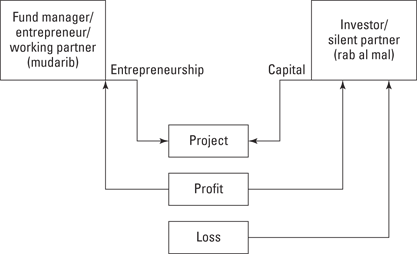

Figure 10-1: The mudaraba contract in action as a financial instrument.

Chapter 10

Familiarizing Yourself with Islamic Financial Instruments

In This Chapter

![]() Eyeing equity participation products

Eyeing equity participation products

![]() Focusing on asset-based financing instruments

Focusing on asset-based financing instruments

![]() Seeing what trade-based financing products are offered

Seeing what trade-based financing products are offered

![]() Taking financial instruments out into the real world

Taking financial instruments out into the real world

Offers and advertisements for conventional banking products are on bank windows and billboards, in your mailbox and newspaper, and virtually everywhere online. Personal loans, credit cards, flexible loans for new graduates, mortgage loans, business loans with variable or fixed terms — by the look of it all, you’d have no clue that the Western banking industry seemed to be flirting with collapse just a few short years ago.

If you ever travel to the Persian Gulf region (Bahrain, Kuwait, Saudi Arabia, Jordan, Oman, Qatar, United Arab Emirates, or Morocco) or to Malaysia, you’ll see similar ads from Islamic banks touting products for sharia-compliant automobile purchases, mortgages, and more.

What’s the story? Why are banks so eager to give people their money? Commercial banks — both conventional and Islamic — must mobilize the funds they receive in order to earn profit and stay in business. As I discuss briefly in Chapter 9, Islamic banks (which don’t offer loans the way conventional banks do) have one way to earn profit: by offering income-generating financial instruments.

Such financial instruments can be discussed in a variety of ways: by focusing on their size, yield, duration, risks, liquidity, or marketability, for example. In this chapter, I discuss financial instruments based on their mode of financing, so you find out about equity financing products, asset-based products, and trade-based products. In each case, I note the type of contract that supports the product so you discover how Islamic banks offer each instrument in a way that complies with sharia principles (which I explain in Chapter 1).

Tailoring product names to the target audience

Sometimes Islamic banks advertise their products by using terminology that’s most familiar to non-Muslim customers (in other words, leaving out the Arabic). For example

![]() Global Islamic finance services group HSBC Amanah offers financial products with names such as working capital, term finance, asset financing, and leasing.

Global Islamic finance services group HSBC Amanah offers financial products with names such as working capital, term finance, asset financing, and leasing.

![]() California-based American Finance House (LARIBA) offers products such as home financing, auto financing, business financing, trade financing, and equipment financing.

California-based American Finance House (LARIBA) offers products such as home financing, auto financing, business financing, trade financing, and equipment financing.

When you see such product names advertised, you may wonder where the Islamic financial instruments come into play; the terms I use in this chapter may appear nowhere in the ads.

Keep in mind that banks are businesses, and they don’t want to lose customers by confusing them. If banks are actively seeking non-Muslim customers, they may avoid Arabic terminology. However, every Islamic finance institution offers products based on Islamic contracts, such as mudaraba, murabaha, musharaka, ijara, and salam (all of which I define in this chapter).

Conversely, some banks — especially those in the Middle East and Asia — make a point to add the Arabic terms to their promotional materials in order to distinguish their products from conventional bank offerings. For example

![]() Qatar Islamic banks generally offer products such as murabaha sales, mudaraba investment, and musharaka investment.

Qatar Islamic banks generally offer products such as murabaha sales, mudaraba investment, and musharaka investment.

![]() Dubai Islamic Bank Limited of Pakistan offers products such as murabaha for purchase order, financial ijara, diminishing musharaka, murabaha import, and istisna’a cum wakala.

Dubai Islamic Bank Limited of Pakistan offers products such as murabaha for purchase order, financial ijara, diminishing musharaka, murabaha import, and istisna’a cum wakala.

Discovering What Islamic Financial Products Are Available

All the financial instruments I explain in this chapter are based on sharia-compliant contracts and techniques, and they all serve customer needs in the real world. Islamic banks use these products to serve the markets and the communities in which they operate. Yes, these financial instruments serve a crucial in-house purpose for the bank: They’re the sole income-generating products an Islamic bank can offer. However, they also support all sorts of economic activity. Here’s just a taste of how these instruments intersect with customer needs:

![]() Consumer financing, including short-term personal and corporate financing, is possible using tawarruq, murabaha, and qard hasan contracts.

Consumer financing, including short-term personal and corporate financing, is possible using tawarruq, murabaha, and qard hasan contracts.

![]() Real estate financing occurs via musharaka, diminishing musharaka, murabaha, bay al-muajil, ijara, and istisna contracts.

Real estate financing occurs via musharaka, diminishing musharaka, murabaha, bay al-muajil, ijara, and istisna contracts.

![]() Auto financing depends on financial instruments supported by murabaha, ijara, musharaka, and bay al-muajil contracts.

