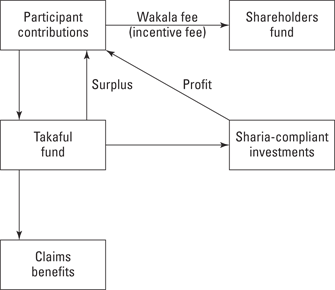

Figure 19-1: The wakala model at work in a takaful fund.

Chapter 19

Takaful and Retakaful Products, Structures, and Governance

In This Chapter

![]() Getting a taste of general and family takaful products

Getting a taste of general and family takaful products

![]() Identifying takaful contract structures

Identifying takaful contract structures

![]() Introducing the retakaful industry

Introducing the retakaful industry

![]() Heeding the governance of the sharia board

Heeding the governance of the sharia board

As I explain in Chapter 18, Islamic scholars don’t accept conventional insurance as being sharia-compliant because it involves prohibited elements of uncertainty, gambling, and interest. Therefore, a fairly new world of commercial insurance products has emerged to satisfy consumers seeking sharia compliance.

If you travel through Malaysia or a country in the Gulf Cooperation Council (Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, or United Arab Emirates), you’ll likely see billboards with messages such as “Share your risk in a sharia-compliant way” or “Save for your family in a sharia-compliant way.” Such ads promote Islamic insurance products called takaful that exist to decrease risks related to everything from travel and retirement to international trading.

Takaful companies are gaining a meaningful global market share in the insurance industry by offering a diverse range of risk-management products. Takaful products are typically categorized into two types: general takaful and family takaful. I describe examples of each in this chapter and give you the scoop on reinsurance products called retakaful. I also touch on the role of sharia boards in the takaful industry.

Checking Out General Takaful Products

The conventional insurance industry offers lots of products that protect items of value, such as homes, cars, and business inventory. General takaful products serve a similar purpose: They protect against the risk that your valuable items may be stolen, damaged, or destroyed. In other words, these products help you replace or repair the stuff you’d have a hard time replacing or repairing on your own.

Takaful operators develop general takaful products to bear the loss of, or damage to, a policyholder’s assets in a sharia-compliant manner. General takaful are short-term policies, typically renewed annually.

All the takaful products I describe in this chapter have conventional insurance counterparts that provide similar coverage but use a different product structure that relies on a different transfer of risk. As I explain in Chapter 18, takaful products of all kinds function with policyholder contributions (gifts) to a pooled takaful fund. If any policyholder suffers a loss — for general takaful, a loss of or damage to assets — the other policyholders (through their contributions) are responsible for covering the member affected by the misfortune, and their fund pool covers the loss or damage.

All the takaful products I describe in this chapter have conventional insurance counterparts that provide similar coverage but use a different product structure that relies on a different transfer of risk. As I explain in Chapter 18, takaful products of all kinds function with policyholder contributions (gifts) to a pooled takaful fund. If any policyholder suffers a loss — for general takaful, a loss of or damage to assets — the other policyholders (through their contributions) are responsible for covering the member affected by the misfortune, and their fund pool covers the loss or damage.

Two major groups of general takaful exist: individual and business takaful. I examine each in the following sections.

Individual general takaful products

Individual general takaful products bear costs related to the repair or replacement of an individual’s takaful-covered assets in a sharia-compliant manner. The takaful products offered may cover assets ranging from luggage to cars to homes — and even someone’s health. (Hence, medical insurance is considered an individual general takaful product.) I examine these four examples here so you can get a sense of what the most common takaful products entail.

Traveler’s takaful

Travel insurance is fairly easy to understand — and essential for people who make frequent trips (such as those conducting international business) and folks traveling a long distance from home. Traveler’s takaful products allow policyholders to contribute to a fund that offers them coverage in case they lose their passports, their luggage, or other property (such as jewelry, cellphones, or laptops) while on the road. It kicks in to offset costs associated with delayed baggage as well.

In addition, traveler’s takaful covers costs when someone experiences a medical emergency far from home. Trip cancellation costs are also covered as are costs related to personal accidents and personal liability toward a third party.

Motor takaful

Motor (auto) insurance is compulsory in the majority of countries across the globe: If you don’t have motor insurance, you aren’t allowed to drive. But for Muslim drivers, conventional insurance products pose a problem because they aren’t sharia-compliant. Therefore, motor vehicle takaful products play a crucial role in the Islamic insurance market: They help sharia-compliant Muslims get the insurance coverage the law requires without compromising consumers’ adherence to the Islamic faith. Most takaful companies provide motor takaful products. (See Chapter 18 for details about why conventional insurance plans aren’t sharia-compliant.)

