackle in Chapter 15). The board of directors governs the bank by setting policies and procedures; it’s selected by the stockholders and should represent the stockholders’ interests. It’s also responsible for many high-level decisions and appoints the bank’s chief executive officer (CEO). This list of duties applies to the boards of both conventional and Islamic commercial banks.

Audit committee

Each commercial bank creates an audit committee that reports directly to the board of directors regarding the bank’s financial reporting, disclosures, and risks. The members of the audit committee are usually selected from within the board of directors.

Commercial banks’ audit committees have become very important since the 2008 financial crisis prompted increased scrutiny of various stakeholders. Audit committees are now taking steps to ensure that they more effectively oversee financial reporting and risk management. These committees scrutinize emerging banking trends and the related risks, and they focus the bank managers’ judgments, assumptions, and scenarios.

Generally, audit committees in commercial banks handle the following tasks:

![]() Ensure that bank operations comply with industry regulations.

Ensure that bank operations comply with industry regulations.

![]() Make sure that the day-to-day operations of the business function according to the company’s internal control policies. (In accountant-speak, internal controls are the systems and processes that a company establishes to ensure that it accomplishes its objectives efficiently, keeps its assets safe, avoids fraud, and generates accurate accounting records.)

Make sure that the day-to-day operations of the business function according to the company’s internal control policies. (In accountant-speak, internal controls are the systems and processes that a company establishes to ensure that it accomplishes its objectives efficiently, keeps its assets safe, avoids fraud, and generates accurate accounting records.)

![]() Conduct internal audits of the bank to make sure that banking operations are performed according to specific internal control procedures and comply with the rules and regulations set by the governing organization. The committee submits internal audits directly to the board of directors.

Conduct internal audits of the bank to make sure that banking operations are performed according to specific internal control procedures and comply with the rules and regulations set by the governing organization. The committee submits internal audits directly to the board of directors.

Keep in mind that internal audits and external audits are completely different processes; however, internal audits can be useful to external (independent) auditors as they conduct their own audits and offer opinions on the company’s financial statements. (Not clear about what external auditors do? You may want to check out Auditing For Dummies by Maire Loughran, also published by Wiley.)

In Islamic banks, the audit committee performs the same functions as it does in conventional banks. In addition, the committee must follow the guidelines of the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) and the Islamic Financial Services Board (IFSB). I describe both of these standard-setters in Chapter 14.

Chief executive officer (CEO)

The CEO of a commercial bank plays a vital leadership role and reports directly to the board of directors. The CEO is expected to mobilize the bank’s funds and utilize them in order to make money. The CEO also has to make sure that the bank meets standards of customer service so it can compete effectively in the industry.

In an Islamic bank, the CEO must also have in-depth experience with the sharia-compliant financial industry. Many Islamic banks prefer to hire CEOs with experience in both conventional and Islamic banks; the CEO needs to interact with stakeholders of both types of banks. (As I explain in depth in Chapter 8, cooperation between Islamic and conventional banks is crucial and occurs regularly.)

Operational-level management

As Figure 7-1 and Figure 7-2 show, the operational-level management occupies a lower tier in the organization chart of a bank. Operational-level management reports directly to the CEO. The people who make up the operational-level management team include the operational managers for banking activities (the chief operating officers) and the departments of finance, marketing, human resources, legal affairs and compliance, information technology, and risk management. You find most of these people and departments in all corporations, but the compliance and risk management departments are unique to banks, as I explain in the following sections.

Compliance department

Each bank has a compliance department to make sure that the bank upholds proper market conduct, that customers are suitably advised, and that the bank serves customers fairly. In other words, compliance departments make sure that banks observe industry regulations and adhere to the following practices:

![]() Follow anti-money-laundering regulations. Compliance departments make sure that banks don’t allow criminals to convert dirty money into clean money.

Follow anti-money-laundering regulations. Compliance departments make sure that banks don’t allow criminals to convert dirty money into clean money.

![]() Comply with data protection acts. In various locales, banks need to comply with applicable data protection acts, which state that certain data need to be deleted when no longer in use.

Comply with data protection acts. In various locales, banks need to comply with applicable data protection acts, which state that certain data need to be deleted when no longer in use.

![]() Treat customers fairly. Compliance regulations state that the products sold to customers must be suitable for them.

Treat customers fairly. Compliance regulations state that the products sold to customers must be suitable for them.

Islamic commercial banks have compliance departments just as conventional banks do, but they also need an entity to oversee sharia compliance, which is the sharia supervisory board.

Risk management department

Banks have inherent risks in their day-to-day transactions. The major risks that banks are exposed to include the following:

![]() Liquidity risk: Negative effects caused by a bank’s inability to meet its obligations

Liquidity risk: Negative effects caused by a bank’s inability to meet its obligations

![]() Credit risk: Negative results in financial standing because a debtor defaults

Credit risk: Negative results in financial standing because a debtor defaults

![]() Market risk: Negative impact of foreign exchange and interest rates, among other factors

Market risk: Negative impact of foreign exchange and interest rates, among other factors

![]() Operational risk: Negative bank performance because of employee or management negligence

Operational risk: Negative bank performance because of employee or management negligence

To manage these and other risks, each bank has a core department called (appropriately enough) the risk management department. I devote Chapter 17 to a thorough description of risk management.