Auto financing depends on financial instruments supported by murabaha, ijara, musharaka, and bay al-muajil contracts.

![]() Credit cards are available thanks to tawarruq, and their service charges are possible because of ujra and ijara contracts. (I don’t discuss ujra in detail in this book; they’re service charges that a bank receives from customers in exchange for a service rendered.)

Credit cards are available thanks to tawarruq, and their service charges are possible because of ujra and ijara contracts. (I don’t discuss ujra in detail in this book; they’re service charges that a bank receives from customers in exchange for a service rendered.)

![]() Financing for international trade is available courtesy of mudaraba, wakala, and murabaha contracts.

Financing for international trade is available courtesy of mudaraba, wakala, and murabaha contracts.

I explain each of these instruments in this chapter, so feel free to jump to the sections that correspond to what you’re interested in exploring.

Examining Equity Financing Products

Islamic banks have developed products based on equity participation. In other words, an Islamic bank doesn’t lend money the way a conventional bank does, but it can participate in a client’s project or business as an investor and share the profit and loss. Two equity participation products are available in the market: partnership based on profit and loss (mudaraba) and joint venture (musharaka).

Sharing the profit and loss with venture capital (mudaraba)

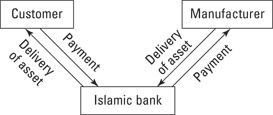

This product is one of the most widely used financial instruments in the Islamic banking sector. A mudaraba contract is based on a partnership in which one partner is the financier (the investor, or silent partner) and the other partner (the fund manager, or working partner) manages the financier’s investment in an economic activity. The second partner (often an entrepreneur) has expertise in applying the venture capital into the economic activities. Both parties agree in advance to a profit and loss sharing (PLS) ratio. In Arabic, the investor is called rab al mal, and the fund manager is called the mudarib. (I remind you of these terms often in this chapter so they can become familiar.)

The mudaraba contract dates back to the early days of Islam. The Prophet Muhammad (pbuh) acted as fund manager (mudarib) for his wife, who was the investor (rab al mal) for several trades. His wife provided the capital and shared the profit with the Prophet (pbuh). (Note: The letters pbuh, which stand for peace be upon him, customarily follow references to the Prophet Muhammad (pbuh) or to any other prophet.)

The mudaraba contract dates back to the early days of Islam. The Prophet Muhammad (pbuh) acted as fund manager (mudarib) for his wife, who was the investor (rab al mal) for several trades. His wife provided the capital and shared the profit with the Prophet (pbuh). (Note: The letters pbuh, which stand for peace be upon him, customarily follow references to the Prophet Muhammad (pbuh) or to any other prophet.)

In this contract, the basic factors of production (from the Islamic economics viewpoint) — capital, labor, and entrepreneurship — are combined to make an economic activity. The rab al mal provides the capital, and the mudarib provides entrepreneurship and labor. The mudarib gets a portion of the profit for his effort, and the rab al mal gets the remaining profits. All mudaraba contracts are limited by a specific time period; they don’t continue indefinitely.

Using mudaraba as a source of funds

Mudaraba contracts can also serve as a source of funds for an Islamic bank. In this chapter, my focus is on explaining mudaraba as it allows for a bank to use funds (with the bank as an investor or rab al mal). In Chapter 9, I explain that deposits in Islamic banks may also be based on mudaraba contracts if the customer is an investor expecting a return based on profit and loss sharing.

When customers deposit money and expect a return, they’re the arbab al mal (the investors), which is the plural form of rab al mal. The bank is the fund manager or working partner — the mudarib. The bank invests the depositors’ money according to sharia guidelines.

When customers deposit money and expect a return, they’re the arbab al mal (the investors), which is the plural form of rab al mal. The bank is the fund manager or working partner — the mudarib. The bank invests the depositors’ money according to sharia guidelines.

Investing in restricted or unrestricted contracts

A rab al mal can choose to invest in two types of mudaraba contracts:

![]() Restricted mudaraba (mudaraba al muqayyadah): The investor specifies a particular business or project where the investment funds are to be used; the working partner should not use the funds for any other business or project.

Restricted mudaraba (mudaraba al muqayyadah): The investor specifies a particular business or project where the investment funds are to be used; the working partner should not use the funds for any other business or project.

![]() Unrestricted mudaraba (mudaraba al mutlaqh): In this mudaraba contract, the investor gives the working partner permission to funnel the funds into any type of business or project that best suits the financial goals of both partners.

Unrestricted mudaraba (mudaraba al mutlaqh): In this mudaraba contract, the investor gives the working partner permission to funnel the funds into any type of business or project that best suits the financial goals of both partners.

When a mudaraba contract is used as a source of bank funds (when the customer deposits money in the bank), the unrestricted mudaraba is most often used. When the contract supports a bank’s equity financial product (when the bank supplies funds to a working partner), the restricted mudaraba is most often in play.

Dividing the spoils

With mudaraba contracts, the rab al mal and the mudarib share profits and losses based on an agreed-upon ratio. The mudarib (manager or working partner) also receives a fixed fee for managing the project, in addition to a share of any profits.