Here’s how it works: Policyholders contribute to a motor takaful fund and agree via contract to help each other in cases of loss or damage to participants’ vehicles and other damages that may result from an auto accident. When the takaful policy reaches maturity (at the end of a year, for example), participants are entitled to a share of any surplus that remains in the takaful fund. The fund participants and takaful operator share the surplus based on a pre-agreed ratio. See the “Sharing surplus” sidebar for an example of how a policyholder may figure his share.

What exactly is covered by a motor takaful product? Generally, a takaful operator offers coverage that compares with that offered by conventional insurance companies. Take the example of the motor takaful offered by Abu Dhabi National Takaful Company in United Arab Emirates. If you participate in its products, here’s the coverage you can get:

What exactly is covered by a motor takaful product? Generally, a takaful operator offers coverage that compares with that offered by conventional insurance companies. Take the example of the motor takaful offered by Abu Dhabi National Takaful Company in United Arab Emirates. If you participate in its products, here’s the coverage you can get:

![]() Loss or damage to the vehicle: If you wreck or roll your car or if it’s stolen, catches on fire, or is otherwise damaged by the “malicious act of any third party,” you’re covered.

Loss or damage to the vehicle: If you wreck or roll your car or if it’s stolen, catches on fire, or is otherwise damaged by the “malicious act of any third party,” you’re covered.

![]() Third-party liability: If your vehicle is involved in a collision that kills or hurts passengers in another car (or bystanders), you’re covered. The takaful fund also pays for damage to property owned by a third party (someone other than you and the other driver).

Third-party liability: If your vehicle is involved in a collision that kills or hurts passengers in another car (or bystanders), you’re covered. The takaful fund also pays for damage to property owned by a third party (someone other than you and the other driver).

![]() Additional coverage: If you get a flat tire, need a tow or roadside assistance, have a dead battery that needs a jump, or run out of gas, the takaful covers the expenses related to getting the help you need. You can also purchase coverage that gives you, your family members, and/or your employees personal accident benefits. Policies that cover your emergency medical expenses and/or replacement of any personal items in your car that are stolen or destroyed in a fire are also available.

Additional coverage: If you get a flat tire, need a tow or roadside assistance, have a dead battery that needs a jump, or run out of gas, the takaful covers the expenses related to getting the help you need. You can also purchase coverage that gives you, your family members, and/or your employees personal accident benefits. Policies that cover your emergency medical expenses and/or replacement of any personal items in your car that are stolen or destroyed in a fire are also available.

Motor takaful participation is accepted as legal insurance coverage in many nations, including some non-Muslim nations, as an alternative to conventional auto insurance. As long as a takaful operator is registered as an insurance company in a particular nation, its coverage is accepted as valid insurance there. For example, motor takaful coverage is available and valid in Indonesia, Kenya, Malaysia, Pakistan, Qatar, Saudi Arabia, Sri Lanka, and United Arab Emirates. Takaful companies have not yet made significant inroads in Western nations, but I expect them to move into Western markets in the near future.

House owner or householder takaful

The house owner or householder takaful provides coverage for residential buildings and household contents (such as furniture, clothing, home computers, and so on). This product is the Islamic alternative to conventional homeowners and renters insurance.

What kind of coverage can you expect from this type of policy? Many options are available that offer a spectrum of coverage. For example, you can shop for a takaful product that specifically covers damage to or loss of assets or cash because of a home burglary. Or you can look for a broader policy that covers a range of risks, such as the Home Takaful Plan offered by SABB Takaful in Saudi Arabia. Participating in this plan allows you to get coverage for the following:

![]() Loss of or damage to the building and its contents: If your home is damaged by fire, a storm, a vehicle, someone else’s “malicious acts” (including burglary), or “other perils” (that aren’t self-inflicted), you’re covered.

Loss of or damage to the building and its contents: If your home is damaged by fire, a storm, a vehicle, someone else’s “malicious acts” (including burglary), or “other perils” (that aren’t self-inflicted), you’re covered.

![]() Loss of rental income and expenses related to finding new accommodations: If you’re renting the home to other people and lose rental income because of the types of perils listed in the previous bullet, you’re covered. If you live in the home and need to move out for a while because it’s so badly damaged, the plan covers that expense as well.

Loss of rental income and expenses related to finding new accommodations: If you’re renting the home to other people and lose rental income because of the types of perils listed in the previous bullet, you’re covered. If you live in the home and need to move out for a while because it’s so badly damaged, the plan covers that expense as well.