Like conventional banks, Islamic banks are exposed to a variety of risks, such as liquidity, operational, and market risk. But certain other risks differ between Islamic and conventional banks. For example, credit risk doesn’t look the same in an Islamic commercial bank because that bank doesn’t offer loans. (The Islamic bank faces credit risk if a customer defaults on an equity-based or asset-based financial instrument.) Also, an Islamic bank faces the risk of losing customers if it fails to comply with sharia. In Chapter 17, I discuss how Islamic banks manage their risks.

Business segments

The preceding sections deal with the top-level and management personnel who make a bank tick. In this section, I shift attention slightly to focus on the functions that occur within a bank’s various business segments.

Retail (consumer) banking

This business segment, also referred to as personal banking, exists in banks that are directly involved with the general public. Most primary and secondary services offered by commercial banks (which I discuss earlier in the chapter) are offered by retail banks. Conventional retail banks provide checking accounts, time deposits, demand deposits, housing mortgages, auto loans, credit cards, and safe-deposit boxes. They provide services to their customers through branch banking, ATMs, and/or online banking.

Islamic banks were started in order to serve the public — to cater to customers’ day-to-day requirements. (I discuss the origins of Islamic banking in Chapter 3.) Only later did Islamic banks develop other segments, such as corporate and investment banking. Islamic banks serve their customers through the same channels (ATMs and so forth) as their conventional cousins do. Islamic retail banks offer their customers current (checking) accounts, savings accounts, demand deposits, Islamic credit cards, sharia-based mortgage and auto loan products, and more.

Corporate banking

Corporate banking is another large segment of commercial banks. The corporate banking units provide services to corporations, large portfolio customers, governments, and other large-scale institutions. Corporate banking services range from simple loans to complex foreign exchange derivatives. The corporate banking segment provides customers with the most suitable customized financial solutions. The most common corporate banking products and services are the following:

![]() Working capital management to meet customers’ day-to-day operation needs so they can do business domestically and internationally

Working capital management to meet customers’ day-to-day operation needs so they can do business domestically and internationally

![]() Commercial mortgages, customized loans, and lease products

Commercial mortgages, customized loans, and lease products

![]() Tools for managing interest rate risk, commodity risk, or foreign exchange rate risk

Tools for managing interest rate risk, commodity risk, or foreign exchange rate risk

Many Islamic banks have already engaged with corporate banking to serve their major corporate customers, and many Islamic corporate financial products exist. For example, the murabaha (cost plus) contract is used to finance working capital and assets and to secure letters of credit, which I discuss in the earlier section “Letters of credit.” Islamic banks also provide leasing options through ijara contracts. (I discuss murabaha and ijara in Chapter 10.) Sukuk are used to issue corporate bonds (see Chapter 13), and takaful (insurance) contracts are used to finance risk management of a corporation (see Part VI). So every product in Islamic corporate banking is based on existing types of Islamic contracts.

Hong Leong, a Malaysian-based Islamic bank, for example, provides the following corporate banking services:

Hong Leong, a Malaysian-based Islamic bank, for example, provides the following corporate banking services:

![]() Flexible-term financing based on the contract called bai bithaman ajil (deferred payment sale)

Flexible-term financing based on the contract called bai bithaman ajil (deferred payment sale)

![]() Commodity-revolving credit services based on the murabaha contract

Commodity-revolving credit services based on the murabaha contract

![]() Accepted bills to finance imports and local purchases, also through a murabaha contract

Accepted bills to finance imports and local purchases, also through a murabaha contract

Investment banking

The investment banking segments of commercial banks don’t take deposits from customers; instead, they provide services to clients. They offer advice and help to individuals, corporations, and government organization on a range of activities. For example, this banking segment provides financial advocatory services (such as advice on corporate mergers and acquisitions), underwriting, and sales and trading of securities (stocks and bonds). Investment banking segments also become involved in the trading of financial instruments such as derivatives, fixed income instruments, commodities, and foreign exchanges. Leading investment banks in the United States include Goldman Sachs, Morgan Stanley, Citigroup, and Credit Suisse.

Islamic commercial banks also have investment banking segments that provide the same basic services as conventional investment banks, but with this difference: Islamic investment services must comply with sharia and are therefore subject to oversight from the bank’s sharia supervisory board (see Chapter 16).

Differentiating between Conventional and Islamic Commercial Banks

Throughout this chapter, I discuss both conventional and Islamic commercial banking functions, structures, personnel, and operations. Although Islamic commercial banks have many products similar to those offered by conventional banks, the two entities differ conceptually. One key difference is that conventional banks earn their money by charging interest and fees for services, whereas Islamic banks earn their money by profit and loss sharing, trading, leasing, charging fees for services rendered, and using other sharia contracts of exchange.

In this section, I touch on four key ways that conventional and Islamic commercial banks differ. Each topic merits in-depth attention, which I offer in other chapters.