If the economic venture results in a loss, that loss is absorbed solely by the investor as the capital provider unless the mudarib (fund manager) has acted negligently or has engaged in misconduct. (In other words, if the mudarib doesn’t act in good faith, he’s on the hook for the financial losses incurred.) You may wonder why losses aren’t shared by the mudarib in all cases. They are, in the sense that the mudarib loses the time and energy he devotes to the venture; the rab al mal loses the cash.

For example, say a client of an Islamic bank approaches the bank for a project or venture based on a PLS agreement. The bank (the rab al mal) provides $100,000 upfront with the agreement that it will get 30 percent of the profit of the project or venture for three years. The client (mudarib) gets the remaining profit returns. If any losses occur, the rab al mal stands to lose both its principal investment (or some portion of it) and its anticipated return.

Figure 10-1 provides a visual of how the mudaraba contract works as a financial instrument.

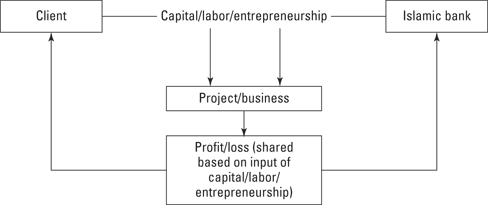

Distinguishing first-tier and two-tier mudaraba

As I note earlier in “Using mudaraba as a source of funds,” the mudaraba contract is applied when someone deposits money in an Islamic bank with the expectation of getting a return. In most cases, the contract applied is a first-tier (or simple) mudaraba contract, meaning that only the customer and the bank are involved. (The bank serves as fund manager for whatever money is deposited.)

However, another type of contract exists: a two-tier (or intermediary) mudaraba contract. In this case, the bank acts as an intermediary between the depositor and the bank’s clients to whom it provides money. In other words, the Islamic bank acts as an intermediary (rab al mal and mudarib) between the investor (rab al mal) and the entrepreneur (mudarib). Islamic scholars promote using this kind of mudaraba model in two scenarios:

![]() The bank on its own doesn’t have the capacity to serve as the investor (the rab al mal). This scenario may mean that the bank doesn’t have enough liquidity to enter a mudaraba contract with an entrepreneur or fund manager.

The bank on its own doesn’t have the capacity to serve as the investor (the rab al mal). This scenario may mean that the bank doesn’t have enough liquidity to enter a mudaraba contract with an entrepreneur or fund manager.

![]() The bank lacks the expertise to serve as the fund manager (mudarib) for an investment.

The bank lacks the expertise to serve as the fund manager (mudarib) for an investment.

In both cases, the two-tier contract allows the bank to create a link between investors and an expert fund manager or entrepreneur so the economic activity can take place.

Figure 10-2 illustrates how the two-tier model works.

Figure 10-2: The two-tier mudaraba contract.

The two-tier method of mudaraba is less-frequently applied than the first-tier method. That’s because banks usually have the liquidity and/or expertise to enter into a first-tier contract and because the two-tier method isn’t quite as profitable for the bank as the first-tier method.

Consider an example of a two-tier mudaraba contract in action. Two contracts must be executed:

![]() One between the depositor as investor (rab al mal) and the bank as a fund manager (mudarib): Say, for example, that the depositor signs a contract with the bank for a two-year sharia-compliant project. The investor and the bank agree to share the profit in a 60:40 ratio (60 percent of profit goes to the investor and 40 percent to the bank). The investment made by the depositor for this specific project is $1 million.

One between the depositor as investor (rab al mal) and the bank as a fund manager (mudarib): Say, for example, that the depositor signs a contract with the bank for a two-year sharia-compliant project. The investor and the bank agree to share the profit in a 60:40 ratio (60 percent of profit goes to the investor and 40 percent to the bank). The investment made by the depositor for this specific project is $1 million.

![]() One between the Islamic bank serving in the capacity of investor (rab al mal) and the project client as the working partner (mudarib): Say that this contract indicates that the two parties will share the profit on a basis of 70:30 (with the Islamic bank getting 70 percent and the client getting 30 percent). Assume that the client isn’t making any capital contribution but is instead investing time, effort, and expertise in the project.

One between the Islamic bank serving in the capacity of investor (rab al mal) and the project client as the working partner (mudarib): Say that this contract indicates that the two parties will share the profit on a basis of 70:30 (with the Islamic bank getting 70 percent and the client getting 30 percent). Assume that the client isn’t making any capital contribution but is instead investing time, effort, and expertise in the project.

In the end, everything goes well, and the project earns $1.5 million by the final contract date. The fund manager or entrepreneur gets 30 percent of the profit, or $150,000, based on the second contract. (The profit is $500,000, and 30 percent of that amount is $150,000.) The bank recovers the capital of $1 million plus a $350,000 profit. The $1 million principal is returned to the initial investor, along with 60 percent of the bank’s profit from the second contract. ($350,000 × 60 percent equals $210,000.) The bank holds onto the remaining 40 percent of $350,000, or $140,000. So the bank earns $140,000 for serving as intermediary between the depositor and the entrepreneur. (Of course, that’s considerably less than the $350,000 it would have made with a regular mudaraba contract.)