![]() Loss or damages when moving: Your possessions are covered when you’re moving.

Loss or damages when moving: Your possessions are covered when you’re moving.

![]() Domestic helper coverage: If you have someone working in your home and that person gets hurt or dies at your home, the takaful covers your expenses related to this situation.

Domestic helper coverage: If you have someone working in your home and that person gets hurt or dies at your home, the takaful covers your expenses related to this situation.

![]() Third-party claims: You can purchase coverage that comes into play when someone visiting your home has an accident that results in injury.

Third-party claims: You can purchase coverage that comes into play when someone visiting your home has an accident that results in injury.

Medical takaful

Are you surprised that health insurance is included in the category of general takaful? Think of it this way: Your health is perhaps your most important asset. Medical takaful products help you protect this asset against damage or loss by helping you pay to see doctors, get medications, and pursue other medical treatment when necessary.

For people who live in parts of the world where federal or state governments don’t provide healthcare benefits, medical insurance is crucial. Anyone who doesn’t have it faces enormous risk related to the costs of seeking treatment in cases of serious injury or illness. Medical takaful products generally cover expenses related to illnesses, accidents, and chronic health conditions. Maternity, optical, and dental expenses are often covered as well. Many takaful operators offer medical takaful funds.

Business general takaful products

Owners tend to invest huge amounts of their savings in a business. They need to protect their investments against the risk of unpredictable events, such as a customer slipping and falling on a retail shop floor or a factory worker suffering an accident during a product manufacturing process. As with conventional business insurance products, takaful operators may offer customized products for business owners. In this section, I introduce you to a handful of the most common business takaful products.

Liability takaful

Takaful operators, in the footsteps of their conventional insurance counterparts, have developed many liability-related business products to protect the assets of business owners. Such products protect a business organization whenever any of its stakeholders — employees, customers, or owners — or the general public incurs damage or loss related to the business’s activities.

Following are some of the liability takaful available in the Islamic insurance industry:

![]() Employer’s liability takaful: This type of product protects an employer when one of its employees incurs an injury, contracts a disease, or dies due to the employee’s own negligence on the job. If a business owner purchases this type of takaful, he reduces his risk of losing large sums of money (or even the entire business operation) because of an employee’s negligence.

Employer’s liability takaful: This type of product protects an employer when one of its employees incurs an injury, contracts a disease, or dies due to the employee’s own negligence on the job. If a business owner purchases this type of takaful, he reduces his risk of losing large sums of money (or even the entire business operation) because of an employee’s negligence.

![]() Workers’ compensation takaful: A companion product to the employer’s liability takaful is the workers’ compensation takaful. Whether due to their own negligence or to factors out of their control, employees run the risk of accident, illness, or even death on the job — no matter what type of work environment they’re in. This type of product, purchased by the business owner, covers employee expenses related to such incidents.

Workers’ compensation takaful: A companion product to the employer’s liability takaful is the workers’ compensation takaful. Whether due to their own negligence or to factors out of their control, employees run the risk of accident, illness, or even death on the job — no matter what type of work environment they’re in. This type of product, purchased by the business owner, covers employee expenses related to such incidents.

![]() Public liability takaful: This type of takaful provides a company with coverage against legal liability to the general public for harm caused by the negligence of the company’s employees or owners or by a defect in the company’s machines or properties. For example, if the business owners fail to maintain a sidewalk in front of the facility and someone trips and falls, or if employee negligence leads to pollutants being released into the public water supply, this type of product comes into play.

Public liability takaful: This type of takaful provides a company with coverage against legal liability to the general public for harm caused by the negligence of the company’s employees or owners or by a defect in the company’s machines or properties. For example, if the business owners fail to maintain a sidewalk in front of the facility and someone trips and falls, or if employee negligence leads to pollutants being released into the public water supply, this type of product comes into play.

![]() Professional indemnity (malpractice) takaful: Clients can sue professionals such as lawyers, doctors, architects, and engineers for losses and damages related to the professionals’ negligence while performing their duties. If a doctor’s patient dies, for example, and the patient’s family believes that doctor negligence is at fault, that doctor may face a very serious and substantial malpractice lawsuit.

Professional indemnity (malpractice) takaful: Clients can sue professionals such as lawyers, doctors, architects, and engineers for losses and damages related to the professionals’ negligence while performing their duties. If a doctor’s patient dies, for example, and the patient’s family believes that doctor negligence is at fault, that doctor may face a very serious and substantial malpractice lawsuit.