The oversight of a sharia board

In Chapter 16, I explain that a sharia board consists of Islamic scholars who are qualified to give opinions on Islamic business contracts. In a commercial bank, the board is also involved in supervising bank operations to make sure they comply with sharia principles.

You may wonder why a bank needs a sharia board to ensure its compliance with sharia principles. If the basic distinction between conventional and Islamic banking hinges on interest, can’t Islamic banks satisfy the requirement by just making sure none of their transactions involves charging interest?

As I explain in Chapter 1, Islamic banks and other financial institutions must comply with a variety of principles besides avoiding interest. I note in that chapter that Islamic finance is based on four core principles:

![]() Prohibiting usury

Prohibiting usury

![]() Avoiding speculation

Avoiding speculation

![]() Avoiding gambling

Avoiding gambling

![]() Investing ethically

Investing ethically

Interpreting each principle is more difficult than you may think. (Just spend a minute chewing on what it means for a financial institution to avoid speculation, and you may get a sense of what I mean.) Scholars spend their lifetimes learning all they can about the intent and past interpretation of sharia law, and they still often have differing opinions about it.

Making sure that Islamic banks comply with sharia isn’t easy — hence the necessity of the sharia supervisory board. This board is the backbone of an Islamic bank; it plays a vital role in establishing and operating the bank.

Concepts of money and the basis of transactions

To say that Islamic banks are different from conventional banks because the former don’t charge interest is accurate, but it’s only the tip of the iceberg. That difference is just one of many ways that the fundamentals of Islamic banking differ from those of conventional commercial banking.

The basic purpose for establishing an Islamic bank is to promote and encourage Islamic principles, specifically those I list in the preceding section. Conventional banks are profit-making organizations that generally aren’t based on religious principles. That said, earning money is also a primary function of an Islamic commercial bank, as I discuss earlier in the chapter. Although the bank has a specific religious purpose, it can’t serve that purpose unless it also meets the objective of earning money. A bank serves no purpose at all if it can’t stay in business!

Islamic banks operate based on Islamic business law (called fiqh-u-muamalat) for their basic transactions, and they also follow the financial laws and regulations of the countries in which they operate. Conventional banks likewise operate based on a country’s financial laws and regulations, but they don’t have contact with any religious body.

“Now, wait,” you’re saying. “If an Islamic bank doesn’t charge interest, does that mean money doesn’t have any value in Islam?” Not exactly. Islamic scholars recognize that money has value, but with limitations. For example, money can’t become more valuable simply because time is passing. (That’s why asking for compensation for lending someone money is prohibited.) However, the value of money can increase if it’s invested in a project that itself is increasing (in size, in success, and so on). In other words, Islamic principles ensure that time by itself doesn’t create any return; the time by itself doesn’t increase value. But if any economic activity takes place, the time spent on that economic activity can create value.

Relationships with clients or customers

When you deposit your paycheck in a conventional bank, your relationship with that bank is one of creditor to debtor; the bank has a responsibility to pay back your money with or without interest according to your account contract. Similarly, the roles reverse when the bank provides you with a loan.

The relationship between a customer and an Islamic bank is completely different; the debtor and creditor relationship does exist at times in Islamic banking. To understand the relationship between the customer and Islamic bank, you must know what contract that relationship is based on. In Chapters 9 and 10, I explain various contracts that provide the basis for common Islamic banking products. For now, here are two examples:

![]() Qard hasan loans: A qard hasan contract is a loan given by the bank to the needy on the basis of social responsibility without any interest attached. The borrower is expected to pay back the principal without any extra charges. (However, the Islamic bank can receive a monetary gift from the borrower.)

Qard hasan loans: A qard hasan contract is a loan given by the bank to the needy on the basis of social responsibility without any interest attached. The borrower is expected to pay back the principal without any extra charges. (However, the Islamic bank can receive a monetary gift from the borrower.)

![]() Wadia contract: In a wadia contract, the customer deposits money in the Islamic bank only for safeguarding, not with the intention of earning profits. In this case, the relationship between parties is established as trustee (the bank) and beneficiary (the customer).

Wadia contract: In a wadia contract, the customer deposits money in the Islamic bank only for safeguarding, not with the intention of earning profits. In this case, the relationship between parties is established as trustee (the bank) and beneficiary (the customer).

Investments in the bank

Investments in conventional commercial banks are based on guaranteed principal and earning a fixed amount of income. For example, say that a customer in a conventional bank deposits $10,000 in a six-month term deposit. After six months, the bank has a liability to pay back the customer the principal plus the interest rate charged for six months. Even if the bank lost the money in an investment, the bank is still liable to pay back all the money due.

In Islamic banking, the concept of investment is different. Although the customer deposits the money in order to earn extra income for her savings, her principal and returns aren’t guaranteed. Suppose the Islamic bank loses money because of an unexpected business failure. In this case, the bank isn’t liable to pay the money to its customer. (Note: The failure of an investment isn’t very common in Islamic banks because the banks are very concerned about their customers and make their investment choices very wisely. If they didn’t, they soon would have no customers at all!)

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.