Supporting joint ventures (musharaka)

The second kind of equity participation financial instrument used by Islamic banks is based on a musharaka contract. It establishes a partnership or joint venture for an economic activity between the bank and one or more clients. In this joint venture, all parties may contribute some (not necessarily equal) percentage of all three factors of economic production (capital, labor, and entrepreneurship).

Having two or more working partners

In a mudaraba contract, one party is a financier (silent partner), and the other party (working partner) provides labor and entrepreneurship. But in a musharaka contract, all participants are working partners.

For example, say that the hypothetical company Jamaldeen, Inc., wants to establish a joint venture project with World’s Best Islamic Bank. Jamaldeen, Inc., brings $200,000 in capital to the table, and the bank contributes $300,000. Jamaldeen, Inc., has most of the expertise needed to get the project off the ground, but the bank also wants to be involved with managing some aspects of the project.

The agreement states that the two parties share the profit this way: Jamaldeen, Inc., gets 80 percent, and the bank gets 20 percent. (Why the disparity? Jamaldeen, Inc., is contributing more labor and expertise for the project, as well as a decent percentage of the capital.) Similarly, both parties bear any losses according to their capital contributions (40 percent for the company and 60 percent for the bank).

This means that if the project is successful and the end product sells for $800,000, the company gets 80 percent of the $300,000 profit ($240,000), and the bank gets the remaining $60,000. If the project falls flat and sells for only $400,000, the $100,000 loss is divided this way: The company accepts $40,000 in loss, and the bank eats $60,000.

Figure 10-3 shows how the musharaka contract plays out.

Islamic banks use the musharaka contract to finance trade, provide working capital, and support other large projects. For example, based on the musharaka contract, Bahrain Islamic Bank (BisB) provides letters of credit (LCs; financial guarantees that I discuss in Chapter 8) to its customers that deal in international trade. On its website (

Islamic banks use the musharaka contract to finance trade, provide working capital, and support other large projects. For example, based on the musharaka contract, Bahrain Islamic Bank (BisB) provides letters of credit (LCs; financial guarantees that I discuss in Chapter 8) to its customers that deal in international trade. On its website (www.bisb.com/Corporate/islamic policies.asp), the bank describes the contract as being a limited partnership that supports customers who lack sufficient funds to import what they need. A customer supplies part of the money, the bank supplies the rest, and the bank issues the letters of credit. Then, after the imported items arrive, one of three scenarios applies:

a) BisB sells its share in the musharaka to the customer on cash payment or deferred basis at an agreed margin

b) The customer sells its share to BisB on cash payment or deferred basis

c) Both sell their shares in the market together

Figure 10-3: The musharaka contract.

Choosing between a consecutive and declining balance partnership

Islamic banks divide musharaka products into two categories based on the retention of the partners in the joint venture (how long the partners will stay in the joint venture):

![]() Consecutive partnership (consecutive musharaka): Each partner can keep its share in the partnership until the very end of the joint venture, project, or business. However, the partners are often allowed to withdraw or transfer their shares (unless the initial contract specifically states that all partners shall remain in the partnership until the date of maturity). If one of the partners withdraws from the contract, the whole partnership doesn’t terminate.

Consecutive partnership (consecutive musharaka): Each partner can keep its share in the partnership until the very end of the joint venture, project, or business. However, the partners are often allowed to withdraw or transfer their shares (unless the initial contract specifically states that all partners shall remain in the partnership until the date of maturity). If one of the partners withdraws from the contract, the whole partnership doesn’t terminate.

![]() Declining balance partnership (diminishing musharaka): One partner is allowed to buy the other partner’s share of equity step by step until the whole equity of the other partner is transferred. It’s called a declining balance partnership because one partner’s equity balance declines gradually.

Declining balance partnership (diminishing musharaka): One partner is allowed to buy the other partner’s share of equity step by step until the whole equity of the other partner is transferred. It’s called a declining balance partnership because one partner’s equity balance declines gradually.

If the diminishing musharaka setup sounds confusing, think of it this way: A client and a bank are willing to enter a partnership for a project or business. The partnership project or business is divided into a number of equity units, and the partners agree on certain periods of time to remain invested; this agreement appears in the contract. The client that eventually wants to have full ownership of the project repurchases the equity units step by step over time. (The client can either repurchase a fixed number of units each period or repurchase an increasing number of units per period.) At the end of the contract, the client owns the full project or property.

The profit and loss sharing (PLS) ratio may be revised every time the client repurchases equity units or according to some other agreement between the bank and the client. The bank derives income from this transaction in two ways. First, the bank’s investment comes back in full (assuming the project or business is a success). Second, the bank receives whatever percentage of profit is designated in the partnership agreement.

Islamic banks use consecutive musharaka when they’re investing in a project, joint venture, or business activity. Both parties share the profits or losses of this partnership based on their initial musharaka agreement.