Marine and aviation takaful

Separate from liability takaful, another type of business general takaful product is the marine and aviation takaful. This type of takaful plan covers the loss or damage of cargo in transit — goods transported by land, air, or sea. For any company that transports its products internationally (or even over a significant distance within its country’s borders), this kind of asset coverage is a must.

Engineering business takaful plan

This type of takaful plan provides coverage for risks and liabilities in the construction industry. It protects against the loss of or damage to projects under construction, including buildings, bridges, and roads. For example, an engineering business takaful product may cover expenses related to problems with a contractor’s plant, electronic equipment, the deterioration of stock, and machinery breakdowns.

General accident takaful

This broad takaful category provides coverage for commercial entities against any risk that’s caused by human action. For example, this category includes takaful for the following scenarios:

![]() Burglary takaful: This product provides coverage for any damage to, or loss of, assets or cash because of burglary (to a retail business, for example).

Burglary takaful: This product provides coverage for any damage to, or loss of, assets or cash because of burglary (to a retail business, for example).

![]() Event cancellation: Canceling an event creates many expenses for the event organizer, such as lost revenue from ticket sales, cancellation charges, and sponsorship expenses. (Consider how much money a concert organizer can lose if the headline performer comes down with pneumonia the day before the show, for example.) This takaful coverage helps to protect against such expenses.

Event cancellation: Canceling an event creates many expenses for the event organizer, such as lost revenue from ticket sales, cancellation charges, and sponsorship expenses. (Consider how much money a concert organizer can lose if the headline performer comes down with pneumonia the day before the show, for example.) This takaful coverage helps to protect against such expenses.

![]() Money plan: This takaful product provides protection for money in transit and money on premises, such as money that’s locked in a safe or placed in a cash register.

Money plan: This takaful product provides protection for money in transit and money on premises, such as money that’s locked in a safe or placed in a cash register.

Exploring Family Takaful Products

Conventional life insurance provides financial help to the insured family in case of death, and conventional disability insurance covers expenses when someone faces the consequences of a serious illness or accident that impedes her ability to work and function as normal. However, these conventional insurance contracts are based on speculation (maysir) and uncertainty (gharar), which are prohibited per Islam. (After all, who can predict the date of the insured’s death or whether a tragic accident will cause long-term injury?) This means that a customer seeking sharia compliance needs an alternative type of product. (See Chapter 18 for details about why conventional insurance plans aren’t sharia-compliant.)

The Islamic alternative to conventional life and disability insurance is family takaful products. These plans are basically savings or investment products that have maturity dates and are designed to fulfill the future needs of the policyholders. Family takaful products provide benefits to the insured family when tragedy strikes, and the policyholder also enjoys the returns from a long-term savings investment.

Applying participants’ contributions

The participants or policyholders in a family takaful fund enter into a long-term, defined-period contract with the takaful operator. As in the conventional system, participants select the most suitable plan (including the length of contract) according to their needs.

Consider a family takaful plan offered by SABB Takaful in Saudi Arabia. Its plan ranges in length from 5 to 30 years and is offered to people between the ages of 18 and 65, with the stipulation that the insured (the policyholder) can’t be older than 75 when the plan matures.

Participants in a family takaful product make contributions (referred to as gifts) to the fund. Most of the contributions go to a part of the fund called the participants’ special account (PSA), which supports fund participants who need help. Any participant who becomes seriously ill or has a disabling accident before the plan’s maturity date can receive assistance from the fund, and the family of a participant who dies before the maturity date also receives assistance. If few participants experience such misfortunes, the surplus funds are shared between participants and the takaful operator based on the takaful model the company follows. (I describe takaful models in the upcoming section “Understanding Takaful Structures.”)

Although most of the participants’ contributions go into the PSA, a portion of their money is simultaneously funneled into a savings or investment account, often called a participants’ account (PA), and invested in sharia-compliant products. The profit or loss from such investments is shared according to a ratio that the policyholders and the takaful operator agree on at the time of the contract. Therefore, although a family takaful product serves the crucial purpose of mitigating risk related to a personal tragedy, it also promotes savings and investment for the family’s long-term benefit.

Assisting policyholders

Family takaful policyholders stand to benefit in different ways depending on whether they stay healthy or experience disability or death prior to the plan’s maturity date. If a participant stays healthy throughout the course of the takaful contract, she doesn’t receive any direct assistance from the PSA. Instead, her participation benefit derives from any surplus in the PSA (because she is entitled to a portion of that surplus) as well as any profits generated by investments in the PA.

If the participant becomes disabled due to illness or accident during the contract period, she may receive funds directly from the PSA to cover her expenses. In this case, she still shares in any profits generated by investments in the PA, but she doesn’t receive a share of any PSA surplus (because she has already benefited from that fund).

If a family takaful policyholder dies during the course of the contract, the policyholder’s beneficiaries receive the accumulated sum in the PA plus any profit available from the investments from the beginning of the contract through the due date before the death. From the PSA account, the policyholder’s beneficiaries are entitled to the amount covered by the specific takaful product.

Exploring family takaful products

The most common types of family takaful products available on the market fall into the categories individual and group. Check them out in the following sections.

Individual family takaful

Many individual family takaful products are savings takaful plans: products that are custom designed to meet the specific financial goals of the customer while offering protection against misfortunes. The customer may choose a product that helps him save toward a home purchase, for example, or for an upcoming marriage. Here are other specific types of savings takaful plans:

![]() Education takaful: This type of plan encourages savings for the future educational needs of the participant’s children. At the same time, it offers a protection component: If the participant becomes disabled or dies during the course of the takaful contract, the takaful company contributes funds for the remainder of the contract period so the savings goals are met.

Education takaful: This type of plan encourages savings for the future educational needs of the participant’s children. At the same time, it offers a protection component: If the participant becomes disabled or dies during the course of the takaful contract, the takaful company contributes funds for the remainder of the contract period so the savings goals are met.

![]() Hajj and Umra takaful: Some takaful companies offer protective coverage and savings plans for customers going on Hajj or Umra (pilgrimages to Islamic holy sites in Mecca). Such plans protect participants against any accidents that occur during the ritual period.

Hajj and Umra takaful: Some takaful companies offer protective coverage and savings plans for customers going on Hajj or Umra (pilgrimages to Islamic holy sites in Mecca). Such plans protect participants against any accidents that occur during the ritual period.

![]() Investment takaful: Although all family takaful products have an investment component, investment takaful products are more aggressively focused on investment than other takaful options. Each participant can determine how much of his contribution is funneled into the pool of protective funds (in case of death or disability) and into the investment account. Participants can also choose among a variety of maturity dates. All investments made by a takaful operator in the effort to generate profit for participants are sharia-compliant.

Investment takaful: Although all family takaful products have an investment component, investment takaful products are more aggressively focused on investment than other takaful options. Each participant can determine how much of his contribution is funneled into the pool of protective funds (in case of death or disability) and into the investment account. Participants can also choose among a variety of maturity dates. All investments made by a takaful operator in the effort to generate profit for participants are sharia-compliant.

![]() Retirement takaful plan: Like the investment takaful plan, the goal of this product is to offer both a protection against misfortune and a sharia-compliant means of investing. The key difference between an investment takaful and retirement takaful is generally the length of contract; for most people, a retirement takaful plan involves a long-term contract with a maturity that coincides with the participant’s planned retirement date.

Retirement takaful plan: Like the investment takaful plan, the goal of this product is to offer both a protection against misfortune and a sharia-compliant means of investing. The key difference between an investment takaful and retirement takaful is generally the length of contract; for most people, a retirement takaful plan involves a long-term contract with a maturity that coincides with the participant’s planned retirement date.

Group family takaful

These takaful plans are designed to cover a group of people in a company, club, or association. Takaful companies sell group takaful products to business owners and association boards of directors, for example, and they require a minimum number of participants.

Why are such plans classified as family takaful and not grouped with the business takaful products I describe earlier in this chapter? They’re life insurance products, like the other family takaful funds, which protect individuals and families against risks associated with death and disability. This version is simply designed with the employees of a certain business or the members of a certain club or association in mind. If your employer offers life and/or disability insurance as one of your employment benefits, you’ve got a conventional insurance product that’s equivalent to group family takaful.

Understanding Takaful Structures

In Chapter 18, I touch on how takaful products are generally structured. All have a few universal elements and managerial aspects. For starters, a takaful fund is basically a pool of money that participants create to help each other. But such funds can’t survive if a country’s regulations don’t allow for a cooperative legal form of business organization or for companies that lack share capital (capital stock).

Therefore, for practical reasons, takaful operators (which are usually limited liability companies and may be Islamic banks) exist to manage these pools of funds. And shareholders exist to support a fund’s startup and ongoing administrative expenses. I describe the functions of takaful operators and shareholders in Chapter 18.

Each takaful company must keep its participants’ contributions separate from its shareholder funds; the two sources of money can’t be mixed. Therefore, each takaful operator manages two separate funds:

![]() The takaful fund: This fund is the participants’ (policyholders’) money. In the case of family takaful products, this fund is divided into two separate accounts, the PSA and the PA, which I cover in the earlier section “Applying participants’ contributions.”