The declining balance partnership contract is applied by Islamic banks and other financial institutions (such as the California-based American Finance House [LARIBA] and Dubai Islamic Bank) mainly to real estate purchases. This contract sets up something akin to a rent-to-own scenario. For example, if you’re planning to purchase a house and you work with an Islamic bank based on the diminishing musharaka contract, the system works this way: You sign a partnership agreement with the bank to purchase the house. (Therefore, both you and the bank own the house.) Then the bank leases its share in the property back to you for a certain period of time; you rent the house. The bank receives your rental income and periodically applies a certain portion of that rent money to the contract (based on whatever percentage and time periods you and the bank agree on initially). Eventually, your ownership in the house increases (and the bank’s ownership decreases) until you become the only owner of the house.

Figuring Out Asset-Based Financing Instruments

In this section, I introduce you to asset-based products available from Islamic banks based on the contracts of murabaha, reverse murabaha, ijara, and istisna. These contracts allow bank customers to finance cars, homes, business supplies, and other major purchases that require more cash than the customer currently has available.

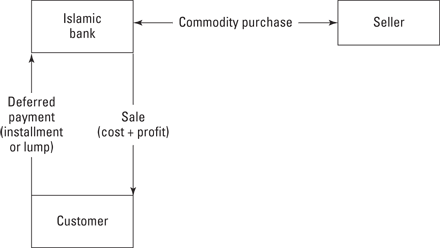

Making purchases with cost plus profit (murabaha) contracts

In this kind of agreement, a commodity is sold for cost plus profit, and both the buyer and seller know the cost and the profit involved. Basically, this product is a kind of trade financing instrument used by Islamic banks.

Understanding murabaha basics

Under a murabaha contract, a bank purchases a commodity in order to supply it to a customer who isn’t financially able to make such a purchase directly. The bank sells the commodity to the customer for the cost plus profit — the profit being a markup that both the bank and customer agree on upfront. The customer can make a lump payment when the commodity is delivered but usually sets up a deferred payment installment schedule.

For example, say a manufacturer wants to buy $100,000 worth of wood but doesn’t have enough funds. The manufacturer approaches the bank and signs an agreement to purchase the wood from the bank at cost ($100,000) plus profit (maybe 20 percent of the contract amount, or $20,000). The manufacturer is liable to pay the bank $120,000 after the bank delivers the goods. Both parties know the profit and the cost of the product at the onset; there’s no financial uncertainty in the transaction.

Sharia scholars don’t advocate using the deferred payment system in a murabaha contract. Instead, they encourage using murabaha as a financial instrument only when other equity financing, such as mudaraba and musharaka, can’t be applied. The bank is allowed to take assets as security against potential future default by the client. However, when no such assets are available, the bank can take the commodity, which is financed by the bank.

Figure 10-4 shows how the cost plus profit contract (murabaha) works.

Figure 10-4: The murabaha contract in action.

The murabaha contract is a basic sale transaction, and certain rules need to be followed to make sure it’s sharia-compliant:

![]() If the client defaults on the payment, the financier isn’t allowed to charge extra fees as late payment or penalty charges. Sharia scholars allow charging additional fees in cases of loss or damage due to a client’s default, and they allow certain penalties to ensure that a buyer is not negligent. But such fees and penalties cannot be treated as income for the bank; they must be given to charity.

If the client defaults on the payment, the financier isn’t allowed to charge extra fees as late payment or penalty charges. Sharia scholars allow charging additional fees in cases of loss or damage due to a client’s default, and they allow certain penalties to ensure that a buyer is not negligent. But such fees and penalties cannot be treated as income for the bank; they must be given to charity.

![]() The contract should be used only for purchases. It’s not intended to be used for financing a working capital requirement.

The contract should be used only for purchases. It’s not intended to be used for financing a working capital requirement.

Here are two types of murabaha contracts an Islamic bank may offer:

![]() Murabaha to the purchase orderer: In this contract, the bank specifically purchases the assets for the client’s order. The client requests that the bank purchase the good(s) on her behalf, and she agrees to buy the good(s) from the bank.

Murabaha to the purchase orderer: In this contract, the bank specifically purchases the assets for the client’s order. The client requests that the bank purchase the good(s) on her behalf, and she agrees to buy the good(s) from the bank.

![]() Commodity murabaha: In Chapter 9, I explain that interbank transactions are a source of funds for Islamic banks. The commodity murabaha is used as an instrument in Islamic interbank transactions. Generally, this financial instrument is used to fund the Islamic bank’s short-term liquidity requirement. This product was developed as an alternative to conventional interbank funding.

Commodity murabaha: In Chapter 9, I explain that interbank transactions are a source of funds for Islamic banks. The commodity murabaha is used as an instrument in Islamic interbank transactions. Generally, this financial instrument is used to fund the Islamic bank’s short-term liquidity requirement. This product was developed as an alternative to conventional interbank funding.

Commodities such as gold, silver, barley, salt, wheat, and dates, which are used as mediums of exchange, aren’t allowed to be traded under the commodity murabaha contract.