The takaful fund: This fund is the participants’ (policyholders’) money. In the case of family takaful products, this fund is divided into two separate accounts, the PSA and the PA, which I cover in the earlier section “Applying participants’ contributions.”

![]() The shareholders fund: Also called the operating fund, this account holds the seed money (the paid-up capital) provided by the company’s shareholders. The shareholder fund pays startup administrative expenses, and remaining capital is invested. Any profits from those investments go back into this fund. In addition, takaful participants pay ongoing management fees that are placed in the shareholders fund to support continuing administrative expenses.

The shareholders fund: Also called the operating fund, this account holds the seed money (the paid-up capital) provided by the company’s shareholders. The shareholder fund pays startup administrative expenses, and remaining capital is invested. Any profits from those investments go back into this fund. In addition, takaful participants pay ongoing management fees that are placed in the shareholders fund to support continuing administrative expenses.

Shareholders are rewarded for their investment with explicit fees that are paid out of this fund periodically. In addition, when a takaful fund earns investment profits, shareholders may receive a share of those profits.

An important point to keep in mind is that any takaful fund (regardless of its particular structure) that experiences a deficit during its operation requires underwriting or capital backing; otherwise, the fund can become insolvent. As I note in Chapter 18, the participants are theoretically responsible for covering a deficit. But in the real world, takaful shareholders underwrite the funds when deficits exist. They do so by giving the fund a qard hasan (interest-free loan). Later, when the deficit disappears and a surplus accrues, the shareholders deduct the loan amount from fund surpluses.

In the following sections, I describe the three structures most commonly used to create takaful products — the wakala, mudaraba, and combination models — so you can see how funds flow into and out of the takaful product and how that product is managed by the takaful operator.

Wakala model: The principal-agent relationship

In Islam, wakala is a contract in which one entity works as an agent for another. In the case of a wakala-based takaful product, the takaful operator works as an agent on behalf of the takaful participants, who are called the principals. (The operator, or agent, is the wakil.)

The takaful operator manages the fund and receives a pre-agreed percentage of the participants’ fund or fixed fee; this management fee is called a wakala fee. In addition, the takaful operator may charge a performance-based fee, which is its incentive to manage the fund as well as possible. The takaful operator determines what fee(s) to charge after consulting with the sharia board. Any fees it collects are placed in the shareholders fund and are used to reward the shareholders as well.

Figure 19-1 illustrates the wakala model. Note that any surplus that the takaful fund or the sharia-compliant investments generate goes back to the participant contributions. (In other words, participant contributions in the subsequent year will be lower, so participants benefit from surpluses.)

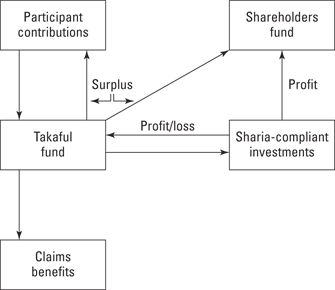

Mudaraba model: Partnership

Mudaraba is an Islamic contract based on a financial partnership in which one party (an investor) gives money to another (a fund manager) for the purpose of investing it in a business or economic activity. The investor puts up all the capital, and the fund manager provides expertise and knowledge to help the activity be successful. Both parties share the profits based on an agreed-upon ratio, but only the investor can lose the initial capital if the activity isn’t successful.

When a takaful product is based on this contract, the shareholders of the takaful company share the profit of the fund with the policyholders. The pol-icyholders are the investing partner (silent partner), called the rab al mal. The takaful company (the takaful operator and shareholders) is the working partner or fund manager, called the mudarib. The takaful company isn’t liable for any loss (unless the loss stems from the company’s own negligence or misconduct). Instead, the participants’ fund bears the loss. (The participants stand to lose money; the company stands to lose the value of its time and efforts.) The takaful company receives a percentage of the fund’s surplus (if one exists) and a percentage of any profit from investments made by the fund.

This model has been criticized by Islamic scholars who say that any surpluses in the participants fund belong to the policyholders and should be used as a reserve. Also, takaful companies share only the profit and not the financial loss of the fund, which isn’t in the best interests of the policyholders. Another concern is that takaful operators may try to increase the fund surpluses so that they can have more shares in those surpluses, which runs contrary to the core takaful concept of mutual assistance among policyholders.