Clearing up misconceptions

Certain misconceptions exist about the cost plus profit contract and conventional banking loans. Many bankers take a view that the murabaha contract is a synthesized loan (a loan divided into pieces based on the risk involved). This misconception is inflamed because Islamic banks use conventional, interest-based benchmarks such as LIBOR (the London Interbank Offered Rate) to determine what profit rate to charge for such contracts. However, conventional bank loans and murabaha contracts are indeed different. In the murabaha contract

Certain misconceptions exist about the cost plus profit contract and conventional banking loans. Many bankers take a view that the murabaha contract is a synthesized loan (a loan divided into pieces based on the risk involved). This misconception is inflamed because Islamic banks use conventional, interest-based benchmarks such as LIBOR (the London Interbank Offered Rate) to determine what profit rate to charge for such contracts. However, conventional bank loans and murabaha contracts are indeed different. In the murabaha contract

![]() Financing is linked to the asset purchased on behalf of the client. No money is actually loaned to the client, as happens with conventional banks.

Financing is linked to the asset purchased on behalf of the client. No money is actually loaned to the client, as happens with conventional banks.

![]() The markup of the asset doesn’t increase if the client defaults on the payment installments. In contrast, conventional banks compound the interest and charge a penalty in this circumstance.

The markup of the asset doesn’t increase if the client defaults on the payment installments. In contrast, conventional banks compound the interest and charge a penalty in this circumstance.

![]() Economic activity is produced when real assets are traded. Conventional banks lend money to clients without any tangible economic activity taking place.

Economic activity is produced when real assets are traded. Conventional banks lend money to clients without any tangible economic activity taking place.

What about the benchmark rates? Because the Islamic banking industry never before had its own benchmark for markup rates, it opted to follow conventional benchmarks such as LIBOR. That doesn’t mean that Islamic banks were charging an interest rate; they simply got guidance for what may constitute acceptable fees. However, in late 2011, Thomson Reuters developed a benchmark called the Islamic Interbank Rate (IIBR) that is likely to alleviate this source of controversy.

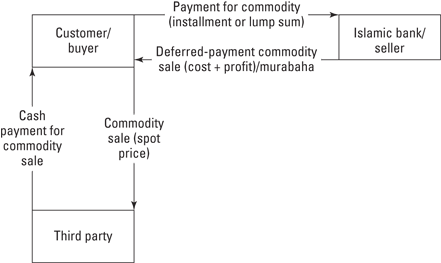

Reverse murabaha (tawarruq)

Tawarruq is a financial instrument in which a buyer purchases a commodity from a seller on a deferred payment basis, and the buyer sells the same commodity to a third party on a spot payment basis (meaning that payment is made on the spot). The buyer basically borrows the cash needed to make the initial purchase. Later, when he secures the cash from the second transaction, the buyer pays the original seller the installment or lump sum payment he owes (which is cost plus markup, or murabaha).

Because the buyer has a contract for a murabaha transaction, and later the same transaction is reversed, this scenario is called a reverse murabaha. Both transactions involved must be sharia-compliant.

Tawarruq is a somewhat controversial product. Because the intention of the commodity purchases isn’t for the buyer’s use or ownership, certain scholars believe that the transactions aren’t sharia-compliant. Their argument is that the absence of any real economic activities creates interest, which is prohibited in sharia. Scholars who accept this contract as valid note that it is based on two valid legal contracts, murabaha and sales. Despite the controversy, however, many Islamic banks, including the United Arab Bank, QNB Al Islamic, Standard Chartered of United Arab Emirates, and Bank Muaamalat of Malaysia, use tawarruq products.

Generally, commodities such as gold, silver, barley, salt, wheat, and dates aren’t allowed in tawarruq. However, the London Metal Exchange (LME) has been used by many Islamic banks as a platform for tawarruq because metal is not part of its commodities transactions.

How does tawarruq work in matters of personal finance? First, the customer purchases a commodity (other than a medium of exchange) from the bank on a cost plus profit basis. Then the customer sells that commodity to a third party. (In reality, the customer simply authorizes the bank to sell the commodity to the third party on his behalf.) The proceeds from the sale are credited to the customer’s account, and the customer pays back the bank (the cost plus profit).

See Figure 10-5 for an illustration of this process. (Note that the illustration doesn’t indicate that the bank generally sells the commodity on behalf of the customer.)

Figure 10-5: The reverse murabaha (tawarruq) process.

Leasing or renting (ijara)

The Arabic term ijara means “providing services and goods temporarily for a wage.” The ijara contract, as you may guess, involves providing products or services on a lease or rental basis. In the ijara contract, a person or party is given the right to use the object (the usufruct) for a period of time; the owner retains the ownership of the assets.

The ijara contract is similar to a conventional lease in which the owner rents or leases his property or goods to a lessee for a specified number of periods for a fee. For example, the lessee is responsible for normal maintenance, and the lessor is responsible for major maintenance, just as with many conventional lease contracts. However, the following features of ijara differentiate it from a conventional lease:

![]() The lessor must own the assets for the full lease period.

The lessor must own the assets for the full lease period.

![]() If the lessee defaults on payments or delays payments, the lessor can’t charge compound interest.

If the lessee defaults on payments or delays payments, the lessor can’t charge compound interest.

![]() The leased asset’s use is specified in the contract.

The leased asset’s use is specified in the contract.

Three types of ijara arrangements can exist according to sharia principles:

![]() Lease-ending ownership/lease with ownership (ijara wa iqtina/ ijara muntahia bitamleek): In this ijara contract, the lessee owns the leased asset at the end of the lease period. This lease contract doesn’t contain any promise to buy or sell the assets, but the bank may offer a (verbal) unilateral promise of transfer of ownership or offer a purchase schedule for the asset. (See Chapter 6 for an explanation of unilateral promises, which are binding only on the party making the promise.) The lessee also is allowed to make a (verbal) unilateral promise to purchase the asset. The purchase price is ultimately decided by the market value of the asset or a negotiated price.

Lease-ending ownership/lease with ownership (ijara wa iqtina/ ijara muntahia bitamleek): In this ijara contract, the lessee owns the leased asset at the end of the lease period. This lease contract doesn’t contain any promise to buy or sell the assets, but the bank may offer a (verbal) unilateral promise of transfer of ownership or offer a purchase schedule for the asset. (See Chapter 6 for an explanation of unilateral promises, which are binding only on the party making the promise.) The lessee also is allowed to make a (verbal) unilateral promise to purchase the asset. The purchase price is ultimately decided by the market value of the asset or a negotiated price.

![]() Operating lease (operating ijara): This type of ijara contract doesn’t include the promise to purchase the asset at the end of the contract. Basically, this setup is a hire arrangement with the lessor.

Operating lease (operating ijara): This type of ijara contract doesn’t include the promise to purchase the asset at the end of the contract. Basically, this setup is a hire arrangement with the lessor.

![]() Forward lease (ijara mawsoofa bil thimma): This contract is a combination of construction finance (istisna, which I explain in the next section) and a redeemable leasing agreement. Because this lease is executed for a future date, it’s called forward leasing. The forward leasing contract buys out the project (generally a construction project) as a whole at its completion or in tranches (portions) of the project.

Forward lease (ijara mawsoofa bil thimma): This contract is a combination of construction finance (istisna, which I explain in the next section) and a redeemable leasing agreement. Because this lease is executed for a future date, it’s called forward leasing. The forward leasing contract buys out the project (generally a construction project) as a whole at its completion or in tranches (portions) of the project.

Many ijara products are on the market with different combinations of contracts. For example, Malaysian-based Maybank offers car financing with a combination of an ijara contract and a bai (purchase) contract. ADCB (Abu Dhabi Commercial Bank) offers ijara home financing, as does SABB (Saudi British Bank) Amanah.

Financing construction projects or purchase orders (istisna)

Istisna is a financial instrument in which a manufacturer agrees to complete a construction project on a future date for a fixed, agreed-upon price and with product specifications that both parties agree to. If the project doesn’t fit the contract specifications, the buyer has the right to withdraw from it.

This financial instrument provides for payment flexibility between the manufacturer and the buyer. The contract doesn’t demand that the buyer pay in advance or that the manufacturer receive only a lump sum at the time of delivery. Instead, both parties can set a schedule of payment. The following sections address some of the finer points of istisna.

Istisna instruments are widely used in the construction industry or for project financing and trade financing. For example,

![]() Kuwait Finance House (KFH) uses the istisna contract for home financing (properties under construction) and project financing.

Kuwait Finance House (KFH) uses the istisna contract for home financing (properties under construction) and project financing.

![]() Qatar Islamic Bank (QIB) signed an istisna agreement in late 2010 to finance a major residential complex in the north of Qatar.

Qatar Islamic Bank (QIB) signed an istisna agreement in late 2010 to finance a major residential complex in the north of Qatar.

Minimizing uncertainty (gharar)

Usually, a contract for a not-yet-manufactured product presents some uncertainty about the product. As I explain in Chapter 1, Islamic law prohibits finance institutions from being part of transactions that involve uncertainty (called gharar). To avoid uncertainty, the istisna contract is as detailed as possible regarding what the end product will be.

In the istisna contract, the customer approaches the bank with the desired asset’s specifications. Both the customer and the bank sign the istisna contract, and then the bank manufactures the product or the asset for the customer through its agent, such as a manufacturer.

Opting for parallel istisna

When the bank provides the customer with the istisna financial instrument, the customer signs the contract with the bank for the specified asset or project. Then the bank (via its manufacturing agent) manufactures the asset or project per the customer’s specifications. However, in some circumstances the bank doesn’t want to produce the item for the customer. In this case, the bank opts to use two mutually independent istisna contracts called parallel istisna.

Here’s how this system works: The customer who wants the project or asset enters an istisna contract with the bank per the customer’s specifications. The bank then enters into a parallel istisna contract with a manufacturer (which is not the bank’s agent; it is a separate third party) to meet those same specifications. In theory, when the manufacturer completes the asset or project, it delivers that product to the bank. (In practice, the manufacturer usually delivers the product directly to the customer.) The bank pays the manufacturer, and the customer pays the bank according to the agreed payment schedule. The bank marks up the manufacturer’s price in the contract with the customer to secure a profit.

Figure 10-6 offers an illustration of the parallel istisna process. Keep in mind that a separate istisna contract exists on both sides: between the customer and the bank, and between the bank and the manufacturer.

Figure 10-6: The parallel istisna process.