This model has been criticized by Islamic scholars who say that any surpluses in the participants fund belong to the policyholders and should be used as a reserve. Also, takaful companies share only the profit and not the financial loss of the fund, which isn’t in the best interests of the policyholders. Another concern is that takaful operators may try to increase the fund surpluses so that they can have more shares in those surpluses, which runs contrary to the core takaful concept of mutual assistance among policyholders.

Figure 19-2 illustrates the mudaraba model as it applies to takaful. Note that the key difference between Figure 19-1 and Figure 19-2 is that a portion of the surpluses from both the takaful fund and the sharia-compliant investments goes into the shareholders fund in a mudaraba-based takaful. The wakala contract rewards shareholders with only a management fee and possibly an incentive fee.

Figure 19-2: The mudaraba model of takaful.

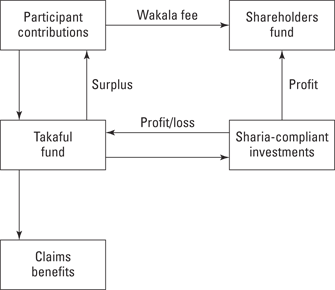

Combination model: Principal-agent relationship and partnership

This structure is the most widely used in the takaful industry and alleviates most criticisms leveled against the pure mudaraba model. Here’s how the combination model works:

![]() Using the wakala contract, the takaful company acts as the agent for the fund management and receives a fee for underwriting the fund.

Using the wakala contract, the takaful company acts as the agent for the fund management and receives a fee for underwriting the fund.

![]() Using the mudaraba contract, the takaful company acts as the fund manager for managing investments and shares the profit for the investment of the takaful fund.

Using the mudaraba contract, the takaful company acts as the fund manager for managing investments and shares the profit for the investment of the takaful fund.

Note that the company doesn’t receive any portion of a surplus in the participants fund in the combination takaful structure. Figure 19-3 illustrates the flow of money in this model.

Figure 19-3: The combination takaful model.

Getting Familiar with Retakaful (Reinsurance)

In the conventional insurance industry, an insurance company reduces its risk of paying large claims by insuring a portion of its risk with another insurance company. The third party is called a reinsurer, and it helps the insurance company in situations involving natural disasters, widespread fires, riots, and other major events that significantly affect many policyholders at once. Retakaful is the Islamic alternative to the reinsurance industry, and I explain it in this section.

Gauging the necessity of retakaful

In a nutshell, a takaful company pays premiums to a retakaful company so the retakaful company assumes a portion of the takaful company’s risks. Why is retakaful important? In reality, a takaful company can’t bear the whole risk of covering its participants’ claims. If disaster strikes, the takaful fund may be depleted quickly and become insolvent, in which case everyone — the participants, the shareholders, and the takaful operator — loses.

By splitting the risk with a retakaful company, the takaful operator is much better able to manage the company through periods of high claims. Therefore, retakaful ensures the stability of takaful companies and the entire industry.

Seeing how retakaful works

Retakaful operates the same way that takaful does. The only difference is that participants (policyholders) of regular takaful products are individuals, businesses, and other commercial organizations. In a retakaful contract, participants (policyholders) are various takaful companies, and the fund operator is the retakaful company. Of course, retakaful companies need to operate according to sharia law and must make any investments or hedges accordingly.

The takaful operator and the retakaful operator sign the retakaful contract. The original policyholders of the takaful products aren’t directly involved in the retakaful contracts (even though the retakaful premiums are paid using a portion of the takaful policyholders’ fund).

If a takaful operator faces insolvency because of unexpected claims by its participants, the retakaful operator provides a qard hasan (interest-free loan) to cover the liability. The loan amount must be paid in subsequent years or is deducted from any retakaful surplus belonging to the takaful operator in the following year.

The contributions or premiums collected by the retakaful company from the takaful operators are invested based on the wakala, mudaraba, or wakala-mudaraba combined contract (see the earlier “Understanding Takaful Structures” section), and profits and fees are shared between the takaful and retakaful companies based on the specific contract agreement.

Spotting some of the players in the retakaful industry

Like the rest of the Islamic finance industry, the retakaful industry is relatively new when compared to conventional insurance; retakaful came into existence only in the late 1970s.

Examining Islamic opinions about conventional reinsurance

Two schools of thought exist among Islamic scholars regarding the permissibility of reinsuring in the conventional insurance industry:

![]() One opinion states that takaful companies can reinsure in the conventional insurance industry based on necessity and dire need when not enough retakaful operators are available to sufficiently fulfill the needs of takaful companies.

One opinion states that takaful companies can reinsure in the conventional insurance industry based on necessity and dire need when not enough retakaful operators are available to sufficiently fulfill the needs of takaful companies.

![]() The second opinion prohibits conventional reinsurance in all circumstances because the reinsurance is based on uncertainty, gambling, and interest. Scholars in this camp argue that because the Muslim community has survived for centuries without conventional reinsurance, no necessity or dire need can exist that justifies working with the conventional reinsurance industry.

The second opinion prohibits conventional reinsurance in all circumstances because the reinsurance is based on uncertainty, gambling, and interest. Scholars in this camp argue that because the Muslim community has survived for centuries without conventional reinsurance, no necessity or dire need can exist that justifies working with the conventional reinsurance industry.

Retakaful operators take two business forms: They exist either as independent companies or as windows (arms or divisions) of conventional reinsurance companies. Currently, more than two dozen dedicated retakaful operators are in operation, as well as six retakaful windows. The first independent retakaful operators to set up shop were these:

![]() 1979: Sudan National Reinsurance Company

1979: Sudan National Reinsurance Company

![]() 1983: Sheikhan Takaful Company in Sudan

1983: Sheikhan Takaful Company in Sudan

![]() 1985: Islamic Insurance and Reinsurance Company in Bahrain and Saudi Arabia

1985: Islamic Insurance and Reinsurance Company in Bahrain and Saudi Arabia

![]() 1985: BEST RE in Tunisia

1985: BEST RE in Tunisia

Other independent retakaful operators now do business from the Bahamas, Egypt, Iran, Kuwait, Malaysia, Saudi Arabia, Singapore, and United Arab Emirates.

The following conventional reinsurance companies provide retakaful window facilities:

![]() Mitsui Sumitomo (headquartered in Tokyo, Japan)

Mitsui Sumitomo (headquartered in Tokyo, Japan)

![]() Swiss Re (headquartered in London, England)

Swiss Re (headquartered in London, England)

![]() Kuwait Re (headquartered in Kuwait City)

Kuwait Re (headquartered in Kuwait City)

![]() Hannover Re (headquartered in Hannover, Germany)

Hannover Re (headquartered in Hannover, Germany)

![]() Trust Re (headquartered in Bahrain)

Trust Re (headquartered in Bahrain)

![]() Labuan Re (headquartered in Malaysia)

Labuan Re (headquartered in Malaysia)

Noting the Role of the Sharia Board in Takaful Companies

Like all other Islamic financial entities, takaful companies need a sharia board’s supervision to make sure they comply with Islamic principles. Each takaful company has its own sharia board, which offers governance and oversight in the following ways:

![]() Product development: The sharia board is responsible for making sure that the company develops any new takaful product according to sharia principles. Therefore, every general or family takaful product that a company wants to introduce to its market must first get a stamp of approval from the company’s sharia board.

Product development: The sharia board is responsible for making sure that the company develops any new takaful product according to sharia principles. Therefore, every general or family takaful product that a company wants to introduce to its market must first get a stamp of approval from the company’s sharia board.

![]() Operation supervision: Although the takaful operator takes care of the company’s daily business, the sharia board supervises the whole operation to make sure it’s being run according to sharia principles. For example

Operation supervision: Although the takaful operator takes care of the company’s daily business, the sharia board supervises the whole operation to make sure it’s being run according to sharia principles. For example

• When the company is being established, the sharia board must make sure that its structural development is sharia-compliant. The board may determine, for instance, that a company based solely on the mudaraba contract isn’t structurally compliant, so it steers the company toward a wakala or combination model instead. (You can read about these structures in “Understanding Takaful Structures” earlier in this chapter.)

• The sharia board verifies that the company’s transactions are sharia-compliant. As I describe in Chapter 18, a takaful company may invest some of its policyholders’ funds in order to generate profit both to support administrative costs and to benefit policyholders and investors. The sharia board ensures that all investments are made in sharia-compliant companies, funds, and sukuk (Islamic bonds) so that the takaful company doesn’t derive any profit from prohibited industries or from interest payments.

• As I explain in the earlier section “Getting Familiar with Retakaful (Reinsurance),” takaful companies pay premiums to retakaful companies (or, sometimes, to conventional reinsurance companies) to share the risk of a catastrophic event that leads to mass claims that may bankrupt the takaful fund. The sharia board decides whether to contract with a retakaful company or a conventional reinsurance company, depending on the board’s opinion regarding the conventional industry.

• The sharia board is responsible for ensuring that the board of directors receives reports about the company’s operations and sharia compliance on a regular basis and that such reports make it into the company’s annual report.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.