For example, fictional customer Acme, Inc., approaches the World’s Best Islamic Bank to manufacture a housing scheme with specifications for $1 million. Then the bank enters an agreement with A Construction Company to build the houses with the same specifications for $800,000. When the construction project is complete, A Construction Company hands over the project to the bank, which verifies the specifications and delivers the product to Acme, Inc., on the payment basis agreed to in that part of the istisna. The bank goes for a parallel contract in this scenario because it can’t produce the assets and doesn’t want to hold the produced assets after their completion. In a parallel contract, the bank has both a buyer for its products and a manufacturer.

Talking about Trade Financing Instruments

Trade-based financing instruments provide short-term liquidity solutions for individuals and corporations. Two Islamic banking instruments that are based on sharia-compliant sales contracts are deferred payment sale and purchase with deferred delivery; I cover both in the next sections.

Deferred payment sale (bay al-muajil)

The deferred payment sale is a simple transaction in which a product is sold for a deferred payment — either an installment or lump sum. Here are two key conditions:

![]() The seller and buyer agree on the price at the time of trade.

The seller and buyer agree on the price at the time of trade.

![]() The seller can’t charge extra if the buyer delays or misses a payment.

The seller can’t charge extra if the buyer delays or misses a payment.

In practice, the bay al-muajil instrument is used in combination with murabaha (cost plus profit; flip to the earlier section “Making purchases with cost plus profit [murabaha] contracts” for more on this product). The bank purchases an asset from a seller and then sells it to the customer at a higher price than the purchase price.

For example, a customer who wants to purchase a house agrees with the seller on a sale price. The customer then seeks an Islamic bank to finance his house purchase, stating the sales price and other facts. The Islamic bank uses an independent valuation to verify the house’s value. Then the Islamic bank acquires the house from the seller by changing the ownership and paying the sales price. After the house becomes the Islamic bank’s property, the bank sells the house to the customer at a higher price. Basically, the Islamic bank signs a murabaha contract with the customer, and the title is transferred. The customer’s payments are secured by the house, and the payment schedule is arranged by both parties.

Purchase with deferred delivery (salam)

In this contract, which may also be called bay al-salam, full advance (on-the-spot) payment is made for goods to be delivered on a future date. This instrument is a mode of financing future economic activity or a product that is going to be produced in the future. The seller promises to supply the specific product(s) to the buyer on the specific future date; the buyer provides the full funds in advance. This upfront payment is the key difference between salam and a conventional forward contract.

Sharia allows salam only as an exceptional instrument to sell something that doesn’t yet exist. Per sharia, for the sale of a product to occur, it must meet the following basic conditions:

![]() The product must physically exist.

The product must physically exist.

![]() The seller must have ownership of the product.

The seller must have ownership of the product.

![]() The product is in the seller’s possession or at least in his control.

The product is in the seller’s possession or at least in his control.

![]() Full payment must be made in advance.

Full payment must be made in advance.

Obviously, the first condition creates a problem when you’re talking about a product that someone wants created for future delivery. Therefore, salam is allowed only with strict conditions, such as these:

![]() The seller legally possesses the product to be delivered.

The seller legally possesses the product to be delivered.

![]() The contract specifies the date and time of the delivery.

The contract specifies the date and time of the delivery.

![]() The product’s quality and quantity can be specified in the contract. For example, specifying a future purchase of precious stones is difficult because every stone is different from others in quality, weight, or size.

The product’s quality and quantity can be specified in the contract. For example, specifying a future purchase of precious stones is difficult because every stone is different from others in quality, weight, or size.

The Prophet Muhammad (pbuh) allowed the salam contract to help farmers buy necessary raw materials. Because interest is prohibited in Islamic law, traders and farmers didn’t have the capital to borrow for their investments. This permission helps farmers and traders get the necessary capital before their production or trading occurs. Otherwise, they would need to seek out interest-bearing borrowing.

Salam versus istisna

Purchase with deferred delivery (salam, a trade-based financing instrument) and construction project finance (istisna, an asset-based product) seem to be quite similar, but they have some key differences. Here’s what distinguishes the two:

![]() The full price of a salam contract is paid in advance, but the istisna payment can be scheduled as a payment in advance, an installment payment, or a lump sum payment after delivery.

The full price of a salam contract is paid in advance, but the istisna payment can be scheduled as a payment in advance, an installment payment, or a lump sum payment after delivery.

![]() The product delivery date needs to be specified for a salam contract but not for an istisna contract. (However, a maximum allowed time frame should be included in the istisna contract.)

The product delivery date needs to be specified for a salam contract but not for an istisna contract. (However, a maximum allowed time frame should be included in the istisna contract.)

In reality, Islamic banks often engage in parallel salam contracts. This setup means that the bank enters a salam contract with a seller for a certain product and makes the full payment in advance for a specified future delivery. Then the bank enters another salam contract (the parallel contract) with a purchaser for the same good (after it’s delivered) for a higher price. Finally, when the good is delivered to the bank, the bank delivers it to the parallel salam purchaser. The bank makes a profit between the two transactions. ADCB Islamic Banking and Dubai Islamic Bank are just two examples of banks that provide parallel salam contracts.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.